Languages

Pages

Legal

1

“ TRANSFORM RISK INTO VALUE.... ”

Effective Financial Asset Effective Financial Asset Management & Trading with Management & Trading with VaRVaR

DusitDusit DomethongDomethongVice President, ThaiBDC

Pornpan Pornpan SakulsrivichaiSakulsrivichaiAssistant Manager, ThaiBDC

2

OutlineOutline1. Introducing to VaR concept2. How to apply VaR in Asset Management & Trading

2.1 Financial Risk ManagementExposure and VaR limit

(by applying asset allocation and selection techniques)Market Risk Charge Correlation Break Down

2.2 Portfolio Management and PerformanceRAROCRisk Attribution

2.3 VaR application to Non-Financial Sectors 3. Conclusion

3

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

What is VaR?

VaR summarizes the worst loss over a target horizon with a given level of confidencee.g. Max loss of 1-day holding period at 99% confidence level.

4

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

VaRVaR is just the is just the leftleft side of the pictureside of the picture..What is theWhat is the rightright sideside??

Fx Portfolio's 10-day Profit & Loss (Additive Approach)

05

1015

2025

P&L

Freq

uenc

y

0.00000

0.00010

0.00020

0.00030

0.00040

Prob

abilit

y

Histogam's Frequency (Left) Probability of P&L (right)

Danger Opportunity

5

Backward-looking Question:How much we gained today?

Forward-looking Question:How much could we lose tomorrowHow much could we lose tomorrow??a) xxxx,,xxxxxx BahtBaht But how could you know about

tomorrow?b) VaRVaR is the answer!

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

VaRVaR DefinitionDefinitionSuppose we just closed our positions of all trading Suppose we just closed our positions of all trading portfoliosportfolios.. Then answer the following questionsThen answer the following questions..

6

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

How to apply How to apply VaRVaR in Asset in Asset Management & TradingManagement & Trading

Financial Risk ManagementExposure and VaR LimitTop management can apply Financial Risk Concept to

control and monitor organization’s risk from top-down and set policy by using VaR as a tool.

7

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

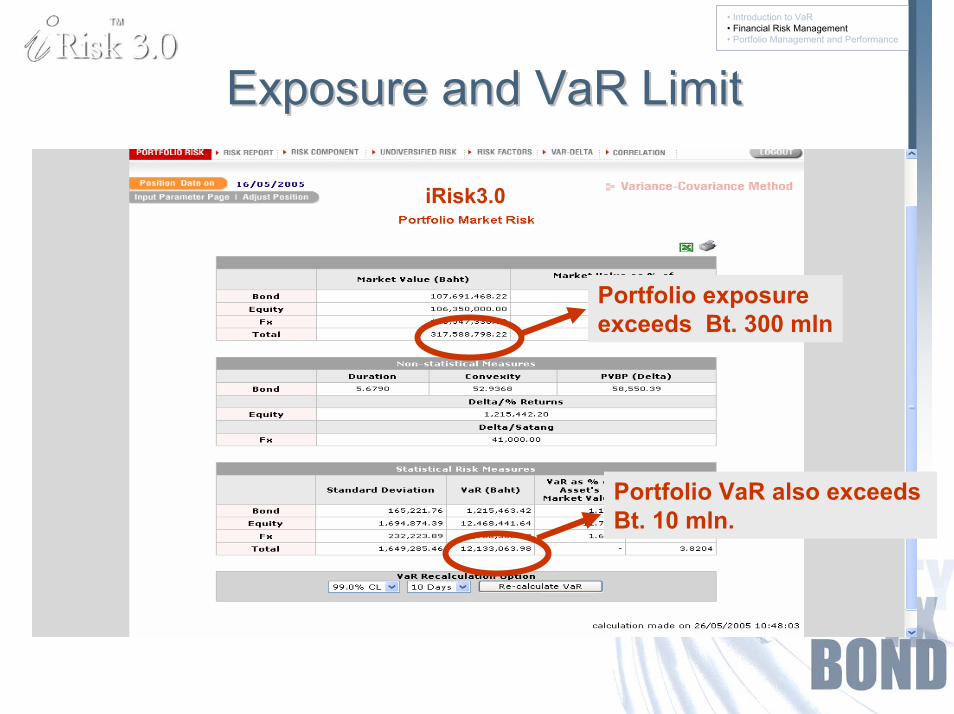

Exposure and Exposure and VaRVaR LimitLimit

• Ex Trading portfolio of company A comprises of 3 asset types; Bonds, Equities and Foreign Currencies.

