Languages

Pages

Legal

Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

LIBOR-Based Futures

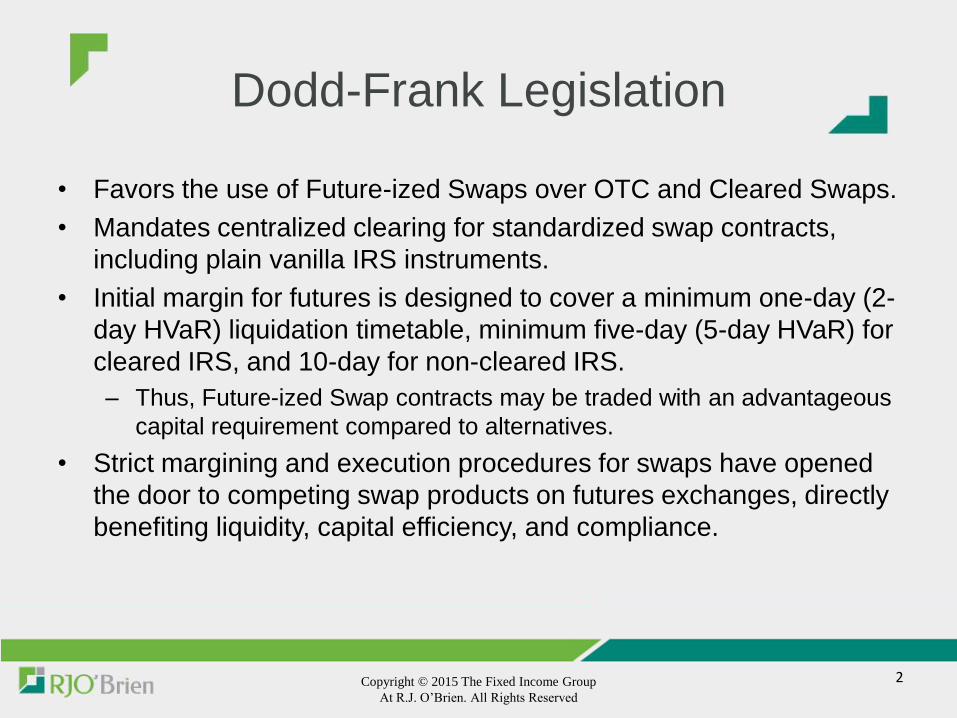

Dodd-Frank Legislation

• Favors the use of Future-ized Swaps over OTC and Cleared Swaps.

• Mandates centralized clearing for standardized swap contracts,

including plain vanilla IRS instruments.

• Initial margin for futures is designed to cover a minimum one-day (2-

day HVaR) liquidation timetable, minimum five-day (5-day HVaR) for

cleared IRS, and 10-day for non-cleared IRS.

– Thus, Future-ized Swap contracts may be traded with an advantageous

capital requirement compared to alternatives.

• Strict margining and execution procedures for swaps have opened

the door to competing swap products on futures exchanges, directly

benefiting liquidity, capital efficiency, and compliance.

Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

2

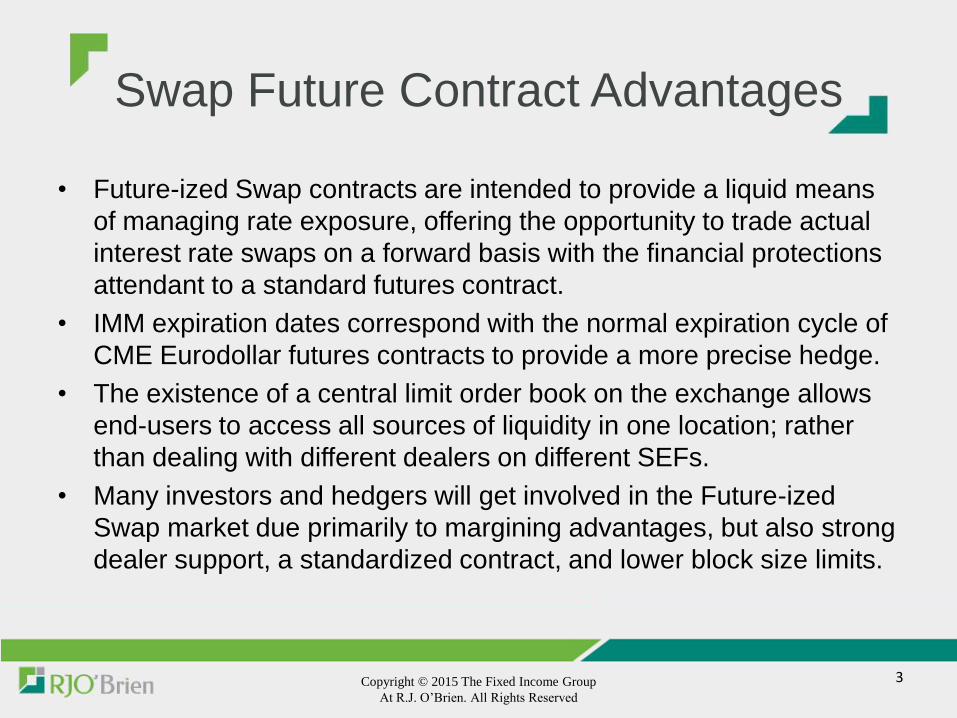

Swap Future Contract Advantages

• Future-ized Swap contracts are intended to provide a liquid means

of managing rate exposure, offering the opportunity to trade actual

interest rate swaps on a forward basis with the financial protections

attendant to a standard futures contract.

• IMM expiration dates correspond with the normal expiration cycle of

CME Eurodollar futures contracts to provide a more precise hedge.

