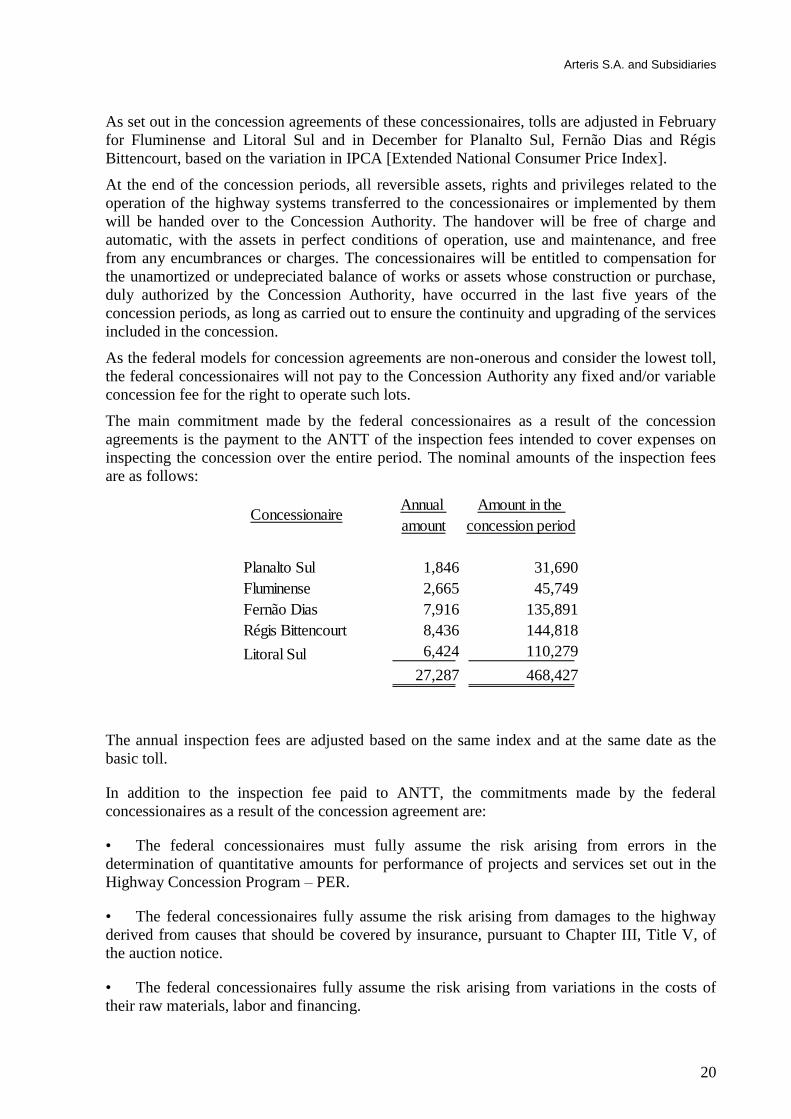

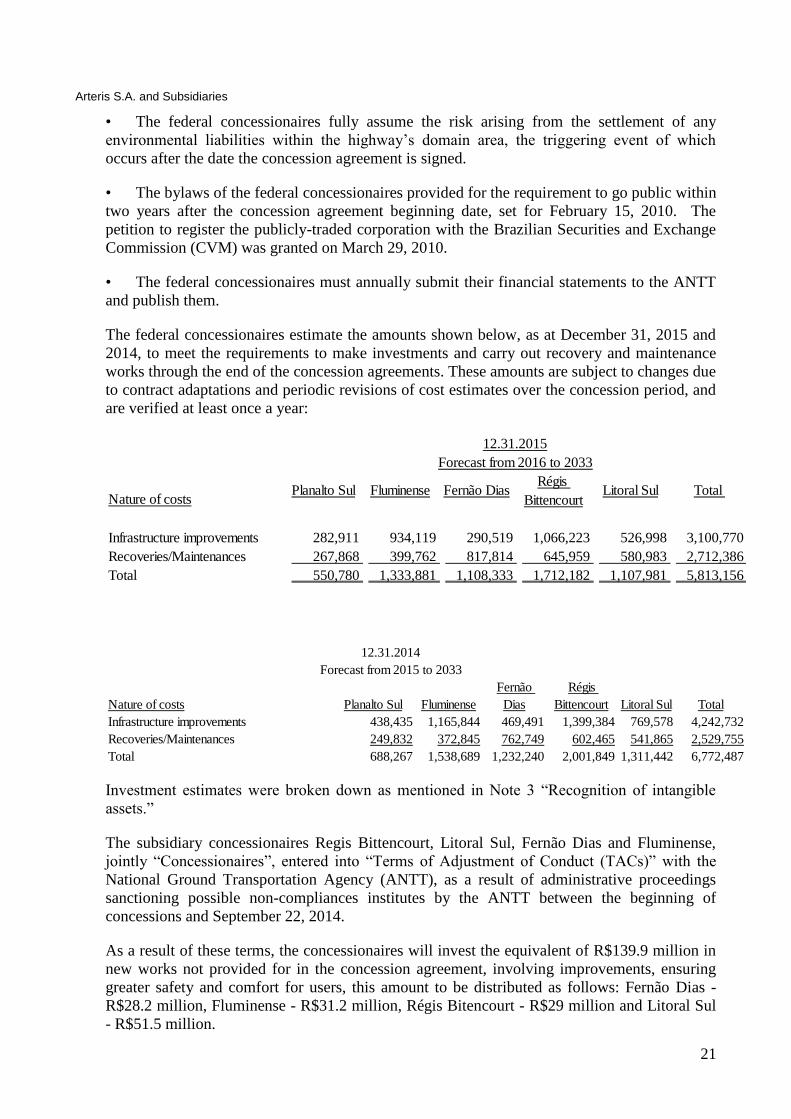

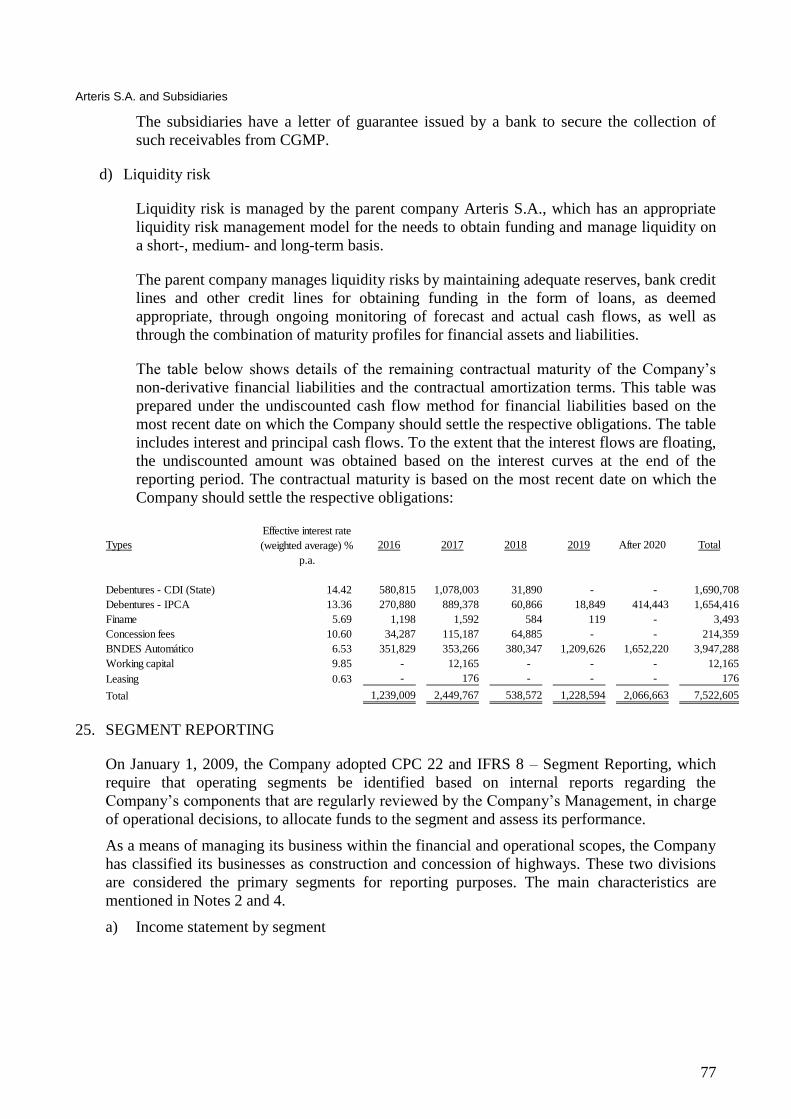

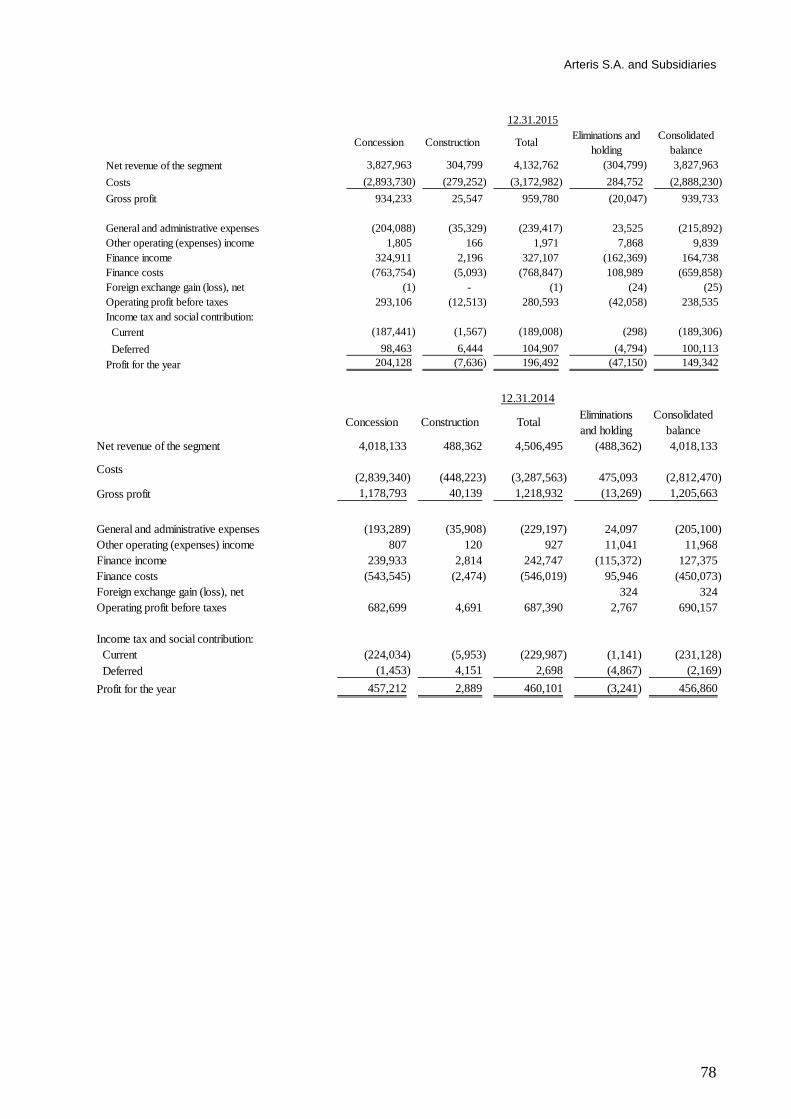

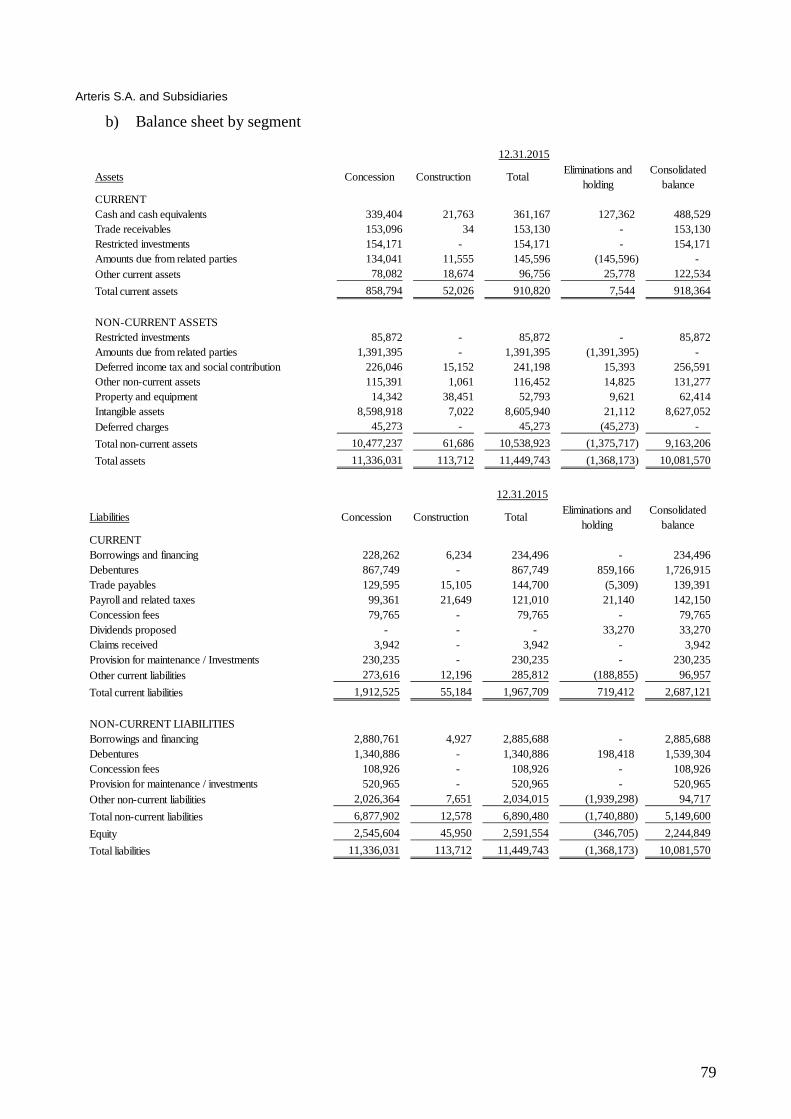

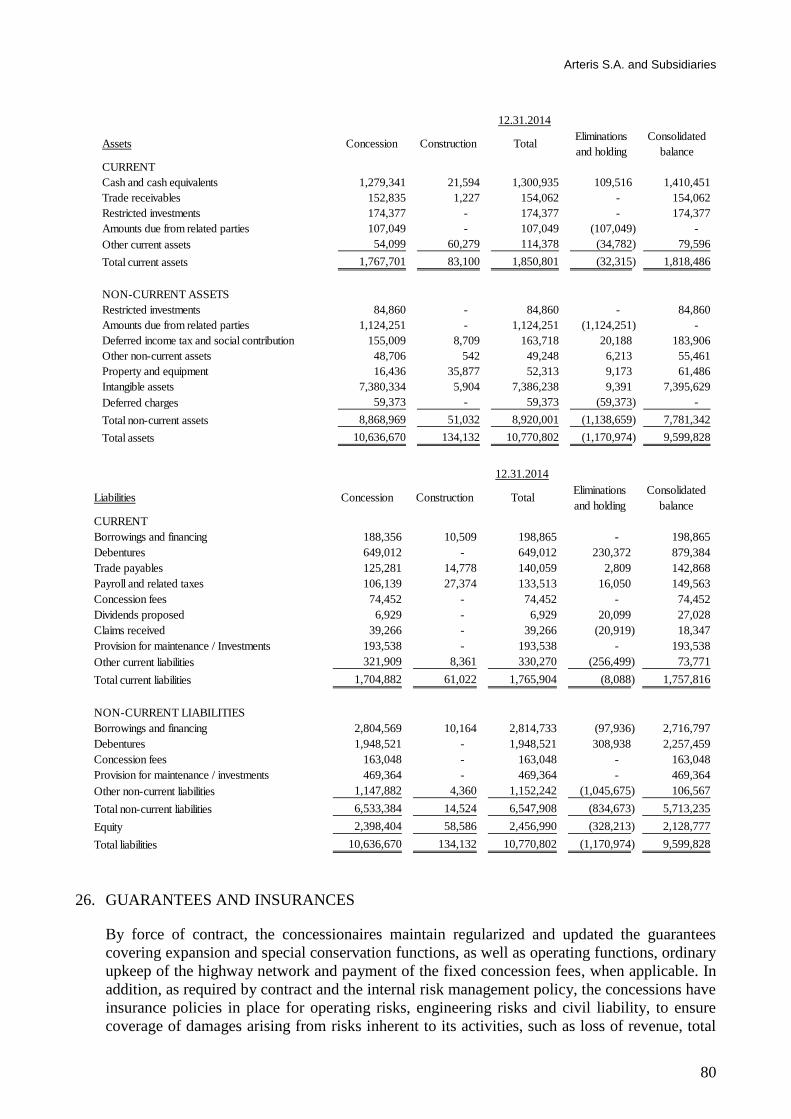

Languages

Pages

Legal

Divulgação de Resultados 2010

25 de março de 2011 Pág. 1 de 1

E-

Complete Annual Financial Statements

