Languages

Pages

Legal

Partnership. Performance. avisonyoung.com

Market Overview

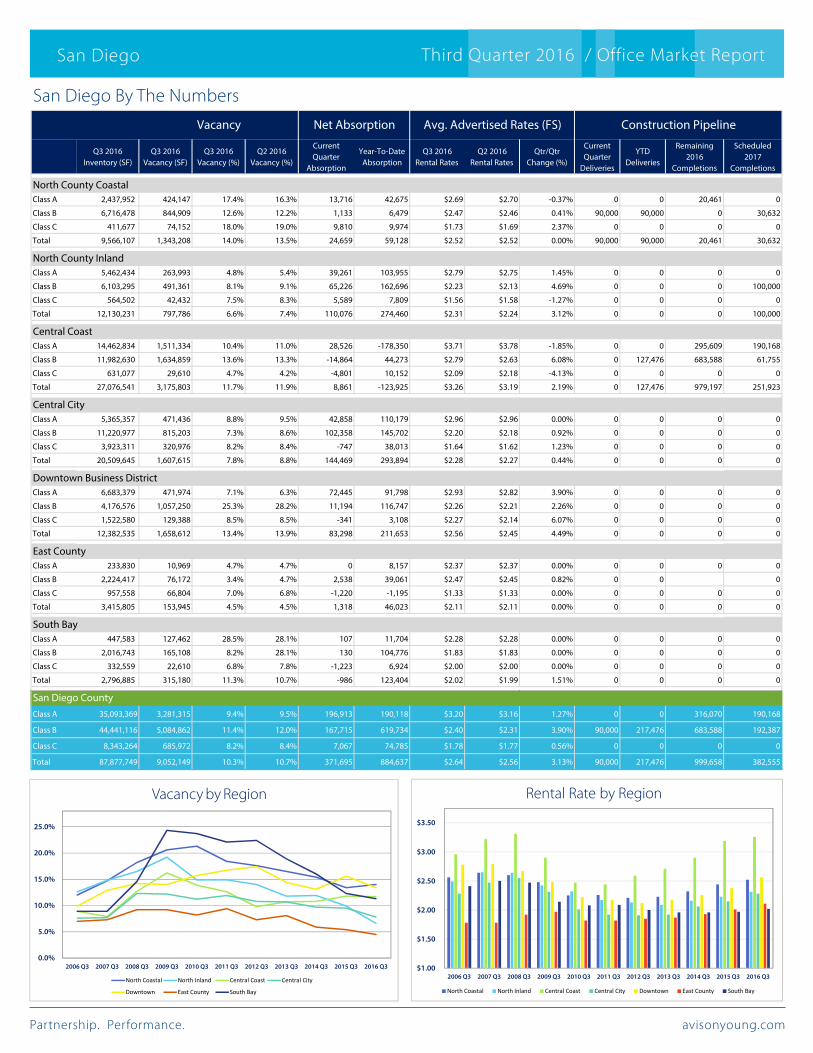

The San Diego office market continued to make steady gains as of the third quarter of 2016. Vacancy is gradually getting tighter, while rent increases have not slowed down. The market is supported by diverse industries and desirable geography while benefitting from strong demand for space by healthcare innovators, independent research institutes and sectors that work closely with the local military. The San Diego County unemployment rate, as of the third quarter of 2016 dropped to 5.0% from 5.1% one year earlier.Vacancy was 10.3% at the end of the third quarter of 2016, down from 11.5% at the same point in 2015.

While vacancy is tighter year-over-year post-recession, vacancy in the third quarter is also down from the previous quarter. Rental increases are not expected to slow, even as new construction is introduced. Office space is spending less time on the market, and fewer months vacant. The rental rate average for all classes reached $2.64 psf FSG at Q3 2016, up from Q3 2015, when rents were at $2.53 psf FSG. The highest rents were in the Central Coast submarket at $3.26 psf FSG with the next highest in the Downtown submarket at $2.55 psf FSG, followed by the North County Coastal area at $2.52 psf FSG. In the past 12-month period, San Diego County recorded a net absorption of positive 1,186,023 sf.

