Languages

Pages

Legal

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 1/34

Corporate Governance and Firm Value:

The Impact of Corporate SocialResponsibility

Hoje JoMaretno A. Harjoto

ABSTRACT. This study investigates the effects of

internal and external corporate governance and moni-

toring mechanisms on the choice of corporate social

responsibility (CSR) engagement and the value of firms

engaging in CSR activities. The study finds the CSR

choice is positively associated with the internal and

external corporate governance and monitoring mecha-

nisms, including board leadership, board independence,

institutional ownership, analyst following, and anti-

takeover provisions, after controlling for various firm

characteristics. After correcting for endogeneity and

simultaneity issues, the results show that CSR engage-

ment positively influences firm value measured by

industry-adjusted Tobin’s q. We find that the impact of

analyst following for firms that engage in CSR on firm

value is strongly positive, while the board leader-

ship, board independence, blockholders’ ownership, andinstitutional ownership play a relatively weaker role in

enhancing firm value. Furthermore, we find that CSR

activities that address internal social enhancement within

the firm, such as employees diversity, firm relationship

with its employees, and product quality, enhance the

value of firm more than other CSR subcategories for

broader external social enhancement such as community

relation and environmental concerns.

KEY WORDS: corporate social responsibility, corpo-

rate governance, analyst following, firm value

JEL CLASSIFICATION: G34, L2, M14

Introduction

Although there has been a noteworthy discussion

among scholars and practitioners over the last two

decades on what constitutes the best corporate

governance practices, corporate governance across

corporate America is more heterogeneous than ever

before. The recent collapse of many firms has not

only proven to be a watershed momentum in U.S.

corporate governance, it also has highlighted theimportance of information transparency. Informa-

tion problems and managerial incentives typically

limit the effectiveness of corporate governance in

public corporations (Jensen, 1993; Miller, 2005). As

a result, there has been a tremendous acceleration of

corporate governance activities, as well as a con-

vergence of certain trends in corporate governance

over the last few years (Hermalin, 2005). While the

literature indicates that effective corporate gover-

nance curtails managerial self-interest and protects

shareholder interests, this study posits that corporate

governance manages the interests of multiple stake-

holders and resolves the conflicts of interest between

shareholders and non-investing stakeholders.

Along with the acceleration of corporate gover-

nance issue, one of the most significant and con-

tentious corporate trends of the last decade is the

growth of Corporate Social Responsibility (CSR).

In essence, CSR is an extension of firms’ efforts

to foster effective corporate governance, ensuring

firms’ sustainability via sound business practices that

promote accountability and transparency. However,

there are various definitions of CSR. Friedman(1970) first defines CSR as follows: ‘‘Corporate so-

cial responsibility is to conduct the business in

accordance with shareholders’ desires, which gen-

erally will be to make as much money as possible

while conforming to the basic rules of society, both

those embodied in law and those embodied in eth-

ical custom.’’ Carroll (1979) and Hill et al. (2007)

define the hierarchical CSR as economic, legal,

moral, and philanthropic actions of firms that

Journal of Business Ethics (2011) 103:351–383 Springer 2011

DOI 10.1007/s10551-011-0869-y

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 2/34

influence the quality of life of relevant stakeholders.

While the definitions of CSR vary, it generally refers

to serving people, communities, and society in ways

that go above and beyond what is legally required of

a firm. According to Barnea and Rubin (2010),however, if CSR initiatives do not maximize firm

value, such initiatives are a waste of valuable re-

sources and a potentially value-destroying proposi-

tion. CSR has continued to be a highly topical

subject regarding whether investments in CSR are

value-enhancing, value-destroying, or even value-

irrelevant. The debates about CSR continue to grow

without a clear consensus on its meaning or value.

In this paper, we first examine the empirical

association between various corporate governance

and monitoring mechanisms and U.S. firms’ choiceof CSR involvement. We then explore how CSR

engagement and various governance mechanisms

affect firm value after correcting for endogeneity and

simultaneity. Well-designed corporate governance

systems would align managers’ incentives with those

of stakeholders. Hence, firms with effective corpo-

rate governance should place a greater emphasis on

value maximization. We examine two categories of

governance devices: internal (ownership concentra-

tion and board structure) and external (institutional

ownership and monitoring by security analysts).

Given that the relations among CSR, corporategovernance, and firm value are mixed, and that

previous studies do not control for the simultaneity

bias and endogeneity, this study explores the impact

of various governance mechanisms on firms’ choice

of CSR engagement and the effect of this engage-

ment on firm value after controlling for both the

simultaneity bias and endogeneity.1

As one of the essential rationales behind CSR

engagement is to build trust relationships and social

capital, increasing attention is being paid to the effects

that social capital has on economic variables.

2

Severalstudies analyze the relation between social capital and

economic growth (Knack and Keefer, 1997); social

capital and trust building (La Porta et al., 1997a, b);

social capital and government performance (La Porta

et al., 1999; Putnam, 1993); and social capital and

financial development (Guiso, et al., 2004). In spite

of the increasing attention given to social capital,

however, only a few studies in finance examine CSR

engagement. Aggrawal and Nanda (2004) investigate

the relation between board size and social objectives

and find that the number of social objectives posi-

tively affects firms’ board size. Fisman et al. (2005)

examine the link between firms’ CSR engagement

and accounting profit. They find that the effect of

CSR on profitability is stronger for firms in morecompetitive industries. Barnea and Rubin (2010)

examine the relation between firms’ CSR ratings and

their ownership and capital structures and find that

insiders tend to over-invest in CSR. Goss and

Roberts (2007) analyze the association between CSR

and the cost of bank loans. They find that firms with

the worst social responsibility scores pay higher loan

costs while firms with good scores do not receive

lower loan costs. Hong and Kacperczyk (2009) find

sin stocks from publicly traded firms that produce

alcohol, tobacco, and gambling have higher risk andreturns indicating that social norms affect stock prices

and returns. Although these studies enhance our

understanding of the important benefits and costs of

CSR engagement, in our view, the previous research

on this issue is still premature to provide any definite

conclusions regarding the impact of CSR engage-

ment on firm value.3

To correctly examine the relationship between

CSR and firm value, we need to consider potential

simultaneity bias and endogenous treatment effects.

Since better quality firms tend to choose CSR

engagement, the contribution of CSR engagementto firm value will be overstated (Greene, 1993) if we

do not correct for the simultaneity and endogeneity

problems. In this paper, we conduct our endoge-

neity and simultaneity analyses in two stages. We

examine the factors determining CSR engagement

extensively in the first stage, and then compare the

firm values of CSR engaging versus CSR non-

engaging firms in the second stage. Based upon a

large sample of 12,527 firm-year (2952 firms)

observations, including both CSR and no-CSR

firms during the 1993–2004 period, we initiallyperform a first-stage probit regression analysis of

CSR engagement. Consistent with the conflict-

resolution hypothesis, the results show that the

likelihood of opting for CSR involvement is sig-

nificantly and positively related to governance

characteristics such as board leadership, board inde-

pendence, institutional ownership, analyst following,

and anti-takeover provisions after controlling for

such firm characteristics as firm size, leverage, prof-

itability, R&D, a firm’s diversification, and risk.

352 Hoje Jo and Maretno A. Harjoto

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 3/34

In the second-stage analysis, we find that after

correcting for the endogenous treatment effect and

simultaneity bias, respectively, firm value, measured

by industry-adjusted Tobin’s q, is positively

related to the CSR choice or the CSR-combinedscores, suggesting that CSR engagement positively

influences firm value. The results support the

conflict-resolution hypothesis, as opposed to the

overinvestment explanation, and remain robust

under various specifications, including the OLS, the

Heckman two-stage regressions, and the instru-

mental variables approach. Our results also suggest

that the value enhancement of firms’ CSR engage-

ment comes from firms’ internal social enhance-

ment, such as diversity, employee relations, and

product issues more than their CSR involvement inbroader external enhancement, such as activities

related to community and environmental issues. In

addition, after controlling for a potential simultaneity

bias, our inferences concerning the positive associ-

ation between CSR and firm value remain intact.

Furthermore, we maintain that security analysts

are important information intermediaries who

improve the transparency of a firm’s CSR activities.

Accordingly, the impact of CSR activities are

stronger when analyst following is higher, and the

impact of analyst following on firm value is also

strongly positive in all models. However, the mon-itoring impact of institutional investors is occasion-

ally positive, but relatively weaker than that of

security analysts, presumably because of their dual

roles of monitors and investors. Overall, our results

suggest that firms’ engagement in CSR activities,

together with external monitoring by security ana-

lysts, is value enhancing. Furthermore, the positive

impact of CSR activities on firm value implies that

U.S. firms do not over-invest in CSR activities in

the sample period.

This paper contributes to the literature on CSRand corporate governance in three distinct ways.

First, we conduct a full examination of the deter-

minants of CSR engagement and provide insights

into how corporate governance influences firms’

choice to engage in CSR by using all CSR firms

and no-CSR firms available from the Kinder,

Lydenberg, and Domini’s (KLD) Stats database,

RiskMetrics (formerly, the Investor Responsibility

Research Center’s (IRRC) governance and direc-

tor) database, and the Institutional Brokers Estima-

tion Services (I/B/E/S) database during the 1993–

2004 period. Second, we consider more extensive

governance and monitoring mechanisms to examine

the impact of CSR on firms’ value and revisit the

over-investment hypothesis and the conflict-resolu-tion explanation in light of CSR. By appropriately

controlling for the endogenous treatment effects and

simultaneity bias, we are able to determine whether

firms over-invest in CSR activities. We postulate

that the role of corporate governance in the choice

of CSR engagement and the impact of that choice

on firm value might be different for each of the

internal and external governance mechanisms. We

believe that this is the first empirical study to for-

mally address both the simultaneity and endogeneity

issues. Third, we provide further evidence that theimpact of security analyst following on firm value is

one of the most significant among several considered

governance and monitoring mechanisms in the

presence of CSR engagement.

Hypotheses

Why do firms engage in CSR?

Despite large literature on CSR (Bowen, 1953;

Donham, 1927; and for an overview, see Whetten,et al., 2002), there is no unified theory behind CSR

engagement, and there are at least two alternative

explanations regarding its existence. First, based on

Jensen and Meckling’s (1976) agency theory, Barnea

and Rubin (2010) consider CSR engagement as a

principal-agent relation between managers and

shareholders, and argue that affiliated insiders have

an interest in overinvesting in CSR in order to

obtain private benefits of building reputation as good

social citizens, possibly at a cost to shareholders.

As reputation improves, top management willenjoy better outside career opportunities and greater

negotiation power, which will eventually lead them

to have overconfidence. Malmendier and Tate

(2005) suggest that there is some evidence of over-

investment by overconfident CEOs. Goel and

Thakor’s (2008) theoretical model also shows that

overconfident managers sometimes make value-

destroying investments. In a related vein, Bertrand

and Mullainathan (2003) argue that when manag-

ers are not closely monitored and insulated from

353Corporate Governance and Firm Value

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 4/34

takeovers, active empire building may not be the

norm and managers may prefer to enjoy a quiet life.

If overconfident CEOs tend to over-invest in order

to build their reputations as good social citizens

without monitoring, we expect an inverse associa-tion between monitoring and CSR choice because

the higher internal and external monitoring through

various governance mechanisms should reduce the

insiders’ incentive for CSR over-investment.

Second, while it may not be completely possible

to satisfy all related stakeholders, there is a growing

literature on conflict resolution based on stakeholder

theory (e,g., Calton and Payne, 2003; Harjoto and

Jo, 2011; Jensen, 2002; Sherere et al., 2006), in

which the role of the corporation is to serve the

interests of other non-investing stakeholders as well.According to the conflict-resolution hypothesis,

to the extent that managers use effective monitor-

ing/governance mechanisms together with CSR

engagement to resolve conflicts among stakeholders,

CSR engagement should be positively related to

effective governance mechanisms. Alternatively, if

various governance and monitoring mechanisms

view the firm’s CSR engagement as an effort of

potential conflict resolution among various stake-

holders, then we would expect a positive association

between corporate governance and CSR engage-

ment.

Hypothesis 1: According to the over-investment

hypothesis, we expect that the choice of CSR

engagement is inversely associated with gover-

nance and monitoring mechanisms after control-

ling for confounding factors, while according to

the conflict-resolution hypothesis, we expect a

positive association between the choice of CSR

engagement and governance and monitoring

mechanisms.