Management Report and Statements - Article 25 (ICVM 480)

Independent Auditor’s Report

Financial Statements for the years ended

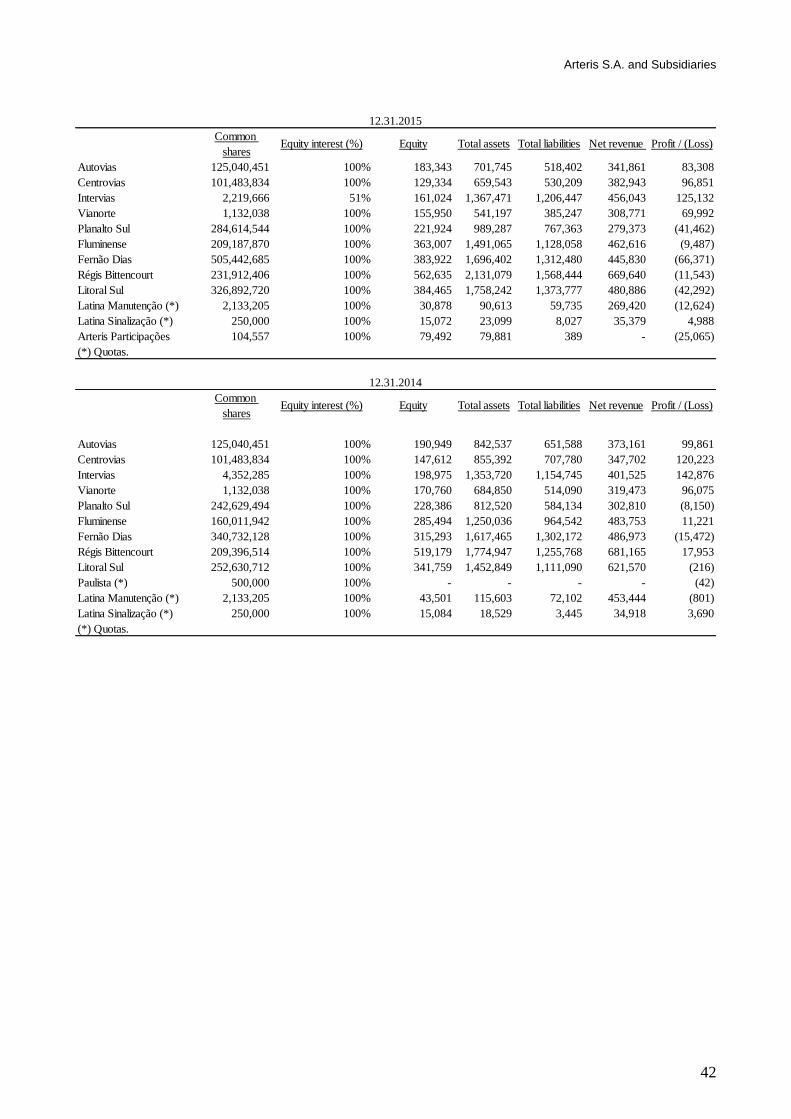

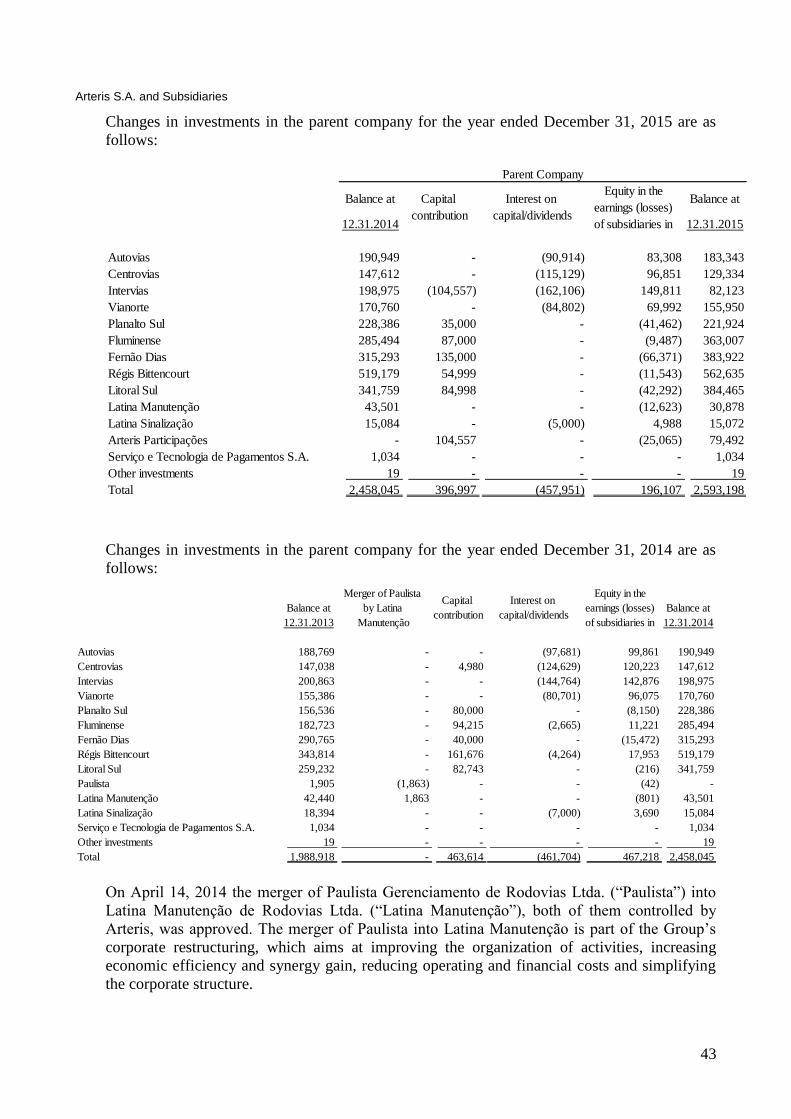

December 31, 2015 and December 31, 2014

Fiscal Council’s Report

Capital Budget Proposal

Arteris S.A.

Message from the CEO – Management Report

For Arteris, 2015 was a year marked by important initiatives that have increased the company’s efficiency and prepared it for the long-term challenges of the highway concession market. Investing has continued to be one of our main priorities, repeating what we have done in recent years thanks to the commitment of our employees. We ended the period with R$1.8 billion allocated to strategic works in the nine concessions managed by the company.

