Languages

Pages

Legal

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 1/50

NEGOTIABLE

INSTRUMENTSACT,1881

SUBMITTED TO:

Dr.KAMLESH BAJAJMADE BY:

1.GINNI CHHABRA {4158}

2.BANDANA PETWAL {4166}

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 2/50

INTRODUCTION ………….

In India, there is reason to believe that instrument to exchange were in use fromearly times and we find that papers representing money were introducing into thecountry by one of the Mohammedan sovereigns of Delhi in the early part of the

fourtheenth century.Before the enactment of the Negotiable Instrument Act, 1881, the law of negotiable

instruments as prevalent in England was applied by the Courts in India. When thenparties were Hindu or Mohammedans, their personal law was held to apply. Thoughneither the law books of Hindu nor those of Mohammedans contain any reference tonegotiable instruments as such, the customs prevailing among the merchants of therespective community were recognised by the courts and applied to the transactions

among them. During the course of time there had developed in the country a strongbody of usage relating to hundis, which even the Legislature could not withouthardship to Indian bankers and merchants ignore. In fact, the Legislature felt the

strength of such local usages and though fit to exempt them from the operation ofthe Act with a proviso that such usage may be excluded altogether by appropriate

words. In the absence of any such customary law, the principles derived from English

law were applied to the Indians as rules of equity justice and good conscience.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 3/50

History of

Negotiable Instruments Act

The history of the present Act is a long one. The Act was originallydrafted in 1866 by the India Law Commission and introduced inDecember, 1867 in the Council and it was referred to a SelectCommittee. Objections were raised by the mercantile community tothe numerous deviations from the English Law which it contained.The Bill had to be redrafted in 1877. After the lapse of a sufficient

period for criticism by the Local Governments, the High Courts andthe chambers of commerce, the Bill was revised by a SelectCommittee. In spite of this Bill could not reach the final stage. In1880 by the Order of the Secretary of State, the Bill had to bereferred to a new Law Commission. On the recommendationof the new Law Commission the Bill was re-drafted and again itwas sent to a Select Committee which adopted most of theadditions recommended by the new Law Commission. The draftthus prepared for the fourth time was introduced in the Council andwas passed into law in 1881 being the Negotiable Instruments Act,1881 (26 of 1881)

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 4/50

Meaning of

Negotiable Instruments

There are certain documents used for payment in businesstransactions and are transferred freely from one person toanother. Such documents are called Negotiable Instruments.Thus, we can say negotiable instrument is a transferabledocument, where negotiable means transferable and instrumentmeans document. To elaborate it further, an instrument, asmentioned here, is a document used as a means for makingsome payment and it is negotiable i.e., its ownership can beeasily transferred.

Thus, negotiable instruments are documents meant for making

payments, the ownership of which can be transferred from oneperson to another many times before the final payment is made.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 5/50

Definition of

Negotiable InstrumentAct , 1881

According to section 13 of the Negotiable Instruments Act,

1881, a negotiable instrument means “promissory note, bill

of exchange, or cheque, payable either to order or to

bearer”.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 6/50

Types of Negotiable Instruments

NEGOTIABLE

INSTRUMENTS

PROMISSORY

NOTE

BILL

OF

EXCHANGE

CHEQUE

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 7/50

Types of

Negotiable Instruments

ON BASIS OF

CUSTOM

&

USAGE

HUNDITREASURY

BILLS

SHARE

WARRANTS

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 8/50

PROMISSORY NOTE

Definition of promissory note ….

Under Section 4 of the Negotiable instruments

Act, 1881 defines a promissory note as ‘an

instrument in writing (not being a bank note or

a currency note) containing an unconditional

undertaking, signed by the maker, to pay a

certain sum of money only to or to the order of a certain person or to the bearer of the

instrument’

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 9/50

Specimen of a

promissory note

s. 5000/- Pune November 25, 2008

Three moths after the date, I promise to pay Mr. X of Mumbai or

order a sum of Rupees Fifty Thousand for value received.

To

Mr.

Address………..

…………… Stamp

Mumbai Signature of Mr Y

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 10/50

Parties to a Promissory Note

There are primarily twoparties involved in apromissory note. They

are:-i. The Maker orDrawer : The personwho makes the noteand promises to paythe amount statedtherein.

ii. The Payee : Theperson to whom the

amount is payable.

