Languages

Pages

Legal

JasaMargaUpdate3Q2017

asofNovember2017

CompanyOverview

Companyoverview

Briefsnapshot Companyhighlights

FY2016segmentalrevenuebreakdown

• LeadingtollroadoperatorinIndonesiawithover38yearsofexperience• 31tollroadconcessionswithtotallengthof1,260km• 70%ownedbytheGovernmentofIndonesia• PublicallylistedontheIndonesiaStockExchangesince2007,witha

marketcapofc.IDR42.5trillionasat9Oct2017• Keybusiness

– ConstrucQon,operaQonandmaintenanceoftollroad

– FaciliQesconstrucQonandsupplementaryservicesinadjacentborderarea

• SupporQngbusiness/otherbusiness– TollRoadOperaQonServices(ProvidesoperaQonservicesforJasaMargaandothertoll

roadinvestors)– TollRoadMaintenanceServices(ProvidesmaintenanceservicesforJasaMargaandother

tollroadinvestor)– Property(agesrestareasandotherproperQesontollroadcorridors)

ü LargesttollroadoperatorinIndonesiawith62.2%marketshareintermsoftollroadslengths(665km)and80%marketshareoftollroadtransacQonvolume

ü ThelongestconcessionperiodholderinAsiareflecQngstableincome

ü Strategicallyimportantwithstronggovernmentownershipü Resilientindustrywithstronggovernmentfocusü Strongfinancialprofilewithpromisinggrowthgoingforward

Vision&Mision

Vision To be the largest, trusted and sustainable national toll road network company.

Mission

1. Lead thedevelopmentof toll roadnetworks inIndonesiatoincreasenaQonalconnecQvity.

2. Managethetollroadbusinessalongtheend-to-end value chain in a professional andsustainablemanner.

3. Maximize the regional development toaccelerate community advancement andincreasecompanyprofitability.

4. Enhance customer saQsfacQon through serviceexcellence

3

Other Operating Revenues 10.25%

Toll Revenue – Jasa Marga (13 old concessions in balance sheet) 80.36%

Toll Revenue - Subsidiaries 9.39%

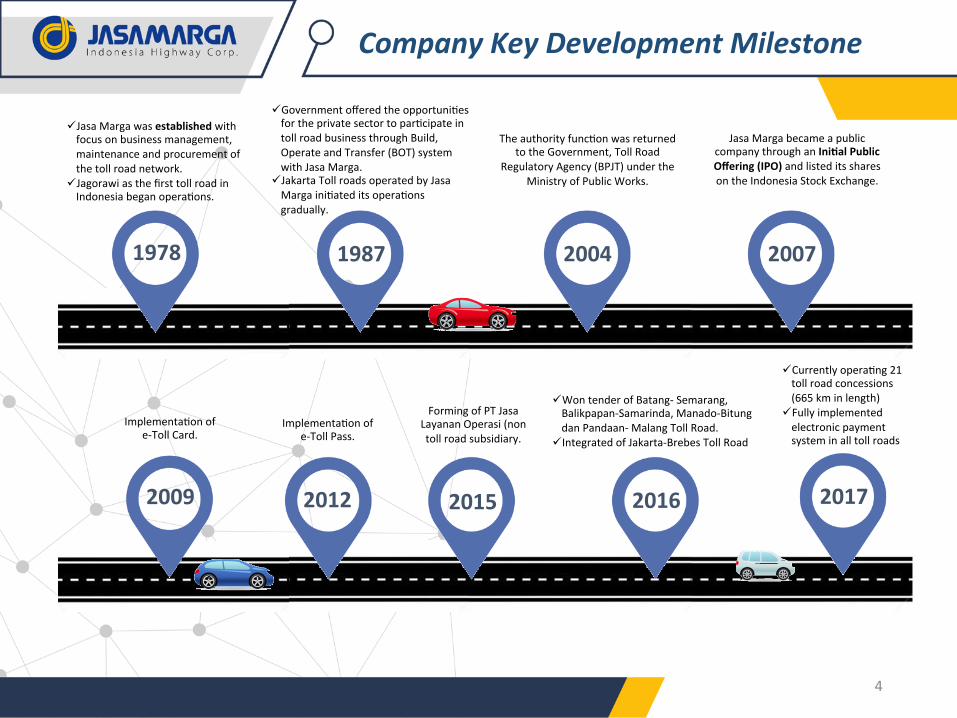

CompanyKeyDevelopmentMilestone

4

ü GovernmentofferedtheopportuniQesfortheprivatesectortoparQcipateintollroadbusinessthroughBuild,OperateandTransfer(BOT)systemwithJasaMarga.

ü JakartaTollroadsoperatedbyJasaMargainiQateditsoperaQonsgradually.

TheauthorityfuncQonwasreturnedtotheGovernment,TollRoad

RegulatoryAgency(BPJT)undertheMinistryofPublicWorks.

JasaMargabecameapubliccompanythroughanIniCalPublicOffering(IPO)andlisteditssharesontheIndonesiaStockExchange.

ü JasaMargawasestablishedwithfocusonbusinessmanagement,maintenanceandprocurementofthetollroadnetwork.

ü JagorawiasthefirsttollroadinIndonesiabeganoperaQons.

ImplementaQonofe-TollCard.

ImplementaQonofe-TollPass.

FormingofPTJasaLayananOperasi(nontollroadsubsidiary.

ü WontenderofBatang-Semarang,Balikpapan-Samarinda,Manado-BitungdanPandaan-MalangTollRoad.