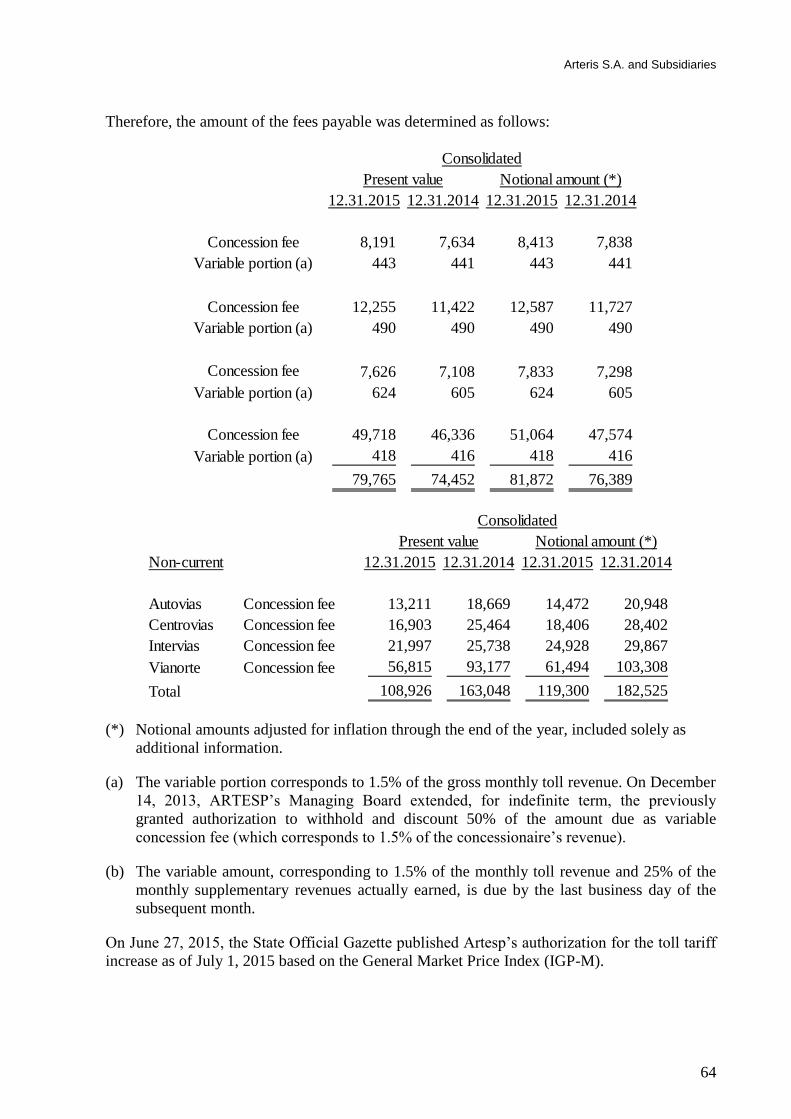

The 3,250-kilometer highway network managed by Arteris was further modernized with the investments made by the company, both in federal and state highways. Autopista Fluminense delivered Avenida do Contorno, in Niterói, offering an important contribution to the traffic flow in the metropolitan region of Rio de Janeiro. The duplication of Serra do Cafezal, in Autopista Régis Bittencourt, also received important advances with the beginning of the works to open the tunnels. In São Paulo highways, the emphasis was on delivering the revitalization of Contorno de Jaú by Centrovias.

All these results are being obtained with cost efficiency and quality assurance. The modern hiring system, especially due to the electronic auctions, have enabled the company to save R$170 million in the hiring of services and products, which represents a discount of around 10% on the amounts originally estimated in the bids. Our group also acted to renegotiate agreements, streamline processes and improve information quality. After all these efforts, we managed to maintain the growth of the company's costs below inflation.

Our goal is to continue working to develop Brazil’s highway infrastructure by assessing opportunities through transparent and productive dialogue with the regulating agencies. Upon request of the National Road Transportation Agency (ANTT), we began studies of our federal concessions related to investments estimated at R$5.2 billion provided for in the Logistics Investment Program (PIL).

Our annual results underline the company’s ability to deal with the current challenges of the Brazilian economy. Adjusted EBITDA totaled R$1.5 billion, with a margin of 64.0%. Gross toll revenue amounted to R$2.4 billion, while net income stood at R$149.3 million. Highlighting the market’s recognition of the solidity of our businesses, we raised R$750 million through a Holding Company debenture issue.

The respect for life, the main value of our company, was also a priority this year. We have improved our labor safety standards and guidelines, adopting stricter parameters than those established in the Brazilian legislation. We are fully committed to eliminating fatal accidents involving our direct and indirect employees. We have not attained that goal yet, but we are highly committed and working hard to achieve that milestone. This is an effort that transcends the Human Resources area; it requires the involvement of professionals from all areas. With road safety in mind, we developed specific action plans for each of the concessionaires. In the end, we achieved a 21% reduction in fatal accidents during the period, taking a decisive step towards the 50% reduction goal for the end of this decade.

In 2016, Arteris plans to continue investing heavily, with estimated investments of R$2.2 billion to be allocated to the company's works. The efforts to achieve cost efficiency and create synergies between the concessionaires are another priority, thus making us believe this year is crucial to our long-term strategy. The current scenario is challenging, but we know the importance of infrastructure to help the country enter a new cycle of economic growth.

David Díaz

Arteris’ CEO

MANAGEMENT REPORT

In compliance with the prevailing legislation and its Bylaws, the Management of Arteris S.A.

(“Arteris” or “Company”) hereby submits its report for the fiscal year ended December 31, 2015

for the appreciation of its investors and the market in general.

Profile

Arteris plays an important role in Brazil’s highway infrastructure sector, being responsible for

improving, extending, maintaining and managing toll roads under the concession programs of

the federal and São Paulo state governments.

Through its concessionaires, Arteris operates and manages 3,250 km of highways within the

country’s main economic centers, comprising the states of São Paulo, Minas Gerais, Paraná,

Rio de Janeiro and Santa Catarina, which are also characterized by their high population

density.

The group has nine concessionaires (four state and five federal), all of which are publicly-held

companies and wholly-owned subsidiaries of Arteris – Autovias S.A. (Autovias), Centrovias

Sistemas Rodoviários S.A. (Centrovias), Concessionária de Rodovias do Interior Paulista S.A.

(Intervias), Vianorte S.A. (Vianorte), Autopista Fernão Dias S.A. (Fernão Dias), Autopista

Fluminense S.A. (Fluminense), Autopista Litoral Sul S.A. (Litoral Sul), Autopista Planalto Sul

S.A. (Planalto Sul) and Autopista Régis Bittencourt S.A. (Régis Bittencourt).

The Company also owns 100% of Latina Manutenção de Rodovias Ltda. (Latina Manutenção)

and Latina Sinalização de Rodovias Ltda. (Latina Sinalização), which are responsible for

highway inspections, works management and maintenance, and retains a 4.68% interest in STP

– Serviços e Tecnologia de Pagamentos S.A., which pursues activities related to the electronic

toll collection system.

Economic Scenario

In 2015, Brazil’s economic performance was well below market expectations. GDP shrank by

3.8%, substantially more than the 0.2% estimated at the beginning of the year.

Arteris and the results of its business were directly affected by the overall state of Brazil’s

economy, especially in regard to inflation, interest and exchange rates, government policies, tax

policies and GDP growth.

In 2015, as the result of the domestic and international economic scenario, the Central Bank’s

Monetary Policy Committee (Copom) increased the Selic base rate from 11.75% to 14.25%, as

part of the government’s efforts to contain inflation, as detailed below.

Inflation measured by the IGP-M general market price index increased from 3.7% in 2014 to

10.5% in 2015, while the extended consumer price index (IPCA) moved up from 6.4% to 10.7%

in the same period. These indices influence the inflationary-economic environment and the

IPCA is used to calculate the adjustment of group concessionaires’ toll tariffs, thus directly

affecting the Company’s toll revenue.

