Languages

Pages

Legal

2012

27th November, 2012

AGM

2012 Slide 2

This presentation has been prepared by Royal Resources Limited (ABN 34 108 102 432) (“Royal”) based on information available to it. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the information, opinions and conclusions contained in this presentation. To the maximum extent permitted by law, none of Royal, its related bodies corporate, its or their directors, employees or agents, advisers, nor any other person accepts any liability for any loss arising from the use of or reliance on this presentation or anything contained in, omitted from or otherwise arising in connection with it, including, without limitation, any liability arising from fault or negligence on the part of Royal, its related bodies corporate or its or their directors, employees or agents.

The details contained in this report that pertain to ore and mineralisation is based upon information compiled by Mr Marcus Flis, a full-time employee of the Company. Mr Flis is a Fellow of the Australasian Institute of Mining and Metallurgy (AUSIMM) and has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the December 2004 edition of the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves” (JORC Code). Mr Flis consents to the inclusion in this report of the matters based upon his information in the form and context in which it appears.

The distribution of this document in jurisdictions outside Australia may be restricted by law and you should observe any such restrictions.

This presentation is not an offer, invitation, solicitation or recommendation to invest in Royal and neither this document nor anything in it shall form the basis of any contract or commitment. The information in this presentation does not take into account the investment objectives, financial situation and particular needs of investors and does not constitute investment, legal, tax or other advice. Before making an investment in Royal an investor should consider whether such an investment is appropriate to their particular investment objectives , financial situation and particular needs and consult a financial adviser if necessary. This presentation does not purport to constitute all of the information that a potential investor may require in making an investment decision. Investments are subject to investment risk, including possible delays in repayment and loss of income or principal invested. Royal does not guarantee the performance of the investment referred to in this presentation, the repayment of any capital invested or any particular rate of return.

Nothing in this presentation is a promise or representation as to the future. Statements or assumptions in this presentation as to future matters may prove to be incorrect and differences may be material. Royal does not make any representation or warranty as to the accuracy of such statements or assumptions.

You acknowledge that circumstances may change and the contents of this presentation may become outdated as a result. Royal accepts no obligation to correct or update the information or opinions in this presentation. Opinions expressed are subject to change without notice.

By accepting this document, you agree to be bound by the above limitations.