CSR, corporate governance, and firm value

The impact of CSR engagement on accounting

performance (i.e., return on assets (ROA)), is a long-

standing, but still unresolved question. According to

the management literature summarized by Margolis

and Walsh (2003), over 120 studies between 1971

and 2001 examine the empirical relation between

CSR and financial performance, and the results are

largely inconclusive. They suggest that previous

studies are subject to various imperfections, such as

measurement problems related to both CSR and

financial performance, a lack of necessary analyses of causality and/or endogeneity, omitted variable

problems, a lack of methodological rigor, and a lack

of theory. While it is hard to draw a definite con-

clusion because of the imperfect nature of many

studies, the review of the empirical CSR literature

conducted by Margolis and Walsh (2003) indicates a

generally positive association between investing in

socially responsible activities and financial perfor-

mance.

The impact of CSR engagement on firm value,

however, is relatively less examined.

4

In particular,there is less evidence regarding how corporate

governance and the CSR engagement jointly affect

firm value after controlling for both the simultaneity

bias and endogeneity. According to the over-

investment hypothesis, insiders such as the CEO and

the board have a natural motivation to over-invest in

CSR activities if doing so enhances their reputation

building process (Barnea and Rubin, 2010). Then,

firm value will be negatively influenced by the

CSR engagement. In contrast, the conflict-resolu-

tion hypothesis suggests that if managers use effective

governance and monitoring mechanisms in con- junction with CSR engagement to resolve conflicts

among stakeholders, then firm value could be posi-

tively associated with CSR engagement and effective

governance mechanisms through reduced conflict-

of-interests among various stakeholders.

Since there is no clear monitoring mechanism to

prevent firms from over-investing in various CSR

activities, we postulate that there should be some

effective monitoring mechanism out of all consid-

ered internal and external governance mechanisms

for the checking and balancing of CSR investments.Board independence can be important in monitoring

the behavior of top management. Fama and Jensen

(1983) maintain that boards can be effective mech-

anisms to monitor top management on behalf of

dispersed shareholders by effectuating management

appointments, dismissals, suspensions, and rewards.

Other studies, however, point toward a paradoxical,

insignificant, or negative association between gov-

ernance quality, as proxied by the percentage of

outside directors on the board, and firm value.

354 Hoje Jo and Maretno A. Harjoto

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 5/34

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 6/34

database includes over 3000 companies containing

various CSR characteristics. In particular, KLD’s

inclusive social rating criteria contain strength ratings

and concern ratings for community, diversity, em-

ployee relations, environment, and product. KLDalso has exclusionary screens, such as alcohol, gam-

bling, military, nuclear power, and tobacco (see

Appendix A). Since KLD’s exclusionary screens

differ from the inclusive screens in that only concern

ratings, but no strength ratings, are assigned, we only

use the inclusive screens in our main tests. While

KLD contains data from approximately 650 firms

listed on the S&P 500 or Domini 400 Social Indexes

each year prior to 2001, the KLD’s ratings comprise

a summary of strengths and concerns assigned to

approximately 1100 (3100) firms listed on the S&P500, the Domini 400 Social Indexes, or the Russell

1000 (Russell 3000) Indexes as of December 31st of

each year for 2001 and 2002 (2003 and 2004). In

2002, KLD renamed the other category as corporate

governance.

Since KLD’s definition of corporate governance,

which includes compensation, ownership, tax dis-

putes, and other issues, is quite different from that of

conventional corporate governance measures, we

use governance and monitoring measures from

RiskMetrics (formerly, the IRRC’s governance and

director) database, CDA/Spectrum 13(f) filings, andthe Institutional Brokers Estimation Services (I/B/

E/S) database instead of KLD’s corporate gover-

nance dimension. The corporate governance and

monitoring measures from the above databases

include the proportion of outside independent

directors, the proportion of institutional holdings,

the proportion of blockholdings, and the number of

security analysts following the firm. Specifically, (i)

our sample firm must be available from the Risk-

Metrics database; (ii) insider blockholder data must

be available; (iii) the data for outside institutionalholdings must be available from CDA/Spectrum

13(f) filings. These filings contain quarterly infor-

mation on common-stock positions greater than

10,000 shares or $200,000 for each institution with

more than $100 million in securities under man-

agement; and (iv) the number of analysts following a

firm must be available from the I/B/E/S database.

Since we also use various accounting and financial

information, we require that sufficient COMPU-

STAT and Center for Research in Security Prices

(CRSP) data are available for our tests. This sample

procedure produces a combined sample of 12,527

firm-year (2952 firms) observations from 1993 to

2004. If there are any (no) observations in the KLD

ratings, then we view them as firms with (no) CSRengagement. We also verify our results based on the

sample containing only positive CSR scores. Actual

samples used in the analyses are slightly different

because the data availability is different for each

regression analysis.

The RiskMetrics does not publish volumes every

year, but publishes volumes in the years of 1993, 1995,

1998, 2000, 2002, and 2004. We fill in the missing

years by assuming that the governance provisions re-

ported in any given year are also in place in the year

preceding the volume’s publication, following Beb-chuk and Cohen (2005) and Gompers et al. (hereafter,

GIM) (2003, 2010). In the case of 2003, for instance,

for which there is no RiskMetrics volume in the

subsequent year, we assume that the governance

provisions are the same as those reported in the

RiskMetrics volume published in 2002. We also

verify whether using a different method based on the

arithmetic average of 2002 and 2004 to assume the

case of 2003 does not change the results. To conduct

the robustness test, we further examine only the

RiskMetrics’s published years of 1993, 1995, 1998,

2000, 2002, and 2004 in the additional test section.

Measurement

To measure external monitoring by institutional

holders, we use the equity ownership of outside

institutional holders as the sum of the greater-than-

five percent owners that are unaffiliated with the

firm (PCTINSTI). We use the number of analysts

who follow the firm to measure external analyst

monitoring by security analysts from the I/B/E/S database. We measure analyst coverage with the

natural logarithm of one plus the number of ana-

lysts following the firm (LOGANAL) because the

number of analysts is highly skewed to the right

(Bushman, et al., 2005; Lim, 2001).

We utilize several structural measures of internal

corporate governance from the RiskMetrics database

(e.g., board characteristics such as independent

outside board proportion, board ownership, and

board leadership, etc.). With these corporate board

356 Hoje Jo and Maretno A. Harjoto

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 7/34

variables, we compare and contrast effective versus

ineffective corporate governance. We first focus on

effective corporate governance, using an indepen-

dent outside director because the rise of such

directors has been a major trend over the last twodecades (see Harris and Raviv, 2008; Hermalin and

Weisbach, 1998, 2003; Raheja, 2005). We follow

the definition of an independent director from that

of the RiskMetrics, which defines an independent

outside director as a director elected by shareholders

who is not affiliated with the company. Based on

Linck et al. (2008), we measure board independence

by the proportion of outside independent directors

(PCTINDEP), and board leadership by a dummy

variable of one if the CEO is the chair of the board

(DUALITY) and another dummy variable if theCEO is the chair or a member of the nomination

committee (CEONOM).

To measure managerial entrenchment, we use the

governance index (GINDEX) developed by GIM

(2003). The RiskMetrics reports 24 anti-takeover

provisions (ATPs) at the firm level because the basic

ingredients for the GINDEX are ATPs. The GIN-

DEX, therefore, ranges from 0 to 24. A high value

indicates stronger managerial power (less takeover

pressure), and a greater potential for managerial

entrenchment. Bebchuk et al. (2009) create an

entrenchment index (ENTINDEX) based on theGINDEX, particularly using six provisions – four

constitutional provisions that prevent a majority of

shareholders from having their way (e.g., staggered

boards, limits to shareholder bylaw amendments,

supermajority requirements for mergers, and super-

majority requirements for charter amendments), and

two takeover-readiness provisions that boards

establish to be ready for a hostile takeover (i.e.,

poison pills and golden parachutes). Bebchuk et al.

(2009) argue that the ENTINDEX based on these

six ATPs drives the main results of firm valuation.This ENTINDEX ranges from 0 to 6, with a higher

value indicating stronger managerial entrenchment.

Thus, we also use Bebchuk et al.’s (2009) ENT-

INDEX to measure managerial entrenchment. See

the definitions of governance, monitoring, and other

control variables in Appendix B.

We measure firm value with Tobin’s q, which is a

widely used measure of firm value in accounting,

economics, and finance literature. Tobin’s q is cal-

culated as: {[Market value of common stock + Book

value of preferred stock + Book value of long-term

debt + Book value of current liabilities- (Book

value of current assets-Book value of Invento-

ries)]/Book value of total assets}. In particular, we

use industry-adjusted Tobin’s q (the natural log of firm’s q divided by the median q in the firm’s

industry) instead of levels of Tobin’s q as a measure

of firm value (Campbell, 1996). The advantage of

using industry-adjusted Tobin’s q (ADJTOBINQ) is

that it neutralizes the effect of specific industries on

Tobin’s q.

Methodology

We conduct an endogeneity correction for thetreatment effects because firm value could come

from two broad sources of unique features: the

choice of CSR engagement and corporate gover-

nance. The CSR involvement’s contribution to firm

value could be overstated if we do not control for

the endogeneity problem (Greene, 1993). Specifi-

cally, it may be that firms engaging into CSR

activities are simply of higher quality and deliver

better performance, regardless of whether they

choose to become involved in CSR. In this case, the

coefficient on the CSR dummy variable might

reveal a value-add from CSR engagement, whenindeed there is no true effect.

Tobin (1958) first identified this endogeneity

problem. If this endogeneity problem is not taken into

consideration in the estimation procedure, an ordin-

ary least-square estimation (OLS) will produce biased

parameter estimates. Heckman (1976, 1979) proposed

a two-stage estimation procedure using the inverse

Mills’ ratio to take account of the endogeneity bias. In

the first step, a regression for observing a positive

outcome of the dependent variable is modeled with a

probit (or logit) model. The estimated parameters areused to calculate the inverse Mills’ ratio, which is then

included as an additional explanatory variable in the

OLS estimation (Greene, 1993). Using Heckman’s

two-stage estimation, we correct the specification for

endogeneity and examine whether CSR activities

enhance firm value.

GIM (2010) employ a different approach, i.e., the

instrumental variable to address the endogene-

ity problem. Heckman and Robb (1985) and

Moffitt (1999) suggest the instrumental variable (IV)

357Corporate Governance and Firm Value

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 8/34

method, which focuses on finding a variable (or

variables) that influences the CSR choice, but does

not influence Tobin’s q (and thus is not correlated

with the random error term in the Tobin’s q

equation). Angrist (2000) asserts that the IV methodworks even when the second-stage model is non-

linear, if the researcher focuses on the causal effects.

Moffitt (1999) further suggests that each IV, that is

indeed uncorrelated with the random error term

in the Tobin’s q equation, will yield unbiased

estimates.5

Our choice of an instrumental variable

is FIRMAGE, which is highly correlated with

CSRDUMMY, but is uncorrelated with industry-

adjusted Tobin’s q (see Table II). We interpret the

results to suggest that older firms can afford CSR

engagement, but not necessarily lead to higher firmvalue.6

Empirical results

Univariate tests and bivariate correlations

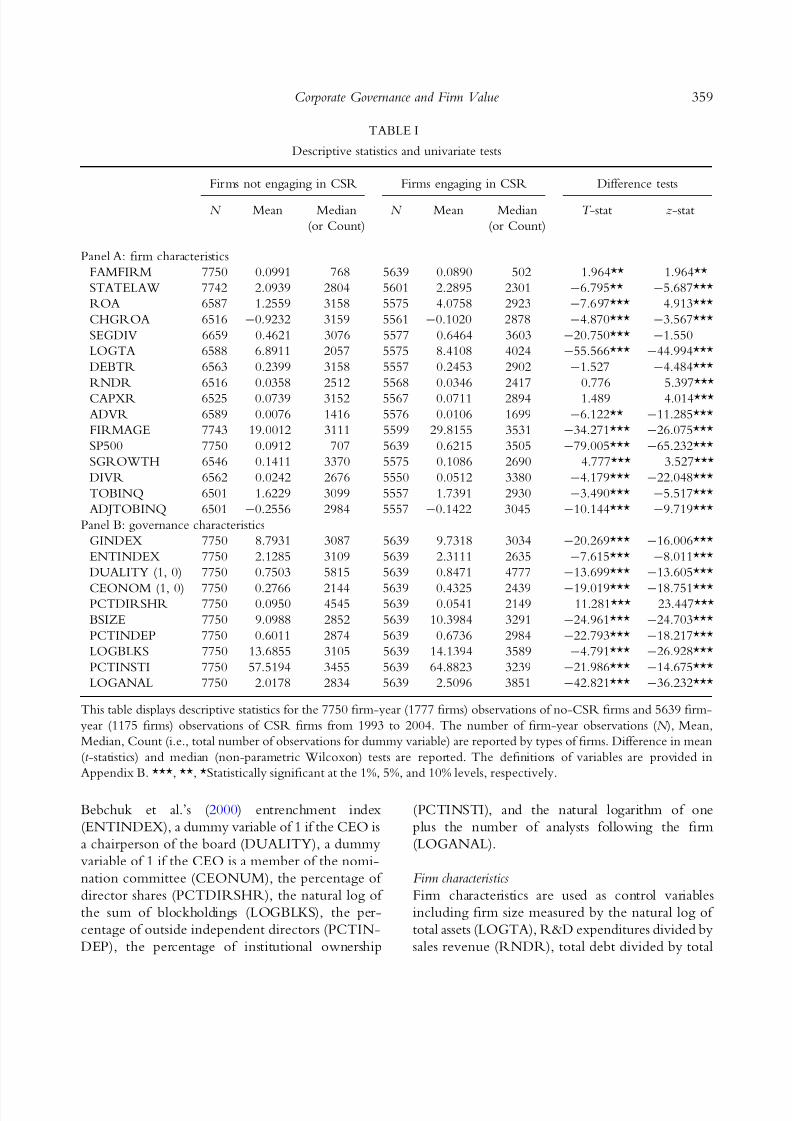

We compare and contrast firm and governance

characteristics in order to test the univariate differ-

ence between CSR firms and no-CSR firms.

