Languages

Pages

Legal

������������ ��

Sydney Technology and Innovation for Banking and Financial Services Conference

23 October 2007Chris Hamilton, CEO, APCA

������� �� � �� ��� ������ �������Australian chip payment cards:

where are we up to?

The overseas chip card experience:

what can we learn?

The industry agenda:

what do we need to do?

� �� ��� ��������• Chip is a paradigm shift: new costs, risks

and opportunities

• Chip is the basis for all future evolution

• The card rules the terminal

• Massive convergence opportunity and risk: transport, micropayments, loyalty.

• Lots of blue sky, but the usual short term implementation pressures

�������������� ����������� ��� �� ��

ATMs 24,000

EFTPOS terminals 540,000

Debit payment cards 21,000,000

Credit and multifunction cards 22,000,000

� �� ��� � ��� � ��� ��� ����

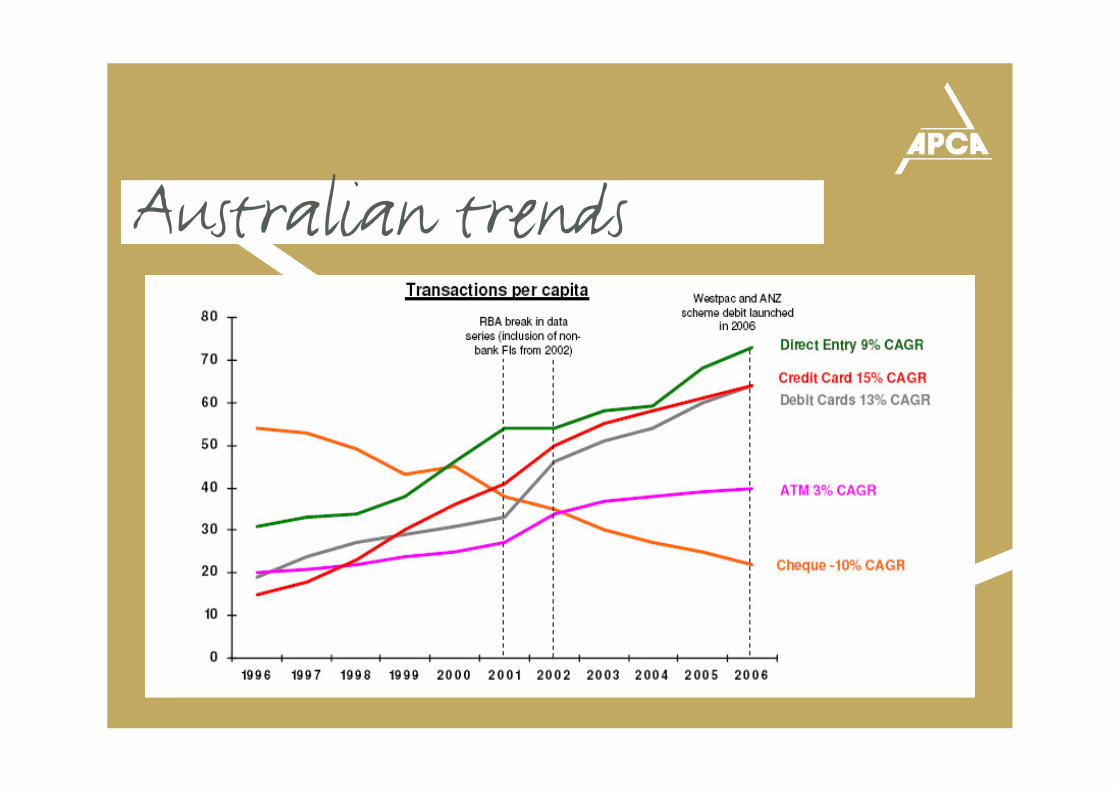

• Successful, reliable, robust & secure.

• Card fraud low by world comparison –(credit 36.9 cents per $1,000, debit 7.7 cents)

• Fraud heading our way?

������ ����� ���� ��!• Many countries “fully chip” (local card, local

terminal)

• Many others migrating

• Chip & magnetic stripe (overseas use)

• Driver = fraud (chip addresses counterfeit), telecom costs (chip allows offline verification)

• Use of magnetic stripe being blocked domestically for domestic cards

• Counterfeit fraud migrating to non-chip areas

� �� ��� � ������• Chip payment credit cards being issued

• EFTPOS terminals being upgraded to accept Chip

• ATM’s - no action yet

• Driver = Card Scheme incentives & liability shift

• Rolling implementation, not big-bang

• Impact on consumers & merchants

• Overseas Chip cards being presented

• Travelling Australians starting to have problems

" # ��� ��������Originally chip & signature, then chip and PIN;

122m cards, 850,000 POS terminals, 40,000 ATMs

Things that worked: industry-wide, central coordination; central testing facilities; large marketing and comms effort (retail staff aspect vital); central data and issues logs

Things that didn’t work: very expensive; started with low-level technology then upgraded; stopped central testing too early, underestimated media adverse “spin”

�� �� ! �� ��$ ���� ��A closer comparison with Australia in terms of size and

complexity, BUT: proximity to US (fraud leakage), and strong domestic card network: Interac

Avoided “big” central infrastructure, But: focus on town trials and retailer engagement, with clear long-term deadlines: ATM mandatory end 2012, POS mandatory end 2015.

So far, so good.

Need for industry collaboration?

• Overseas experience:– Interoperability issues– Industry approach

• APCA Forum:– Agreement that industry collaboration is a

necessary part of successful chip rollout in Australia

• Engage with all stakeholders (card schemes, merchants, FI’s)

• Identify areas requiring collaboration

%����� �����! �&' ��(�������)

Potentialcrisistrigger

• Obviousdisruption

• Memberreport

Initialassessment(Declare a crisis or not)

• Analyseinformation

• Request moreinformation

Invoke crisiscommunicationplan – managethe crisis

• Majordisruptionor event

Declare thecrisis as over

• Agree the crisis is over

Possible areas for collaboration

* � ! &� � �

Agree industry minimum standards and debit specification

• Account selection• Online/offline PIN

authorisation• EMV specification

interpretation• SDA/DDA• Risk parameters• PIN bypass• Plain text vs encrypted PIN

Industry timeframes

Education

Industry testing capability

• Customer• Merchant

Problem resolution / information sharing

Communications

Publicrelations

• Consumers

• All stakeholders

� �� ������ �

We need to implement EMV for tomorrow, not just today:

• Loyalty, healthcare, ticketing, mass transit etc. etc.

• Contactless, mobile phones and PDAs.

• Secure payment services via personal computers, interactive TV, etc.

• Build for future volumes!

$ �� �� ��� �� ���! �

+ �(� ������� ����The historical segregation of cards and payments is

breaking down

• Real-time payment assurance

• Mass-market reach

• Increasing importance of online business

=

Changing consumer demand: Will we be ready?

������������ ��

Sydney Technology and Innovation for Banking and Financial Services Conference

23 October 2007Chris Hamilton, CEO, APCA

Top Related