Languages

Pages

Legal

AugustAugustAugustAugust 200 200 200 2002222

TELECOMMUNICATIONS BUREAU,MINISTRY OF PUBLIC MANAGEMENT,HOME AFFAIRS, POSTS ANDTELECOMMUNICATIONS (MPHPT)

i

Contents

I. Development of Japanese pro-competition policy ........................................................... 11. Outline......................................................................................................................... 12. Pro-competition policy in telecommunications business for

promoting IT revolution ............................................................................................... 23. Establishment of interconnection rules ....................................................................... 44. Outline of NTT Reorganization Scheme ..................................................................... 5

II. Current situation surrounding the telecommunications business..................................... 61. Changes in the total number of telecommunications carriers..................................... 62. Current Status of Main Foreign Investment in Telecommunications Carriers............. 73. Changes in market size / investment in facilities and equipment ............................... 94. Shares of NTT / KDD and NCC ................................................................................ 105. Current Status of Rate Reductions ........................................................................... 12

III. Internet ........................................................................................................................... 141. Total Internet user population and Internet diffusion rate.......................................... 142. International comparison of full-time Internet connection fees ................................. 163. Construction of fiber-optic networks ......................................................................... 174. Major support systems for fiber-optic networks and broadband access network ..... 19

IV. Mobile communications.................................................................................................. 201. Status of diffusion of mobile phones......................................................................... 202. Growth Factors in the Mobile Phone Market ............................................................ 21

V. Introduction of new wireless system .............................................................................. 221. The third-generation mobile communications system .............................................. 222. The fourth-generation mobile communications system ............................................ 233. Wireless access system............................................................................................ 25

VI. Diffusion of major radio stations ..................................................................................... 261. Transition in the Number of Cellular Phones ............................................................ 262. Transition in the Number of PHS Subscribers .......................................................... 263. Transition in the Number of Radio Pagers................................................................ 274. Transition in the Number of VAST Earth Stations..................................................... 27

References

Reference 1. Diffusion of cable television ............................................................................... 29Reference 2. Current Status of Broadcasting Business in Japan ........................................... 30

1

1985

.4(L

iber

aliz

atio

n of

the

tele

com

mun

icat

ions

bus

ines

s)

○ U

ser r

ates

refo

rm:

Abol

ition

of a

sys

tem

by

whi

ch th

e go

vern

men

t offi

cial

ly a

ppro

ves

the

tele

com

serv

ice

fees

(Nov

embe

r 199

8)

○ U

ser r

ates

refo

rm:

Abol

ition

of a

sys

tem

by

whi

ch th

e go

vern

men

t offi

cial

ly a

ppro

ves

the

tele

com

serv

ice

fees

(Nov

embe

r 199

8)19

99.7

○ U

ser r

ates

regu

latio

n fo

r NTT

Wes

t/Eas

t:In

trodu

ctio

n of

a p

rice-

cap

syst

em (O

ctob

er 2

000)

○ U

ser r

ates

regu

latio

n fo

r NTT

Wes

t/Eas

t:In

trodu

ctio

n of

a p

rice-

cap

syst

em (O

ctob

er 2

000)

○ F

orei

gn o

wne

rshi

p re

stric

tion:

Lifti

ng o

f the

rest

rictio

ns o

n fo

reig

n-ca

pita

l inv

estm

ent i

n th

e Ty

pe 1

car

riers

(Exc

ludi

ng in

vest

men

t in

NTT

and

KD

D) (

Febr

uary

199

8)

○ F

orei

gn o

wne

rshi

p re

stric

tion:

Lifti

ng o

f the

rest

rictio

ns o

n fo

reig

n-ca

pita

l inv

estm

ent i

n th

e Ty

pe 1

car

riers

(Exc

ludi

ng in

vest

men

t in

NTT

and

KD

D) (

Febr

uary

199

8)

○ E

ntry

into

the

mar

ket:

Abol

ition

of t

he re

gula

tion

on s

uppl

y an

d de

man

d (N

ovem

ber 1

997)

○ In

terc

onne

ctio

n:Es

tabl

ishm

ent o

f new

rule

on

inte

rcon

nect

ions

, inc

ludi

ng in

trodu

ctio

n of

gen

eral

oblig

atio

ns fo

r typ

e-I c

arrie

rs to

inte

rcon

nect

with

oth

er n

etw

orks

(Nov

embe

r19

97)

○ E

ntry

into

the

mar

ket:

Abol

ition

of t

he re

gula

tion

on s

uppl

y an

d de

man

d (N

ovem

ber 1

997)

○ In

terc

onne

ctio

n:Es

tabl

ishm

ent o

f new

rule

on

inte

rcon

nect

ions

, inc

ludi

ng in

trodu

ctio

n of

gen

eral

oblig

atio

ns fo

r typ

e-I c

arrie

rs to

inte

rcon

nect

with

oth

er n

etw

orks

(Nov

embe

r19

97)

○In

terc

onne

ctio

n:In

trodu

ctio

n of

a lo

ng-ru

n in

crem

enta

l cos

t met

hodo

logy

.○

Inte

rcon

nect

ion:

Intro

duct

ion

of a

long

-run

incr

emen

tal c

ost m

etho

dolo

gy.

Reo

rgan

izat

ion

of N

TT

Priv

atiz

atio

n of

Nip

pon

Tele

grap

h an

dTe

leph

one

Publ

icC

orpo

ratio

n

○Te

leco

mm

unic

atio

ns C

ounc

il R

epor

t:

The

first

repo

rt on

des

irabl

e pr

o-co

mpe

titiv

e po

licie

s in

the

tele

com

mun

icat

ions

busi

ness

fiel

d fo

r pro

mot

ing

the

IT re

volu

tion

com

pile

d by

the

Tele

com

mun

icat

ions

Cou

ncil

(Dec

embe

r 200

0)

○Te

leco

mm

unic

atio

ns C

ounc

il R

epor

t:

The

first

repo

rt on

des

irabl

e pr

o-co

mpe

titiv

e po

licie

s in

the

tele

com

mun

icat

ions

busi

ness

fiel

d fo

r pro

mot

ing

the

IT re

volu

tion

com

pile

d by

the

Tele

com

mun

icat

ions

Cou

ncil

(Dec

embe

r 200

0)

Rev

iew

of t

he fr

amew

ork

ofpr

o-co

mpe

titio

n po

licy

Rev

iew

of t

he fr

amew

ork

ofpr

o-co

mpe

titio

n po

licy

○ D

iscu

ssio

ns o

n th

e en

viro

nmen

t for

fair

com

petit

ion

invo

lvin

g al

lse

ctor

s, in

clud

ing

cont

ents

and

app

licat

ions

.○

Dis

cuss

ions

on

the

envi

ronm

ent f

or fa

ir co

mpe

titio

n in

volv

ing

all

sect

ors,

incl

udin

g co

nten

ts a

nd a

pplic

atio

ns.

2001

.6

○Th

e Te

leco

mm

unic

atio

ns C

ounc

il’s s

econ

d re

com

men

datio

n tit

led

“Inte

rcon

nect

ion

rule

s in

the

age

of in

form

atio

n te

chno

logy

” (Ju

ly20

01)

○Th

e Te

leco

mm

unic

atio

ns C

ounc

il’s s

econ

d re

com

men

datio

n tit

led

“Inte

rcon

nect

ion

rule

s in

the

age

of in

form

atio

n te

chno

logy

” (Ju

ly20

01)

○Th

e fir

st re

com

men

datio

n fro

m th

e Te

leco

mm

unic

atio

ns C

ounc

ilon

the

"Rev

iew

of i

nter

conn

ectio

n ru

les"

(Dec

embe

r 200

0)○

The

first

reco

mm

enda

tion

from

the

Tele

com

mun

icat

ions

Cou

ncil

on th

e "R

evie

w o

f int

erco

nnec

tion

rule

s" (D

ecem

ber 2

000)

Rev

isio

n of

the

Tele

com

mun

icat

ions

Bus

ines

s La

w a

ndot

her L

egis

latio

n

I. Development of Japanese pro-competition policy

1. Outline

2

2. Pro-competition policy in the telecommunications carriers business forpromoting the IT revolution○ On the basis of the first recommendation compiled by the Telecommunications Council

concerning the pro-competition policy in the telecommuncations industry to promotethe IT revolution (published on Dec. 21, 2000), the three-year deregulation planapproved by the Cabinet on March 31, 2001, and others, the government submittedrevision bills of the Telecommunications Business Law and other related laws to the151 Regular Diet session. The bills were legislated on June 15, 2001 and most of themwere put into force on Nov. 30 of the same year.

3

Esta

blis

hmen

t of r

ules

for f

air c

ompe

titio

nFu

rther

der

egul

atio

nPr

omot

ion

of e

stab

lishm

ent o

f an

IT in

frast

ruct

ure

Esta

blis

hmen

t of a

sym

met

ric re

gula

tions

Esta

blis

hmen

t of a

sys

tem

con

cern

ing

univ

ersa

l tel

epho

ny s

ervi

ce

Esta

blis

hmen

t of a

com

mitt

ee to

set

tle

disp

utes

invo

lvin

g th

e te

leco

mm

unic

atio

ns

carri

ers

busi

ness

Dra

stic

der

egul

atio

n fo

r the

car

riers

who

are

not

dom

inan

t in

the

mar

ket

Expa

nsio

n of

the

busi

ness

of N

TT E

ast a

nd W

est

Rel

axat

ion

of N

TT s

hare

s re

stric

tions

Smoo

th im

plem

enta

tion

of c

able

layi

ng, e

tc.