ü IntegratedofJakarta-BrebesTollRoad

1978 1987 2004 2007

2009 2012 2015 2016 2017

ü CurrentlyoperaQng21tollroadconcessions(665kminlength)

ü Fullyimplementedelectronicpaymentsysteminalltollroads

CompanyStructure

GovernmentofIndonesia

(“GOI”)

MinistryofState-OwnedEnterprises

(“MSOE”)

70%

Public30%

Government 70%

Foreign 17%

Individual 1%

Domestic Institution

8%

Mutual Fund

4%

ShareholdingStructure

Currently, PT Jasa Marga (Persero) Tbk (“Company”) is owned 70% by the Government of Indonesia through Ministry of State Owned Enterprise and the remaining 30% is owned by public (both institutional and individuals).

Asof31stOct2017

1. Cawang-Tomang-Pluit2. (JakartaInnerRingRoad)3. Prof.Dr.Ir.Sedyatmo(Airport)4. Purbaleunyi5. Jakarta-Cikampek6. Palikanci7. Jagorawi8. Surabaya-Gempol9. Semarang10. JakartaOuterRingRoad11. Ulujami-PondokAren12. Jakarta-Tangerang13. Belmera

ParentLevel

5

KeyStrategy

FundingStrategyOperaCngStrategy

• TollRoadBusinessDevelopment

– AddingtollroadstoincreasethevalueoftheCompanyandtomaintaincurrentmarketleadershipintheforeseeablefuture

– Inthelongterm,aimtoconQnueoperaQngthebestqualitycommercialtollroads,differenQaQngfrom2ndlargestcompeQtor,HutamaKarya,andmaintainmajorityofmarketshareinIndonesia

• TollRoadOperaCon– OperaQngefficient,safe,andhighqualitytollroadto

improveoperaQonalperformance– Providingexcellentservicetoroadusers,community,and

government

• OtherBusinessDevelopment– Developotherbusinessesthatarestrategicallystrengthening

developmentstrategiesandoperaQonoftollroads– Increaserevenuebyleveragingtheresourcesofthe

Company

• BankLoansFacility:

Tobridgefundingneedsbeforeapproachingthecapitalmarket

• ProjectBondsinatProjectlevel:

To replace the bank loan financingwith fixed interest rateandtheprincipalpaymentinlinewiththecashflow

• Bond/SukukIssuanceatCorporatelevel:Tofinanceinvestmentfornewtollroadproject

• EquityFundRaising:Tomaintainourprofitabilityandalsoleveragingourfinancingcapacity.

• SecuriCzaCononselectedtollroad:Toleveragematureassetsfordebtfinancingwithoutincurringanyinterestburden.

6

IndustryOverview

8

OverviewoftheauthoriCesinvolved

MinistryofPublicWorks

GovernmentofIndonesia

DirectorateGeneralofhighways

IndonesianTollRoadAuthority

(BPJT)

MinistryofStateOwnedEnterprises

Privatetollroadinvestors

Concessionagreement Concessionagreement

Toll Tariff

• IniQaltolltariffiscalculatedbasedoninvestmentfeasibility,tollroaduser’sabilitytopayandvehicleoperaCngcostsaving- InvestmentfeasibilityiscalculatedbasedonesQmatedinvestmentcostand

projectedrevenueduringtermoftheconcession• IniQaltolltariffissQpulatedinconcessionagreementpriortostartof

construcCon• Tariffadjustmentisregulatedbylaw,iscalculatedbasedonregionalCPIandis

adjustedonceevery2years• IniQaltolltariffsetupandsubsequentadjustmentisdecidedbyMinisterof

PublicWorksdecree- Theministrymaypostponetariffincreasesifatollroadfailstocomplywith

minimumservicestandards

Land acquisition • LandacquisiConisgovernment’sresponsibilityandisundertakenbyland

procurementcommifeeappointedbytheGovernment• ThelandacquisiQoncomprisesfourstages:planning,preparaCon,execuCon

anddelivery- ThelawalsoregulatesadeadlineforlandacquisiQonof312toamaximum

of552workingdays• Priceisdeterminedbyindependentappraiserbasedonfairmarketprice• InvestorsmayprovidebridgefinancingforlandacquisiQoncoststospeedup

theacquisiConprocess,governmentwillrepaytheinvestorsforthelandacquisiQoncosts

104workingdays 108workingdays

72workingdays

118workingdays

74workingdays

30workingdays 60workingdays44workingdays

74workingdays

14workingdays

90workingdays

60workingdays30workingdays

PublicconsultaConrepeated

PublicconsultaConIniCaldatacollecCon

StateadministraCvecourt

LocaConseclement

VerificaCon&revision

Inventory&idenQficaQon&appraisal&announcement

ImplementaConAppraiserdeterminaQon

andappraisal

NegoQaQononformofcompensaQon

RevocaQonofright

Handover

HandoverPreparaCon134-250workingdays104-242workingdays

ReviewteamAppealtosupremecourt

Appealtosupremecourt

Planning

Improved land acquisition process – a significant step towards achieving the government's toll road expansion plan

OverviewoftheIndonesianTollRegulaNon

Projectsand

OperaNonalDetails

9

LeadingTollRoadsinIndonesia

738 738 799 987

1,260

2012 2013 2014 2015 2016

Accumulated Toll Road Concessions (km)

JavaSea

TimorSea

StraitofMalacca

BandaSea

IndianOcean

SULAWESI

PAPUAKALIMANTAN

MALUKUSUMATRA

CENTRAL JAVA § Semarang: 24.75 km § Semarang-Solo: 72.64 km § Solo-Ngawi: 90.1 km § Ngawi-Kertosono: 87.02 km § Semarang-Batang: 75 km

EAST JAVA § Surabaya-Gempol: 49.00 km § Gempol-Pandaan: 13.61 km § Gempol-Pasuruan: 34.15 km

