Languages

Pages

Legal

BE GROUPINTERIM REPORTJANUARY – JUNE 2011

Roger Johansson, President & CEO

Slide 1

Torbjörn Clementz, CFO & Executive Vice President

Q2 – A quarter with continued growth

Financial HighlightsN t l i f 14%Net sales increase of 14%

Delivered tonnage increase of 7%

Operating result of 66 MSEK with an operating margin of 4.2%

Slide 2

Q2 – Good sales despite weakened steel market

Operational highlightsContinued phasing in of operational investments

Market highlightsOverall good demand on our productsSt ti it i i i t investments

Started transformation of Polish business with a unit for production service

Strong activity in engineering sectorImproved activity in construction sectorIncreased sales prices in all three

serviceHigh focus on inventory management to be well balanced for Q3S

business areasThe bullish price development from steel producers in Q1 turned to decline

Several internal initiatives launched to improve gross margin

Slide 3

FINANCIALS IN DETAIL

Slide 4

Continued growth in sold tonnage

125

150

500

600 Increased tonnage despite weak start of the quarter

Tonnage (‘000 tons)

75

100

125

300

400

500 q

Sold tonnage 7% higher than Q2 2010

25

50

75

100

200

300

In total tons best quarter since Q2 2008

0

25

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q40

100

2009 2010 2011

Slide 5

Quarterly Rolling 12 months

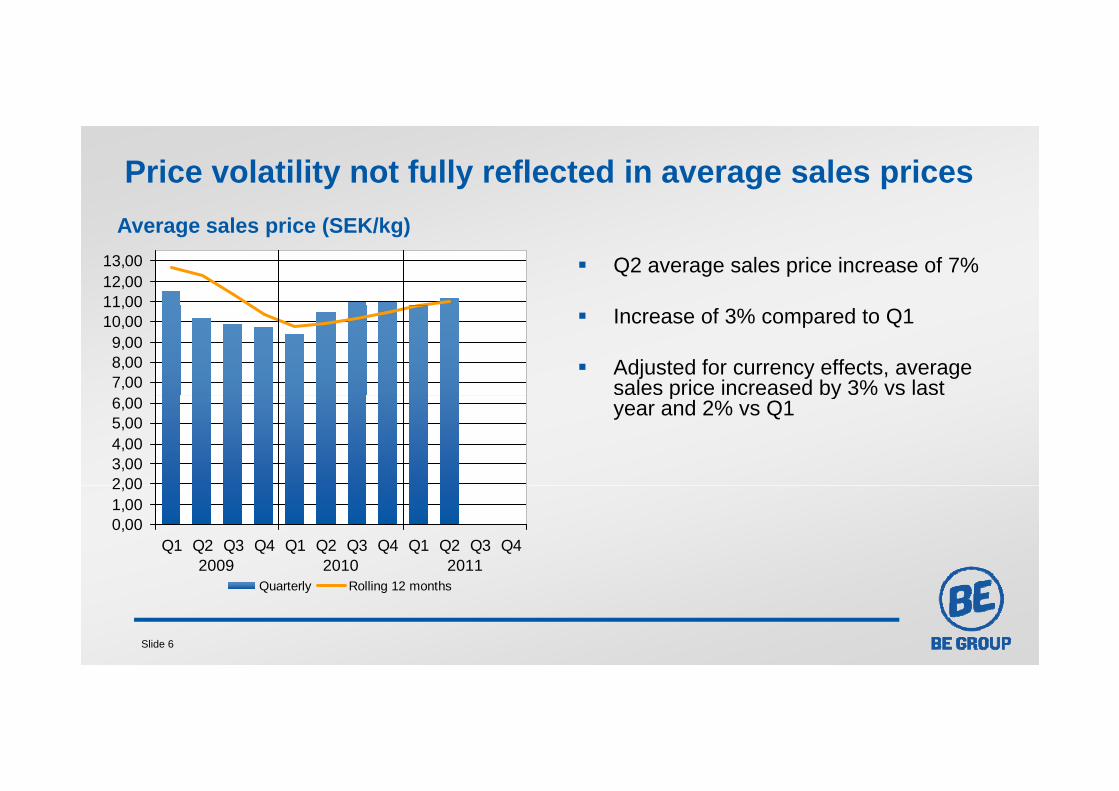

Price volatility not fully reflected in average sales prices

11,0012,0013,00 Q2 average sales price increase of 7%

Average sales price (SEK/kg)