In course of transfer of apromissory note bypayee and others, theparties involved may be:-

i. The Endorser : Theperson who endorsesthe note in favour of

another person.

ii. The Endorsee : Theperson in whose favourthe note is negotiated

by endorsement.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 11/50

Features of a

promissory note

1. A promissory note must be in writing, duly signedby its maker and properly stamped as per Indian

Stamp Act.2. It must contain an undertaking or promise to pay.

Mere acknowledgement of indebtedness is notenough.

3. The promise to pay must not be conditional.

4. It must contain a promise to pay money only.

5. The parties to a promissory note, i.e. the maker andthe payee must be certain.

6. A promissory note may be payable on demand or

after a certain date.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 12/50

BILL OF EXCHANGE

Section 5 of the Negotiable Instruments Act, 1881

defines a bill of exchange as „an instrument inwriting containing an unconditional order, signedby the maker, directing a certain person to pay acertain sum of money only to or to the order of a

certain person, or to the bearer of the instrument‟

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 13/50

Specimen of a Bill of Exchange

Rs.10,000/- Bangalore

07-04-2005

Six months after date pay to “X” or order the sum ofRupees Ten Thousand Only for value received.

To “S” Nitte Institute of Technology

Yelahanka.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 14/50

Parties to a

Bill of Exchange

There are three parties involved in a bill ofexchange.

• The Drawer : The person who makes the order for

making payment.• The Drawee : The person to whom the order to pay is

made.He is generally a debtor of the drawer.• The Payee : The person to whom the payment is to

be madeThe drawer can also draw a bill in his own

name thereby he himself becomes the payee. Herethe words in the bill would be Pay to us or order.In a bill where a time period is mentioned it is calleda Time Bill. But a bill may be made payable ondemand also. This is called a Demand Bill.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 15/50

Features of a

bill of exchange

i. A bill must be in writing, duly signed by itsdrawer, accepted by its drawee and properlystamped as per Indian Stamp Act.

ii. It must contain an order to pay. Words like„please pay Rs 5,000/- on demand and oblige‟are not used.iii. The order must be unconditional. iv. The order must be to pay money and moneyalone.v. The sum payable mentioned must be certainor capable of being made certain.vi. The parties to a bill must be certain.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 16/50

CHEQUE

The Negotiable Instruments Act, 1881 defines acheque “as a bill of exchange drawn on aspecified banker and not expressed to bepayable otherwise than on demand”. Actually, a

cheque is an order by the account holder of thebank directing his banker to pay on demand, thespecified amount, to or to the order of the personnamed therein or to the bearer .Cheque is a verycommon form of negotiable instrument.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 17/50

Specimen of a Cheque

07-04-2005

PAY “s”_ _______________________________

____________________________________________OR BEARER

RUPEES TEN THOUSAND ONLY-----------------------------------------------

UTI BANK LTD.

YELAHANKA ___________________

(Signature of the Account Holder)

Rs. 10,000/-

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 18/50

Features of a cheque

i. A cheque must be in writing and duly signed bythe drawer.

ii. It contains an unconditional order.iii. It is issued on a specified banker only.

iv. The amount specified is always certain and mustbe clearly mentioned both in figures and words.

v. The payee is always certain.vi. It is always payable on demand.

vii. The cheque must bear a date otherwise it isinvalid and shall not be honoured by the bank.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 19/50

