Languages

Pages

Legal

Food Systems & Integrated Agrologistics

Improving agro-food chains performance for food security

Prof dr Ruerd Ruben

Wageningen University & Research (WUR)

Plant Sciences

Animal & Marine Sciences

Environmental Sciences

Food & Biobiased

Social Sciences

Food Safety (RIKILT)

Training & Capacity Building (CDI)

Agrotech& food

research

Animal research

Plant research

Social research

Wageningen UR: an integrated perspective

3

Physical (hardware)

activities

Organisa-tional

(orgware) activities

Infor-mation

(software) activities

Scientific research & education: Wageningen University

Applied research: Institutes, e.g.

WEcR, FBR, WLR

Agrologistics for robust performance

4

Specific agrifoodfeatures

(complexity, dynamics,

uncertainty)

Robust perfor-mance

(costs, quality, sustainability, reliability, etc.)

Product quality

Resource Sustain-ability

Technology(ICT, transport,

processes, storage, etc.)

Wageningen UR works across this scope

Agrologistics: more than hardware

5

Physical (hardware)

activities

Organisa-tional

(orgware) activities

Infor-mation

(software) activities

Right product quality

Right volume

Right time

Right consumer

Minimal loss of product

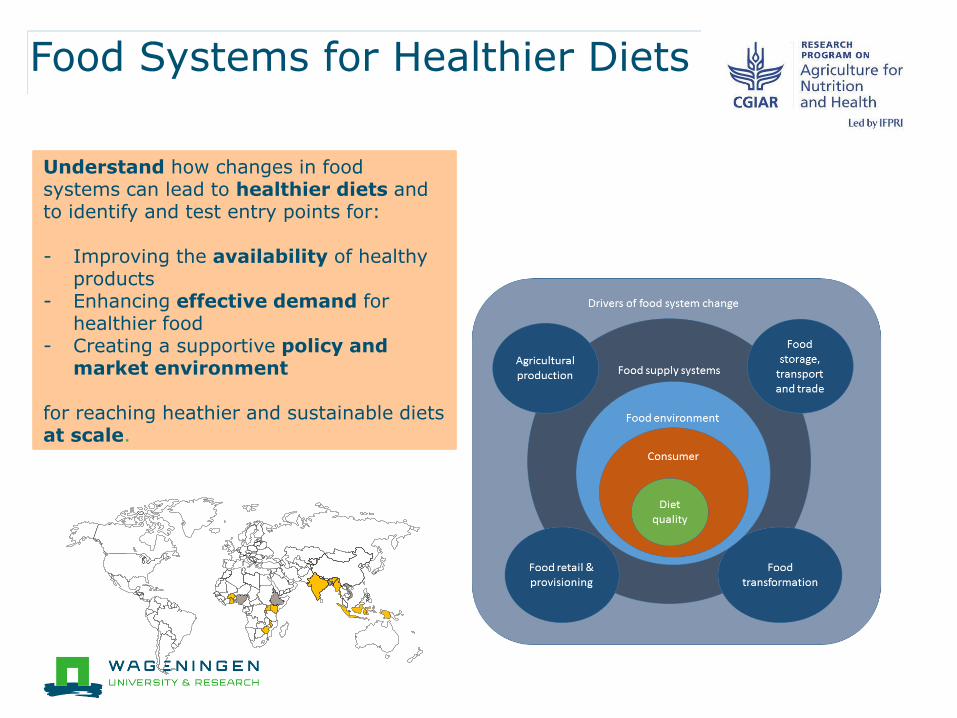

Food Systems for Healthier Diets

Understand how changes in food systems can lead to healthier diets and to identify and test entry points for:

- Improving the availability of healthy products

- Enhancing effective demand for healthier food

- Creating a supportive policy and market environment

for reaching heathier and sustainable diets at scale.

Triple burden of malnutrition

▪ 52% of children are Malnourished

(GNR 2015 – stunting & wasting)

▪ Micronutrient deficiencies (iron, zinc, Vit A)

▪ Overweight: 20-25% (adults); Obesity: 8-15% (adults)

▪ Investment to combat malnutrition: N188.3 billion ($837 million) to save 180,000 lives, and avert 3 million cases of stunting a year.

▪ GLOPAN for Nigeria: 40% stunting reduction results in GDP rise of 29.3 billion.

▪ in Africa, every dollar invested in reducing chronic undernutrition in children yields a US$ 16 return.