Intro

duct

ion

of th

e w

hole

sale

te

leco

mm

unic

atio

ns s

ervi

ces

syst

em

To p

rom

ote

the

IT re

volu

tion,

effo

rts s

houl

d be

mad

e to

enc

oura

ge fa

ir co

mpe

titio

n an

d to

max

imiz

e th

e pr

ofit

of u

sers

(Obj

ectiv

e)Es

tabl

ishm

ent o

f a s

yste

m to

set

tle p

rom

ptly

and

effe

ctiv

ely

disp

utes

invo

lvin

g in

terc

onne

ctio

ns a

nd o

ther

pro

blem

s be

twee

nte

leco

mm

unic

atio

ns c

arrie

rs(O

utlin

e)i)

Esta

blis

hmen

t of a

dis

pute

-set

tlem

ent c

omm

ittee

(an

orga

niza

tion

to b

e se

t up

in a

ccor

danc

e w

ith A

rticl

e 8)

, whi

ch is

orga

niza

tiona

lly in

depe

nden

t of t

he d

ivis

ion

in c

harg

e of

gra

ntin

gof

ficia

l app

rova

ls a

nd p

erm

issi

ons.

ii)In

trodu

ctio

n of

sim

pler

and

spe

edie

r dis

pute

-set

tlem

ent

proc

edur

es (m

edia

tion,

arb

itrat

ion)

iii)Es

tabl

ishm

ent o

f a s

yste

m in

whi

ch p

erso

nnel

cha

nges

of t

heco

mm

ittee

are

mad

e af

ter a

ppro

val b

y th

e D

iet,

and

anot

her

syst

em in

whi

ch n

ew m

embe

rs a

re re

com

men

ded

to th

e M

inis

ter

of P

ublic

Man

agem

ent,

Hom

e Af

fairs

, Pos

ts a

ndTe

leco

mm

unic

atio

ns.

(Obj

ectiv

e)Es

tabl

ishm

ent o

f a s

yste

m in

whi

ch a

ll ca

rrier

s be

nefit

ing

from

the

univ

ersa

l tel

epho

ny s

ervi

ce b

ear a

n ap

prop

riate

am

ount

of t

heco

sts

(ext

erna

l ass

ista

nce)

.(O

utlin

e)Es

tabl

ishm

ent o

f a s

yste

m in

whi

ch q

ualif

ied

tele

com

mun

icat

ions

carri

ers

rece

ive

subs

idie

s to

cov

er p

art o

f the

cos

t of p

rovi

ding

univ

ersa

l tel

epho

ny s

ervi

ce, t

hrou

gh a

des

igna

ted,

neu

tral a

nd fa

irco

rpor

atio

n.

(Obj

ectiv

e)Im

plem

enta

tion

of d

ram

atic

der

egul

atio

n of

exi

stin

g re

stric

tions

toth

e ex

tent

whe

re it

doe

s no

t dam

age

the

inte

rest

of u

sers

(Out

line)

To a

bolis

h al

l offi

cial

app

rova

l sys

tem

s in

volv

ing

gene

ral

cont

ract

ual c

ondi

tions

, int

erco

nnec

tion

agre

emen

ts, a

nd jo

int-u

seag

reem

ents

of n

on-d

omin

ant c

arrie

rs, a

nd to

intro

duce

ano

tific

atio

n sy

stem

in th

e sa

me

man

ner a

s th

e ta

riff s

yste

m.

(Obj

ectiv

e)To

enh

ance

free

man

agem

ent o

f bus

ines

s op

erat

ions

by

NTT

East

and

Wes

t, a

new

sys

tem

will

be e

stab

lishe

d in

whi

ch th

e tw

oco

mpa

nies

are

allo

wed

to e

nter

new

sec

tors

, suc

h as

Inte

rnet

-re

late

d se

rvic

es.

(Out

line)

To e

nabl

e N

TT E

ast a

nd W

est t

o la

unch

new

tele

com

mun

icat

ions

busi

ness

es b

usin

g its

faci

litie

s, te

chno

logy

or p

erso

nnel

afte

rob

tain

ing

the

appr

oval

of t

he M

inis

ter o

f Pub

lic M

anag

emen

t,H

ome

Affa

irs, P

osts

and

Tel

ecom

mun

icat

ions

. The

two

firm

s w

illbe

allo

wed

to d

o so

as

long

as

the

new

bus

ines

s do

es n

otob

stru

ct th

e sm

ooth

ope

ratio

n of

thei

r mai

nsta

y bu

sine

sses

, and

does

not

ham

per f

air c

ompe

titio

n in

the

tele

com

mun

icat

ions

mar

ket.

(Obj

ectiv

e)To

sup

port

the

expa

nsio

n of

NTT

-Gro

up b

usin

esse

s gl

obal

ly(O

utlin

e)i)

Rel

axat

ion

of re

stric

tions

on

fore

ign

inve

stm

ent i

n th

e ho

ldin

gco

mpa

ny (f

rom

less

than

20

perc

ent t

o on

e th

ird o

f the

tota

l cap

ital)

ii)Es

tabl

ishm

ent o

f exc

eptio

nal m

easu

res

for t

he is

suan

ce o

f new

shar

es b

y th

e ho

ldin

g co

mpa

nyiii)

Abol

ition

of a

sys

tem

requ

iring

the

NTT

Gro

up to

obt

ain

offic

ial

appr

oval

whe

n its

hol

ding

com

pany

sel

ls s

hare

s in

NTT

Com

mun

icat

ions

Cor

p.

(Obj

ectiv

e)To

impr

ove

the

flexi

bilit

y of

con

stru

ctin

g ne

twor

ks b

yte

leco

mm

unic

atio

ns c

arrie

rs(O

utlin

e)To

mak

e it

clea

r tha

t pro

cedu

res

for r

esol

ving

dis

pute

s ov

er th

eus

e of

ele

ctric

pol

es, c

ondu

its, e

tc.,

stip

ulat

ed in

the

Tele

com

mun

icat

ions

Bus

ines

s La

w, w

ill in

volv

e of

ficia

lly-o

wne

dla

nd. T

o es

tabl

ish

proc

edur

es fo

r med

iatio

n be

twee

n a

tele

com

mun

icat

ions

car

rier a

nd p

erso

n or

offi

ce in

cha

rge

ofm

anag

ing

road

s.

(Obj

ectiv

e)To

pro

mot

e ef

fect

ive

use

of fi

ber-o

ptic

net

wor

ks b

y lo

cal

gove

rnm

ents

, pub

lic u

tiliti

es, e

tc. a

nd to

enh

ance

the

flexi

bilit

y of

netw

ork

cons

truct

ion

by te

leco

mm

unic

atio

ns c

arrie

rs(O

utlin

e)i)

To in

trodu

ce a

sys

tem

whi

ch e

nabl

es p

rovi

sion

of f

lexi

ble

who

lesa

le te

leco

mm

unic

atio

ns s

ervi

ces

base

d on

indi

vidu

alco

ntra

cts

betw

een

tele

com

mun

icat

ions

car

riers

(wha

t is

calle

dth

e “c

arrie

r’s c

arrie

r con

tract

“).ii)

To a

bolis

h th

e tra

ditio

nally

pro

vide

d se

rvic

es n

ot in

clud

ed in

the

gene

ral c

ontra

ctua

l agr

eem

ent (

subj

ect t

o th

e of

ficia

l app

rova

lsy

stem

), an

d to

intro

duce

a n

otifi

catio

n sy

stem

in w

hich

all

who

lesa

le s

ervi

ces

will

be re

porte

d to

the

auth

oriti

es.

(Obj

ectiv

e)To

cre

ate

a ty

pica

l pat

tern

of t

elec

omm

unic

atio

ns c

arrie

rs th

atdo

min

ate

the

mar

ket (

both

in th

e re

gion

al fi

xed

tele

phon

y se

rvic

ese

ctor

and

the

mob

ile c

omm

unic

atio

ns s

ecto

r), a

nd to

ens

ure

prop

er o

pera

tion

of th

eir b

usin

ess.

(Out

line)

i)To

cre

ate

typi

cal p

atte

rns

of a

nti-c

ompe

titio

n ac

ts w

hich

sho

uld

be fo

rbid

den,

and

to fo

rmul

ate

mea

sure

s to

pro

mpt

ly e

limin

ate

such

act

s.ii)

Mea

sure

s to

enh

ance

tran

spar

ency

and

fairn

ess

ofin

terc

onne

ctio

ns (M

easu

res

to m

ake

it co

mpu

lsor

y fo

r car

riers

tofo

rmul

ate

and

publ

ish

thei

r gen

eral

con

tract

ual a

gree

men

ts).

