Languages

Pages

Legal

CONFIDENTIAL

BPI Investor UpdateStrength and Quality in Earnings

As of September 30, 2017

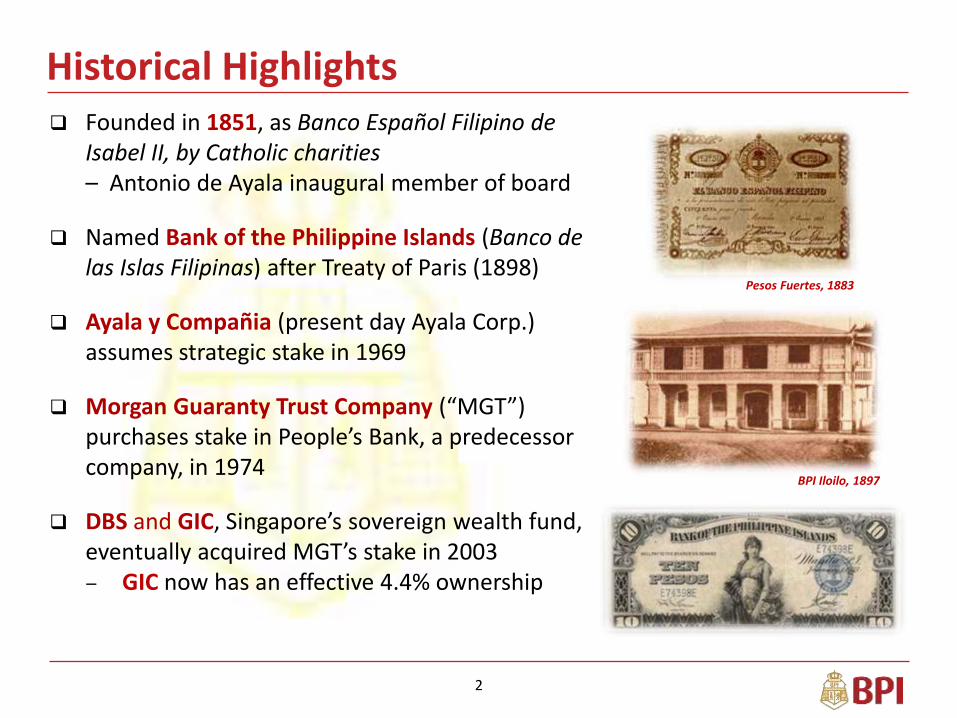

Founded in 1851, as Banco Español Filipino de Isabel II, by Catholic charities– Antonio de Ayala inaugural member of board

Named Bank of the Philippine Islands (Banco de las Islas Filipinas) after Treaty of Paris (1898)

Ayala y Compañia (present day Ayala Corp.) assumes strategic stake in 1969

Morgan Guaranty Trust Company (“MGT”)purchases stake in People’s Bank, a predecessor company, in 1974

DBS and GIC, Singapore’s sovereign wealth fund, eventually acquired MGT’s stake in 2003– GIC now has an effective 4.4% ownership

