Languages

Pages

Legal

MTC BAAQMD BCDCABAG

MARIN COUNTY WORKSHOP

DAVID VAUTIN, MTC – MAY 20, 2017

Source: https://www.flickr.com/photos/pepemichelle/33855582715/

WHAT IS VITAL SIGNS?

Vital Signs tracks 40 performance indicators to understand if the Bay Area is (or is not) making progress towards key regional goals.

2

WHAT IS VITAL SIGNS?

The interactive Vital Signs website allows residents to explore trends on the regional, county, city, and even neighborhood levels.

vitalsigns.mtc.ca.gov3

WHAT IS VITAL SIGNS?

The interactive Vital Signs website allows residents to explore trends on the regional, county, city, and even neighborhood levels.

vitalsigns.mtc.ca.gov4

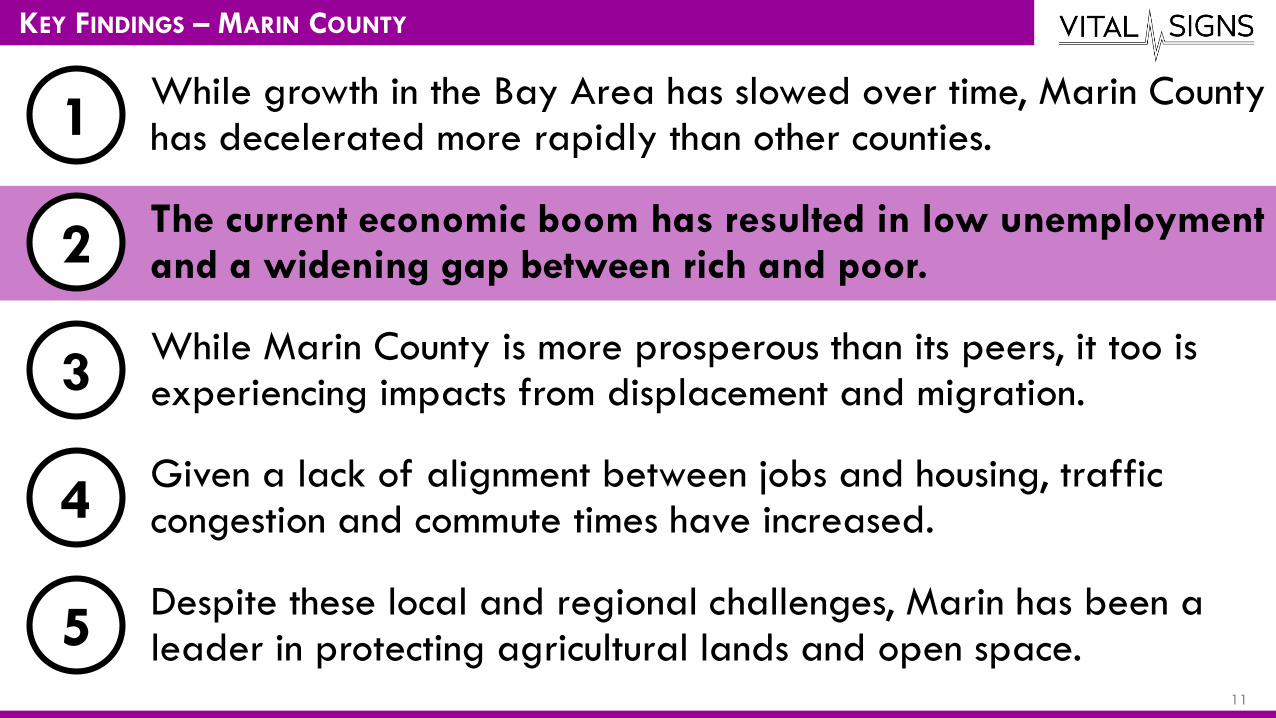

KEY FINDINGS – MARIN COUNTY

While growth in the Bay Area has slowed over time, Marin County has decelerated more rapidly than other counties.1

2

3

4

5

The current economic boom has resulted in low unemployment and a widening gap between rich and poor.

While Marin County is more prosperous than its peers, it too is experiencing impacts from displacement and migration.

Given a lack of alignment between jobs and housing, traffic congestion and commute times have increased.

Despite these local and regional challenges, Marin has been a leader in protecting agricultural lands and open space.