Third Quarter 2016 / Office Market Report

San Diego

Market Facts

5.0%San Diego County

Unemployment RateAs Of August 2016

371,695 SFPositive Net Absorption

Current Quarter

Positive 884,637 SFYear-To-Date

10.3%Total Vacancy Rate

Up From 10.7% In Q2 2016

$2.64 PSFAsking Rental RateWeighted Average

San Diego Office Vacancy Tightens,

As Rents Surge Ahead

Partnership. Performance. avisonyoung.com

Third Quarter 2016 / Office Market Report San Diego

SalesSales volume for the past twelve months has reached $2.6 billion, down moderately from the previous twelve months which reached $3.1 billion. This total includes local portions of larger portfolio sales. Class A inventory has increased in trading volume during the past twelve months, while Class B experienced a retraction after being heavily favored in 2015. The average sale price per square foot is up over the past twelve months, to $240 psf, from the previous twelve months of $212 psf.

Investment Sale401 Mile of Cars Way National City

The largest investment sale during the third quarter was Sorrento Gateway, a two-building life science campus in Sorrento Mesa, purchased by Kilroy Realty Corporation for $355 psf. In total, the buildings were approximately 56% occupied by a single tenant at the time of sale. The next largest deal was South Bay Corporate Center, at 401 Mile of Cars Way in National City, purchased by Bosa Development Corporation, for $225 psf. The building was 77% leased to multiple tenants. Another significant sale consisted of three properties at multiple locations; Bernardo Regency Centre and Foremost Professional Plaza, both in Rancho Bernardo, and Three Governor Park, in Governor Park. The multi-tenant portfolio was 90% leased, and sold to Omninet Capital for $209 psf.

ConstructionThe San Diego office market had ten investment-grade office projects under construction at the third quarter of 2016, including life science projects.

These projects amount to more than 1,382,213 sf of new inventory that will be delivered throughout 2016 and 2017, approximately 83% of which is already pre-committed, with the remainder currently on the market. All new office construction is currently located in the Central Coast and North County areas. The three largest projects reflect the growing needs of the life science sector in the Central Coast area of San Diego.

Transaction Volume

by Property Sector

San Diego County

In total there is nearly one million square feet of space under construction with designated lab buildout to accommodate life science companies. The Rancho Santa Fe market saw the completion of Palma De La Reina, a 20,461 square foot multi-tenant office building, constructed without tenant pre-commitments. There is currently nearly 15 million square feet of proposed office development on record in the county, which is an increase of more than 60% from the same time in the previous year.

Construction3420 Carmel Mountain RoadDel Mar Heights

Partnership. Performance. avisonyoung.com

Top Leases

Top Sales

Under Construction

Asking Rent Vacancy Rates Net Absorption

San Diego Third Quarter 2016 / Office Market Report

Buyer Price SFAddress

4939-4955 Directors Place, Sorrento Mesa - Life Science HCP, Inc.

Seller

Kilroy Realty Corporation $49,000,000 138,090

401 Mile Of Cars Way, National City Bosa Development Corporation Walton Street Capital, LLC $42,750,000 189,588

Rancho Bernardo/Governor Park, Portfolio Omninet Capital The Blackstone Group LP $30,500,000 146,234

10421-10431 Wateridge Circle, Sorrento Mesa Angelo, Gordon & Co. SteelWave, Inc. $28,000,000 123,675

