Languages

Pages

Legal

Does Firing the CEO Improve the Company’s Performance in the Long Run?

Yifan Zhu Washington University in St.Louis

Economics Department Honors Thesis

March 17th , 2013

Abstract

This paper investigates whether firing the CEO of a publicly traded company improves or harms

long-run stock performance. I employ a matched sample design where every company with an

involuntary CEO replacement is matched with a company without a CEO replacement in the

same 4-digit SIC industry. The regression results show a negative and statistically insignificant

relationship between CEO firing and stock return. While the lower returns for firms replacing

their CEO is insignificant, the magnitude is substantial, suggesting that the board should handle

CEO replacements with extra caution.

Acknowledgement

I would like to thank my thesis advisor, Professor Bruce Petersen, for his invaluable contributions

and kind support. Without him, I could not have completed my thesis. I would also like to thank

Professor Roni Kisin for all his assistance and much appreciated feedback, and the Business

School Librarian Ronald Allen for permitting me to have access to WRDS. Finally, I would like

to thank Professor Dorothy Petersen for coordinating this wonderful event that allows us to write

an original research paper.

1. Introduction:

The amount of CEO turnover in U.S. publicly traded companies has been high for several

decades and has increased sharply in recent years. For example, according to the article Bargain

bosses in a September 2012 issue of The Economist, in the 1970s, about 10% of the CEOs were

fired each year because of the bad performance of their respective companies. By the 2000s, the

figure had jumped to more than 15%. As a consequence, average CEO tenure declined from 8

years in the 1990s to 6 years today.

Generally, the board of directors makes the decision concerning CEO firing. Existing

literature suggests that forced termination of a CEO’s employment is usually a response to poor

organizational performance (Khurana and Nohria, 2000). When a firm’s performance

deteriorates, the board of directors is under great pressure from shareholders to make changes in

order to improve the confidence of shareholders and investors. However, most changes are likely

to take years to implement and may not be very visible to shareholders. On the other hand, firing

the CEO is something that can be done very quickly, and it is a dramatic action that is highly

visible to shareholders. So, boards’ first reaction to bad performance and shareholder pressure

may be to fire the CEO, even if the true problems facing the firm may not be a problem of

leadership. Given that it is rather expensive to replace CEOs, this naturally gives rise to the

following question: on average, does the performance of firms improve or decline following the

firing of its CEO?

Given the importance of this question, there is surprisingly little previous research on this

topic. Therefore in my thesis I explore whether the removal of a CEO has an impact on the long-

run value of the firm. I carefully construct a matched sample of firms that do not experience CEO

turnover that I use to control for changes in financial performance due to factors other than the

CEO turnover. No previous studies have employed a matched sample methodology and this

approach should provide more accurate results regarding the effect of CEO replacements. My

sample consists of 44 companies with involuntary CEO turnover from 2003-2009 together with

44 matching companies without CEO turnover. I find that the effect of firing a CEO on the

company performance, measured by stock price return, is negative and statistically insignificant.

While the different in performance between companies with and without turnovers is statistically

insignificant, the quantitative effect is not necessarily small. I am somewhat limited about how far

I can push my findings, as my sample size at this time is not that large. A larger sample would

permit more precise estimation of the CEO turnover effect, which would likely permit stronger

conclusions concerning the impact of involuntary CEO turnover on firm performance.

I believe that my findings have implications for the board of directors. When a firm gets

in trouble, one of the quickest and most dramatic actions that the board can take is to fire the CEO.

But if firing a CEO does not typically improve the company performance in the long run, then the

board of directors may need to rely more heavily on other strategies to bring about improvement

in the long-run performance of a company.

2. Motivations and Previous Research

Taylor (2010) develops a dynamic model of a rational board of directors that maximizes

shareholder value and decides at each point whether to fire or keep their current CEO. In his

model, some CEOs are more capable than others and can therefore produce higher profits for

their firms. Taylor (2010) concludes from his empirical model that boards in large firms fire

CEOs at excessive rates, and one of the possible reasons is in large, poorly performing companies,

boards use a CEO replacement as a scapegoat to protect their own benefits. Therefore, it is

possible that CEO involuntary replacement may, on average, lead to little or no improvement in

firm performance.