5

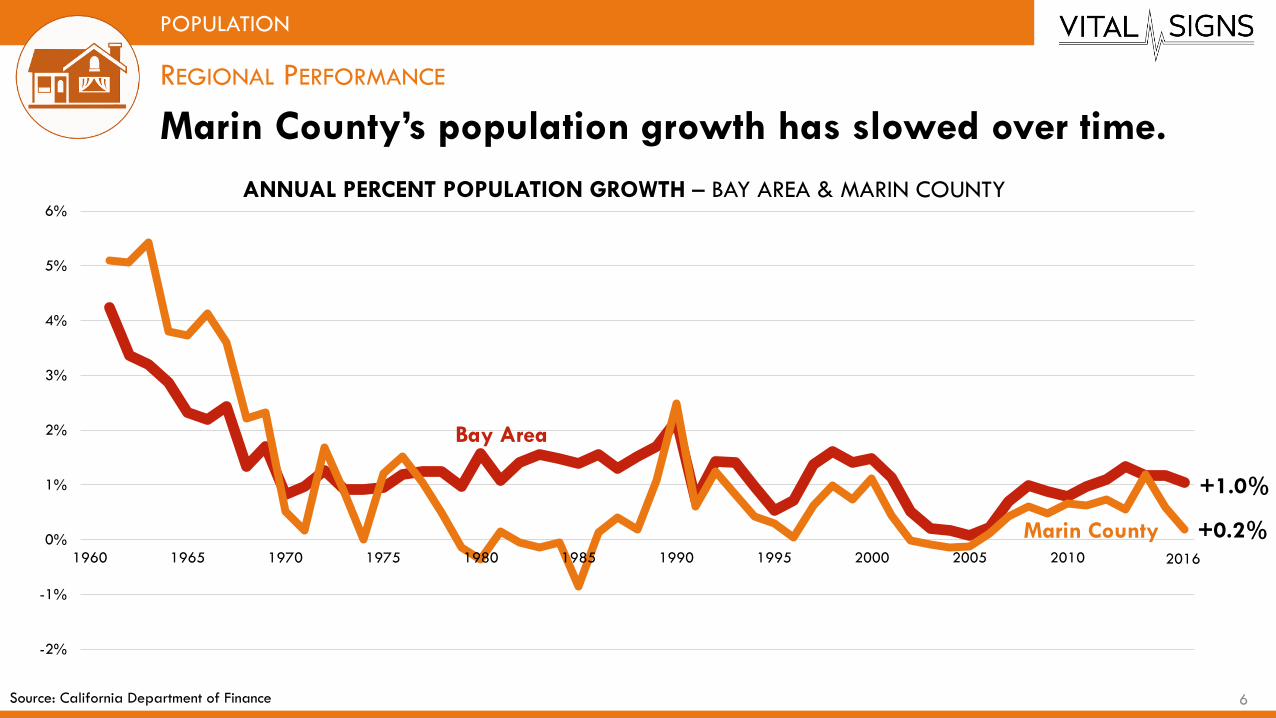

Marin County’s population growth has slowed over time.

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

ANNUAL PERCENT POPULATION GROWTH – BAY AREA & MARIN COUNTY

2016

REGIONAL PERFORMANCE

POPULATION

+1.0%

Source: California Department of Finance

+0.2%

Bay Area

Marin County

6

Marin County’s job growth has slowed in recent years.

-8%

-6%

-4%

-2%

0%

2%

4%

6%

1990 1995 2000 2005 2010 2015

ANNUAL PERCENT JOBS GROWTH – BAY AREA & MARIN COUNTY

REGIONAL PERFORMANCE

JOBS

+3.6%

Source: California Department of Finance

Bay Area

Marin County

+1.8%

7

North Bay counties have similar growth trajectories; regional growth has been increasingly concentrated in the core.

LOCAL FOCUS

POPULATION165

147

62

13

(25)

113

423

37 58

32

100

14

20

(37)

30

230

63 9

5

171

147

8 12 4

5

62

203

104

89

160

141

16

13 4

9

55

179

53

69

73 1

04

6 13 32

13

105

21

27

118

74

10

6

61

48

146

18

18

ALAMEDA CONTRA COSTA

MARIN NAPA SAN FRANCISCO

SAN MATEO SANTA CLARA SOLANO SONOMA

NOMINAL CHANGE BY COUNTY (IN THOUSANDS)

1960s 1970s 1980s 1990s 2000s 2010s

Source: California Department of Finance; note: 2010s spans six years between 2010 and 2016 8

Permitting has declined on the regional and county levels.

REGIONAL PERFORMANCE

HOUSING GROWTH

Source: Construction Industry Research Board (1967-2010); California Homebuilding Foundation (2011-2015)

