Languages

Pages

Legal

CORPORATE PRESENTATIONDecember, 2014

“Inspiration and Innovation”

TSX: RIO BVL: RIO NYSE: RIOM 2

Cautionary Statement

Certain statements contained in this presentation may constitute forward-looking statements. These statements relate to future events or the future performance of Rio AltoMining Limited (“Rio Alto”) and Sulliden Gold Corporation Ltd. (“Sulliden”). All statements, other than statements of historical fact, may be forward-looking statements. Forward-looking statements are often, but not always, identified by the use of words such as "seek", "anticipate", "plan", "continue", "estimate", "expect", "may", "will", "project","predict", “propose”, "potential", "targeting", "intend", "could", "might", "should", "believe" and similar expressions. These statements involve known and unknown risks,uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking statements. Rio Alto believes that theexpectations reflected in those forward-looking statements are reasonable but no assurance can be given that these expectations will prove to be correct and such forward-lookingstatements included in this presentation should not be unduly relied upon by investors as actual results may vary. Unless required to be updated pursuant to securities laws, thesestatements speak only as of the date of this presentation and are expressly qualified, in their entirety, by this cautionary statement.

In particular, this presentation contains forward-looking statements, pertaining to the following: the anticipated benefits of the Arrangement to Rio Alto, Sulliden and theirrespective shareholders; the timing and anticipated receipt of required regulatory, court, and shareholder approvals for the Arrangement; the ability of Rio Alto, Sulliden andSpinCo to satisfy the other conditions to, and to complete, the Arrangement; the anticipated timing of the mailing of the information circular regarding the Arrangement; theclosing of the Arrangement; the development of the Shahuindo gold mine; the future gold production of Rio Alto and Sulliden; future cash costs of production; the gold resourcesand reserves of Rio Alto and Shahuindo; the development of the La Arena sulphide copper gold project; capital expenditure programs and cash flow estimates; the development ofdeposits, resources and reserves including the development of the La Arena sulphide project and the Shahuindo gold project; treatment under regulatory regimes; treatment undertaxation regimes or other government financial regimes; expectations regarding Rio Alto’s ability to raise capital and complete the feasibility study for the La Arena sulphideproject; the ability to bring the Shahuindo project to production; timing with respect to production from the Shahuindo project; the ability to realize value from Sulliden’s non-coreassets; expected synergies between the La Arena and Shahuindo projects; work plans to be conducted by Rio Alto; and the production and production growth of gold and copperfrom Rio Alto’s La Arena project and gold from Sulliden’s Shahuindo project.

With respect to forward-looking statements listed above and contained in this presentation, Rio Alto has made assumptions regarding, among other things: the legislative andregulatory environment; the impact of increasing competition; current technological trends; unpredictable changes to market prices for gold and copper; that costs related todevelopment of the gold and copper properties and the development of gold and copper production projects will remain consistent with historical experiences; anticipated resultsof exploration and development activities; and Rio Alto’s ability to obtain additional financing on satisfactory terms.

Rio Alto’s actual results could differ materially from those anticipated in these forward-looking statements as a result of the risk factors set forth below and elsewhere in thispresentation: uncertainties regarding the regulatory regime and the application approval process; volatility in the market prices for gold and copper; uncertainties associated withestimating and developing resources; geological, technical, construction and processing problems; liabilities and risks, including environmental liabilities and risks, inherent indeveloping gold and copper production projects; fluctuations in currency and interest rates; competition for, among other things, capital, acquisitions of reserves, undevelopedlands and skilled personnel; and unpredictable weather conditions.

TSX: RIO BVL: RIO NYSE: RIOM 3

Cautionary Statement

Rio Alto’s plans and results could differ materially from those anticipated in these forward-looking statements as a result of these risk factors set forth above. Rio Alto recommendsthat you also review its and Sulliden’s most recent Annual Information Form and Annual MD&A for a discussion of other material risks that could cause actual results to differsignificantly from current expectations.