Oth

ers

Obj

ectiv

e of

the

revi

sion

Esta

blis

hmen

t of r

egul

atio

ns c

once

rnin

g re

view

s

(Out

line)

“Pro

mot

ion

of fa

ir co

mpe

titio

n” s

houl

d be

cle

arly

stip

ulat

ed in

the

purp

ose

of th

e Te

leco

mm

unic

atio

ns B

usin

ess

Law

(Out

line)

Esta

blis

hmen

t of r

egul

atio

ns c

once

rnin

g a

com

preh

ensi

ve re

view

of s

yste

ms

invo

lvin

g th

e te

leco

mm

unic

atio

ns b

usin

ess,

in th

esu

pple

men

tary

pro

visi

ons

of th

e re

vise

d la

w.

Outline of partial revisions of the Telecommunications Law and related laws

4

3. Establishment of interconnection rules

○November 1997: A law to revise part of the Telecommunications Business Law wasenforced《Formulation of basic rules on interconnection》

○September 2000: Establishment of rules concerning unbundling of subscriber lines○October 2000: Establishment of rules concerning collocation○December 2000: The first recommendation from the Telecommunications Council on

the “review of interconnection rules.”○April 2001: Establishment of rules concerning unbundling of fiber optic

networks.○July 2001: The second recommendation from the Telecommunications Council

concerning “interconnection rules in the age of informationtechnology.”

(1) Unbundling of subscriber lines and fiber-optic networksThis means that telecommunications carriers divide network components and lease themto Internet connection providers

Typical examples

- Subscriber lines (not overlapped by telephone lines) 2,062 yen- Subscriber lines (overlapped by telephone lines) 187 yen- Subscriber fiber-optic lines 5,231 yen- Relay carriers’ fiber-optic networks 4.29 yen / meter + 157 yen

(2) CollocationThis means that Internet connection providers install the equipment necessary forconnection, in the facilities of NTT East, NTT West, etc.

Procedures for collocation(within one month) (within six months) (within three months)

Applicationfor prior

examination

Results ofprior

examinationApplication Start of

construction Completion

(within one month)

(3) Efforts made in response to the recommendation on “interconnection rules in theage of information technology”・Ministry ordinance

Further unbundling of fiber-optic networks and non-discriminatory treatment of domesticand foreign carriers in taking procedures for the use of fiber-optic networks (inquiry to asubcommittee on Sept. 21, 2001).・Future efforts

Resale of public networks, further unbundling of subscriber lines, etc.

5

4. Outline of NTT Reorganization Scheme

References

1. special corporation, private company

2. The holding company holds all shares of NTT East Corp. and NTT West Corp.

Holding Company(Nippon Telegraph and

Telephone Corp.)

- Using its right as a shareholder to ensure thatregional communications services are providedby the regional communications companies ona stable basis

- Promoting fundamental research anddevelopment on telecommunications

NTT West Corp.(Nippon Telegraph andTelephone West Corp.)

NTT East Corp.(Nippon Telegraph andTelephone East Corp.)

NTTCommunications

Corp.

- Providing regional communications service inWestern Japan (Tokai, Hokuriku, Kansai, Chugoku,Shikoku, Kyushu and Okinawa)

- Being obliged to provide universal service oftelephony in Western Japan

- Providing regional communicationsservice in Eastern Japan (Hokkaido,Tohoku, Kanto, Tokyo and Shin'etsu)

- Being obliged to provide universalservice of telephony in Eastern Japan

6

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

Apr.

120

01Ap

r. 1

2002

Jun.

120

02Se

pt. 1

2002

27

1337

4562

6870

8086

111

126

138

153

178

249

342

384

387

392

11

11

11

11

11

11

11

13

33

33

11

11

11

11

11

11

11

11

--

--

--

--

--

--

19

99

99

99

99

99

-5

1135

4360

6668

7775

100

115

127

142

167

236

330

372

375

380

-3

35

55

55

55

55

56

1221

3235

3433

--

34

47

77

810

1116

2847

7715

927

431

932

332

9

-2

22

22

23

32

24

45

65

55

55

--

223

3146

5253

6158

8290

9084

7251

1913

1313

Cel

lula

r Pho

nes

--

-2

48

89

1515

1721

2121

2121

85

55

Rad

io P

agin

g-

-2

2026

3336

3636

3131

3131

3131

193

22

2

PHS

--

--

--

--

--

2328

2828

189

52

22

Con

veni

ence

Rad

ioPh

one

(CR

P)-

--

--

24

47

77

66

--

--

--

-

Ship

Tel

epho

ne-

--

11

23

32

21

--

--

--

--

-

Airp

ort R

adio

Tel

epho

ne-

--

--

--

--

22

22

22

23

33

3

Dat

a co

mm

unic

atio

ns-

--

--

11

11

11

22

2-

--

--

-

Rad

io a

cces

s sy

stem

--

--

--

--

--

--

--

--

-1

11

--

11

1-

--

--

--

--

--

--

--

8520

935

653

069

384

194

31,

036

1,17

91,

589

2,10

73,

134

4,58

85,

871

6,60

27,

651

9,00

610

,137

10,1

9210

,376

09

1018

2528

3136

3639

4450

7895

8810

111

311

211

211

3

8520

034

651

266

881

391

21,

000

1,14

31,

550

2,06

33,

084

4,51

05,

776

6,51

47,

550

8,89

310

,025

10,0

8010

,263

8721

636

956

773

790

31,

011

1,10

61,

259

1,67

52,

218

3,26

04,

726

6,02

46,

780

7,90

09,

348

10,5

2110

,576

10,7

68

NTT

DoC

oMo,

Inc.

and

its

grou

p co

mpa

nies

New

Typ

e I

Tele

com

munic

atio

ns

Car

riers

Reg

iona

l Car

riers

Typ

e I T

ele

com

munic

atio

ns

Car

riers

NTT

Spec

ial T

ype

IITe

leco

mm

unic

atio

ns C

arrie

rs

Gen

eral

Typ

e II

Tele

com

mun

icat

ions

Car

riers

Tota

lKDD Lo

ng-

dist

ance

/Inte

rnat

iona

lC

arrie

rs

Sate

llite

Car

riers

Mob

ile C

omm

unic

atio

ns

Oth

ers

Typ

e II Tel

ecom

munic

atio

ns C

arriers

Not

es:

1.Ty

pe I

carri

ers

offe

r ser

vice

s by

est

ablis

hing

thei

r ow

n te

leco

mm

unic

atio

ns c

ircui

t fac

ilitie

s.2.

Type

II c

arrie

rs o

ffer s

ervi

ces

by le

asin

g te

leco

mm

unic

atio

ns c

ircui

t fac

ilitie

s.3.

NTT

was

reor

gani

zed

into

two

regi

onal

Typ

e I c

arrie

rs (N

TT E

ast C

orp.

and

NTT

Wes

t Cor

p.) a

nd o

ne lo

ng-d

ista

nce/

inte

rnat

iona

l car

rier (

NTT

Com

mun

icat

ions

Cor

p.) u

nder

one

hol

ding

com

pany

(NTT

) on

July

1, 1

999.

4.O

n O

ctob

er 1

, 200

0, D

DI C

orp.

, KD

D C

orp.

and

IDO

Cor

p. w

ere

mer

ged

into

DD

I Cor

p. (K

DD

I)

II. Current situation surrounding thetelecommunications business

1. Changes in the total number of telecommunications carriers

7

2. Current Status of Main Foreign Investment in TelecommunicationsCarriers

(1) Type I telecommunications carriers (As of Sept. 1, 2002)

Carrier Foreigncapital ratio Major foreign investors

Cable & Wireless IDC Inc. 98.02% Cable & Wireless plc (C&W), etc.J-COM Kanto Co., Ltd. 59.00% Liberty Japan, Inc., Liberty Jupiter, Inc., Microsoft Holding Inc.J-COM Kansai Co., Ltd. 58.11% Liberty Japan, Inc., Liberty Jupiter, Inc., Microsoft Holding Inc.KVH Telecom Co., Ltd. 100.00% KVH Telecom Holding SCDRLPCCA Private Limited 100.00% Corporate Access Group LTD.PanAmSat InternationalSystems, Inc.

100.00% Hughes Electronics etc.

MCI WorldCom Japan, Ltd. 100.00% MCI WorldCom, Inc.Metromedia Fiber NetworkJapan K.K.

100.00% Metromedia Fiber Network Service, Inc.

Global One CommunicationsNetwork, Inc.

100.00% Global One Communications World Holding

Primus Japan K.K. 100.00% Primus Telecommunications Group, Inc.K.K. Telegloble Japan 100.00% Teleglobe Communications Corp.RSL COM Service Japan K.K. 100.00% RSL COM Asia Pacific Ltd.Singapore Telecom Japan,Co., Ltd.

100.00% Singapore Telecommunications Ltd.