§ Surabaya-Mojokerto: 36.27 km

§ Pandaan-Malang: 37.62 km

NORTH SUMATERA § Belmera: 42.70 km § Medan-Kualanamu-Tebing Tinggi: 61.70 km

GREATER JAKARTA & WEST JAVA § Jagorawi: 59.00 km § Jakarta-Tangerang: 33.00 km § Ulujami-Pondok Aren: 5.55 km § Jakarta Inner Ring Road: 23.55 km § Prof. Dr. Ir. Sedyatmo: 14.30 km § Jakarta-Cikampek: 83.00 km § JORR: 28.3 km § Cikampek-Padalarang: 58.50 km § Padaleunyi: 64.40 km § Palikanci: 26.30 km § JORR W2 North: 7.70 km § Bogor Outer Ring Road: 11.00 km

§ Cengkareng-Kunciran: 14.19 km

§ Kunciran-Serpong: 11.19 km

§ Cinere-Serpong: 10.14 km § Jakarta-Cikampek II Elevated: 36.4 km

JAVA

BALI

BALI § Nusa Dua-Ngurah Rai-Benoa: 10.00 km

EAST KALIMANTAN § Balikpapan-Samarinda: 99.35 km

NORTH SULAWESI § Manado-Bitung: 39.9 km

JavaSea

TimorSea

StraitofMalacca

BandaSea

IndianOcean

SULAWESI

PAPUAKALIMANTAN

MALUKUSUMATRA

CENTRAL JAVA § Semarang: 24.8 km § Semarang-Solo: 72.6 km § Solo-Ngawi: 90.1 km § Ngawi-Kertosono: 87.0 km § Semarang-Batang: 75.0 km

EAST JAVA § Surabaya-Gempol: 49.0 km § Gempol-Pandaan: 13.6 km § Gempol-Pasuruan: 34.2 km

§ Surabaya-Mojokerto: 36.3 km

§ Pandaan-Malang: 37.6 km

NORTH SUMATERA § Belmera: 42.7 km § Medan-Kualanamu-Tebing Tinggi: 61.7 km

GREATER JAKARTA & WEST JAVA § Jagorawi: 59.0 km § Jakarta-Tangerang: 33.0 km § Ulujami-Pondok Aren: 5.56 km § Jakarta Inner Ring Road: 23.6 km § Prof. Dr. Ir. Sedyatmo: 14.3 km § Jakarta-Cikampek: 83.0 km § JORR: 28.3 km § Cikampek-Padalarang: 58.5 km § Padaleunyi: 64.4 km § Palikanci: 26.3 km § JORR W2 North: 7.7 km § Bogor Outer Ring Road: 11.0 km

§ Cengkareng-Kunciran: 14.2 km

§ Kunciran-Serpong: 11.2 km

§ Cinere-Serpong: 10.1 km § Jakarta-Cikampek II Elevated: 36.4 km

JAVA

BALI

BALI § Nusa Dua-Ngurah Rai-Benoa: 10.0 km

EAST KALIMANTAN § Balikpapan-Samarinda: 99.4 km

NORTH SULAWESI § Manado-Bitung: 39.9 km

: Owned before 2004 and operating (13 projects)

: Awarded after 2004 and fully operated (2 new projects)

: Awarded after 2004 and half operated (6 new projects)

: Awarded after 2004 and in land acquisition/ construction (10 new projects)

665 km Toll Road in Operation*

Transactions volume

Market Shares

62.2% 80%

*Asof31stOct2017 10

StrongOperaNngTrackRecordWithLongestConcessionPeriodProvidingIncomeVisibility

11

ü Stable cash flow from mature assets under operations

ü Strong long term visibility of cash flow, with an average remaining concession life of 30 years across all operating assets

ü Minimum remaining concession life of 28 years

ü Expects concession renewals with commitments to ongoing investments in projects

ü 35+ concession years across new projects

ü Long horizon to enjoy economic benefits post typical ramp-up period

41 28 31 39 33 38 28 28 28 28 28 28 28 28 28 28 28 28 28

45 40 40 35 45 35 35 35 35 35 38 42

Jakarta-Cikampek II Elevated Manado-Bitung

Balikpapan-Samarinda Pandaan-Malang

Batang-Semarang Serpong-Cinere

Ngawi-Kertosono Solo-Ngawi

Kunciran-Serpong Cengkareng-Kunciran

Medan-Kualanamu-Tebing Tinggi Gempol-Pasuruan

Nusa Dua-Ngurah Rai-Benoa JORR W2 Utara

Gempol-Pandaan Semarang-Solo

Surabaya-Mojokerto Bogor Outer Ring Road

Ulujami-Pondok Aren Cipularang

Palikanci Jakarta Outer Ring Road

Padaleunyi Jakarta-Cikampek

Jakarta Inner Ring Road Belmera

Surabaya-Gempol Prof. Dr. Ir.Sedyatmo

Jakarta-Tangerang Semarang

Jagorawi

Concession years remaining - Operating projects Concession years remaining - New projects

JasaMarga’sProjectAwardedPost2004AsofOct2017

SecCon ConcessionPeriod Length(km)JMOwnership(%)

A.FullyOperated 1 NusaDua-NgurahRai-Benoa(1) 2057 10.0 55.0%2 JORRW2North(partofJORR)(2) 2044 7.7 65.0%

B.HalfOperated 3 Gempol-Pandaan(3) 2049 13.6 92.2%4 BogorOuterRingRoad(4) 2054 11.0 55.0%5 Semarang-Solo(partofTransJava)(5) 2055 72.6 58.9%6 Surabaya-Mojokerto(partofTransJava)(6) 2049 36.3 55.0%7 Gempol-Pasuruan(partofTransJava)(7) 2058 34.2 98.8%8 Medan-Kualanamu-TebingTinggi(8) 2054 61.7 55.0%