Historical Highlights

Pesos Fuertes, 1883

BPI Iloilo, 1897

2

GIC, 4.4%

RCAM*, 8.3%

Ayala Corp,48.2%

Public Float,39.1%

Shareholders & Equity Profile

Fundamentals Description

PCOMP Index 4.97% weight

Stock Price P103.90 per share

BV per share P45.45

P-B Ratio 2.29x

P-E Ratio 17.55x

Dividends P1.80 per share

Issued Shares 3.939 bn

Market Cap P409.304 bn

Shareholders As of November 24, 2017

* Roman Catholic Archdiocese of Manila

3

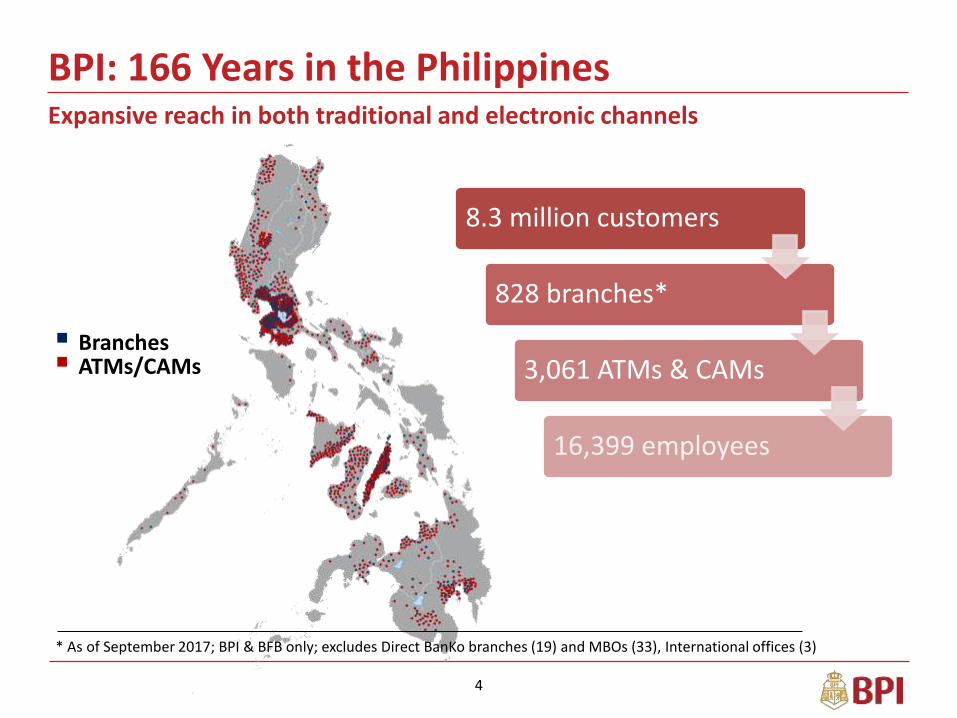

BPI: 166 Years in the Philippines

Branches ATMs/CAMs

Expansive reach in both traditional and electronic channels

8.3 million customers

828 branches*

3,061 ATMs & CAMs

16,399 employees

4

* As of September 2017; BPI & BFB only; excludes Direct BanKo branches (19) and MBOs (33), International offices (3)

Electronic ChannelsSignificant leadership in technology-based banking

5

+14.2%

+23.3%

-0.5%

-

Express Mobile

Express Phone -3.5%

No. of Clients Sep 2015 Sep 2016 Sep 2017

Express Online 2,178,921 2,513,293 2,870,517

Express Mobile 1,547,201 1,951,842 2,405,698

Express Phone 821,966 799,919 771,887

ExpressLink 25,289 29,138 29,002

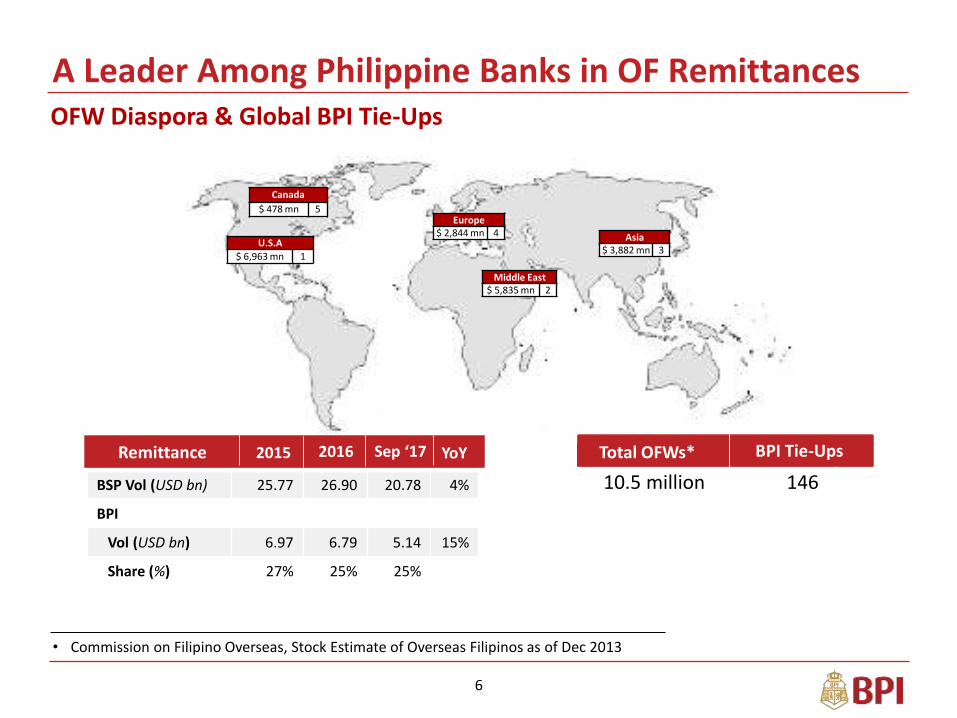

• Commission on Filipino Overseas, Stock Estimate of Overseas Filipinos as of Dec 2013