DISCLAIMER AND COMPETENT PERSON’S STATEMENT

2012 Slide 3

Corporate

Projects Update

Outlook

OUTLINE

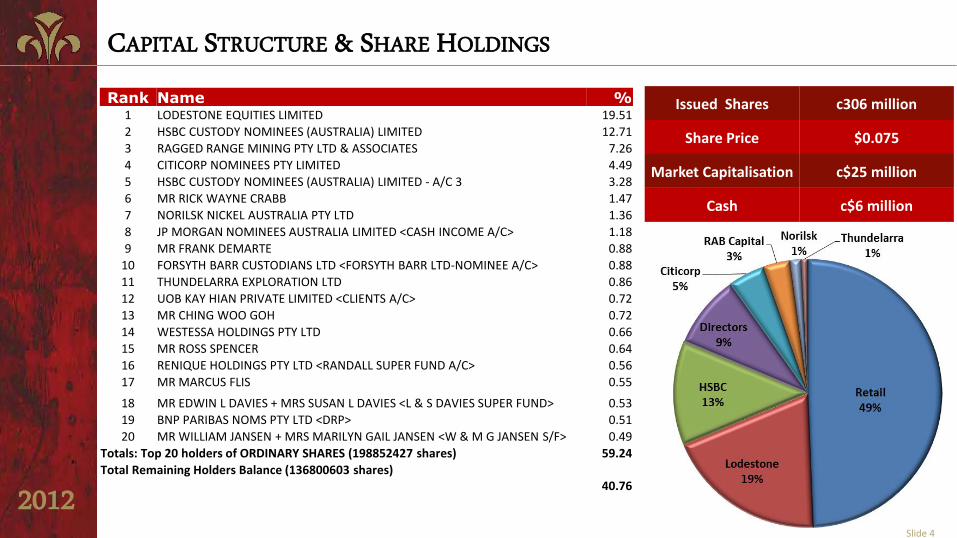

2012 Slide 4

Issued Shares c306 million

Share Price $0.075

Market Capitalisation c$25 million

Cash c$6 million

CAPITAL STRUCTURE & SHARE HOLDINGS

Rank Name % 1 LODESTONE EQUITIES LIMITED 19.51

2 HSBC CUSTODY NOMINEES (AUSTRALIA) LIMITED 12.71

3 RAGGED RANGE MINING PTY LTD & ASSOCIATES 7.26

4 CITICORP NOMINEES PTY LIMITED 4.49

5 HSBC CUSTODY NOMINEES (AUSTRALIA) LIMITED - A/C 3 3.28

6 MR RICK WAYNE CRABB 1.47

7 NORILSK NICKEL AUSTRALIA PTY LTD 1.36

8 JP MORGAN NOMINEES AUSTRALIA LIMITED <CASH INCOME A/C> 1.18

9 MR FRANK DEMARTE 0.88

10 FORSYTH BARR CUSTODIANS LTD <FORSYTH BARR LTD-NOMINEE A/C> 0.88

11 THUNDELARRA EXPLORATION LTD 0.86

12 UOB KAY HIAN PRIVATE LIMITED <CLIENTS A/C> 0.72

13 MR CHING WOO GOH 0.72

14 WESTESSA HOLDINGS PTY LTD 0.66

15 MR ROSS SPENCER 0.64

16 RENIQUE HOLDINGS PTY LTD <RANDALL SUPER FUND A/C> 0.56

17 MR MARCUS FLIS 0.55

18 MR EDWIN L DAVIES + MRS SUSAN L DAVIES <L & S DAVIES SUPER FUND> 0.53

19 BNP PARIBAS NOMS PTY LTD <DRP> 0.51

20 MR WILLIAM JANSEN + MRS MARILYN GAIL JANSEN <W & M G JANSEN S/F> 0.49

Totals: Top 20 holders of ORDINARY SHARES (198852427 shares) 59.24

Total Remaining Holders Balance (136800603 shares) 40.76

2012 Slide 5

ROYAL’S 12 MONTH SHARE PRICE PERFORMANCE & LIQUIDITY

2012 Slide 6

CORPORATE

Lodestone Equities Limited bought out the SinTang Development Pte Ltd

block of Royal shares and has become a significant shareholder in Royal

A capital raising of approx. $3.7 Million was undertaken at a 14%

premium to the market share price at the time. The placement was made

to Lodestone

Mr Brian Richardson resigned as a Non-executive Director

Mr Tony Heslop was appointed Company Secretary

A strategic decision was made to completely exit the Pilbara

Launch of the company’s newsletter, “Razorback”

2012 Slide 7

ANOTHER WAY TO COMMUNICATE WITH SHAREHOLDERS!

2012 Slide 8

Corporate

Projects Update

Outlook

OUTLINE

2012 Slide 9

PROJECTS UPDATE

2012 Slide 10

NON CORE PROJECTS

Royal exited the Pilbara on the basis of the stranded nature of the

prospects and the lack of size potential

The Warriedar Iron and Gold JVs were exited for a total consideration of

$8 million, alleviating the need for capital raising during the year

Successfully finalised the disposal of the bulk of our US uranium assets to

TSX listed Aldershot Resources Ltd

Buyers are being sought for the Fields Find and Water Tank tenements in

WA, with only minor field work been undertaken during the year

Drilling on our NT uranium tenements did not return any significant

results with work now being curtailed going into the wet season

2012 Slide 11

RED DRAGON VENTURE – FOUR AREAS ESTABLISHED & TWO AREAS EXPLORED

Razorback

Iron Peak

Iron Back Hill

Interzone

Dragon’s Head

Manunda

2012 Slide 12

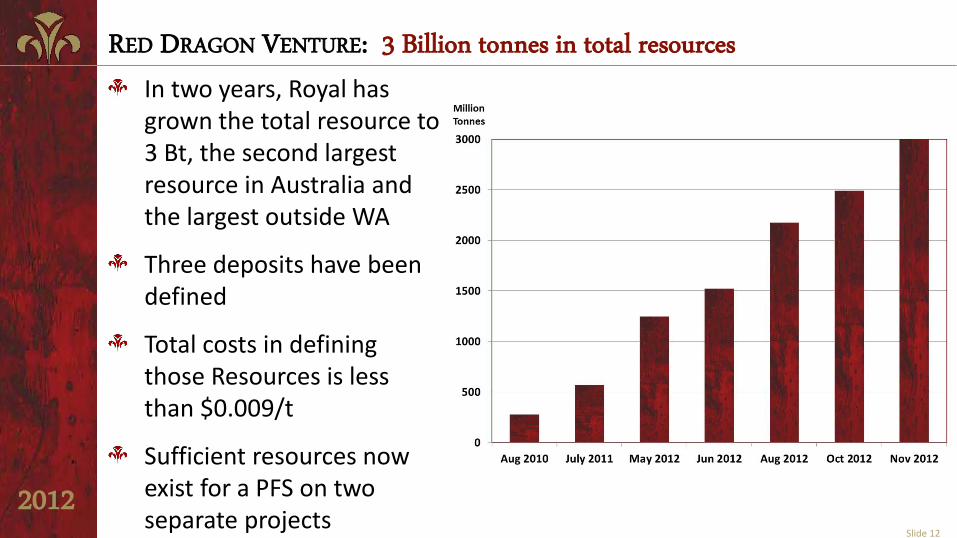

RED DRAGON VENTURE: 3 Billion tonnes in total resources

In two years, Royal has grown the total resource to 3 Bt, the second largest resource in Australia and the largest outside WA

Three deposits have been defined

Total costs in defining those Resources is less than $0.009/t

Sufficient resources now exist for a PFS on two separate projects

2012 Slide 13

RAZORBACK PREMIUM IRON PROJECT : 1.8 Billion tonnes of resources

JORC Resource Classification

Million Tonnes

Fe% SiO2% Al2O3% P%

Inferred 621 19.9 45.6 7.40 0.24 Indicated 1193 21.5 43.3 7.07 0.20 Total 1815 21 44.1 7.2 0.22