C.InLandAcquisiConandConstrucCon 9 JORR2(Cengkareng-Kunciran) 35yearsfromeffecQvedate 14.2 76.2%10 JORR2(Kunciran-Serpong) 35yearsfromeffecQvedate 11.2 60.0%11 Solo-Ngawi(partofTransJava) 35yearsfromeffecQvedate 90.1 60.0%12 Ngawi-Kertosono(partofTransJava) 35yearsfromeffecQvedate 87.0 60.0%13 JORR2(Serpong-Cinere) 35yearsfromeffecQvedate 10.1 55.0%14 Batang-Semarang(partofTransJava) 45yearsfromeffecQvedate 75.0 60.0%15 Pandaan-Malang 35yearsfromeffecQvedate 37.6 60.0%16 Balikpapan-Samarinda 40yearsfromeffecQvedate 99.4 55.0%17 Manado-Bitung 40yearsfromeffecQvedate 39.9 65.0%18 Jakarta-CikampekIIElevated 45yearsfromeffecQvedate 36.4 80.0%

TOTAL 748.0

Notes: (1)Operatedsince01October2013.(2)SecQonKebonJeruk-Cileduk(5.70km)isoperatedsince04January2014;SecQonCileduk-Ulujami(2.00km)isoperatedsince22July2014.(3)SecQonGempol-Pandaan(12km)isoperatedsince12June2015.(4)SecQon1:Sentul-KedungHalang(3.85km)isoperatedsince23November2009;SecQon2A:KedungHalang-KedungBadak(1.95km)isoperatedsince04June2014. (5)SecQon1:Semarang-Ungaran(10.80km)isoperatedsince17November2011;SecQon2:Ungaran-Bawen(12.30km)isoperatedsince04April2014;SecQonBawen-SalaQga(17,6km)is

operatedsince25September2017. (6)SecQon1A:Waru-Sepanjang(2.30km)isoperatedsince05September2011,SecQon4:Kriyan-Mojokertoisoperatedsince19March2016. (7)Gempol-Pasuruan:SecQonBangil-Rembang(7,1km)isoperatedsince13April2017&SecQonGempol-Bangil(6,8km)isoperatedsinceJuli2017(8)SecQon3-6:Kualanamu-Seirampah-Perbarakan(42km)isoperatedsince20October2017.

12

BogorOuterRingRoad(BORR)(11km)(SecAon2BKd,Badak–Yasmin)

ProgressLandAcquisiAon:97.00%ProgressConstrucAon:60.40%

Cengkareng–Kunciran(14.19km)ProgressLandAcquisiAon:30.92%

ProgressConstrucAon:4.02%

Kunciran–Serpong(11.19km)ProgressLandAcquisiAon:89.18%

ProgressConstrucAon:13.29%

Serpong–Cinere(10.14km)ProgressLandAcquisiAon:58.89% JakartaCikampekIIElevated(36.40km)

ProgressConstrucAon:13.74%

HalfOperated

InLandAcquisiConandConstrucCon

5projects

*Asof2Nov2017

JasaMarga’sUpcomingProjects:GreaterJakarta

13

Semarang-Batang(75km)ProgressConstrucAon:55.71%ProgressLandAcquisiAon:98.16%

Semarang–Solo(73km)ProgressConstrucAon(SalaAga–Solo):36.30%ProgressLandAcquisiAon(SalaAga–Solo):99.49%

Solo–Ngawi(90km)ProgressConstrucAon:80.14%ProgressLandAcquisiAon:94.70%

Ngawi–Kertosono(49km)ProgressConstrucAon:90.69%ProgressLandAcquisiAon:99.88%

Surabaya–Mojokerto(36.3km)ProgressConstrucAon:98.33%ProgressLandAcquisiAon:100%

Gempol–Pandaan(12km)

Gempol–Pasuruan(34.2km)ProgressConstrucAon:85.53%ProgressLandAcquisiAon:85.29%

Pandaan–Malang(37.62km)ProgressConstrucAon:29.43%ProgressLandAcquisiAon:77.08%

HalfOperated

InLandAcquisiConandConstrucCon

8projects

*Asof2Nov2017

JasaMarga’sUpcomingProjects:Java

14

Medan-Kualanamu-TebingTinggi(61.7km)ProgressConstrucAon:79.95%ProgressLandAcquisiAon:93.29%

SUMATRA

KALIMANTAN

Balikpapan-Samarinda(99.35km)ProgressConstrucAon:36.60%ProgressLandAcquisiAon:94.82%

