Languages

Pages

Legal

United States:2015 Financial Sector Assessment Program

Stress Testing (ST): Technical Wrap-up

March 5, 2015

This presentation is intended as background for discussions with the U.S. stress testing experts in the context of the U.S. FSAP. The calculations and results included herein have not yet undergone a full

internal review and should not be shared outside the technical team involved in the U.S. FSAP.

Outline• Banks

– Bank solvency ST (“IMF top-down”)– Bank liquidity risk analysis– Big 6 bank network ST

• Market-price based network analysis and ST (banks and nonbanks)

• Other items covered in the Technical Note– Insurance ST (separate wrap-up)– Mutual fund liquidity risk analysis– Discussion of DFAST results (Fed, company-run)

2

Coverage etc.

3

[REDACTED]

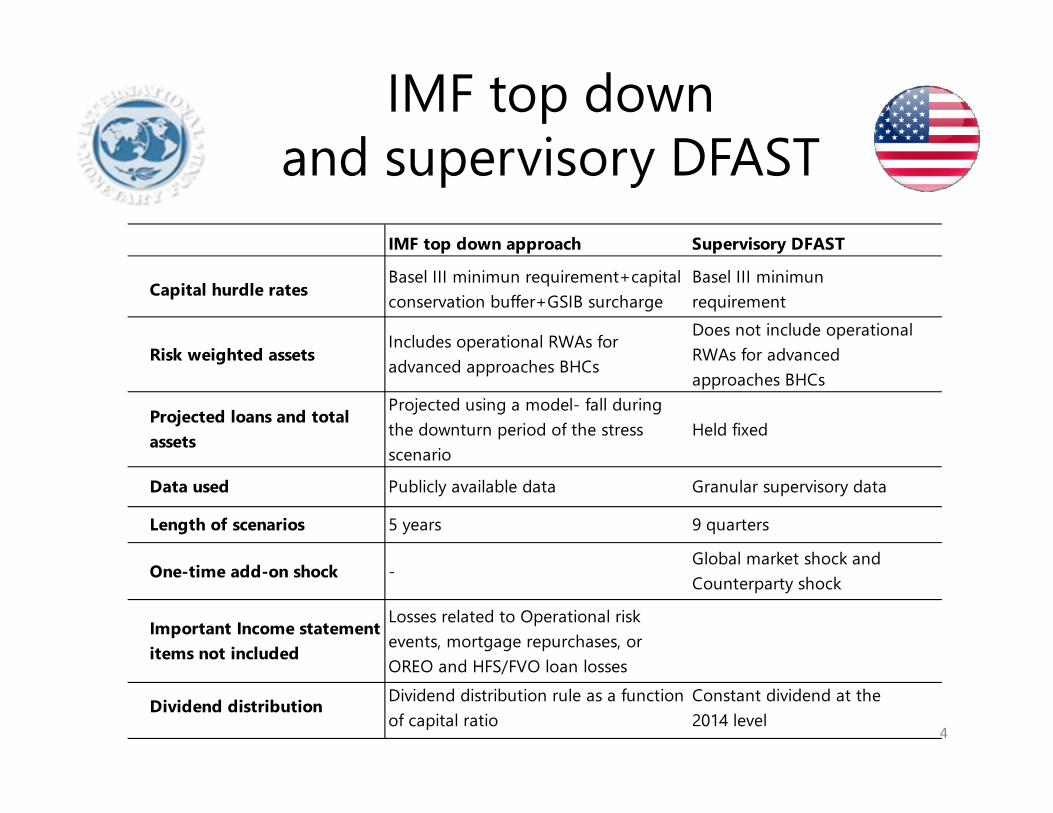

IMF top down and supervisory DFAST

IMF top down approach Supervisory DFAST

Capital hurdle ratesBasel III minimun requirement+capital conservation buffer+GSIB surcharge

Basel III minimun requirement

Risk weighted assetsIncludes operational RWAs for advanced approaches BHCs

Does not include operational RWAs for advanced approaches BHCs

Projected loans and total assets

Projected using a model- fall during the downturn period of the stress scenario

Held fixed

Data used Publicly available data Granular supervisory data

Length of scenarios 5 years 9 quarters

One-time add-on shock -Global market shock and Counterparty shock

Important Income statement items not included

Losses related to Operational risk events, mortgage repurchases, or OREO and HFS/FVO loan losses