2530 Campbell Place, Carlsbad Testa Family, LP II Oddo Family Trust $13,000,000 41,000

Developer SF CompletionAddress

4775-4785 Executive Dr, UTC - Lab Space Biomed Realty 316,262 Q3 2016

10290 Campus Point Dr, UTC - Lab Space Alexandria Real Estate Equities, Inc. 304,326 Q4 2016

5200 Illumina Way, UTC - Lab Space Alexandria Real Estate Equities, Inc. 295,609 Q4 2016

16909 W Bernardo Dr, Rancho Bernardo Sharp Rees-Stealy 100,000 Q3 2017

9779 Towne Centre Dr, UTC The Irvine Company 96,435 Q1 2017

Type Address Submarket SFTenant

WeWork New 600 B Street Downtown 88,273

Sorrento Therapeutics - Lab Space New 4955 Directors Place Sorrento Mesa 76,687

AutoGenomics - Lab Space New 1600 Faraday Avenue Carlsbad 59,860

Department of Child Support Services New 3666 Kearny Villa Road Kearny Mesa 58,222

Novatel Wireless, Inc. Sublease 9605 Scranton Road Sorrento Mesa 41,383

‐300,000

0

300,000

600,000

900,000

1,200,000

2011 Q3 2012 Q3 2013 Q3 2014 Q3 2015 Q3 2016 Q3

$1.80

$2.00

$2.20

$2.40

$2.60

$2.80

2011 Q3 2012 Q3 2013 Q3 2014 Q3 2015 Q3 2016 Q3

8.0%

10.0%

12.0%

14.0%

16.0%

2011 Q3 2012 Q3 2013 Q3 2014 Q3 2015 Q3 2016 Q3

Partnership. Performance. avisonyoung.com

San Diego By The Numbers

San Diego Third Quarter 2016 / Office Market Report

Q3 2016 Inventory (SF)

Q3 2016 Vacancy (SF)

Q3 2016 Vacancy (%)

Q2 2016 Vacancy (%)

Current Quarter

Absorption

Year-To-Date Absorption

Q3 2016 Rental Rates

Q2 2016 Rental Rates

Qtr/Qtr Change (%)

Current Quarter

Deliveries

YTD Deliveries

Remaining 2016

Completions

Scheduled 2017

Completions

North County CoastalClass A 2,437,952 424,147 17.4% 16.3% 13,716 42,675 $2.69 $2.70 -0.37% 0 0 20,461 0

6,716,478 844,909 12.6% 12.2% 1,133 6,479 $2.47 $2.46 0.41% 90,000 90,000 0 30,632

411,677 74,152 18.0% 19.0% 9,810 9,974 $1.73 $1.69 2.37% 0 0 0 0

Class B

Class C

Total 9,566,107 1,343,208 14.0% 13.5% 24,659 59,128 $2.52 $2.52 0.00% 90,000 90,000 20,461 30,632

North County InlandClass A 5,462,434 263,993 4.8% 5.4% 39,261 103,955 $2.79 $2.75 1.45% 0 0 0 0

6,103,295 491,361 8.1% 9.1% 65,226 162,696 $2.23 $2.13 4.69% 0 0 0 100,000

564,502 42,432 7.5% 8.3% 5,589 7,809 $1.56 $1.58 -1.27% 0 0 0 0

Class B

Class C

Total 12,130,231 797,786 6.6% 7.4% 110,076 274,460 $2.31 $2.24 3.12% 0 0 0 100,000

Central CoastClass A 14,462,834 1,511,334 10.4% 11.0% 28,526 -178,350 $3.71 $3.78 -1.85% 0 0 295,609 190,168

Class B 11,982,630 1,634,859 13.6% 13.3% -14,864 44,273 $2.79 $2.63 6.08% 0 127,476 683,588 61,755

Class C 631,077 29,610 4.7% 4.2% -4,801 10,152 $2.09 $2.18 -4.13% 0 0 0 0

Total 27,076,541 3,175,803 11.7% 11.9% 8,861 -123,925 $3.26 $3.19 2.19% 0 127,476 979,197 251,923

Central CityClass A 5,365,357 471,436 8.8% 9.5% 42,858 110,179 $2.96 $2.96 0.00% 0 0 0 0