This Presentation also discloses mineral resources. Mineral resources that are not mineral reserves do not have demonstrated economic viability. Certain technical and scientificinformation contained in this presentation has been taken from the La Arena Project, Peru - Technical Report (the “July 2010 Report”) with effective date of July 31, 2010, preparedby Coffey Mining Pty Ltd. (“Coffey Mining”) on behalf of Rio Alto Mining Limited or is based upon supporting documentation provided by Coffey Mining. A copy of the TechnicalReport is available on Rio Alto’s SEDAR profile at www.sedar.com. This presentation also includes updated resource estimates dated effective September 30, 2011 in respect of theoxide and sulphide projects that comprise La Arena Project. A technical report which provides for these updated resource estimates has been filed on Rio Alto’s SEDAR profile. Thetechnical and scientific information contained in this presentation has been reviewed and verified by Mr. Enrique Garay, M Sc., P. Geo (AIG Member), Vice President Geology of RioAlto, the Qualified Person (as defined by NI 43-101) responsible for managing Rio Alto’s exploration programs and disclosure of drilling results, and by Mr. Ian Dreyer, B.App. Sc.(AUSIMM 305241,CP), a Qualified Person (as defined by NI 43-101), formerly of Coffey Mining, who designed and reviewed Rio Alto’s Quality Control and Assurance Program andprepared the updated resource estimates.

Certain technical and scientific information with respect to the Shahuindo project contained in this presentation has been taken from the technical report entitled “TechnicalReport on the Shahuindo Heap Leach Project, Cajabamba, Peru” (the “Shahuindo Technical Report”) with an effective date of September 26, 2012, prepared by Mr. Paul Tietz, CPG,and Mr. Thomas L. Dyer, both of Mine Development Associates, Inc., and Mr. Carl Defilippi of Kappes, Cassiday & Associates. A copy of the Shahuindo Technical Report is availableon Sulliden’s SEDAR profile at www.sedar.com.

“Cash costs" per ounce figures are non-GAAP measures. This data is furnished to provide additional information and is a non-IFRS measure. Cash costs presented do not have astandardized meaning under IFRS and may not be comparable to similar measures presented by other mining companies. It should not be considered in isolation as a substitute formeasures of performance prepared in accordance with IFRS.

TSX: RIO BVL: RIO NYSE: RIOM 4

Acquisition of Sulliden Gold Corp.

Created a leading mid-tier gold producer with a strong portfolio of assets in a world-class mining district in Peru

Low-Cost

Development

Enhanced

Growth

Leverage Core

Competencies

Increased

Resources &

Reserves

Accretive to

Key Metrics

Strong Re-Rate

Potential

Gold

Production

Enhanced

Financial

Position

Ownership in

SpinCo

TSX: RIO BVL: RIO NYSE: RIOM

Capital Structure

5

TSX: RIOBVL: RIONYSE: RIOM

Shares Issued (November 27, 2014) 332.6 million

Warrants Outstanding (Agnico Eagle @ $2.40 by April 12 2015) 9.9 million

Options Outstanding: (Av. Exercise Price – C$ 1.91) 17.6 million

Fully Diluted: 360.1 million

Share Price: C$2.79as at Nov 27, 2014

Market Cap (issued capital): approx. C$927.9 million

TSX: RIO BVL: RIO NYSE: RIOM 6

Share Price Performance – 3 years

Sulliden AcquisitionAnnounced

TSX: RIO BVL: RIO NYSE: RIOM

Dr. Klaus Zeitler | Non Exec Chairman

Alex Black | President, CEO

Victor Gobitz Colchado | Director

Drago Kisic Wagner | Director

Sidney Robinson | Director

Ram Ramachandran | Director

Peter Tagliamonte | Director

Bruce Humphrey | Director

7

Management Team

Board of DirectorsManagement

• Alex Black (President, CEO, Director)– 33 years of industry experience

– Founder & former Managing Director of Global Mining Services

– Founder AGR Limited (Boroo Gold Project, Mongolia & Salman Gold Project, Ghana)

– Founder of Rio Alto Mining Limited

• Eduardo Loret de Mola (Chief Operating Officer)– Over 35 years of industry experience

– Former Corporate Manager for Trafigura

– Former International Operations Manager for Hochschild

• Kathryn Johnson (Chief Financial Officer)– Former Corporate Controller at Petaquilla Minerals