ITSC Meeting

A Leader Among Philippine Banks in OF Remittances

BSP Vol (USD bn) 25.77 26.90 20.78 4%

BPI

Vol (USD bn) 6.97 6.79 5.14 15%

Share (%) 27% 25% 25%

Total OFWs* BPI Tie-Ups10.5 million 146

OFW Diaspora & Global BPI Tie-Ups

Canada

$ 478 mn 5Europe

$ 2,844 mn 4 Asia$ 3,882 mn 3

Middle East$ 5,835 mn 2

U.S.A

$ 6,963 mn 1

Remittance 2015 2016 Sep ‘17 YoY Total OFWs* BPI Tie-Ups

6

Excellence in Debt Capital Markets

7

Underwriter Mkt Share (%) Issues

China Banking Corp 1 16.4 12

BDO Capital Investment 2

BPI Capital Corporation 3

ING Group 4

5Unicapital Inc.

Standard Chartered 6

7Security Bank Corp

16.2

13.2

12.2

7.1

6.8

6.4

10

8

6

5

6

9

Sept 2017 Rank

Dec 2016

Feb 2017

Jun 2017

Sep 2017

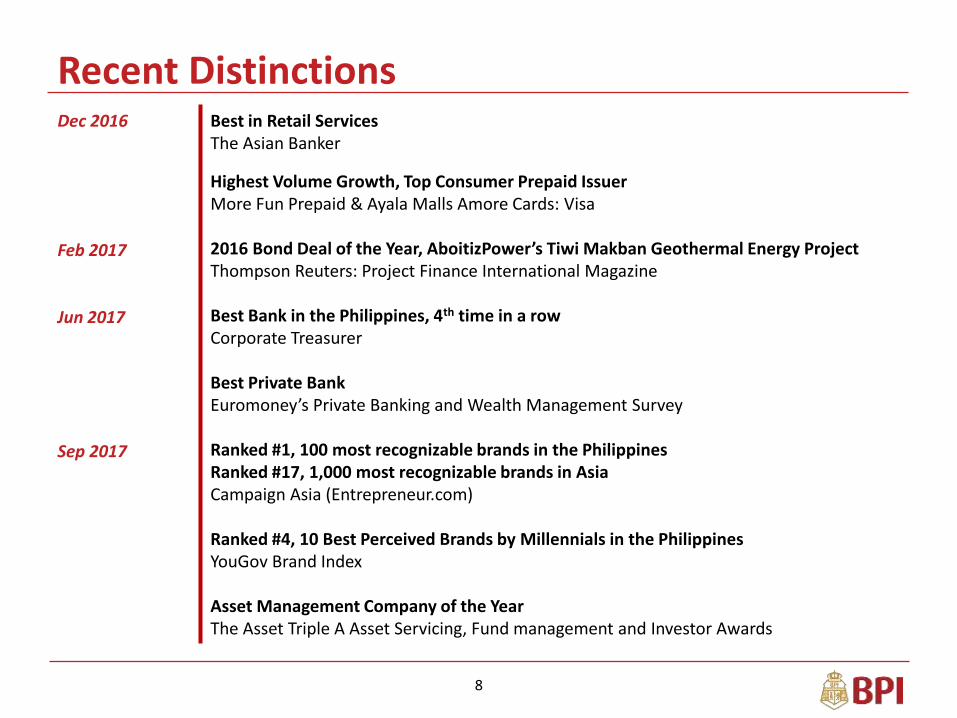

Best in Retail ServicesThe Asian Banker

Highest Volume Growth, Top Consumer Prepaid IssuerMore Fun Prepaid & Ayala Malls Amore Cards: Visa

2016 Bond Deal of the Year, AboitizPower’s Tiwi Makban Geothermal Energy ProjectThompson Reuters: Project Finance International Magazine

Best Bank in the Philippines, 4th time in a rowCorporate Treasurer

Best Private BankEuromoney’s Private Banking and Wealth Management Survey

Ranked #1, 100 most recognizable brands in the PhilippinesRanked #17, 1,000 most recognizable brands in AsiaCampaign Asia (Entrepreneur.com)