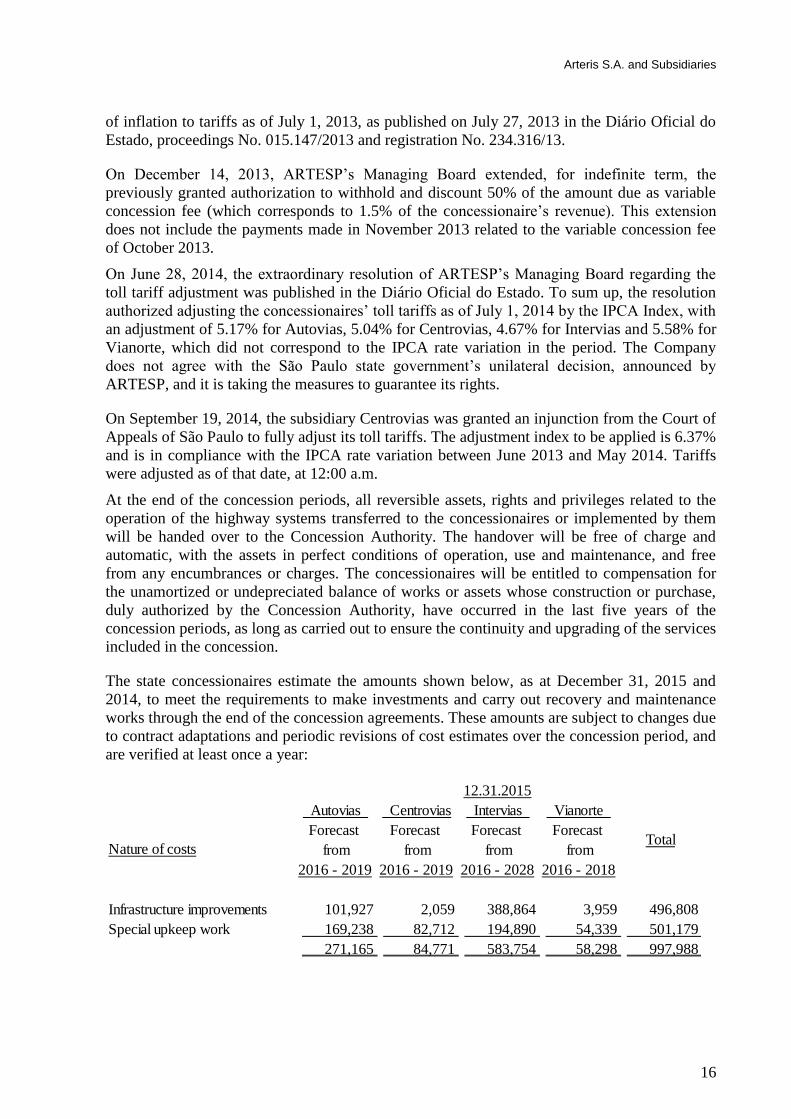

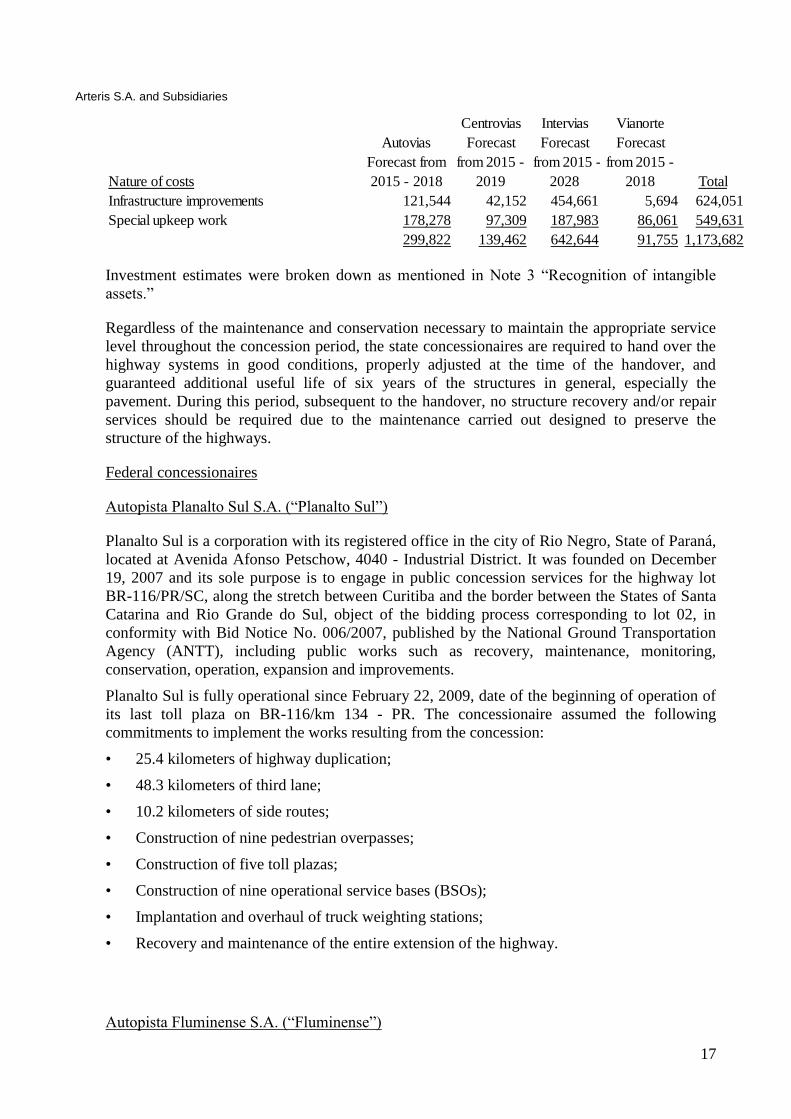

Material Events

Public Tender Offer:

On April 30, 2015, the Company informed the market of its controlling shareholders’ intention to

hold a Public Tender Offer for the Acquisition of Arteris Shares for purpose of cancellation of the

Company’s registration as category A publicly held company and delisting from the Novo

Mercado segment. The process is currently under analysis of the CVM. Shareholders are

awaiting CVM’s confirmation to publish the notice and hold the offer.

Tender Offer summarized schedule:

August 25, 2015: ASM – BNP Paribas was elected to prepare the Valuation Report

September 22, 2015: Availability of the Valuation Report (range of value: R$8.74 to

R$9.55 per share)

September 23, 2015: Participes en Brasil S.L. informed it would follow the Tender Offer

procedure

March 21, 2016: Availability of the new Valuation Report comprising CVM’s

requirements related to several official letters (new range of value: R$8.86 to R$9.58

per share)

March 23, 2016: Participes en Brasil S.L. informed it would follow the Tender Offer

procedure

Suspended Axles:

In April 2015, the Truck Drivers’ Law became effective, eliminating the charge on the

suspended axles of empty heavy vehicles on the federal highways. This impact was e impact

was rebalanced by tariff adjustments in the latest contractual tariff revisions in December 2015

and February 2016. This prohibition has not been applied in state concessions from the state of

São Paulo.

Change in accounting practices:

In 2015, the Company changed the criterion for amortizing its intangible assets from the traffic

curve method to the straight line method.

Supported by the guidelines issued by the Accounting Committee Pronouncement no. 5 (CPC

5), the Company believes that the change (adoption of a straight-line amortization method),

reflects the effects of the wear and tear of its intangible assets in a more realistic manner.