• CFO assigns policy regarding Exposure and VaR Limit as follows;– Portfolio exposure not exceeds Bt. 300 mln.– Portfolio VaR not exceeds Bt. 10 mln. at holding period 10 days

and confidence level at 99%. • How to follow this policy by using iRisk3.0

8

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

Exposure and Exposure and VaRVaR LimitLimitAssume that existing position on May 16, 2005 as follow;

2,000,000MYR10,000,000SSI20,000PTT116A5

900,000SGD200,000ADVANC20,000ATC106A4

300,000GBP2,500,000ITD20,000EGAT127A3

400,000EUR100,000PTT20,000LB22NA2

500,000USD200,000BBL20,000LB08DA1

UnitSymbolUnitSymbolUnitSymbolNo.

Foreign CurrencyEquityBond

9

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

Exposure and Exposure and VaRVaR Limit Limit

Portfolio exposureexceeds Bt. 300 mln

Portfolio VaR also exceeds Bt. 10 mln.

iRisk3.0

10

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

Exposure and Exposure and VaRVaR LimitLimit

Traders can handle this case in many alternatives based on their strategies i.e.

Portfolio Management(Asset Allocation and Selection)

Use hedging toolsetc.

11

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

Exposure and Exposure and VaRVaR Limit Limit

iRisk3.0 Use Individual and Component VaR as a toolfor Portfolio Adjustment

12

Possible ways to manage portfolio by using useful information from iRisk3.0 results

Selling ITD totallyAllocate bonds, equities and FX positions to follow the policy But if we sell LB22NA, what situation will be occurred?Let’s try to find solution by iRisk3.0

Exposure and Exposure and VaRVaR Limit Limit

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

13

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

Exposure and Exposure and VaRVaR Limit Limit The examples of possible results unit: Mln. Bht.

12.16(Former VaR was

12.13)

296.93But if selling LB22NA

8.60276.79Selling BBL+PTT totally

8.29293.84Selling ITD totally

VaR Limit(Not exceed Bht. 10 Mln)

Exposure Limit(Not exceed Bht.300 Mln)

Alternatives

14

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

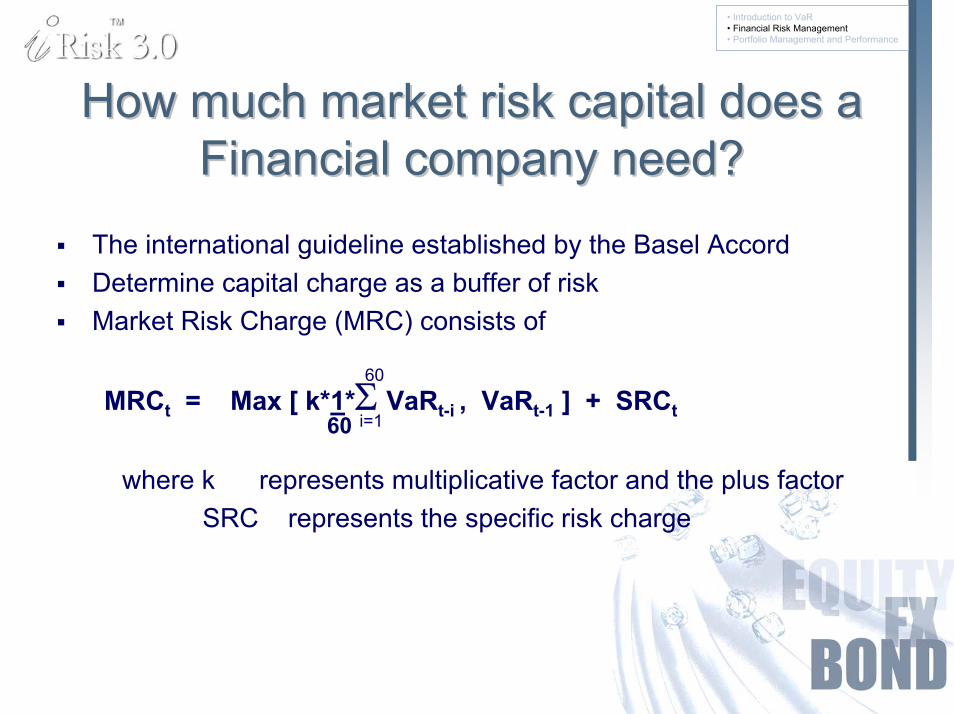

How much market risk capital does a How much market risk capital does a Financial company need? Financial company need?