Table I presents the means and medians of the

control and governance variables. In Panel A, wefirst examine the differences of the firm character-

istics. In particular, CSR involvement is, on average,

adopted by firms with a lower R&D expenditure

ratio. CSR also is more common among diversified

firms, older firms, larger firms, highly leveraged

firms, more profitable firms, firms belong to the S&P

500, firms using a higher advertising expense ratio,

and firms with a higher Tobin’s q.

The differences of governance characteristics be-

tween CSR firms and no-CSR firms are presented

in Panel B. CSR firms are, on average, associatedwith more active board leadership measured by a

higher proportion of CEOs who are also chairs of

the boards (DUALITY) or chairs or members of

nomination committees (CEONOM), and more

anti-takeover provisions (ATPs), respectively. In

addition, CSR engagement is adopted by firms with

higher total block ownership, higher board inde-

pendence, and a higher percentage of institutional

share ownership. They are also covered by more

security analysts. However, they have a lower per-

centage of director ownership and a larger board

size.

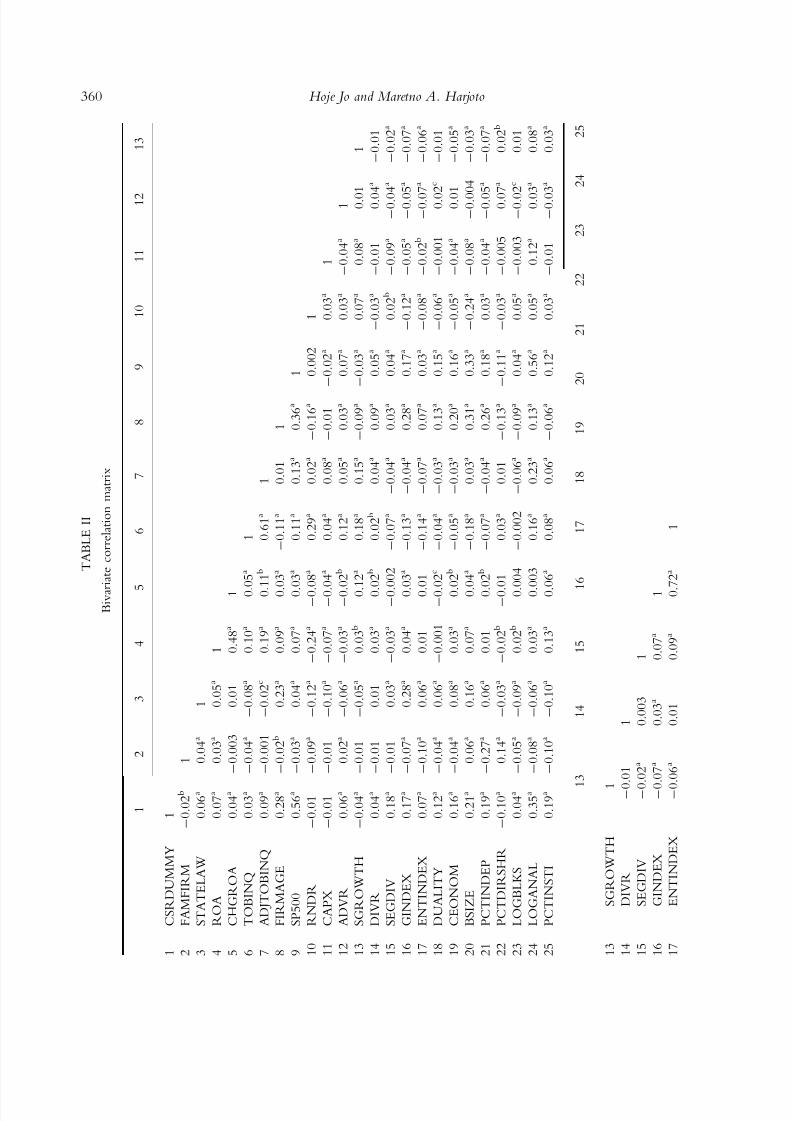

Table II presents the bivariate correlation matrix

for the variables of our main interest discussed in the

previous section. Consistent with the positive asso-ciation between CSR engagement status (CSR) and

board independence (PCTINDEP) or analyst cov-

erage, or institutional share ownership reported

earlier, CSR is positively related to analyst follow-

ing, PCTINDEP, GINDEX, or PCTINSTI. The

correlation coefficients between CSR and the other

variables of interest are relatively high in absolute

numbers, ranging from 0.17 to 0.35. All of the

above correlations are statistically significant ( p val-

ues< 0.01). All governance variables (variable

numbers 16 through 25) are significantly correlatedwith the CSR variable as well. Tobin’s q is positively

related to the CSR variable (0.03, with p val-

ues< 0.01).

The determinants of CSR engagement

To understand the differences between firms with

and without CSR involvement, we adopt a probit

analysis of the choice decision, with the following

model:

Pr ½CSR it jZ it ¼ U½B 0 Z it

where CSR it is a dummy variable equal to one if

firm i has CSR engagement in year t , and 0 other-

wise. Z it is a vector of firm, governance, or moni-

toring characteristics at the time of firm i ’s choice

of CSR engagement. B is a vector of coefficients.

To understand firm and governance characteris-

tics that lead some firms to choose CSR engage-

ment, we choose several variables to model the

probability of that choice. Based on the previous

literature and our chosen governance metrics, weinclude the variables as components of Z and explain

in detail in the following sections.

Governance and monitoring variables

We hypothesize that internal and external moni-

toring and governance mechanisms should be related

to the choice of CSR engagement. Thus, we include

various internal and external governance variables,

including the number of anti-takeover provisions

using the GIM (2003) g index (GINDEX), or

358 Hoje Jo and Maretno A. Harjoto

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 9/34

Bebchuk et al.’s (2000) entrenchment index

(ENTINDEX), a dummy variable of 1 if the CEO is

a chairperson of the board (DUALITY), a dummy

variable of 1 if the CEO is a member of the nomi-

nation committee (CEONUM), the percentage of

director shares (PCTDIRSHR), the natural log of

the sum of blockholdings (LOGBLKS), the per-

centage of outside independent directors (PCTIN-

DEP), the percentage of institutional ownership

(PCTINSTI), and the natural logarithm of one

plus the number of analysts following the firm

(LOGANAL).

Firm characteristics

Firm characteristics are used as control variables

including firm size measured by the natural log of

total assets (LOGTA), R&D expenditures divided by

sales revenue (RNDR), total debt divided by total

TABLE I

Descriptive statistics and univariate tests

Firms not engaging in CSR Firms engaging in CSR Difference tests

N Mean Median N Mean Median T -stat z-stat

(or Count) (or Count)

Panel A: firm characteristics

FAMFIRM 7750 0.0991 768 5639 0.0890 502 1.964** 1.964**

STATELAW 7742 2.0939 2804 5601 2.2895 2301 -6.795** -5.687***

ROA 6587 1.2559 3158 5575 4.0758 2923 -7.697*** 4.913***

CHGROA 6516 -0.9232 3159 5561 -0.1020 2878 -4.870*** -3.567***

SEGDIV 6659 0.4621 3076 5577 0.6464 3603 -20.750*** -1.550

LOGTA 6588 6.8911 2057 5575 8.4108 4024 -55.566*** -44.994***

DEBTR 6563 0.2399 3158 5557 0.2453 2902 -1.527 -4.484***

RNDR 6516 0.0358 2512 5568 0.0346 2417 0.776 5.397***

CAPXR 6525 0.0739 3152 5567 0.0711 2894 1.489 4.014***

ADVR 6589 0.0076 1416 5576 0.0106 1699 -6.122** -11.285***

FIRMAGE 7743 19.0012 3111 5599 29.8155 3531 -34.271*** -26.075***

SP500 7750 0.0912 707 5639 0.6215 3505 -79.005*** -65.232***

SGROWTH 6546 0.1411 3370 5575 0.1086 2690 4.777*** 3.527***

DIVR 6562 0.0242 2676 5550 0.0512 3380 -4.179*** -22.048***

TOBINQ 6501 1.6229 3099 5557 1.7391 2930 -3.490*** -5.517***

ADJTOBINQ 6501 -0.2556 2984 5557 -0.1422 3045 -10.144*** -9.719***

Panel B: governance characteristics

GINDEX 7750 8.7931 3087 5639 9.7318 3034 -20.269*** -16.006***

ENTINDEX 7750 2.1285 3109 5639 2.3111 2635 -7.615*** -8.011***

DUALITY (1, 0) 7750 0.7503 5815 5639 0.8471 4777 -13.699*** -13.605***

CEONOM (1, 0) 7750 0.2766 2144 5639 0.4325 2439 -19.019*** -18.751***PCTDIRSHR 7750 0.0950 4545 5639 0.0541 2149 11.281*** 23.447***

BSIZE 7750 9.0988 2852 5639 10.3984 3291 -24.961*** -24.703***

PCTINDEP 7750 0.6011 2874 5639 0.6736 2984 -22.793*** -18.217***

LOGBLKS 7750 13.6855 3105 5639 14.1394 3589 -4.791*** -26.928***

PCTINSTI 7750 57.5194 3455 5639 64.8823 3239 -21.986*** -14.675***

LOGANAL 7750 2.0178 2834 5639 2.5096 3851 -42.821*** -36.232***

This table displays descriptive statistics for the 7750 firm-year (1777 firms) observations of no-CSR firms and 5639 firm-

year (1175 firms) observations of CSR firms from 1993 to 2004. The number of firm-year observations (N ), Mean,

Median, Count (i.e., total number of observations for dummy variable) are reported by types of firms. Difference in mean

(t -statistics) and median (non-parametric Wilcoxon) tests are reported. The definitions of variables are provided in

Appendix B. ***, **, *Statistically significant at the 1%, 5%, and 10% levels, respectively.

359Corporate Governance and Firm Value

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 10/34

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 11/34

assets (DEBTR), and the Fama–French 48-industry

classification. GIM (2010) suggest using the State

Law as anti-takeover index. Similar to GIM, we

also use the State Law anti-takeover index

(STATELAW), family firms (FAMFIRM), ROA,the natural log of the change in ROA (CHGROA)

to measure profitability, and the diversification

dummy (SEGDIV). We choose family firms instead

of GIM’s name variable because the private benefits

of control should be more relevant to family

firms, following Anderson and Reeb (2003) and

Villalonga and Amit (2006).

In Table III, we estimate the choice of CSR

engagement using a probit function. We estimate five

models with different sets of explanatory variables

to compare and contrast the various impacts of con-trol variables and corporate governance variables.

Throughout Model (1) to Model (5), we replace or add

some of the explanatory variables to investigatethe role

of governance and monitoring in the analysis.7

Consistent with prior literature, we can see that

many of our chosen variables are highly significant in

explaining the likelihood of choosing CSR engage-

ment for all Models (1) to (5). Model (1) shows that

larger firms, highly leveraged firms, profitable firms,

firms with higher R&D, and diversified firms are

more likely to choose CSR engagement while the

coefficient on FAMFIRM is insignificant. Model (2)shows the same results with the industry adjustment.

Basically, the results are similar, except the signifi-

cance of CHGROA disappears. In model (3), we

report the results for the governance variables only.