There are a number of papers discussing CEO turnover and their relationship to company

performance. Clayton, Hartzell and Rosenberg (2005) focus on the change in volatility in equity

returns caused by CEO turnover. They conclude (p.3) that “all types of changes in executive

leadership result in equity volatility increases”, and that the effects can last up to 2 years after the

event. They do not, however, examine whether CEO turnover leads to better or worse

performance as measured by the level of stock prices. Grusky (1963) studies the effect of

management and coaching changes on the performance of baseball teams and finds a negative

relationship between coach replacement and performance. He argues that an executive

replacement has the byproduct of a decline in company performance because of its disruptive

affect on an organization’s processes and routines. Gamson and Scotch (1964) reanalyze Grusky's

data and argue that performance is largely outside the control of managers. They find that there is

no significant relationship between turnover and performance.

The study most closely related to my investigation is Khurana and Nohria (2000), who

explore whether CEO turnover, and different types of successions, has an impact on the firm

performance. They measure firm performance with return on assets, which they adjust for

industry effects by taking the difference between the firm’s ROA and the average ROA in the 2-

digit SIC industry in which the firm resides. Their key explanatory variables are dummy variables

denoting the types succession following a turnover, which can be either an “insider” or an

“outsider.” One problem with their approach is that 2-digit SICs are very aggregated (e.g.,

chemicals, electrical machinery), and thus industry performance at the 2-digit SIC is likely to be a

very crude control. When they examine all CEO turnovers in their sample, they find that forced

turnovers generally have a quantitatively small positive, but significant effect 1-3 years after the

announcement. In addition, they report that the effect of forced turnover with outsider succession

has a statistically significant positive effect on performance while the effect of forced turnover

with insider succession is small and statistically insignificant.

This paper’s goals are to analyze the long-run effects of CEO involuntary turnover by

looking at the companies’ stock return for up to three years after the announcement of the

turnover. My study contributes to the existing literature along a couple of dimensions. First, my

paper extends the research of Khurana and Nohria (2000) by analyzing the years 2003-2009, a

period of rapidly rising CEO turnover and shortened CEO tenure. Second, I use stock returns as

my measure of performance, since shareholders care mainly about stock performance and stock

price captures both the company’s current performance and expected future performance. Third,

instead of comparing the company performance with the industry average (at the 2-digit SIC level)

as Khurana and Nohria did in their paper, I employ a matched sample approach by matching

every company with a CEO turnover in my sample with a comparable company that does not

experience a CEO turnover.

3. Data and Construction of the Sample

Data Sources and Industries

I gather CEO replacement data from the Compustat Executive Compensation Database. I

collect the data for public companies for the period 2003 to 2009. I do not consider CEO turnover

after 2009 because there is insufficient time after the turnover to explore the long-term

performance.

I limit my research to companies in the manufacturing (SIC code 2000-3999), retail (SIC

code 5000-5999) and service (SIC code 7000-7999) sectors. I do not investigate companies in the

public sector because the relatively heavier government regulation gives less freedom to the CEO

and therefore we expect to see smaller effects of changing the CEO.

Identifying Involuntary Turnovers

In my study, I focus on involuntary CEO replacements since previous studies (e.g., Zald

and Berger (1978)) have shown that involuntary turnovers have larger impact on firm

performance. My database classifies the reasons for CEO turnovers as: 1) Resigned, 2) Deceased,

3) Retired, 4) Unknown. I limit my sample to CEOs who “resigned”. To identify resignations

that are involuntary turnovers, I follow the method of Khurana and Nohria (2000). First, I delete

turnovers where the CEO is over 60 years old because they are plausibly resigning because of age

or health reasons, rather than being forced to resign. Second, I double-checked whether CEOs

who left the company took another CEO position; I exclude all cases where the departed CEO did

in fact find a CEO position elsewhere. Therefore, as Kharana and Nohria did, I conclude that the

CEO turnovers that remain in my sample are very likely to be involuntary.