Economic and Financial Performance

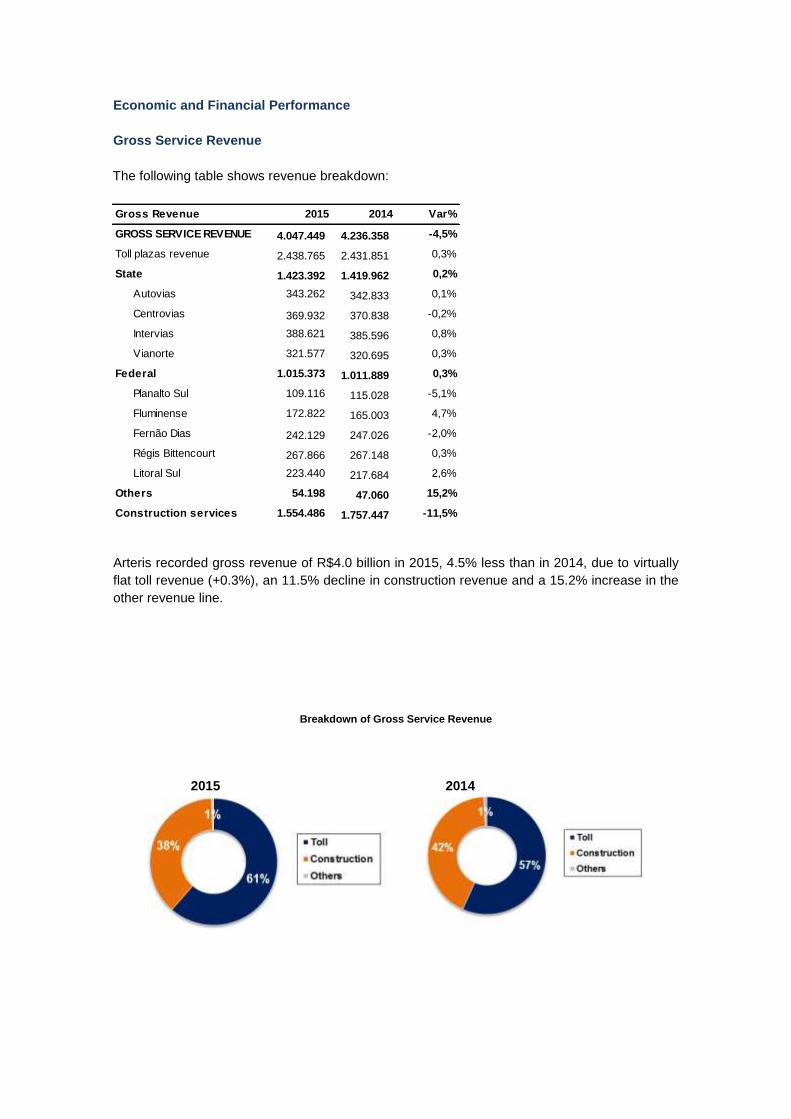

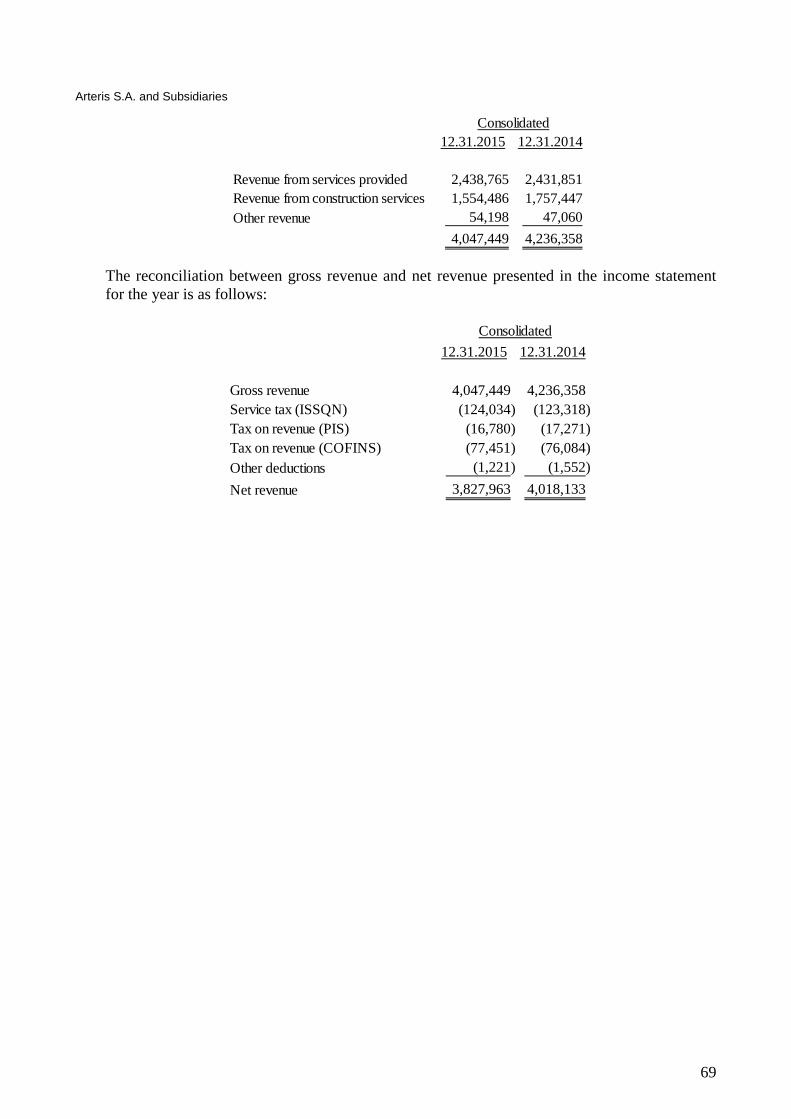

Gross Service Revenue

The following table shows revenue breakdown:

Arteris recorded gross revenue of R$4.0 billion in 2015, 4.5% less than in 2014, due to virtually

flat toll revenue (+0.3%), an 11.5% decline in construction revenue and a 15.2% increase in the

other revenue line.

Breakdown of Gross Service Revenue

2015 2014

Gross Revenue 2015 2014 Var%

GROSS SERVICE REVENUE 4.047.449 4.236.358 -4,5%

Toll plazas revenue 2.438.765 2.431.851 0,3%

State 1.423.392 1.419.962 0,2%

Autovias 343.262 342.833 0,1%

Centrovias 369.932 370.838 -0,2%

Intervias 388.621 385.596 0,8%

Vianorte 321.577 320.695 0,3%

Federal 1.015.373 1.011.889 0,3%

Planalto Sul 109.116 115.028 -5,1%

Fluminense 172.822 165.003 4,7%

Fernão Dias 242.129 247.026 -2,0%

Régis Bittencourt 267.866 267.148 0,3%

Litoral Sul 223.440 217.684 2,6%

Others 54.198 47.060 15,2%

Construction services 1.554.486 1.757.447 -11,5%

Toll Plaza Revenue

Toll plaza revenue remained virtually flat (+0.3%) in 2015, totaling R$2.4 billion, despite the

annual reduction in traffic, thanks to the tariff adjustments in all concessions. Some of the

federal highway adjustments were above inflation due to the rebalancing of the contracts.

The state concessions accounted for 58% of the total, moving up by 0.2% over 2014, to R$1.4

billion, while the federal highways recorded a 0.1% improvement to R$1 billion.

Breakdown of Toll Revenue

2015 2014

Tolled Traffic: The Company’s tolled traffic volume came to 680,623 thousand vehicle

equivalents in 2015, 6.3% up on 2014.

The deterioration in Brazil’s economic environment and the consequent shrinkage of GDP, especially in

regard to industrial production, led to a substantial reduction in the volume of tolled vehicles in recent

quarters. The impact of the slowdown led to a hefty decline in heavy traffic, mainly on our federal

highways, an average 70% of whose traffic consists of heavy vehicle equivalents, versus 60%

on the state highways.

Another factor contributing to the traffic downturn was the application, since April 2015, of the

Truck Drivers’ Law, which eliminated the charge on the suspended axles of empty heavy

vehicles on the federal highways and whose impact was rebalanced by tariff adjustments in the

contractual tariff revision. If this law had not been in effect, federal highway and consolidated

tolled traffic would have fallen by 4.0%.

Vehicle-Equivalents (Thousand) 2015 2014 Var%

State Concessions 204,458 213,097 -4.1%

Autovias 46,774 48,939 -4.4%

Centrovias 55,330 58,336 -5.2%

Intervias 64,967 66,937 -2.9%

Vianorte 37,387 38,885 -3.9%

Federal Concessions 476,165 513,198 -7.2%

Planalto Sul 26,462 30,185 -12.3%

Fluminense 45,934 48,653 -5.6%

Fernão Dias 150,652 164,275 -8.3%

Régis Bittencourt 133,668 148,263 -9.8%

Litoral Sul 119,449 121,823 -1.9%

Total 680,623 726,295 -6.3%

In terms of composition, 61.4% of 2015 tolled traffic in the state concessions (measured in

vehicle equivalents) consisted of heavy vehicles and 38.6% of light vehicles, with respective

ratios of 69.8% and 30.2% in the federal concessions.

