Sydney Technology and Innovation for Banking and...

14

Sydney Technology and Innovation for Banking and Financial Services Conference 23 October 2007 Chris Hamilton, CEO, APCA

Transcript of Sydney Technology and Innovation for Banking and...

������������ ��

Sydney Technology and Innovation for Banking and Financial Services Conference

23 October 2007Chris Hamilton, CEO, APCA

������� �� � �� ��� ������ �������Australian chip payment cards:

where are we up to?

The overseas chip card experience:

what can we learn?

The industry agenda:

what do we need to do?

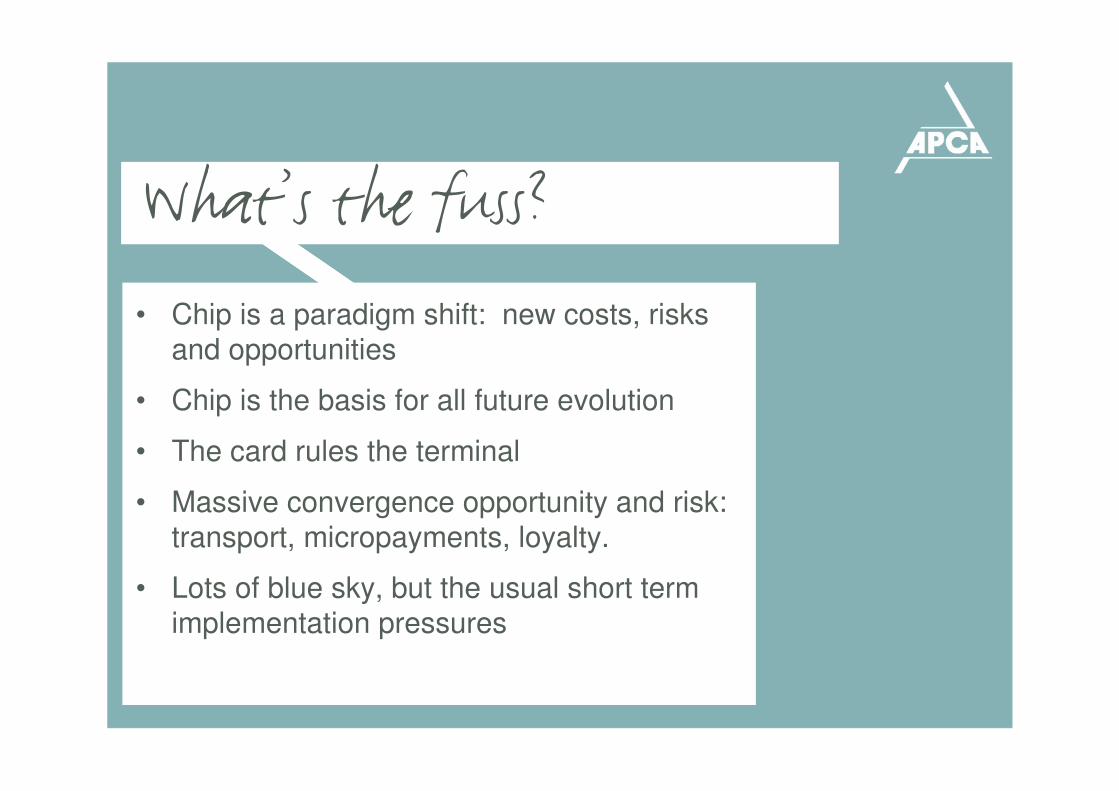

� �� ��� ��������• Chip is a paradigm shift: new costs, risks

and opportunities

• Chip is the basis for all future evolution

• The card rules the terminal

• Massive convergence opportunity and risk: transport, micropayments, loyalty.