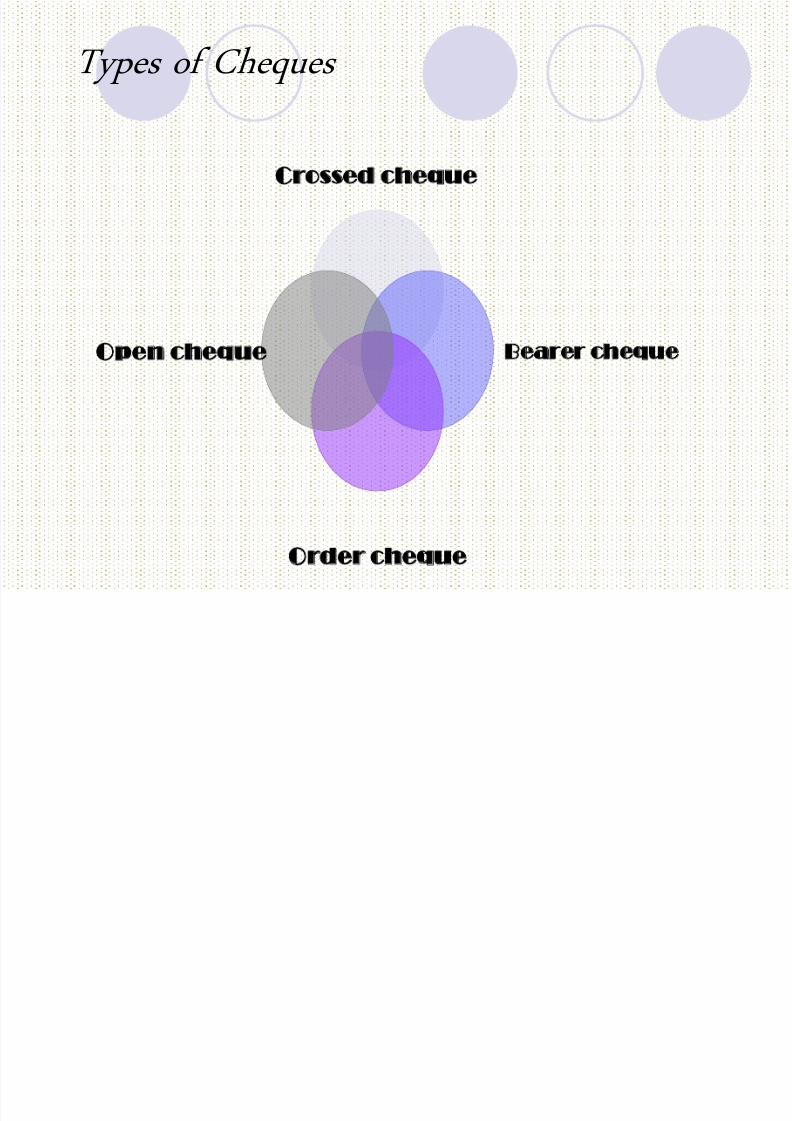

Types of Cheques

Crossed cheque

Bearer cheque

Order cheque

Open cheque

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 20/50

Types of Cheque

a) Open cheque : A cheque is called„Open‟ when it is possible to getcash over the counter at the bank.

b) Crossed cheque: Since opencheque is subject to risk of theft, itis dangerous to issue suchcheques. This risk can be avoidedby issuing another types ofcheque called „Crossed cheque‟.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 21/50

Continued………..

c) Bearer cheque: A cheque which is payable toany person who presents it for payment at thebank counter is called „Bearer cheque‟. A bearer

cheque can be transferred by mere delivery andrequires no endorsement.

d) Order cheque: An order cheque is one whichis payable to a particular person. In such a

cheque the word „bearer‟ may be cut out orcancelled and the word „order‟ may be written.The payee can transfer an order cheque tosomeone else by signing his or her name on theback of it.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 22/50

There is another

categorization of cheques :-

1. Ante-dated cheques:- Cheque in which the drawer mentionsthe date earlier to the date of presenting if for payment.

2. Stale Cheque:- A cheque which is issued today must bepresented before at bank for payment within a stipulatedperiod. After expiry of that period, no payment will be madeand it is then called „stale cheque‟.

3. Mutilated Cheque:- In case a cheque is torn into two or more

pieces and presented for payment , such a cheque is called amutilated cheque. The bank will not make payment againstsuch a cheque without getting confirmation of the drawer. But ifa cheque is torn at the corners and no material fact is erased orcancelled, the bank may make payment against such acheque.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 23/50

4. Post-dated Cheque:- Cheque on which drawer mentions a

date which is subsequent to the date on which it ispresented, is called post-dated cheque.