• Augusto Chung (VP Projects)– Former Generate Manager of Compania Minera Milpo

– Project manager for the construction of Lagunas Norte

• Tim Williams (VP Operations)– Over 18 years of industry experience

– Former operations manager for GyM – Stracon in Peru

• Enrique Garay (VP Geology)– Over 22 years of industry experience

– Previously worked with Barrick, Hochschild, Trafigura and ConsorcioMinero Horizonte

Extensive Operating Capabilities and In-Region Expertise in Latin America

TSX: RIO BVL: RIO NYSE: RIOM 8

Project Locations – Peru Focus

Vancouver

Admin Office

Lima Head

Office

#1 Gold producer in Latin America

#6 Gold producer in the world

#2 Silver producer in the world

#2 Copper producer in the world

#3 Zinc and Tin producer in the world

Major International Companies in Peru

• Barrick Gold • Hudbay

• Newmont Mining • Glencore Xstrata

• Buenaventura • Anglo American

• BHP Billiton • Jianxi Copper

• Gold Fields • Rio Tinto

• Southern Copper • MMG

• Pan American Silver • Chinalco

• Teck

Source: Company disclosure

1. Forecasts based on Sulliden’s technical report entitled “Technical Report on the Shahuindo Heap Leach Project, Cajabamba, Peru” (the “Shahuindo Technical Report”) with an effective date of September 26, 2012

2. Based on Rio Alto’s 2014 production and cost guidance

La Arena Oxides2

2014E Production:

2014E Cash Costs:

2P Reserves Au:

M&I Resources Au:

200-220koz Au

$629-$695/oz Au

1.1Moz @ 0.43g/t

1.3Moz @ 0.41g/t

La Arena Sulphides

2P Reserves Au:

M&I Resources Au:

2P Reserves Cu:

M&I Resources Cu:

2.1Moz @ 0.24g/t

3.8Moz @ 0.21g/t

1.9Blbs @ 0.33%

3.7Blbs @ 0.30%

Shahuindo1

Avg Prod (10ktpd):

Avg Cash Costs:

2P Reserves Au:

M&I Resources Au:

84.5koz Au

$552/oz Au

1.0Moz @ 0.84g/t

2.4Moz @ 0.52g/t

Lima

Pierina

World-Class Gold District

Cerro

CoronaTantahuatay

La Zanja

Yanacocha

Conga

Lagunas Norte

TSX: RIO BVL: RIO NYSE: RIOM 9

Solid Track Record – Execution & Delivery

Leverage Experience from La Arena to Fast Track Production at Shahuindo

2009-10

2011

2012

2013

Today

The FutureRio Alto Will Apply its Development Approach

for La Arena to the Development of Shahuindo

• Q1 production of 53,463 gold ounces

• 2014 production guidance of 200-220 kozs gold at cash

costs of $629-$695 per oz

• Cost optimization of oxide operations

• Oxides reserves increased by ~95% since startup

• Phase II Feasibility study in Q4 2014

• Continued expansion of oxide mineralization

• Production of 214,742 gold ounces

• Consistent positive grade reconciliation

• Production of 201,113 gold ounces

• Expansion to 36,000 tpd 18 months post start-up

• Acquisition of La Arena from IAMGOLD

• Increased reserves to 821 kozs and began construction

• Startup at 10,000 tpd; Production of 51,398 gold ounces

• US$50 million capex with a 10 month build

• Expansion to 24,000 tpd 12 months post start-up

TSX: RIO BVL: RIO NYSE: RIOM 10

Balanced Pipeline of Quality Assets

Strong Organic Growth From Combined Project Pipeline

Current

Production

Near-Term

Construction

Brownfield

Expansion and

Development

Exploration Potential

• La Arena production of 200 – 220 kozs in 2014 at attractive and decreasing cash costs

• Opportunity for further extension of current oxide heap leach operation via ongoing exploration success

• Commencement of Shahuindo construction in 2015 with first production bylate 2015 / early 2016

• Forecast initial production of approximately 100 kozs gold per annum fromShahuindo at 10,000tpd