SULAWESI

MALUKU

Manado-Bitung(39.9km)ProgressConstrucAon:8.64%ProgressLandAcquisiAon:44.83%

3projects

HalfOperated

InLandAcquisiConandConstrucCon

*Asof2Nov2017

JasaMarga’sUpcomingProjects:Sumatera,Kalimantan,andSulawesi

15

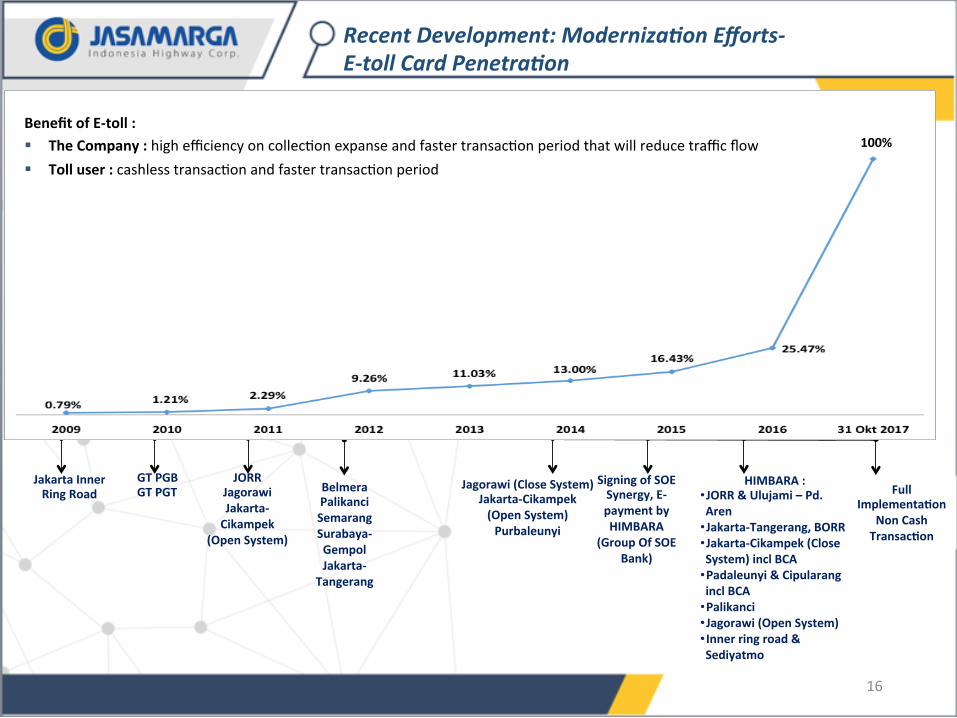

HIMBARA:• JORR&Ulujami–Pd.Aren

• Jakarta-Tangerang,BORR• Jakarta-Cikampek(CloseSystem)inclBCA

• Padaleunyi&CipularanginclBCA

• Palikanci• Jagorawi(OpenSystem)• Innerringroad&Sediyatmo

JakartaInnerRingRoad

GTPGBGTPGT

JORRJagorawiJakarta-Cikampek

(OpenSystem)

BelmeraPalikanciSemarangSurabaya-GempolJakarta-

Tangerang

SigningofSOESynergy,E-paymentbyHIMBARA

(GroupOfSOEBank)

Jagorawi(CloseSystem)Jakarta-Cikampek(OpenSystem)Purbaleunyi

FullImplementaCon

NonCashTransacCon

100%BenefitofE-toll:§ TheCompany:highefficiencyoncollecQonexpanseandfastertransacQonperiodthatwillreducetrafficflow§ Tolluser:cashlesstransacQonandfastertransacQonperiod

RecentDevelopment:ModernizaNonEfforts-E-tollCardPenetraNon

16

0

200

400

600

800

1000

1200

1400

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

E

2018

E

2019

E

2020

E

2021

E -

200

400

600

800

1,000

1,200

1,400

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Traffic on Jasa Marga Toll Road (in million) Car Sales in Indonesia (in thousand vehicles)

ü Robust estimated growth in car sales is a positive driver for the toll road industry

EconomicSlowDown

Directimpactoffuelpricehike(1)

Source: BMI Research Source: Jasa Marga

ü Consistent growth in traffic demonstrates resilience of toll road industry

WellPosiNonedInAResilientIndustryWithFavorableGrowthTrends

17

Fluctuating car sales growth in Indonesia has minimal impact to our traffic volume, however increase in car sales will contribute to higher traffic volumes in the long run.

FinancialHighlights

ExcellentFinancialProfileWithStableMargins,ReducingLeverageAndStrongCashflows

6.65 7.12 7.935.91 6.06

0.58 0.510.91

0.57 0.72

2014 2015 2016 9M2016 9M2017

TollRevenue OtherBusiness

Prudent financial management enable company to lower its cost of debt over time

EBITDA & EBITDA Margin

Interest Coverage Ratio (ICR)

(IDR bn) (%)

(x)

Note : figures of 2014, 2015, &2016 audited; 3Q2016 & 3Q2017 limited review

Debt to Equity Ratio (DER)

Revenue

(IDR tn)

7.23 7.63 8.84

6.48 6.78

CAGR10.6%

CAGR14.2%

(x)

1.21 1.29

1.53 1.55

2014 2015 2016 9M2017

2014 2015 2016 9M2017

3.30 3.063.45

4.45

2014 2015 2016 9M2017

2014 2015 2016 9M2017

4.01 4.32

5.23

3.79 3.99

55.4% 56.6% 59.2% 58.5% 58.9%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2014 2015 2016 9M2016 9M2017

EBITDA EBITDAMargin

19

Note:• FinancialstatementsareauditedfortheyearsendinginDecember312014,2015,and2016• LimitedreviewstatementsfortheperiodendinginSeptember302016and2017

SummaryofConsolidatedIncomeStatement(IDRmillion)

20

(FYE 31 Dec) Y2014 Y2015 Y2016 3Q2016 3Q2017 ∆Rp ∆%

(Audited) (Audited) (Audited) (Unaudited) (Unaudited) (YoY) (YoY)

REVENUE 7.227,8 7.630,7 8.832,3 6.477,2 6.782,3 305,1 4,7%

Toll and Other Operating Expenses (3.562,8) (3.518,0) (4.022,9) (2.963,8) (3.079,8) (116,0) 3,9%

General and Administrative Expenses (884,8) (893,3) (949,0) (656,0) (784,7) (128,6) 19,6%