For example, if a cheque presented on 8 th May 2003 bearsa date of 25 th May 2003, it is a post-dated cheque.The

bank will make payment only on or after 25 th May 2003.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 24/50

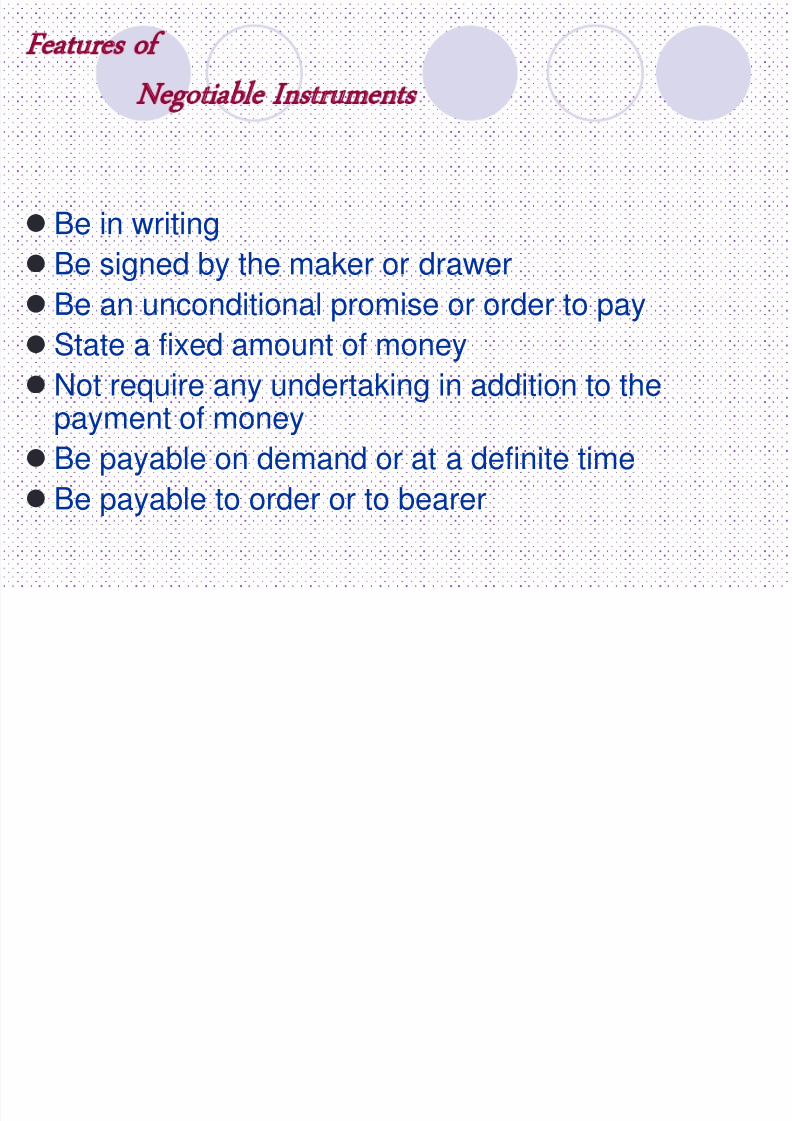

Features of

Negotiable Instruments

Be in writing

Be signed by the maker or drawer Be an unconditional promise or order to pay

State a fixed amount of money

Not require any undertaking in addition to the

payment of money Be payable on demand or at a definite time

Be payable to order or to bearer

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 25/50

Holder in due course

"Holder in due course" means any person who

for consideration became the possessor of apromissory note, bill of exchange or cheque ifpayable to bearer, or the payee or indorsethereof, if [payable to order] before theamount mentioned in it became payable,

and without having sufficient cause to believethat any defect existed in the title of theperson from whom he derived his title.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 26/50

Privileges of a

Holder in due course

1. He gets a better title than the Transferor.

2. Privilege in case of Inchoate stampedinstruments.

3. Liability of prior parties.

4. Privilege in case of fictitious bills.

5. Privilege when an instrument delivered

conditionally is negotiated.6. Estoppel against denying original validityof instrument.