Class B 11,220,977 815,203 7.3% 8.6% 102,358 145,702 $2.20 $2.18 0.92% 0 0 0 0

Class C 3,923,311 320,976 8.2% 8.4% -747 38,013 $1.64 $1.62 1.23% 0 0 0 0

Total 20,509,645 1,607,615 7.8% 8.8% 144,469 293,894 $2.28 $2.27 0.44% 0 0 0 0

Downtown Business DistrictClass A 6,683,379 471,974 7.1% 6.3% 72,445 91,798 $2.93 $2.82 3.90% 0 0 0 0

4,176,576 1,057,250 25.3% 28.2% 11,194 116,747 $2.26 $2.21 2.26% 0 0 0 0

1,522,580 129,388 8.5% 8.5% -341 3,108 $2.27 $2.14 6.07% 0 0 0 0

Class B

Class C

Total 12,382,535 1,658,612 13.4% 13.9% 83,298 211,653 $2.56 $2.45 4.49% 0 0 0 0

East CountyClass A 233,830 10,969 4.7% 4.7% 0 8,157 $2.37 $2.37 0.00% 0 0 0 0

Class B 2,224,417 76,172 3.4% 4.7% 2,538 39,061 $2.47 $2.45 0.82% 0 0 0

Class C 957,558 66,804 7.0% 6.8% -1,220 -1,195 $1.33 $1.33 0.00% 0 0 0 0

Total 3,415,805 153,945 4.5% 4.5% 1,318 46,023 $2.11 $2.11 0.00% 0 0 0 0

South BayClass A 447,583 127,462 28.5% 28.1% 107 11,704 $2.28 $2.28 0.00% 0 0 0 0

Class B 2,016,743 165,108 8.2% 28.1% 130 104,776 $1.83 $1.83 0.00% 0 0 0 0

Class C 332,559 22,610 6.8% 7.8% -1,223 6,924 $2.00 $2.00 0.00% 0 0 0 0

Total 2,796,885 315,180 11.3% 10.7% -986 123,404 $2.02 $1.99 1.51% 0 0 0 0

San Diego County Class A 35,093,369 3,281,315 9.4% 9.5% 196,913 190,118 $3.20 $3.16 1.27% 0 0 316,070 190,168

Class B 44,441,116 5,084,862 11.4% 12.0% 167,715 619,734 $2.40 $2.31 3.90% 90,000 217,476 683,588 192,387

Class C 8,343,264 685,972 8.2% 8.4% 7,067 74,785 $1.78 $1.77 0.56% 0 0 0 0

Total 87,877,749 9,052,149 10.3% 10.7% 371,695 884,637 $2.64 $2.56 3.13% 90,000 217,476 999,658 382,555

Vacancy Net Absorption Avg. Advertised Rates (FS) Construction Pipeline

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2006 Q3 2007 Q3 2008 Q3 2009 Q3 2010 Q3 2011 Q3 2012 Q3 2013 Q3 2014 Q3 2015 Q3 2016 Q3

Vacancy by Region

North Inland Central CoastNorth Coastal Central City

Downtown East County South Bay

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

Rental Rate by Region

2006 Q3 2007 Q3 2008 Q3 2009 Q3 2010 Q3 2011 Q3 2012 Q3 2013 Q3 2014 Q3 2015 Q3 2016 Q3

North Coastal North Inland Central Coast Central City Downtown East County South Bay