Model (3) suggests that the coefficients on GINDEX,

DUALITY, CEONOM, PCTINDEP, PCTINSTI,

and LOGANAL are significantly positive at the 1%

significance level, implying that firms with a higher

board leadership (DUALITY and CEONOM), a

higher proportion of outside independent directors

(PCTINDEP), a higher proportion of institutionalinvestors (PCTINSTI), more analysts following the

firm (LOGANAL), or more anti-takeover provisions

(GINDEX) are more likely to choose CSR engage-

ment.8 We find that the estimated slope coefficients

on PCTINDEP and LOGANAL have the highest

economic significance on the firms’ choice of CSR

engagement. These findings suggest that internal and

external governance measured by board leader-

ship, independent boards, institutional investors, and

security analysts are positively related to the choice of

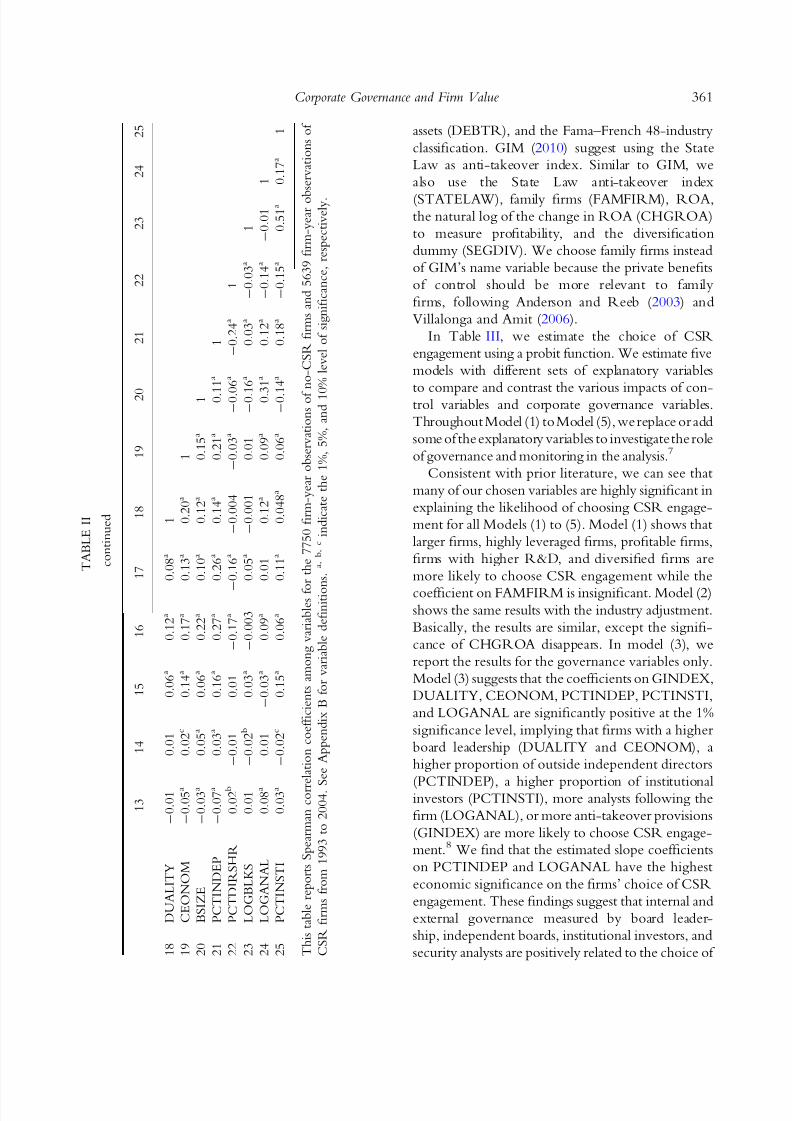

T A B L E I I

c o n t i n u e d

1 3

1 4

1 5

1 6

1 7

1 8

1 9

2 0

2 1

2 2

2 3

2 4

2 5

1 8

D U A L I T Y

- 0 . 0 1

0 . 0 1

0 . 0 6 a

0 . 1 2 a

0 . 0 8 a

1

1 9

C E O N O M

- 0 . 0 5 a

0 . 0 2 c

0 . 1 4 a

0 . 1 7 a

0 . 1 3 a

0 . 2 0 a

1

2 0

B S I Z E

- 0 . 0 3 a

0 . 0 5 a

0 . 0 6 a

0 . 2 2 a

0 . 1 0 a

0 . 1 2 a

0 . 1 5 a

1

2 1

P C T I N D E P

- 0 . 0 7 a

0 . 0 3 a

0 . 1 6 a

0 . 2 7 a

0 . 2 6 a

0 . 1 4 a

0 . 2 1 a

0 . 1

1 a

1

2 2

P C T D I R S H R

0 . 0 2 b

- 0 . 0 1

0 . 0 1

- 0 . 1 7 a

-

0 . 1 6 a

- 0 . 0 0 4

- 0 . 0 3 a

- 0 . 0

6 a

- 0 . 2 4 a

1

2 3

L O G B L K S

0 . 0 1

- 0 . 0 2 b

0 . 0 3 a

- 0 . 0 0 3

0 . 0 5 a

- 0 . 0 0 1

0 . 0 1

- 0 . 1

6 a

0 . 0 3 a

- 0 . 0 3 a

1

2 4

L O G A N A L

0 . 0 8 a

0 . 0 1

- 0 . 0 3 a

0 . 0 9 a

0 . 0 1

0 . 1 2 a

0 . 0 9 a

0 . 3

1 a

0 . 1 2 a

- 0 . 1 4 a

- 0 . 0 1

1

2 5

P C T I N S T I

0 . 0 3 a

- 0 . 0 2 c

0 . 1 5 a

0 . 0 6 a

0 . 1 1 a

0 . 0 4 8 a

0 . 0 6 a

- 0 . 1

4 a

0 . 1 8 a

- 0 . 1 5 a

0 . 5 1 a

0 . 1 7 a

1

T h i s t a b l e r e p o r t s S p e a r m a n c o r r e l a t i o n c o e f fi c i e n t s a m o n g v a r i a b l e s f o

r t h e 7 7 5 0 fi r m - y e a r o b s e r v a t i o n s o f n o - C S R fi r m s a n d 5 6 3 9 fi r m - y e a r o b

s e r v a t i o n s o f

C S R fi r m s f r o m 1 9 9 3 t o 2 0 0 4 . S

e e A p p e n d i x B f o r v a r i a b l e d e fi n i t i o n s .

a ,

b ,

c

i n d i c a t e t h e 1 % , 5 % , a n d 1 0

% l e v e l o f s i g n i fi c a n c e , r e s p e c t i v e l y .

361Corporate Governance and Firm Value

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 12/34

TABLE III

Propensity to engage in CSR activities

Model (1) Model (2) Model (3) Model (4) Model (5)

INTERCEPT -3.710

(44.07)***

-4.912

(14.21)***

-3.258

(10.05)***

-5.607

(16.25)***

-5.491

(16.11)***

Governance variables

GINDEX 0.071

(12.29)***

0.049

(7.71)***

ENTINDEX 0.031

(2.87)***

DUALITY 0.121

(3.69)***

0.019

(0.53)

0.030

(0.87)

CEONOM 0.254

(9.35)***

0.102

(3.50)***

0.113

(3.85)***

PCTDIRSHR -0.002

(0.03)

-0.037

(0.54)

-0.065

(0.91)PCTINDEP 0.708

(8.90)***

0.470

(5.47)***

0.529

(6.16)***

LOGBLKS -0.002

(0.65)

0.002

(0.70)

0.002

(0.58)

PCTINSTI 0.010

(11.42)***

0.008

(8.79)***

0.008

(8.83)***

LOGANAL 0.692

(32.14)***

0.150

(5.31)***

0.149

(5.26)***

Control variables

LOGTA 0.429

(43.09)***

0.583

(47.39)***

0.495

(32.25)***

0.506

(32.89)***

DEBTR -0.296(3.86)***

-0.724(7.88)***

-0.793(8.57)***

-0.776(8.41)***

RNDR 2.184

(11.48)***

1.485

(6.33)***

1.264

(5.31)***

1.211

(5.13)***

FAMFIRM -0.054

(1.25)

-0.062

(1.37)

0.135

(2.81)***

0.134

(2.79)***

STATELAW 0.025

(3.27)***

0.022

(2.74)***

0.011

(1.26)

0.029

(3.47)***

ROA 0.022

(9.69)***

0.013

(5.45)***

0.009

(3.78)***

0.009

(3.80)***

CHGROA -0.004

(2.06)**

0.004

(0.18)

0.001

(0.67)

0.001

(0.63)

SEGDIV 0.369

(14.58)***

0.450

(16.59)***

0.387

(13.43)***

0.383

(13.31)***

F–F 48 industry No Yes Yes Yes Yes

Pseudo R 2 0.1937 0.2571 0.1777 0.2778 0.2746

Observations 11,901 11,901 11,901 11,901 11,901

Number of firms 2493 2493 2493 2493 2493

This table reports the coefficient of estimates from the probit model explaining the determinants of CSR engagement.

The dependent variable is the CSR, which is a dichotomous variable that equals to one if a firm has involved into CSR

activities. Otherwise equals to zero. Model (1) and (2) report only control variables. Model (3), (4), and (5) include

internal and external corporate governance variables. Fama–French (F–F) 48 industry is included all Models except Model

(1). T -statistics are adjusted for robust and clustered (by firm) standard errors and reported in parentheses. Appendix B

provides variable definitions. ***, **, *Statistically significant at the 1%, 5%, and 10% levels, respectively.

362 Hoje Jo and Maretno A. Harjoto

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 13/34

CSR engagement, supporting the conflict-resolution

hypothesis, as stated in hypothesis 1.

Other variables are insignificant at the conventional

level. In models (4) and (5), we report the results when

we include both control variables and governancevariables. The results for the governance variables are

qualitatively similar to those of model (3), except the

insignificance of the DUALITY variable. It is

important to note that the internal and external gov-

ernance variables are highly significant, suggesting

that they are major determinants of CSR engagement.