0

10

20

30

40

50

60

70

1967 1973 1979 1985 1991 1997 2003 2009 2015

Thousa

nds

of

Perm

itte

d U

nits

PERMITTED UNITS BY YEAR – BAY AREA

Single-Family Units Multi-Family Units

0

1

2

3

4

5

6

7

1967 1973 1979 1985 1991 1997 2003 2009 2015Thousa

nds

of

Perm

itte

d U

nits

PERMITTED UNITS BY YEAR – MARIN COUNTY

Single-Family Units Multi-Family Units

9

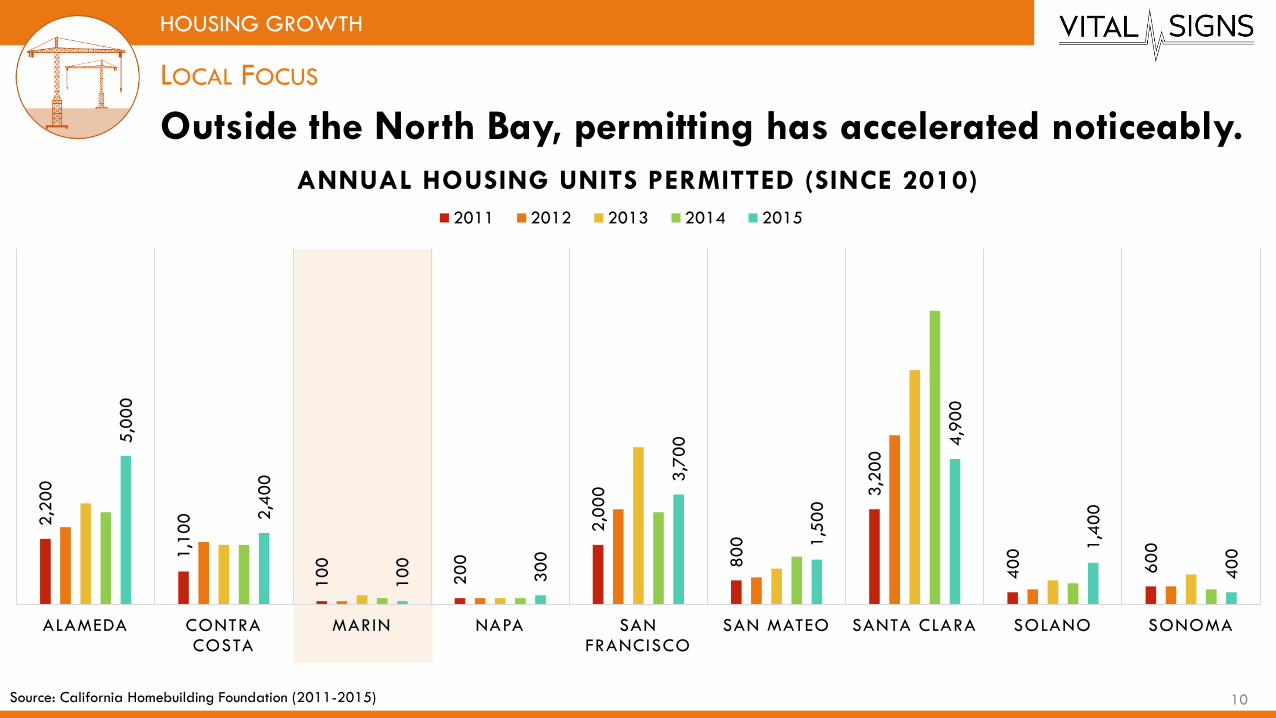

Outside the North Bay, permitting has accelerated noticeably.

LOCAL FOCUS

HOUSING GROWTH

Source: California Homebuilding Foundation (2011-2015)

2,2

00

1,1

00

10

0

20

0

2,0

00

80

0

3,2

00

40

0

60

0

5,0

00

2,4

00

10

0

30

0

3,7

00

1,5

00

4,9

00

1,4

00

40

0

ALAMEDA CONTRA COSTA

MARIN NAPA SAN FRANCISCO

SAN MATEO SANTA CLARA SOLANO SONOMA

ANNUAL HOUSING UNITS PERMITTED (SINCE 2010)

2011 2012 2013 2014 2015

10

KEY FINDINGS – MARIN COUNTY

While growth in the Bay Area has slowed over time, Marin County has decelerated more rapidly than other counties.1

2

3

4

5

The current economic boom has resulted in low unemployment and a widening gap between rich and poor.

While Marin County is more prosperous than its peers, it too is experiencing impacts from displacement and migration.

Given a lack of alignment between jobs and housing, traffic congestion and commute times have increased.

Despite these local and regional challenges, Marin has been a leader in protecting agricultural lands and open space.

11

The Bay Area economy is growing rapidly – especially in the San Francisco and San Jose MSAs.

$0

$100

$200

$300

$400

$500

$600

$700

$800

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

GRP (in

bill

ions

of

2015 d

olla

rs)

GROSS REGIONAL PRODUCT BY SUB-REGION

LOCAL FOCUS

ECONOMIC OUTPUT

Source: Bureau of Economic Analysis (inflation-adjusted to 2015 dollars)

Note: GRP is reported at the MSA level; the San Jose MSA include Santa Clara County and San Benito County

Napa CountySolano CountySonoma County

San Jose MSA

(2 counties)

San Francisco MSA

(5 counties)

$7$15$22

$133

$331

$9$17$24

$145

$360 $371

$173

$22$17$8

$9$20$26

$235

$432

12

Silicon Valley is booming, widening the gap in per capita GRP between northern and southern parts of the Bay Area.