Partnership. Performance. avisonyoung.com

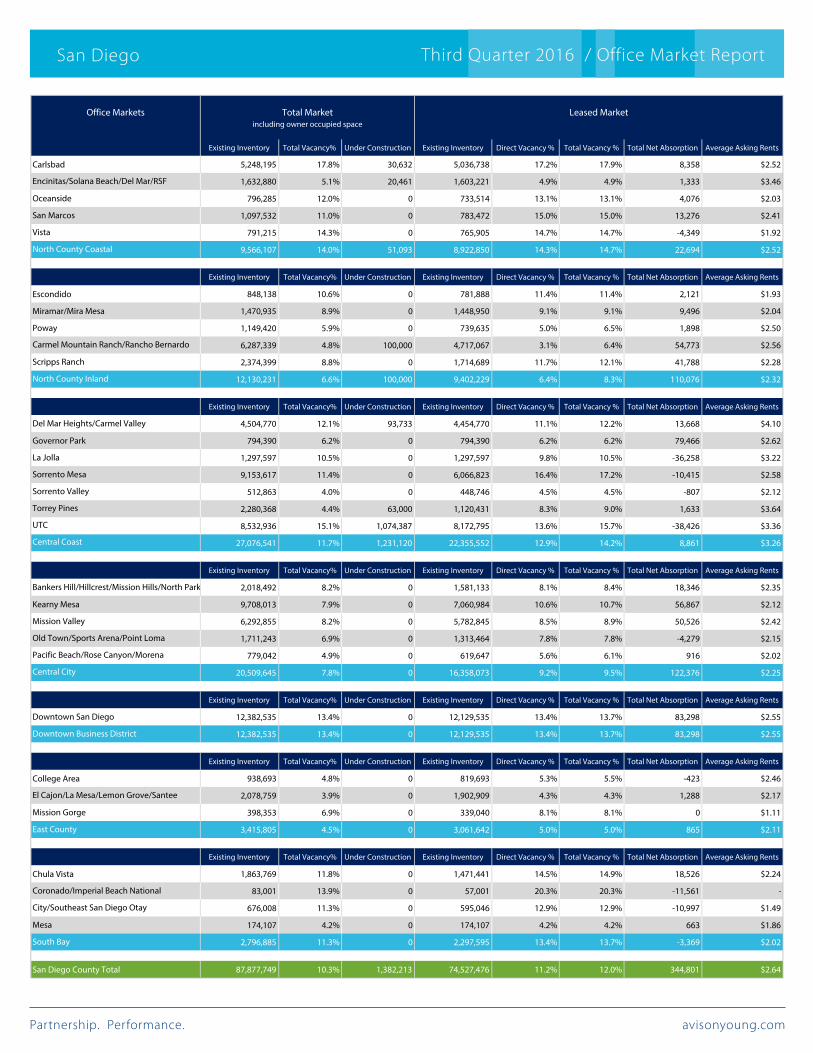

San Diego Third Quarter 2016 / Office Market Report

Office Markets

Existing Inventory Total Vacancy% Under Construction Existing Inventory Direct Vacancy % Total Vacancy % Total Net Absorption Average Asking Rents

5,248,195 17.8% 30,632 5,036,738 17.2% 17.9% 8,358 $2.52

1,632,880 5.1% 20,461 1,603,221 4.9% 4.9% 1,333 $3.46

796,285 12.0% 0 733,514 13.1% 13.1% 4,076 $2.03

1,097,532 11.0% 0 783,472 15.0% 15.0% 13,276 $2.41

791,215 14.3% 0 765,905 14.7% 14.7% -4,349 $1.92

Carlsbad

Encinitas/Solana Beach/Del Mar/RSF

Oceanside

San Marcos

Vista

North County Coastal 9,566,107 14.0% 51,093 8,922,850 14.3% 14.7% 22,694 $2.52

Existing Inventory Total Vacancy% Under Construction Existing Inventory Direct Vacancy % Total Vacancy % Total Net Absorption Average Asking Rents

