Languages

Pages

Legal

The preparation of the Financial Stability Review (FSR) is one of the avenues

through which Bank Indonesia achieves its mission “to safeguard the stability of the Indonesian

Rupiah by maintaining monetary and financial system stability for sustainable national

economic development”.

Publisher:

Bank Indonesia

Information and Orders:

This edition is published in March 2012 and is based on data and information available as of September 2011,unless stated otherwise.

Source: Bank Indonesia, unless stated otherwise.

The PDF format is downloadable from: http://www.bi.go.id

For inquiries, comments and feedback please contact:

Bank Indonesia

Department of Banking Research and Regulation

Financial System Stability Group

Jl.MH Thamrin No.2, Jakarta, Indonesia

Phone: (+62-21) 381 8902, 381 8075

Fax: (+62-21) 351 8629

Email: [email protected]

FSR is published biannually with the objectives:

To improve public insight in terms of understanding financial system stability.

To evaluate potential risks to financial system stability.

To analyze the developments of and issues within the financial system.

To offer policy recommendations to promote and maintain financial system stability.

Financial Stability Review

( No. 18, March 2012)

Directorate of Banking Research and Regulation

Financial System Stability Bureau

ii

iii

Table of Contents ......................................................................................................................................... ........... iii

Foreword .............. .................................................................................................................................................... vii

Overview ......... ......................................................................................................................................................... 3

Chapter 1. External and Internal Conditions .............................................................................................................. 5

1.1. Potential External Vulnerabilities ............................................................................................................... 7

1.2. Potential Internal Vulnerabilities ................................................................................................................ 8

Box 1.1. Household Behaviour ......................................................................................................................... 14

Chapter 2. Financial System Resilience ....................................................................................................................... 17

2.1. Structure and Resilience of the Financial System ....................................................................................... 19

2.2. Risk in the Banking System ....................................................................................................................... 20

2.3. Potential Financial Market Risk and Financing Risk .................................................................................... 29

Box 2.1 An Upgraded Sovereign Rating and Financial System Stability ............................................................. 38

Chapter 3. Challenges and Prospects of Financial System Stability .............................................................................. 41

3.1. Threat of Global Economic Slowdown on Indonesian Economy ................................................................ 43

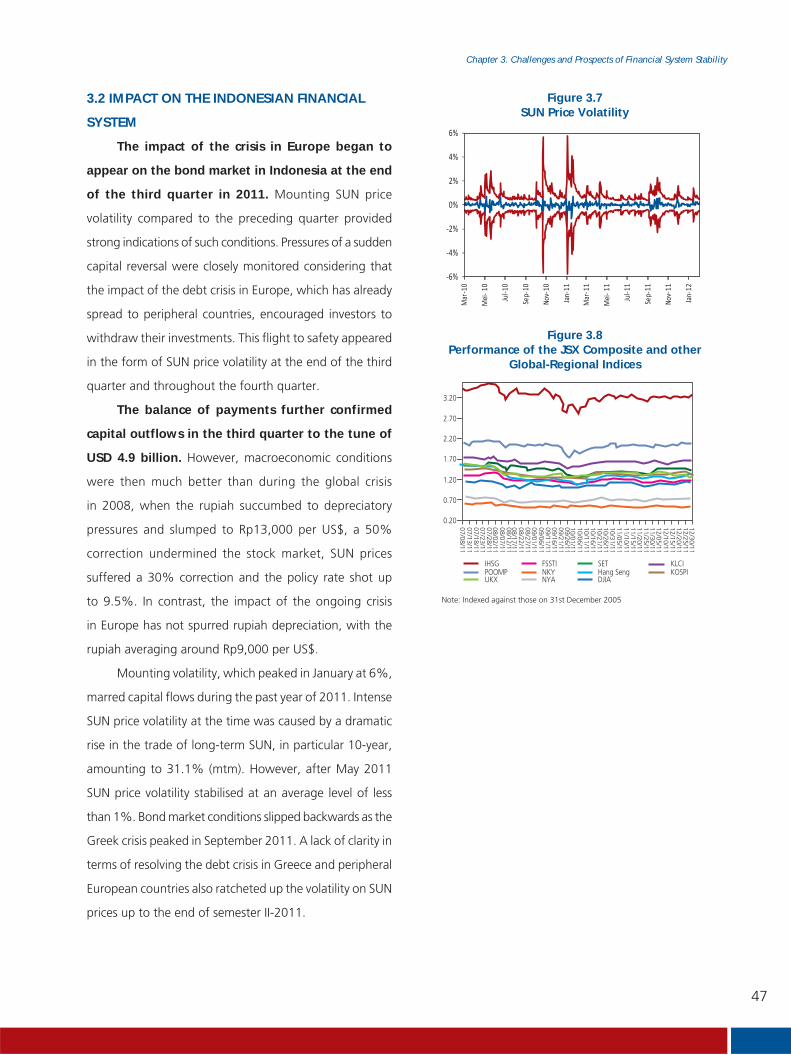

3.2. Impact on the Indonesian Financial System ............................................................................................... 47

3.3. Impact on the Banking Sector .................................................................................................................. 48

3.4. The Outlook of the Financial System Stability ............................................................................................ 49

Chapter 4. Topical Issues............................................................................................................................................ 51

4.1. Stress Testing the Impact of International Trade and Foreign Loans of the Corporation on Banks ................. 53

4.2. Strengthening Bank Capital as Part of the Efforts to Maintain Financial System Stability ........................... 56

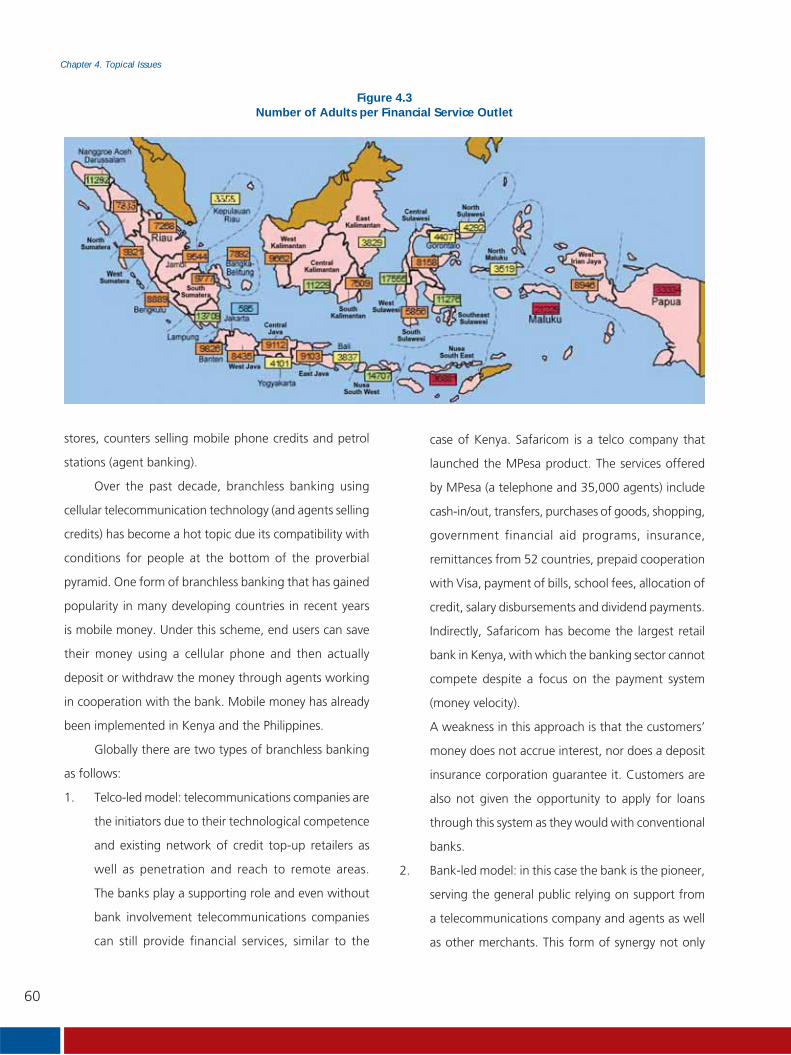

4.3. Broadening Public Access to Financial Services through Bank Network Expansion ..................................... 58

4.4. European Crisis ........................................................................................................................................ 63

Article ................ ...................................................................................................................................................... 67

Article 1 External Shocks, Macroeconomic Stability, and Monetary Regimes in the Small-open New Keynesian

Model of the Indonesian Economy .................................................................................................... 69

Article 2 Macroprudential and Microprudential Surveillance and Policies .......................................................... 79

Article 3 Determinants of the Household Liquidity Requirement in Indonesia: an Empirical Study with

Data from the Household Balance Sheet Survey ................................................................................ 95

Table of Contents

iv

1.1 Total Indonesian Exports and Imports .............. 71.2 International Commodity Prices (USD) ............. 71.3 Transition in the Share of Indonesia Exports ... 81.4 Confidence Index ........................................... 81.5 Inflation in several ASEAN Countries .............. 81.6 Composition of Direct Investment and Portfolio Investment to Indonesia ................... 91.7 Indonesia Balance of Payments ....................... 91.8 Rupiah Exchange Rate .................................... 91.9 Rupiah Exchange Rate Volatility ...................... 101.10 ROA and ROE of Non-Financial Public Listed Companies ..................................................... 111.11 DER and TL/TA of Non-Financial Public Listed Companies ..................................................... 111.12 Key Corporate Financial Indicators .................. 111.13 Credit and NPL to the Household Sector ......... 121.14 Composition of Credit to the Household Sector by Type (per December 2011) .............. 131.15 Performance of Credit to the Household Sector by Type ............................................... 131.16 NPL in Household Sector by Type ................... 13Figure Box 1.1.1 Composition of Total Household Spending 2009-2011 ..................................... 14Figure Box 1.1.2 Changes in Price (ytd) ..................... 14Figure Box 1.1.3 Sources of Household Debt ............. 15Figure Box 1.1.4 Composition of Household Assets ... 16

2.1 Asset Composition of Financial Institutions ..... 192.2 Financial Stability Index 1996-2011 ................ 202.3 Share of Bank Funding and Financing ............. 202.4 Growth in Deposits by Semester ..................... 202.5 Deposit Growth based on Ownership ............. 212.6 Composition of Bank Liquid Assets ................. 212.7 Share of Bank Placements at Bank Indonesia .. 212.8 Share of Liquid Assets .................................... 222.9 Credit Growth by Currency ............................ 222.10 Credit Funding by Currency ............................ 222.11 Credit Growth by Type ................................... 232.12 Credit Growth by Economic Sector ................. 232.13 Growth and Share of Property Credit ............. 232.14 Non-Performing Loans (NPL) ........................... 232.15 NPL Growth by Currency ................................ 242.16 NPL Ratio by Currency .................................... 24

List of Tables and Figures

Figures

1.1 Government Foreign Debt .............................. 101.2 Government Debt Service Ratio ...................... 101.3 Probability of Default using the Contingent Claims Analysis Method ................................. 12

2.1 Number of Financial Institutions ..................... 212.2 Liquid Assets Growth ..................................... 212.3 Profit/Loss of Banking Industry ....................... 262.4 Profitability and Credit by Bank Group ........... 262.5 Performance of the Prime Lending Rate ............ 282.6 SBN Ownership .............................................. 322.7 Financing sourced from Credit, Shares and Bonds ............................................................ 342.8 Financial Indicators of Finance Companies ...... 362.9 NPL by Type of Finance .................................. 362.10 Insurance Company Investment ...................... 37