$0

$20

$40

$60

$80

$100

$120

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Per

Capita G

RP (in

tho

usa

nds

of

2015 d

olla

rs)

GROSS REGIONAL PRODUCT PER CAPITA

LOCAL FOCUS

ECONOMIC OUTPUT

Napa County

Solano CountySonoma County

San Jose MSA

San Francisco MSA

Sources: Bureau of Economic Analysis (inflation-adjusted to 2015 dollars); Department of Finance

Note: GRP is reported at the MSA level; the San Jose MSA include Santa Clara County and San Benito County 13

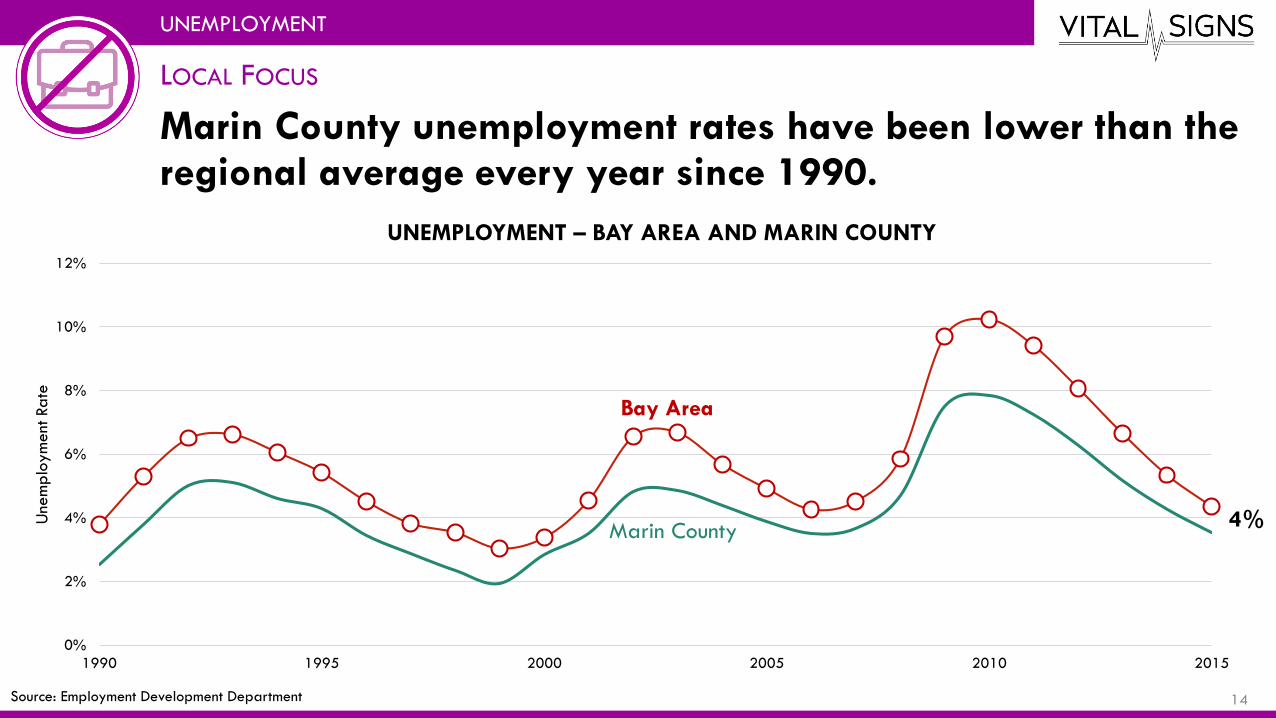

Marin County unemployment rates have been lower than the regional average every year since 1990.

0%

2%

4%

6%

8%

10%

12%

1990 1995 2000 2005 2010 2015

Unem

plo

ym

ent Rate

UNEMPLOYMENT – BAY AREA AND MARIN COUNTY

LOCAL FOCUS

UNEMPLOYMENT

Source: Employment Development Department

Bay Area

Marin County4%

14

Marin County residents have some of the highest incomes in the Bay Area – but many work outside of the county.

$50

$60

$70

$80

$90

$100

$110

$120

1970 1980 1990 2000 2010

Media

n H

ouse

hold

Inc

om

e(in

thous

and

s of

2015 d

olla

rs)

MEDIAN HOUSEHOLD INCOME BY COUNTY

LOCAL FOCUS

INCOME

Santa ClaraSan MateoMarinSan Francisco

Contra CostaAlameda

Napa

SolanoSonoma

Sources: U.S. Census Bureau/American Community Survey (inflation-adjusted to 2015 dollars); Bureau of Labor Statistics 15