Current Inferred and Indicated Resources at the Razorback Deposit stand at:

Importantly, the indicative product grade is a premium grade concentrate*:

Premium Product Yield% Fe% SiO2% Al2O3% TiO2% V2O5% P% S%

Magnetite 16.3 68.3 3.80 0.43 0.098 0.017 0.013 0.003

LG Product Yield% Fe% SiO2% Al2O3% TiO2% V2O5% P% S%

Haematite 5.8 58.5 11.78 0.97 0.702 0.019 0.102 0.015

with the potential to increase yield to c22% by recovering a haematite concentrate*:

* Indicative grades only. Final product specification will depend on the final adopted flow sheet and project economics

2012 Slide 14

RAZORBACK PREMIUM IRON PROJECT: Pre-Feasibility Study near completion*

Completed To be done

Pit optimisation with annual

mining schedule

Beneficiation plant – flow sheet

Train load-out and transport to Pt

Pirie

Slurry pipeline options

Ship loading options

Water options

Power draw & options

Full equipment list

CAPEX estimates

OPEX estimates

Risk analysis

Financial Model

Getting the PFS in on time is nice, Getting it right is essential!

*Results of the PFS are due for release on its completion; currently planned for the end of 2012

2012 Slide 15

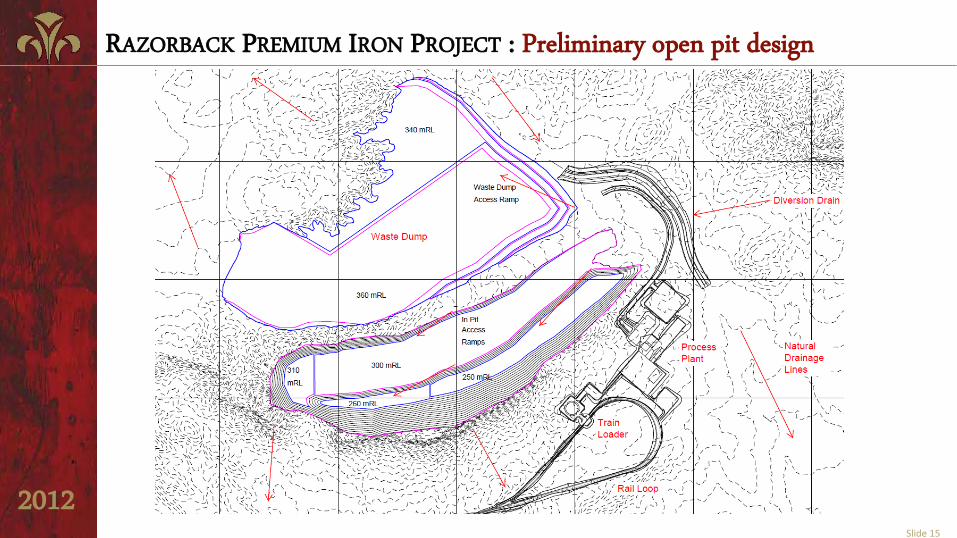

RAZORBACK PREMIUM IRON PROJECT : Preliminary open pit design

2012 Slide 16

RAZORBACK PREMIUM IRON PROJECT : Beneficiation plant layout

2012 Slide 17

RAZORBACK PREMIUM IRON PROJECT : Train load out option

2012 Slide 18

RAZORBACK PREMIUM IRON PROJECT : Transport options

2012 Slide 19

An exploration Native Title Mining Agreement is in place

A mining Native Title Mining Agreement has begun to be negotiated in

preparation for a Mining Licence Proposal application

A compensation package for the mining NTMA is likely to include

(based on peer packages):

• A monetary per tonne exported amount

• A commitment to employ aborigines

• Education and vocational training scholarships

• Cultural enhancement programmes

RAZORBACK PREMIUM IRON PROJECT : Native Title

2012 Slide 20

Source: Brook Hunt, BREE, Credit Suisse, Aug ‘12

RAZORBACK PREMIUM IRON PROJECT : Scoping Study Financials

Range of RPIP CFR OPEX

* Based on preliminary assessment; to be finalised CFR: Cost & Freight Source: Credit Suisse, Metalytics, Aug ‘12

Over 800Mt of higher cost iron ore needs to drop out of the seaborn iron market before affecting the RPIP product – RPIP is robust*

RPIP

*

2012 Slide 21

Corporate

Projects Update

Outlook

OUTLINE

2012 Slide 22

RAZORBACK PREMIUM IRON PROJECT : Next steps

2012 2013 2014 2015 2016

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Drilling to define min 1Bt

Pre Feasibility Study (PFS)

PFS Optimisation

Feasibility Study Funding

Feasibility Study

Permitting & Native Title

Project Financing

Board Approval

Design & Procurement

Construction & Commissioning

Razorback Start-up

2012 Slide 23

A MOUNTAIN OF IRON