Creation of a Matched Sample

Ideally, we want to study the effects CEO replacement has on company performance by

studying a situation where CEO turnover is randomly assigned; however, this obviously is not

possible in the real world. Instead, I use a matched sample design. A matched sample design has

not been used to study CEO replacement, but it has been employed in other studies in the finance

literature. For example, Megginson and Weiss (1991) explore whether VC-backed firms (who are

obviously not randomly assigned) have lower underpricing when they go public. Megginson and

Weiss (1991) match VC-backed firms going public with a non-VC backed firm in the same 4-

digit industry and of similar size. Another example is Brown (2005), who explores the impact of

VC-backing on the long-run performance of publicly traded high-tech firms. Brown (2005) also

creates a matched sample of VC-backed and non-VC-backed firms in the same industry and of

similar age and size.

In my study, I follow a similar approach as the above papers by employing a matched

sample design where the matching occurs on asset size and the 4-digit SIC code. I use four rules

to define a matching company. First, the matched firm is in the database for exactly the same

years as the firm with the turnover. Second, the matching company must be in the same (4-digit

SIC) industry of the firm with an involuntary turnover. Third, in the year of the turnover, the

matching company must fall within a ±20% range in consolidated asset size. When I have

multiple companies that fall into the range, I select the one that is closest to the turnover company

in terms of asset size. Finally, the matching company cannot have CEO turnovers 2 years before

or 4 years after the announcement date of the company with CEO replacement. I note that 4-digit

SIC industries are far less aggregated than 2-digit SIC industries, and thus should serve as better

controls than what Kharana and Nohria (2000) used.1

The logic behind employing a matched sample design is that firms in the same 4-digit

SIC industry with similar asset sizes are likely to experience similar industry demand and supply

1 For example, in manufacturing, there are only 20 2-digit SIC industries in manufacturing compared to over 400 4-digities industries.

shocks. This hopefully permits the analysis to isolate the impact of CEO turnover from other

factors that drive stock prices.

Of course, the matched sample design is not perfect. In my study, I had to drop some

firms from my sample because I couldn’t find a match for them. In addition, there are likely

unobserved differences between firms experiencing a CEO turnover and those that do not. In

particular, companies that fire their CEO are likely firms that are doing worse than the industry

average. Fortunately, this difference in the initial quality of firms is presumably capitalized in the

stock price of the firm just prior to the announcement of the turnover. That is, if CEO turnover

firms are of lower quality, that should be reflected in a lower initial stock prices. So what I hope

to capture in my research design is the improvement in stock performance after the new CEO

takes over relative to similar firms in the same industry, recognizing that matched firms may be,

on average, of higher initial quality, but that this quality difference is arguably captured by higher

initial stock prices.

Measuring Stock Returns

I use stock prices as my main measure of company performance. Stock prices are

arguably what equity investors care most about and thus this is what the board of directors should

focus on in making decisions concerning whether or not to fire the existing CEO. Stock prices are

also a forward-looking measure, and the expected future performance of the firm is already

capitalized into the stock market at the time of the CEO turnover. If the CEO improves the firm

performance, this should show up in higher stock prices, but it presumably takes time for the

CEO to impact performance and for the stock market to recognize the better performance. Hence,

I will look at future stock prices compared to the stock price just one day before the

announcement of the CEO turnover.

I use the CRSP® US Stock Database to get the daily stock price in order to calculate the

stock price return as my dependent variable. I compute stock returns as follows: I first obtain the

daily closing price one day before the announcement date, and the closing price 1, 2, and 3 years

after the announcement date respectively. I then compute the change in the stock price from the

date of the CEO turnover to n-years in the future for both the turnover firm and its matched

counterpart using the natural logarithm function.

𝑂𝑛𝑒 𝑦𝑒𝑎𝑟 𝑅𝑒𝑡𝑢𝑟𝑛 = 𝑙𝑛𝑆𝑡𝑜𝑐𝑘 𝑃𝑟𝑖𝑐𝑒!!!𝑆𝑡𝑜𝑐𝑘 𝑃𝑟𝑖𝑐𝑒!!!

The two-year and three-year returns are calculated with the same log return function. In

order to eliminate potential outliers in my sample, I deleted companies that have yearly returns

over +500% or -80%.