• The existence of a central limit order book on the exchange allows

end-users to access all sources of liquidity in one location; rather

than dealing with different dealers on different SEFs.

• Many investors and hedgers will get involved in the Future-ized

Swap market due primarily to margining advantages, but also strong

dealer support, a standardized contract, and lower block size limits.

3 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

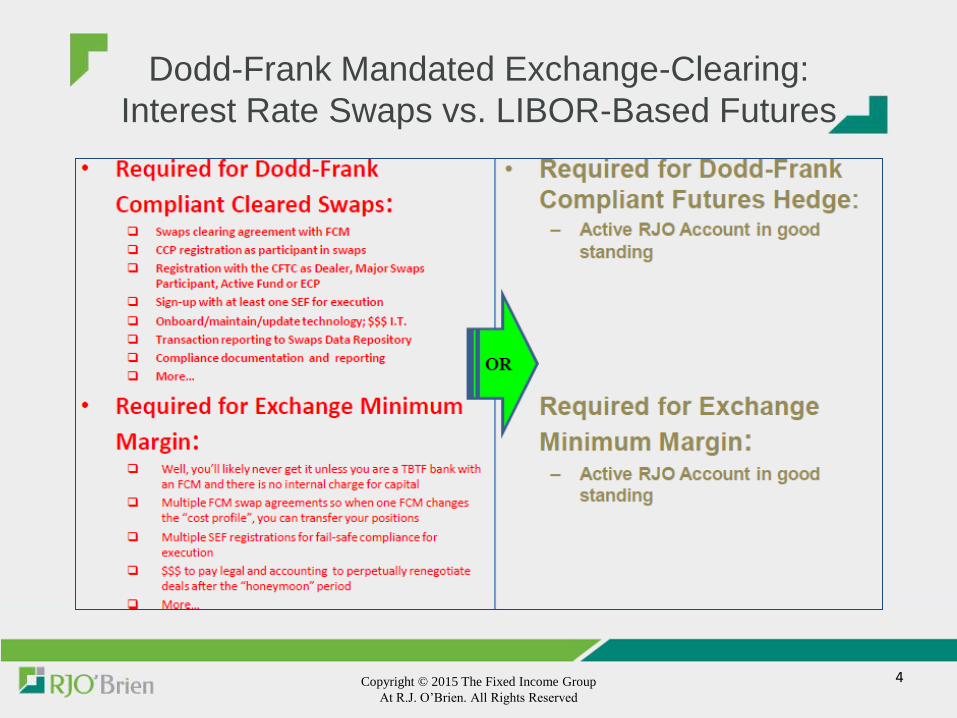

Dodd-Frank Mandated Exchange-Clearing:

Interest Rate Swaps vs. LIBOR-Based Futures

4 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

Exchange Traded LIBOR Futures • Offering:

A. Inherent Dodd-0Frank-compliance- CCP-clearing & competitive execution

B. Total market transparency— bid/ask, size, actionable markets

C. Best-in-capital-markets Liquidity— universal access to all users

D. Maximum capital efficiency— D/F min 2-day HVaR margining

For interest rate hedging: use exchange-cleared LIBOR-based futures.

• Eligible risk transfer vehicles for interest rate hedging; cleared through best-in-class CME:

– 3-month LIBOR futures (“Eurodollar” futures)

– 2, 5, 7, 10 & 30-year flex-tenor LIBOR Swap futures (Eris Swap Futures)

– 2, 5, 10 & 30-year LIBOR Deliverable Swap Futures

• For fixed-rate amortizing loans, a combination of futures contracts required for best hedge accuracy.

• ***Cleared OTC Swaps—not futures—exist at substantially higher (~2x collateral) margins, require SEF execution, additional Dodd-

Frank compliance mandates, designed as non-dynamic, portfolio hedge vehicle PRIOR TO development of swap futures.

5 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

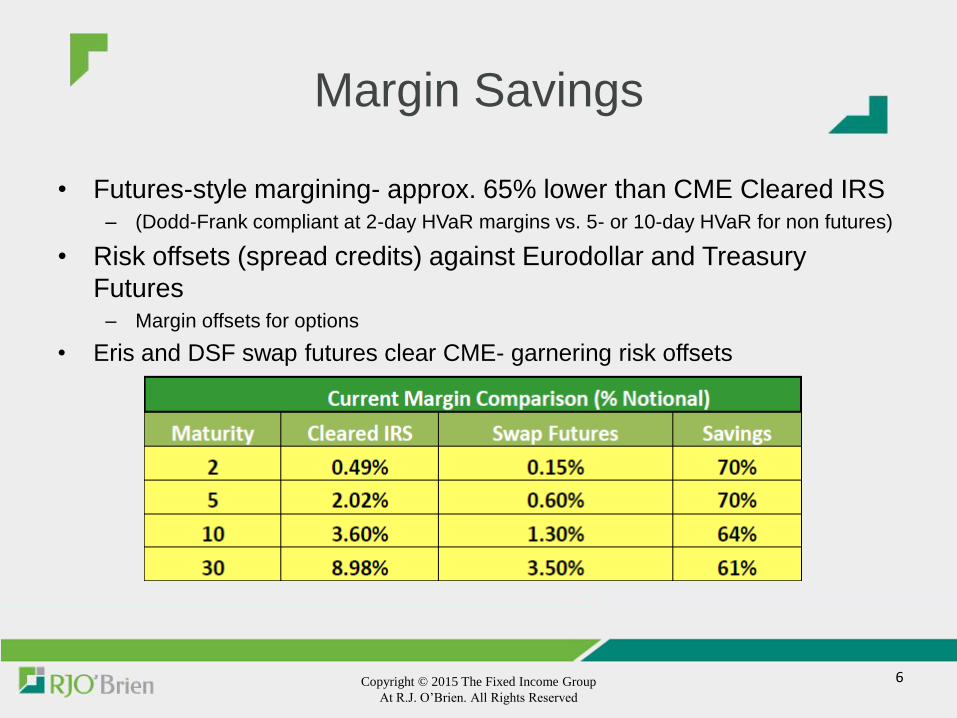

Margin Savings

• Futures-style margining- approx. 65% lower than CME Cleared IRS – (Dodd-Frank compliant at 2-day HVaR margins vs. 5- or 10-day HVaR for non futures)

