Languages

Pages

Legal

Loss Reserving Approaches for

Mortgage Guaranty Insurance

2003 CAS Annual MeetingNew Orleans Marriott

John F. Gibson, FCAS, MAAAPrincipal

PricewaterhouseCoopers, LLP

2

Outline of Presentation

• Loss Reserving Distinctives• Factors that Influence Ultimate Losses• Data to Analyze• Contingency Reserves• Industry Loss Reserving Approach• Problems with Traditional Loss Development Methods• Loss Reserving Approaches• Current and Future Trends

3

Loss Reserving Distinctives

• Claim = Loan that has defaulted as of the statement date

• Not a reserve for the life of the loan

• Type and amount of coverage

• Amounts paid can exceed theoretical coverage

4

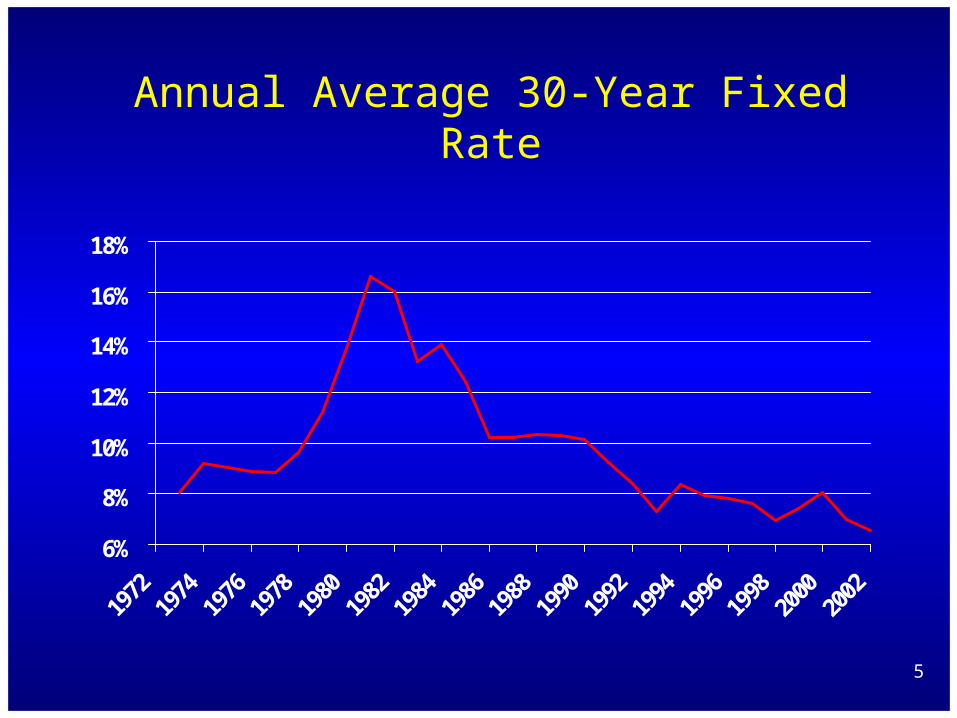

Factors that Influence Ultimate Losses

• Housing Values

• Unemployment

• Interest Rates

• Claim Settlement Practices

5

Annual Average 30-Year Fixed Rate

6%

8%

10%

12%

14%

16%

18%

6

Data to Analyze

• Analysis by region or state

• Analysis by type of loan – LTV

• Analysis by size of loan

• Analysis by age of loan

• Analysis of Pool Insurance and other higher risk segments

7

Contingency Reserves – Need

•Premiums and losses have mismatched timing

•Losses realized when loans become delinquent

•But economic catastrophes can drive 100+% loss ratios for a number of consecutive years

•Mortgage insurers are monoline

8

Contingency Reserves - Determination

50% of premium each year is set aside into a contingency reserve and held for 10 years

Losses in excess of a 35% loss ratio in a calendar year can be removed on a FIFO basis

After 10 years, remaining funds, if any, can be moved to free surplus

9

Industry Loss Reserving Approach

• Identification of claims by status – for example:

1. Delinquent

2. Pending Foreclosure

3. Foreclosure

4. Claim Filed

• Severity Factor – Percentage of exposure to be paid – greater than 100% for filed claim

10

Industry Loss Reserving Approach

• IBNR Provision = % of reported

• Regional analysis

• Pool business analysis

• Recent runoff history very favorable

11

Recent Runoff History(in $ millions)