7,008,009,00

10,0011,00

Increase of 3% compared to Q1

Adjusted for currency effects, average sales price increased by 3% vs last

2 003,004,005,006,00

p yyear and 2% vs Q1

0,001,002,00

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42009 2010 2011

Slide 6

Quarterly Rolling 12 months

Q2 Q2 Ch Q1

Q2: Higher sales with result not on par with last yearQ2 Q2 Change Q1

SEK M 2011 2010 2011

Net sales 1,597 1,399 +198 1,519

Underl ing EBIT 43 46 3 47Underlying EBIT 43 46 -3 47% of Sales 2.7% 3.3% -0.6% 3.1%

Inventory gain/loss 23 40 -17 2

EBIT 66 86 -20 45EBIT 66 86 20 45% of Sales 4.2% 6.2% -2.0% 2.9%

Earnings before tax 57 59 -2 36

Net earnings 44 46 -2 23

EPS (SEK) 0.89 0.92 -0.03 0.46

Cash-flow before change in net debt -52 -30 -22 63

Net debt 851 832 +19 783

Slide 7

e deb 85 83 9 83

Net debt / Equity 98% 104% -6% 96%

EBIT improved vs latest quarter

1 3831 519

1 597

1 3991 400

1 600

140

160EBIT of 66 MSEK below last year due to lower inventory gains

Underlying gross margin pressure by

Sales, EBIT and uEBIT (SEK M)Sales EBIT

1 2731 3831 399

66

86

800

1 000

1 200

80

100

120Underlying gross margin pressure by production ramp-up

Leverage from acquisitions not fully achieved

43474632 7

4548

200

400

600

20

40

60Inventory gains of 23 MSEK (40)

EBIT margin of 4.2% (6.2)

-8-200

0

Q2 10 Q3 10 Q4 10 Q1 11 Q2 11-20

0

S S S

Slide 8

Net sales, SEK M Underlying EBIT, SEK M EBIT, SEK M

Well managed working capital supports cash-flow

11,710,4

800Working capital increase due to higher business volume

Working capital (SEK M)

9,28,2 8,2

400

600 Tight working capital management contributes to positive YTD cash-flow

Cash-flow from investment activities 37 MSEK ( 10) d i th t

200

-37 MSEK (-10) during the quarter

Net debt of 851 MSEK (832)

Unused credit facilities and available557 632 519 478 569

0Q2 10 Q3 10 Q4 10 Q1 11 Q2 11

Period end working capital, SEK M

Unused credit facilities and available cash of 435 MSEK

Gearing of 98% (104)