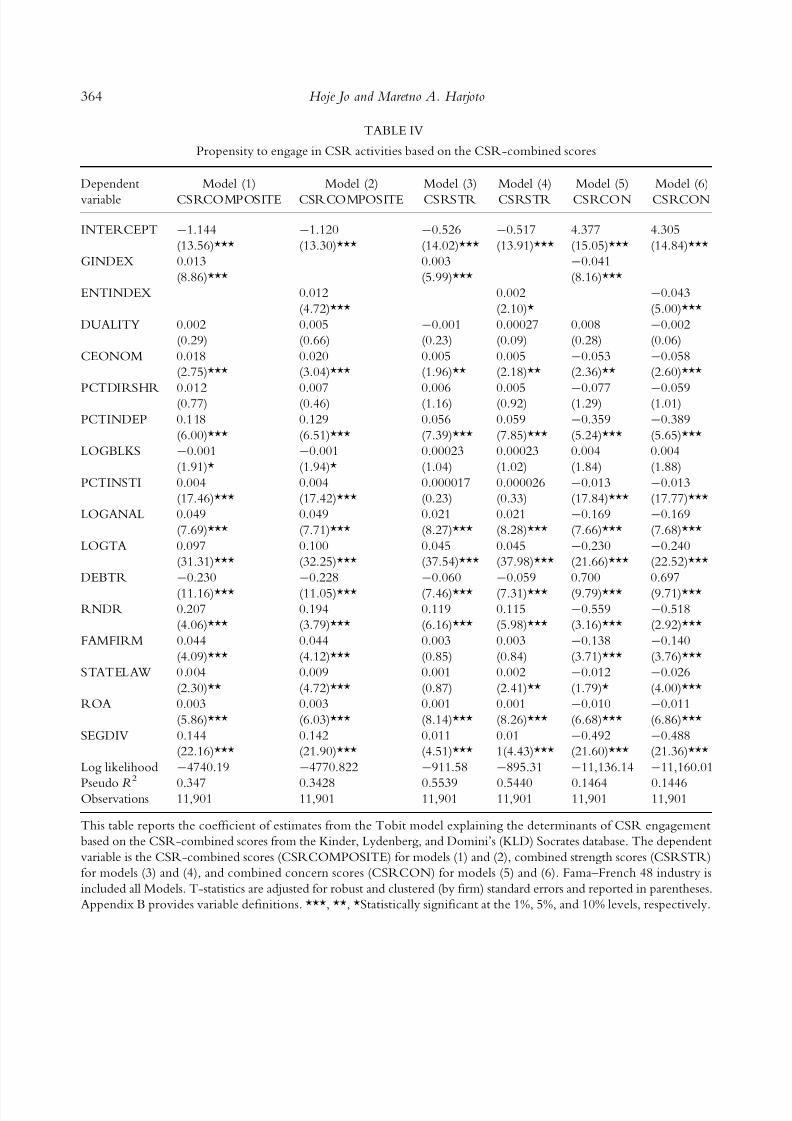

Table IV reports the coefficient of estimates from

the Tobit model explaining the determinants of

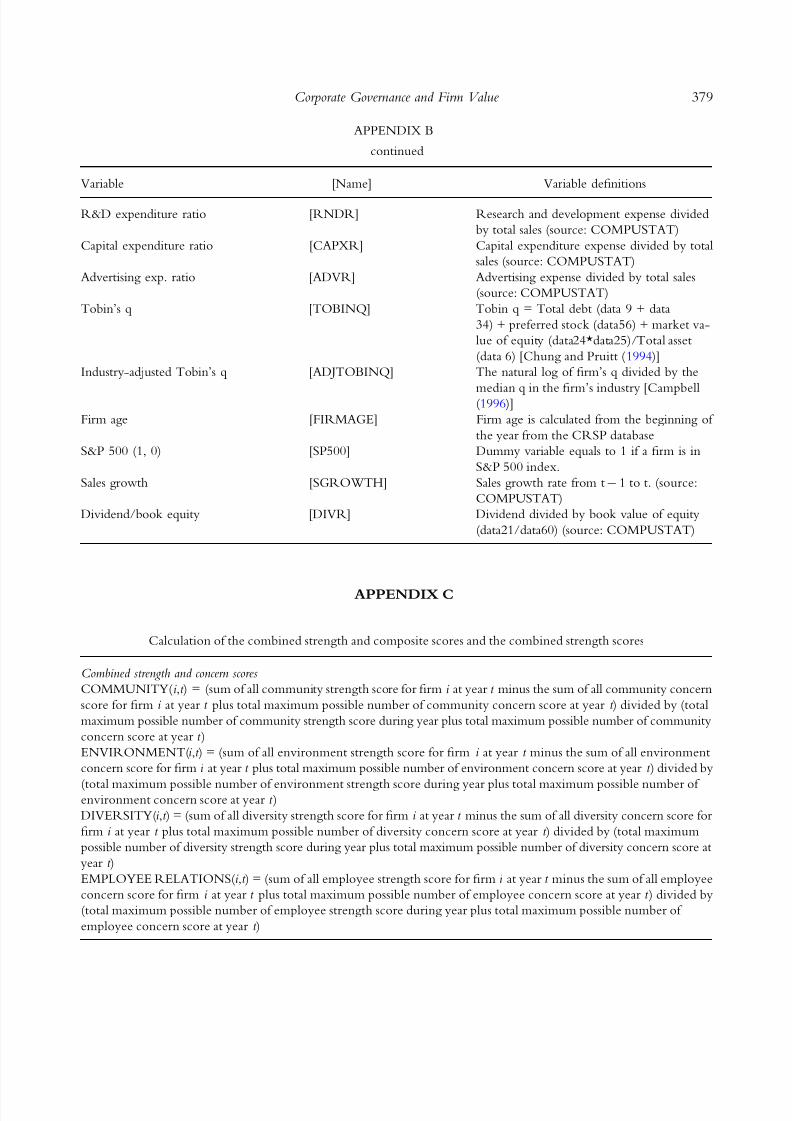

CSR engagement based on the CSR-combined

scores instead of the CSR choice (dummy) variable.

We use the Tobit model because the dependentvariables are left censored at zero rather than

dichotomous variables. The Tobit model is an

econometric model proposed by Tobin (1958)

to describe the relation between a non-negative

dependent variable and an independent variable (or

vector). We compute the arithmetic average of the

combined scores of KLD inclusive strengths and

concerns of community, environment, diversity,

employee relations, and product criteria to get

combined CSR scores. KLD scores report both

strengths and concerns for the above-mentioned

dimensions. The dependent variable is the CSR-combined scores, including both strengths and

concerns (CSRCOMPOSITE) for models (1) and

(2), combined strength scores (CSRSTR) for models

(3) and (4), and combined concern scores (CSR-

CON) for models (5) and (6), respectively [see the

calculation procedures of the combined strengths

and concerns, combined strength, and combined

concern scores (unreported, but similar to the cal-

culation of strength scores in Appendix C)]. The

results closely mirror those of Table III, in that

the governance and monitoring variables positivelyaffect the firms’ decisions about CSR engagement,

supporting the conflict-resolution hypothesis. As

expected, the signs of the coefficients on all the

variables based on CSRCON are exactly opposite of

those of the coefficients based on CSRSTR.

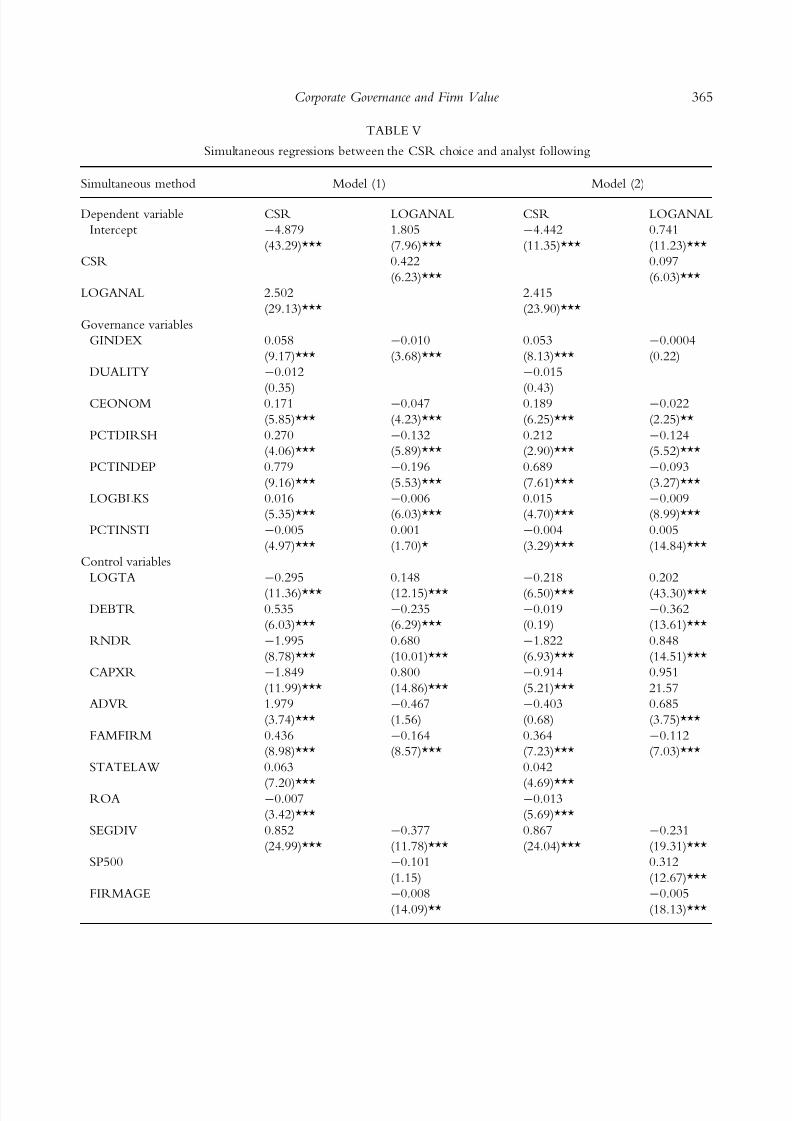

Table V shows the results of the 2SLS with the two

dependent variables of CSR and LOGANAL. We

employ the 2SLS estimation method described in

Maddala (1983) for simultaneous equations models in

which one of the endogenous variables is continuous

(LOGANAL) and the other endogenous variable is

dichotomous (CSR). Our results suggest that after

correcting for a potential simultaneity bias, the possi-

bility that firms with a greater analyst following tend to

engage in CSR engagement (with t -values of 23.90– 29.13) is much higher than the possibility that firms

choosing CSR tend to have a higher analyst following

(with t -values of 6.03–6.23). It seems that firms with

greater analyst coverage (i.e., firms with a transparent

information environment) opt for CSR engagement

after incorporating the reverse causality. In addition,

although the top management of CSR firms can

control the number of outside independent directors,

they cannot control the number of analysts following

the firm. Accordingly, security analysts, as third-party

information intermediaries, can provide an externalmonitoring mechanism in the top management’s

decision-making about CSR engagement.

So far, we use board independence as one of the

measures for the quality of the firm’s internal gov-

ernance. But for two reasons there may not be a

one-to-one relation between governance quality and

board independence. First, Coles et al. (2008) indi-

cate that board independence reflects such things as

firm diversification, firm size, firm age, and insider

ownership. These researchers claim that board

independence reflects, and is driven by, other

characteristics of the firm and its line of business.There is no single board structure that fits all

firms. Rather, board independence is endogenously

determined by firm and managerial characteristics.

This indicates that board independence may or may

not be an indicator of governance quality. Suppose,

for example, that ceteris paribus, board independence

does improve governance. Then, firms with few

independent directors might have more blockhold-

ers, or fewer takeover defenses, or more bond cov-

enants, to offset the effects of having few

independent directors. The result could be that suchfirms have better governance, not worse. Thus, we

include such variables, including firm diversification,

firm size, firm age, insider ownership, blockholder

ownership, and GIM index, etc. in the independent

director equation to address the endogeneity issue.

Our unreported results based on two-stage least-

square (2SLS) regressions, in which both CSR

engagement and the percentage of outside indepen-

dent directors are dependent variables, again support

the monitoring role of outside independent directors.

363Corporate Governance and Firm Value

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 14/34

TABLE IV

Propensity to engage in CSR activities based on the CSR-combined scores

Dependent

variable

Model (1) Model (2) Model (3) Model (4) Model (5) Model (6)

CSRCOMPOSITE CSRCOMPOSITE CSRSTR CSRSTR CSRCON CSRCON

INTERCEPT -1.144

(13.56)***

-1.120

(13.30)***

-0.526

(14.02)***

-0.517

(13.91)***

4.377

(15.05)***

4.305

(14.84)***

GINDEX 0.013

(8.86)***

0.003

(5.99)***

-0.041

(8.16)***

ENTINDEX 0.012

(4.72)***

0.002

(2.10)*

-0.043

(5.00)***

DUALITY 0.002

(0.29)

0.005

(0.66)

-0.001

(0.23)

0.00027

(0.09)

0.008

(0.28)

-0.002

(0.06)

CEONOM 0.018

(2.75)***

0.020

(3.04)***

0.005

(1.96)**

0.005

(2.18)**

-0.053

(2.36)**

-0.058

(2.60)***

PCTDIRSHR 0.012(0.77) 0.007(0.46) 0.006(1.16) 0.005(0.92)

-

0.077(1.29)

-

0.059(1.01)

PCTINDEP 0.118

(6.00)***

0.129

(6.51)***

0.056

(7.39)***

0.059

(7.85)***

-0.359

(5.24)***

-0.389

(5.65)***

LOGBLKS -0.001

(1.91)*

-0.001

(1.94)*

0.00023

(1.04)

0.00023

(1.02)

0.004

(1.84)

0.004

(1.88)

PCTINSTI 0.004

(17.46)***

0.004

(17.42)***

0.000017

(0.23)

0.000026

(0.33)

-0.013

(17.84)***

-0.013

(17.77)***

LOGANAL 0.049

(7.69)***

0.049

(7.71)***

0.021

(8.27)***

0.021

(8.28)***

-0.169

(7.66)***

-0.169

(7.68)***

LOGTA 0.097

(31.31)***

0.100

(32.25)***

0.045

(37.54)***

0.045

(37.98)***

-0.230

(21.66)***

-0.240

(22.52)***

DEBTR -0.230

(11.16)***

-0.228

(11.05)***

-0.060

(7.46)***

-0.059

(7.31)***

0.700

(9.79)***

0.697

(9.71)***RNDR 0.207

(4.06)***

0.194

(3.79)***

0.119

(6.16)***

0.115

(5.98)***

-0.559

(3.16)***

-0.518

(2.92)***

FAMFIRM 0.044

(4.09)***

0.044

(4.12)***

0.003

(0.85)

0.003

(0.84)

-0.138

(3.71)***

-0.140

(3.76)***

STATELAW 0.004

(2.30)**

0.009

(4.72)***

0.001

(0.87)

0.002

(2.41)**

-0.012

(1.79)*

-0.026

(4.00)***

ROA 0.003

(5.86)***

0.003

(6.03)***

0.001

(8.14)***

0.001

(8.26)***

-0.010

(6.68)***

-0.011

(6.86)***

SEGDIV 0.144

(22.16)***

0.142

(21.90)***

0.011

(4.51)***

0.01

1(4.43)***

-0.492

(21.60)***

-0.488

(21.36)***

Log likelihood -4740.19 -4770.822 -911.58 -895.31 -11,136.14 -11,160.01

Pseudo R 2

0.347 0.3428 0.5539 0.5440 0.1464 0.1446Observations 11,901 11,901 11,901 11,901 11,901 11,901

This table reports the coefficient of estimates from the Tobit model explaining the determinants of CSR engagement

based on the CSR-combined scores from the Kinder, Lydenberg, and Domini’s (KLD) Socrates database. The dependent

variable is the CSR-combined scores (CSRCOMPOSITE) for models (1) and (2), combined strength scores (CSRSTR)

for models (3) and (4), and combined concern scores (CSRCON) for models (5) and (6). Fama–French 48 industry is

included all Models. T-statistics are adjusted for robust and clustered (by firm) standard errors and reported in parentheses.