• Shahuindo expansion from 10,000 tpd to 25,000 – 36,000 tpd

• Future growth from development of La Arena Phase II copper-gold porphyry

• ~55,800 hectare land package in a highly prospective region of Peru that hosts several significant deposits

• Significant exploration upside at both properties

TSX: RIO BVL: RIO NYSE: RIOM 11

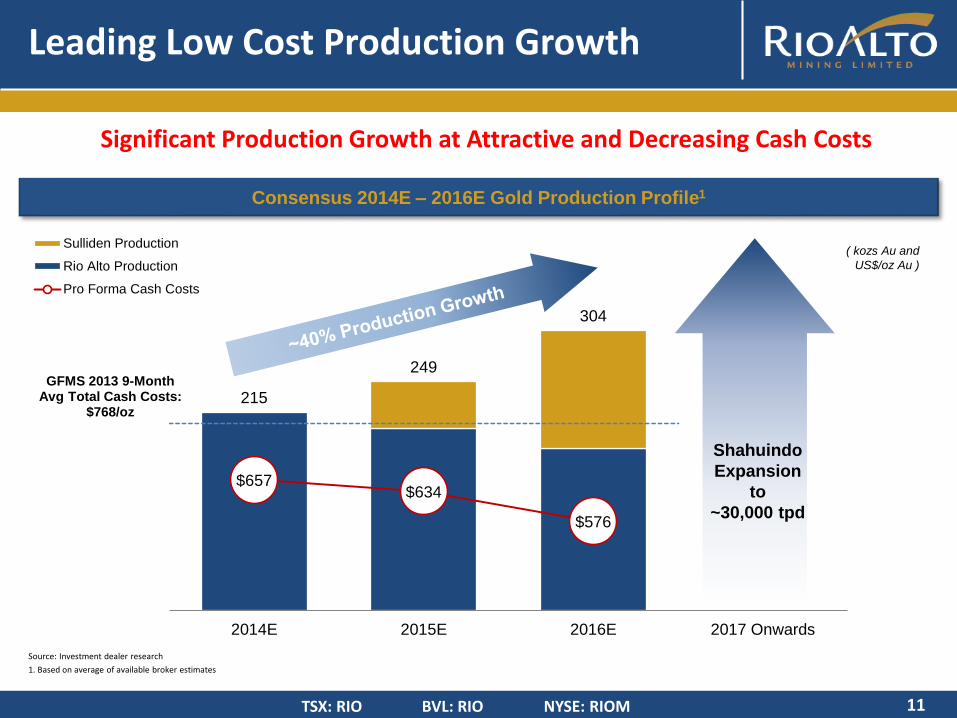

Leading Low Cost Production Growth

Significant Production Growth at Attractive and Decreasing Cash Costs

Consensus 2014E – 2016E Gold Production Profile1

215

249

304

GFMS 2013 9-Month Avg Total Cash Costs:

$768/oz

$657 $634

$576

2014E 2015E 2016E 2017 Onwards

Sulliden Production

Rio Alto Production

Pro Forma Cash Costs

Shahuindo

Expansion

to

~30,000 tpd

( kozs Au and

US$/oz Au )

Source: Investment dealer research

1. Based on average of available broker estimates

TSX: RIO BVL: RIO NYSE: RIOM 12

Robust Mineral Resource Base

Significant Resources to Support Production Growth and Long Life Operations

Oxide Mineral Reserves and Resources1 Global Mineral Resources1

1.1 1.1

0.2 0.2

1.0

1.0 1.4

1.4

Rio Alto Sulliden New Rio Alto

SUE Inferred Resources

SUE M&I Resources (exclusive)

SUE 2P Reserves

RIO Inferred Resources

RIO M&I Resources (exclusive)

RIO 2P Reserves

( Mozs Au )

5.2 5.2

2.4

2.4

1.6

1.6

Rio Alto Sulliden New Rio Alto

SUE Inferred Resources

SUE M&I Resources (inclusive)

RIO Inferred Resources

RIO M&I Resources (inclusive)

( Mozs Au )