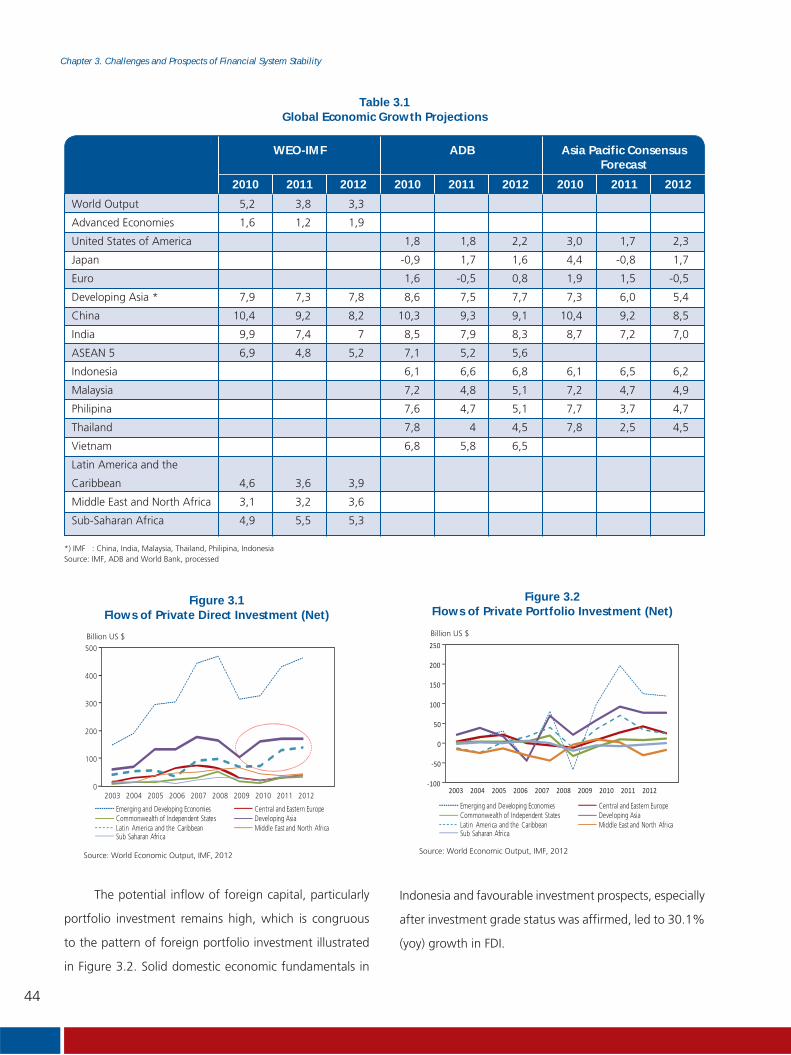

3.1 Global Economic Growth Projections .............. 443.2 Simulation of Easing Fuel Subsidies ................ 463.3 Projected GDP and Inflation ........................... 463.4 Stock Exchange Correlations .......................... 48

4.1 Summary of Results for Stress Test 1: Impact on Bank Liquidity ................................ 554.2 Summary of Results for Stress Test 2: Impact on Bank CAR and NPL ........................ 554.3 A Capital Comparison between Prevailing Regulations and the Requirements according to Basel III ...................................................... 574.4 Adoption of Financial Services ........................ 584.5 Access to Financial Services ............................ 59

Tables

v

2.17 NPL Growth by Credit Type ............................ 242.18 NPL Ratio by Credit Type ................................ 252.19 NPL Ratio by Economic Sector ........................ 252.20 NPL Ratio of Property Credit ........................... 252.21 Composition of Bank Profit/Loss ..................... 262.22 Composition of Interest Income for the Banking Industry (%) ...................................... 272.23 Rupiah Interest Rate Spread (%) ..................... 272.24 Bank ROA and BOPO (%) ............................... 272.25 Capital, the Minimum Statutory Reserve and Bank CAR ...................................................... 282.26 CAR by Bank Group (%) ................................ 282.27 MSM Credit Growth (yoy) .............................. 292.28 Non-Performing MSM Bank Loans (%) ........... 292.29 A Map of Financial System Stability ................ 302.30 Non-resident Flows of Shares, Government

Securities (SBN) and Bank Indonesia Certificates (SBI) ............................................. 302.31 SBN Prices by Tenor ........................................ 312.32 FR Benchmark Series SBN Prices ..................... 312.33 SBN VaR by Tenor .......................................... 312.34 SBN Price Volatility ......................................... 312.35 SBN Maturity Profile ....................................... 322.36 The JSX Composite and other Global Price Indices ............................................................ 322.37 The JSX Composite by Sector ......................... 322.38 Share Prices in the Banking Sector .................. 332.39 Stock Market Volatility in the Region .............. 332.40 Volatility on Regional Bourse .......................... 332.41 Mutual Fund by Type ..................................... 332.42 Issuers and Stock Issuances ............................ 342.43 Issuers and Corporate Bond Issuances ............ 342.44 Finance Company Performance ...................... 352.45 Share of Finance Company Financing ............. 352.46 Sources of Funds for Finance Companies ........ 352.47 Market Share of 11 Insurance Companies ...... 38Figure Box 2.1.1 Share of Foreign Ownership in January

2012 .............................................................. 39Figure Box 2.1.2 Inflows of Foreign Ownership to the

Indonesian Financial Market ........................... 393.1 Flows of Private Direct Investment (Net) .......... 443.2 Flows of Private Portfolio Investment (Net) ...... 44

3.3 Composition of Foreign Capital Inflows to Indonesia ....................................................... 453.4 Composition of Foreign Capital Inflows to Indonesia ....................................................... 453.5 Ratio of Credit to GDP in Indonesia, Malaysia, the Philippines and Thailand ............................ 463.6 Long-Term Trend of Credit to GDP ................. 463.7 SUN Price Volatility ......................................... 473.8 Performance of the JSX Composite and other Global-Regional Indices .................................. 473.9 Projected Credit Growth ................................ 493.10 Projected Growth in Deposits (% yoy) ............ 503.11 Financial Stability Index .................................. 50

4.1 Average projected Contraction on European Banks’ Balance Sheets .................... 644.1 European Bank Lending to Emerging Economies (in trillions of US$) ........................ 64

Figures Figures

vi

List of Abbreviations

ADB Asian Development BankAPBN Anggaran Pendapatan dan Belanja NegaraAS Amerika SerikatASEAN Association of Southeast Asian NationsATMR Aktiva Tertimbang Menurut RisikoBapepam- LK Badan Pengawas Pasar Modal dan Lembaga

KeuanganBCBS Basel Committee on Banking SupervisoryBIS Bank for International SettlementBNM Bank Negara MalaysiaBOPO Rasio Biaya Operasional terhadap

Pendapatan OperasionalBPD Bank Pembangunan DaerahBPR Bank Perkreditan RakyatBPRS Bank Perkreditan Rakyat Syariahbps basis pointBRC BPD Regional ChampionBRIC Brazil, Rusia, India, dan ChinaBUS Bank Umum SyariahCAR Capital Adequacy RatioCC Code of ConductCCP Central Counter PartiesCDS Credit Default SwapCRA Credit Rating AgencyCRBC China Banking Regulations CommissionsDER Debt to Equity RatioDPK Dana Pihak KetigaDSM Direktorat Statistik Ekonomi dan MoneterEFSF European Financial Stability FacilityETF Exchange-Traded FundEU European UnionFASB Financial Accounting Standard BoardFDI Foreign Direct InvestmentFSA Financial Service AuthorityFSAP Financial Sector Assessment ProgramFSB Financial Supervisory BoardFSI Financial Stability IndexG20 The Group of TwentyGDP Gross Domestic ProductGIM Gerakan Indonesia MenabungG-SIFI Global Systemically Important Financial

InstitutionsGWM Giro Wajib MinimumIAIS International Association of Insurance

SupervisorIASB International Accounting Standard BoardIDMA Inter-dealer Market AssociationIHK Indeks Harga KonsumenIHSG Indeks Harga Saham Gabungan

IMF International Monetary FundIOSCO International Organization of Securities

CommissionsJCI Jakarta Composite IndexJPSK Jaring Pengaman Sistem KeuanganKCBA Kantor Cabang Bank AsingKI Kredit InvestasiKK Kredit KonsumsiKMK Kredit Modal KerjaKPR Kredit Pemilikan RumahLBU Laporan Bulanan Bank UmumLC Letter of CreditLDR Loan to Deposit RatioL/R Laba RugiMEA Masyarakat Ekonomi ASEANMKM Mikro, Kecil, dan MenengahNAB Nilai Aktiva BersihNII Net Interest IncomeNIM Net Interest MarginNPF Non Performing FinancingNPI Neraca Pembayaran IndonesiaNPL Non Performing LoanOPEC Organization of the Petroleum Exporting

CountriesOTC Over the CounterPD Probability of DefaultPDB Produk Domestik BrutoPDN Posisi Devisa NetoPIIGS Portugal, Ireland, Italy, Greece and SpainPLN Pinjaman Luar NegeriPMA Penanaman Modal AsingPMDN Penanaman Modal Dalam NegeriPMK Peraturan Menteri KeuanganPMK BI Protokol Manajemen Krisis Bank IndonesiaPNS Pegawai Negeri SipilPP Perusahaan PembiayaanRBB Rencana Bisnis BankROA Return on Asset ROE Return on EquitySBDK Suku Bunga Dasar KreditSBI Sertifikat Bank IndonesiaSBN Surat Berharga NegaraSIFI Systemically Important Financial InstitutionsSUN Surat Utang NegaraTKI Tenaga Kerja IndonesiaTL/TA Rasio total kewajiban terhadap total aset TPI Tim Pengendalian InflasiTPID Tim Pengendalian Inflasi DaerahUMP Upah Minimum Provinsi

List of Abbreviations

ADB Asian Development BankAEC Asean Economic CommunityASEAN Association of Southeast Asian NationsBapepam- LK Capital market and Financial Institution

Supervisory BoardBCBS Basel Committee on Banking Supervisory

BIS Bank for International SettlementBEI Indonesia Stock Exchange

BNM Bank Negara MalaysiaBPD Regional Banksbps basis pointsBRC BPD Regional ChampionBRIC Brazil, Rusia, India, dan ChinaCAR Capital Adequacy RatioCC Code of ConductCCP Central Counter PartiesCDS Credit Default SwapCPI Consumer Price IndexCRA Credit Rating AgencyCRBC China Banking Regulations CommissionsDER Debt to Equity RatioEFSF European Financial Stability FacilityETF Exchange-Traded FundEU European UnionFASB Financial Accounting Standard BoardFDI Foreign Direct InvestmentFSA Financial Service AuthorityFSAP Financial Sector Assessment ProgramFSB Financial Supervisory BoardFSI Financial Stability IndexG20 The Group of TwentyGDP Gross Domestic ProductGIM Indonesian Saving MovementG-SIFI Global Systemically Important Financial

InstitutionsIAIS International Association of Insurance

SupervisorIASB International Accounting Standard BoardIDMA Inter-dealer Market AssociationIMF International Monetary FundIOSCO International Organization of Securities

CommissionsIHSG/JSXComposite

Jakarta Stock Exchange Index

JPSK Financial System Safety NetLBU Commercial Bank ReportLC Letter of CreditLDR Loan to Deposit RatioMSM Micro Small and Medium Credit

NII Net Interest IncomeNIM Net Interest MarginNOP Net Open PositionNPF Non Performing FinancingNPL Non Performing LoanOPEC Organization of the Petroleum Exporting

CountriesOTC Over the CounterPBI Bank Indonesia RegulationPD Probability of DefaultPIIGS Portugal, Ireland, Italy, Greece and SpainPMK BI Bank Indonesia’s Crisis Management

Protocol

ROA Return on Asset PUAB Interbank Money Market

ROE Return on EquitySBI Bank Indonesia CertificatesSBN Government SecuritiesSIFI Systemically Important Financial Institutions

SUN Government BondsSSB Securities

TL/TA Total Loss to Total Asset RatioUS United States of America UU Act

vii

Bank Indonesia publishes this 18th Edition of the Financial Stability Review (FSR), March 2012, as a form of

accountability and transparency regarding the task and function of Bank Indonesia in terms of maintaining financial

system stability. The publication is expected to assist stakeholders, particularly financial market players and policymakers,

monitor risk in the financial system at an early stage, while simultaneously helping to mitigate the risk.