The international guideline established by the Basel AccordDetermine capital charge as a buffer of riskMarket Risk Charge (MRC) consists of

60

MRCt = Max [ k*1*Σ VaRt-i , VaRt-1 ] + SRCt60 i=1

where k represents multiplicative factor and the plus factorSRC represents the specific risk charge

15

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

Market Risk Charge applied with Market Risk Charge applied with iRiskiRisk60

MRCt = Max [ k*1*Σ VaRt-i , VaRt-1 ] + SRCt60 i=1

Back Testing methodDaily VaR Calculation

4.00≥10Red

3.403.503.653.753.85

56789

Yellow3.000 to 4Green

kNo. of Exceptions

Zone

From Back testingPlus factor

0 to 1Qualitative Risk measurement

Multiplicative factor Value between 3 to 5

16

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

Correlation BreakdownCorrelation Breakdown

• Sometimes correlation between assets are not similar to the past i.e. having the Economic Crisis,Political and Leader Change, Natural Disaster (Tsunami) even Terrorism.

• Stress test by adjusting asset correlation is needed to handle the abnormal situation.

• iRisk3.0 allows users to calculate VaR by changingcorrelation based on their assumptions.

17

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

Correlation BreakdownCorrelation Breakdown

Stress test by AdjustingVolatility and Correlation

18

33.0921.77Portfolio VaR

CorrelationBreakdown

ρ= 0.51.5xVol

Normal correlation(Bank, USD)ρ = −0.245512

Correlation BreakdownCorrelation Breakdown

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

Assume that portfolio has 2 assets; BBL 2,000,000 units and USD 500,000 unit

unit: Bht. Mln

19

Conventional Performance Conventional Performance Measurement: BalanceMeasurement: Balance--sheet Analysissheet Analysis

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

RETURN• FIXED ASSETS• FINANCIAL ASSETS• OTHERS

ASSETSRETURN ON ASSET (ROA)

CAPITAL RETURN ON CAPITAL (ROC)SUBORDINATEDDEBT

EQU

ITYCAPITALRESERVE RETURN ON EQUITY (ROE)

CAPITAL

20

RAPMi = ProfitiVaRi

RAROC

RAPM1

RAPMi = Net ReturniComponent CaRi

RAPM2

Development to Modern RDevelopment to Modern RAROCAROC

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

RAROC = Net Earning Economic Capital

21

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

Portfolio Performance MeasurementPortfolio Performance Measurement

RAROC (Risk- adjusted Return on Capital)Initiated by Bankers Trust, 1970Mostly used to measure economic profit and performance measurement in banks and finance

RAROC = Net Earning . Economic Capital at Risk

Operational Risk

Liquidity Risk

Credit RiskMarket Risk

22

BondBondLB08DALB08DALB22NALB22NA

ATC106AATC106AEGAT127AEGAT127APTT116APTT116A

EquityEquityBBLBBLPTTPTTITDITD

ADVANCADVANCSSISSI

USDUSDEUREURGBPGBPSGDSGDMYRMYR

FxFx

100,000,000

100,000,000RAROC for Fund Allocation RAROC for Fund Allocation

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

100,000,000

23

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

How do we compare Portfolio Performance?How do we compare Portfolio Performance?