La Arena La ArenaShahuindo ShahuindoCombined CombinedSource: Company disclosure

1. See slide 25 and 26 for detailed information on mineral reserves and resources for La Arena and Shahuindo

TSX: RIO BVL: RIO NYSE: RIOM 13

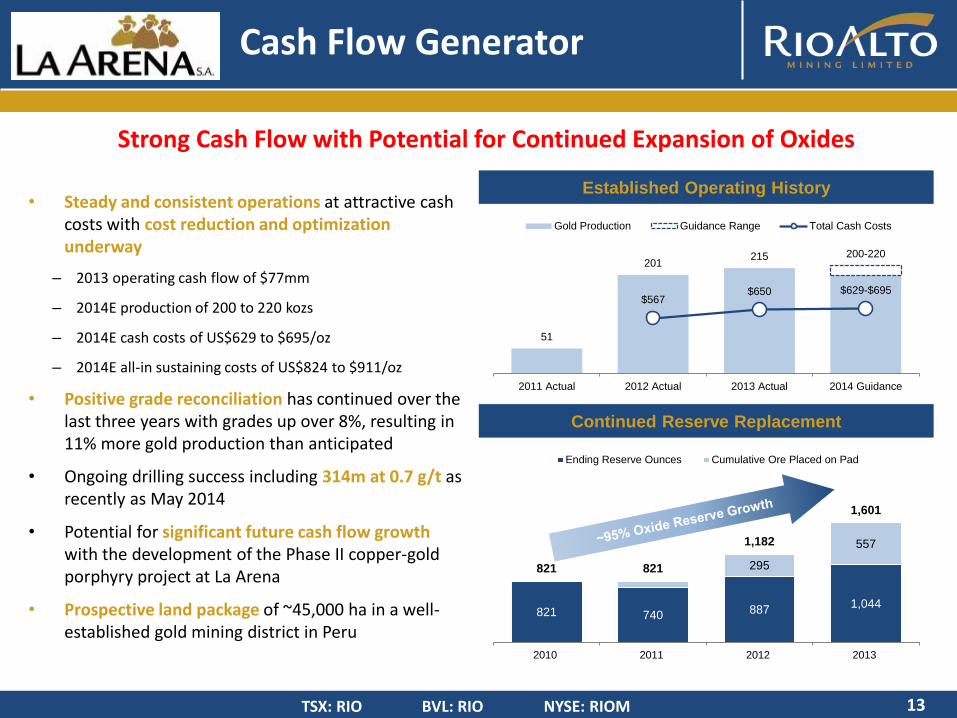

Cash Flow Generator

Strong Cash Flow with Potential for Continued Expansion of Oxides

• Steady and consistent operations at attractive cash costs with cost reduction and optimization underway

– 2013 operating cash flow of $77mm

– 2014E production of 200 to 220 kozs

– 2014E cash costs of US$629 to $695/oz

– 2014E all-in sustaining costs of US$824 to $911/oz

• Positive grade reconciliation has continued over the last three years with grades up over 8%, resulting in 11% more gold production than anticipated

• Ongoing drilling success including 314m at 0.7 g/t as recently as May 2014

• Potential for significant future cash flow growth with the development of the Phase II copper-gold porphyry project at La Arena

• Prospective land package of ~45,000 ha in a well-established gold mining district in Peru

Established Operating History

51

201 215 200-220

$567 $650 $629-$695

2011 Actual 2012 Actual 2013 Actual 2014 Guidance

Gold Production Guidance Range Total Cash Costs

Continued Reserve Replacement

821 740 887 1,044

295

557

821 821

1,182

1,601

2010 2011 2012 2013

Ending Reserve Ounces Cumulative Ore Placed on Pad

TSX: RIO BVL: RIO NYSE: RIOM 14

Production & Sales

Production 2012 201,113 oz

Production 2013 214,742 oz

Production Guidance 2014 200 – 220,000 oz_________________________________________________________________________________________________________________________________________________

Cost Guidance for 2013 (WGC) Actual

Adjusted Operating Cost US$ 675 to US$ 725 / oz $ 650

All-in sustaining costs US$ 900 to US$ 1,000 / oz $ 880

All-in costs US$ 1,200 to US$ 1,300 / oz $ 1,073 ________________________________________________________________________________________________________________________________________________

