Languages

Pages

Legal

WORLD AGRICULTURAL SITUATION Niagara Falls, October 2009Niagara Falls, October 2009

Farmers had a miserable time in 2008 and early 2009

Scarce credit owing to banking crisis

Reduced demand owing to recession

Fall in trade with product backed up on domestic markets

Collapse in commodity prices in 2nd half 2008

High input prices especially for fuel, fertiliser and feed

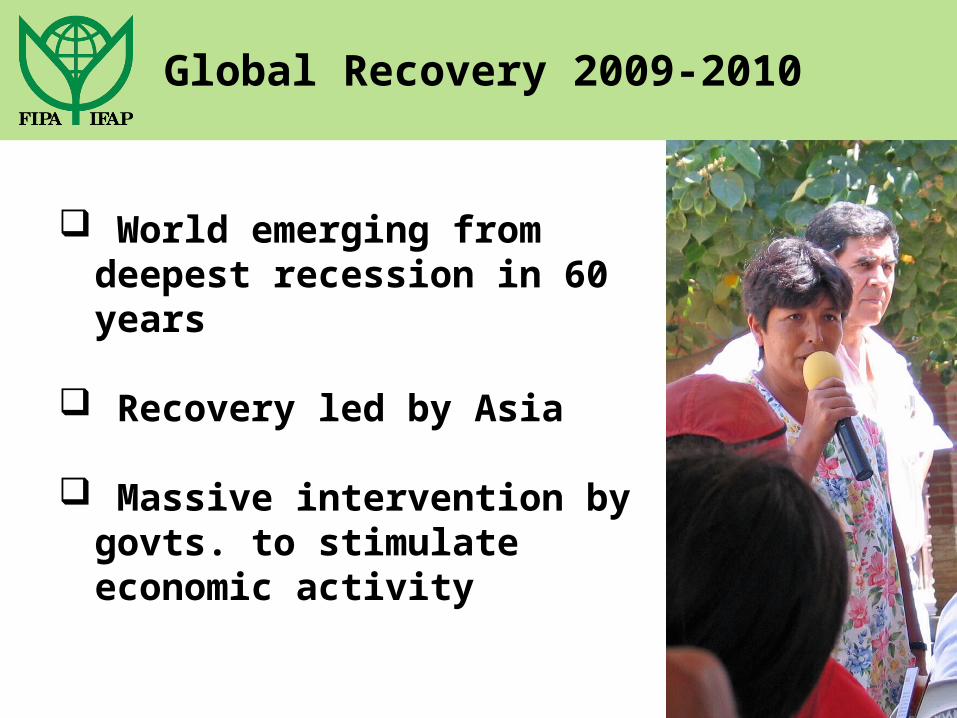

Global Recovery 2009-2010

World emerging from deepest recession in 60 years

Recovery led by Asia

Massive intervention by govts. to stimulate economic activity

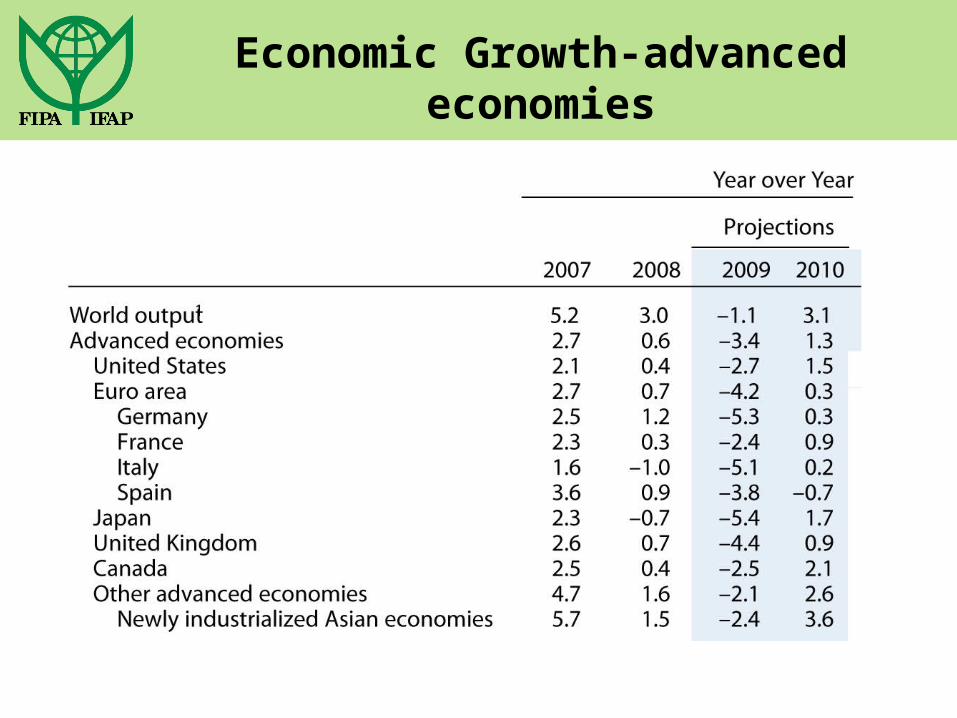

Economic Growth-advanced economies

Economic Growth–developing countries

Real GDP Growth (%)– World & Advanced countries

Source: IMF

Recovery in the BRIC Countries

Trade and commodity prices are recovering

Trade is picking up especially with Asia

Commodity prices are recovering

Food and agriculture was more resilient to the recession than other sectors

Trade volume & Commodity prices (% changes)