Context

▪ Population growth – 9bn by 2050

● Mainly in Africa- population will double

▪ Retail Revolution

● Supermarkets & Convenience (fast) Food

▪ Urbanization

● By 2050 : 70% city population globally

● Rapid urbanization in Africa (Nigeria: 48%)

▪ Natural resources pressure

● Water, Land, Energy

● Food Losses & Waste

● Climate Change & Emissions

Global challenges

0

200

400

600

800

1000

1 6 11 16 21 26

Gro

wth

(2

00

5 =

10

0)

Year (2005 = 1)

The Growing Wedge (forecast)

Year

Economicgrowth

GrowthAgiculturalProductivity

Urban middle class : shift consumption basket

-> higher quality & more convenience

Dairy, Meat, Fish, Fresh Fruit Juices, Beverages

Convenience

Foods

Diet/Functional/

Organic Foods

Snacks/Prepared

Meals

Carbohydrate Staples

Surviving Mass

Market

Convenience

Food Service

Snacking

Quality

Hygiene

High

Technology

Africa (Sub-

Sahara)

India, China,SE Asia Latin America

Eastern Europe

N. America, Japan, W. Europe, Australia

AVAILABILITYGovernment, laws, choice of suppliers

FOOD SAFETY

FOOD QUALITY

ETHICS

CHAIN QUALITY

Changing market & product characteristics

Period 1960s 1970s 1980s 1990s 2000s

Demands consumer

Performance company

Focus

of

company

PriceQuality Variety Lead time

Efficiency Quality Flexibility

Speed

Chain Chain NetworkCompany Bi-lateral Focus :

2010s

Su

sta

inability

Innovation

power

Uniqueness

Efficient Quality Flexible Innovative

-15%

-5%

5%

15%

25%

35%

45%

12

Nigeria - Frequency of food purchase by wealth index – difference between highest and lowest groups)

Base: All households, lowest (n=165), secondary (n=196), middle (n=198), fourth (n=198), highest (n=179))I8.1

>20% purchasing frequency difference between highest and lowest SEC groups

Increased purchase as

SEC decreases

% p

oin

t d

iffe

ren

ce b

etw

een

at

leas

t w

eekl

y p

urc

ha

sin

g am

on

g h

igh

est

an

d

low

est

SEC

gro

up

s

Water

Fruit juice/ soft drinks

Alcohol

Bananas

Chicken Milk, yoghurt, cheese

Snacks

Sweet snacks

Noodles/ pasta

Fresh eggs

All other vegetables

Bread

Fresh fish

Tea/ coffee

Orange/ yellow veg

(e.g. carrots)