• Risk offsets (spread credits) against Eurodollar and Treasury

Futures – Margin offsets for options

• Eris and DSF swap futures clear CME- garnering risk offsets

6 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

Eurodollar Futures

Packs and Bundles

• The simultaneous purchase or sale of a consecutive series of Eurodollar

contracts in equal proportions

7 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

Underlying Eurodollar Time Deposit having a principal value of USD $1,000,000 with a three-month maturity. 3-month LIBOR Rate

Contract Size Notional Amount: $1,000,000. $25 per tick ($1,000,000 x (90/360) = $25).

Minimum Price Quoted in IMM Index Points. One-quarter of one basis point.

Price Fluctuation (Tick) (0.0025 = $6.25 per contract) in the nearest expiring contract month. One-half of one basis point (0.005 = $12.50 per contract) in all other contract months.

Contract Months March, June, September and December extending out 10 years (total of 40 contracts). Plus the four nearest serial expirations (months that are not in the March quarterly cycle).

Bloomberg Symbols EDA CMDTY CT <GO> EDSF <GO> MPAK <GO>

Last Trading Day IMM Dated. Second London bank business day prior to the third Wednesday of the contract month.

Final Settlement Cash settlement to 100 minus the British Bankers’ Association survey of 3-month LIBOR. Final settlement price will be rounded to four decimal places, equal to 1/10,000 of a percent, or $0.25 per contract.

Trading Hours CME Globex Electronic Markets: 6:00 p.m. to 5:00 p.m. ET Sunday – Friday

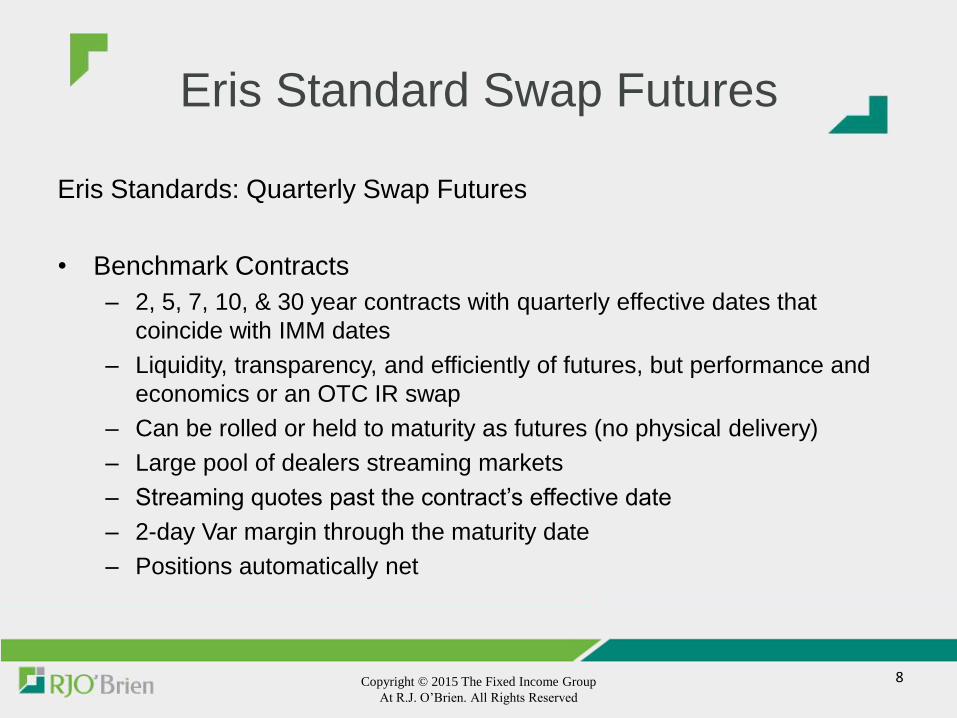

Eris Standard Swap Futures

Eris Standards: Quarterly Swap Futures

• Benchmark Contracts

– 2, 5, 7, 10, & 30 year contracts with quarterly effective dates that

coincide with IMM dates

– Liquidity, transparency, and efficiently of futures, but performance and

economics or an OTC IR swap

– Can be rolled or held to maturity as futures (no physical delivery)