Appendix B provides variable definitions. ***, **, *Statistically significant at the 1%, 5%, and 10% levels, respectively.

364 Hoje Jo and Maretno A. Harjoto

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 15/34

TABLE V

Simultaneous regressions between the CSR choice and analyst following

Simultaneous method Model (1) Model (2)

Dependent variable CSR LOGANAL CSR LOGANAL

Intercept -4.879

(43.29)***

1.805

(7.96)***

-4.442

(11.35)***

0.741

(11.23)***

CSR 0.422

(6.23)***

0.097

(6.03)***

LOGANAL 2.502

(29.13)***

2.415

(23.90)***

Governance variables

GINDEX 0.058

(9.17)***

-0.010

(3.68)***

0.053

(8.13)***

-0.0004

(0.22)

DUALITY -0.012

(0.35)

-0.015

(0.43)CEONOM 0.171

(5.85)***

-0.047

(4.23)***

0.189

(6.25)***

-0.022

(2.25)**

PCTDIRSH 0.270

(4.06)***

-0.132

(5.89)***

0.212

(2.90)***

-0.124

(5.52)***

PCTINDEP 0.779

(9.16)***

-0.196

(5.53)***

0.689

(7.61)***

-0.093

(3.27)***

LOGBLKS 0.016

(5.35)***

-0.006

(6.03)***

0.015

(4.70)***

-0.009

(8.99)***

PCTINSTI -0.005

(4.97)***

0.001

(1.70)*

-0.004

(3.29)***

0.005

(14.84)***

Control variables

LOGTA -0.295

(11.36)***

0.148

(12.15)***

-0.218

(6.50)***

0.202

(43.30)***DEBTR 0.535

(6.03)***

-0.235

(6.29)***

-0.019

(0.19)

-0.362

(13.61)***

RNDR -1.995

(8.78)***

0.680

(10.01)***

-1.822

(6.93)***

0.848

(14.51)***

CAPXR -1.849

(11.99)***

0.800

(14.86)***

-0.914

(5.21)***

0.951

21.57

ADVR 1.979

(3.74)***

-0.467

(1.56)

-0.403

(0.68)

0.685

(3.75)***

FAMFIRM 0.436

(8.98)***

-0.164

(8.57)***

0.364

(7.23)***

-0.112

(7.03)***

STATELAW 0.063

(7.20)***

0.042

(4.69)***ROA -0.007

(3.42)***

-0.013

(5.69)***

SEGDIV 0.852

(24.99)***

-0.377

(11.78)***

0.867

(24.04)***

-0.231

(19.31)***

SP500 -0.101

(1.15)

0.312

(12.67)***

FIRMAGE -0.008

(14.09)**

-0.005

(18.13)***

365Corporate Governance and Firm Value

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 16/34

We find that the coefficients on PCTINDEP and

CSR are positive and statistically significant ( p va-lue< 0.01). We also find that the coefficients on

PCTDIRSHR, LOGBLKS, and LOGANAL are

significantly positive. These results suggest that having

a certain governance structure is important in deter-

mining CSR involvement. However, we also find

that the causality runs from some governance and

control variables to board independence. Since nei-

ther CSR engagement nor board independence

changes frequently, simple 2SLS results may not

capture causality precisely.9 Nevertheless, this reverse

causality suggests that after correcting for a potentialsimultaneity bias, the possibility that firms choosing

CSR engagement tend to have outside independent

directors (with t -values of 9.17–10.35) is slightly

smaller than the possibility that firms with a higher

proportion of independent directors engage in CSR

engagement (with t -values of 17.58–19.12). It seems

that the potential simultaneity bias does not signifi-

cantly change our inferences concerning the associa-

tion between the governance and monitoring

variables and CSR engagement.

The value of firms with CSR engagement

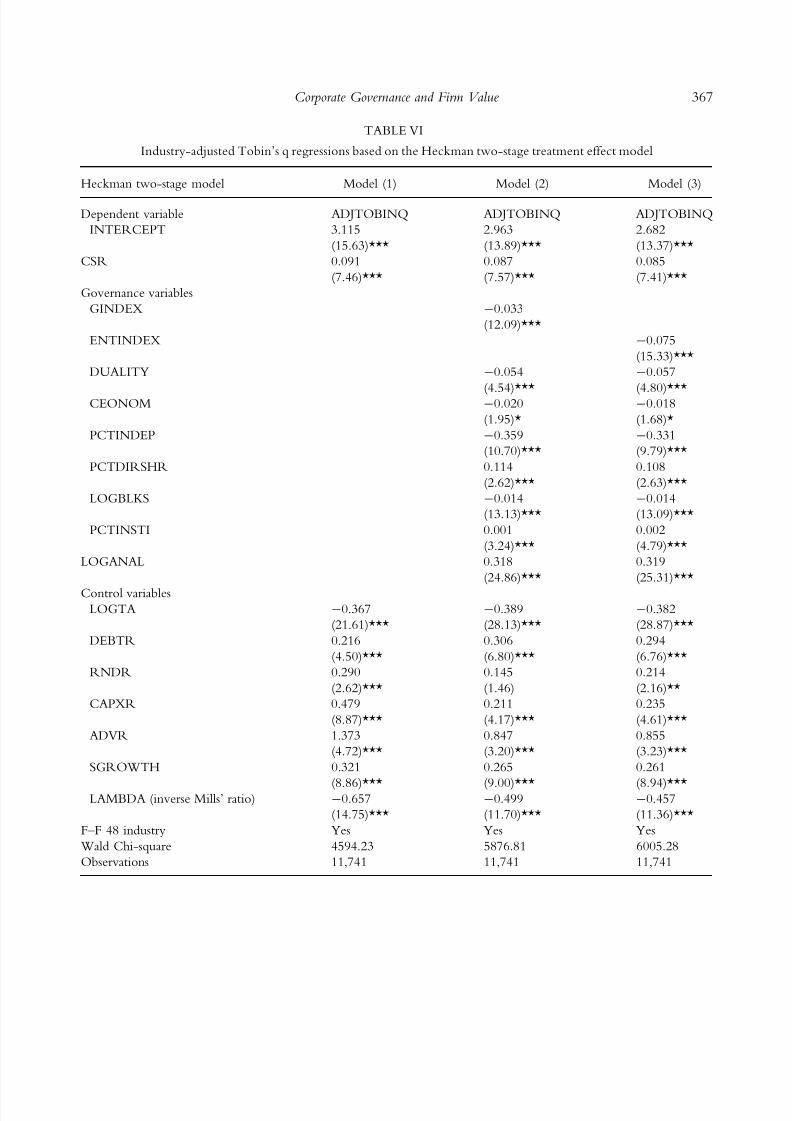

Next, this study examines the impact of CSR

involvement on firm value, measured by industry-

adjusted Tobin’s q (ADJTOBINQ) because Camp-

bell (1996) suggests that ADJTOBINQ neutralizes

the industry effect on Tobin’s q. Using Heckman’s

(1979) two-stage model, we report several models in

Table VI. In model (1), following GIM (2010), Shin

and Stulz (2000), and Morck and Yang (2001), we

include capital expenditures divided by total sales

(CAPXR), the ratio of advertising to sales (ADVR),growth options measured by R&D expenditure

divided by sales (RNDR), and sales growth

(SGROWTH). The evidence suggests that CSR

engagement positively affects firm value measured

by industry-adjusted Tobin’s q after correcting for

the endogenous treatment effect, supporting the

conflict-resolution hypothesis as opposed to the

overinvestment hypothesis.

Next, we add governance and monitoring vari-

ables to examine whether any governance or moni-

toring variables influence firm value after theendogeneity correction, and report the results of the

positive association between CSR and ADJTO-

BINQ in model (2). In particular, a one unit increase

of CSR engagement is followed by an increase of

0.085 times of ADJTOBINQ. In addition, the

coefficient on LOGANAL is significantly positive

with a t -value of 24.86, suggesting that security

analysts provide an additional monitoring role, which

is supportive for hypothesis 2(b). This evidence is

consistent with Chung and Jo (1996), who find that

analyst coverage makes a firm’s information envi-

ronment transparent and positively affects firm value.

The coefficient on PCTINSTI is also positive, but its

magnitude is only marginal. In contrast, however, the

coefficients on DUALITY and GINDEX are sig-

nificantly negative, indicating that the dual role of the

CEO and the chairperson and many take-over de-

fenses through anti-takeover provisions (GINDEX)

adversely affect firm value. In particular, an inverse

association between GINDEX and industry-adjusted

Tobin’s q implies that too much take-over defense

TABLE V

continued

Simultaneous method Model (1) Model (2)

F–F 48 Industry No No Yes Yes

Pseudo R 2 0.2862 0.3130

Adjusted R 2 0.5305 0.5304

Observations 11,808 11,808 11,808 11,808

This table shows the results from two-stage estimation method described in Maddala (1983) for simultaneous equations

models in which one of the endogenous variables is continuous (LOGANAL) and the other endogenous variable is

dichotomous (CSR). T-statistics are adjusted for robust and clustered (by firm) standard errors and reported in parentheses.

See Appendix B for variable definitions. ***, **, *Statistically significant at the 1%, 5%, and 10% levels, respectively.

366 Hoje Jo and Maretno A. Harjoto

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 17/34

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 18/34

adversely affects firm value, which is consistent with

Cremers and Nair (2005) and GIM (2003).

Model (3) shows that the results based on Bebchuket al.’s (2009) entrenchment index are even more

significantly and inversely associated with industry-

adjusted Tobin’s q, confirming the adverse effects of

managerial entrenchment on firm value. More

importantly, the positive associations between CSR

and ADJTOBINQ and LOGANAL and ADJTO-

BINQ remain unchanged. Although unreported, the

above results do not change when we run the

regressions with each governance variable separately

to reduce potential problems due to multicollinear-

ity. Consistent with Agrawal and Knoeber (1996),we also find a negative association between ADJT-

OBINQ and the proportion of outside independent

directors. The coefficients on lambda (inverse Mills’

ratio), however, are significantly negative in all three

models, implying a possibility that the above results

contain some sample selection bias.

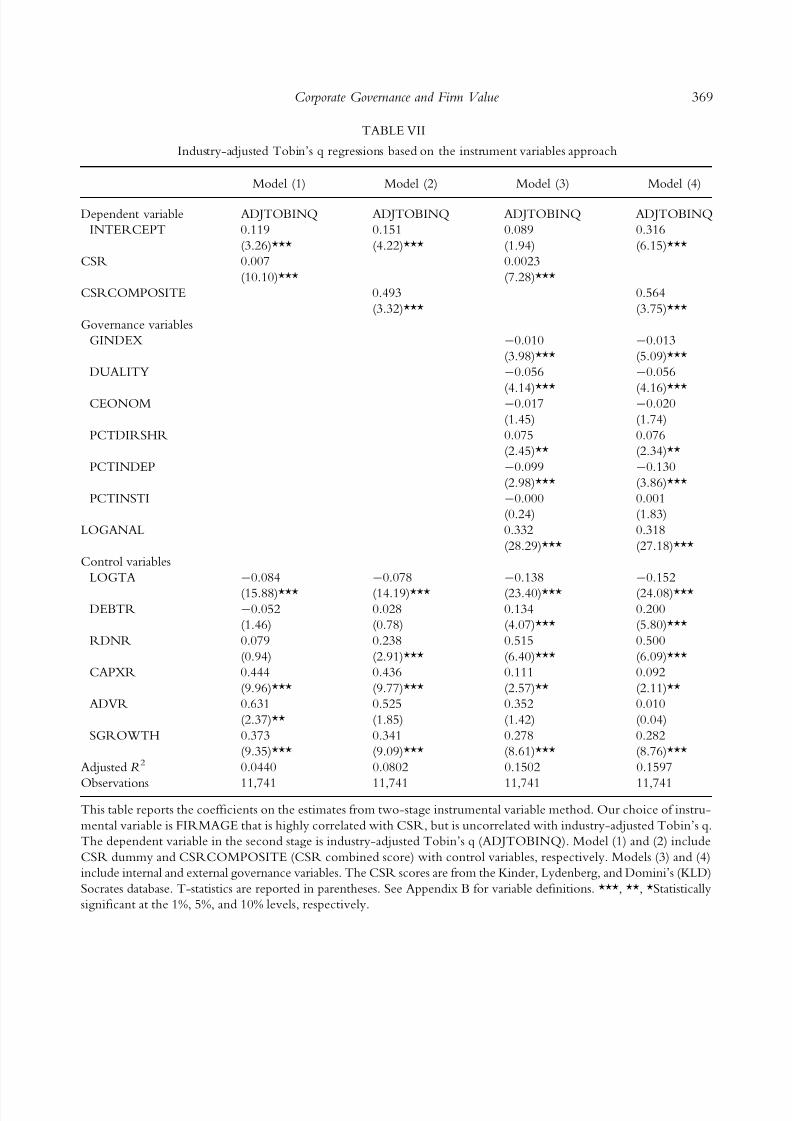

Thus, to address the selection bias problem, we

report the results based on the instrumental variables

approach in Table VII. The results, in general, clo-

sely mirror the Heckman two-stage results based on

endogeneity control. Most notably, both the coef-

ficients on the CSR dummy and the CSRCOM-

POSITE (CSR combined score) suggest that CSR

engagement is positively associated with firm value

with or without governance variables as independent

variables, supporting our hypothesis 2 (a) of CSR as

a conflict-resolution. The positive impact of analyst

following on firm value is also strongly significant in

all models. The results remain robust under various

specifications using the Heckman two-stage, OLS

(unreported), and instrumental variables approach,

strongly supporting hypothesis 2(b) for the external

monitoring role of security analysts. Notably, how-

ever, the coefficients on PCTINSTI become insig-nificant, possibly because of their dual roles of

monitors and investors.