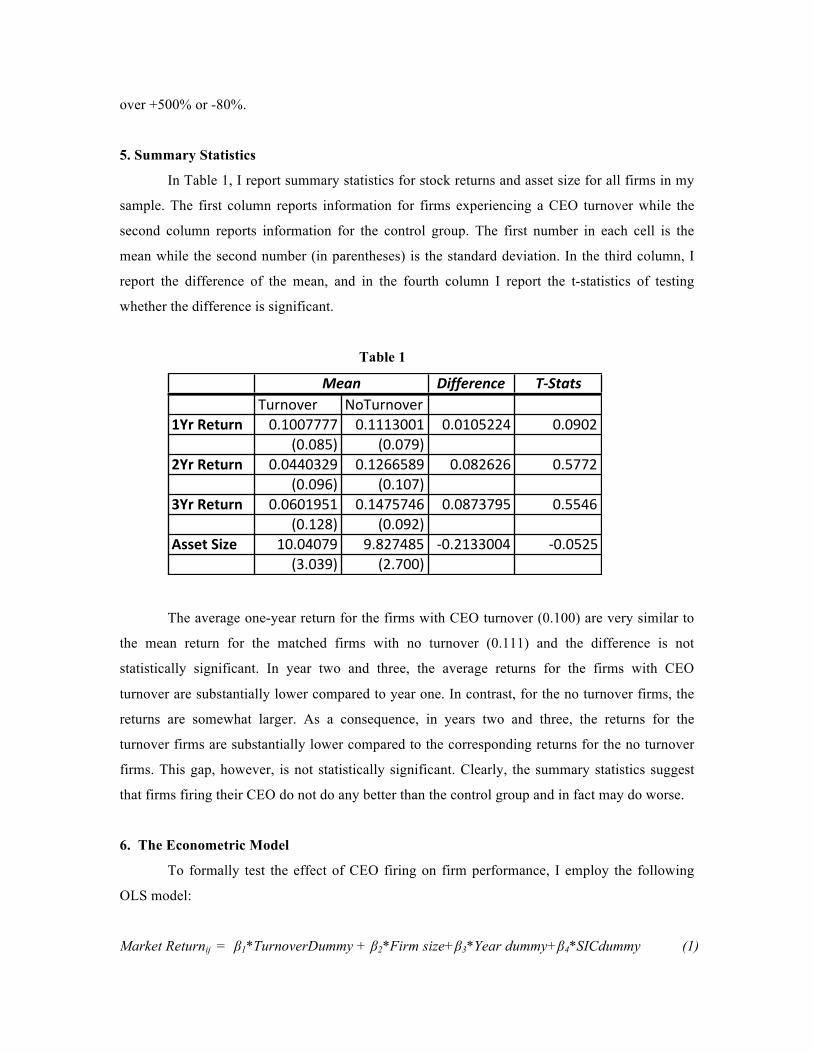

5. Summary Statistics

In Table 1, I report summary statistics for stock returns and asset size for all firms in my

sample. The first column reports information for firms experiencing a CEO turnover while the

second column reports information for the control group. The first number in each cell is the

mean while the second number (in parentheses) is the standard deviation. In the third column, I

report the difference of the mean, and in the fourth column I report the t-statistics of testing

whether the difference is significant.

Table 1

The average one-year return for the firms with CEO turnover (0.100) are very similar to

the mean return for the matched firms with no turnover (0.111) and the difference is not

statistically significant. In year two and three, the average returns for the firms with CEO

turnover are substantially lower compared to year one. In contrast, for the no turnover firms, the

returns are somewhat larger. As a consequence, in years two and three, the returns for the

turnover firms are substantially lower compared to the corresponding returns for the no turnover

firms. This gap, however, is not statistically significant. Clearly, the summary statistics suggest

that firms firing their CEO do not do any better than the control group and in fact may do worse.