Other Expenses (20,3) (29,8) (99,0) (42,5) (153,2) (110,7) 260,3%

Others Income 287,9 272,9 357,1 230,6 782,0 551,3 239,0%

OPERATING INCOME 3.072,7 3.477,7 4.165,5 3.072,0 3.634,9 562,9 18,3%

Operating Income Margin 42,5% 45,6% 47,2% 47,4% 53,6% N/A 6,2%

EBITDA 4.006,8 4.285,0 5.228,5 3.791,3 3.993,1 201,8 5,3%

EBITDA Margin 55,4% 56,2% 59,2% 58,5% 58,9% N/A 0,3%

Finance Cost (1.215,3) (1.405,0) (1.509,0) (1.109,4) (896,0) 213,4 -19,2%

INCOME BEFORE TAX 1.850,7 2.068,3 2.649,7 1.956,1 2.660,9 704,8 36,0%

Income Tax Expense (613,7) (749,1) (846,6) (659,7) (819,4) (159,6) 24,2%

NET INCOME 1.421,7 1.466,4 1.889,3 1.345,3 1.902,1 556,8 41,4%

Net Income Margin 19,7% 19,2% 21,4% 20,8% 28,0% N/A 7,3%

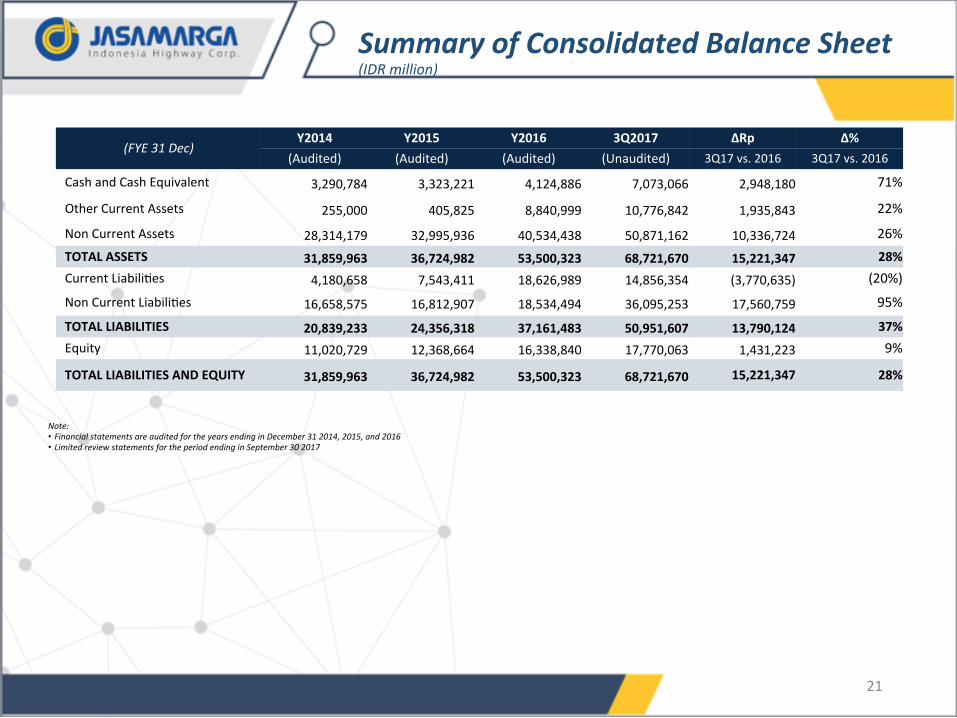

SummaryofConsolidatedBalanceSheet(IDRmillion)

(FYE31Dec)Y2014 Y2015 Y2016 3Q2017 ∆Rp ∆%

(Audited) (Audited) (Audited) (Unaudited) 3Q17vs.2016 3Q17vs.2016

CashandCashEquivalent 3,290,784 3,323,221 4,124,886 7,073,066 2,948,180 71%

OtherCurrentAssets 255,000 405,825 8,840,999 10,776,842 1,935,843 22%

NonCurrentAssets 28,314,179 32,995,936 40,534,438 50,871,162 10,336,724 26%TOTALASSETS 31,859,963 36,724,982 53,500,323 68,721,670 15,221,347 28%CurrentLiabiliQes 4,180,658 7,543,411 18,626,989 14,856,354 (3,770,635) (20%)

NonCurrentLiabiliQes 16,658,575 16,812,907 18,534,494 36,095,253 17,560,759 95%

TOTALLIABILITIES 20,839,233 24,356,318 37,161,483 50,951,607 13,790,124 37%Equity 11,020,729 12,368,664 16,338,840 17,770,063 1,431,223 9%

TOTALLIABILITIESANDEQUITY 31,859,963 36,724,982 53,500,323 68,721,670 15,221,347 28%

Note:• FinancialstatementsareauditedfortheyearsendinginDecember312014,2015,and2016• LimitedreviewstatementsfortheperiodendinginSeptember302017

21

DesiArryani–ChiefExecuCveOfficer• Haswork experience in ConstrucQon sectormore than 25 years. Previously served asOperaQonsDirector I of PTWaskita Karya (Persero) Tbk.which is SOE

contractorinIndonesia.• CompletedherBachelordegreeinCivilEngineeringfromUniversityofIndonesia(1987)andMasterdegreeinManagementfromPrasetyaMulya(2008).

DonnyArsal–ChiefFinancialOfficer• HasworkexperienceinFinancialsectormorethan23years.PreviouslyservedasManagingDirectorPTMandiriSekuritas,thatlookamerforInvestmentBanking

Division.• CompletedBachelorDegreefromUniversityofIndonesia(1994).

MohammadSofyan–OperaConalDirectorI• JoinJasaMargasince1997andhasleadinvarioussectormorethan20yearssuchustollroadproject,ITandstrategiccorporateplanning.Previouslyservedas

CorporateSecretaryPTJasaMarga(Persero)Tbk.• CompletedBachelorDegreeinCivilEngineeringatSepuluhNovemberInsQtuteofTechnologySurabaya(1996)andMasterDegreeinProjectManagementfrom

UniversityofIndonesia(2003)andMasterBusiness&ITfromMelbourneUniversity(2007).