This edition of the FSR contains information on financial system stability in Indonesia during the second half of

2011 and how the domestic financial system flourished despite the financial crisis in Europe. Financial system stability

bolstered national economic performance, thus prompting several international rating agencies to upgrade Indonesia’s

sovereign rating to investment grade.

The global economic slowdown and uncertainty surrounding crisis resolution in Europe had the potential to escalate

risk in the banking sector. Notwithstanding, the impact on the banking industry in Indonesia remained relatively limited

due to low exports from Indonesia to Europe as well as low domestic bank exposure to Europe. Meanwhile, banking sector

performance was positive, as reflected by adequate capital and stable profitability. Likewise, the performance of finance

companies also improved dramatically on the back of solid credit growth and the downward interest rate trend.

Nevertheless, vigilance and caution are still required looking forward considering that the direction of the global

economy can change in an instant, thereby exacerbating pressures on financial system stability. The impact of deleveraging

in the European banking sector, the efficacy of risk management and the possibility of mounting volatility on the stock

and bond markets all require closer attention, in addition to debtor performance and potential credit risk as well as an

increase in the intermediation function in productive sectors.

God willing the publication of FSR will always provide useful information to Bank Indonesia’s stakeholders, in particular

that regarding the results of research and monitoring conducted at Bank Indonesia pertinent to financial system stability.

We remain open to comments, recommendations and criticisms from any party in order to improve future editions of

the Financial Stability Review.

Jakarta, March 2012

GOVERNOR OF BANK INDONESIA

Darmin Nasution

Foreword

This page intentionally blank

Overview

1

Overview

2

Overview

This page intentionally blank

Overview

3

Financial system resilience and stability were well

preserved in Semester II 2011 despite encountering

pressure in the middle of the semester. The financial

crisis in Europe continued to overshadow risk in Indonesia

and globally, however, domestic markets and financial

institutions successfully absorbed the risk emanating from

global and domestic shocks. The success of Indonesia in

terms of maintaining financial system stability was clearly

appreciated by a couple of rating agencies, namely Fitch

and Moody’s, who upgraded Indonesia’s sovereign rating

to investment grade. This upgrade will surely translate into

capital for Indonesia in the face of potential risk looking

ahead.

Externally, a slowdown in the global economy

and uncertainty surrounding crisis resolution in

Europe had the potential to amplify risk in the

banking sector. Europe slipping into a moderate recession

as a result of fiscal consolidation, bank deleveraging and

the sovereign debt crisis prompted the IMF and World Bank

to revise down their global economic growth projections

from 4% and 3.6% to 3.25% and 2.8% respectively. Such

conditions undermined global demand and precipitated

a decline in exports from developing countries, including

Indonesia. Notwithstanding, the impact on the domestic

banking industry was limited because Indonesian exports

and exposure to Europe were relatively small. Concerning

foreign capital inflows, investment portfolio to Indonesia

experienced a decline but Foreign Direct Investment (FDI)

surged in line with solid domestic economic prospects.

Domestically, real sector performance was

steady. Global economic shocks had no significant

impact on the corporate sector in Indonesia. The corporate

probability of default indeed increased compared to the

same position in the preceding year with profitability

placed under increasing pressure. Nonetheless, the level of

corporate debt also tended to decline; hence, as a whole,

risk in the corporate sector was well managed. Meanwhile,

public confidence in the economy and the downward

interest rate trend encouraged the household sector

to increase its level of debt and consumption. This was

demonstrated by robust credit growth to the household

sector for mortgages and automotive loans compared to

other types of loan. Although credit performed well in the

reporting period, concerns emerged over the rapid pace

of consumption loans, which has the potential to create

problems at a later date.

The domestic financial market responded well

to pressures in Semester II 2011, fully recovering by

the close of the year. Greater risk aversion from global

investors had an impact on the domestic financial market.

The price of government securities (SBN) experienced

a significant decline before rebounding and stabilising

with monetary operations that concomitantly maintained

stability on the rupiah interbank money market (PUAB).

On the capital market, the JSX Composite and net asset

value (NAV) of mutual funds came under pressure but

market confidence was fully restored by the end of the

year. Financing through the capital market, primarily

Bab 1 Overview

4

Overview

shares, slumped due to the wait-and-see attitude of

potential issuers.

The banking industry and finance companies

performed steadily. Bank capital remained at a level

considered adequate to absorb risk as the global crisis

unfolded. Profitability was stable supported by a decline

in the cost of loan loss provisions as well as a wider net

interest margin for the banks. Meanwhile, rupiah and

foreign exchange credit grew rapidly in nearly all economic

sectors. The performance of finance companies also

improved significantly, the majority of which stemmed

from consumer financing for the purchase of motor

vehicles. This was buttressed by solid credit performance

as well as the downward interest rate trend.

RISK OUTLOOK

The outlook for the financial system in Indonesia

up to Semester I 2012 is more stable compared to

Semester II 2011. If they materialise, the impact of oil

price hikes in semester I 2012 will be felt in the subsequent

semester, while foreign capital flows are expected to

stabilise thus alleviating volatility on the financial market. In

addition, measures to improve prudence are also expected

to ease bank credit risk.

Nevertheless, global economic and political dynamics,

which can change in the blink of an eye, demand greater

prudence. Consequently, the banking sector and financial

market players are expected to:

• Remain alert to the deleveraging process of banks in

Europe, which has the potential to undermine credit

lines as well as USD interbank lending.

• Conduct stress tests and review liquidity contingency

plans in order to mitigate liquidity risk, in particular

for banks that depend heavily on global wholesale

funding.

• Augment risk management and stay alert to the

possibility of mounting volatility on the stock and

bond markets.

• Monitor the performance of borrowers who depend

heavily on trade with countries that are currently

experiencing difficulties.

• Remain alert to the possibility of escalating

consumption credit risk in the household sector and

enhance the intermediation function in productive

sectors.

Caution is advised in terms of maintaining adequate

liquidity amid the apparent trend of slower growth in

deposits and accelerated credit growth.

5

Chapter 1. External and Internal Conditions

Chapter 1External and Internal Conditions

6

Chapter 1. External and Internal Conditions

This page intentionally blank

7

Chapter 1. External and Internal Conditions

1.1 POTENTIAL EXTERNAL VULNERABILITIES

Mounting risk from the crisis in Europe has left

future domestic economic growth uncertain. External

risk factors, such as the sovereign debt crisis in the euro zone

and economic slowdowns in developed countries, sparked

risk in the domestic economy. Recent developments in the

euro area have indicated signs of contagion to surrounding

and trade partner countries, primarily through banks and

the economy. Consequently, the IMF revised down its

global economic growth projection from 4% to 3.25%.

The economy of Indonesia responds to changes in external

conditions, therefore, domestic economic activity could

also have experienced a slight contraction.

The economic slowdown was also attributable

to specific problems affecting certain countries.

Japan, for instance, contracted from positive 4% growth

to minus 0.9%, principally as a result of the earthquake in

March 2011. The disaster destroyed physical infrastructure,

thereby disrupting production activity, knocked out

electricity supply from the stricken nuclear power plant

and undermined consumption. Brazil, which had posted

impressive 7.5% growth in 2010, only achieved 2.9% in

2011 due to an array of structural problems that forced

the adoption of a tight monetary policy stance, prudential

policy that curbed credit growth and fiscal policy that failed

to provide economic stimuli.

This turmoil, which shows no signs of abating,

persisted in the form of fiscal policy in the US, while Europe

consistently failed to agree how to overcome the fiscal and

financial problems in financial crisis struck PIIGS countries,

as well as the second bailout for Greece that has still not

been approved by the Greek Parliament. By yearend 2011

several rating agencies downgraded the sovereign ratings

of the US and nine European countries, which spurred

increasingly risk averse sentiment from global investors.

Chapter 1 External and Internal Conditions

Source: Indonesian Financial Statistics, Bank Indonesia

Source: Indonesian Financial Statistics, Bank Indonesia

Figure 1.1Total Indonesian Exports and Imports

Figure 1.2International Commodity Prices (USD)

Million USD

-

4.000

2.000

8.000

6.000

12.000

10.000

16.000

14.000

18.000

20.000

Total Export Total Import

Feb-

07A

pr-0

7Ju

n-07

Aug

-07

Oct

-07

Dec

-07

Feb-

08A

pr-0

8Ju

n-08

Aug

-08

Oct

-08

Dec

-08

Feb-

09A

pr-0

9Ju

n-09

Aug

-09

Oct

-09

Dec

-09

Feb-

10A

pr-1

0Ju

n-10

Aug

-10

Oct

-10

Dec

-10

Feb-

11A

pr-1

1Ju

n-11

Aug

-11

Oct

-11

Dec

-11

0

200

400

600

800

1000

1200

1400

Dec-

06M

ar-0

7Ju

n-07

Sep-

07De

c-07

Mar

-08

Jun-

08Se

p-08

Dec-

08M

ar-0

9Ju

n-09

Sep-

09De

c-09

Mar

-10

Jun-

10Se

p-10

Dec-

10M

ar-1

1Ju

n-11

Sep-

11De

c-11

0

50

100

150

200

250

Natural Gas Palm Oil Coal (right) Crude Oil (right)

8

Chapter 1. External and Internal Conditions

Source: Survey conducted by the Directorate of Economic and Monetary Statistics, Bank Indonesia

Source: Indonesian Financial Statistics, Bank Indonesia

Source: Bloomberg

6.10% posted in 2010, on the back of public confidence

and business player confidence. This was further

corroborated by the increase in the consumer confidence

index1 in December 2011, which peaked at its highest level

in three years, namely 116.6 (Figure 1.4).