Meat

Cocoa drinks

Dried fish

Meals away from home

Nuts

Green vegetables

Beans

Vegetables for soups

Tomato and

onion

Spices and herbs Mango/

papaya

Yam/ potato/ cassava

Vegetable/ groundnut oil

Stock cubes

Palm oil Rice

Ground maize

<20% purchasing frequency difference between highest and lowest SEC groups

All other fruitsThe difference in weekly

frequency of purchase between the highest and

the lowest groups

Purchased at least once a week

Q. I8.1. How often did you purchase any products from the following categories in the last 30 days?

13

DAILY DIET

1%

1%

2%

3%

3%

4%

6%

7%

8%

21%

45%

Other vitamin A-rich…

Eggs

Other fruits

Nuts and seeds

Other vegetables

Vitamin A-rich dark green…

Beans and peas

Flesh foods

Dairy

No category

All starchy staple foods

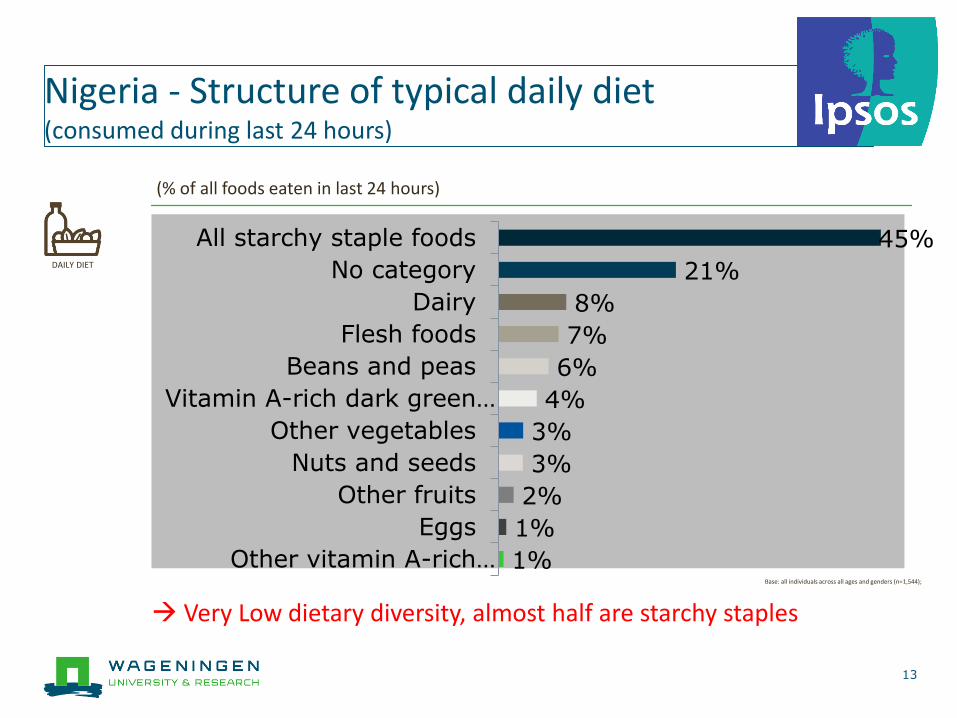

Base: all individuals across all ages and genders (n=1,544);

(% of all foods eaten in last 24 hours)

Nigeria - Structure of typical daily diet (consumed during last 24 hours)

Very Low dietary diversity, almost half are starchy staples

14

Key decisions in Agro-Logistics

ProducerProcessor/

Middle menLSP Retail Consumer

- Inventorycontrol (which products, amounts, where and when …)

- Network design (factories; DC’s; Retailers)

- Transportation (collection; routing; loading ...)

- Production (planning; blending; scheduling …)

- Integral aspects (Supply Chain Management)

Key issues in Global Agro-Logistics Networks

▪ Cost reduction and increase of reliability/flexibility

● Efficient logistics: deliver right quantity at right time, place, condition, price

● Need for reliable and responsive supply of goods

▪ Food security, food quality and food losses

● Ensuring access to local markets and reduce losses (30-40%)

● Increasing consumer discern towards safe, healthy and quality food

▪ Request for traceability and sustainability

● Transparency in food chain “from farm gate to food plate”

● Sustainable supply chain strategies (water, carbon, energy footprints)