-10

0

10

20

30

40

50

60

Wheat Coarse grains

Oilseeds Sugar Pigmeat Poultry SMP

%

OECD Non-OECD World

Export growth from 2006-08 average to 2018

Developing countries driving growth in farm exports

Exchange rate movements (Index 2000=100)

Major currencies Emerging and developing economies

Commodity Price Developments

Commodity and Petroleum Prices

Impact on farmers

Oil prices rising faster than food prices

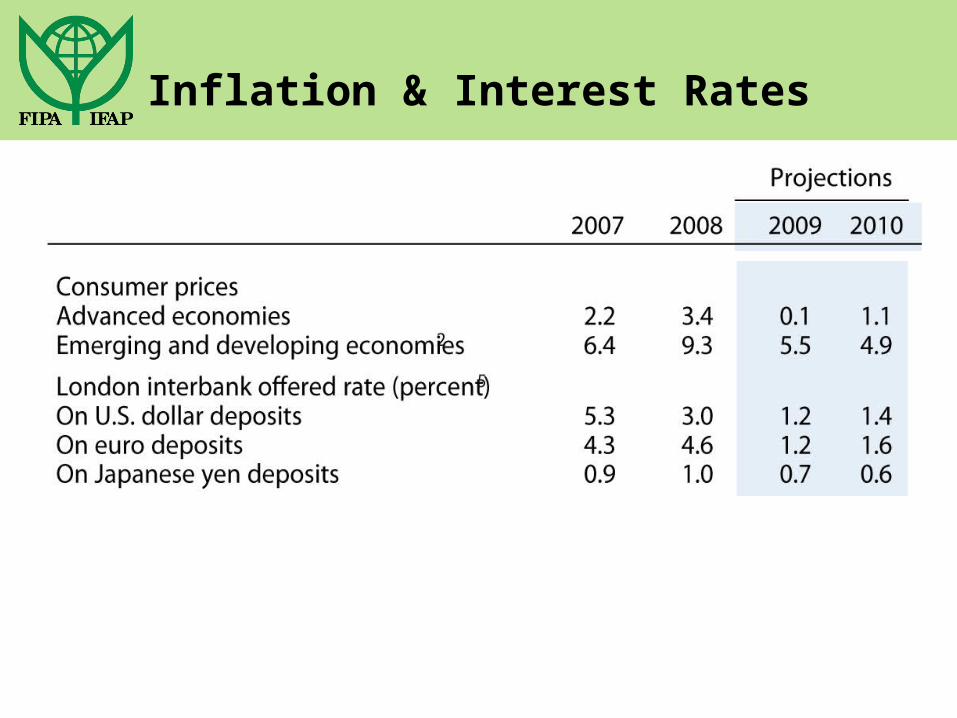

Low inflation & interest rates

Large govt. fiscal imbalances

Stable food and agric. markets

Inflation & Interest Rates

Government Fiscal Balances (% GDP)