SubakCSyukur–OperaConalDirectorII• Join JasaMargasince1986andhasworkexperience in toll roadoperaQonsmore than30years.Previously servedasPresidentDirectorofPTMargaLingkar

Jakarta(oneofJasaMarga’sSubsidiary).• Completed Bachelor Degree in Civil Engineering from Bandung InsQtute of Technology (1986) and Master degree in Management from Universitas Kristen

Dwipayana(2010).

Hasanudin–DevelopmentDirector• Join JasaMarga since 1988 and haswork experience in toll road projectmanagement and operaQonsmore than 30 years. Previously served as OperaQons

DirectorPTJasaMarga(Persero)Tbk..• CompletedBachelorDegreeinCivilTransportaQonEngineeringatSepuluhNovemberInsQtuteofTechnology,Surabaya(1987)andUniversityofNewSouthWales

forMaster’sDegree.

KushartantoKoeswiranto–HumanCapitalandGeneralAffairs/IndependentDirector• Has work experience in Human Resources sector more than 30 years. Previously served as President Director KTalents Asia, Group Director HR of Agung

PodomoroGroup,andHR&BusinessSupportDirectorLofeShoppingIndonesia.• CompletedEconomyBachelorDegreeatDiponegoroUniversityandMBAatIPMI.

Experiencemanagementwithover25 yearsofexperience,deepunderstandingon the industry/sector, and long-term relaConshipwithstakeholders

Strongcorporategovernanceandhighlyqualifiedmanagementteam

22

Appendix

TrafficVolumebySecNon(MillionvehicletransacAons)

24

No Branch/Subsidiary 2014 2015 2016 3Q2016 3Q2017 ∆% 3Q17 vs. 3Q16 CAGR 2014-2016

1 Jagorawi 201.32 204.16 207.65 154.20 151.53 -1.73% 1.56%

2 Jakarta-Cikampek * 206.13 215.00 221.75 165.94 156.34 -5.79% 3.72%

3 Jakarta-Tangerang 119.83 127.43 130.89 97.04 98.68 1.69% 4.51%

4 Cawang-Tomang-Cengkareng 282.81 284.66 294.90 218.29 224.11 2.67% 2.12%

6 Purbaleunyi 66.35 66.25 67.49 50.20 51.73 3.05% 0.85%

8 Surabaya-Gempol 82.87 89.56 97.66 72.40 75.80 4.70% 8.56%

9 Semarang 48.12 50.41 51.76 38.27 39.87 4.18% 3.71%

10 Belmera 25.39 24.79 25.75 19.05 20.94 9.92% 0.71%

11 Palikanci ** 19.93 23.04 19.04 15.64 11.07 -29.22% -2.25%

12 JORR Non S 84.50 90.71 95.76 70.97 73.07 2.96% 6.45%

13 Ulujami-Pondok Aren 45.13 43.73 46.11 34.10 35.47 4.02% 1.09%

14 PT Marga Sarana Jabar 13.68 15.34 16.49 12.13 11.92 -1.76% 9.77%

15 PT Jasamarga Surabaya Mojokerto 12.05 13.02 15.36 11.27 12.64 12.16% 12.89%

16 PT Trans Marga Jateng 15.56 18.70 20.50 15.16 15.51 2.28% 14.77%

17 PT Jasamarga Bali Tol 14.31 16.54 17.46 12.64 14.63 15.76% 10.46%

18 PT Marga Lingkar Jakarta 14.49 24.71 26.90 19.75 22.59 14.36% 36.27%

19 PT Jasamarga Pandaan Tol 0.00 2.80 5.84 4.24 5.06 19.34% N/A

20 PT Trans Jatim Pasuruan 0.00 0.00 0.00 0.17 N/A N/A

TOTAL 1252.47 1310.85 1361.31 1011.29 1021.12 0.97% 4.25%

Note:*ThechangesinthetrafficpafernandtheimpactfromtheremovaloftollgatescikopobecauseofintegraQonofcluster1(Cikampek,Padaleunyi,Cipularang,Cikopo-Palimanan)**ThereischangesintrafficrecordastheimpactofremovalgatePlumbon3,Plumbon4,danCipernaUtamadikarenakanintegrasiClusterII(Palimanan-Kanci,Kanci-Pejagan,Pejagan-

BrebesTimur)