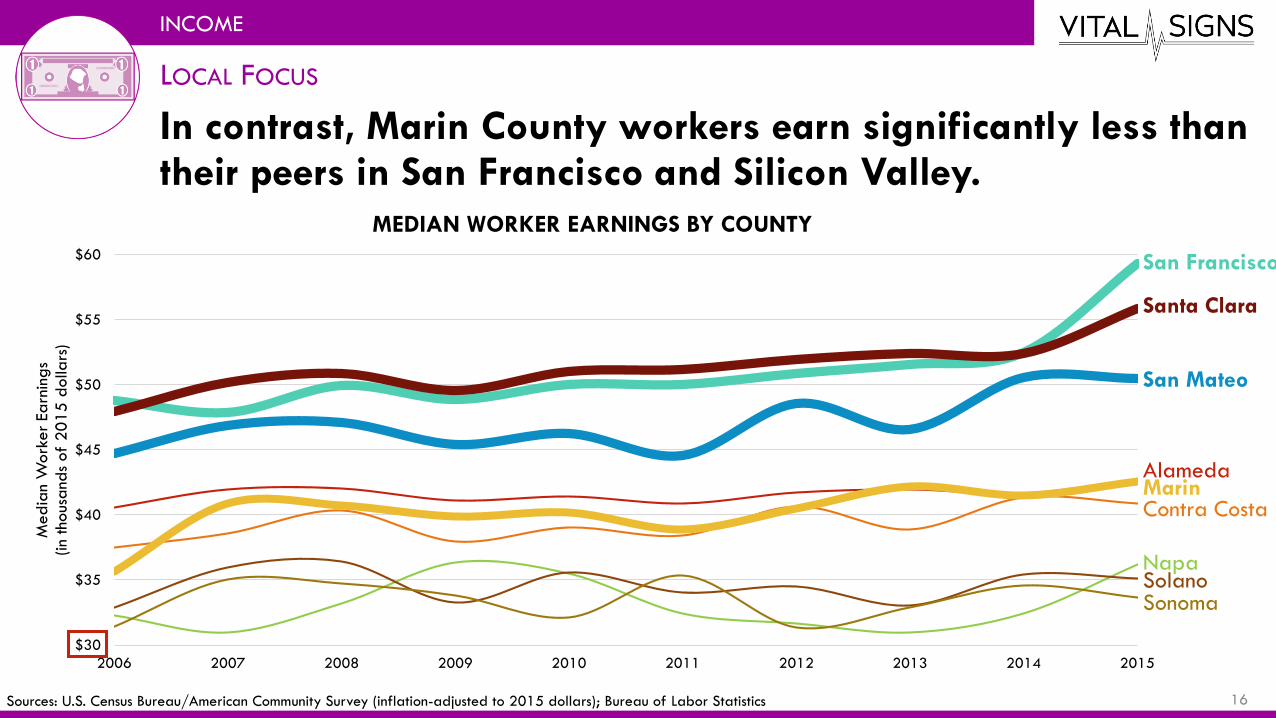

In contrast, Marin County workers earn significantly less than their peers in San Francisco and Silicon Valley.

$30

$35

$40

$45

$50

$55

$60

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Media

n W

ork

er

Earn

ings

(in

thous

and

s of

2015 d

olla

rs)

MEDIAN WORKER EARNINGS BY COUNTY

LOCAL FOCUS

INCOME

Santa Clara

San Mateo

Marin

San Francisco

Contra Costa

Alameda

NapaSolanoSonoma

Sources: U.S. Census Bureau/American Community Survey (inflation-adjusted to 2015 dollars); Bureau of Labor Statistics 16

KEY FINDINGS – MARIN COUNTY

While growth in the Bay Area has slowed over time, Marin County has decelerated more rapidly than other counties.1

2

3

4

5

The current economic boom has resulted in low unemployment and a widening gap between rich and poor.

While Marin County is more prosperous than its peers, it too is experiencing impacts from displacement and migration.

Given a lack of alignment between jobs and housing, traffic congestion and commute times have increased.

Despite these local and regional challenges, Marin has been a leader in protecting agricultural lands and open space.

17

In contrast to neighboring North Bay counties, Marin County’s poverty rate is the lowest in the region.

30%28% 28%

25% 25% 24%

21% 21%19%

SOLANO SONOMA NAPA SAN FRANCISCO

ALAMEDA CONTRA COSTA

SANTA CLARA SAN MATEO MARIN

Share

Of

Popul

ation In

Pove

rty (200%

Leve

l)

2015 POVERTY RATE BY COUNTY

LOCAL FOCUS

POVERTY

Source: U.S. Census Bureau/American Community Survey, 2015

Note: poverty is defined as living below twice the national poverty level

Bay Area Regional Poverty Rate – 24%

18

Marin County home prices have risen since the end of the recession but remain below their 2007 peak.

$0

$200

$400

$600

$800

$1,000

$1,200

1997 2000 2003 2006 2009 2012 2015

Media

n H

om

e S

ale

Price

(in

thous

and

s of

2015 d

olla

rs)

MEDIAN HOME SALE PRICE BY COUNTY

LOCAL FOCUS

HOME PRICES

San Francisco

San Mateo

MarinSanta Clara

Alameda

NapaSonomaContra Costa

Solano

Sources: Zillow (inflation-adjusted to 2015 dollars); Bureau of Labor Statistics 19