Reach Networks Japan K.K. 100.00% Reach Networks Hong Kong LimitedReach Networks K.K. 100.00% Level 3 International Inc.EGN B.V. 100.00% Equant Finance B.V.T Systems Japan K.K. 100.00% Deutsche Telecom AGSony Corp. 44.56% Moxley & Co., State Street Bank and Trust Company, etc.FLAG Telecom Japan Limited 100.00% FLAG Telecom Ireland LimitedNew Century Global Net Corp. 100.00% NCG Holdings L.P.Genuity Japan K.K. 100.00% Genuity Inc.Asia Global Crossing JapanCorporation

100.00% Asia Global Crossing Limited

World Exchange 100.00% World Exchange CommunicationsCircle Asia Corporation 54.39% Grand River Group Limited, etc.J-COM Kitakyushu Co., Ltd. 44.78% Liberty Japan, Inc., Liberty Jupiter, Inc., Microsoft Holding Inc.J-COM Shonan Co., Ltd. 41.00% Liberty Japan, Inc., Liberty Jupiter, Inc., Microsoft Holding Inc.J-COM Sapporo Co., Ltd. 46.32% Liberty Japan, Inc., Liberty Jupiter, Inc., Microsoft Holding Inc.Kisarazu Cable TV 45.78% Liberty Japan, Inc., Liberty Jupiter, Inc., Microsoft Holding Inc.J-COM Gunma Co., Ltd. 59.00% Liberty Japan, Inc., Liberty Jupiter, Inc., Microsoft Holding Inc.GTE Far East (Services) Ltd. 100.00% Verizon Hawaii InternationalAT&T CommunicationsService Japan Ltd.

100.00% AT&T TransOceanic Communications L.L.C.

Williams Communications, Inc. 100.00% Williams Communications ParticipationsSprint International Japan Co.,Ltd.

100.00% Sprint International Holding Inc.

Tyco Networks Japan Co., Ltd. 100.00% TCN Holding LuxemburgC2C Japan Co., Ltd. 100.00% C2C Pte LimitedQwest CommunicationsJapan Co., Ltd.

100.00% Qwest Communications International

Japan Telecom Co., Ltd. 45.00% Vodafone International Holdings BVPower Band Co., Ltd. 64.20% J.H. WHITNEY IV LP, World View Technology Partners III LPJ-phone Co., Ltd. 69.72% Boderphone International Holdings B.V., etc.ORBCOMM Japan Limited 37.91% ORBCOMM Asia LimitedNote: This list includes companies with foreign capital ratio of more than a third.

8

(2) Special Type II telecommunications carriers (As of Sept. 1, 2002)

CarrierForeign

capital ratioMajor foreign investors

IBM Japan, Ltd. 100.00% IBM WTC (U.S.A)Information Service International-Dentsu, Ltd. 34.00% GE Information Service (U.S.A)Xpedite 100.00% Xpedite Systems Inc. (U.S.A)Compaq Computer K.K. 100.00% Digital Equipment Corp. (U.S.A)Cable & Wireless Japan Ltd. 85.80% Cable & Wireless plc. (U.K.)Concert Global Network Japan 100.00% Concert Global Networks (U.S.A) Inc.Deutsche Telecom K.K. 100.00% Deutsche Telekom AG (Germany)Reach Holdings Singapore Japan 100.00% Reach Ltd. (Hong Kong)Saiki-Tech Communications Japan Co., Ltd. 100.00% SAIKI TECH INVESTMENT HOUSE (ISRAEL) LTD.TMI Telemedia International Hong Kong Ltd. 100.00% TMI Telemedia International Hong Kong Ltd.(Hong Kong)IXnet Japan Co., Ltd. 100.00% Saturn Global Network Holding Ltd. (U.K.)UUNet Japan Co., Ltd. 100.00% UUNet Technologies Inc. (U.S.A)MCI International (Japan) Co., Ltd. 100.00% MCI International, Inc. (U.S.A)AT & T Communications Service Japan Ltd. 100.00% AT & T Corp. (U.S.A)MCI WorldCom Communications Japan Ltd. 100.00% MCI WorldCom, Inc. (U.S.A)Far East Data Ltd. 90.00% Far East Enterprises, Ltd. (U.S.A)DoCoMo AOL, Inc. 40.30% America Online, Inc. (U.S.A)PSINet Japan Inc. 100.00% PSINet Inc. (U.S.A)Coyote Network Systems, Inc. 100.00% Coyote Network, Systems, Inc. (U.S.A)Magde Web Japan Co., Ltd. 100.00% Tullett & Tokyo Forex Europe B.V.(the Netherlands)Equant Co., Ltd. 100.00% EGN B.V. (the Netherlands)Primus Telecommunications K.K. 100.00% Primus Telecommunications International, Inc. (U.S.A)City Telecom (Japan) Co., Ltd. 100.00% City Telecom (H.K.) Ltd. (Hong Kong)Telegroup Japan, Inc. 100.00% Telegroup, Inc. (U.S.A)RSL COM Japan, K.K. 100.00% RSL Communications Ltd. (U.S.A)Teleglobe Services Japan, Inc. 100.00% Teleglobe International Corp. (U.S.A)Pacific Gateway Exchange Japan Inc. 100.00% Pacific Gateway Exchange Inc. (U.S.A)GINGA Communications International, Inc. 100.00% Unitrendix Corp. (U.S.A)Singapore Telecom Japan Co., Ltd. 100.00% Singapore Telecommunications Ltd. (Singapre)Nippon WorldxChange Ltd. 100.00% WorldxChange Communications (U.S.A)Genuity International Inc. (Japan) 100.00% Genuity International Inc. (U.S.A)AIC Telecom (Japan) Ltd. 100.00% AIC (Asia Pacific) Ltd. (Hong Kong)i-Tel Corp. 100.00% Impact Telecommunications, Inc. (U.S.A)AT & T Global Network Services Japan LLC 85.00% AT & T Corp. (U.S.A)Verizon Global Solutions Holdings Limited 100.00% Verizon International Holdings Limited (Bermuda (U.K. territory))Cignal Telecommunications Japan K.K. 100.00% Cignal Global Communications Holding B.V. (the Netherlands)Korea Telecom Japan K.K. 100.00% Korea Telecom (South Korea)REUTERS Japan Ltd. 100.00% Reuters Group PLC (U.K.)Telecom New Zealand Japan K.K. 100.00% Telecom New Zealand International Ltd. (New Zealand)Wherever Japan K.K. 100.00% Wherever Technology Corp. (Taiwan)At Home Japan Ltd. 57.2% At Home Corp. (U.S.A)KPN Japan, Ltd. 100.00% Royal KPN N.V. (the Netherlands)Nittan Telecom (Japan) Ltd. 100.00% Nittan Telecom Ltd. (Hong Kong)Global Crossing Japan Corp. 100.00% Asia Global Crossing (U.S.A)M3Com (Japan) K.K. 100.00% Millenium 3 Communications, Inc. (U.S.A)AboveNet Japan KK 40.0% AboveNet Communications, Inc. (U.S.A)Savvis Japan Ltd. 100.00% Savvis Communications, Inc. (U.S.A)Bazillion Inc. 90.0% Bazillion Inc. (U.S.A)WAM!NET Holding Japan KK 100.00% WAMNET Inc. (U.S.A)Hewlett-Packard Japan, Ltd. 100.00% Hewlett-Packard Company (U.S.A)At Network Japan KK 100.00% Network Inc. (U.S.A)Streamscape 99.00% Streamscape Network Inc. (U.S.A)Enron Broadband Services Network 100.00% Enron Corporation (U.S.A)QoS Network Services Japan 100.00% QoS Network Services Ltd. (Ireland)Sprint International Holding, Inc. 100.00% Sprint International Holding, Inc. (U.S.A)Angstrom Network Japan 100.00% Angstrom Networks Ltd. (U.S.A)iBasis Japan Co., Ltd. 100.00% iBasis Global, Inc. (U.S.A)XA Aliance Co., Ltd. 100.00% OMM Holdings Limited (Cayman Islands (U. K. territory))Infoserve Technology Co., Ltd 100.00% Infoserve Tech Corp. (U.S.A)BELGACOM Japan Co., Ltd 100.00% BELGACOM S.A. (Bergen)PCCW Communications Japan Co., Ltd 100.00% PCCW Holdings Limited (Cayman Islands (U. K. territory))SK Cyberpass Co., Ltd. 100.00% SK Telink (Korea)Chinalink Networks Co., Ltd. 99.8% Chinalink Networks LimitedJapan run xun Communications Co., Ltd. 100.00% Chinamotion (Hong Kong)

9

3. Changes in market size / investment in facilities and equipment

(1) Changes in market size of type-1 carriers

① The market size (combined sales) of type 1 carriers in fiscal 2001 was 17,245.3 billionyen (up 9.8 percent from the previous year)

② Supported by the growth of the mobile communications business, the combined salessurged from the previous year.

100,289121,370

133,048 138,615155,783

169,826 172,453 171,236

0

50,000

100,000

150,000

200,000

95 96 97 98 99 00 01 02(Projection)

(100 million yen)

Fiscal year

(2) Equipment investment by type-1 carriers (Plans for fiscal 2002)

① The total amount of equipment investment projected for fiscal 2002 is 2,882.3 billion yen(down 3.8 percent from the previous year’s total)

② This represents the second-highest amount in equipment investment projected by allindustries (37,671.9 billion yen).

③ Equipment investment by type-1 carriers is the second largest, next to that of theelectrical power and gas industries.