– Large pool of dealers streaming markets

– Streaming quotes past the contract’s effective date

– 2-day Var margin through the maturity date

– Positions automatically net

8 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

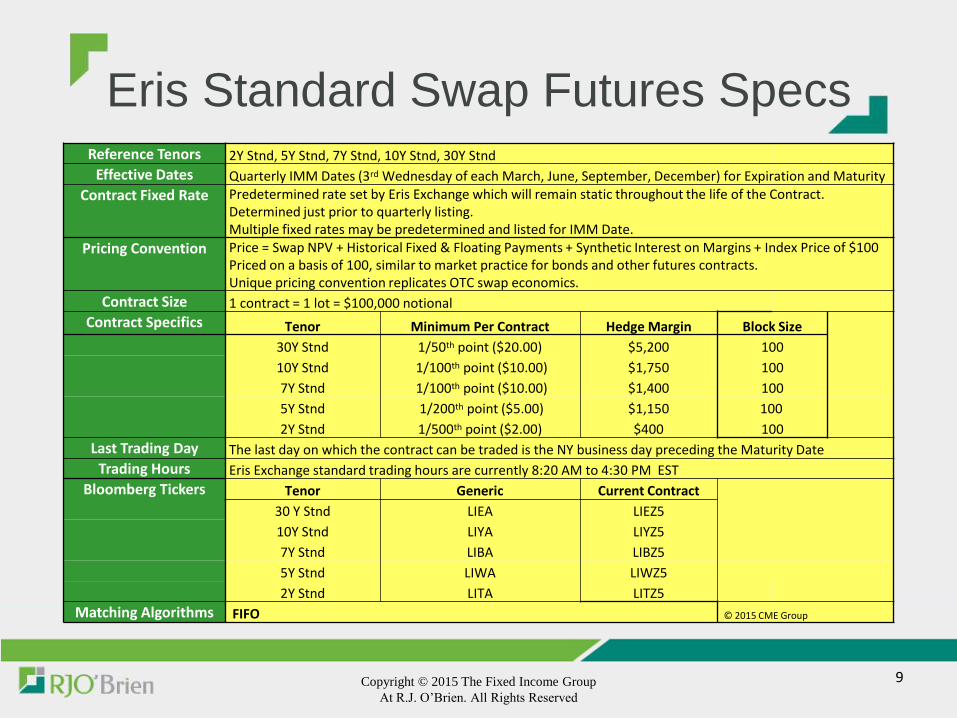

Eris Standard Swap Futures Specs

9 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

Reference Tenors 2Y Stnd, 5Y Stnd, 7Y Stnd, 10Y Stnd, 30Y Stnd

Effective Dates Quarterly IMM Dates (3rd Wednesday of each March, June, September, December) for Expiration and Maturity

Contract Fixed Rate Predetermined rate set by Eris Exchange which will remain static throughout the life of the Contract. Determined just prior to quarterly listing. Multiple fixed rates may be predetermined and listed for IMM Date.

Pricing Convention Price = Swap NPV + Historical Fixed & Floating Payments + Synthetic Interest on Margins + Index Price of $100 Priced on a basis of 100, similar to market practice for bonds and other futures contracts. Unique pricing convention replicates OTC swap economics.

Contract Size 1 contract = 1 lot = $100,000 notional

Contract Specifics Tenor Minimum Per Contract Hedge Margin Block Size

30Y Stnd 1/50th point ($20.00) $5,200 100

10Y Stnd 1/100th point ($10.00) $1,750 100

7Y Stnd 1/100th point ($10.00) $1,400 100

5Y Stnd 1/200th point ($5.00) $1,150 100

2Y Stnd 1/500th point ($2.00) $400 100

Last Trading Day The last day on which the contract can be traded is the NY business day preceding the Maturity Date

Trading Hours Eris Exchange standard trading hours are currently 8:20 AM to 4:30 PM EST