7. Estoppel against denying capacity of the

payee to indorse.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 27/50

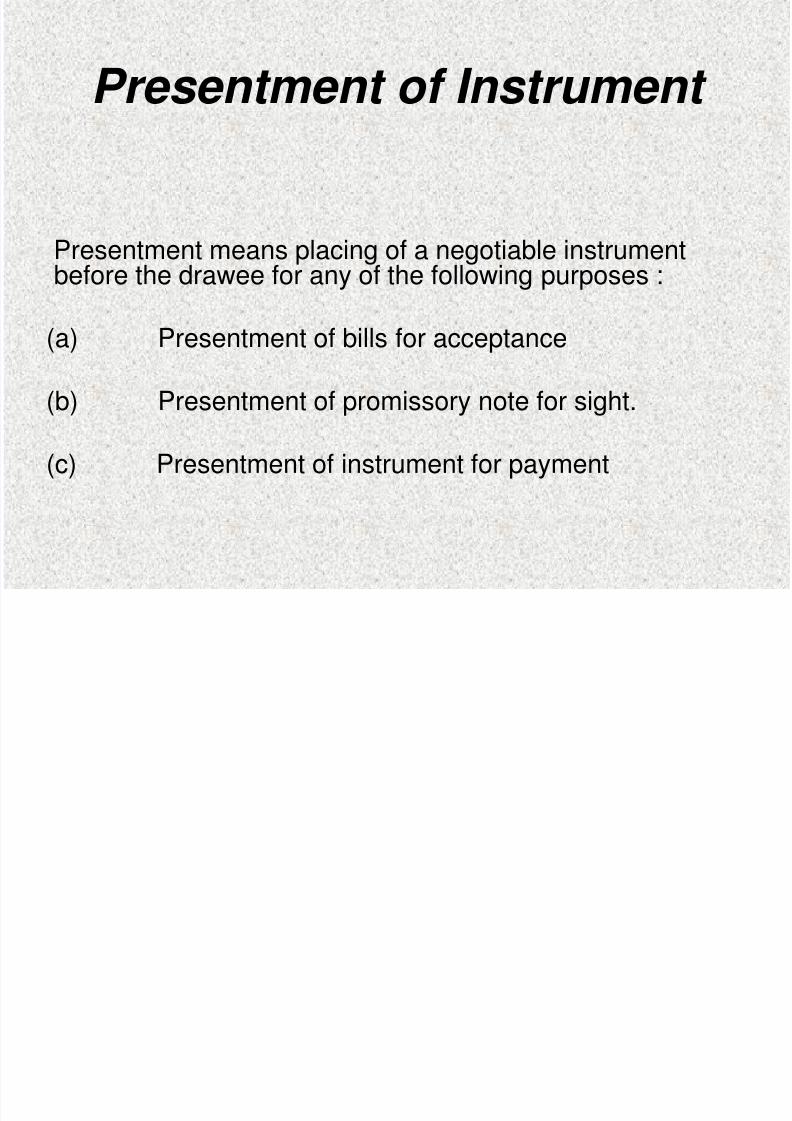

Presentment of Instrument

Presentment means placing of a negotiable instrument

before the drawee for any of the following purposes :

(a) Presentment of bills for acceptance

(b) Presentment of promissory note for sight.

(c) Presentment of instrument for payment

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 28/50

Place of presentment

The bill should be presented eitherat the residence or at the normalplace of business of the draweeunless some other place has beenspecified in the bill.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 29/50

Time for presentment

Time for presentment of the instrument may be dividedinto following categories :

a.Where the presentment is optional the bill may be presented at anytime before the time for payment.

b.Where the time has been specified in the bill for presentment in the bill, it shall be presented within the specified time.

c.In case of bill payable after sight, if no time is specifiedtherein for presentment for acceptance, it shall be presented within a reasonable time after it is drawn.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 30/50