3.2(▲12.5)

Mobilecommunications

business:1.5 (▲10.3)

2.9(▲15.4)

2.9(▲20.7) 2.5

(▲24.0)

1.5(▲8.2)

1.5(▲1.7)

1.4(▲20.4)

0.5(▲26.1) 0.3

(▲17.2)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Electrical power, Gas

Type I telecommunications business

Services

Electric machinery

Chemicals

Automobiles

Real estate

Iron and steel

Construction

(Unit: 1 trillion yen)※ The combined amount of equipment investment by all industries:

37,671.9 billion yen (down 9.1 percent)

10

4. Shares of NTT and NCC

(1) Sales of NTT-Group companies in each type of service (FY2001)

Note:1. “NTT”

Comm2. The fig

servic3. The fig

comm

Voice communications(5,431.3 billion yen)

Mobile communications(6,033.5 billion yen)

Data transmission(467.4 billion yen)

Leased line(1,145.9 billion yen)

NTT(83.8%)

NTT Docomo(60.5%)

N(5

N(7

NCC (16.2%)

NCC (39.5%)NCC (46.5%)

NCC (26.3%)

TT3.5%)

indicates the combined sales of NTT East, NTTunications.ures in the charts of voice communications, lea

es are those of the fixed telephone service proviure for mobile communication indicates the com

unications service providers.

TT3.7%)

West, and NTT

sed line, and data transmissionders.bined sales of all mobile

11

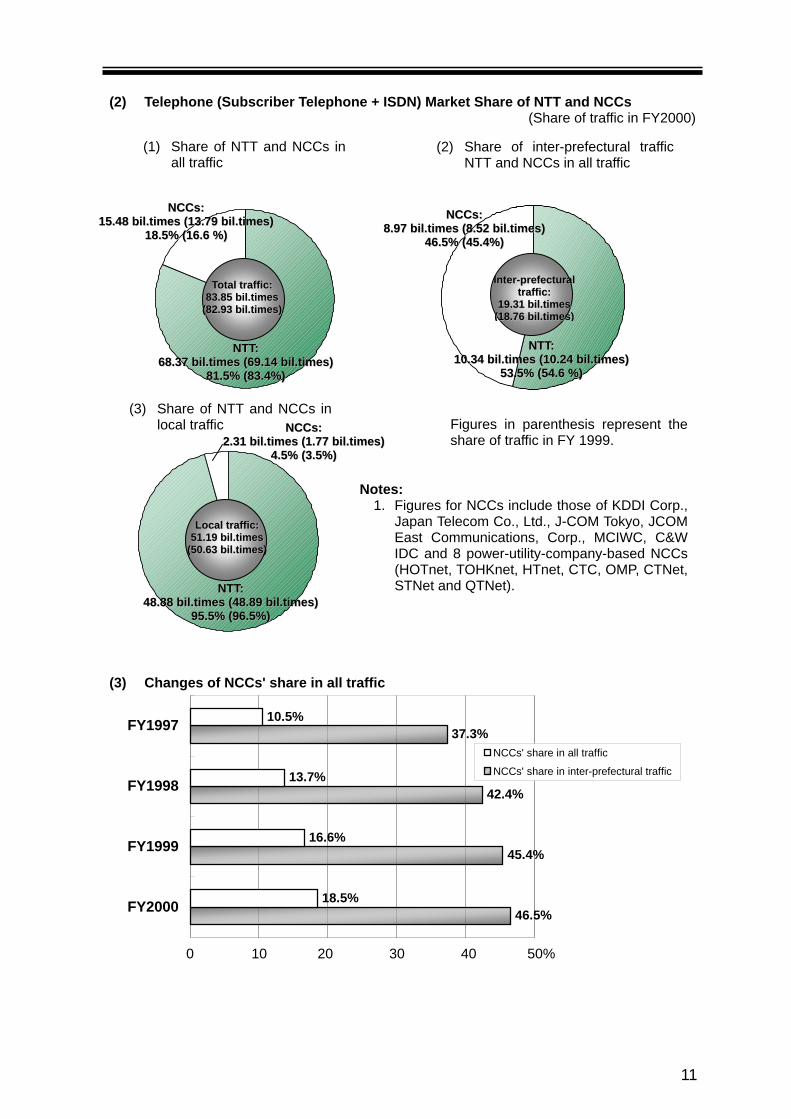

(2) Telephone (Subscriber Telephone + ISDN) Market Share of NTT and NCCs(Share of traffic in FY2000)

(3) Changes of NCCs' share in all traffic

46.5%

45.4%

42.4%

37.3%

18.5%

16.6%

13.7%

10.5%

FY2000

FY1999

FY1998

FY1997

NCCs' share in all traffic

NCCs' share in inter-prefectural traffic

NNCCCCss::1155..4488 bbiill..ttiimmeess ((1133..7799 bbiill..ttiimmeess))

1188..55%% ((1166..66 %%))

NNTTTT::6688..3377 bbiill..ttiimmeess ((6699..1144 bbiill..ttiimmeess))

8811..55%% ((8833..44%%))

TToottaall ttrraaffffiicc::8833..8855 bbiill..ttiimmeess

((8822..9933 bbiill..ttiimmeess))

(2) Share of inter-prefectural trafficNTT and NCCs in all traffic

NNCCCCss::88..9977 bbiill..ttiimmeess ((88..5522 bbiill..ttiimmeess))

4466..55%% ((4455..44%%))

NNTTTT::1100..3344 bbiill..ttiimmeess ((1100..2244 bbiill..ttiimmeess))

5533..55%% ((5544..66 %%))

IInntteerr--pprreeffeeccttuurraallttrraaffffiicc::

1199..3311 bbiill..ttiimmeess((1188..7766 bbiill..ttiimmeess))

(3) Share of NTT and NCCs inlocal traffic NNCCCCss::

22..3311 bbiill..ttiimmeess ((11..7777 bbiill..ttiimmeess))44..55%% ((33..55%%))

NNTTTT::4488..8888 bbiill..ttiimmeess ((4488..8899 bbiill..ttiimmeess))

9955..55%% ((9966..55%%))

LLooccaall ttrraaffffiicc::5511..1199 bbiill..ttiimmeess

((5500..6633 bbiill..ttiimmeess))

Notes:1. Figures for NCCs include those of KDDI Corp.,

Japan Telecom Co., Ltd., J-COM Tokyo, JCOMEast Communications, Corp., MCIWC, C&WIDC and 8 power-utility-company-based NCCs(HOTnet, TOHKnet, HTnet, CTC, OMP, CTNet,STNet and QTNet).

(1) Share of NTT and NCCs inall traffic

0 10 20 30 40 50%

Figures in parenthesis represent theshare of traffic in FY 1999.

12

5. Current Status of Rate Reductions

(1) Long-distance call (Tokyo-Osaka)

3 minutes, daytime, weekdays

050

100150200250300350400450

(2) Local call

3 minutes, daytime, weekdays

0

5

10

15

¥¥¥444000000

¥¥¥222000¥¥¥444555¥¥¥555444¥¥¥888000July 21, 1983

NTTApril 1, 2001~

Fusion,Dec. 12, 2001~

HEISEI DEN DENJan., 2002~ MEDiA

Dec. 1, 2000~C&WIDC

Mar. 1, 2001~TTNet

Mar. 1, 2001~NTT-C, JT

KDDI

▲▲▲▲95%

¥¥¥999~~~~~~~~~~~~

¥¥¥888...777

¥¥¥888...555~~~~~~~~~~~~

¥¥¥888...444

¥¥¥999¥¥¥111000

TTNet,QTNet ¥9

NTT East andWest, KDDI, JT,NTT-C ¥8.5TTNet, QTNet¥8.4

NTT East ¥9TTNet ¥8.7

▲▲▲▲25%~~~~▲▲▲▲15%

Nov. 17, 1976~NTT

Jan.7, 1998~ TTNetApril 1, 1999~ QTNet

Jan. 10, 2001~ May 1, 2001~

¥¥¥888...222~~~~~~~~~~~~

¥¥¥777...555

MEDiA ¥8.2HEISEI DEN DEN

¥7.5

MEDiA Jan. 30, 2002~HEISEI DEN DENFeb. 1, 2002~

(3) International call (Japan-U.S.A)

3 minutes, daytime, weekdays

0

500

1000

1500

2000

(4) Cellular phone (800MHz digital system)

Note: On March 25, 1993, the "800MHz digital cellular phone service" started.NTT DoCoMo reduced the basic charge to 4,500 yen (including a free call allowanceworth 200) in June 2000.