Figure 1.5Inflation in several ASEAN Countries

Figure 1.4Confidence Index

Figure 1.3Transition in the Share of Indonesia Exports

0%

5%

10%

15%

20%

25%

Japan China India ASEAN US Europe Others

2000 2005 2011

Consumer Confidence IndexCurrent Economic Conditions IndexConsumer Expectations Index

(Index)140

130

120

110

100

90

80

70

60 1 2 3 4 5 6 7 8 9 10 11 12

2009

1 2 3 4 5 6 7 8 9 10 11 12

2010

1 2 3 4 5 6 7 8 9 10 11 12

2011

Average weightedfor 18 cities

-6

-2

-4

2

0

4

6

10

8

14

yoy (%)

12

Jan

- 07

Apr -

07

Jun

- 07

Oct -

07

Jan

- 08

Apr -

08

Jun

- 08

Oct -

08

Jan

- 09

Apr -

09

Jun

- 09

Oct -

09

Jan

- 10

Apr -

10

Jun

- 10

Oct -

10

Jan

- 11

Apr -

11

Jun

- 11

Oct -

11

Philippines Malaysia Thailand Indonesia

1 Based on the results of the 2011 BI Consumer Survey.

1.2 POTENTIAL INTERNAL VULNERABILITIES

1.2.1 Macroeconomic Conditions and the Real Sector

Although not as high as the preceding year, the

performance of exports from Indonesia remained

positive. Based on Bank Indonesia data, during Semester

II 2011 exports from Indonesia grew by 6%, totalling

USD 201.5 billion for the year, which is up by 27.5% on

the previous year. Imports in Semester II 2011 also grew

more slowly compared to the previous semester at 10%,

achieving USD 166.1 billion (fob) for the year, which is

an increase of 30% over the preceding year. The decline

in exports was chiefly due to a slump in the commodity

prices of mainstay exports from Indonesia like palm oil,

crude oil and coal.

Slower export growth has already begun to

affect Indonesia but on a relatively small scale. The

rise in imports exceeded the rise in exports, thereby eroding

the current account surplus at the end of Semester II 2011

compared to the previous semester (Figure 1.1 and Figure

1.2). Posting a surplus amid the recession in Europe was

possible by increasingly diversified export destinations from

Indonesia, with the current trend of favouring emerging

market countries (Figure 1.3).

Low inflation helped catalyse business activity. In

terms of prices, headline inflation in Semester II 2011

tended to ease well below the inflation target of 5%

±1. Headline inflation was 3.79% (yoy) at the end of

the semester (Figure). A downward inflation trend was

reported in many countries; however, Indonesia remained

as the country with the highest level of inflation in

ASEAN-5.

Solid international trade and strong domestic

consumption buoyed economic growth. Six point five

percentgrowth was achievedin 2011, which exceeded the

9

Chapter 1. External and Internal Conditions

in Indonesia increased on the previous year from 47% to

76%, while the portion of portfolio investment contracted

from 53% to 24% (Figure 1.6). The sectors that enjoyed

the most additional direct investment in Semester II 2011

were the manufacturing sector totalling USD 529 million,

real estate, leasing and business services with USD 369

million and the agricultural sector amounting to USD 92

million.

The balance of payments recorded a surplus of

US$11.9 billion overall for the year despite relatively

intense pressures in Semester II. Foreign exchange reserves

in Indonesia at the end of Semester II 2011 amounted to

USD 110.12 billion, which is equivalent to 6.4 months of

imports and government foreign debt repayments. This

figure is smaller than the position recorded at the end of

Semester I 2011, namely USD 119.7 billion but larger than

yearend 2010 at USD 96.2 billion.

Market risk had the potential to escalate due to

the weak rupiah coupled with mounting exchange rate

volatility. In harmony with the balance of payments, the

rupiah exchange rate depreciated by around 114 points

compared to the previous semester to a level of Rp8,825

per USD (Figure 1.8) at the end of 2011. Furthermore,

average exchange rate volatility was also more pronounced

compared to the previous semester, increasing from 0.18%

(Figure 1.9) to 0.25%.

1.2.2 Investment and the Balance of Payments

The impact of a decline in portfolio investment

growth on the financial market required close monitoring.

Investment flows into Indonesia in Semester II 2011 were

negative, indicating investment outflow totalling USD 5.4

billion. The torrent of investment outflow was due to risk

averse global investors appearing in the second half of

2011 following prolonged and widespread uncertainty

surrounding the fiscal problems in Greece and the languid

recovery in the US. Notwithstanding, overall in 2011

investment flowing into Indonesia remained positive

amounting to USD 14 billion; down 47.2% on the previous

year.

Source: Indonesian Financial Statistics, Bank Indonesia

Figure 1.6Composition of Direct Investment and Portfolio

Investment to Indonesia

Figure 1.7Indonesia Balance of Payments

0%

20%

30%

10%

40%

50%

70%

60%

90%

80%

2005 2006

Direct Investment Portfolio Investment

2007 2008 2009 2010 2011

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1*Q2*Q3*Q4*

2006 2007 2008 2009 2010 2011

-10000

-5000

0

5000

10000

15000

FDI PI Other Investment Financial Account

Direct investment is expected to drive economic

activity and the financial market. Based on share, the

share of direct investment (FDI) against total investment Source: Bloomberg, processed

Figure 1.8Rupiah Exchange Rate

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12

2008 2009 2010 2011

Monthly Average Quarterly Average Semesterly Average

10

Chapter 1. External and Internal Conditions

The government debt to service ratio increased

slightly but the government implemented measures

to gradually reduce its debt while simultaneously

seeking low-risk sources of finance. Pressures from a

slowdown in exports also undermined the debt to service

ratio of Indonesia from 22.5% to 27.3% (Table 1.2). The

upgraded rating affirmed for Indonesia at the end of 2011

is expected to encourage the return of investment flows,

thereby meeting the domestic requirement for foreign

exchange. The ratio of debt to GDP dropped to 25% in

2011 and is scheduled to slide further to 22% in 2014.

Source: Bloomberg, processed

Source: Indonesian Financial Statistics, Bank Indonesia

Figure 1.9Rupiah Exchange Rate Volatility

1.2.3 Condition of the Public Sector

The budget deficit remained below the safe

threshold of 3% of GDP. The state budget (APBN) for

Semester II 2011 posted a deficit of Rp88.3 trillion (2.1%

of GDP), far below the target deficit of Rp150.8 trillion.

A reduction in the budget deficit was possible through

the higher-than-expected collection of non-tax revenues,

while central government spending in 2011 only reached

96.7% of the 2011 APBN-P.

The smaller deficit provided the government

leeway to reduce domestic and foreign debt, thereby

reinforcing fiscal posture in terms of stimulating

development. At the end of Quarter III 2011 government

foreign debt had reached USD 112.96 billion; equivalent

to Rp1,002 trillion at a rate of Rp8,875/1USD.

Amid ubiquitous uncertainty surrounding global

economic conditions, the government needs to create

- 1,5

- 1

- 0,5

0

0.5

1

1.5

Volatility

Lower Limit

1 31 61 91 121 151 181 211 241 271

Upper Limit Actual

253 days Period

Table 1.1Government Foreign Debt

Dec-09 Nov-11Jun-10 Dec-10 Jun-11

Central

Government 90.853 97.571 106.860 114.887 112.962

Monetary

Authority 8.412 8.126 11.764 13.222 10.272

Total 99.265 105.697 118.624 128.109 123.234

millions of USD

Table 1.2Government Debt Service Ratio

Q-I Q-I

2010 2011

Q-II Q-IIQ-III Q-IIIQ-IV Q-IV

Foreign Exchange Reserves 71.823 76.321 86.551 96.207 105.709 119.655 114.503 110.123

In months of imports and foreign

debt repayments 6,7 6,0 6,9 7,2 7,4 7,2 7,1 6,4

Debt Service Ratio (%) 21,2% 23,2% 20,3% 23,7% 18,0% 22,5% 21,2% 27,3%

a more enabling environment for domestic economic

growth, which can be achieved through greater

government spending, particularly that which enhances

the investment climate and boosts the income of the

general public.

11

Chapter 1. External and Internal Conditions

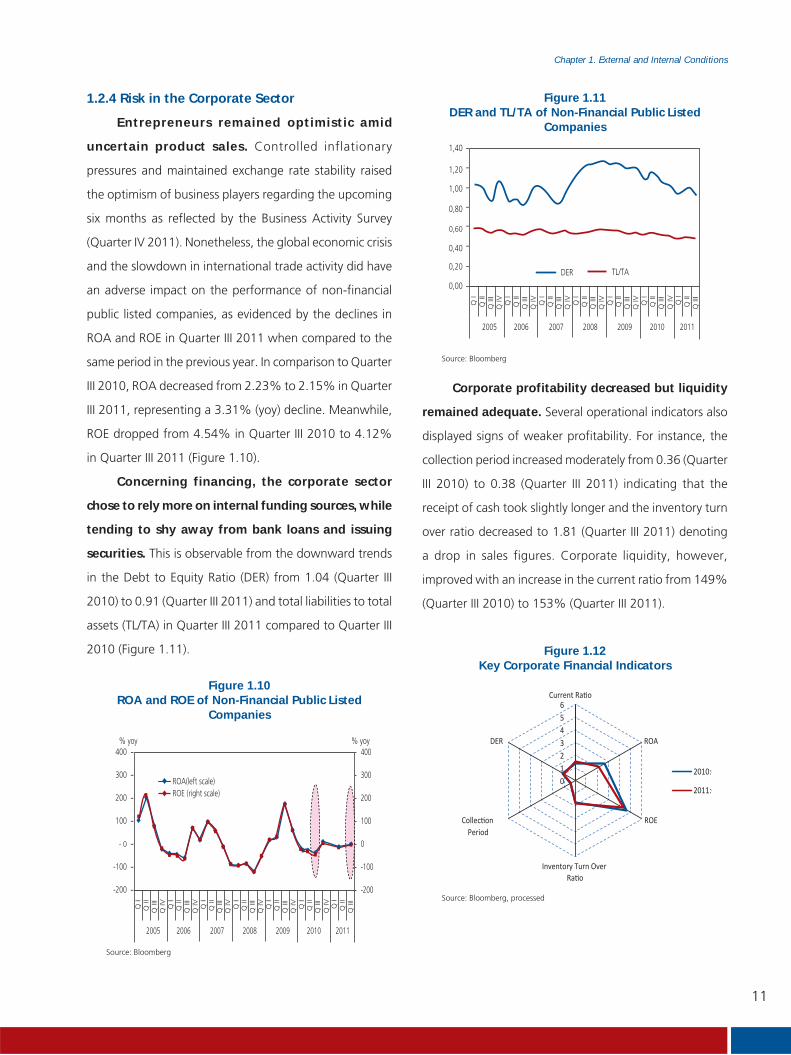

1.2.4 Risk in the Corporate Sector

Entrepreneurs remained optimistic amid

uncertain product sales. Controlled inflationary

pressures and maintained exchange rate stability raised

the optimism of business players regarding the upcoming

six months as reflected by the Business Activity Survey

(Quarter IV 2011). Nonetheless, the global economic crisis

and the slowdown in international trade activity did have

an adverse impact on the performance of non-financial

public listed companies, as evidenced by the declines in

ROA and ROE in Quarter III 2011 when compared to the

same period in the previous year. In comparison to Quarter

III 2010, ROA decreased from 2.23% to 2.15% in Quarter

III 2011, representing a 3.31% (yoy) decline. Meanwhile,

ROE dropped from 4.54% in Quarter III 2010 to 4.12%

in Quarter III 2011 (Figure 1.10).

Concerning financing, the corporate sector

chose to rely more on internal funding sources, while

tending to shy away from bank loans and issuing

securities. This is observable from the downward trends

in the Debt to Equity Ratio (DER) from 1.04 (Quarter III

2010) to 0.91 (Quarter III 2011) and total liabilities to total

assets (TL/TA) in Quarter III 2011 compared to Quarter III

2010 (Figure 1.11).

Corporate profitability decreased but liquidity

remained adequate. Several operational indicators also

displayed signs of weaker profitability. For instance, the

collection period increased moderately from 0.36 (Quarter

III 2010) to 0.38 (Quarter III 2011) indicating that the

receipt of cash took slightly longer and the inventory turn

over ratio decreased to 1.81 (Quarter III 2011) denoting

a drop in sales figures. Corporate liquidity, however,

improved with an increase in the current ratio from 149%

(Quarter III 2010) to 153% (Quarter III 2011).