11.5813.71

2.68

1.09

1531

54

2035

100 100

12.09

1.70

20.5

4.5

25

100

RAROC

VaR

Net Earning

Cost of Fund

Gross Income

Initial Investment Fund

Bond Equity Fx

11.58

24

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

Portfolio ReallocationPortfolio Reallocation1 LB08DA 17,500 1 BBL 200,000 1 USD 500,000 2 LB22NA 17,500 2 PTT 100,000 2 EUR 450,000 3 EGAT127A 17,500 3 ITD 2,110,000 3 GBP 280,000 4 ATC106A 25,000 4 ADVANC 200,000 4 SGD 800,000 5 PTT116A 17,500 5 SSI 9,000,000 5 MYR 1,800,000

100,000,000 100,000,000 100,000,000

Bond Port Equity Port Fx Port

Market Value Market Value Market Value

1 LB08DA 20,000 1 BBL 100,000 1 USD 800,000 2 LB22NA 20,000 2 PTT 100,000 2 EUR 500,000 3 EGAT127A 20,000 3 ITD 2,000,000 3 GBP 300,000 4 ATC106A 23,000 4 ADVANC 200,000 4 SGD 800,000 5 PTT116A 20,000 5 SSI 7,500,000 5 MYR 750,000

110,000,000 85,000,000 105,000,000

Bond Port Equity Port Fx Port

Market Value Market Value Market Value

25

RAROC & Portfolio AdjustmentRAROC & Portfolio Adjustment• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

2.6012.09

1.70

11.89

1.81

21.5

4.5

26

105

RAROC

VaR

Net Earning

Cost of Fund

Gross Income

Initial Investment Fund

Fx2

3.01

30.5

3.95

14.26

1.23

17.5

5.5

2334

110 85

Bond2 Equity2

9.96

300

Total Port1

300

Total Port2

5.37

12.38

66.5

13.5

80

7.108

9.715

69.05

13.95

8313.71

1.09

15

5

20

100

Bond1

11.58

2.68

31

4

35

100

Equity1

11.5812.09

1.70

20.5

4.5

25

100

Fx1

26

• Introduction to VaR• Financial Risk Management• Portfolio Management and Performance

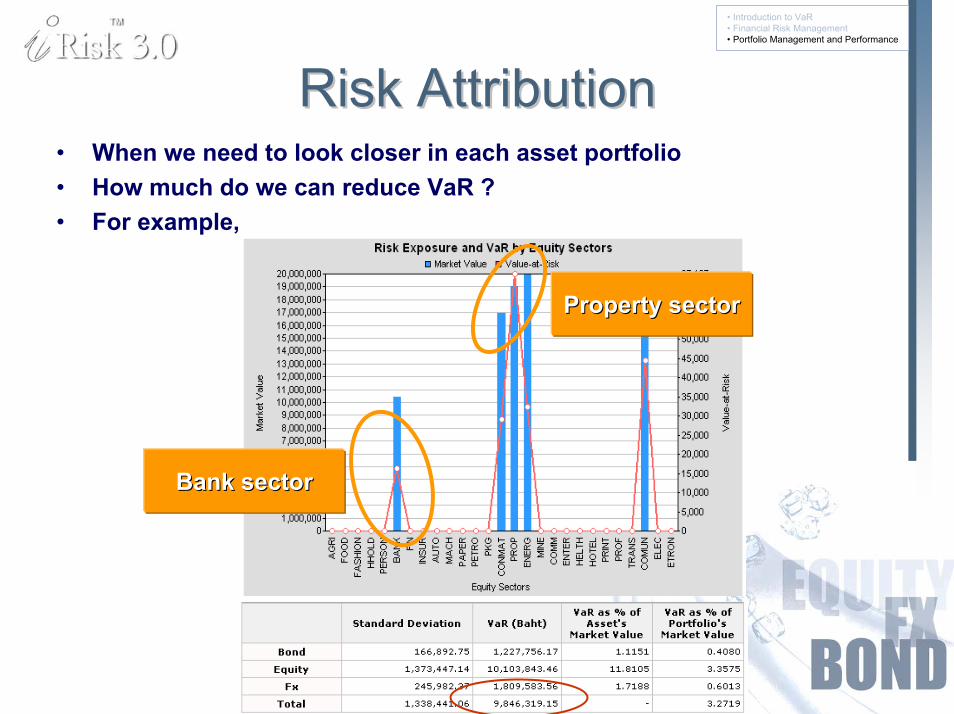

Risk AttributionRisk Attribution• When we need to look closer in each asset portfolio• How much do we can reduce VaR ?• For example,

Bank sectorBank sector

Property sectorProperty sector

27

Besides financial sector, VaR is also taking hold in the corporate world i.e.