YearOriginal

Loss Reserve

Developed Reserves Thru ’02

Developed to Original

1997 1,152 621 (46%)

1998 1,260 504 (60%)

1999 1,307 530 (60%)

2000 1,337 642 (52%)

2001 1,477 1,098 (26%)

12

Problems with Traditional Loss Development Methods

• Leverage effect of economic cycle on number of defaults, cure rates and amounts paid can produce significant volatility

• Economic cycle operates on a calendar year, not an accident year

13

Loss Reserving ApproachProjection of Ultimate Reported Delinquencies

• Delinquencies are reported quickly – 85% at 12 months, more that 99% at 24 months

• Eliminates need for separate IBNR provision

14

Loss Reserving ApproachDelinquency Rate

2.0%

2.5%

3.0%

3.5%

4.0%

1999 2000 2001 2002 2003 2004

15

Loss Reserving ApproachProjections of Ultimate Claims Paid - Approaches

• Project directly – very volatile

• Project Closed Without Payment (Cured) claims and subtract from ultimate reported

• Bornhuetter – Ferguson method using a priori ratio of closed with payment (CWP) to loan balances

16

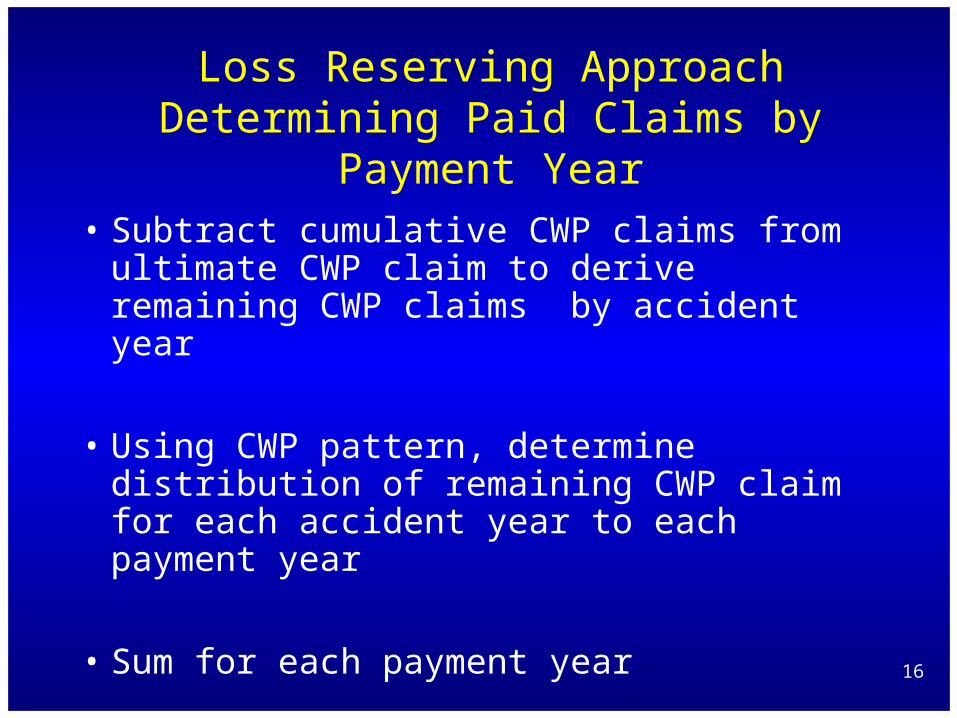

Loss Reserving ApproachDetermining Paid Claims by Payment Year

• Subtract cumulative CWP claims from ultimate CWP claim to derive remaining CWP claims by accident year

• Using CWP pattern, determine distribution of remaining CWP claim for each accident year to each payment year

• Sum for each payment year

17

Loss Reserving ApproachCure Rate

65%

70%

75%

80%

85%

90%

95%

18

Distribution of Outstanding Closed Claims with Payments to Closure Year

As of 12/31/02 Outstanding Closed Claims with Closure Year Accident Payments

Year at 12/31/02 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 (1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11) (12)