Source: Bloomberg

Figure 1.10ROA and ROE of Non-Financial Public Listed

Companies

-200

-100

0

100

200

300

400

- 0

-200

-100

100

200

300

400

Q I

Q II

Q II

IQ

IV Q I

Q II

Q II

IQ

IV Q I

Q II

Q II

IQ

IV Q I

Q II

Q II

IQ

IV Q I

Q II

Q II

IQ

IV Q I

Q II

Q II

I

Q II

Q II

I

Q IV Q

I

2005 2006 2007 2008 2009 2010 2011

% yoy% yoy

ROA(left scale)ROE (right scale)

Source: Bloomberg

Figure 1.11DER and TL/TA of Non-Financial Public Listed

Companies

0,60

0,00

0,20

0,40

0,80

1,00

1,20

1,40

Q I

Q II

Q II

IQ

IV Q I

Q II

Q II

IQ

IV Q I

Q II

Q II

IQ

IV Q I

Q II

Q II

IQ

IV Q I

Q II

Q II

IQ

IV Q I

Q II

Q II

I

Q II

Q II

I

Q IV Q

I

2005 2006 2007 2008 2009 2010 2011

DER TL/TA

Figure 1.12Key Corporate Financial Indicators

0123456

ROA

ROE

Inventory Turn Over

DER

2010:Q

2011:Q

Source: Bloomberg, processed

12

Chapter 1. External and Internal Conditions

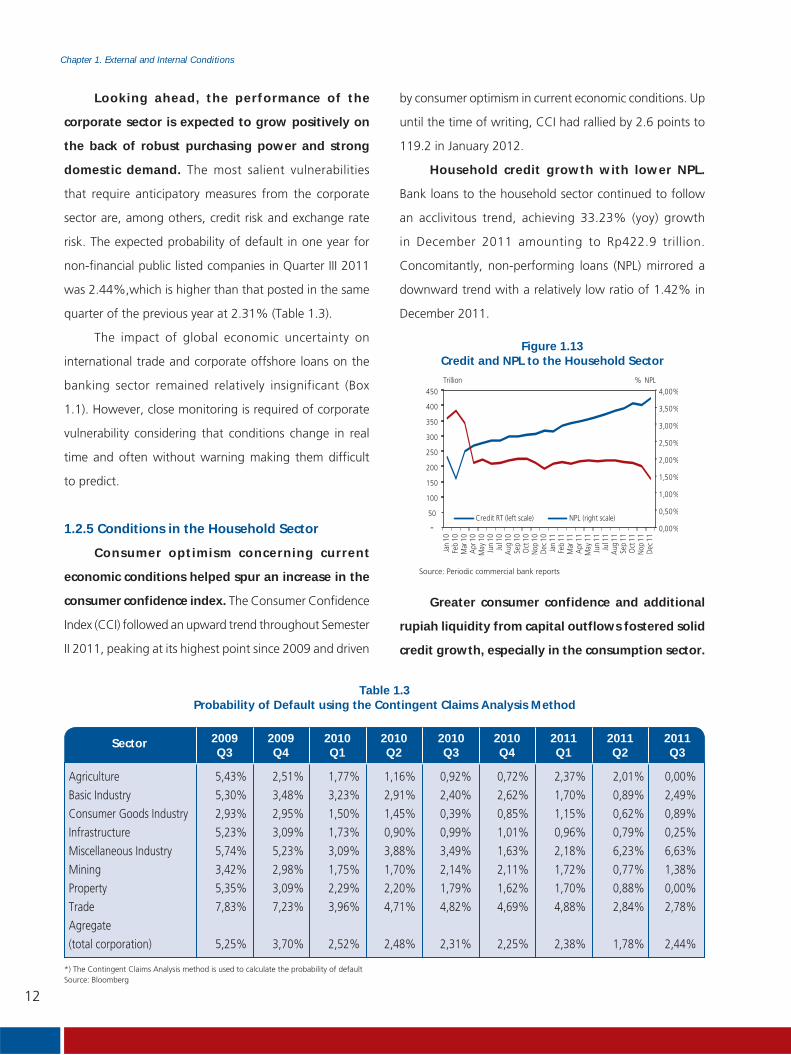

Looking ahead, the performance of the

corporate sector is expected to grow positively on

the back of robust purchasing power and strong

domestic demand. The most salient vulnerabilities

that require anticipatory measures from the corporate

sector are, among others, credit risk and exchange rate

risk. The expected probability of default in one year for

non-financial public listed companies in Quarter III 2011

was 2.44%,which is higher than that posted in the same

quarter of the previous year at 2.31% (Table 1.3).

The impact of global economic uncertainty on

international trade and corporate offshore loans on the

banking sector remained relatively insignificant (Box

1.1). However, close monitoring is required of corporate

vulnerability considering that conditions change in real

time and often without warning making them difficult

to predict.

1.2.5 Conditions in the Household Sector

Consumer optimism concerning current

economic conditions helped spur an increase in the

consumer confidence index. The Consumer Confidence

Index (CCI) followed an upward trend throughout Semester

II 2011, peaking at its highest point since 2009 and driven

by consumer optimism in current economic conditions. Up

until the time of writing, CCI had rallied by 2.6 points to

119.2 in January 2012.

Household credit growth with lower NPL.

Bank loans to the household sector continued to follow

an acclivitous trend, achieving 33.23% (yoy) growth

in December 2011 amounting to Rp422.9 trillion.

Concomitantly, non-performing loans (NPL) mirrored a

downward trend with a relatively low ratio of 1.42% in

December 2011.

Table 1.3Probability of Default using the Contingent Claims Analysis Method

2009Q3

Sector 2009Q4

2010Q1

2011Q1

2010Q2

2011Q2

2010Q3

2011Q3

2010Q4

Agriculture 5,43% 2,51% 1,77% 1,16% 0,92% 0,72% 2,37% 2,01% 0,00%

Basic Industry 5,30% 3,48% 3,23% 2,91% 2,40% 2,62% 1,70% 0,89% 2,49%

Consumer Goods Industry 2,93% 2,95% 1,50% 1,45% 0,39% 0,85% 1,15% 0,62% 0,89%

Infrastructure 5,23% 3,09% 1,73% 0,90% 0,99% 1,01% 0,96% 0,79% 0,25%

Miscellaneous Industry 5,74% 5,23% 3,09% 3,88% 3,49% 1,63% 2,18% 6,23% 6,63%

Mining 3,42% 2,98% 1,75% 1,70% 2,14% 2,11% 1,72% 0,77% 1,38%

Property 5,35% 3,09% 2,29% 2,20% 1,79% 1,62% 1,70% 0,88% 0,00%

Trade 7,83% 7,23% 3,96% 4,71% 4,82% 4,69% 4,88% 2,84% 2,78%

Agregate

(total corporation) 5,25% 3,70% 2,52% 2,48% 2,31% 2,25% 2,38% 1,78% 2,44%

*) The Contingent Claims Analysis method is used to calculate the probability of defaultSource: Bloomberg

Source: Periodic commercial bank reports

Figure 1.13Credit and NPL to the Household Sector

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

3,00%

3,50%

4,00%

50

100

150

200

250

300

350

400

450

Jan

10Fe

b10

Mar

10A

pr10

May

10Ju

n10

Jul1

0A

ug10

Sep

10O

ct10

Nop

10De

c10

Jan

11Fe

b11

Mar

11A

pr11

May

11Ju

n11

Jul1

1A

ug11

Sep

11O

ct11

Nop

11De

c11

% NPLTrillion

Credit RT (left scale) NPL (right scale)

Greater consumer confidence and additional

rupiah liquidity from capital outflows fostered solid

credit growth, especially in the consumption sector.

13

Chapter 1. External and Internal Conditions

Based on type, most credit to the household sector

(46.68%) was in the form of mortgages, followed by

motor vehicle loans (24.99%), multipurpose loans (24.9%)

and others. The upward growth trend for mortgages and

motor vehicle loans outpaced that of bank loans in general.

Referring to the position in December 2011 for instance,

mortgages grew by 34% (yoy), while bank loans only

achieved 23% (yoy). In fact, motor vehicle loans grew by

an impressive 62.2% on the previous year. Although the

NPL ratio for mortgages and motor vehicle loans remained

relatively low, more specifically at 0.9% and 0.8%

respectively in December 2011, the current downward

interest rate trend together with more widespread public

optimism regarding economic conditions have led to

concerns over excessive public euphoria when applying

for consumption loans. This is possible due to pragmatic

bank behaviour in favouring the allocation of consumption

credit. Countercyclical measurement should be considered

to prevent this, which can curb excessively rapid growth

in mortgages and motor vehicle loans.

Source: Bloomberg, processed

Figure 1.14Composition of Credit to the Household Sector by

Type (per December 2011)

Housing46,68%

motor vehicle24,99%

household appliances0,58%

Multipurpose24,90%

Others2,86%

Source: Periodic commercial bank reports

Figure 1.15Performance of Credit to the Household Sector

by Type

-

50

100

150

200

250

Jan

10Fe

b10

Mar

10A

pr10

May

10Ju

n10

Jul1

0A

ug10

Sep

10O

ct10

Nop

10De

c10

Jan

11Fe

b11

Mar

11A

pr11

May

11Ju

n11

Jul1

1A

ug11

Sep

11O

ct11

Nop

11De

c11

Trillion Rupiah

Housing Motor vehicle Household appliances Multipurpose Others

Sumber: LBU

Grafik 1.16NPL in Household Sector by Type

10 10 10 10 10 10 10 10 10 10 10 10 11 11 11 11 11 11 11 11 11 11 11 11

Percent

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

8,0%

9,0%

Jan

Feb

Mar

Apr

May Jun Jul

Aug Se

pO

ctNo

pDe

cJa

nFe

bM

arA

prM

ay Jun Jul

Aug Se

pO

ctNo

pDe

c

Housing Motor vehicle Household appliances Multipurpose Others

14

Chapter 1. External and Internal Conditions

Household Behaviour

Since 2007, Bank Indonesia has routinely

conducted an annual survey of household balance

sheets (Survei NRT). The survey is performed because

economic dynamics and financial system stability in a

country are not merely influenced by macroeconomic

variables but also by specific household factors like

spending, debt and assets.

1. Spending

prices of basic necessities increased, households tended

to allocate spending to basic needs while reducing

spending on non-essential items2. Conversely, in the

event of lower prices the household sector tended to

spend more on non-essential items. This trend can

be observed from a couple of surveys conducted by

Bank Indonesia. In 2010 when food prices soared,

the portion of spending on staple foods increased

from 30% to 33% while non-essential consumption

declined.

In 2011, the share of spending allocated

to basic necessities, in particular food staples

and transportation, declined again. An increase

in spending on basic necessitieswas only reported for

clothing and fashion, as a result of a significant hike

in the price of clothing from 1.85% (2010) to 3.63%

(2011).