Bloomberg Tickers Tenor Generic Current Contract

30 Y Stnd LIEA LIEZ5

10Y Stnd LIYA LIYZ5

7Y Stnd LIBA LIBZ5

5Y Stnd LIWA LIWZ5

2Y Stnd LITA LITZ5

Matching Algorithms FIFO © 2015 CME Group

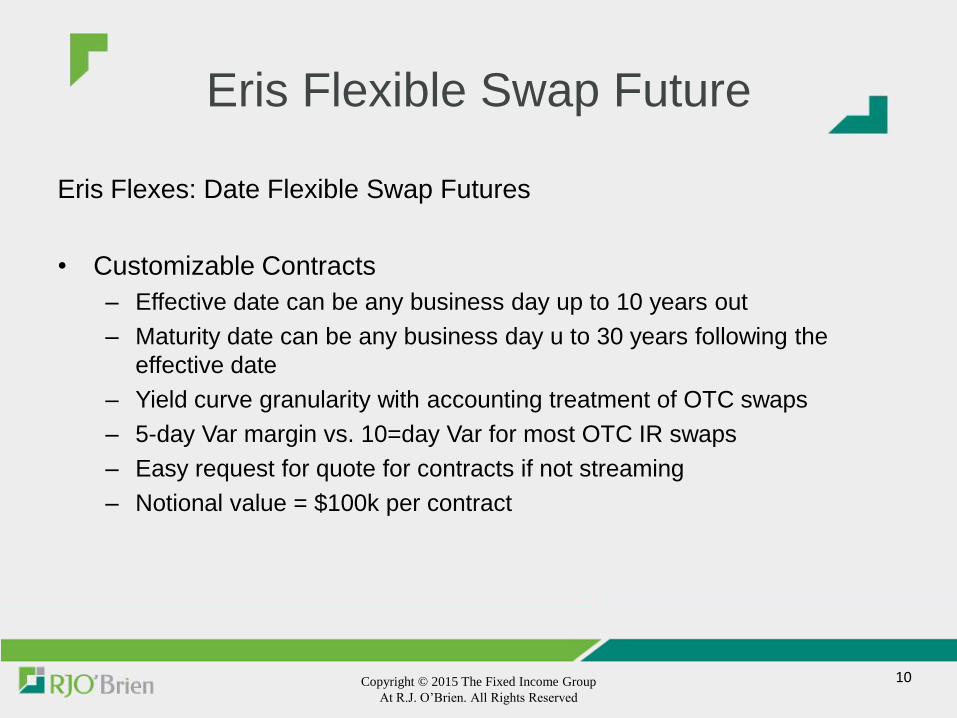

Eris Flexible Swap Future

Eris Flexes: Date Flexible Swap Futures

• Customizable Contracts

– Effective date can be any business day up to 10 years out

– Maturity date can be any business day u to 30 years following the

effective date

– Yield curve granularity with accounting treatment of OTC swaps

– 5-day Var margin vs. 10=day Var for most OTC IR swaps

– Easy request for quote for contracts if not streaming

– Notional value = $100k per contract

10 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

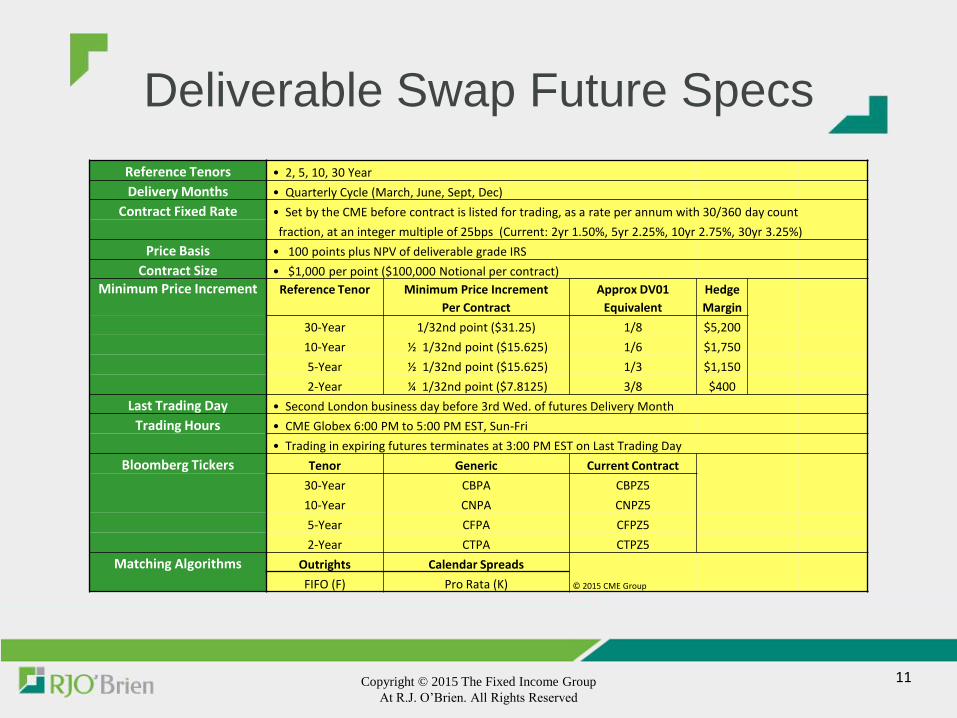

Deliverable Swap Future Specs

11 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

Reference Tenors • 2, 5, 10, 30 Year

Delivery Months • Quarterly Cycle (March, June, Sept, Dec)

Contract Fixed Rate • Set by the CME before contract is listed for trading, as a rate per annum with 30/360 day count

fraction, at an integer multiple of 25bps (Current: 2yr 1.50%, 5yr 2.25%, 10yr 2.75%, 30yr 3.25%)

Price Basis • 100 points plus NPV of deliverable grade IRS

Contract Size • $1,000 per point ($100,000 Notional per contract)

Minimum Price Increment Reference Tenor Minimum Price Increment Approx DV01 Hedge

Per Contract Equivalent Margin

30-Year 1/32nd point ($31.25) 1/8 $5,200

10-Year ½ 1/32nd point ($15.625) 1/6 $1,750

5-Year ½ 1/32nd point ($15.625) 1/3 $1,150

2-Year ¼ 1/32nd point ($7.8125) 3/8 $400

Last Trading Day • Second London business day before 3rd Wed. of futures Delivery Month