6. The Econometric Model

To formally test the effect of CEO firing on firm performance, I employ the following

OLS model:

Market Returnij = β1*TurnoverDummy + β2*Firm size+β3*Year dummy+β4*SICdummy (1)

Difference T)StatsTurnover NoTurnover

1Yr$Return 0.1007777 0.1113001 0.0105224 0.0902(0.085) (0.079)

2Yr$Return 0.0440329 0.1266589 0.082626 0.5772(0.096) (0.107)

3Yr$Return 0.0601951 0.1475746 0.0873795 0.5546(0.128) (0.092)

Asset$Size 10.04079 9.827485 60.2133004 60.0525(3.039) (2.700)

Mean

The key explanatory variable in my study is the turnover dummy, which takes on a value

of one whenever there is a CEO replacement. The rest of the variables in the regressions are

control variables. Even though I used firm size in creating my matched sample, my matching is

not perfect and therefore I include firm size (measured in 100 millions) as a control variable. In

addition, stock returns may be impacted by firm size. The most important control variables are

the year dummies. The year in which a turnover occurs will no doubt have a very large impact on

future stock prices, so I include year dummies in the regression, where each year dummy is

defined for the year in which the announcement takes place2. For example, if an announcement

took place in 2007, then the 2007 years dummy takes on a value of one. Furthermore, in the

regression exploring stock returns one year following the announcement, I expect the 2007 and

2008 year dummies to be negative, as stock prices in 2008 fell sharply for nearly all firms.