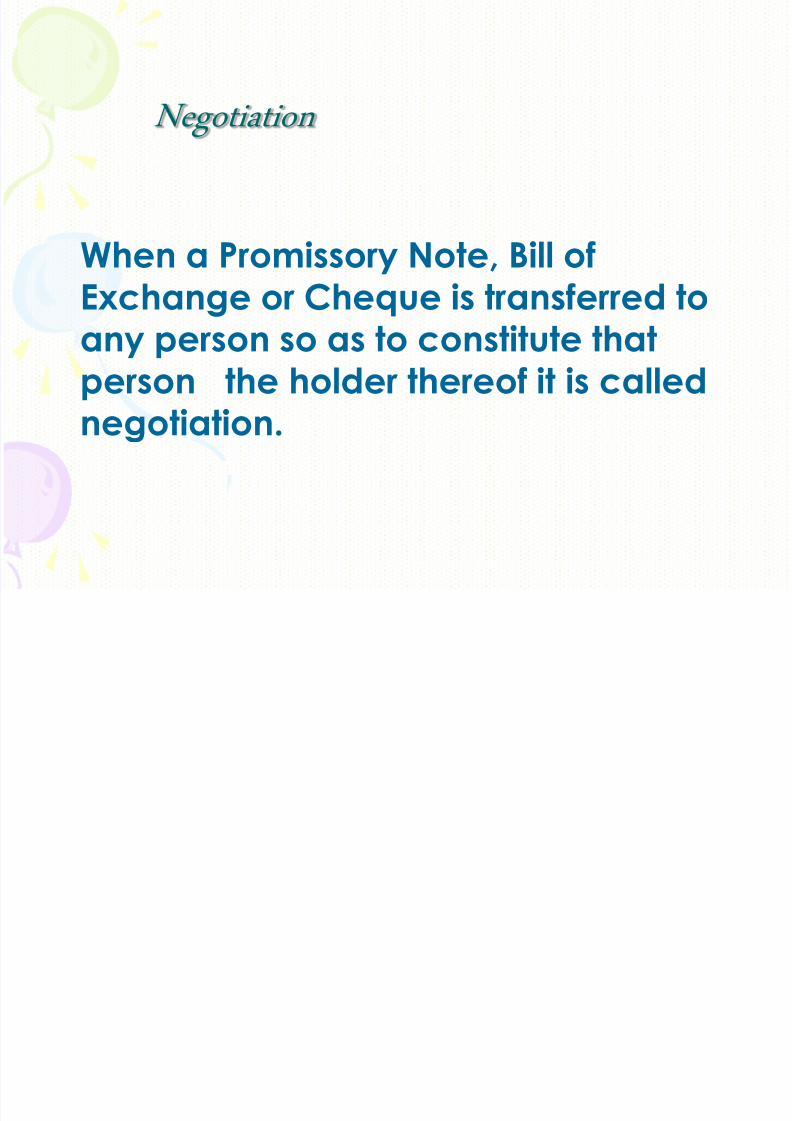

Negotiation

When a Promissory Note, Bill ofExchange or Cheque is transferred toany person so as to constitute thatperson the holder thereof it is called

negotiation.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 31/50

Presumptions about

Negotiable Instruments

Until contrary is proved, presumptions are:

1. It has consideration.

2. Date is as shown/seen on the instrument.

3. Time of acceptance – within reasonable time.

4. Order of endorsement – as seen apparently on theinstrument.

5. Stamp – properly paid, in case of lost instrument.

6. Holder is in due course.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 32/50

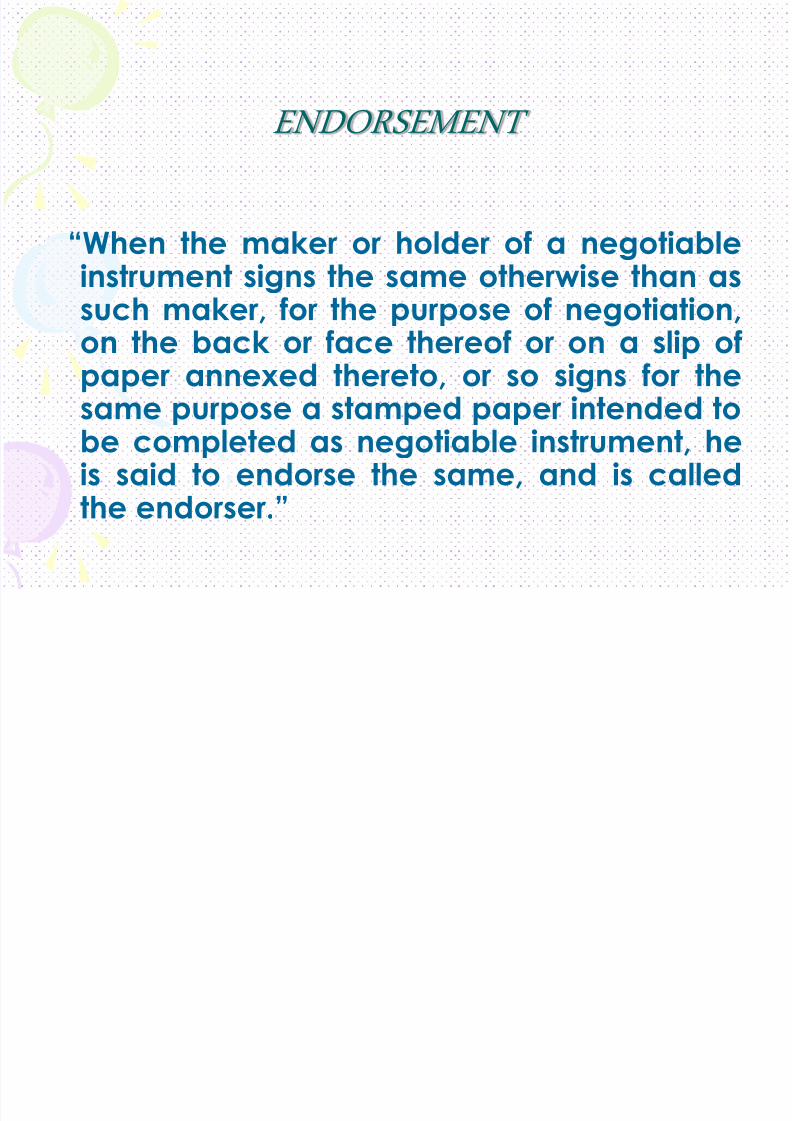

ENDORSEMENT

“When the maker or holder of a negotiable

instrument signs the same otherwise than assuch maker, for the purpose of negotiation,on the back or face thereof or on a slip ofpaper annexed thereto, or so signs for the

same purpose a stamped paper intended tobe completed as negotiable instrument, heis said to endorse the same, and is calledthe endorser.”

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 33/50

Types of Endorsement

General or blank endorsement -

Endorser signs his name either on theback or face of the instrument.

Full or special endorsement - It

specifies the name of the person towhom or to whose order thepayment must be made.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 34/50

Continued……………..

•Partial endorsement-Endorsement is

made for remaining balance ofpayment.

•Conditional endorsement-The liability

of the endorser is limited or negative.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 35/50

Discharge of Instrument

A negotiable instrument may be

discharged in any of following ways :1. By payment in due course.

2. Debtor as holder.

3. By express waiver.

4. By cancellation.

5. By material alteration or lapse of time.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 36/50

Dishonour

Section 92 of the Act reads as under –

“A promissory note, bill of exchange or cheque is said to be dishonoured by non-payment when the

maker of the note, acceptor of the bill or drawee of the cheque makes default in payment upon beingduly required to pay the same.”

If on presentation the banker does not pay thendishonour takes place and the holder acquired atonce the right of recourse against the drawer andthe other parties on the cheque.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 37/50

Dishonour of

negotiable instrument

• Negotiable instruments, Promissorynotes and Cheques may bedishonored by non payment .

• Bills of exchange may be dishonoredby non payment or by non-acceptance as they requireacceptance from drawees.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 38/50

MATURITY

Section 22 of the Negotiable Instruments Act states:-

“The maturity of a promissory note or bill of exchange is

the date at which it falls due.”

D ays of grace :-

Every promissory note or bill of exchange which is not

expressed to be payable on demand, at sight or on presentment is at maturity on the third day after the day on which it is expressed to be so payable.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 39/50

Continued……..

Negotiable instruments, except cheques, may be madepayable either on demand or on a specified date or after aspecified period of time. Cheques are always payable ondemand. The date on which a negotiable instrument falls duefor payment is the date of maturity of the instrument.

An instrument payable on demand or on sight becomepayable immediately on the date of execution and there is noquestion of its maturity. Thus, the question of maturity arisesonly in case of instruments payable otherwise than ondemand.Time instruments are given three days of grace and should bepresented for payment only on the last day of grace.

Presentment of instrument earlier than third day will bepremature. Thus, an instrument will be deemed to have beendishonoured only if it remains unpaid after the expiry of thegrace period.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 40/50

Rules for calculating maturity 1. Payable after stated number of months : If a note or bill is made

payable a specified number of months after the date or after insight,or after a certain event, it matures or becomes payable three daysafter the corresponding date of the month after the stated month. fthe month in which the instrument becomes payable does not have acorresponding date, the period shall terminate on last day of the

month.2. When made payable after stated number of days : If a note or bill is

made payable after a certain number of days after date or after sightor after a certain event, the maturity is calculated by excluding theday on which the instrument is drawn or presented for acceptance orsight or on which the event happens.