Trading Hours • CME Globex 6:00 PM to 5:00 PM EST, Sun-Fri

• Trading in expiring futures terminates at 3:00 PM EST on Last Trading Day

Bloomberg Tickers Tenor Generic Current Contract

30-Year CBPA CBPZ5

10-Year CNPA CNPZ5

5-Year CFPA CFPZ5

2-Year CTPA CTPZ5

Matching Algorithms Outrights Calendar Spreads

FIFO (F) Pro Rata (K) © 2015 CME Group

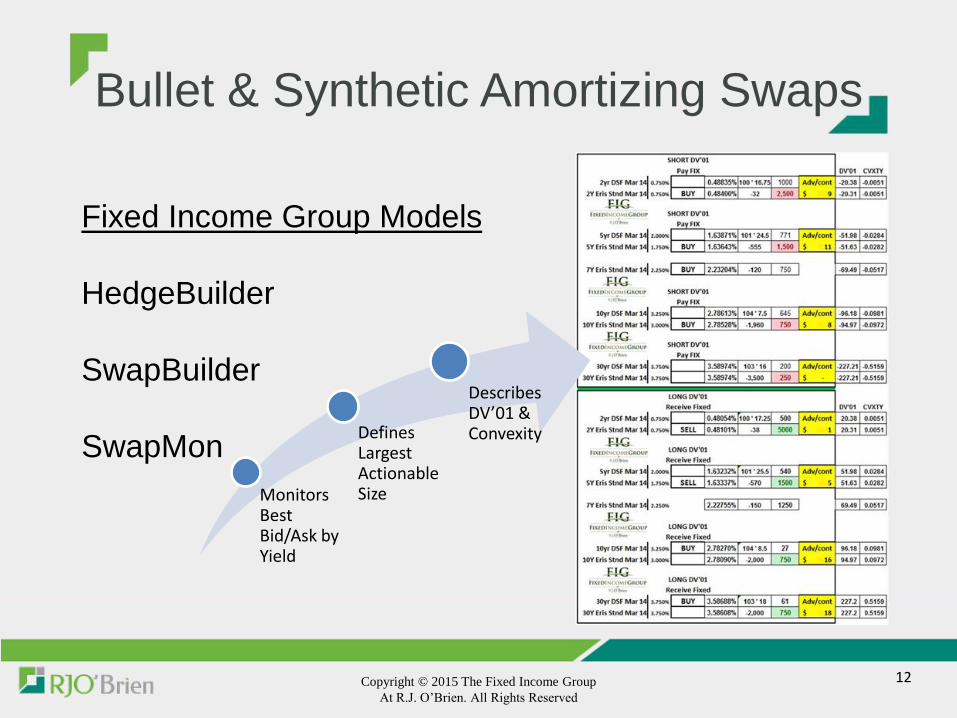

Bullet & Synthetic Amortizing Swaps

12 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

Fixed Income Group Models

HedgeBuilder

SwapBuilder

SwapMon

Monitors Best Bid/Ask by Yield

Defines Largest Actionable Size

Describes DV’01 & Convexity

HedgeBuilder: ED$-Based Swap Replication Software

Cash Flow and

Balance-Based

Eurodollar Strip

Construction

Liability-Side

Accounting

Description

Live Feed

Excel Platform

13 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

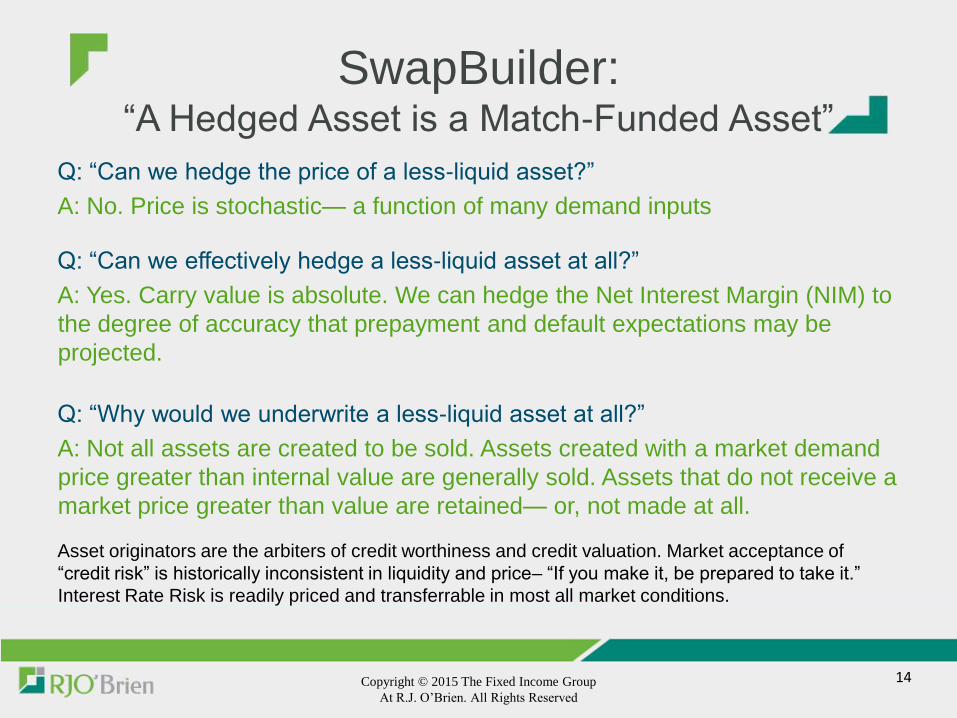

SwapBuilder: “A Hedged Asset is a Match-Funded Asset”

Q: “Can we hedge the price of a less-liquid asset?”

A: No. Price is stochastic— a function of many demand inputs

Q: “Can we effectively hedge a less-liquid asset at all?”

A: Yes. Carry value is absolute. We can hedge the Net Interest Margin (NIM) to

the degree of accuracy that prepayment and default expectations may be

projected.

Q: “Why would we underwrite a less-liquid asset at all?”

A: Not all assets are created to be sold. Assets created with a market demand

price greater than internal value are generally sold. Assets that do not receive a

market price greater than value are retained— or, not made at all.

Asset originators are the arbiters of credit worthiness and credit valuation. Market acceptance of

“credit risk” is historically inconsistent in liquidity and price– “If you make it, be prepared to take it.”

Interest Rate Risk is readily priced and transferrable in most all market conditions.