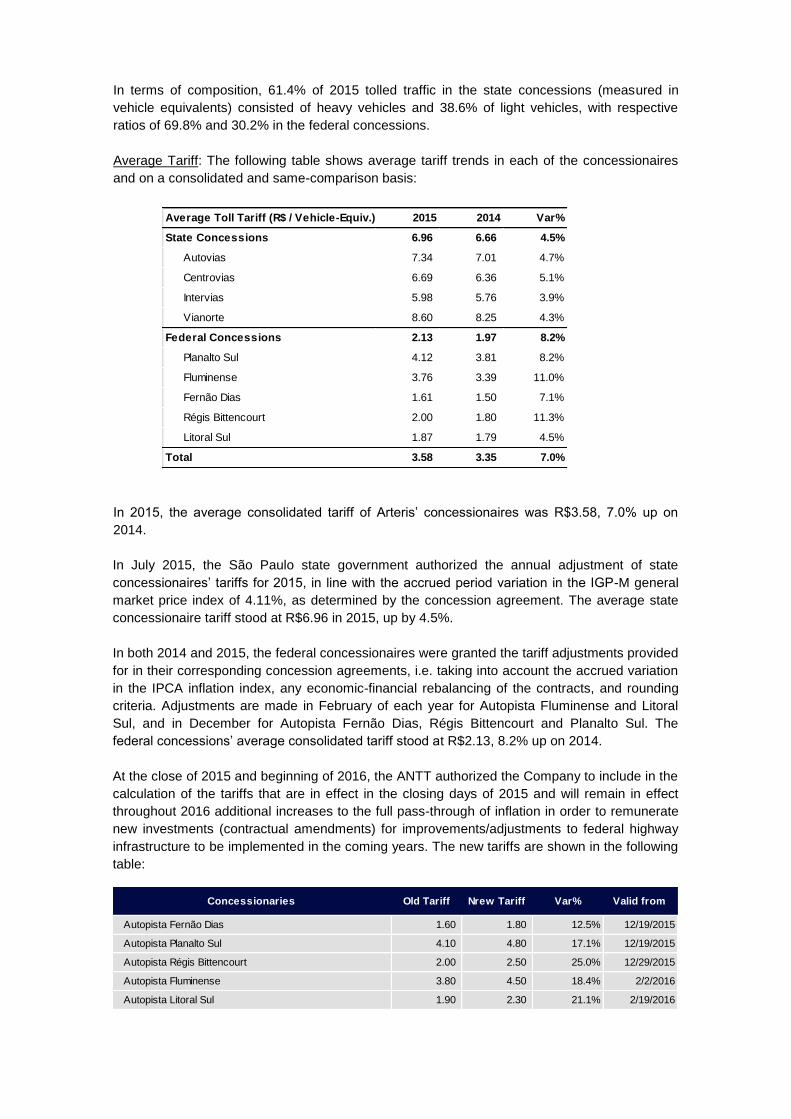

Average Tariff: The following table shows average tariff trends in each of the concessionaires

and on a consolidated and same-comparison basis:

In 2015, the average consolidated tariff of Arteris’ concessionaires was R$3.58, 7.0% up on

2014.

In July 2015, the São Paulo state government authorized the annual adjustment of state

concessionaires’ tariffs for 2015, in line with the accrued period variation in the IGP-M general

market price index of 4.11%, as determined by the concession agreement. The average state

concessionaire tariff stood at R$6.96 in 2015, up by 4.5%.

In both 2014 and 2015, the federal concessionaires were granted the tariff adjustments provided

for in their corresponding concession agreements, i.e. taking into account the accrued variation

in the IPCA inflation index, any economic-financial rebalancing of the contracts, and rounding

criteria. Adjustments are made in February of each year for Autopista Fluminense and Litoral

Sul, and in December for Autopista Fernão Dias, Régis Bittencourt and Planalto Sul. The

federal concessions’ average consolidated tariff stood at R$2.13, 8.2% up on 2014.

At the close of 2015 and beginning of 2016, the ANTT authorized the Company to include in the

calculation of the tariffs that are in effect in the closing days of 2015 and will remain in effect

throughout 2016 additional increases to the full pass-through of inflation in order to remunerate

new investments (contractual amendments) for improvements/adjustments to federal highway

infrastructure to be implemented in the coming years. The new tariffs are shown in the following

table:

Average Toll Tariff (R$ / Vehicle-Equiv.) 2015 2014 Var%

State Concessions 6.96 6.66 4.5%

Autovias 7.34 7.01 4.7%

Centrovias 6.69 6.36 5.1%

Intervias 5.98 5.76 3.9%

Vianorte 8.60 8.25 4.3%

Federal Concessions 2.13 1.97 8.2%

Planalto Sul 4.12 3.81 8.2%

Fluminense 3.76 3.39 11.0%

Fernão Dias 1.61 1.50 7.1%

Régis Bittencourt 2.00 1.80 11.3%

Litoral Sul 1.87 1.79 4.5%

Total 3.58 3.35 7.0%

Concessionaries Old Tariff Nrew Tariff Var% Valid from

Autopista Fernão Dias 1.60 1.80 12.5% 12/19/2015

Autopista Planalto Sul 4.10 4.80 17.1% 12/19/2015

Autopista Régis Bittencourt 2.00 2.50 25.0% 12/29/2015

Autopista Fluminense 3.80 4.50 18.4% 2/2/2016

Autopista Litoral Sul 1.90 2.30 21.1% 2/19/2016

Electronic Collection: Revenue from toll plaza electronic payments (AVI System) in the state

concessionaires accounted for 66.8% of total revenue in 2015, versus 66.4% in 2014, while the

average ratio in the federal concessionaires was 53.2% in 2015, compared to 52.5% in 2014.

Construction Revenue

Construction revenue — an accounting representation of the Company’s investments in

intangible assets and therefore with no cash effect — declined by 11.5% over 2014 to R$1.6

billion, due to the fact that a portion of the increase in investments was related to maintenance

works that are not recorded in this line.

Other Revenue

The “other revenue” line is composed exclusively of ancillary revenue from the exploration/sale

of highway right-of-way services. In 2015, this item came to R$54.2 million, 15.2% up on 2014.

Net Service Revenue and Deductions from Revenue

Net revenue came to R$3.8 billion in 2015, 4.7% down on 2014.

Revenue deductions, composed of PIS, COFINS and ISS taxes, totaled R$219.5 million in

2015.