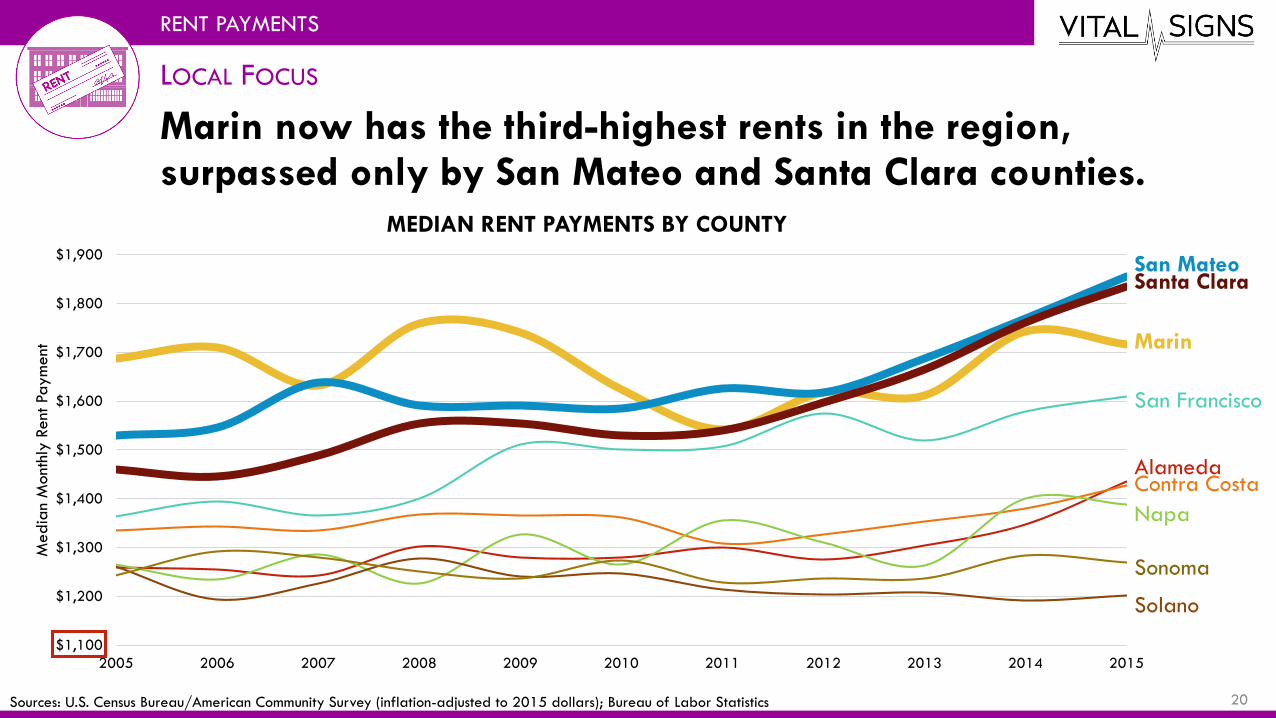

Marin now has the third-highest rents in the region, surpassed only by San Mateo and Santa Clara counties.

$1,100

$1,200

$1,300

$1,400

$1,500

$1,600

$1,700

$1,800

$1,900

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Media

n M

onth

ly R

ent Paym

ent

MEDIAN RENT PAYMENTS BY COUNTY

LOCAL FOCUS

RENT PAYMENTS

San MateoSanta Clara

Marin

San Francisco

AlamedaContra Costa

Napa

Sonoma

Solano

Sources: U.S. Census Bureau/American Community Survey (inflation-adjusted to 2015 dollars); Bureau of Labor Statistics 20

Marin County’s housing affordability – as a share of income – has closely tracked regional trends since 1980.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1980 1985 1990 1995 2000 2005 2010 2015

Share

of

House

hold

s

SHARE OF HOUSEHOLD INCOME SPENT ON HOUSING – BAY AREA

REGIONAL PERFORMANCE

HOUSING AFFORDABILITY

Less than 20% of Income

20% to 34% of Income

At least 35% of Income 31%

32%

37%48%

30%

22%

Source: U.S. Census Bureau/American Community Survey

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1980 1985 1990 1995 2000 2005 2010 2015Share

of

House

hold

s

SHARE OF HOUSEHOLD INCOME SPENT ON HOUSING – MARIN COUNTY

Less than 20% of Income

20% to 34% of Income

At least 35% of Income 33%

31%

36%46%

30%

24%

21

Of the nine Bay Area counties, Marin County’s lower-income residents are the most at risk of displacement.

0%

20%

40%

60%

1990 1995 2000 2005 2010 2015

Sha

re o

f Lo

wer-

Inco

me H

ouse

hold

s at Risk

DISPLACEMENT RISK BY COUNTY

LOCAL FOCUS

DISPLACEMENT RISK

Sources: U.S. Census Bureau/American Community Survey; Longitudinal Tract Database; note that recent data relies upon 5-year rolling averages; only 2010 and 2015 are shown for clarity

San Francisco

San Mateo

Solano

Marin

Alameda

Santa Clara

Sonoma

Contra Costa

Napa

San Francisco

San Mateo

Solano

Marin

Alameda

Santa Clara

Sonoma

Contra Costa

Napa

22

North Bay residents are increasingly moving out of the region and are being replaced by new arrivals from the West Bay.