Finally, I create a dummy variable for each 2-digit SIC code.3

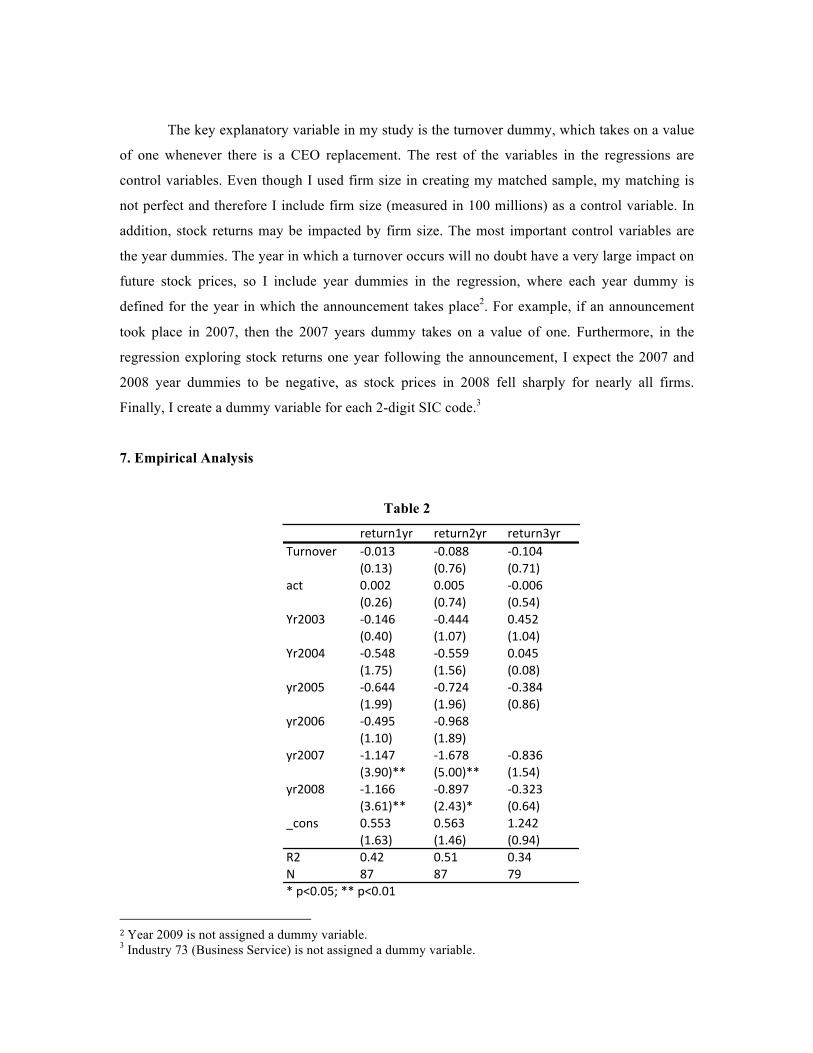

7. Empirical Analysis

Table 2

return1yr return2yr return3yrTurnover -0.013 -0.088 -0.104

(0.13) (0.76) (0.71)act 0.002 0.005 -0.006

(0.26) (0.74) (0.54)Yr2003 -0.146 -0.444 0.452

(0.40) (1.07) (1.04)Yr2004 -0.548 -0.559 0.045

(1.75) (1.56) (0.08)yr2005 -0.644 -0.724 -0.384

(1.99) (1.96) (0.86)yr2006 -0.495 -0.968

(1.10) (1.89)yr2007 -1.147 -1.678 -0.836

(3.90)** (5.00)** (1.54)yr2008 -1.166 -0.897 -0.323

(3.61)** (2.43)* (0.64)_cons 0.553 0.563 1.242

(1.63) (1.46) (0.94)R2 0.42 0.51 0.34N 87 87 79*@p<0.05;@**@p<0.01

2 Year 2009 is not assigned a dummy variable. 3 Industry 73 (Business Service) is not assigned a dummy variable.

In Table 2, I report results for equation (1) using three different dependent variables: 1

year, 2 years and 3 year returns. In all three regressions, the coefficient for the turnover dummy is

completely consistent with the summary statistics reported in Table 1. Since mean returns for

turnover firms are less than mean returns for non-turnover firms (in the summary statistics), I

expect a negative coefficient for the turnover dummy, and this is the case in all three regressions.

The negative coefficient is, however, in all cases statistically insignificant. With regards to

statistical significance, it is important to note that my sample is small and if I expand my sample

it may well be that these negative coefficients would be statistically significant.

It is also noteworthy that the point estimates for the turnover coefficient in the second and

third regressions are not trivial. In the second regression, the point estimate suggests that if a

company had a CEO replacement, in 2 years, the stock price return will be 8.8% lower than firms

in the matched sample. In the third regression, the point estimate suggests that in 3 years, the

stock price return will be 10.4% lower for the firms with turnover compared to their peers who

did not experience the replacement. The lower returns for turnover companies are very much in

line with the size of the gap in returns between turnover companies and the matching companies

in the summary statistics.

The asset size control variable is both statistically insignificant and quantitatively small.

All the year dummies are statistically insignificant except for 2007 and 2008 in the first and

second regressions, which have statistically significant and large negative coefficients. The large

negative coefficients in those years are expected, given the sharp declines in stock prices that

occurred in 2008 and 2009. To save space, I did not report the SIC dummies, and they are all

statistically insignificant.

8.Robustness

To test the robustness of my regression results, I use stock price one day after the

announcement instead of the price one day before the announcement when calculating the stock

return for 1, 2 and 3 year periods. Suppose the problems facing turnover firms are not fully

capitalized by the stock market because of incomplete information, firing the CEO could provide

the stock market new information that causes the price of the firm to decline immediately after

the announcement. Therefore, by comparing stock price several years after the announcement

and one day after the announcement, we will be able to analyze whether the successor CEO is

doing his job to improve the company performance once he takes office.

I run three regressions with the new dependent variable, and the results are in table 3.

Table 3

roreturn1yr roreturn2yr roreturn3yr Turnover -‐0.079 -‐0.154 -‐0.186

(0.62) (1.14) (1.07) act 0.004 0.008 -‐0.003

(0.5) (0.9) (0.24) yr2003 -‐0.245 -‐0.544 -‐0.267

(0.54) (1.13) (0.51) yr2004 -‐0.567 -‐0.578 -‐0.596

(1.45) (1.38) (0.9) yr2005 -‐0.601 -‐0.68 -‐0.96

(1.48) (1.58) (1.79) yr2006 0.12 -‐0.354

(0.21) (0.59)

yr2007 -‐1.142 -‐1.673 -‐1.451

(3.11)** (4.28)** (2.22)* yr2008 -‐1.153 -‐0.884 -‐0.929

(2.85)** (2.05)* (1.54) _cons 0.616 0.627 1.573

(1.46) (1.39) (0.99) R2 0.34 0.44 0.28 N 87 87 79

* p<0.05; ** p<0.01

The results from the robustness test are very similar to the original regressions, where the

turnover dummies are statistically insignificant and quantitatively large. It is worth noticing that

the point estimates for the turnover dummy are larger than those in the original regressions,

suggesting that the CEO replacement news will improve the stock price in a short time period

(immediately after the announcement); however, the shifted expectation cannot last into long run.