Figure Box 1.1.1Composition of Total Household Spending

2009-2011

Food

2009

Wealth accumulation

Transportation, vehiclemaintenance, fuelDebt repaymentsEducationOthers

Food

2010

Debt repayments

Transportation, vehiclemaintenance, fuelElectricity, water,communicationsEducationOthers

Food

2011

Debt repayments

EducationClothing and FashionElectricity, waterOthers

The household sector remained sufficiently

flexible in terms of adjusting its composition of

spending when faced with price hikes. When the

Figure Box 1.1.2 Changes in Price (ytd)

Source: Survey of Household Balance Sheets

Percent

-6,00

-4,00

-2,00

0,00

2,00

4,00

6,00

8,00

2009 2010 2011

Foodstuffs Processed foodsHouses, electricity, water, gas ClothingHealth Education and recreation

Transportation andcommunications

2 Basic Necessities: Clothing, food, housing, transportation, electricity and water. Everything else is considered a non-essential item.

15

Chapter 1. External and Internal Conditions

More moderate food price hikescompared to

2010 as well as easing inflationary pressures in Semester

II 2011 were addressed by the household sector with

increased spending on non-essential items. Most

growth in spending on non-essential items affected

the celebration of religious festivities and vacations,

which increased by 25.85%, followed by the purchase

of motor vehicles (17%) and the purchase of durable

household goods that could be resold(14%).

The increase in spending on clothing and fashion,

motor vehicles and durable household appliances is

thought to be the result of lower interest rates as well

as increased public optimism regarding the domestic

economy. This is congruous with the results of the

consumer confidence index (CCI) survey, which showed

that in December 2011 CCI peaked at 116.6, its highest

level for the past three years.

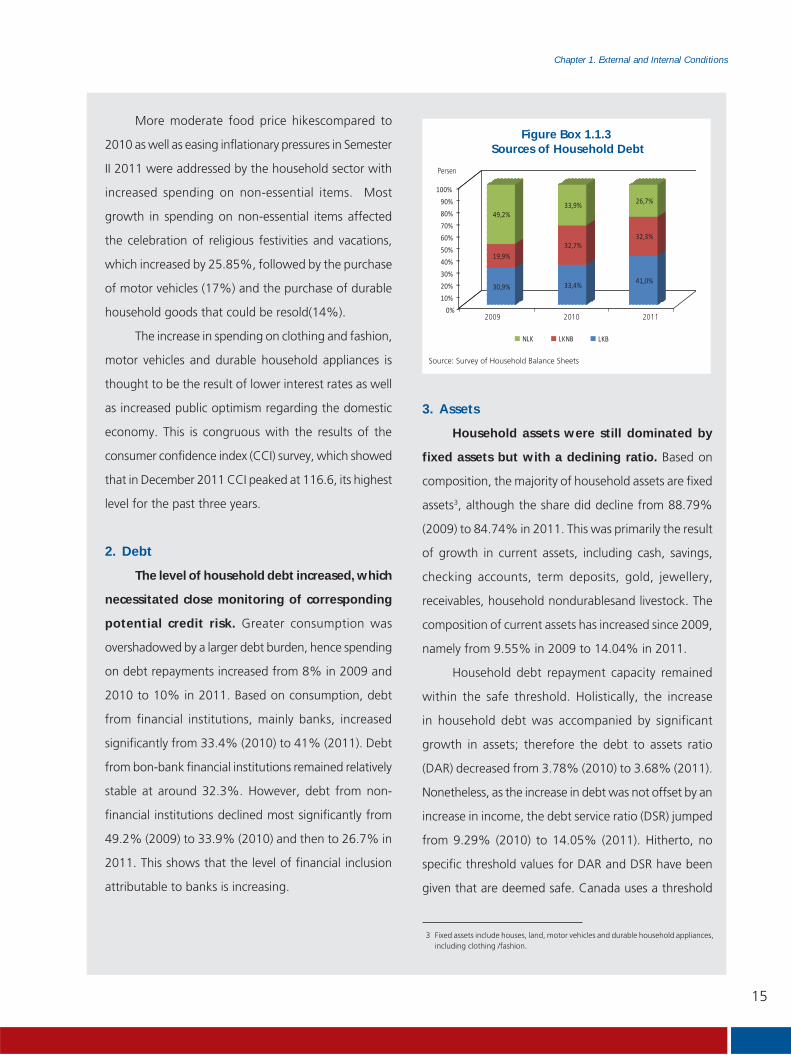

2. Debt

The level of household debt increased, which

necessitated close monitoring of corresponding

potential credit risk. Greater consumption was

overshadowed by a larger debt burden, hence spending

on debt repayments increased from 8% in 2009 and

2010 to 10% in 2011. Based on consumption, debt

from financial institutions, mainly banks, increased

significantly from 33.4% (2010) to 41% (2011). Debt

from bon-bank financial institutions remained relatively

stable at around 32.3%. However, debt from non-

financial institutions declined most significantly from

49.2% (2009) to 33.9% (2010) and then to 26.7% in

2011. This shows that the level of financial inclusion

attributable to banks is increasing.

Figure Box 1.1.3 Sources of Household Debt

Source: Survey of Household Balance Sheets

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

30,9% 33,4%41,0%

19,9%32,7%

32,3%

49,2%33,9% 26,7%

NLK LKNB LKB

Persen

2009 2010 2011

3. Assets

Household assets were still dominated by

fixed assets but with a declining ratio. Based on

composition, the majority of household assets are fixed

assets3, although the share did decline from 88.79%

(2009) to 84.74% in 2011. This was primarily the result

of growth in current assets, including cash, savings,

checking accounts, term deposits, gold, jewellery,

receivables, household nondurablesand livestock. The

composition of current assets has increased since 2009,

namely from 9.55% in 2009 to 14.04% in 2011.

Household debt repayment capacity remained

within the safe threshold. Holistically, the increase

in household debt was accompanied by significant

growth in assets; therefore the debt to assets ratio

(DAR) decreased from 3.78% (2010) to 3.68% (2011).

Nonetheless, as the increase in debt was not offset by an

increase in income, the debt service ratio (DSR) jumped

from 9.29% (2010) to 14.05% (2011). Hitherto, no

specific threshold values for DAR and DSR have been

given that are deemed safe. Canada uses a threshold

3 Fixed assets include houses, land, motor vehicles and durable household appliances, including clothing /fashion.

16

Chapter 1. External and Internal Conditions

of 80% for DAR, which is categorised as high, while

Davaney (1994) used a benchmark DSR of 30%.

The current persistent downward interest rate

trend has stimulated public consumption as reflected

by an increase in certain types of consumption credit

that far outpaced that of credit growth in general.

Accordingly, appropriate macroprudential policy

is required to ease the rate of consumption credit

growth.

Figure Box 1.1.4 Composition of Household Assets

Source: Survey of Household Balance Sheets

Percent

2009 2010 2011

9,55% 10,86% 13,38%0,11% 0,41%0,34%1,09% 0,24%0,25%

88,79% 88,27% 85,46%

0,47% 0,22% 0,60%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Other Assets Fixed assetsInvestment

Restricted assets, Current assets

17

Chapter 2. Financial System Resilience

Chapter 2Financial System Resilience

18

Chapter 2. Financial System Resilience

This page intentionally blank

19

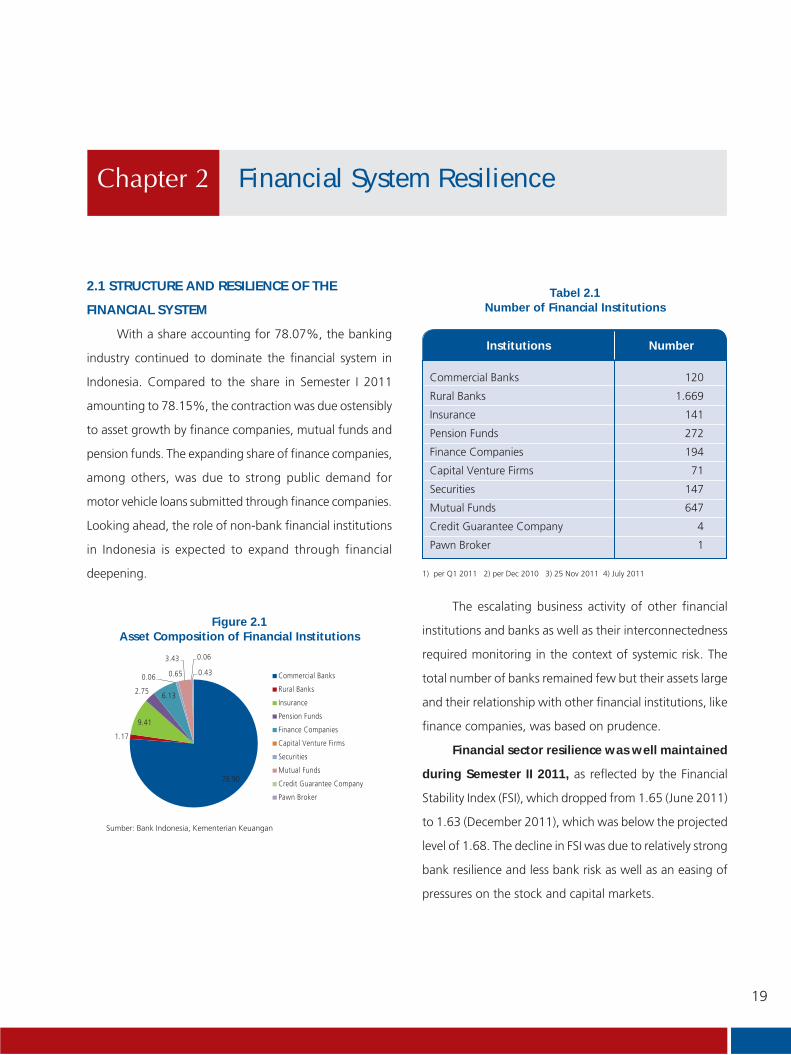

Chapter 2. Financial System Resilience

The escalating business activity of other financial

institutions and banks as well as their interconnectedness

required monitoring in the context of systemic risk. The

total number of banks remained few but their assets large

and their relationship with other financial institutions, like

finance companies, was based on prudence.

Financial sector resilience was well maintained

during Semester II 2011, as reflected by the Financial

Stability Index (FSI), which dropped from 1.65 (June 2011)

to 1.63 (December 2011), which was below the projected

level of 1.68. The decline in FSI was due to relatively strong

bank resilience and less bank risk as well as an easing of

pressures on the stock and capital markets.

76.90

1.17

9.41

2.75 6.13

0.06 0.65

3.43 0.06

0.43 Commercial Banks

Rural Banks

Insurance

Pension Funds

Finance Companies

Capital Venture Firms

Securities

Mutual Funds

Credit Guarantee Company

Pawn Broker

Financial System Resilience

2.1 STRUCTURE AND RESILIENCE OF THE

FINANCIAL SYSTEM

With a share accounting for 78.07%, the banking

industry continued to dominate the financial system in

Indonesia. Compared to the share in Semester I 2011

amounting to 78.15%, the contraction was due ostensibly

to asset growth by finance companies, mutual funds and

pension funds. The expanding share of finance companies,

among others, was due to strong public demand for

motor vehicle loans submitted through finance companies.

Looking ahead, the role of non-bank financial institutions

in Indonesia is expected to expand through financial

deepening.