Call rate (cellular phone → fixed phone, intra-prefectural)

¥¥¥111,,,555333000KDD: ¥450 (Nov. 23, 1996)JT: ¥440 (Dec. 20, 1996)C&W: IDC ¥440 (Dec. 20, 1996)

April 1, 1985~KDDI

MCIWCJ: ¥150 (Dec. 1, 1998)JT ¥180: (Oct. 1, 1999)C&W IDC: ¥180 (Oct. 5, 1999)KDDI: ¥180 (Nov. 1, 1999)TTNet: ¥132 (Nov. 1, 1999)DTJ: ¥75 (Dec.10, 2000)NTT-COM: ¥160 (April 3, 2000)Fusion: ¥45 (Sept. 1, 2001)MEDiA: ¥45 (Jan. 30, 2002)HEISEI DEN DEN: ¥45(Feb. 1, 2002)

0

5000

10000

15000

20000 4

3

2

1

¥¥¥111777,,,000000000▲▲▲▲75%

NTT DoCoMo,Mar. 25, 1993~

¥¥¥444,,,333000000

¥¥¥222666000▲▲▲▲73%

¥¥¥777000

J-Phone,June 1, 1999~

NTT DoCoMo and nineother companies,

Dec. 1, 2000~

NTT DoCoMo,Mar. 25, 1993~

Basic fee

▲▲▲▲90~~~~96%

00

00

00

00

13

14

47.0

8

27.0

6

16.9

4

11.5

5

3.3

%

11.0

%

19.1

%

11.7

%

50.4

%

68.2

%

80.0

%

34.0

%

6.4

%

88.6

%

0

1,0

00

2,0

00

3,0

00

4,0

00

5,0

00

6,0

00

7,0

00

8,0

00

9,0

00

10,0

00

End

of C

Y199

5En

d of

CY1

996

End

of C

Y199

7En

d of

CY1

998

End

of C

Y199

9En

d of

CY2

000

End

of 2

005

0.0

%

10.0

%

20.0

%

30.0

%

40.0

%

50.0

%

60.0

%

70.0

%

80.0

%

90.0

%

100.0

%

Num

ber o

f Int

erne

t use

rs(J

apan

)Pe

netra

tion

rate

inho

useh

olds

Pene

tratio

n ra

te in

ente

rpris

es

(Uni

t: 1

milli

on)

(%

)

872

(Est

imat

e )

End

of C

Y200

1

55.9

3 60.5

%

97.6

%95.8

%

※Bu

sine

sses

are

thos

e ha

ving

mor

e th

an 3

00 w

orke

rs o

n th

eir p

ayro

lls, a

nd a

re lo

cate

d in

Jap

an(e

xclu

ding

bus

ines

ses

in th

e ag

ricul

ture

, for

estry

, fis

herie

s an

d m

inin

g in

dust

ries)

.So

urce

: WH

ITEP

APER

Info

rmat

ion

and

Com

mun

icat

ions

in J

apan

200

1, e

tc.

III. Internet

1. Total Internet user population and Internet diffusion rate

(1) Environment surrounding telecommunications business

14

15

0

500,

000

1,00

0,00

0

1,50

0,00

0

2,00

0,00

0

2,50

0,00

0

3,00

0,00

0

3,50

0,00

0

4,00

0,00

0

4,50

0,00

0

99-3

99-6

99-9

99-1

200

-300

-600

-900

-12

01-3

01-6

01-9

01-1

202

-302

-602

-9

133.

4 th

ousa

nd13

0.3

thou

sand

32.9

thou

sand

115.

1 th

ousa

nd

9.2

thou

sand

62.5

thou

sand

3.2

thou

sand6.6

thou

sand

15.4

thou

sand

21.6

thou

sand

46.3

thou

sand

78.4

thou

sand

96.7

thou

sand

139.

9 th

ousa

nd

145.

6 th

ousa

nd

171.

0 th

ousa

nd

153.

3 th

ousa

nd 162.

6 th

ousa

nd

156.

7 th

ousa

nd

1,52

4,56

4

1,78

7,59

8

1,20

4,56

492

1,86

7

650,

796

510,

339

400,

760

291,

333

178,

737

70,6

55

112,

182

9,72

32,

537

1,23

521

119

2,37

8,79

5

3,02

8,55

6

2,69

9,28

5

2,07

6,30

2

3,91

5,74

0

3,61

0,19

9

3,30

0,92

6

0

10,0

00

20,0

00

30,0

00

40,0

00

50,0

00

60,0

00

70,0

00

80,0

00

90,0

00

00-9

00-1

201

-301

-601

-901

-12

02-3

02-6

02-9

abt.

3,10

0ab

t. 2,

500

abt.

450

abt.

900

abt.

6,50

0ab

t. 8,

000

abt.

15,0

00

abt.

5,00

0

abt.

10,5

00

abt.

21,0

00

abt.

18,5

0012

,33718

,188

abt.

9,30

0ab

t. 4,

700

50,9

30

abt.

200

abt.

500

abt.

1 ,40

0

26,4

0034,9

30

84,9

03

68,6

00

Cab

le In

tern

et・Su

bscr

iber

s: a

bt. 1

,710

,000

・Bu

sine

sses

: 270

(A

s of

the

end

of J

uly

2002

)

Cab

le In

tern

etC

able

Inte

rnet

・Su

bscr

iber

s: a

bt. 1

,710

,000

・Bu

sine

sses

: 270

(A

s of

the

end

of J

uly

2002

)

DSL

・Su

bscr

iber

s: 3

,915

,740

(As

of t

he e

nd o

f Aug

. 200

2)・Bu

sine

sses

: 47

(A

s of

the

end

of A

ug. 2

002)

DSL

DSL

・Su

bscr

iber

s: 3

,915

,740

(As

of t

he e

nd o

f Aug

. 200

2)・Bu

sine

sses

: 47

(A

s of

the

end

of A

ug. 2

002)

Fibe

r-op

tic n

etw

orks

(for G

ener

al u

sers

)・Su

bscr

iber

s: 8

4,90

3・Bu

sine

sses

: 10

(As

of t

he e

nd o

f Jul

y 20

02)

Fibe

r-op

tic n

etw

orks

Fibe

r-op

tic n

etw

orks

(for G

ener

al u

sers

)・Su

bscr

iber

s: 8

4,90

3・Bu

sine

sses

: 10

(As

of t

he e

nd o

f Jul

y 20

02)

Wire

less

・Su

bscr

iber

s: a

bt. 2

1,00

0・Bu

sine

sses

: 25

(As

of t

he e

nd o

f Jul

y 20

02)

Wire

less

Wire

less

・Su

bscr

iber

s: a

bt. 2

1,00

0・Bu

sine

sses

: 25

(As

of t

he e

nd o

f Jul

y 20

02)

(2) Changes in the total number of subscribers to high-speed and ultra-high-speedInternet services

Current Status of Broadband Penetration - Number of Subscribers

15

16

2002

0606

2,90

03,

100

2,45

32,

932

2,05

62,

700

4,35

3

5,90

37,

085

2,01

2 FT

2,51

9 D

T

1,95

0 N

TT-C

1,95

0 N

TT-C

0

1,0

00

2,0

00

3,0

00

4,0

00

5,0

00

6,0

00

7,0

00

8,0

00

9,0

00

Com

mun

icat

ions

ser

vice

fees

Inte

rnet

acc

ess

rate

Tota

l5,

050

yen

Tota

l4,

850

yen

Tota

l2,

453

yen

Tota

l5,

903

yen

Tota

l4,

353

yen

Tota

l4,

944

yen

Tota

l7,

085

yen

Tota

l4,

575

yen

Tota

l2,

700

yen

(ye

n)

Yaho

oVe

rizon

Com

mun

icat

ions

(New

Yor

k)B

T(L

ondo

n)N

TT E

ast

FT(P

aris

)D

T(G

erm

any)

KT

(Kor

ea)

1.5

Mbps

/512kb

ps

512kb

ps

/256kb

ps

500kb

ps

/128kb

ps

8M

bps

/900kb

ps

768kb

ps

/128kb

ps

1.5

Mbps

/128kb

ps

768kb

ps

/128kb

ps

1.5

Mbps

/256kb

ps

8M

bps

/1M

bps

Not

e: 1.Th

e ra

tes

indi

cate

d ar

e th

ose

of J

uly

2002

.2.

Exch

ange

rate

s of

Jul

y 10

, 200

2 w

ere

used

to c

onve

rt ra

tes

in e

ach

coun

try (U

S$1

= ¥1

18.1

8; £

1 = ¥1

82.6

5; 1

eur

o = ¥1

16.9

0; 1

won

= 0

.09

yen)

3.Ta

xes

wer

e no

t inc

lude

d fo

r all

rate

s.

2.

Cur

rent

Con

ditio

ns in

Ele

ctro

nic

Com

mun

icat

ions

(Int

erna

tiona

l com

paris

on o

f ful

l-tim

e In

tern

et c

onne

ctio

n fe

es (A

DSL

))

16

17

3. Deployment of fiber-optic networks

(1) Current status in terms of cable length used(As of the end of FY2001; unit: 1,000km)

Item Cable length Fiber-optic cable

Backbone networks 283 257

Access networks 1,400 291

Total 1,683 548

(2) Changes in ratio of fiber-optic cables to all cables (cable length)(Unit: %)

End of FiscalYear FY91 FY92 FY93 FY94 FY95 FY96 FY97 FY98 FY99 FY00 FY01

Backbonenetworks 36.4 42.1 48.0 55.4 60.3 65.8 70.9 78.1 86.0 89.4 90.6

Accessnetworks 2.3 2.9 3.8 4.7 6.4 9.7 13.2 15.2 17.7 18.9 20.7

Total 8.6 10.1 12.4 15.1 17.3 21.4 25.1 27.7 32.6 31.4 32.5

Note: Since the end of FY2000, the total length of the International cables has been deductedfrom the total length of the relay carriers’ cables.