848,138 10.6% 0 781,888 11.4% 11.4% 2,121 $1.93

1,470,935 8.9% 0 1,448,950 9.1% 9.1% 9,496 $2.04

1,149,420 5.9% 0 739,635 5.0% 6.5% 1,898 $2.50

6,287,339 4.8% 100,000 4,717,067 3.1% 6.4% 54,773 $2.56

2,374,399 8.8% 0 1,714,689 11.7% 12.1% 41,788 $2.28

Escondido

Miramar/Mira Mesa

Poway

Carmel Mountain Ranch/Rancho Bernardo

Scripps Ranch

North County Inland 12,130,231 6.6% 100,000 9,402,229 6.4% 8.3% 110,076 $2.32

Existing Inventory Total Vacancy% Under Construction Existing Inventory Direct Vacancy % Total Vacancy % Total Net Absorption Average Asking Rents

4,504,770 12.1% 93,733 4,454,770 11.1% 12.2% 13,668 $4.10

794,390 6.2% 0 794,390 6.2% 6.2% 79,466 $2.62

1,297,597 10.5% 0 1,297,597 9.8% 10.5% -36,258 $3.22

9,153,617 11.4% 0 6,066,823 16.4% 17.2% -10,415 $2.58

512,863 4.0% 0 448,746 4.5% 4.5% -807 $2.12

2,280,368 4.4% 63,000 1,120,431 8.3% 9.0% 1,633 $3.64

8,532,936 15.1% 1,074,387 8,172,795 13.6% 15.7% -38,426 $3.36

Del Mar Heights/Carmel Valley

Governor Park

La Jolla

Sorrento Mesa

Sorrento Valley

Torrey Pines

UTC

Central Coast 27,076,541 11.7% 1,231,120 22,355,552 12.9% 14.2% 8,861 $3.26

Existing Inventory Total Vacancy% Under Construction Existing Inventory Direct Vacancy % Total Vacancy % Total Net Absorption Average Asking Rents

2,018,492 8.2% 0 1,581,133 8.1% 8.4% 18,346 $2.35

9,708,013 7.9% 0 7,060,984 10.6% 10.7% 56,867 $2.12

6,292,855 8.2% 0 5,782,845 8.5% 8.9% 50,526 $2.42

1,711,243 6.9% 0 1,313,464 7.8% 7.8% -4,279 $2.15

779,042 4.9% 0 619,647 5.6% 6.1% 916 $2.02

Bankers Hill/Hillcrest/Mission Hills/North Park

Kearny Mesa

Mission Valley

Old Town/Sports Arena/Point Loma

Pacific Beach/Rose Canyon/Morena

Central City 20,509,645 7.8% 0 16,358,073 9.2% 9.5% 122,376 $2.25

Existing Inventory Total Vacancy% Under Construction Existing Inventory Direct Vacancy % Total Vacancy % Total Net Absorption Average Asking Rents

12,382,535 13.4% 0 12,129,535 13.4% 13.7% 83,298 $2.55Downtown San Diego

Downtown Business District 12,382,535 13.4% 0 12,129,535 13.4% 13.7% 83,298 $2.55

Existing Inventory Total Vacancy% Under Construction Existing Inventory Direct Vacancy % Total Vacancy % Total Net Absorption Average Asking Rents

938,693 4.8% 0 819,693 5.3% 5.5% -423 $2.46

2,078,759 3.9% 0 1,902,909 4.3% 4.3% 1,288 $2.17

398,353 6.9% 0 339,040 8.1% 8.1% 0 $1.11

College Area

El Cajon/La Mesa/Lemon Grove/Santee

Mission Gorge

East County 3,415,805 4.5% 0 3,061,642 5.0% 5.0% 865 $2.11

Existing Inventory Total Vacancy% Under Construction Existing Inventory Direct Vacancy % Total Vacancy % Total Net Absorption Average Asking Rents

1,863,769 11.8% 0 1,471,441 14.5% 14.9% 18,526 $2.24

83,001 13.9% 0 57,001 20.3% 20.3% -11,561 -

676,008 11.3% 0 595,046 12.9% 12.9% -10,997 $1.49

174,107 4.2% 0 174,107 4.2% 4.2% 663 $1.86

Chula Vista

Coronado/Imperial Beach National

City/Southeast San Diego Otay

Mesa

South Bay 2,796,885 11.3% 0 2,297,595 13.4% 13.7% -3,369 $2.02

San Diego County Total 87,877,749 10.3% 1,382,213 74,527,476 11.2% 12.0% 344,801 $2.64

Total Marketincluding owner occupied space

Leased Market

avisonyoung.com

© 2016 Avison Young - Southern California, Ltd. All rights reserved. E. & O.E.: The information contained herein was obtained from sources which we deem reliable and, while thought to be correct, is not guaranteed by Avison Young.