Sumber: Bank Indonesia, Kementerian Keuangan

Figure 2.1Asset Composition of Financial Institutions

Institutions Number

Tabel 2.1Number of Financial Institutions

Commercial Banks 120

Rural Banks 1.669

Insurance 141

Pension Funds 272

Finance Companies 194

Capital Venture Firms 71

Securities 147

Mutual Funds 647

Credit Guarantee Company 4

Pawn Broker 1

1) per Q1 2011 2) per Dec 2010 3) 25 Nov 2011 4) July 2011

20

Chapter 2. Financial System Resilience

2.2. RISK IN THE BANKING SYSTEM

2.2.1. Funding and Liquidity Risk

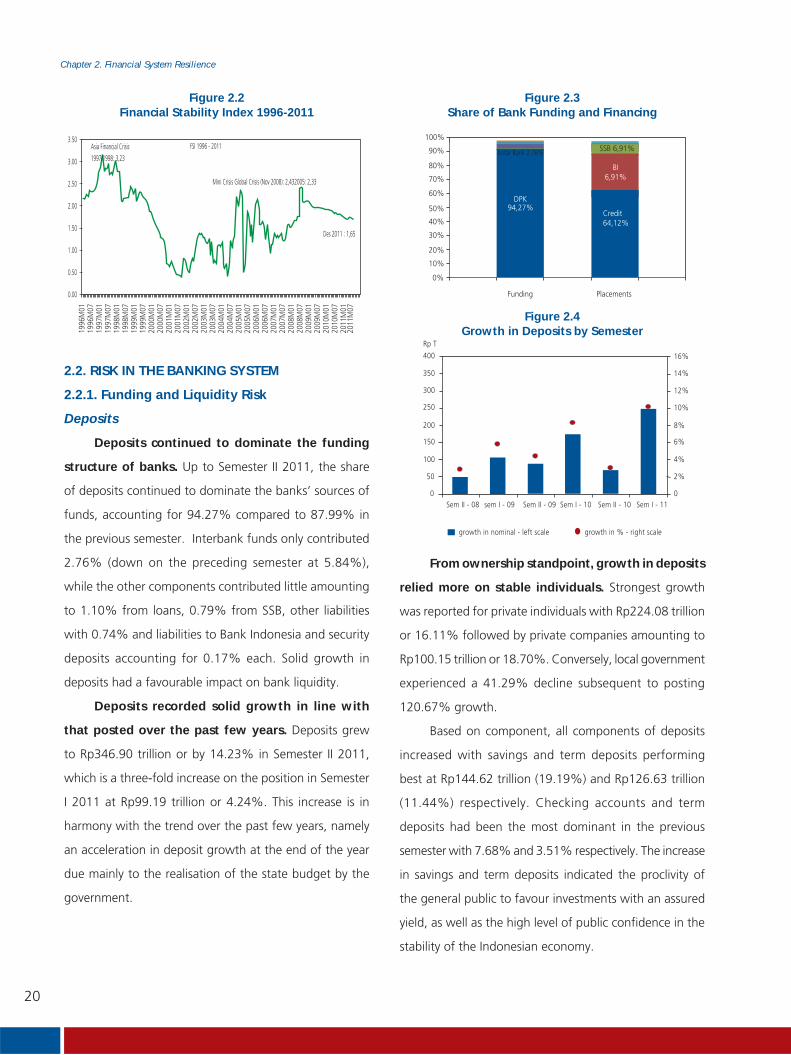

Deposits

Deposits continued to dominate the funding

structure of banks. Up to Semester II 2011, the share

of deposits continued to dominate the banks’ sources of

funds, accounting for 94.27% compared to 87.99% in

the previous semester. Interbank funds only contributed

2.76% (down on the preceding semester at 5.84%),

while the other components contributed little amounting

to 1.10% from loans, 0.79% from SSB, other liabilities

with 0.74% and liabilities to Bank Indonesia and security

deposits accounting for 0.17% each. Solid growth in

deposits had a favourable impact on bank liquidity.

Deposits recorded solid growth in line with

that posted over the past few years. Deposits grew

to Rp346.90 trillion or by 14.23% in Semester II 2011,

which is a three-fold increase on the position in Semester

I 2011 at Rp99.19 trillion or 4.24%. This increase is in

harmony with the trend over the past few years, namely

an acceleration in deposit growth at the end of the year

due mainly to the realisation of the state budget by the

government.

Figure 2.2Financial Stability Index 1996-2011

94,27%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Funding Placements

DPK

Antar Bank 2,76%

Credit64,12%

SSB 6,91%

BI6,91%

0

100

50

250

200

150

300

350

400

0

6%

4%

2%

12%

10%

8%

14%

16%

Sem II - 08 sem I - 09 Sem II - 09 Sem I - 10 Sem II - 10 Sem I - 11

Rp T

growth in nominal - left scale growth in % - right scale

Figure 2.3Share of Bank Funding and Financing

Figure 2.4Growth in Deposits by Semester

From ownership standpoint, growth in deposits

relied more on stable individuals. Strongest growth

was reported for private individuals with Rp224.08 trillion

or 16.11% followed by private companies amounting to

Rp100.15 trillion or 18.70%. Conversely, local government

experienced a 41.29% decline subsequent to posting

120.67% growth.

Based on component, all components of deposits

increased with savings and term deposits performing

best at Rp144.62 trillion (19.19%) and Rp126.63 trillion

(11.44%) respectively. Checking accounts and term

deposits had been the most dominant in the previous

semester with 7.68% and 3.51% respectively. The increase

in savings and term deposits indicated the proclivity of

the general public to favour investments with an assured

yield, as well as the high level of public confidence in the

stability of the Indonesian economy.

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

1996

M01

1996

M07

1997

M01

1997

M07

1998

M01

1998

M07

1999

M01

1999

M07

2000

M01

2000

M07

2001

M01

2001

M07

2002

M01

2002

M07

2003

M01

2003

M07

2004

M01

2004

M07

2005

M01

2005

M07

2006

M01

2006

M07

2007

M01

2007

M07

2008

M01

2008

M07

2009

M01

2009

M07

2010

M01

2010

M07

2011

M01

2011

M07

Des 2011 : 1,65

Asia Financial Crisis

1997/1998: 3,23

Mini Crisis Global Crisis (Nov 2008): 2,432005: 2,33

FSI 1996 - 2011

21

Chapter 2. Financial System Resilience

0

250

200

150

100

50

-50

-100

Centr

al Go

vernm

ent

Local

Gov

ernme

ntPri

vate i

ndivid

uals

Privat

e - Fin

ancia

l Instit

ution

sPri

vate C

ompa

nies

Othe

r priv

ate

Non-r

eside

nts

Rp T

semester I 2011 semester II 2010

Figure 2.5Deposit Growth based on Ownership

Primary ReservesTertiary Reserve

Secondary ReserveLiquid Assets (right)

0

600

Rp T Rp T

400

200

1,100

1,000

900

800

700

600

Dec

- 1

0

Jan -

11

Feb -

11

Mar

- 1

1

Apr

- 11

Mey

- 1

1

Jun -

11

Aug -

11

Sep -

11

Oct

- 1

1

Nov

- 11

Dec

- 1

1

Jul -

11

Figure 2.6Composition of Bank Liquid Assets

Table 2.2Total Number of Financial Institutions

Growth ytdDec

2011(Rp T)

Nominal(Rp T)

Nominal(Rp T)

% %

Growth yoy

Primary Reserves 314.09 37.78 13.67 87.55 38.65

Secondary Reserves 663.41 114.67 20.90 96.80 17.08

Tertiary Reserves 69.24 (3.12) (4.32) (4.76) (6.43)

Total 1,046.74 149.32 16.64 179.59 20.71

* The components of liquid assets above has not exclude primary reserve obligation

Based on currency, growth in deposits was

contributed by those denominated in rupiah as well as

foreign currency. Rupiah deposits grew during the reporting

semester to Rp305.50 trillion or 88.06% of total growth

in deposits, while dollar deposits accounted for Rp41.40

trillion or 11.94% of the total. This increase in dollar deposits

exceeded the Rp3.26 trillion contraction experienced in the

previous semester.

Liquidity Risk

The growth in liquid assets (16.64%) outpaced

that of deposits (14.23%). Total bank liquid assets

increased by 16.64% in Semester II 2011 to Rp1,046.74

trillion. The growth in liquid assets stemmed primarily from

the increase in secondary reserves consisting of SBI, other

placements at Bank Indonesia, Trading SUN and available-

for-sale SUN making up 20.90% and an increase in primary

reserves comprising of cash and checking accounts held

at Bank Indonesia amounting to 13,67%. Meanwhile,

the banks’ tertiary reserves declined in Semester II 2011

by 4.32%.

The increase in bank secondary reserves was

principally due to an increase in other placements at

Bank Indonesia (consisting of the Deposit Facility and Call

Money) and increases in Trading SUN.

BI Checking Account Placements in other BI instrumentsSBI

0%

100%

Rp T

90%80%70%60%50%40%30%20%10%

Dec-1

0

Jan-1

1

Feb-

11

Mar-

11

Apr-1

1

May

-11

Jun-

11

Jul-1

1

Aug-1

1

Sep-

11

Oct-11

Nov-1

1

Dec-1

1

Figure 2.7Share of Bank Placements at Bank Indonesia

22

Chapter 2. Financial System Resilience

Bank liquidity remained adequate to meet the

corresponding liabilities. The AL/NCD ratio increased

from 182.34% to 184.70% compared to the position

at the end of Semester I 2011. This was due chiefly to

a significant increase in liquid assets in Semester II 2011

despite an uneven spread of liquidity and funds. The

majority of liquid assets and deposits were held by 14 large

banks with a share accounting for more than 70%, while

116 other banks shared less than 30% between them.

In terms of liquidity risk, the level of liquid

assets held to anticipate deposit withdrawals was

adequate. Based on the results of stress tests, no individual

bank had the potential to experience liquidity shortfalls

under a scenario of a 5% decline in deposits (during the

2008 crisis average deposit withdrawals reached 5%).

Meanwhile, when compared to conditions at the end of

December 2008, the position of individual banks in terms

of covering the withdrawal of non-core deposits continued

to improve. In this context, there remained many banks

with a ratio of liquid assets to non-core deposits in excess

of 100% and not one bank had a ratio below 50%.

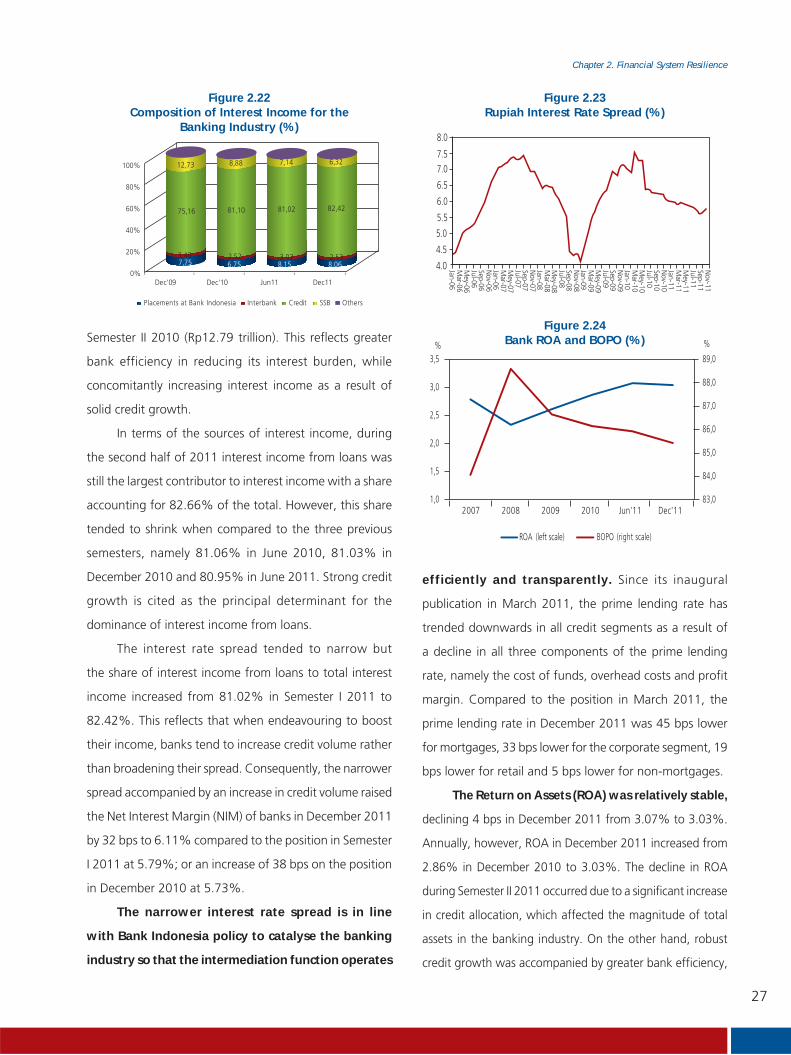

2.2.2. Credit Risk and Performance

Credit Performance

Bank loans to productive sectors increased.