I also try tightening my criterion of defining outliers. Originally, I deleted companies that

have yearly returns over +500% or -80%, I have re-run the regressions after deleting companies

have yearly returns over +300% or -75% and have gotten very similar results.

9. Conclusions

In this paper, I seek to investigate the relationship between CEO firing and company

performance for up to three years after the announcement date. I employ a matched sample design

(matched by industry and size) to compare companies with and without CEO turnover. My

sample size, however, is limited. Through the years 2003-2009, I have 44 companies with

turnovers and 44 companies without turnovers. My OLS model uses the stock return as the

dependent variable, while the turnover dummy is my key explanatory variable. I find that the

estimated coefficient for the turnover dummy is negative in all cases and always statistically

insignificant. While the turnover dummy is statistically insignificant, the point estimates for the

turnover coefficient are quantitatively large in two of the regressions. If I were to expand my

sample, it is quite possible that the negative coefficients may become statistically significant.

At present, I cannot draw strong conclusions from my study, given the size of the sample.

However, my findings are consistent with a view that CEOs are fired at excessive rates, but not

totally consistent with Khurana and Nohria (2000), who concluded that CEO turnovers have

small but significant positive effects several years after. Nevertheless, my results are consistent

with previous studies that have concluded that firing the CEO has either an insignificant or a

negative effect on the company performance, and therefore I suggest the boards of directors

should seek other means to improve the company performance rather than firing the CEO and

hoping the successor will do a better job.

There are a number of improvements I would like to make to my research. In particular, it

is important to increase my sample size by including more CEO firings. A larger sample should

lower the standard errors and permit stronger conclusions concerning the impact of firing the

CEO on firm performance. I would use factiva.com to check the news on CEO resignations,

which should get me a more complete sample of CEO firing events.

Though limitations exist in my paper, my preliminary evidence suggests that firing CEOs

does not improve firm stock market performance. Therefore, given the high cost of replacing a

CEO, the board of directors should handle such replacement with great caution.

Reference Megginson, William L., and Kathleen A. Weiss, “Venture Capital Certification in Initial Public Offerings,” Journal of Finance, 46, 1991, pp. 879-903. Brown, James R., “Venture Capital and Firm Performance over the Long-Run: Evidence from High-Tech IPOs in the U.S.,” Journal of Entrepreneurial Finance and Business Ventures, 2005, pp. 1-33. Zald, M. N., and Berger, M. A., “Social movements in organizations: Coup d'etat, insurgency, and mass movements,” American Journal of Sociology, 83, 1978, pp. 823-861.

Grusky, O., “Managerial succession and organizational effectiveness,” American Journal of Sociology, 69, 1963, pp. 21-31.

Gamson, W. A., and Scotch, N., “Scapegoating in baseball”, American Journal of Sociology, 70, 1964 pp.69-72.

Taylor, L. A., “Why Are CEOs Rarely Fired? Evidence from Structural Estimation,” The Journal of Finance, 65, 2010, pp. 2051–2087.

Khurana, R., and Nohria, N., “The performance consequences of CEO turnover,” Working paper. 2000.

"Bargin Bosses." The Economists. September 2012. Print.

Appendix:

Complete Table 2

return1yr return2yr return3yr return4yr Turnover -‐0.013 -‐0.088 -‐0.104 0.129

(0.13) (0.76) (0.71) (0.64)

act 0.002 0.005 -‐0.006 0.010

(0.26) (0.74) (0.54) (0.71)

Yr2003 -‐0.146 -‐0.444 0.452 0.459

(0.40) (1.07) (1.04) (0.88)

Yr2004 -‐0.548 -‐0.559 0.045

(1.75) (1.56) (0.08)

yr2005 -‐0.644 -‐0.724 -‐0.384 -‐1.070

(1.99) (1.96) (0.86) (2.25)*

yr2006 -‐0.495 -‐0.968

0.087

(1.10) (1.89)