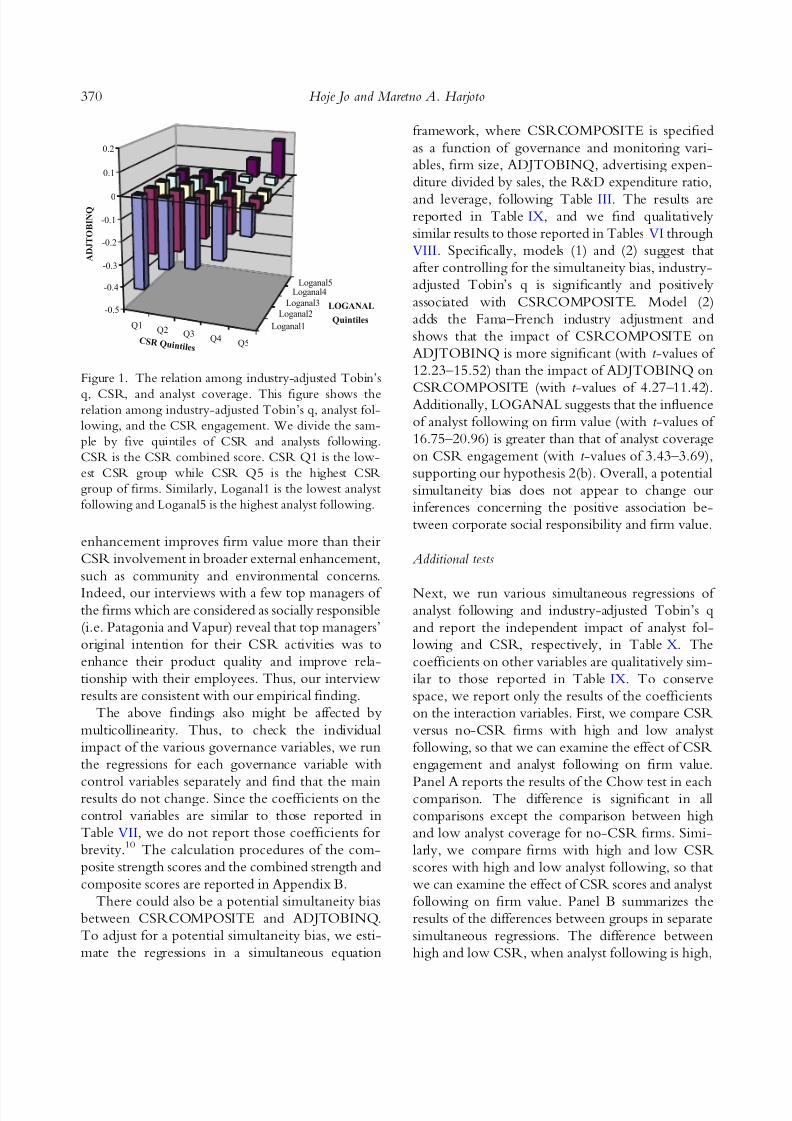

The visual effects of these relations are depicted in

Figure 1 for industry-adjusted Tobin’s q. In gen-

eral, these figures indicate that firms with higher

engagement in CSR activities are more likely to be

followed by security analysts and tend to have a

higher industry-adjusted Tobin’s q, while firms with

a higher analyst following tend to have a higher

industry-adjusted Tobin’s q.

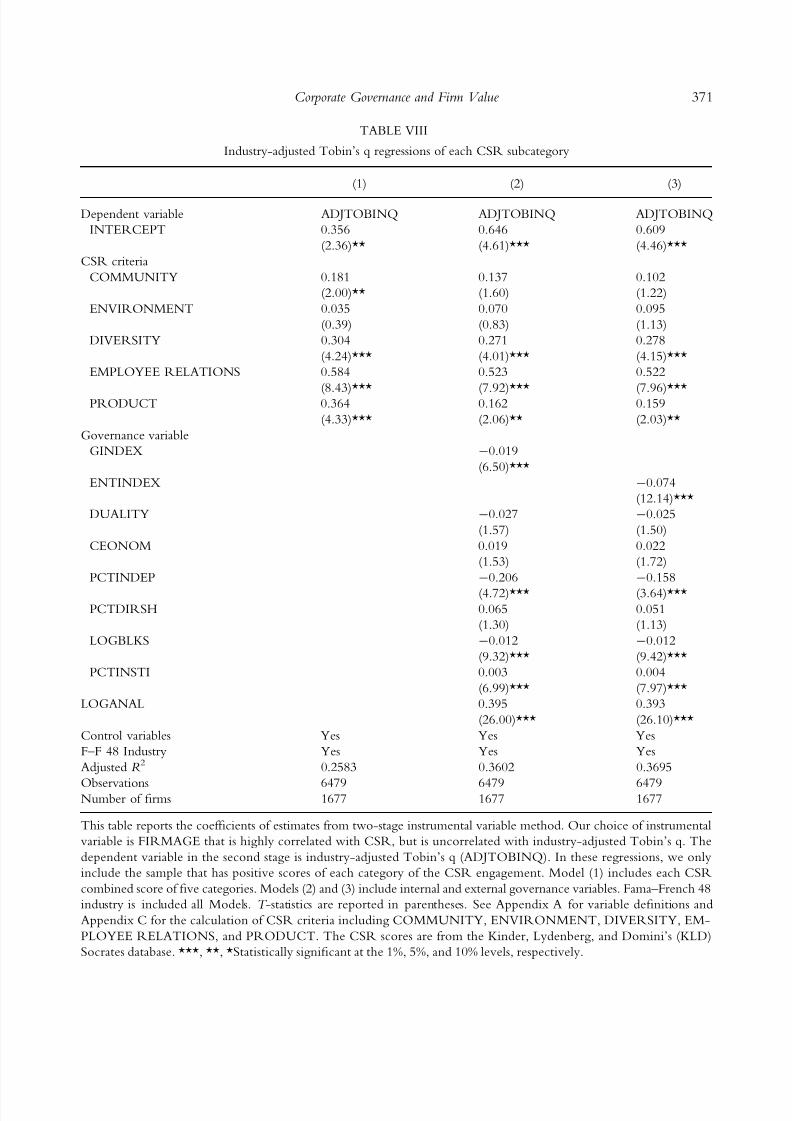

To examine the effects of individual CSR-inclusive criteria on firm value, we report the

coefficients of the estimates from the instrumental

variable method in Table VIII. Our choice of an

instrumental variable is FIRMAGE, which is highly

correlated with CSR, but is uncorrelated with

industry-adjusted Tobin’s q. The dependent variable

in the second stage is industry-adjusted Tobin’s q

(ADJTOBINQ). In these regressions, we include

only the sample that has positive scores for each

category of CSR engagement to focus on the pure

impact of CSR engagement on firm value. Model

(1) includes each CSR combined score for five

inclusive criteria. Models (2) and (3) include the

internal and external governance variables. The

results indicate that while the coefficients on DI-

VERSITY, EMPLOYEE RELATIONS, and

PRODUCT are positive and significant at least at

the five-percent level, the coefficients on COM-

MUNITY and ENVIRONMENT are, in general,

insignificant, suggesting that firms’ CSR engage-

ment directly related to their firms’ internal social

TABLE VI

continued

Heckman two-stage model Model (1) Model (2) Model (3)

Number of firms 2463 2463 2463

This table reports the coefficients of estimates from Heckman two-stage treatment effect models. In the first stage, we run

the probit model with same specification in Table III. We include Lambda (inverse Mills’ ratio) in the second stage with

control variables. The dependent variable in the second stage is industry-adjusted Tobin’s q (ADJTOBINQ). Model (1)

reports the results of control variables. Models (2) and (3) include internal and external corporate governance variables.

Fama–French 48 industry is included all Models. T-statistics are reported in parentheses. See Appendix B for variable

definitions. ***, **, *Statistically significant at the 1%, 5%, and 10% levels, respectively.

368 Hoje Jo and Maretno A. Harjoto

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 19/34

TABLE VII

Industry-adjusted Tobin’s q regressions based on the instrument variables approach

Model (1) Model (2) Model (3) Model (4)

Dependent variable ADJTOBINQ ADJTOBINQ ADJTOBINQ ADJTOBINQ

INTERCEPT 0.119

(3.26)***

0.151

(4.22)***

0.089

(1.94)

0.316

(6.15)***

CSR 0.007

(10.10)***

0.0023

(7.28)***

CSRCOMPOSITE 0.493

(3.32)***

0.564

(3.75)***

Governance variables

GINDEX -0.010

(3.98)***

-0.013

(5.09)***

DUALITY -0.056

(4.14)***

-0.056

(4.16)***CEONOM -0.017

(1.45)

-0.020

(1.74)

PCTDIRSHR 0.075

(2.45)**

0.076

(2.34)**

PCTINDEP -0.099

(2.98)***

-0.130

(3.86)***

PCTINSTI -0.000

(0.24)

0.001

(1.83)

LOGANAL 0.332

(28.29)***

0.318

(27.18)***

Control variables

LOGTA -0.084

(15.88)***

-0.078

(14.19)***

-0.138

(23.40)***

-0.152

(24.08)***DEBTR -0.052

(1.46)

0.028

(0.78)

0.134

(4.07)***

0.200

(5.80)***

RDNR 0.079

(0.94)

0.238

(2.91)***

0.515

(6.40)***

0.500

(6.09)***

CAPXR 0.444

(9.96)***

0.436

(9.77)***

0.111

(2.57)**

0.092

(2.11)**

ADVR 0.631

(2.37)**

0.525

(1.85)

0.352

(1.42)

0.010

(0.04)

SGROWTH 0.373

(9.35)***

0.341

(9.09)***

0.278

(8.61)***

0.282

(8.76)***

Adjusted R 2 0.0440 0.0802 0.1502 0.1597

Observations 11,741 11,741 11,741 11,741

This table reports the coefficients on the estimates from two-stage instrumental variable method. Our choice of instru-

mental variable is FIRMAGE that is highly correlated with CSR, but is uncorrelated with industry-adjusted Tobin’s q.

The dependent variable in the second stage is industry-adjusted Tobin’s q (ADJTOBINQ). Model (1) and (2) include

CSR dummy and CSRCOMPOSITE (CSR combined score) with control variables, respectively. Models (3) and (4)

include internal and external governance variables. The CSR scores are from the Kinder, Lydenberg, and Domini’s (KLD)

Socrates database. T-statistics are reported in parentheses. See Appendix B for variable definitions. ***, **, *Statistically

significant at the 1%, 5%, and 10% levels, respectively.