14 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

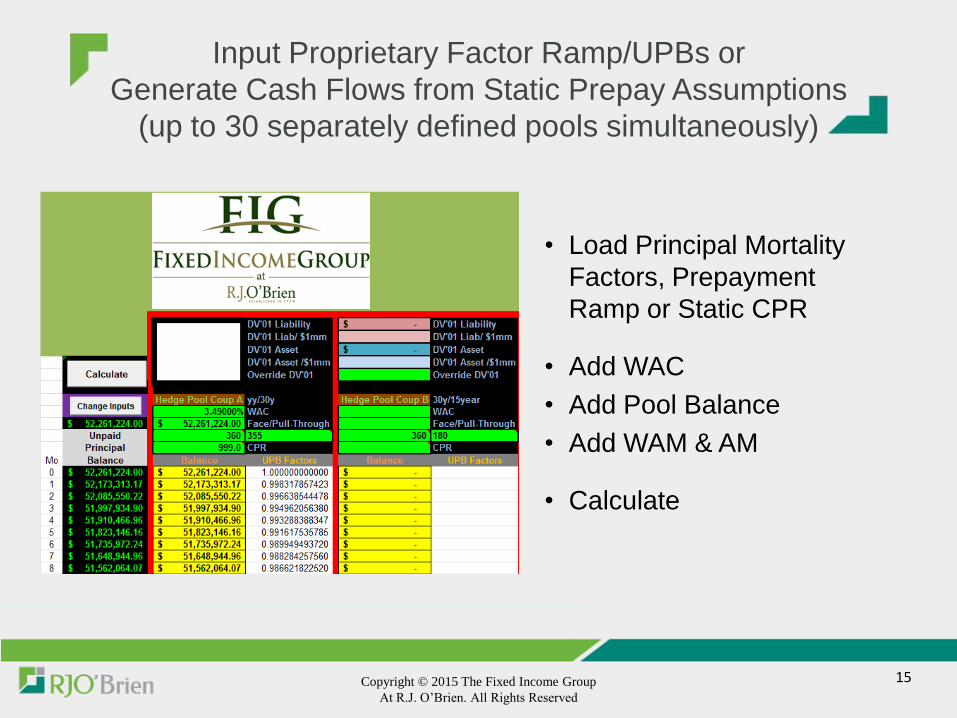

Input Proprietary Factor Ramp/UPBs or

Generate Cash Flows from Static Prepay Assumptions

(up to 30 separately defined pools simultaneously)

• Load Principal Mortality

Factors, Prepayment

Ramp or Static CPR

• Add WAC

• Add Pool Balance

• Add WAM & AM

• Calculate

15 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

The Fixed Income Group maintains a vital “best-ex” presence on the trading floor to complement electronic execution for amortizing Eurodollar strips.

“Value” attributes of the pool are calculated:

Max Value at Market

Max Net Interest Margin (NIM) Present Value

Risk attributes of the loan pool are calculated and analyzed monthly

Partial/Monthly interest rate sensitivities for both liability and asset generated

Other hedge performance (Convexity, PAI, etc) attributes are imparted

Input Proprietary Factor Ramp/UPBs or Generate Cash Flows from Static Prepay Assumptions

(up to 30 separately defined pools simultaneously)