3. If grace period ends on Sunday or another holiday : If the date onwhich a bill or note is at maturity is a public holiday, the instrumentshall be deemed to be due on the next preceding business day. Thus,if the maturity falls on Sunday, it shall be deemed to be payable onSaturday.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 41/50

Payment in due course

Under Section 10 of the NegotiableInstrument Act –

“Payment in due course” means payment inaccordance with the apparent tenor of theinstruments in good faith and without negligence to any person in possessionthereof under circumstances which do not afford a reasonable ground for believingthat he is not entitled to receive payment of the amount therein mentioned.”

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 42/50

Essentials for a

Payment in Due Course

Payment on or after the maturity

Payment in cash only

Payment to a person in possession Payment in good faith

)

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 43/50

Noting

“When a promissory note or bill of exchange hasbeen dishonoured by non-acceptance or non-payment, the holder may cause such dishonour to

be noted by a notary public upon the instrument, orupon a paper attached thereto, or partly uponeach.

Such note must be made within a reasonable timeafter the dishonour, and must specify the date of

dishonour, the reason, if any, assigned for suchdishonour, or, if the instrument has not beenexpressly dishonoured, the reason why the holdertreats it as dishonoured, and the notary‟s charges”

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 44/50

Advantages of noting

1. Under section 104A, wherever protestis required to be made within a

specified time, it is sufficient if noting ismade within that time.

2. A bill of exchange may be accepted

for honour after it has been noted.3. A bill of exchange may be paid for

honour after it has been noted.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 45/50

Time for noting

As per section 105, the noting shall bemade by the notary public within a

reasonable time. It has been held thatthe noting shall take place on the day ofdishonour or not later than the next

business day unless the holder isprevented by circumstances beyond hiscontrol .

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 46/50

Protest

“When a promissory note or bill of exchangehas been dishonoured by non-acceptance or non-payment, the holder may, within a

reasonable time, cause such dishonour to benoted and certified by a notary public. Suchcertificate is called a protest.”

When an instrument is dishonoured, the holdermay cause the fact not only to be noted, but

also to be certified by a Notary Public that thebill has been dishonoured. Such a certificate isreferred to as a protest.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 47/50

Advantage of Protest

Neither noting nor protesting is compulsory in the case of inlandbills, But under Section 104 every foreign bill of exchange must beprotested for dishonour when such a protest is required by the lawof the country where the bill was drawn. The advantage of bothnoting and protesting is that this constitutes prima facie good

evidence in the Court of the fact that instrument has beendishonoured in accordance with the provisions of section 119, theCourt is bound to recognize a protest . Provisions of section 104Ashall also be noted which provide that – “For the purpose of this Act, where a bill or note is required to be protestedwithin a specified time or before some further proceeding is taken, it issufficient that the bill has been noted for protest before the expiration ofthe specified time or the taking of the proceeding; and the formal protestmay be extended at any time thereafter as of the date of noting.” Thus, where a document has been noted within the time requiredby law, legal proceeding cannot be vitiated on account of protestnot having been made.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 48/50

Contents of Protest

Section 101 provides that the protest must contain the followingparticulars :

1. The instrument itself or literal transcript of the instrument of

everything written or printed thereon.2. The name of the person for whom and against whom the

instrument has been protested.3. The fact and reasons of dishonour, i.e. a statement that

payment or acceptance or better security, as the case maybe, was demanded by the notary public from the person

concerned and he refused to give it, or did not answer, or thathe could not be found.4. The time and place of dishonour.5. The signature of the notary public.6. In the case of acceptance for honour or payment for honour,

the names of the persons by whom and for whom it is

accepted or paid.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 49/50

Hundis

A Hundi is a negotiable instrument byusage. It is often in the form of a bill ofexchange drawn in any local language inaccordance with the custom of the place.Some times it can also be in the form of apromissory note. A hundi is the oldest knowninstrument used for the purpose of transfer of

money without its actual physicalmovement. The provisions of the NegotiableInstruments Act shall apply to hundis onlywhen there is no customary rule known tothe people.

8/3/2019 Law Poject

http://slidepdf.com/reader/full/law-poject 50/50

Thank you ....….

Top Related