Cost Guidance for 2014 (WGC) Actual Q1 ‘14 Q2 ‘14

Adjusted Operating Cost US$ 629 to US$ 695 / oz $ 651 $ 569

All-in sustaining costs US$ 824 to US$ 911 / oz $ 773 $ 772

All-in costs US$ 990 to US$ 1,094 / oz $ 914 $ 879

COST REDUCTION AND OPTIMIZATION ONGOING –

HEADING IN RIGHT DIRECTION

Great Result !!!

Cost Optimization Program

TSX: RIO BVL: RIO NYSE: RIOM 15

Social & Community

TSX: RIO BVL: RIO NYSE: RIOM 16

Reclamation work on waste dump No. 1

Environmental Responsibility

TSX: RIO BVL: RIO NYSE: RIOM 17

Calaorco Pit Panorama – July 2014

Site Panorama – March 2014

Mining Progress

TSX: RIO BVL: RIO NYSE: RIOM 18

Near-Term Growth Driver

Near-Term Low Cost Heap Leach Gold Production with a Substantial Resource

• Highly attractive scalable project with top tier economics based on the September 2012 Feasibility Study

10,000 tpd operation and low strip ratio of 1.91:1

Initial production forecast to be ~100,000 ounces gold per year with a 10 year mine life

Cash costs of US$552/oz gold and US$826/oz gold all-in

Initial capex of US$132 million

NPV of US$249 million at US$1,415/oz gold and 5% discount rate

IRR of ~38% and payback period of 2.2 years

• Currently in advanced stages of permitting

Environmental Impact Assessment (“EIA”) approved by the Peruvian Government in September 2013

Remaining process permits, authorizations and applications underway and moving towards construction phase

• Large resource base with strong upside potential to support expanded operating scenarios and long-life operations

Mineral reserves represent only ~40% of M&I oxide resources

Numerous regional targets remain largely unexplored

Source: Sulliden’s technical report entitled “Technical Report on the Shahuindo Heap Leach Project, Cajabamba, Peru” (the “Shahuindo Technical Report”) with an effective date of September 26, 2012 and other company disclosure