16 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

Behind The Scenes- Risk Reversal

Hedge alternatives are cascaded through multiple optimization

routines

Best-Fit interest rate neutralization and synthetic match funding are

generated

Last Trade, Mid, Bid or Ask market levels (user defined) are

rechecked and final hedge amortization is defined

Real-time data and yield curve levels pulled through Bloomberg™ API

17 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

Risk & Required Hedge Output

Existing Risk Defined

Existing Hedge Defined

Best Fit Hedge/Adjusted Defined

Required Transaction to

Neutralize to Best Fit Defined

Graphic Presentation to Illustrate

Excess Yield Curve Exposure

Numerical Risk Figures For

Loan Pool

DV’01 Hedge Contribution for

Each LIBOR Futures Position

18 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

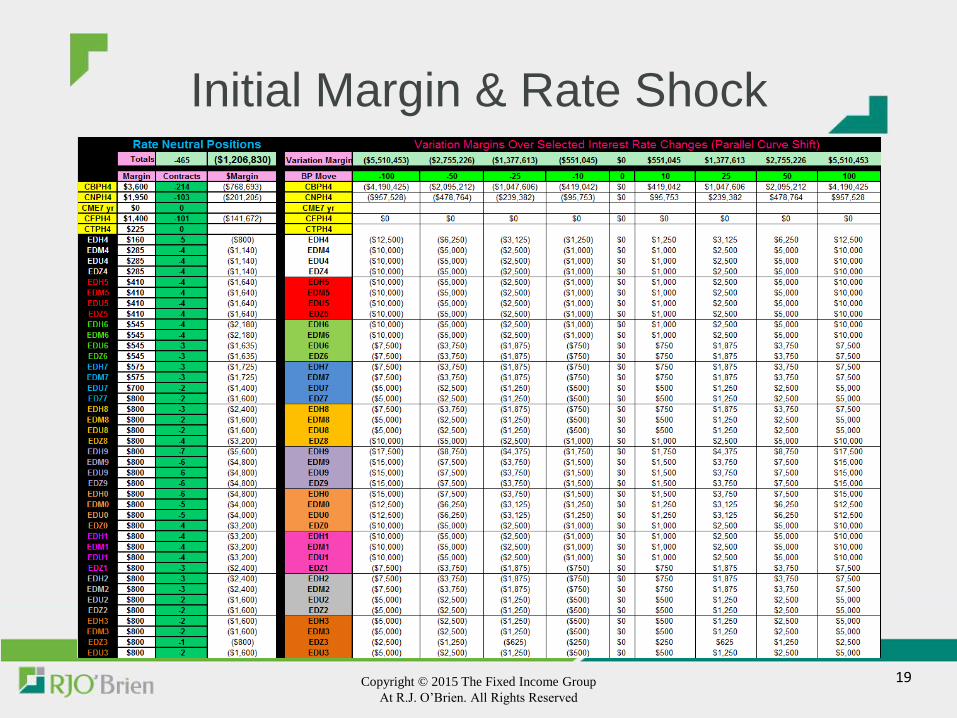

Initial Margin & Rate Shock

19 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

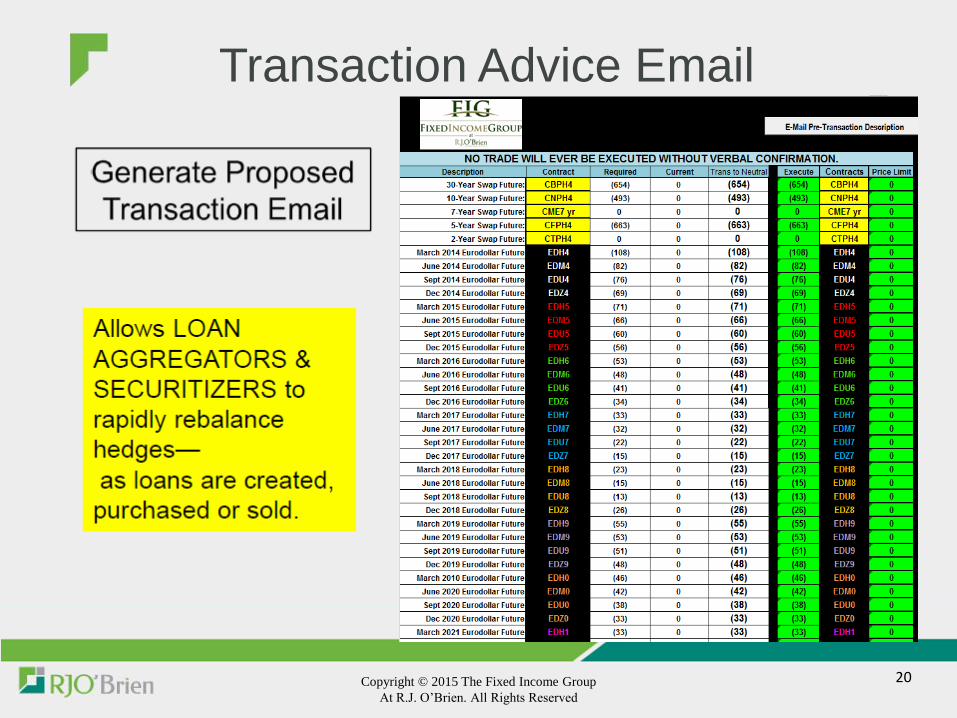

Transaction Advice Email

20 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

About R.J. O’Brien

• RJO has the size, resources and experience that you need in a global FCM.

– We are the 11th largest FCM in the United States as measured by Segregated Assets

• RJO has vast expertise across many markets.

– Agricultural Products

– Fixed Income

– Energies

– Metals

• Client Service is at the core of who we are.

– Unparalleled willingness and ability to provide customized solutions to our clients.

– High tech support throughout the life of the relationship for vetting new opportunities, strategic planning, and conflict resolution.

• Collaborative approach to risk management

– Working with RJO provided systems and staff to understand the entire picture, not just what the numbers present on the surface.

• RJO does not have a proprietary trading unit, eliminating the potential for conflicts.

21 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

FIG – The Fixed Income Group

• The Fixed Income Group unified in 1997 at R.J. O’Brien.

• Our service is solely directed to institutional clients.

• Using exchange-traded futures and options, we design, execute, and clear hedge and derivative solutions at the request of our clients and the perceived needs of the industry.

• Current focus is motivated by Dodd-Frank mandates that necessitate traditional effectiveness but emphasize margin and compliance efficiency.

• FIG’s proprietary swap futures software optimizes for margin minimization, convexity maximizations, as well as arbitrage opportunities between the new Deliverable Swap Futures, Eris Swap Futures, and Eurodollar-based synthetic interest rate swap positions.

• Historically we focus on assets, portfolios, and businesses with significant non-linear risk profiles/asymmetric behavior and leverage: mortgage derivatives, adjustable rate mortgages, Jumbo, Alt-A & non-conforming credit, MSRs, IO, ABS, equipment leasing, structured financing/repo, vega immunization, synthetic swap/cap/floor/swaptions, rate lock…

• The FIG maintains a vital best-execution presence on the trading floor to handle option arbitrage, inter-market spreads and weighted “tailing” strategies –transactions that routinely result in less-efficient execution on electronic platforms.

22 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

The Company Segregation of Customer Funds

• RJO does not engage in proprietary trading. The firm operates as an agency model

brokerage company which focuses all resources squarely on customers.

• Through our entire history, RJO has maintained proper segregation of all client

assets. In fact, we currently carry approximately $190 million in excess of what is

required by the Commodity Exchange Act.

• RJO invests customer assets within the guidelines of CFTC Rule 1.25 and in many

cases are even more conservative than the rule states.

• When customer segregated funds are deposited with a banking institution, the bank

signs a written acknowledgment stating it will not use the funds for anyone other than

the customer. RJO’s segregated customer funds are deposited principally at Harris

Bank, Wells Fargo, Fifth Third Bank, JPMorgan, and the various exchanges on which

RJO transacts business.

23 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

Contact Information

Chicago Office 800.367.3349

Corrine Abele [email protected]

John Coleman [email protected]

Rob Powell [email protected]

Brian Rachwalski [email protected]

Dan Sobolewski [email protected]

Evan Vollman [email protected]

Sacramento Office 312.286.0491

Jeff Bauman [email protected]

Chicago Floor 800.367.3650

Rocco Chierici [email protected]

Rich Goldblatt [email protected]

24 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien and is, or is in the nature of, a solicitation.

This material is not a research report prepared by R.J. O’Brien’s Research Department. By accepting this communication, you agree that you

are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely

solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS

COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR

RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE

PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD

NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable

investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading

advice is based on information taken from trades and statistical services and other sources that R.J. O’Brien believes are reliable. We do not

guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith

judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades.

Disclaimer

25 Copyright © 2015 The Fixed Income Group

At R.J. O’Brien. All Rights Reserved

Top Related