(3) Trends in actual investment in fiber-optic networks(Unit: ¥1 billion)

End of FiscalYear FY94 FY95 FY96 FY97 FY98 FY99 FY00 FY01

Backbonenetworks 3,414 2,972 3,387 3,446 2,247 2,859 2,037 1,957

Accessnetworks 1,299 2,447 3,315 3,033 2,415 2,774 2,052 2,153

Total 4,713 5,419 6,702 6,479 4,662 5,633 4,089 4,110

18

(4) Target of fiber optic Infrastructure

100%

59%

Make efforts to complete nationwide fiber-opticaccess networks by FY2005"(Policy Measures for Economic Rebirth: November1999)

Coverage (target)

Establishment of the IT StrategyHeadquarters

Enforcement of the Basic Law onInformation Technology (IT Basic Law)

Provisional Measures Lawfor Telecommunications

Infrastructure

Special Financing System for theDevelopment of the Optical Subscriber

Loop System

Set up Advanced Information andTelecommunications Society

Promotion Headquarters

Reo

rgan

izat

ion

Actual result Initial plan(Telecommunications Council

Report of May 1994)

Efforts made tocomplete the network

as early as 2005

FY 1994 1995 1996 1997 1998 1999 2000 2001

Coverage abt. 10% abt. 13% abt. 16% abt. 19% abt. 27% abt. 36% abt. 43% abt. 59%

nationwaide

1994 201020052001

2000

From 2001:

From 1991:

August 1994:

From 1995:

January 6, 2001:

19

4. Major support systems for fiber-optic networks and broadband accessnetworks

Financing Systems

No/low interest financing by theDevelopment Bank of Japan

No/low interest financing by the Development Bank ofJapan for perators introducing broadband accessnetworks such as fiber optic/DSL, etc.(No interest for public corporation, low interest forprivate corporation)

No-interest loan(NTT-C / the Third Sector)

Low-interest loan(NTT-C' / Private Sector)

Ultra-low interest financing by theDevelopment Bank of Japan andTelecommunication Advancement

Organization (TAO)

TAO makes interest-based assistance for privatecorporation with low interest financing from theDevelopment Bank of Japan.

Tax benefit incentives

Special redemptionfor corporate tax

Decrease of the taxstandard for fixed

assets tax

Operators introducing broadband access networks such as fiberpotic/DSL, etc. can apply for a special 6-18% redemption for corporatetax.

Operators introducing broadband access networks such as fiberoptic/DSL, etc. can decrease the tax standard for fixed assets tax by 20-25%.

Guarantee ofliabilities

TAO guarantees the debt liabilities of operators introducing broadbandaccess networks such as fiber potic/DSL, etc.

To receive the following support, applicants should obtainauthorization of deployment plans from MPHPT in line with theProvisional Measures Law for Telecommunications InfrastructureImprovement.

20

IV. Mobile communications1. Status of diffusion of mobile phones

Mar.80

Mar.81

Mar.82

Mar.83

Mar.84

Mar.85

Mar.86

Mar.87

Mar.88

Mar.89

Mar.90

Mar.91

Mar.92

Mar.93

Mar.94

Mar.95

Mar.96

Mar.97

Mar.98

Mar.99

Mar.00

Nov.01

Mar.02

Aug.02

Deposit ¥200,000 ¥100,000 Abolished

Subscription fee ¥80,000 ¥72,000 ¥45,800 ¥21,000→¥9,000→¥6,000→Free

Monthly basiccharge

¥30,000 ¥18,000 ¥15,000 ¥9,500 ¥8,400 ¥6,600 Abolished(Analog)

(800MHz, digital) ¥8,800 ¥6,800 ¥4,900 ¥4,500

Call charge(3 minutes)

¥280 ¥260 ¥230→¥200→¥150→¥ Abolished(Analog)

(800MHz, digital) ¥260 ¥200→¥180→¥110→¥80→¥70 (Dec. 2000)

Note: Figures are cellular phone rates of NTT DoCoMo (standard plan rate for 3 minutes during daytime hours on weekdays [when the personreceiving the call is using a standard telephone within the central business zone of NTT DoCoMo]).

Year 2000 Year 2010Forecast in April 1996 25.0~32.5 million -

↓Forecast in February 1997 42.8~47.3 million 59.9~66.2 million

↓Forecast in Sept. 1999 6.2~6.7 million 7.5~10.0 million

Source: Telecommunications Technology Council Report

Revised forecast for mobile telephone market

Mar. 31, 2000: 63.883 million subscribersCellular phones: 60.942 millionPHS: 5.842 million

July 95: Market entry of PHS carriers

December 79:NTT started service

April 85:Telecom Reform

4

April 94: Introduction of competition, by 4 carriers ineach regional block (market entry of digitalmobile carriers) and COAM system

433

July 93: NTT DoCoMo split into 9 companies

213

July 92: NTT separated mobile communications service

138

December 88: NCCs' entry

24

As of the end of Mar. 2002: 73.211 million subscribersCellular phones: 69.121 millionPHS: 5.7 million

1,000

0

5,000

4,000

3,000

2,000

6,000

8,000

7,000

As of the end of Aug. 2002: 77.267 million subscribersCellular phones: 71.622 millionPHS: 5.645 million

21

2. Growth Factors in the Mobile Phone Market

● Mobile phone market is growing with an annual increase of 10 million subscribers eachyear.26.91 million (FY96) → 38.25 million (FY97) → 47.31 million (FY98) →56.85 million (FY99) → 66.78 million (FY2000) (Cellular phone: 60.94 million, PHS: 5.84million) → 74.817 million (As of the end of Mar.) (Cellular phone: 69.12 million, PHS:5.697 million)

● High growth is fostered by pro-competition policy and technological innovation whichaccelerate rate reduction and diversification

Pro-competition policy

(1) July 1992: Separation of mobile business unit from NTTJuly 1993: Division of the mobile business carrier separated from NTT into 9 companies

(2) 1994: Introduction of competition by 3 or 4 carriers in each market blockThis became the most pro-competitive policy in the world

(3) Permission for 3 PHS carriers in each market block

(4) April 1994: Introduction of COAM (Customer Owned and Maintained) system

(5) Dec. 1998: Nine NTT Personal Group companies transferred their PHS business to NTTDoCoMo Group companies in each region. (5 or 6 cellular and PHS carriers in eachregional block)

Technological innovation

(1) 1993: Digital mobile phone services launched - Higher quality, privacy function, etc.

(2) Down-sizing and weight-reduction of terminals, longer battery life, low-priced terminals

1997 2002New subscription fees 0 → 0Basic fees 6800 → 4500Communication fees 130 → 70

Rate reduction anddiversification

(1) With the implementation of the above-mentioned pro-competition policy and the progressof technological innovation, we succeeded in cutting our rates sharply. The newsubscription fee was reduced to zero starting December 1996. The basic charge was cutby about 34% and the telephone call rate, by about 46% during the past five years, saidNTT DoCoMo, Inc.

(2) April 1994: Introduction of "Low-volume call rate" tariff opened market to personal users.

(3) April 1995: NTT DoCoMo introduced "Area-by-area call rate" tariff (3 min. ¥70: 800MHz,digital).

• Realization of fair and competitive markets containing six carriersin each market

• Digitalization and drastic technological innovation in terminalequipment

• Rapid reduction and diversification of rates

22

V. Introduction of new wireless systems1. The third generation mobile communications system (IMT-2000)

※IMT-2000: International Mobile Telecommunications - 2000

◎ Characteristics Realization of an internationally unified system → Global service that can be used

worldwide High transmission speed about 200 times faster than that of existing mobile telephones

(capable of transmitting simple, moving images) Capable of providing a voice-communications service whose quality is as good as that of

the fixed telephone network.

◎ Schedule for launching services- NTT DoCoMo Group・・・・・・・・ In May 2001, this group launched the third-generation

mobile communications service on an experimental basis.(Japanese/European system)In October 2001, this group launched the full-fledgedservice.

- J-Phone・・・・・・・・・・・・・・・・・・・ This group launched the experimental service in June 2002.(Japan/European System)It will start the full-fledged service in December 2002.