TSX: RIO BVL: RIO NYSE: RIOM 19

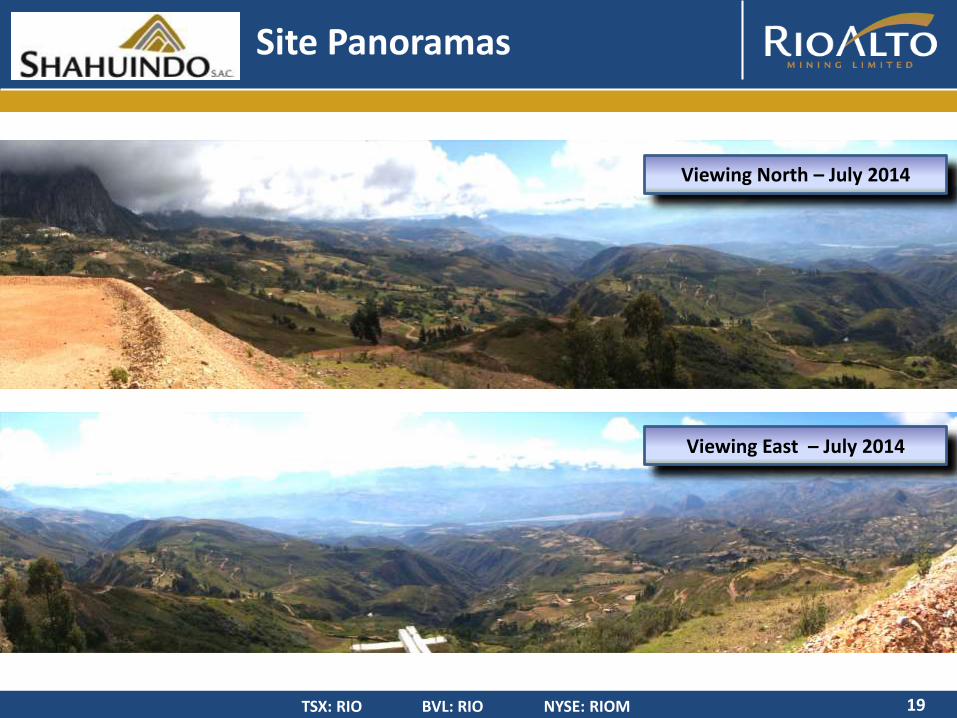

Site Panoramas

Viewing North – July 2014

Viewing East – July 2014

TSX: RIO BVL: RIO NYSE: RIOM 20

Production Scale & Growth

2014E / 2016E Consensus Gold Production (kozs Au)1

406

220 215 202160 138

300

215

123

612

308 304 272

231 210 210 176

127

B2Gold AuRico New Rio Primero Alamos Argonaut OceanaGold Rio Alto Timmins

Gold Mineral Reserves (mm ozs Au)

6.5

5.4

4.2

3.2 3.1 3.0

2.3 2.0

1.6

AuRico B2Gold New Rio Rio Alto OceanaGold Argonaut Primero Alamos Timmins

Source: FactSet, Bloomberg, company disclosure, available broker reports

1. Shown on a basic basis

TSX: RIO BVL: RIO NYSE: RIOM 21

Next Steps

• Integrate personnel and operating philosophies

• Leverage La Arena experience and re-evaluate Shahuindo development approach

• Evaluate synergies and opportunities to maximize value at Shahuindo

• Deliver on key operational goals, including the accelerated start-up of Shahuindoby late 2015 / early 2016

• Continue expanding La Arena oxides and evaluate the Phase II expansion

• Pursue growth opportunities in the Americas

TSX: RIO BVL: RIO NYSE: RIOM

1.3

3.8

Current New Rio Alto Future

22

Summary

Rio Alto is Ideally Positioned as a

New Leading Low-Cost Mid-Tier Gold Producer

• High quality operating and development gold assets in a world-class mining jurisdiction

• Significant resource base supporting leading organic production growth

• Strong financial position with superior and growing cash flow

• Experienced and proven management team with a track record of execution and delivery

• Low-cost heap leach producer in mining friendly Peru should attract a premium multiple

• Compelling value proposition driven by quality

215

304

Current(2014 Consensus)

New Rio Alto(2016 Consensus)

Future

~40% Production Growth by 2016

Shahuindo

Expansion to

~36,000 tpd

~180% Increase to M&I Oxide Resources

Prospective

Exploration

Packages

(kozs)

(Mozs)

Source: Company disclosure, available broker reports

Contact Us:

Rio AltoSuite 1950 – 400 Burrard Street

Vancouver, BC V6C 3A6

Telephone: +1 604 628 1401

Investor Relations: +1 877 628 1401

Alex Black, Director, President & CEO [email protected]

Alejandra Gomez, Manager Investor Relations [email protected]

TSX: RIO BVL: RIO NYSE: RIOM

La Arena – Positive Cash Generator

24

Worried by a declining gold price and the impact on RIO???

Great upside to a rising gold price!!!

The New Rio Alto - A Leading Americas Focused Mid-Tier Gold Producer

Quantity Grades Contained

Gold Silver Copper Gold Silver Copper

(kt) (g/t) (g/t) (%) (kozs) (kozs) (Mlbs)

Proven & Probable Reserves

Oxides - Proven Reserves 2,800 0.35 0.6 0.03% 32 -- --

Oxides - Probable Reserves 75,400 0.43 0.4 0.04% 1,046 -- --

Oxides - Proven & Probable Reserves 78,200 0.43 0.5 0.04% 1,078 -- --

Sulphides - Proven Reserves 100 0.32 -- 0.29% 1 -- 1

Sulphides - Probable Reserves 268,700 0.24 -- 0.33% 2,091 -- 1,946

Sulphides - Proven & Probable Reserves 268,900 0.24 -- 0.33% 2,092 -- 1,947

Total - Proven Reserves 2,900 0.35 -- 0.01% 33 -- 1

Total - Probable Reserves 344,100 0.28 -- 0.26% 3,137 -- 1,946

Total - Proven & Probable Reserves 347,100 0.28 -- 0.25% 3,170 -- 1,947

Measured and Indicated Resources (Inclusive of Reserves)