● Resource ue efficiency

Food Losses & Waste

Global food waste = 1.3bn Ton

Industrialized Countries

670 mln Ton

Developing Countries

630 mln Ton

Industrialized Countries

$680bn

Developing Countries

$310bn

Global food waste ≈ $1 trillion

Food loss reduction needed

Source: Lipinski et al., WRI 2013

Top 10 causes of postharvest losses

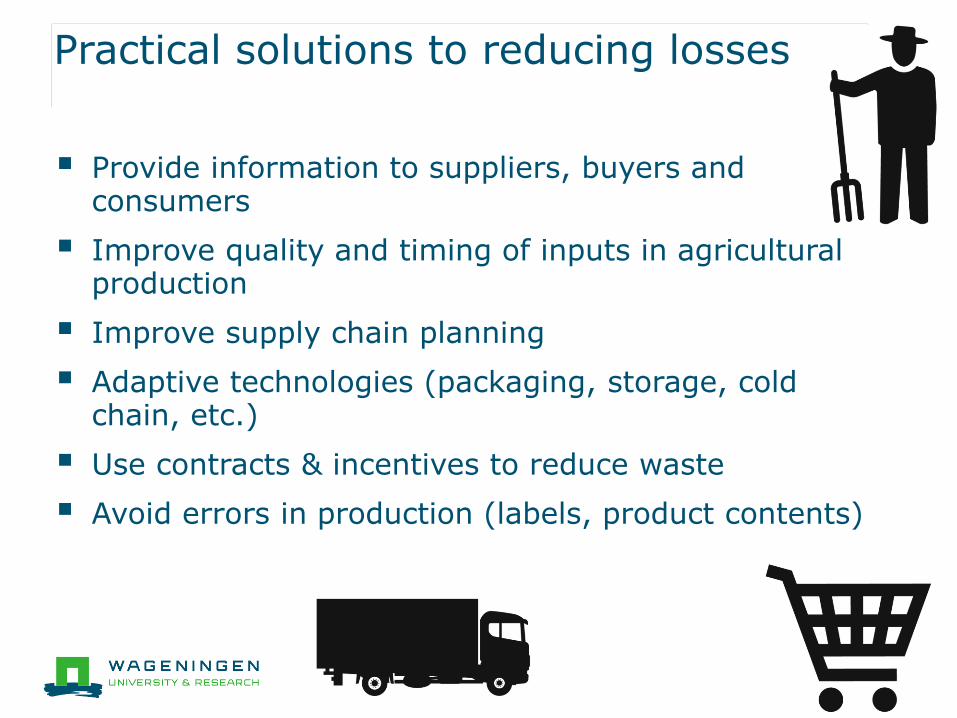

Practical solutions to reducing losses

▪ Provide information to suppliers, buyers and consumers

▪ Improve quality and timing of inputs in agricultural production

▪ Improve supply chain planning

▪ Adaptive technologies (packaging, storage, cold chain, etc.)

▪ Use contracts & incentives to reduce waste

▪ Avoid errors in production (labels, product contents)

Behavioural Solutions to reducing losses

▪ Raise consumer awareness, educate professionals,

▪ Adapt marketing standards

▪ Reduce margins of best-before dates when possible

▪ Customized meal/portion servings

▪ Innovations in promotion

▪ Finding alternative uses of secondary streams

▪ Increase awareness of consumers

▪ avoid buying too much (shopping lists)

▪ cook in correct quantities (measures)

Business realities & value chain dynamics

▪ Preventing/reducing loss may be (very) cost-effective

▪ But, investing in reducing losses:

● May involve too much risk

● May not lead to a net-benefit (waste = business)

● May involve a long payback time

● May not be possible due to constraints in resources, (e.g.

access to credit)

● May lead to benefits for other value chain actors

reducing the potential for costs recovery

▪ There may not be a ready market for the extra produce

● In the longer term: development new markets

● In the long term: change of production patterns

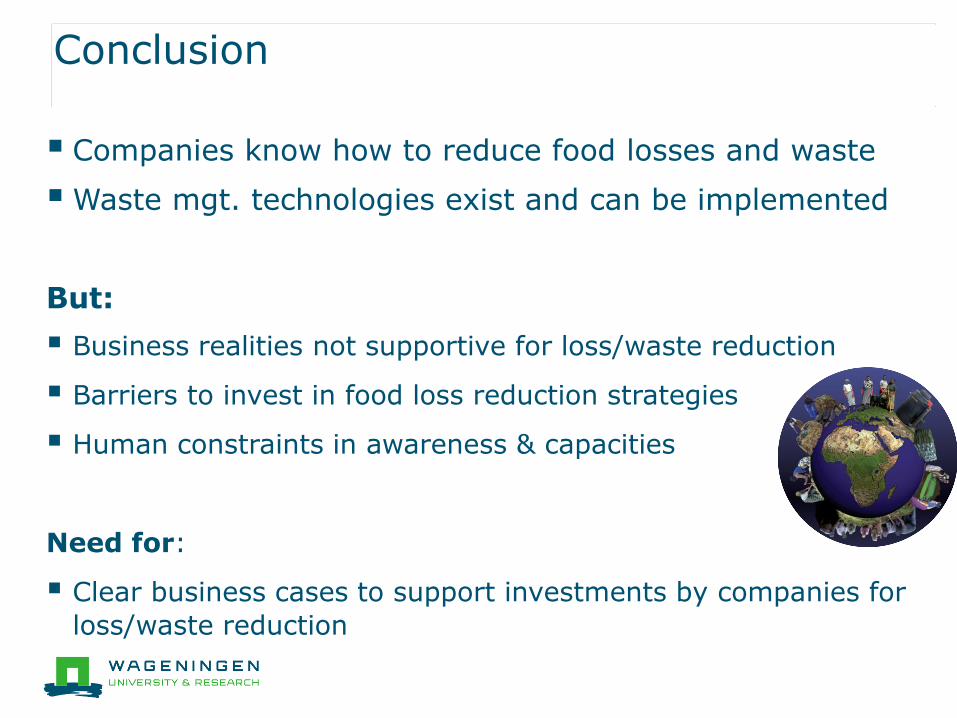

Conclusion

▪ Companies know how to reduce food losses and waste

▪Waste mgt. technologies exist and can be implemented

But:

▪ Business realities not supportive for loss/waste reduction

▪ Barriers to invest in food loss reduction strategies

▪ Human constraints in awareness & capacities

Need for:

▪ Clear business cases to support investments by companies for

loss/waste reduction

WG

1Governance

WG

2Regulatory framework

WG

3Infrastructure

WG

4Investment

WG

5Innovation

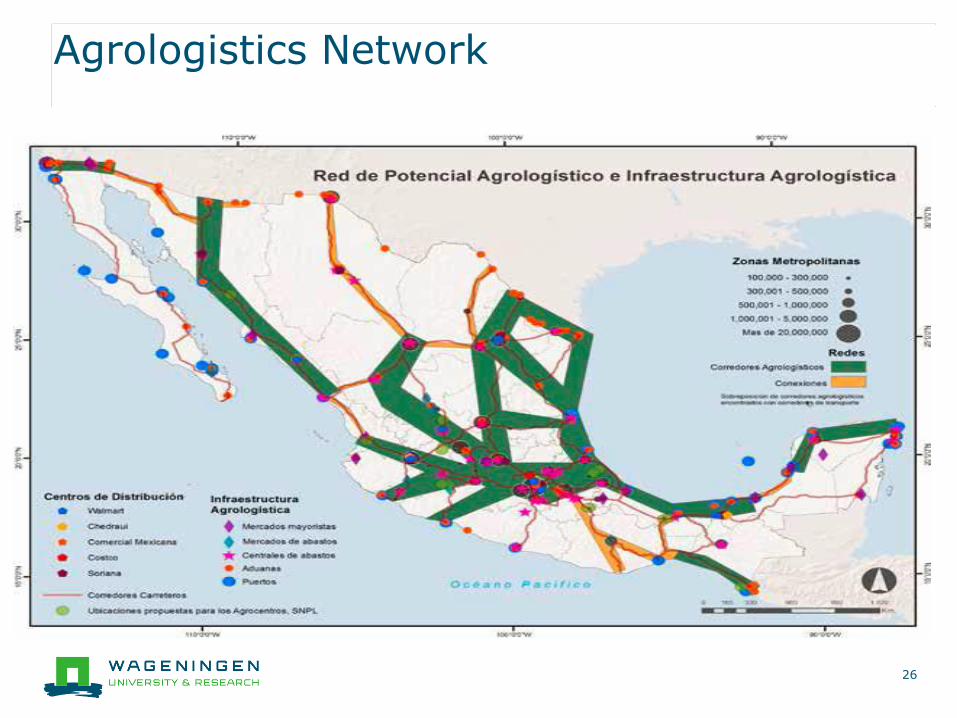

National Agrologistics Program (Mexico)

25

“Becoming a world leader in export of

agri-food products by the year 2030”