LOCAL FOCUS

MIGRATION

Sources: American Community Survey/U.S. Census Bureau – County-to-County Migration Data; note that data relies upon 5-year rolling averages; immigration from abroad not shown for simplicity

2014 NET MIGRATION BY SUBREGION

SAN FRANCISCO + SILICON VALLEY EAST BAY NORTH BAY

East Bay:

-14,100 people

Out of Region:

-5,900 people

SF +

Silicon Valley:

+14,100 people

North Bay:

-3,600 people

North Bay:

+600 people

Out of Region:

-9,100 people

SF +

Silicon Valley:

+3,600 people

East Bay:

-600 people

Out of Region:

-1,800 people

23

KEY FINDINGS – MARIN COUNTY

While growth in the Bay Area has slowed over time, Marin County has decelerated more rapidly than other counties.1

2

3

4

5

The current economic boom has resulted in low unemployment and a widening gap between rich and poor.

While Marin County is more prosperous than its peers, it too is experiencing impacts from displacement and migration.

Given a lack of alignment between jobs and housing, traffic congestion and commute times have increased.

Despite these local and regional challenges, Marin has been a leader in protecting agricultural lands and open space.

24

Because of the county’s job-housing imbalance, significant shares of workers and residents commute between counties.

LOCAL FOCUS

COMMUTE PATTERNS

Source: U.S. Census Bureau – Census Transportation Planning Package

Marin County64%

Sonoma County14%

San Francisco6%

Other Bay Area Counties

9%

Outside the Bay Area

2%

Other31%

COMMUTE ORIGINS OF MARIN COUNTY WORKERS

Marin County65%

San Francisco

22%

Other Bay Area Counties

12%

Outside the Bay Area

1%

Other35%

COMMUTE DESTINATIONS OF MARIN COUNTY RESIDENTS

25

Commute times have ticked upward regionally in recent years – and Marin County is no exception to this trend.

0

5

10

15

20

25

30

35

1980 1985 1990 1995 2000 2005 2010 2015

Media

n C

om

mute

Tim

e

COMMUTE TIMES – BAY AREA AND MARIN COUNTY

REGIONAL PERFORMANCE

COMMUTE TIME

Source: U.S. Census Bureau

Bay Area

Marin County31 min.

30 min.

26

While traffic congestion in Marin remains slightly less severe than the region as a whole, it has grown markedly since 2008.

0%

1%

2%

3%

4%

5%

6%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Congest

ed S

hare

of

Freew

ay V

MT

MILES TRAVELED IN CONGESTION – BAY AREA AND MARIN COUNTY

REGIONAL PERFORMANCE

MILES TRAVELED IN CONGESTION

Source: Iteris/PeMS, 2015

Bay Area

Marin County

6%

4%

27

The Bay Area has made significant progress in shifting travel modes in recent years, but at a slower pace in Marin.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1960 1970 1980 1990 2000 2010

COMMUTE MODE SHARE – BAY AREA

Auto Transit Walk, Bike, Other Work at Home

70%

81%79%76%

REGIONAL PERFORMANCE

COMMUTE MODE CHOICE

Source: U.S. Census Bureau

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1960 1970 1980 1990 2000 2010

COMMUTE MODE SHARE – MARIN COUNTY

Auto Transit Walk, Bike, Other Work at Home

73%77% 76%

75%

28

In the case of Marin, this trend is due in part to declining bus ridership even as ferry usage has increased.

0

10

20

30

40

1991 1996 2001 2006 2011 2016

Ave

rage W

eekday B

oard

ings

(in tho

usa

nds)

ANNUAL AVERAGE WEEKDAY RIDERSHIP FOR MARIN COUNTY OPERATORS

LOCAL FOCUS

TRANSIT RIDERSHIP

Note: Estimated average weekday boardings is annual boardings divided by 300 (standard MTC factor)

Source: FTA NTD Annual Database, 2015; FTA NTD Monthly Adjusted Data (preliminary), 2016

Bus(Marin Transit +

Golden Gate Bus)

Ferry(Golden Gate

Ferry)

29

PM2.5

1

2

3

4

5Despite these local and regional challenges, Marin has been a leader in protecting agricultural lands and open space.

KEY FINDINGS – MARIN COUNTY

While growth in the Bay Area has slowed over time, Marin County has decelerated more rapidly than other counties.

The current economic boom has resulted in low unemployment and a widening gap between rich and poor.

While Marin County is more prosperous than its peers, it too is experiencing impacts from displacement and migration.

Given a lack of alignment between jobs and housing, traffic congestion and commute times have increased.

30

Greenfield protection policies in Marin County and beyond have made a difference in protecting natural lands.