(0.13)

yr2007 -‐1.147 -‐1.678 -‐0.836 -‐0.934

(3.90)** (5.00)** (1.54) (1.85)

yr2008 -‐1.166 -‐0.897 -‐0.323

(3.61)** (2.43)* (0.64)

SIC28 0.383 0.621 -‐0.324 2.060

(0.81) (1.16) (0.24) (2.38)*

SIC20 0.340 -‐0.255

(0.35) (0.23)

SIC33 0.415 0.599 -‐0.878 1.868

(0.78) (0.98) (0.67) (2.29)*

SIC34 0.117 0.228 -‐0.795 0.596

(0.20) (0.35) (0.56) (0.58)

SIC35 0.034 0.120 -‐1.101 1.274

(0.08) (0.26) (0.73) (1.22)

SIC36 0.557 0.579 -‐0.684 1.494

(1.16) (1.06) (0.52) (1.78)

SIC38 -‐0.010 0.091 -‐1.245 0.800

(0.02) (0.15) (0.98) (1.32)

SIC39 0.093 0.384 -‐0.731 0.858

(0.18) (0.67) (0.51) (0.72)

SIC50 0.318 0.258 -‐0.995 1.661

(0.63) (0.45) (0.71) (1.85)

SIC53 -‐0.035 0.481 -‐1.694

(0.05) (0.63) (1.31)

SIC55 0.240 0.389 -‐0.823 1.369

(0.45) (0.63) (0.64) (1.64)

SIC58 0.305 0.831 -‐0.245

(0.58) (1.39) (0.18)

SIC70 0.500 -‐0.147 -‐0.726 0.810

(0.87) (0.22) (0.54) (0.82)

SIC73 0.178 0.146 -‐0.879 0.734

(0.41) (0.29) (0.65) (0.89)

_cons 0.553 0.563 1.242 -‐0.816

(1.63) (1.46) (0.94) (0.86)

R2 0.42 0.51 0.34 0.44 N 87 87 79 57 * p<0.05; ** p<0.01

Complete Table 3

roreturn1yr roreturn2yr roreturn3yr Turnover -‐0.079 -‐0.154 -‐0.186

(0.62) (1.14) (1.07) act 0.004 0.008 -‐0.003

(0.5) (0.9) (0.24) yr2003 -‐0.245 -‐0.544 -‐0.267

(0.54) (1.13) (0.51) yr2004 -‐0.567 -‐0.578 -‐0.596

(1.45) (1.38) (0.9) yr2005 -‐0.601 -‐0.68 -‐0.96

(1.48) (1.58) (1.79) yr2006 0.12 -‐0.354

(0.21) (0.59)

yr2007 -‐1.142 -‐1.673 -‐1.451

(3.11)** (4.28)** (2.22)* yr2008 -‐1.153 -‐0.884 -‐0.929

(2.85)** (2.05)* (1.54) SIC28 0.309 0.547 -‐0.04

(0.53) (0.87) (0.03) SIC20 0.03 -‐0.564

(0.02) (0.44)

SIC33 0.4 0.584 -‐0.536

(0.6) (0.82) (0.34) SIC34 0.058 0.169 -‐0.497

(0.08) (0.22) (0.29) SIC35 0.027 0.113 -‐0.749

(0.05) (0.21) (0.42) SIC36 0.509 0.531 -‐0.376

(0.85) (0.83) (0.24) SIC38 -‐0.366 -‐0.265 -‐1.246

(0.54) (0.37) (0.82) SIC39 0.079 0.37 -‐0.384

(0.13) (0.55) (0.23) SIC50 0.235 0.174 -‐0.719

(0.37) (0.26) (0.43) SIC53 -‐0.918 -‐0.403 -‐2.227

(1.09) (0.45) (1.44) SIC55 0.175 0.323 -‐0.535

(0.26) (0.45) (0.35) SIC58 0.258 0.784 0.068

(0.4) (1.13) (0.04) SIC70 0.379 -‐0.267 -‐0.493

(0.53) (0.35) (0.3) SIC73 0.13 0.098 -‐0.568

(0.24) (0.17) (0.35) _cons 0.616 0.627 1.573

(1.46) (1.39) (0.99) R2 0.34 0.44 0.28 N 87 87 79

* p<0.05; ** p<0.01

Top Related