Ranked #4, 10 Best Perceived Brands by Millennials in the PhilippinesYouGov Brand Index

Asset Management Company of the YearThe Asset Triple A Asset Servicing, Fund management and Investor Awards

Recent Distinctions

8

BPI Management Team

Picture

Cezar P. ConsingPresident & CEO

RetailClients

EnterpriseServices

Financial Products &

Services

Corporate Clients

Global Markets

JosephGotuaco

NatividadAlejo

Daniel Montecillo

SimonPaterno

AntonioPaner

Ramon Jocson

Theresa Javier

Edgardo Madrilejo

EVP EVP EVP EVPEVP &

Treasurer EVP SVP & CFO SVP & CRO

Strategy &Dev’t

Risk Mgmt

9

Microfinance

Sept 2017 Performance HighlightsSustained growth in assets

in P Bn 2016 2017 YoY (ppt)

Balance Sheet

Assets 1,590.0 1,799.8 13.2%

Net Loans 931.1 1,122.2 20.5%

Deposits 1,320.2 1,504.9 14.0%

CASA 992.9 1,073.2 8.1%

Capital 165.6 179.0 8.1%

Income Statement

Net Revenues 50.4 53.0 5.2%

Net Int Income 31.3 35.5 13.5%

Non-Int Income 19.1 17.5 -8.4%

Opex 25.6 27.9 8.9%

Provisions 4.0 3.6 -8.7%

Net Income 17.4 17.0 -1.9%

Comp Income 18.7 17.3 -7.5%

10

Sept 2017 Performance HighlightsAdequate capital, and strong asset quality

2016 2017 YoY (ppt)

Balance Sheet

LDR 71% 75% 4.0%

CASA Ratio 75% 71% -3.9%

Profitability

CIR 51% 53% 1.8%

ROE 14.7% 13.1% -1.6%

ROA 1.5% 1.3% -0.2%

Asset Quality

Gross 90-Day NPL 1.64% 1.47% -0.2%

NPL Cover 112% 126% 13.8%

Capital

CAR 14.2% 13.4% -0.8%

CET1 13.3% 12.5% -0.8%

11

18.7 17.3

Sep 2016 Sep 2017

17.4 17.0

Sep 2016 Sep 2017

Strong Earnings QualityNet Income slightly down YoY; Excluding one-off gains, up 33%

12

Net IncomeP bn

Comprehensive IncomeP bn

-1.9%

YoY Growth

-7.5%

YoY Growth

31.3 35.5

19.1 17.5

50.4 53.0

Sep 2016 Sep 2017

Revenue Growth Remains PositiveCore intermediation business continued to be strong driver of revenues

13

RevenuesP bn

Revenue Mix

Net Interest Income Non-Interest Income

13.5%

-8.4%

YoY Growth

5.2%

62.0% 66.9%

38.0% 33.1%

Sep 2016 Sep 2017

12.615.1

6.6 2.4

19.117.5

Sep 2016 Sep 2017

Non-Interest Income

14

Securities & FX trading decrease P4.13 bn (-63.1) vs last year

Fees & other income up by P2.5 bn (20.1%) vs last yeardriven by:– Credit card income– Bank Commissions– Corporate Finance – Asset Sales