369Corporate Governance and Firm Value

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 20/34

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 21/34

TABLE VIII

Industry-adjusted Tobin’s q regressions of each CSR subcategory

(1) (2) (3)

Dependent variable ADJTOBINQ ADJTOBINQ ADJTOBINQ

INTERCEPT 0.356

(2.36)**

0.646

(4.61)***

0.609

(4.46)***

CSR criteria

COMMUNITY 0.181

(2.00)**

0.137

(1.60)

0.102

(1.22)

ENVIRONMENT 0.035

(0.39)

0.070

(0.83)

0.095

(1.13)

DIVERSITY 0.304

(4.24)***

0.271

(4.01)***

0.278

(4.15)***

EMPLOYEE RELATIONS 0.584

(8.43)***

0.523

(7.92)***

0.522

(7.96)***PRODUCT 0.364

(4.33)***

0.162

(2.06)**

0.159

(2.03)**

Governance variable

GINDEX -0.019

(6.50)***

ENTINDEX -0.074

(12.14)***

DUALITY -0.027

(1.57)

-0.025

(1.50)

CEONOM 0.019

(1.53)

0.022

(1.72)

PCTINDEP -0.206

(4.72)***

-0.158

(3.64)***PCTDIRSH 0.065

(1.30)

0.051

(1.13)

LOGBLKS -0.012

(9.32)***

-0.012

(9.42)***

PCTINSTI 0.003

(6.99)***

0.004

(7.97)***

LOGANAL 0.395

(26.00)***

0.393

(26.10)***

Control variables Yes Yes Yes

F–F 48 Industry Yes Yes Yes

Adjusted R 2 0.2583 0.3602 0.3695

Observations 6479 6479 6479Number of firms 1677 1677 1677

This table reports the coefficients of estimates from two-stage instrumental variable method. Our choice of instrumental

variable is FIRMAGE that is highly correlated with CSR, but is uncorrelated with industry-adjusted Tobin’s q. The

dependent variable in the second stage is industry-adjusted Tobin’s q (ADJTOBINQ). In these regressions, we only

include the sample that has positive scores of each category of the CSR engagement. Model (1) includes each CSR

combined score of five categories. Models (2) and (3) include internal and external governance variables. Fama–French 48

industry is included all Models. T -statistics are reported in parentheses. See Appendix A for variable definitions and

Appendix C for the calculation of CSR criteria including COMMUNITY, ENVIRONMENT, DIVERSITY, EM-

PLOYEE RELATIONS, and PRODUCT. The CSR scores are from the Kinder, Lydenberg, and Domini’s (KLD)

Socrates database. ***, **, *Statistically significant at the 1%, 5%, and 10% levels, respectively.

371Corporate Governance and Firm Value

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 22/34

TABLE IX

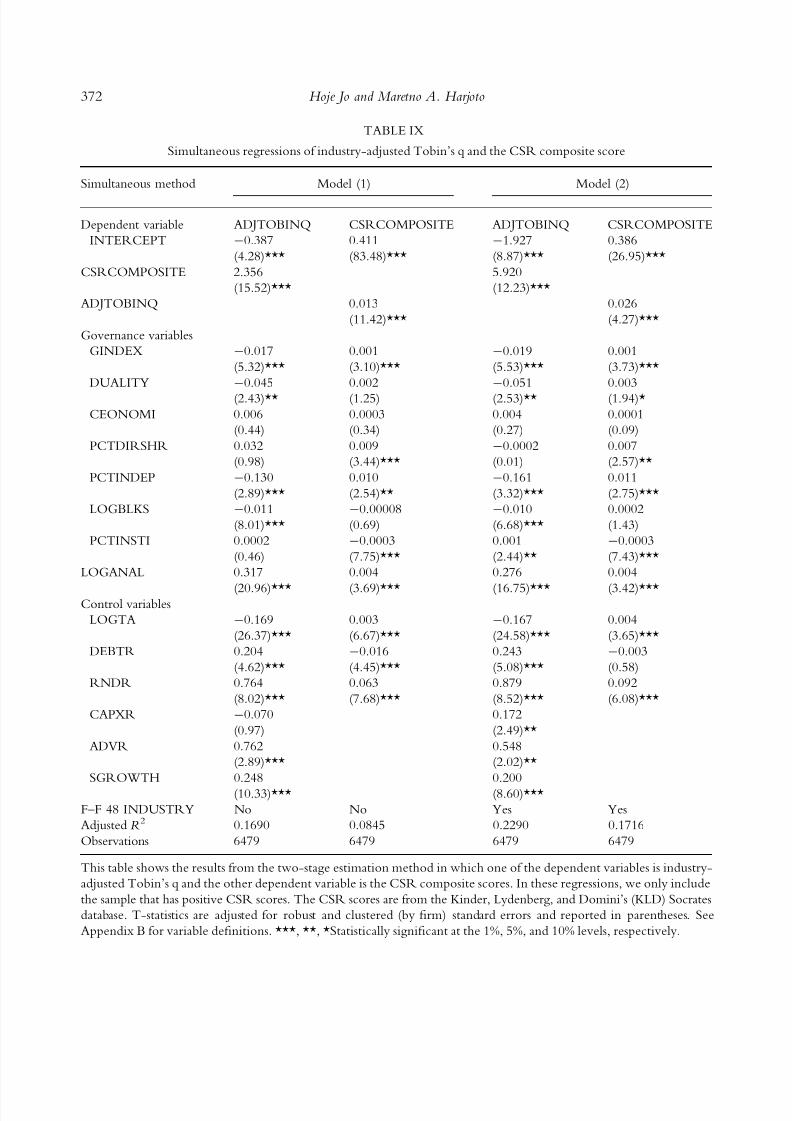

Simultaneous regressions of industry-adjusted Tobin’s q and the CSR composite score

Simultaneous method Model (1) Model (2)

Dependent variable ADJTOBINQ CSRCOMPOSITE ADJTOBINQ CSRCOMPOSITE

INTERCEPT -0.387

(4.28)***

0.411

(83.48)***

-1.927

(8.87)***

0.386

(26.95)***

CSRCOMPOSITE 2.356

(15.52)***

5.920

(12.23)***

ADJTOBINQ 0.013

(11.42)***

0.026

(4.27)***

Governance variables

GINDEX -0.017

(5.32)***

0.001

(3.10)***

-0.019

(5.53)***

0.001

(3.73)***

DUALITY -0.045

(2.43)**

0.002

(1.25)

-0.051

(2.53)**

0.003

(1.94)*

CEONOMI 0.006

(0.44)

0.0003

(0.34)

0.004

(0.27)

0.0001

(0.09)

PCTDIRSHR 0.032

(0.98)

0.009

(3.44)***

-0.0002

(0.01)

0.007

(2.57)**

PCTINDEP -0.130

(2.89)***

0.010

(2.54)**

-0.161

(3.32)***

0.011

(2.75)***

LOGBLKS -0.011

(8.01)***

-0.00008

(0.69)

-0.010

(6.68)***

0.0002

(1.43)

PCTINSTI 0.0002

(0.46)

-0.0003

(7.75)***

0.001

(2.44)**

-0.0003

(7.43)***

LOGANAL 0.317

(20.96)***

0.004

(3.69)***

0.276

(16.75)***

0.004

(3.42)***Control variables

LOGTA -0.169

(26.37)***

0.003

(6.67)***

-0.167

(24.58)***

0.004

(3.65)***

DEBTR 0.204

(4.62)***

-0.016

(4.45)***

0.243

(5.08)***

-0.003

(0.58)

RNDR 0.764

(8.02)***

0.063

(7.68)***

0.879

(8.52)***

0.092

(6.08)***

CAPXR -0.070

(0.97)

0.172

(2.49)**

ADVR 0.762

(2.89)***

0.548

(2.02)**

SGROWTH 0.248

(10.33)***

0.200

(8.60)***

F–F 48 INDUSTRY No No Yes Yes

Adjusted R 2 0.1690 0.0845 0.2290 0.1716

Observations 6479 6479 6479 6479

This table shows the results from the two-stage estimation method in which one of the dependent variables is industry-

adjusted Tobin’s q and the other dependent variable is the CSR composite scores. In these regressions, we only include

the sample that has positive CSR scores. The CSR scores are from the Kinder, Lydenberg, and Domini’s (KLD) Socrates

database. T-statistics are adjusted for robust and clustered (by firm) standard errors and reported in parentheses. See

Appendix B for variable definitions. ***, **, *Statistically significant at the 1%, 5%, and 10% levels, respectively.

372 Hoje Jo and Maretno A. Harjoto

8/12/2019 Csr and Corporate Governace

http://slidepdf.com/reader/full/csr-and-corporate-governace 23/34

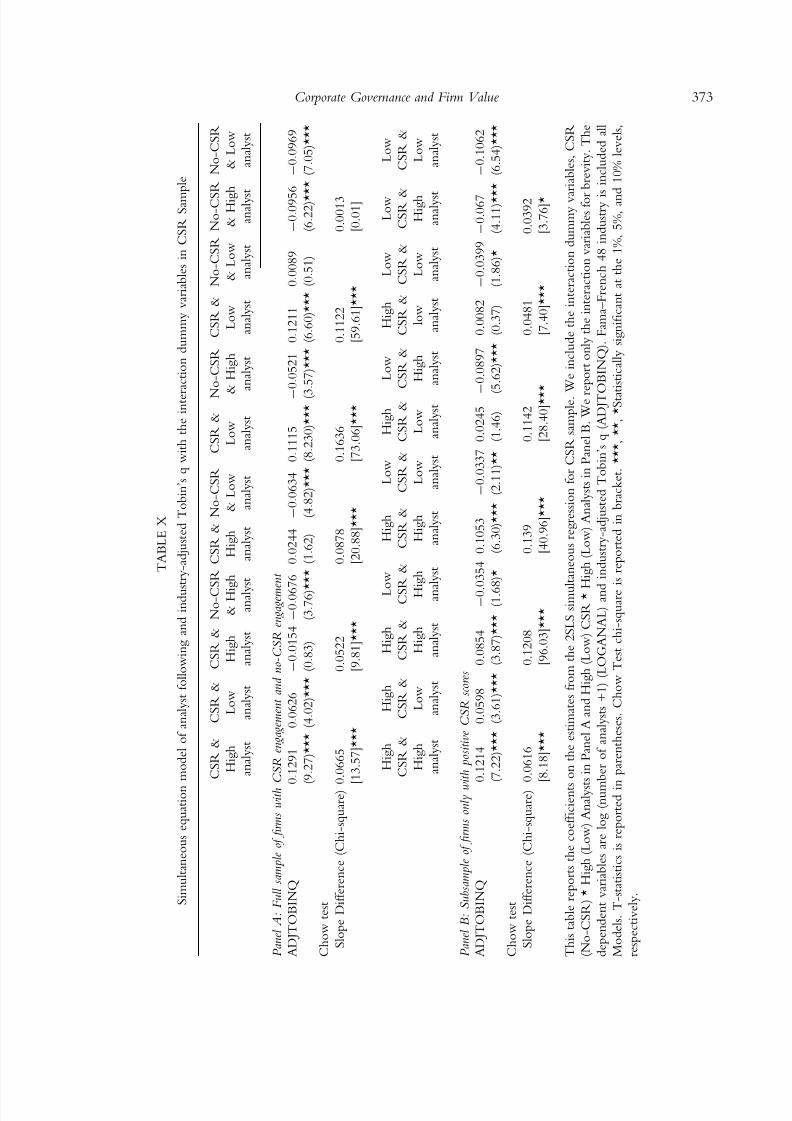

T A B L E X

S i m u l t a n e o u s e q u a t i o n m o d e l o f a n a l y s t f o l l o w i n g a n d i n d u s t r y - a d j u s t e d T o b i n ’ s q w i t h t h e i n t e r a c t i o n d u m m y v a r i a b l e s i n C S R S a m p l e

C S R &

H i g h

a n a l y s t

C S R &

L o w

a n a l y s t

C S R &

H i g h

a n a l y s t

N o - C S R

& H i g h

a n a l y s t

C S R &

H i g h

a n a l y s t

N o - C S R

& L o w

a n a l y s t

C S R &

L o w

a n a l y s t

N

o - C S R

&

H i g h

a n a l y s t

C S R &

L o w

a n a l y s t

N o - C S R

& L o w

a n a l y s t

N o - C S R

& H i g h

a n a l y s t

N o - C S R

& L o w

a n a l y s t

P a n e l A : F u l l s a m p l e o f fi r m s w i t h C

S R e n g a g e m e n t a n d n o - C S R e n g a g e m e

n t

A D J T O B I N Q

0 . 1 2 9 1

( 9 . 2 7 ) * * *

0 . 0 6 2 6

( 4 . 0 2 ) * * *

- 0 . 0 1 5 4

( 0 . 8 3 )

- 0 . 0 6 7 6

( 3 . 7 6 ) *

* * 0 . 0 2 4 4

( 1 . 6 2 )

- 0 . 0 6 3 4

( 4 . 8 2 ) * * *

0 . 1 1 1 5

( 8 . 2 3 0 ) * * *

-

0 . 0 5 2 1

( 3 . 5 7 ) * * *

0 . 1 2 1 1