Agrologistics Network

26

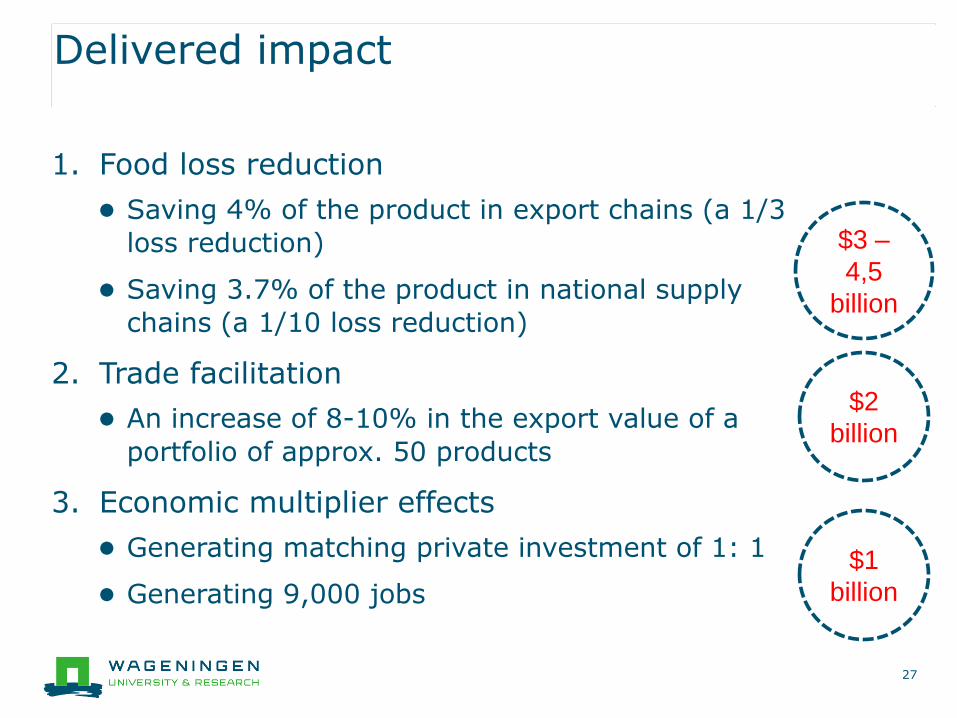

Delivered impact

1. Food loss reduction

● Saving 4% of the product in export chains (a 1/3

loss reduction)

● Saving 3.7% of the product in national supply

chains (a 1/10 loss reduction)

2. Trade facilitation

● An increase of 8-10% in the export value of a

portfolio of approx. 50 products

3. Economic multiplier effects

● Generating matching private investment of 1: 1

● Generating 9,000 jobs

$3 –

4,5

billion

$2

billion

$1

billion

27

DaVinc3i floriculture logistics

▪ Develop new logistics concepts for floriculture, to ensure the Dutch leadership position is strengthened

▪ Focus on:

● Quality Controlled Logistics

● Multimodal transport

● ICT for transparent supply chains

● New business models for cooperation

▪ Engage SMEs in (logistics) research

28

Integrating logistics networks

29

72

62

80

Kosten Tijd CO2

IMPACT ON

Warehouse Receipts (Cotton, Maize)

30

Temporal Arbitrage: Demand for storage if expected future price is high enough to compensate for costs of credit, time and risk

Fresh supply chain in Egypt

Bottlenecks:

▪ Lack of focus on product quality, bad roads, congestion, no cold chain

▪ High food waste (20% (e.g. in tomatoes) up to 80%)

▪ Shortage of water

Contract farming

▪ Large integrated farms

▪ use modern agricultural techniques,

▪ use patented varieties for specific

markets,

▪ well-organized supply chains that

include export (4-20x higher prices).

Traditional farming

▪ poor small farmers

▪ use basic agriculture

techniques,

▪ no access to new varieties,

▪ selling via middle man

▪ no incentive to innovate

First quality grade to Europe, second to Gulf States, rest local.

Dairy Collection in Asia

32

Milk collection & processing: generating added value, guaranteeing self sufficiency, creating sustainability & securing quality and safety

ICT system for quality logistics

34

Future Internet: Farming in the Cloud

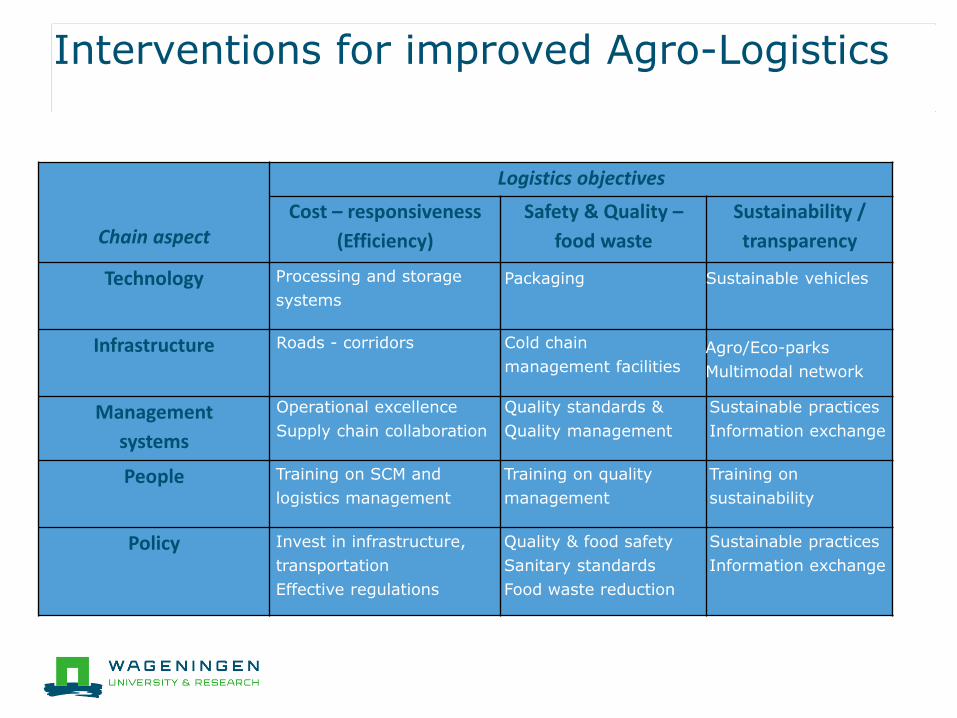

Interventions for improved Agro-Logistics

Chain aspect

Logistics objectives

Cost – responsiveness

(Efficiency)