Dividend distribution Dividend distribution rule as a function of capital ratio

Constant dividend at the 2014 level

4

IMF solvency stress test

5

[REDACTED]

IMF liquidity risk analysis

6

[REDACTED]

IMF liquidity ST-liquidity metric-

7

[REDACTED]

IMF liquidity ST-liquid assets and outflows-

8

[REDACTED]

“Big 6” network ST

9

[REDACTED]

Big 6 network ST

10

[REDACTED]

Big 6 network ST

11

[REDACTED]

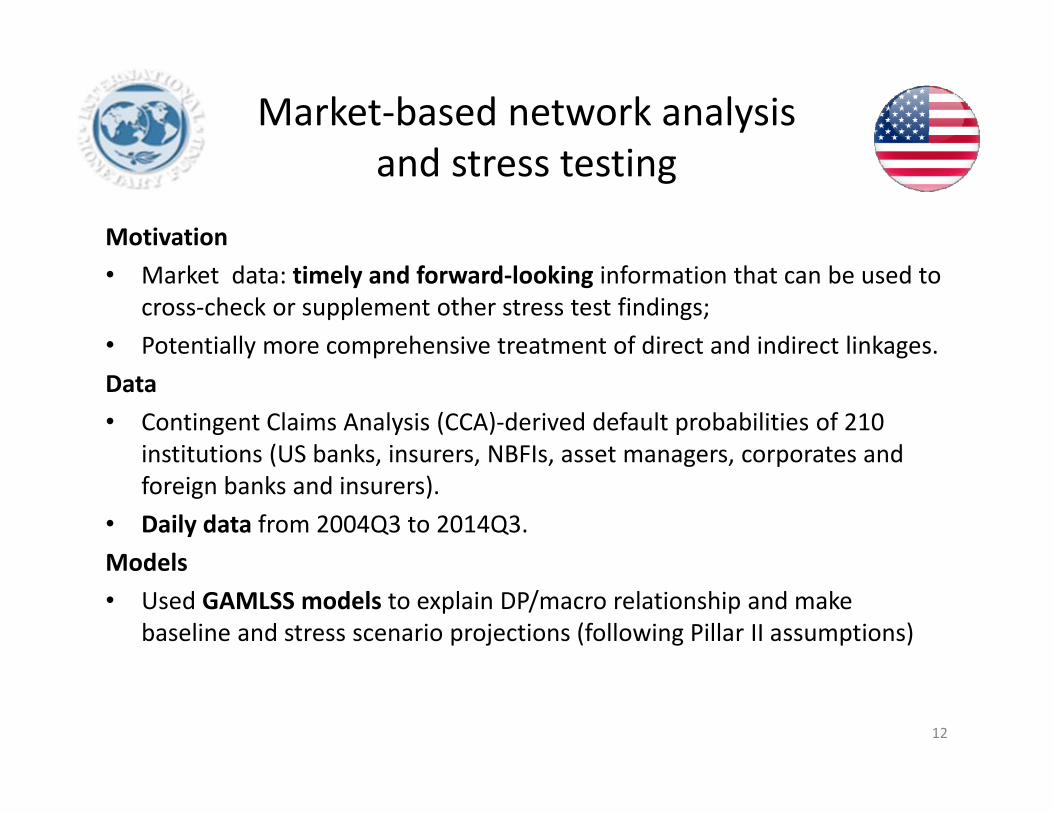

Motivation• Market data: timely and forward‐looking information that can be used to

cross‐check or supplement other stress test findings;• Potentially more comprehensive treatment of direct and indirect linkages.Data • Contingent Claims Analysis (CCA)‐derived default probabilities of 210

institutions (US banks, insurers, NBFIs, asset managers, corporates and foreign banks and insurers).

• Daily data from 2004Q3 to 2014Q3.Models• Used GAMLSS models to explain DP/macro relationship and make

baseline and stress scenario projections (following Pillar II assumptions)

Market‐based network analysis and stress testing

12

Projections

13

[REDACTED]

Projections

14

[REDACTED]

Spillovers

15

[REDACTED]

*Connectivity measure for the U.S. financial system is based on 176 US institutions default probabilities(banks, insurers, asset managers, NBFIs, and corporates)

Connectivity

16

[REDACTED]

Summary of findings

17

[REDACTED]

Recommendations

18

[REDACTED]

Top Related