Oxides - Measured Resources 2,000 0.43 2.6 0.04% 28 -- --

Oxides - Indicated Resources 98,200 0.41 1.5 0.04% 1,299 -- --

Oxides - Measured & Indicated Resources 100,200 0.41 1.5 0.04% 1,327 -- --

Sulphides - Measured Resources -- -- -- -- -- -- --

Sulphides - Indicated Resources 561,700 0.21 0.4 0.30% 3,829 -- 3,746

Sulphides - Measured & Indicated Resources 561,700 0.21 0.4 0.30% 3,829 -- 3,746

Total - Measured Resources 2,000 0.43 2.6 0.04% 28 -- --

Total - Indicated Resources 659,900 0.24 0.0 0.26% 5,128 -- 3,746

Total - Measured & Indicated Resources 661,900 0.24 0.0 0.26% 5,156 -- 3,746

Inferred Resources

Oxides - Inferred Resources 300 0.20 0.7 0.01% 2 -- --

Sulphides - Inferred Resources 32,500 0.11 0.4 0.19% 116 -- 137

Total - Inferred Resources 32,800 0.11 0.0 0.19% 118 -- 137

Mineral Reserves and Resources – La Arena

25

Note: La Arena oxide mineral reserves and resources as at December 31, 2013. La Arena sulphide mineral resources as at January 1, 2013

The New Rio Alto - A Leading Americas Focused Mid-Tier Gold Producer

Quantity Grades Contained

Gold Silver Copper Gold Silver Copper

(kt) (g/t) (g/t) (%) (kozs) (kozs) (Mlbs)

Proven & Probable Reserves

Oxides - Proven Reserves 14,994 0.90 10.4 -- 434 5,008 --

Oxides - Probable Reserves 22,595 0.80 8.8 -- 582 6,396 --

Oxides - Proven & Probable Reserves 37,589 0.84 9.4 -- 1,015 11,404 --

Mixed - Proven Reserves 165 0.71 17.6 -- 4 93 --

Mixed - Probable Reserves 93 0.87 21.3 -- 3 64 --

Mixed - Proven & Probable Reserves 258 0.76 18.9 -- 6 157 --

Total - Proven Reserves 15,159 0.90 10.5 -- 437 5,102 --

Total - Probable Reserves 22,688 0.80 9.4 -- 584 6,459 --

Total - Proven & Probable Reserves 37,847 0.84 9.5 -- 1,022 11,561 --

Measured and Indicated Resources (Inclusive of Reserves)

Oxides - Measured Resources 40,500 0.59 8.1 -- 766 10,530 --

Oxides - Indicated Resources 104,840 0.48 6.3 -- 1,624 21,080 --

Oxides - Measured & Indicated Resources 145,340 0.51 6.8 -- 2,390 31,610 --

Mixed - Measured Resources 780 0.75 33.7 -- 19 850 --

Mixed - Indicated Resources 1,190 0.77 23.8 -- 29 910 --

Mixed - Measured & Indicated Resources 1,970 0.76 27.8 -- 48 1,760 --

Total - Measured Resources 41,280 0.59 8.6 -- 785 11,380 --

Total - Indicated Resources 106,030 0.48 6.5 -- 1,653 21,990 --

Total - Measured & Indicated Resources 147,310 0.52 7.1 -- 2,438 33,370 --

Inferred Resources

Oxides - Inferred Resources 9,570 0.40 4.3 -- 124 1,330 --

Mixed - Inferred Resources 20 0.68 12.2 -- 0 10 --

Sulphides - Inferred Resources 61,410 0.76 22.9 -- 1,504 45,220 --

Total - Inferred Resources 71,000 0.71 20.4 -- 1,628 46,560 --

Mineral Reserves and Resources – Shahuindo

26

Note: Shahuindo mineral reserves and resources as at September 2012

Top Related