• Lots of blue sky, but the usual short term implementation pressures

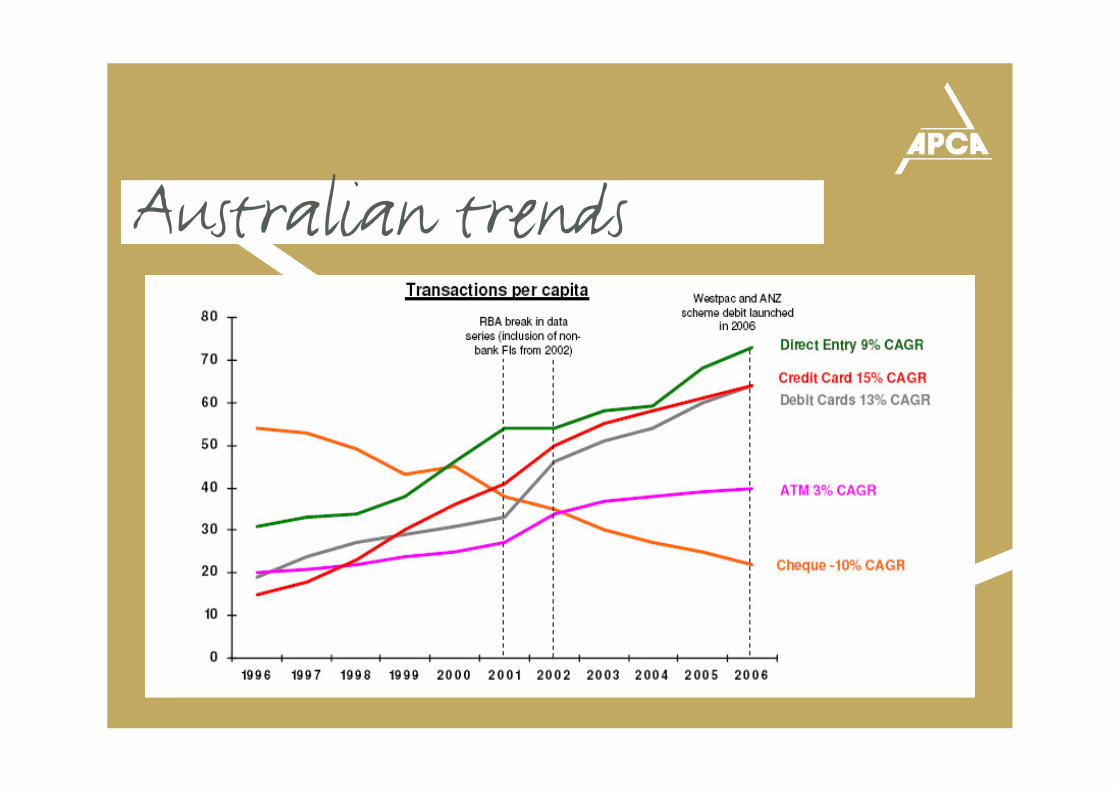

�������������� ����������� ��� �� ��

ATMs 24,000

EFTPOS terminals 540,000

Debit payment cards 21,000,000

Credit and multifunction cards 22,000,000

� �� ��� � ��� � ��� ��� ����

• Successful, reliable, robust & secure.

• Card fraud low by world comparison –(credit 36.9 cents per $1,000, debit 7.7 cents)

• Fraud heading our way?

������ ����� ���� ��!• Many countries “fully chip” (local card, local

terminal)

• Many others migrating

• Chip & magnetic stripe (overseas use)

• Driver = fraud (chip addresses counterfeit), telecom costs (chip allows offline verification)

• Use of magnetic stripe being blocked domestically for domestic cards

• Counterfeit fraud migrating to non-chip areas

� �� ��� � ������• Chip payment credit cards being issued

• EFTPOS terminals being upgraded to accept Chip

• ATM’s - no action yet

• Driver = Card Scheme incentives & liability shift

• Rolling implementation, not big-bang

• Impact on consumers & merchants

• Overseas Chip cards being presented

• Travelling Australians starting to have problems

" # ��� ��������Originally chip & signature, then chip and PIN;

122m cards, 850,000 POS terminals, 40,000 ATMs

Things that worked: industry-wide, central coordination; central testing facilities; large marketing and comms effort (retail staff aspect vital); central data and issues logs

Things that didn’t work: very expensive; started with low-level technology then upgraded; stopped central testing too early, underestimated media adverse “spin”

�� �� ! �� ��$ ���� ��A closer comparison with Australia in terms of size and

complexity, BUT: proximity to US (fraud leakage), and strong domestic card network: Interac

Avoided “big” central infrastructure, But: focus on town trials and retailer engagement, with clear long-term deadlines: ATM mandatory end 2012, POS mandatory end 2015.

So far, so good.

Need for industry collaboration?

• Overseas experience:– Interoperability issues– Industry approach

• APCA Forum:– Agreement that industry collaboration is a

necessary part of successful chip rollout in Australia

• Engage with all stakeholders (card schemes, merchants, FI’s)

• Identify areas requiring collaboration

%����� �����! �&' ��(�������)

Potentialcrisistrigger

• Obviousdisruption

• Memberreport

Initialassessment(Declare a crisis or not)

• Analyseinformation

• Request moreinformation

Invoke crisiscommunicationplan – managethe crisis

• Majordisruptionor event

Declare thecrisis as over

• Agree the crisis is over

Possible areas for collaboration

* � ! &� � �

Agree industry minimum standards and debit specification

• Account selection• Online/offline PIN

authorisation• EMV specification

interpretation• SDA/DDA• Risk parameters• PIN bypass• Plain text vs encrypted PIN

Industry timeframes

Education

Industry testing capability

• Customer• Merchant

Problem resolution / information sharing

Communications

Publicrelations

• Consumers

• All stakeholders

� �� ������ �

We need to implement EMV for tomorrow, not just today:

• Loyalty, healthcare, ticketing, mass transit etc. etc.

• Contactless, mobile phones and PDAs.

• Secure payment services via personal computers, interactive TV, etc.

• Build for future volumes!

$ �� �� ��� �� ���! �

+ �(� ������� ����The historical segregation of cards and payments is

breaking down

• Real-time payment assurance

• Mass-market reach

• Increasing importance of online business

=

Changing consumer demand: Will we be ready?

������������ ��

Sydney Technology and Innovation for Banking and Financial Services Conference

23 October 2007Chris Hamilton, CEO, APCA