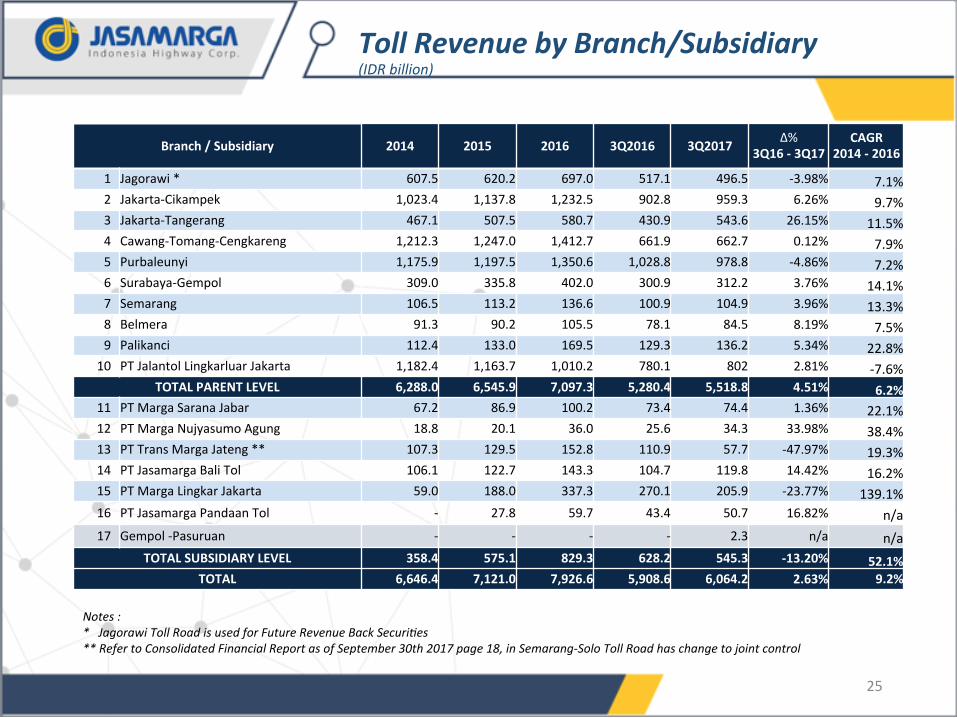

TollRevenuebyBranch/Subsidiary(IDRbillion)

Branch/Subsidiary 2014 2015 2016 3Q2016 3Q2017 ∆%3Q16-3Q17

CAGR2014-2016

1 Jagorawi* 607.5 620.2 697.0 517.1 496.5 -3.98% 7.1%2 Jakarta-Cikampek 1,023.4 1,137.8 1,232.5 902.8 959.3 6.26% 9.7%3 Jakarta-Tangerang 467.1 507.5 580.7 430.9 543.6 26.15% 11.5%4 Cawang-Tomang-Cengkareng 1,212.3 1,247.0 1,412.7 661.9 662.7 0.12% 7.9%5 Purbaleunyi 1,175.9 1,197.5 1,350.6 1,028.8 978.8 -4.86% 7.2%6 Surabaya-Gempol 309.0 335.8 402.0 300.9 312.2 3.76% 14.1%7 Semarang 106.5 113.2 136.6 100.9 104.9 3.96% 13.3%8 Belmera 91.3 90.2 105.5 78.1 84.5 8.19% 7.5%9 Palikanci 112.4 133.0 169.5 129.3 136.2 5.34% 22.8%

10 PTJalantolLingkarluarJakarta 1,182.4 1,163.7 1,010.2 780.1 802 2.81% -7.6%TOTALPARENTLEVEL 6,288.0 6,545.9 7,097.3 5,280.4 5,518.8 4.51% 6.2%

11 PTMargaSaranaJabar 67.2 86.9 100.2 73.4 74.4 1.36% 22.1%12 PTMargaNujyasumoAgung 18.8 20.1 36.0 25.6 34.3 33.98% 38.4%13 PTTransMargaJateng** 107.3 129.5 152.8 110.9 57.7 -47.97% 19.3%14 PTJasamargaBaliTol 106.1 122.7 143.3 104.7 119.8 14.42% 16.2%15 PTMargaLingkarJakarta 59.0 188.0 337.3 270.1 205.9 -23.77% 139.1%16 PTJasamargaPandaanTol - 27.8 59.7 43.4 50.7 16.82% n/a17 Gempol-Pasuruan - - - - 2.3 n/a n/a

TOTALSUBSIDIARYLEVEL 358.4 575.1 829.3 628.2 545.3 -13.20% 52.1%TOTAL 6,646.4 7,121.0 7,926.6 5,908.6 6,064.2 2.63% 9.2%

25

Notes:*JagorawiTollRoadisusedforFutureRevenueBackSecuriAes**RefertoConsolidatedFinancialReportasofSeptember30th2017page18,inSemarang-SoloTollRoadhaschangetojointcontrol

Disclaimer

By attending this presentation, you are agreeing to be bound by the restrictions set out below. Any failure to comply with these restrictions may constitute a violation of applicable securities laws. The information and opinions contained in this presentation are intended solely for your personal reference and are strictly confidential. The information and opinions contained in this presentation have not been independently verified, and no representation or warranty, expressed or implied, is made as to, and no reliance should be placed on the fairness, accuracy, completeness or correctness of, the information or opinions contained herein. It is not the intention to provide, and you may not rely on this presentation as providing, a complete or comprehensive analysis of the condition (financial or other), earnings, business affairs, business prospects, properties or results of operations of the company or its subsidiaries. The information and opinions contained in this presentation are provided as at the date of this presentation and are subject to change without notice. Neither the company (including any of its affiliates, advisors and representatives) nor the underwriters (including any of their respective affiliates, advisors or representatives) shall have any responsibility or liability whatsoever (in negligence or otherwise) for the accuracy or completeness of, or any errors or omissions in, any information or opinions contained herein nor for any loss howsoever arising from any use of this presentation. In addition, the information contained in this presentation contains projections and forward-looking statements that reflect the company's current views with respect to future events and financial performance. These views are based on a number of estimates and current assumptions which are subject to business, economic and competitive uncertainties and contingencies as well as various risks and these may change over time and in many cases are outside the control of the company and its directors. No assurance can be given that future events will occur, that projections will be achieved, or that the company's assumptions are correct. Actual results may differ materially from those forecast and projected. This presentation is not and does not constitute or form part of any offer, invitation or recommendation to purchase or subscribe for any securities and no part of it shall form the basis of or be relied upon in connection with any contract, commitment or investment decision in relation thereto. This presentation may not be used or relied upon by any other party, or for any other purpose, and may not be reproduced, disseminated or quoted without the prior written consent of the company. Any investment in any securities issued by the company or its affiliates should be made solely on the basis of the final offer document issued in respect of such securities. Relaying copies of this presentation to other persons in your company or elsewhere is prohibited.

26

ThankYou

Top Related