- KDDI Group ・・・・・・・・・・・・・・・ This group launched the service in April 2002. (NorthAmerican system)

The 2 GHz service will be launched in April 2003 on anexperimental basis, and the full-fledged service, inOctober, 2003.

~~~~Changes in the mobile communications system~~~~◆The first-generation mobile telephone (analogue system)

This system was launched in 1979, using the frequency band of 800MHz. Voice communications serviceonly.

◆The second-generation mobile telephone (digital system)This system was launched in 1993, using the frequency bands of 800MHz and 1.5GHz. Voice-communications and low-speed data transmission services (transmission speed of 9.6 – 64 kbps)

◆PHS (Personal Handy Phone System)This system was launched in 1995, using the frequency band of 1.9 GHz. Voice-communications and low-speed data transmission services (transmission speed of 32 – 128 kbps)

64,128,144kbps

Switching center

Fixed network

Other mobile network

Other IP network

Base station

Base station

64 kbps mobile device

64~~~~384kbpsPDA

Indoor applications

2Mbps (384kbps immediately after this system was introduced)

Multimedia devicesFixed/mobile

network

Indoor equipment

Telephone

Devices installed in a car

Multimedia devices

384 kbps → moving images

23

2. The fourth-generation mobile communications system

移動通信システムの分類Classification of mobile

communications systems

0.01 0.1 1 10 100

High speed

Walking environment

Stationary environment

Mov

ing

spee

d

Digitalmobilephone

(Second-generation

system)PHS

4G System(Fourth-generation

system)

IMT 2000 (Third-generation

system)

Communication speed (Mbit/s)

Wireless access /Wireless LAN

The next-generation mobile communications system will come after IMT-2000. Thefollowing high technology will be achieved.

・ The downstream (from the base station to terminal devices) transmission speed will beincreased to 50-100 Mbps. (In the case of IMT-2000, the maximum speed of both thedownstream and upstream transmission is 2Mbps.)

・ Multimedia mobile communications, including the transmission of high-definition, movingimages.

・ Increased compliance with the Internet protocol, and is compatible with IPv6.

・ Introduction of the next-generation mobile communications technology, includingwireless technology software (the technology that makes it possible to flexibly changethe frequency, communications system, etc. via software)

Image of the system

24

1980’s

Starting period Growing periodExpanding period

(customization of mobile devices Personal use) Maturing period

Analogue,Mobile / cartelephone,

Cordless telephone(First generation)

Digital,Mobile / cartelephone,

Cordless telephone(2 - 2.5 generation)

IMT 2000(Third generation)

-

Multimedia mobilecommunications

systems, includingimage and broadband

services(Fourth generation)

Mainly voicecommunications

Voice / ordinary data ~64 kbps

voice / ordinary data~384kbps (~2Mbps) 50-100 Mbps

移動通信の変遷Trends of mobile communications

2000’s1990’s

2001: Recommendation from the Telecommunications Council (June)(Basic concept, plans involving technological development /standardization, methods of achieving such plans, etc.)⇒ Proposal to ITU

2002: Formulation of the policy on the frequency bands for future mobilecommunications, such as the fourth-generation mobile communications

2005 : Improvements and sophistication of the existing systemsEstablishment of the technology required for the fourth-generation mobilecommunication system

Around 2006: International allocation of the frequency bands for the fourth- generationmobile communications system (WRC-2006?)

By 2010: To put the fourth-generation mobile communications system into practicaluse

Application Schedule

25

3. Wireless access system

○○○○ E-Japan Priority Policy Program (Decided by the IT Strategy Headquarters on March29, 2001)

ExtractsBefore the end of the year 2001, the frequency band available for high-speed wireless Internet accesswill be expanded. At the same time, the allocation of frequency will be reviewed and the re-allocationwill be carried out by FY2002, to secure the frequency for fourth-generation mobile communicationssystems, etc.

Frequency bands System Maximumtransmission speed

Transmissiondistance

Institutionalization

Number ofcompanies

entered

Point-to-Point(P-P)※1 Around 10Mbps※2 Around 5km※3

2.4 GHz bandPoint-to-multipoint

(P-MP)※1 Around 2 Mbps Around 400m※3

1999.10(Expansion ofthe frequency-usable areas)

12

22/26/38 GHzband

Point-to-Point(P-P) Around 156 Mbps Around 4km 11※4

26/38 GHz band Point-to-multipoint(P-MP) Around 10 Mbps Around (radius)

1km

1998.1210※4

25 GHz band Point-to-PointPoint-to-multipoint Around 100 Mbps Around 100m 2002.2 ――

Notes:1. P-P: A system used when one radio station communicates with another radio subscriber station.

P-MP: A system used when one base station communicates with more than one subscriber station.2. The most widely-used system (IEEE 802.11b)

The revision of the current regulation in February 2002 enabled higher-speed telecommunications ofmore than 20 Mbps.

3. Because this frequency band is used for other purposes as well, the transmission distance is greatlyaffected by the surrounding environment. (High-directional antenna capable of extending transmissiondistance three-fold will be introduced around the spring of 2002.)

4. Some companies use both systems. As a result, the number of the companies in this market totaled 15.

SubscriberP-MP communications system

Base station

Subscriber

Subscriber

Subscriber

Fiber optics

P-Pcommunications

system

26

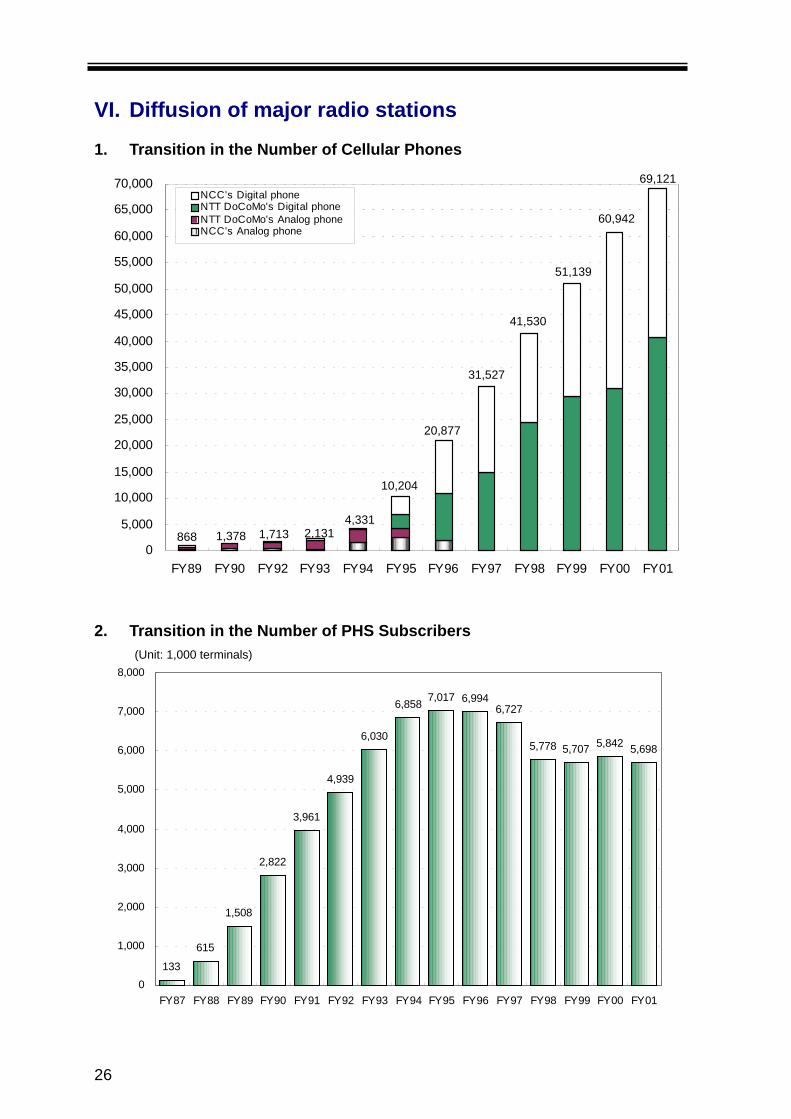

VI. Diffusion of major radio stations1. Transition in the Number of Cellular Phones

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

70,000

FY89 FY90 FY92 FY93 FY94 FY95 FY96 FY97 FY98 FY99 FY00 FY01

NCC's Digital phoneNTT DoCoMo's Digital phoneNTT DoCoMo's Analog phoneNCC's Analog phone

2. Transition in the Number of PHS Subscribers

133

615

1,508

2,822

3,961

4,939

6,030

6,858 7,017 6,9946,727

5,778 5,707 5,842 5,698

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY87 FY88 FY89 FY90 FY91 FY92 FY93 FY94 FY95 FY96 FY97 FY98 FY99 FY00 FY01

60,942

51,139

41,530

31,527

10,204

20,877

4,3312,1311,7131,378868

(Unit: 1,000 terminals)

69,121

27

3. Transition in the Number of Radio Pagers

0

2,000

4,000

6,000

8,000

10,000

12,000

FY88 FY89 FY90 FY91 FY92 FY93 FY94 FY95 FY96 FY97 FY98 FY99 FY00 FY01

NTT DoCoMo NCC

4. Transition in the Number of SA Earth Stations

1,066 1,157

2,597

3,227

3,7934,279

5,611

6,931

8,024

8,8728,588

8,876

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

FY90 FY91 FY92 FY93 FY94 FY95 FY96 FY97 FY98 FY99 FY00 FY01

(Unit: 1,000 subscribers)

3,520

10,61110,074

7,116

3,766

9,353

8,064

6,689

5,911

5,083

1,4392,071

4,247

(Unit: Number of VASTs)

1,137

28

References

Reference I. Status of diffusion of cable television

Reference II. Current Status of Broadcasting Businessin Japan

29

Reference I. Status of diffusion of cable television1. Changes in the total number of subscriber households, diffusion rate

1303

500

947 1048

794

672

27.1

20.0

17.0

14.6

11.0

21.8

0

200

400

600

800

1000

1200

1400

FY1996 (37.5%) FY1997 (34.4%) FY1998 (18.1%) FY1999 (19.3%) FY2000 (10.6%) FY2001 (24.4%)

[10,000 households]

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Diffusion rate [%]