(2,000)

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

2-Y

ear

Gro

wth

in

Deve

loped L

and in

Acr

es

TWO-YEAR CHANGE IN REGIONAL GREENFIELD DEVELOPMENT(CHANGE IN DEVELOPED LAND)

REGIONAL PERFORMANCE

GREENFIELD DEVELOPMENT

Source: Department of Conservation, Farmland Mapping and Monitoring Program

Marin County

Rest of Region

31

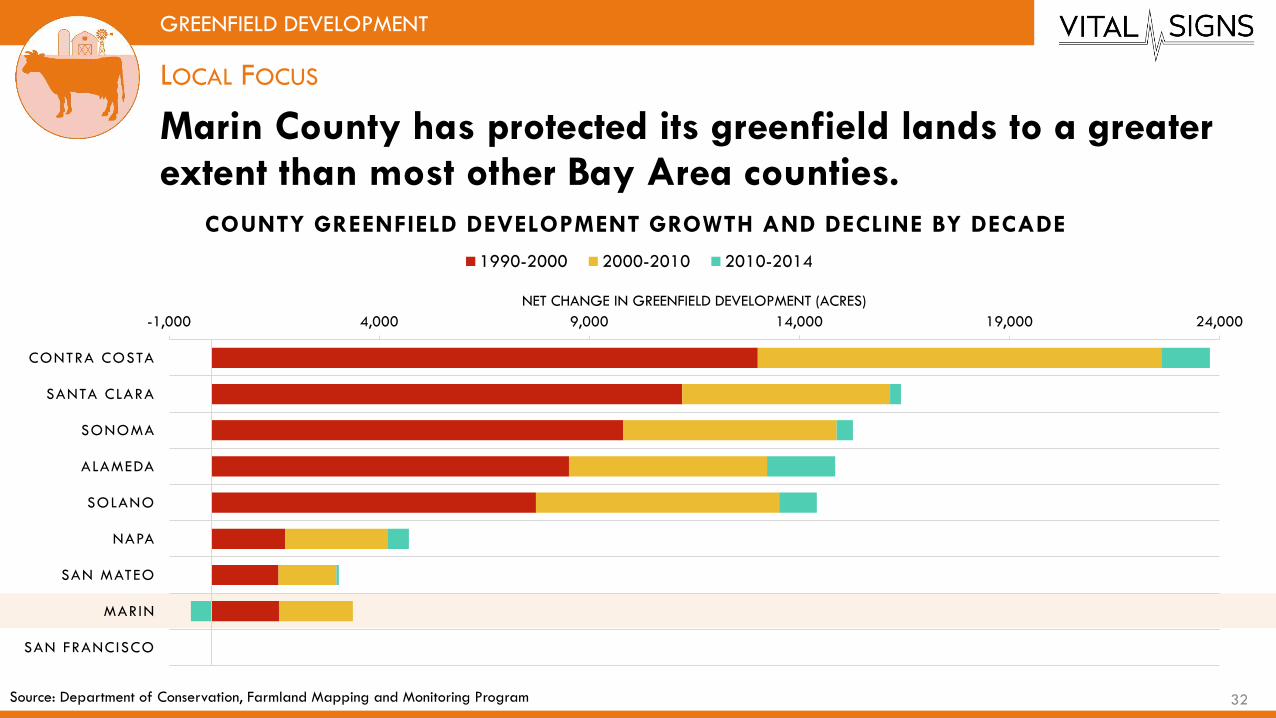

Marin County has protected its greenfield lands to a greater extent than most other Bay Area counties.

-1,000 4,000 9,000 14,000 19,000 24,000

CONTRA COSTA

SANTA CLARA

SONOMA

ALAMEDA

SOLANO

NAPA

SAN MATEO

MARIN

SAN FRANCISCO

NET CHANGE IN GREENFIELD DEVELOPMENT (ACRES)

COUNTY GREENFIELD DEVELOPMENT GROWTH AND DECLINE BY DECADE

1990-2000 2000-2010 2010-2014

LOCAL FOCUS

GREENFIELD DEVELOPMENT

Source: Department of Conservation, Farmland Mapping and Monitoring Program 32

PM2.5

Major investments in wetland restoration in the mid-2000s resulted in thousands of new acres of Bay surface area.

REGIONAL PERFORMANCE

BAY RESTORATION

Source: BCDC Annual Report, 2015

-1,000

1,000

3,000

5,000

7,000

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Acr

es

of

Annual C

hang

e

ANNUAL CHANGE IN SAN FRANCISCO BAY SURFACE AREA

Major wetland restorations in Sonoma

County, Solano County, and Hayward

Major wetland

restorations in Novato

Major wetland

restorations in Redwood

City and North Bay

Major wetland

restorations in

Solano County

33

MTC BAAQMD BCDCABAG

DAVID VAUTIN, MTC

UPCOMING DATA RELEASES:

LATE SPRING 2017 – TRANSPORTATION

SUMMER 2017 – ENVIRONMENT

Source: https://www.flickr.com/photos/isolino/8338786790/

vitalsigns.mtc.ca.gov

QUESTIONS?

Top Related