Slide 9

Period end working capital, SEK MWorking capital tied up, %

H1 H1 Ch

H1: All in all an improvement vs last year H1 H1 Change

SEK M 2011 2010

Net sales 3,116 2,473 +643

Underl ing EBIT 90 36 +54Underlying EBIT 90 36 +54% of Sales 2.9% 1.4% +1.5%

Inventory gain/loss 25 22 +3

EBIT 111 58 +53EBIT 111 58 +53% of Sales 3.6% 2.3% +1.3%

Earnings before tax 93 27 +66

Net earnings 67 21 +46

EPS (SEK) 1.35 0.42 +0.93

Cash-flow before change in net debt 11 -90 +101

Net debt 851 832 +19

Slide 10

e deb 85 83 9

Net debt / Equity 98% 104% -6%

BUSINESS AREASSTATUS Q2 2011

Slide 11

BA Sweden – Improvement in demand

800 80 Strengthened demand during the quarter after weak start

Sales, EBIT and uEBIT (SEK M)Sales EBIT

573

668740 748

673

40500

600

700

50

60

70Improvement from customers in both engineering and construction sector

Net sales increase with 11%

2116

3240

28

200

300

400

20

30

40Net sales increase with 11%

Operating margin improvement vs Q1

Integration of Lecor Stålteknik and RTS 2423

18 1711

0

100

200

Q2 10 Q3 10 Q4 10 Q1 11 Q2 110

10

20 gProduktion ongoing

Ongoing investment in new production facility for Lecor Stålteknik

Slide 12

Q2 10 Q3 10 Q4 10 Q1 11 Q2 11

Net sales, SEK M Underlying EBIT, SEK M EBIT, SEK M

BA Finland – Good margins despite production capacity ramp-upp y p p

600 60Stable demand with certain weakening at the end of period

Sales, EBIT and uEBIT (SEK M)Sales EBIT

474 479

546574

507

4433

48400

500

40

50 Net sales increase of 13% with a tonnage increase of 7%

Operating margin of 7 7%

293333

2115

29

200

300

20

30Operating margin of 7.7%

Increased production capacity yet to have an impact on sales

70

100

Q2 10 Q3 10 Q4 10 Q1 11 Q2 110

10 Decision on extension of production facility in Lapua. Investment of 20 MSEK

Slide 13

Q2 10 Q3 10 Q4 10 Q1 11 Q2 11

Net sales, SEK M Underlying EBIT, SEK M EBIT, SEK M

BA CEE – Transformation in Poland started

400 40 Continued increase in demand from

Sales, EBIT and uEBIT (SEK M)Sales EBIT

265 258 264307

254200

300

20

30engineering sector with certain weakening at the end of the quarter

Increase in net sales of 21% due to increase in shipped tonnage

110

0 13

8

20

100

0

10increase in shipped tonnage

EBIT weakened to 1 MSEK (8) due to declining price trend

-14-2

-16-200

-100

Q2 10 Q3 10 Q4 10 Q1 11 Q2 11-20

-10 Investment of 15 MSEK in new production service center in Trebaczew started

Slide 14

Q2 10 Q3 10 Q4 10 Q1 11 Q2 11

Net sales, SEK M Underlying EBIT, SEK M EBIT, SEK M

OUTLOOK

Slide 15

BE Group outlook

Signs of continued increase in demand during H2/11 based on customer forecasts

Pricing development to customers will vary depending on product

B i k t tl t bl ith j tBuying market currently stable with no major movements

Continued focus on improving margins and building the best modus operandi in the sectorin the sector

Slide 16

Business ambitions for the next few years

Profitable growth

Sustainable profitability in CEE

Service sales 50% of total sales

Follow customers internationally

Create leverage within the Groupg p

Slide 17

Slide 18

APPENDIXFINANCIAL INFORMATION

Slide 19

Appendix: Financial summary2010 2011 Full year2010 2011 Full year

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2010 R12

Tonnage 114 133 116 126 140 143 489 525

Net Sales 1,074 1,399 1,273 1,383 1,519 1,597 5,129 5,772Net Sales 1,074 1,399 1,273 1,383 1,519 1,597 5,129 5,772

Underlying EBIT -10 46 32 7 47 43 75 129% of Sales -0.9% 3.3% 2.5% 0.5% 3.1% 2.7% 1.5% 2.2%

EBIT -28 86 48 -8 45 66 98 151% of Sales -2.6% 6.2% 3.8% -0.6% 2.9% 4.2% 1.9% 2.6%

Net earnings -25 46 26 -18 23 44 29 75

Earnings/share1 -0.50 0.92 0.52 -0.37 0.46 0.89 0.58 1.51

Cash flow2 -60 -30 -51 30 63 -52 -110 -9

Working Capital3 473 557 632 519 478 569 519 569

Underlying EBITA(%) -0.8 3.4 2.9 0.8 3.3 3.1 1.7 2.6

Slide 20

Underlying ROOC(%) -3.8 21.3 15.8 5.0 24.2 22.7 9.8 16.51 Earnings per share after dilution 3 Period end working capital2 Cash flow before change in Net Debt

Appendix: Sales per customer segment

5253

OEM &partners

January-June Q2

5253

OEM &partners

23

53

22Project 23

53

23Project

1716

Pre-processing 16

15

Pre-processing

89

0% 10% 20% 30% 40% 50% 60%

Retail 99

0% 10% 20% 30% 40% 50% 60%

Retail

Slide 21

0% 10% 20% 30% 40% 50% 60%

2011

0% 10% 20% 30% 40% 50% 60%

2010 2011 2010

Appendix: Sales per product area

450399+13Long

steel

January-June Q2

879716

Longsteel +23

575

134

489

130

+18

+3Reinforce-ment

Flatsteel

1 122

245

879

201Reinforce-

ment

Flatsteel +28

+22

271

86

130

245 +10

ment

Stainlesssteel

Al i

541

171

201

446

ment

Stainlesssteel

Al i

+21

8691

8145

-6Aluminum

Other

171167

15864

Aluminum

Other

+2

Slide 22

0% 5% 10% 15% 20% 25% 30% 35% 40%

2011 2010 Change %

0% 5% 10% 15% 20% 25% 30% 35% 40%

2011 2010 Change %

Appendix: Sales per channel

555

January-June Q2

283555

1 612

504Direct +10

283

830

286Direct -1

1 612

1 296Inventory

+24830

729

Inventory+14

904

643

0% 10% 20% 30% 40% 50%

Service+41

458

362

0% 10% 20% 30% 40% 50%

Service+27

Slide 23

2011 2010 Change %2011 2010 Change %

Sales outside scope of channels not included Sales outside scope of channels not included

Top Related