Source: IMF

Major Food Crops - prices

Source: IMF

Major Food Crops - stocks

2) Corn, soybeans wheat, rice. Source: IMF

Major Food Crops - demand

Source: IMF

Major Food Crops - biofuel

Source: IMF

Demand for vegetable oil

0 5 10 15 20 25 30 35

2006-08

2018

2006-08

2018

2006-08

2018

Million tonnes

non-biofuel use

biofuel useIndo

nesi

aU

SAEU

Source: OECD

Meat & Dairy prices

Source: OECD

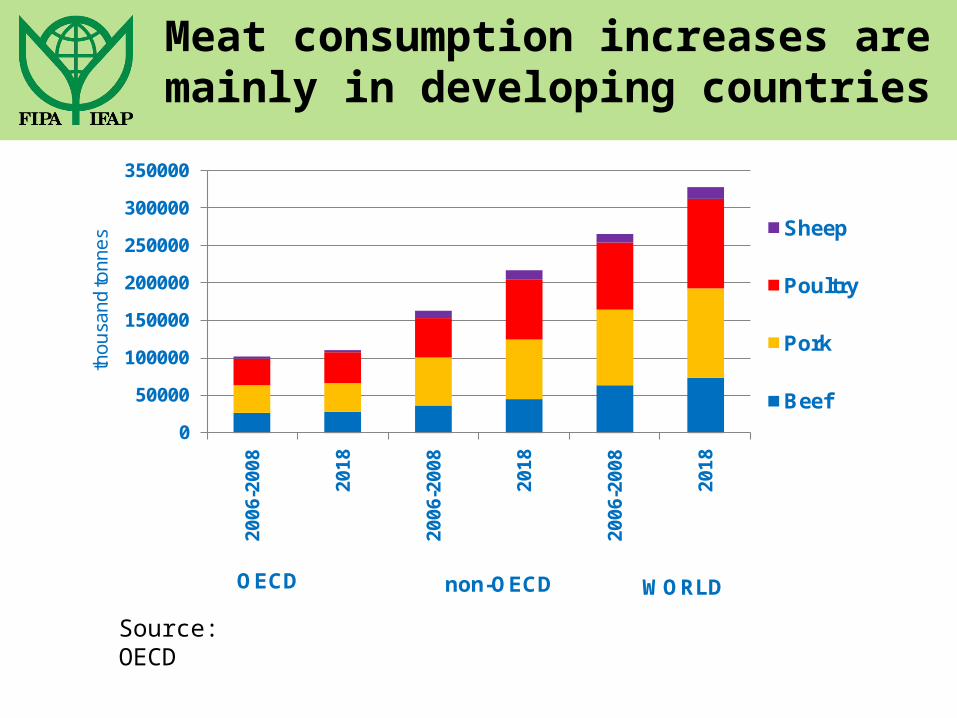

Meat consumption increases are mainly in developing countries

0

50000

100000

150000

200000

250000

300000

350000

20

06-

20

08

20

18

20

06-

20

08

20

18

20

06-

20

08

20

18

tho

usa

nd

ton

ne

s Sheep

Poultry

Pork

Beef

OECD non-OECD WORLD

Source: OECD

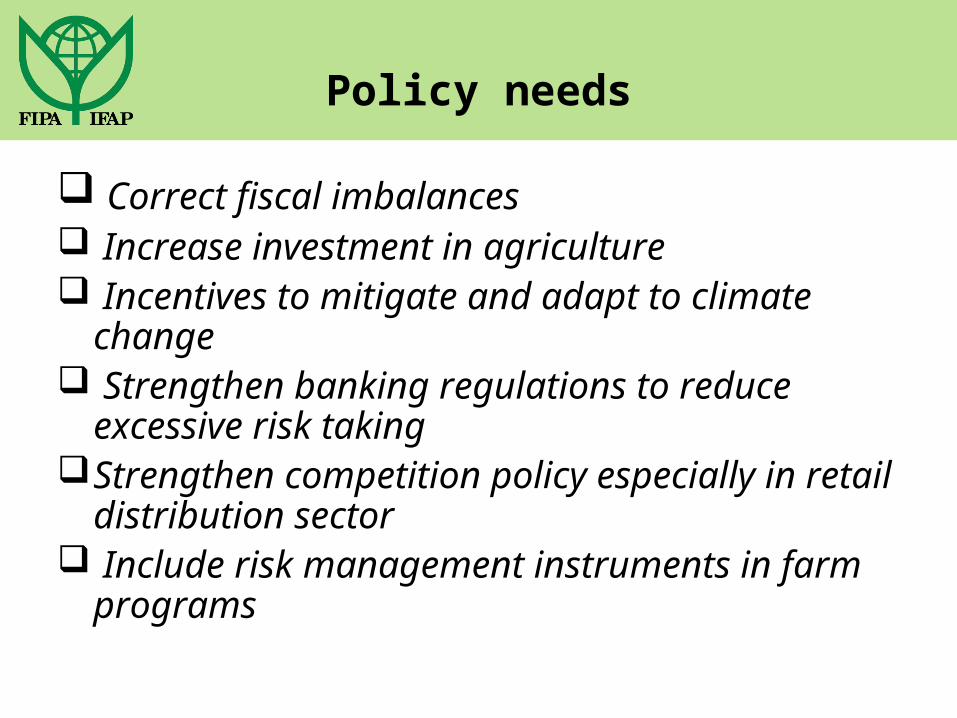

Policy needs

Correct fiscal imbalances Increase investment in agriculture Incentives to mitigate and adapt to

climate change Strengthen banking regulations to reduce

excessive risk takingStrengthen competition policy especially in

retail distribution sector Include risk management instruments in

farm programs

The world economy is growing again – along with trade - but growth is slow and uncertain

Farm commodity markets are strengthening

However, credit to remain tight; weather patterns irregular

Overall the future looks better for farmers – until of course the next economic recession due around 2020

Conclusions

www.ifap.org

Thank you for your attention

… the farmers’ voice at the world level

Top Related