Breakdown of Non-Interest IncomeP bn

-27.84%

12.1%

20.1%

-63.1%

YoY Growth

-8.4%

66% 86%

34% 14%

Fees & Others

Sec & FX

Slowdown in securities trading shrunk non-interest income in Sept 2017

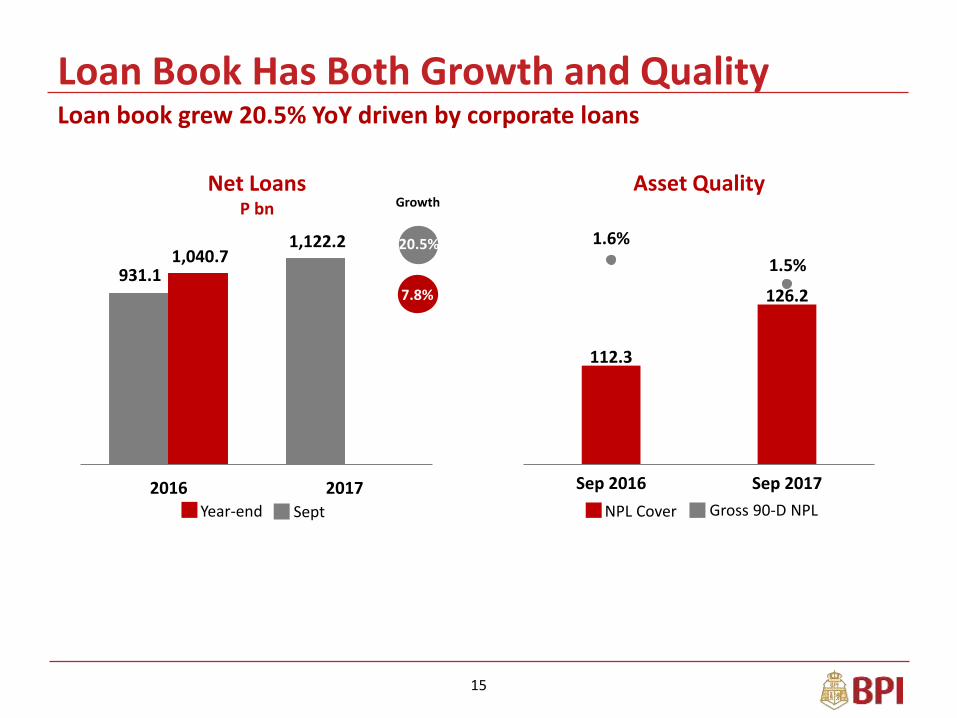

931.1

1,122.2 1,040.7

2016 2017

Loan Book Has Both Growth and Quality

15

Net LoansP bn

Asset Quality

NPL Cover Gross 90-D NPL

7.8%

Growth

20.5%

Year-end Sept

Loan book grew 20.5% YoY driven by corporate loans

112.3

126.2

1.6%

1.5%

Sep 2016 Sep 2017

112.9 117.1

53.3 57.1

40.348.8

Sep 2016 Sep 2017

656.8

834.6

82.2

81.1

Sep 2016 Sep 2017

YoY Growth

Sustained Growth in Loan Segments

Corporate Loan BalancesP bn

Retail Loan BalancesP bn

89% 91%Corp&MM%

11% 9%SME%

55% 52%Housing%

26% 26%Auto%

19% 22%Cards%

23.9%

-1.3%

27.1%

739.0

915.7

206.5222.9

1 Cards inclusive of Personal Loans.

3.7%

7.0%

21.0%

7.9%

YoY Growth

Going beyond marginal bookings

16

75.2%

71.3%70.5%

74.6%

Sep 2016 Sep 2017

1,320.2 1,504.9

992.9 1,073.2

Sep 2016 Sep 2017

Deposit and CASA Growth Remains StrongEfficiency continues to improve with LDR ratio