Safety & Quality –

food waste

Sustainability /

transparency

Technology

Infrastructure

Management

systems

People

Policy

PackagingProcessing and storage

systems

Sustainable vehicles

Cold chain

management facilities

Roads - corridors Agro/Eco-parks

Multimodal network

Quality standards &

Quality management

Operational excellence

Supply chain collaboration

Sustainable practices

Information exchange

Training on quality

management

Training on SCM and

logistics management

Training on

sustainability

Quality & food safety

Sanitary standards

Food waste reduction

Invest in infrastructure,

transportation

Effective regulations

Sustainable practices

Information exchange

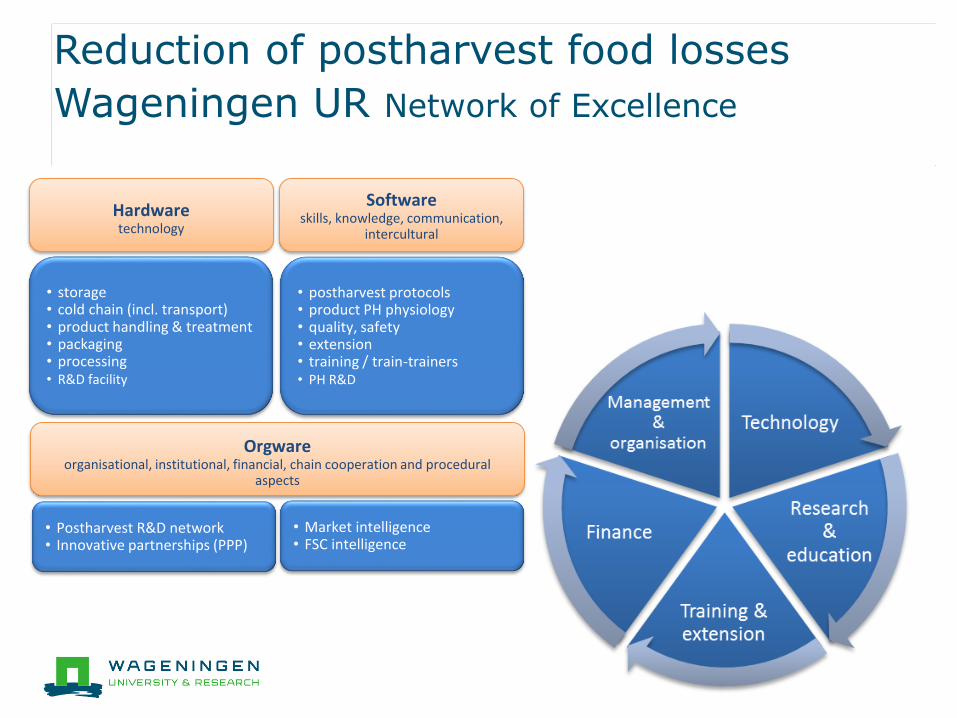

Reduction of postharvest food losses

Wageningen UR Network of Excellence

Hardwaretechnology

Softwareskills, knowledge, communication,

intercultural

Orgwareorganisational, institutional, financial, chain cooperation and procedural

aspects

• storage • cold chain (incl. transport)• product handling & treatment • packaging• processing• R&D facility

• postharvest protocols• product PH physiology• quality, safety • extension• training / train-trainers• PH R&D

• Postharvest R&D network • Innovative partnerships (PPP)

• Market intelligence • FSC intelligence

Outlook

1. Improving FULL logistics infrastructure

2. Enhancing quality management practices

3. Collaborative initiatives to increase (public & private)

investments for reducing postharvest losses

4. Encourage political willingness and good governance

5. Conduct extended Proof of Concept (PoC) studies

Key is to integrate all aspects into one vision.

Top Related