1991 0 0 0 0 0 0 0 0 0 0 0 0 1992 0 0 0 0 0 0 0 0 0 0 0 0 1993 1 1 0 0 0 0 0 0 0 0 0 0 1994 6 3 3 0 0 0 0 0 0 0 0 0 1995 13 4 4 4 0 0 0 0 0 0 0 0 1996 25 13 4 4 4 0 0 0 0 0 0 0 1997 31 14 8 3 3 3 0 0 0 0 0 0 1998 57 31 12 7 2 2 2 0 0 0 0 0 1999 67 30 20 8 5 2 2 2 0 0 0 0 2000 192 113 36 23 9 5 2 2 2 0 0 0 2001 1,258 916 201 64 42 16 10 3 3 3 0 0 2002 3,831 2,215 1,177 258 82 53 21 12 4 4 4 0

Total 5,481 3,341 1,466 372 146 81 36 19 9 7 4 0

Closed Claim With Months Developed Payment Pattern 12 24 36 48 60 72 84 96 108 120 132

(13) Cumulative 6.6% 60.6% 89.3% 95.6% 97.6% 98.9% 99.4% 99.7% 99.8% 99.9% 100.0% (14) Incremental 6.6% 54.0% 28.7% 6.3% 2.0% 1.3% 0.5% 0.3% 0.1% 0.1% 0.1%

19

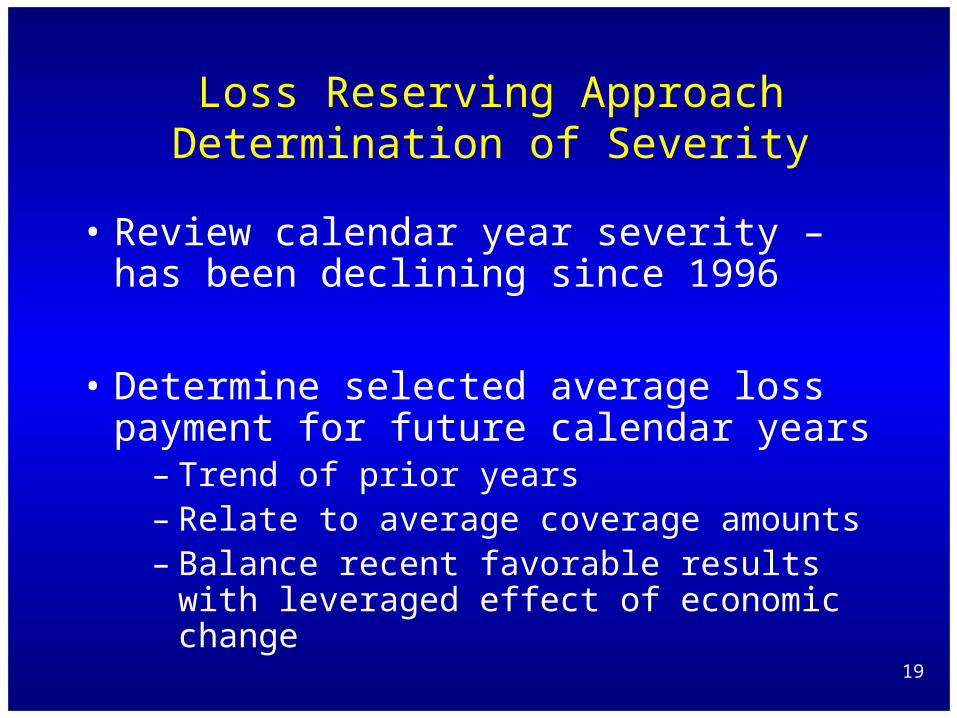

Loss Reserving ApproachDetermination of Severity

• Review calendar year severity – has been declining since 1996

• Determine selected average loss payment for future calendar years

– Trend of prior years– Relate to average coverage amounts – Balance recent favorable results with

leveraged effect of economic change

20

0

5,000

10,000

15,000

20,000

25,000

Loss Reserving ApproachAverage Paid Severity by Calendar Year

21

Loss Reserving ApproachReserve Estimates

• Loss reserve by payment year is projected claims to be closed by payment year times projected loss payment by payment year

• Supplement with traditional loss development methods

22

Loss Reserving ApproachDetermination of Reserve Range

• Based on conservative and optimistic assumptions for defaults, cure rates and severity

• Reserve range is much wider than most P&C lines of business

23

Current & Future Trends

• Impact of the Economic Cycle

• Refinance Cycle

• House Price Appreciation

• Deterioration of Credit Quality

Top Related