213.935.7435

Regional Managing Director: Chris Cooper - Corporate 555 S Flower St, Ste 3200 Los Angeles, CA [email protected]

Contact Information - Southern California, United States

213.935.7430 323.851.6666 310.899.1800

Los Angeles - Downtown 555 S Flower St, Ste 3200Los Angeles, CA 90071 Primary Contact: Ted [email protected]

Los Angeles - North6711 Forest Lawn DrLos Angeles, CA 90068 Primary Contact: Mark Evanoff [email protected]

Los Angeles - West10940 Wilshire Blvd, Ste 2100 Los Angeles, CA 90024 Primary Contact: Jonathan Larsen [email protected]

Los Angeles - Santa Monica 301 Arizona Ave, Ste 303 Santa Monica, CA 90401 Primary Contact: Randy [email protected]

San Diego - La Jolla4225 Executive Sq, Ste 600 La Jolla, CA 92037Primary Contact: Jerry Keeney [email protected]

858.201.7077

Orange County - Irvine 2030 Main Street, Ste 150 Irvine, CA 92614Primary Contact: Stan Yoshihara [email protected] 858.201.7072

Report Prepared By:Amber Jagers - Research Manager 4225 Executive Sq, Ste 600La Jolla, CA [email protected]

213.471.1069

A Growing, Multinational Presence

Avison Young is the world’s fastest-growing commercial real estate services firm. Headquartered in Toronto, Canada, Avison Young is a collaborative, global firm owned and operated by its principals. Founded in 1978, the company comprises 2,400 real estate professionals in 79 offices, providing value-added, client-centric investment sales, leasing, advisory, management, financing and mortgage placement services to owners and occupiers of office, retail, industrial and multi-family properties.

Avison Young at a Glance

GREENVILLE

ATLANTA

EDMONTON

CALGARY

MINNEAPOLISCHICAGO (2)

DETROIT

COLUMBUS

CHARLOTTE

BOSTONHALIFAXMONCTONOTTAWA

MONTREAL

QUEBEC CITYCLEVELAND

PITTSBURGH

LAS VEGAS

RENO

INDIANAPOLIS

SACRAMENTO

LOS ANGELES (4)ORANGE COUNTYSAN DIEGO

TORONTO (2)TORONTO NORTHTORONTO WESTWATERLOO REGION

RALEIGH-DURHAM (2)

PHILADELPHIANEW JERSEY

SUBURBAN MARYLANDWASHINGTON, DCTYSONS CORNER

FAIRFIELD/WESTCHESTER LONG ISLANDNEW YORK CITY

SAN FRANCISCOOAKLANDSAN MATEO

DENVER

WINNIPEG

REGINA

CHARLESTON

HAMBURG

LONDON (2)

THAMES VALLEY

FRANKFURT

MUNICH

DUESSELDORF

BERLIN

NASHVILLE

KNOXVILLE

ST. LOUIS

MEMPHIS

HARTFORD

MEXICO CITY

COVENTRY

TAMPA

ORLANDO

DALLASHOUSTON

AUSTIN

SAN ANTONIO

PHOENIX

VANCOUVER

LETHBRIDGE

WEST PALM BEACH BOCA RATON

JACKSONVILLE

FORT LAUDERDALEMIAMI

Founded: 1978 Total Real Estate Professionals: 2,400

Offices: 79Brokerage Professionals: 900+

Property Under Management: 100 million sf

Top Related