Credit grew by 12.78% in the second semester of 2011 or

24.59% for the year (yoy), which exceeded that recorded

in the same semester of the preceding year at 11.3%.

The acceleration in credit growth in Semester II 2011 was

linked to increasingly conducive economic conditions that

allowed the banks to allocate more credit, especially to

productive sectors.

Foreign exchange denominated credit grew

rapidly by 16.2%, up on the previous semester.

Rapid forex credit growth has endured since Semester II

2010, which seemed inextricably linked to the trend of

rupiah appreciation. Consequently, banks are urged to

remain cautious of risks stemming from a weaker rupiah

that could undermine the debt repayment capacity of

borrowers and eventually lead to non-performing loans.

Forex credit was financed in Semester II 2011 by liquidating

86%

7%

4% 3%1%

1_mo

1_3_mo

3_6_mo

6_12_mo

12_mo

50,5

(29,7)

8,3

Loans

Interbank (Net)

Placement at BI

(3,6)

(5,5)

41,4

(40)(20) 0 20 40 60

Other Liabilities

Borrowing

Total Deposits

Rp T

Figure 2.10Credit Funding by Currency

Figure 2.9Credit Growth by Currency

9.7%

21.0%

11.3%9.9%

13.6%

10.5%12.1%

16.2%

12.8%

0%

5%

10%

15%

20%

25%

Rupiah FX Total

sem II/10 sem I/11 sem II/11

Liquid Assetsof 14 Large Bank

73%

Other BankLiquid Unit

27%

Deposits of14 Large Bank72%

Other BankDeposits

28%

Share of liquid assetsin the banking industry

Share of Funds inthe banking industry

Figure 2.8Share of Liquid Assets

23

Chapter 2. Financial System Resilience

interbank foreign exchange funds that tended to be short

term in nature, while foreign exchange deposits actually

experienced positive growth. Unstable global economic

conditions stemming from the protracted debt crisis in

Europe and the slowdown in the US encouraged bankers to

opt for foreign exchange funds to finance domestic credit

allocation. Therefore, the banking sector must remain

vigilant of such funding sources due to the possibility of

a mismatch, which has the potential to trigger additional

losses in the exchange rate.

The role of credit to productive sectors was

relatively dominant during Semester II 2011.

Compared to the prior semester, investment credit grew

by 14.1% to Rp464.3 trillion, working capital credit grew

by 13.6% to Rp1,068.7 trillion, and consumption credit

by 10.6% to Rp667.12 trillion. Solid investment credit

growth is expected to benefit the real sector and contribute

to national economic growth. Nevertheless, the banking

15.8%

6.8%

13.6%

3.5%

16.8%

14.1%

9.7%

12.3%

10.6%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

sem II/10 sem I/11 sem II/11

Working capital credit Investment credit Consumption credit

Figure 2.11Credit Growth by Type

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Agric

ultu

re

Min

ing

Man

ufac

turin

gIn

dust

ry

Elec

tric

ity

Cons

truc

tion

Trad

e

Tran

spor

tatio

n

Buss

ines

sSe

rvic

e

Soci

al S

ervi

ce

Oth

ers

sem II/10 semI/11 semII/11

Figure 2.12Credit Growth by Economic Sector

0

10

20

30

40

50

60

0

1

2

3

4

5

6

2007 2008 2009 2010 2011

RpT%Loan Loss Provisions

(right-hand scale)

Nominal NPL (right-hand scale)

Gross NPL(left-hand scale)Net NPL

(left-hand scale)

0%

2%

4%

6%

8%

10%

12%

14%

16%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2004 2005 2006 2007 2008 2009 2010 2011

Share of property credit against total credit (right-hand scale)

Property credit growth (yoy) (left-hand scale)

Figure 2.13Growth and Share of Property Credit

Figure 2.14Non-Performing Loans (NPL)

sector must continue to closely monitor investment credit

risk, particularly in terms of bank funding sources that

tend to be short term while the majority of investment

credit tends to be longer term. Meanwhile, based on

sector, all productive sectors grew positively compared

to June 2011.

Growth in property credit, which collapsed in

2009, rebounded in the middle of 2010. Property credit

growth in Semester II 2011 increased by 12.4% or 23.8%

(yoy), which exceeded that posted in Semester I 2011 at

just 10.1% or 17.8% (yoy) as well as that reported for

the same position a year earlier at 7% or 15.5% (yoy).

The share of property credit in total bank credit remained

relatively small at 13.1% of the total. However, with a

large unmet requirement from residents for housing,

property credit and especially mortgages will have further

opportunity to flourish.

24

Chapter 2. Financial System Resilience

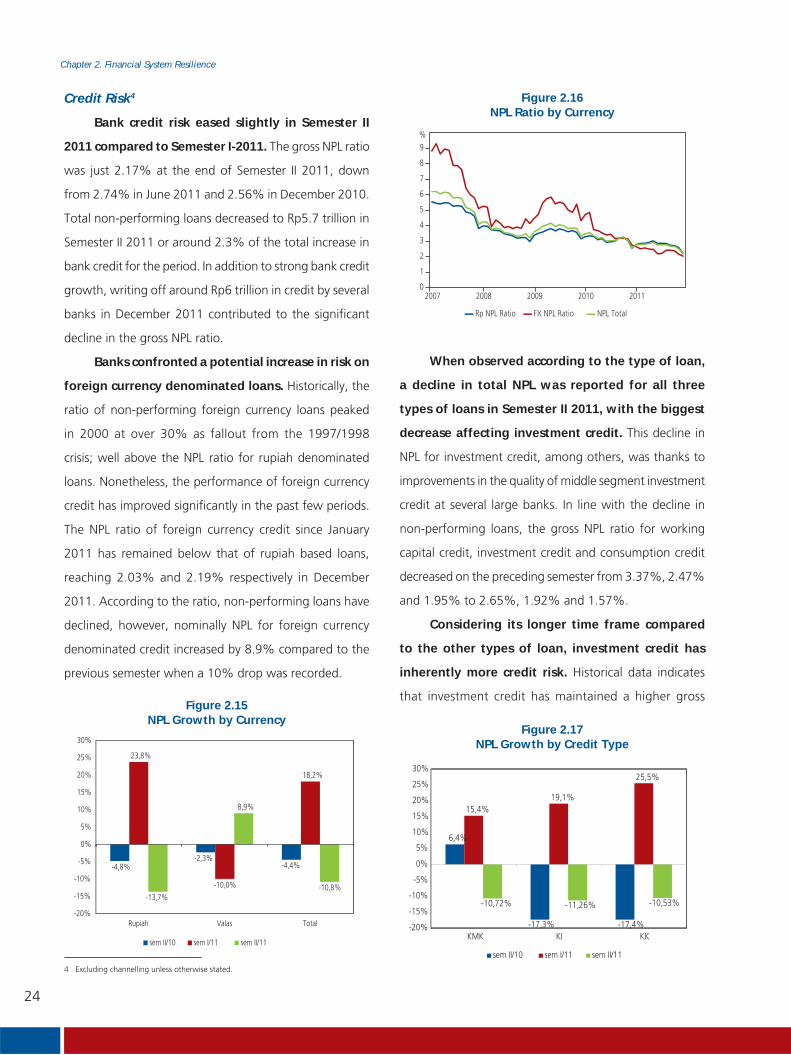

Credit Risk4

Bank credit risk eased slightly in Semester II

2011 compared to Semester I-2011. The gross NPL ratio

was just 2.17% at the end of Semester II 2011, down

from 2.74% in June 2011 and 2.56% in December 2010.

Total non-performing loans decreased to Rp5.7 trillion in

Semester II 2011 or around 2.3% of the total increase in

bank credit for the period. In addition to strong bank credit

growth, writing off around Rp6 trillion in credit by several

banks in December 2011 contributed to the significant

decline in the gross NPL ratio.

Banks confronted a potential increase in risk on

foreign currency denominated loans. Historically, the

ratio of non-performing foreign currency loans peaked

in 2000 at over 30% as fallout from the 1997/1998

crisis; well above the NPL ratio for rupiah denominated

loans. Nonetheless, the performance of foreign currency

credit has improved significantly in the past few periods.

The NPL ratio of foreign currency credit since January

2011 has remained below that of rupiah based loans,

reaching 2.03% and 2.19% respectively in December

2011. According to the ratio, non-performing loans have

declined, however, nominally NPL for foreign currency

denominated credit increased by 8.9% compared to the

previous semester when a 10% drop was recorded.

6,4%

-17,3% -17,4%

15,4%19,1%

25,5%

-10,72% -11,26% -10,53%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

KKKIKMK

sem II/10 sem I/11 sem II/11

Figure 2.17NPL Growth by Credit Type

0

1

2

3

4

5

6

7

8

9

2007 2008 2009 2010 2011

%

Rp NPL Ratio FX NPL Ratio NPL Total

-4,8%-2,3%

-4,4%

23,8%

-10,0%

18,2%

-13,7%

8,9%

-10,8%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Rupiah Valas Total

sem II/10 sem I/11 sem II/11

Figure 2.15NPL Growth by Currency

Figure 2.16NPL Ratio by Currency

When observed according to the type of loan,

a decline in total NPL was reported for all three

types of loans in Semester II 2011, with the biggest

decrease affecting investment credit. This decline in

NPL for investment credit, among others, was thanks to

improvements in the quality of middle segment investment

credit at several large banks. In line with the decline in

non-performing loans, the gross NPL ratio for working

capital credit, investment credit and consumption credit

decreased on the preceding semester from 3.37%, 2.47%

and 1.95% to 2.65%, 1.92% and 1.57%.

Considering its longer time frame compared

to the other types of loan, investment credit has

inherently more credit risk. Historical data indicates

that investment credit has maintained a higher gross

4 Excluding channelling unless otherwise stated.

25

Chapter 2. Financial System Resilience

0

3

6

9

12

2007 2008 2009 2010 2011

%

consumptioncredit

Investmentcredit

workingcapital credit

Figure 2.18NPL Ratio by Credit Type

Figure 2.19NPL Ratio by Economic Sector

0

2

4

6

8

10

2007 2008 2009 2010 2011

%

Agriculture Mining Manufacturing Industry Electricity Construction

0

2

4

6

8

10

2007 2008 2009 2010 2011

%

Trade Transportation Business Services Social Services Others

NPL ratio than the other two types of loan since the year

2000. However, since 2009 the NPL ratio of investment