Import and Export-Related Business Manufacturing Industry Transportation Industry Energy Industry Propertyand so on.

VaRVaR application to other industriesapplication to other industries

• VaR applications• Conclusion

28

• VaR applications• Conclusion

VaRVaR application to other industriesapplication to other industries

Ex Import-Export BusinessCompany A imports chemical products from USA amount USD 3 mln. and will has a payment settlement in next 10 days.

There are 3 major alternatives as follows;– Buying at spot rate today– Wait to Buy at spot rate in next 10 days– Buying derivatives i.e. forwards or options.

29

• VaR applications• Conclusion

VaRVaR application to other industriesapplication to other industries

30

• VaR applications• Conclusion

VaRVaR application to other industriesapplication to other industries

Buy USD at spot ratetoday

31

• VaR applications• Conclusion

VaRVaR application to other industriesapplication to other industries

Max reserve for Probability of Baht devaluation inNext 10 days

32

• Hence if company A choose the alternative 2, it should reserve the money for payment settlement approximately;

= Baht value at spot rate + VaR for next 10 days(position on 16 May 05)

= 118,883,700 + 2,342,783

= 121,226,483 Baht

VaRVaR application to other industriesapplication to other industries

• VaR applications• Conclusion

33

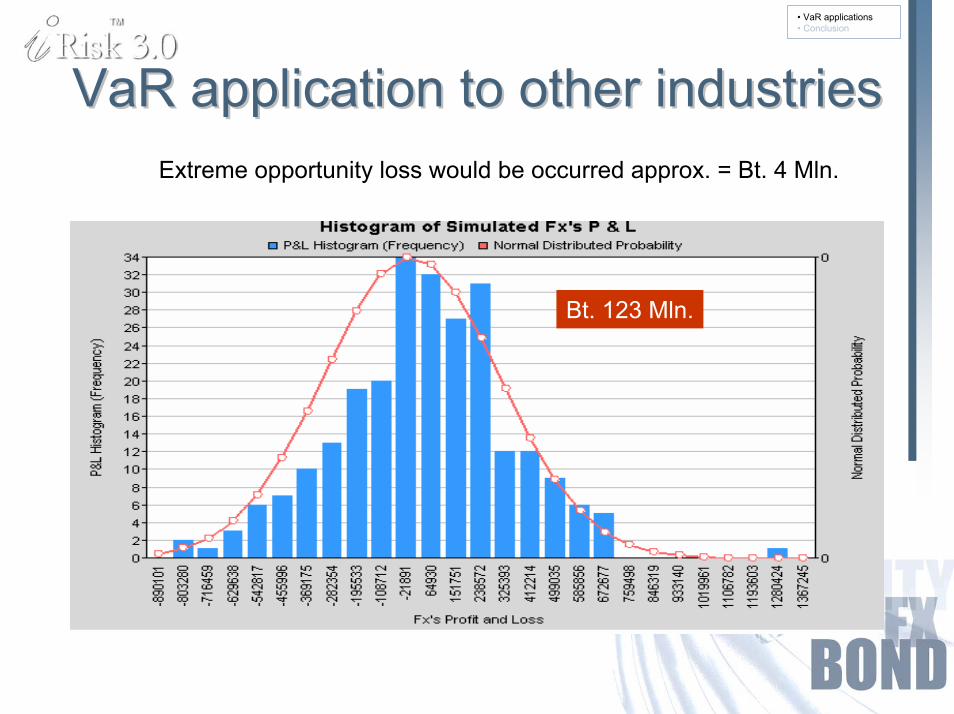

Bt. 123 Mln.

VaRVaR application to other industriesapplication to other industries• VaR applications• Conclusion

Extreme opportunity loss would be occurred approx. = Bt. 4 Mln.

34

• VaR applications• Conclusion

Conclusion: Evolution of Conclusion: Evolution of VaRVaR ApplicationApplication

Reporting Risk• Disclosure to shareholders• Management Reports• Regulatory requirements

• Passive

Controlling Risk• Setting Risk Limits(Desk level and firmwide)

• Defensive

Allocating Risk• Performance evaluation• Capital allocation• Strategic Business Decision

• Active

Top Related