DepositsP bn

CASA Ratio, LDR

14.0%

8.1%

YoY Growth

Total Deposits CASA Deposits CASA Ratio LDR

17

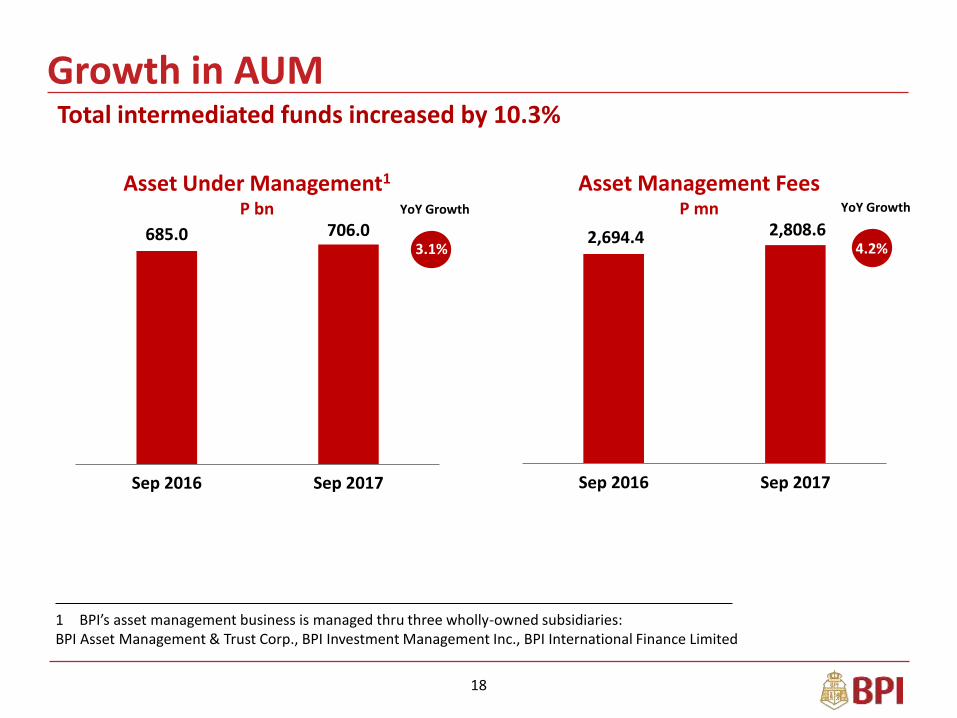

2,694.4 2,808.6

Sep 2016 Sep 2017

685.0 706.0

Sep 2016 Sep 2017

Growth in AUM

18

Asset Under Management1

P bn

Asset Management FeesP mnYoY Growth

3.1%

-15.8%

YoY Growth

4.2%

Total intermediated funds increased by 10.3%

1 BPI’s asset management business is managed thru three wholly-owned subsidiaries:BPI Asset Management & Trust Corp., BPI Investment Management Inc., BPI International Finance Limited

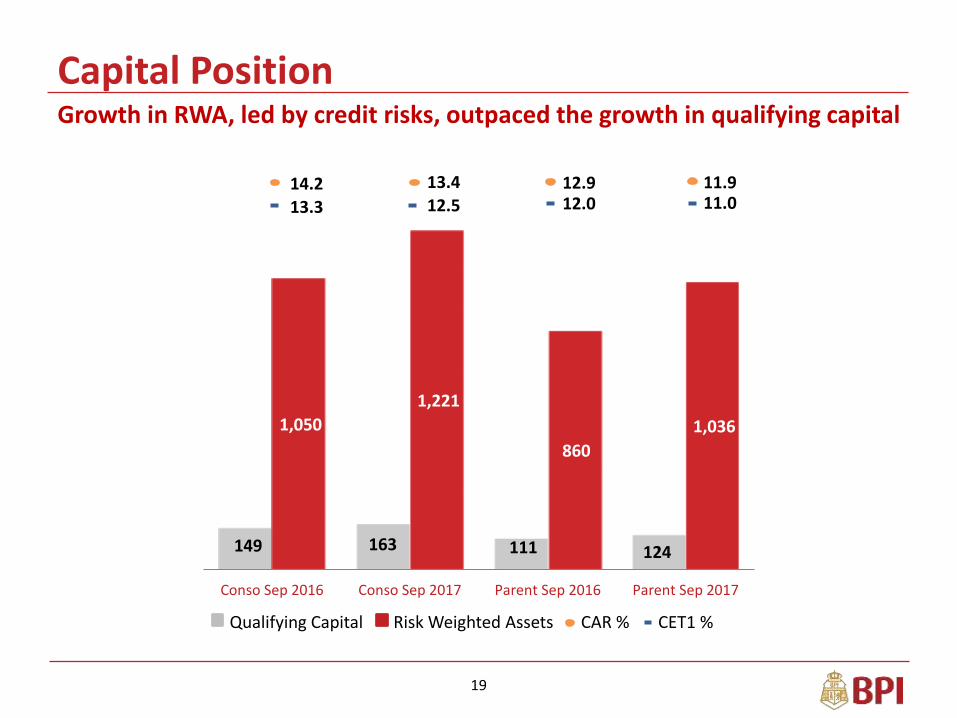

149 163 111 124

1,050

1,221

860

1,036

Conso Sep 2016 Conso Sep 2017 Parent Sep 2016 Parent Sep 2017

Capital Position

19

13.314.2 13.4

12.512.912.0

11.911.0

CAR % CET1 %Qualifying Capital Risk Weighted Assets

Growth in RWA, led by credit risks, outpaced the growth in qualifying capital

Credit RatingsMoody’s1 Fitch Ratings2 Capital

Intelligence3

Bank Financial Strength Rating

- - BBB

LT Local Currency Rating

- BBB- -

LT Foreign Currency Rating

Baa2/Prime-2 BBB- BBB

Outlook Stable Stable Stable

LT Foreign -Philippines

- BBB- -

/1 As of Sept 2017; /2 As of February 2017; /3 As of October 2017

22

CONFIDENTIAL

Thank you.

As of September 30, 2017

BPI Investor UpdateStrength and Quality in Earnings

Top Related