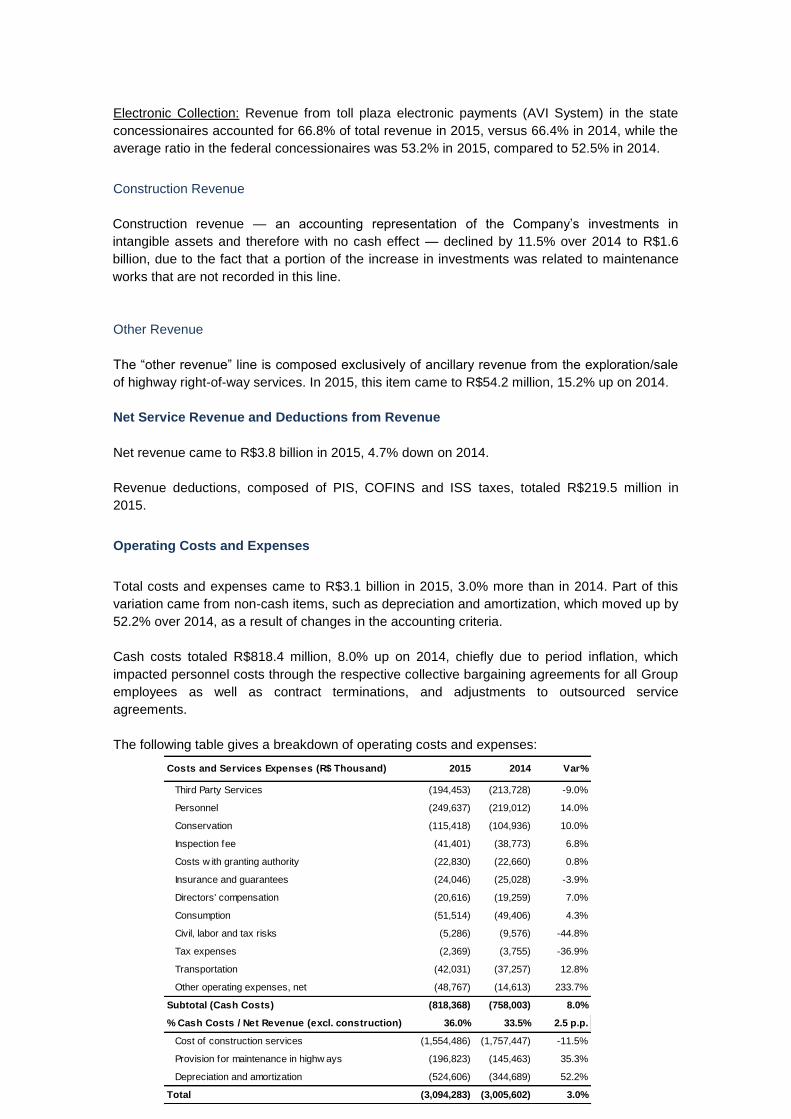

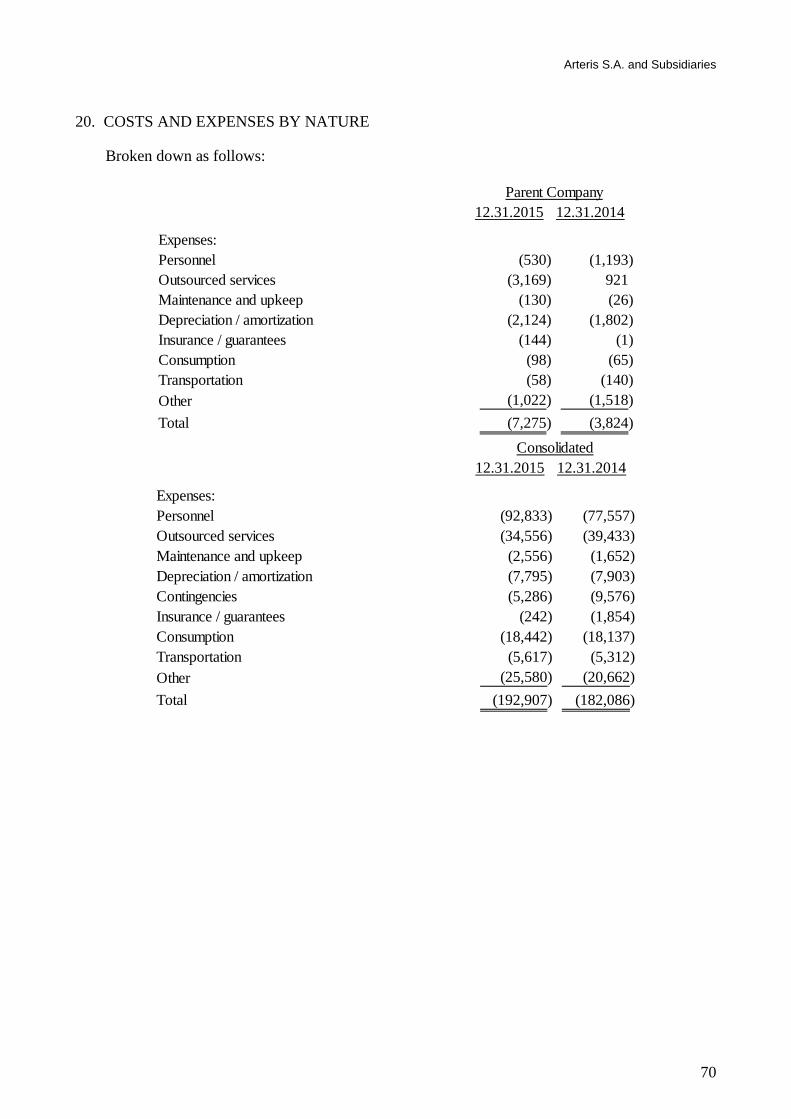

Operating Costs and Expenses

Total costs and expenses came to R$3.1 billion in 2015, 3.0% more than in 2014. Part of this

variation came from non-cash items, such as depreciation and amortization, which moved up by

52.2% over 2014, as a result of changes in the accounting criteria.

Cash costs totaled R$818.4 million, 8.0% up on 2014, chiefly due to period inflation, which

impacted personnel costs through the respective collective bargaining agreements for all Group

employees as well as contract terminations, and adjustments to outsourced service

agreements.

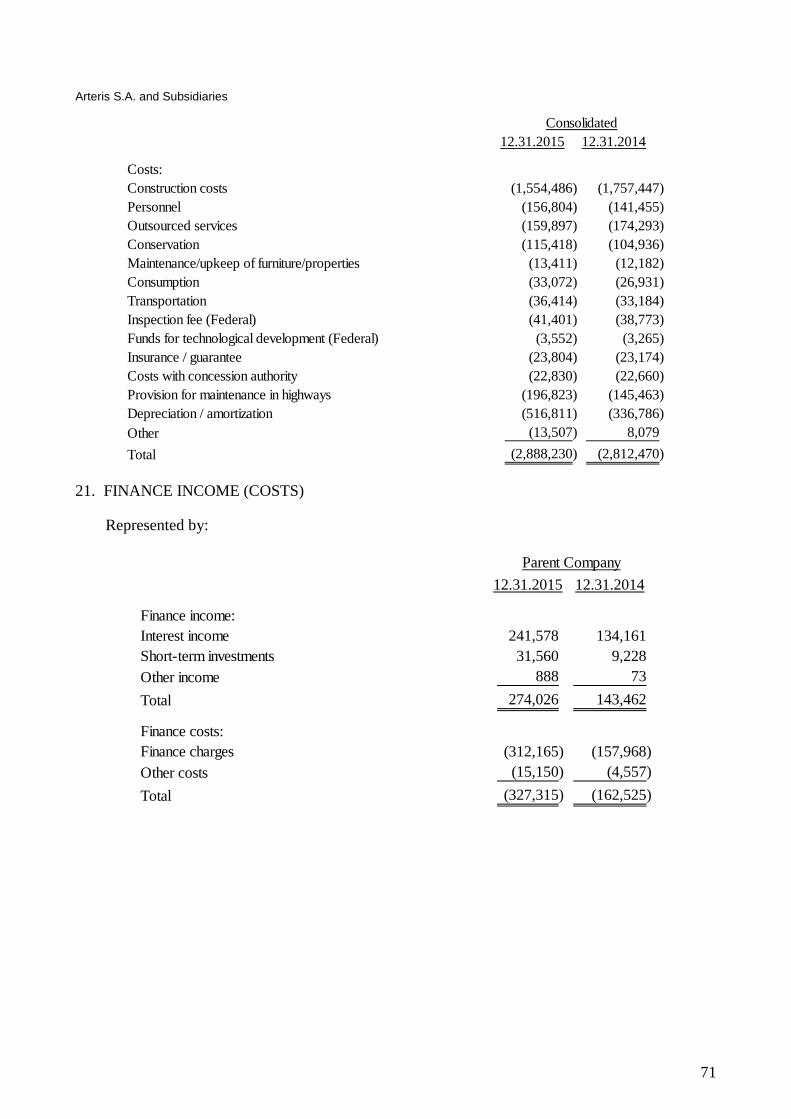

The following table gives a breakdown of operating costs and expenses:

Costs and Services Expenses (R$ Thousand) 2015 2014 Var%

Third Party Services (194,453) (213,728) -9.0%

Personnel (249,637) (219,012) 14.0%

Conservation (115,418) (104,936) 10.0%

Inspection fee (41,401) (38,773) 6.8%

Costs w ith granting authority (22,830) (22,660) 0.8%

Insurance and guarantees (24,046) (25,028) -3.9%

Directors' compensation (20,616) (19,259) 7.0%

Consumption (51,514) (49,406) 4.3%

Civil, labor and tax risks (5,286) (9,576) -44.8%

Tax expenses (2,369) (3,755) -36.9%

Transportation (42,031) (37,257) 12.8%

Other operating expenses, net (48,767) (14,613) 233.7%

Subtotal (Cash Costs) (818,368) (758,003) 8.0%

% Cash Costs / Net Revenue (excl. construction) 36.0% 33.5% 2.5 p.p.

Cost of construction services (1,554,486) (1,757,447) -11.5%

Provision for maintenance in highw ays (196,823) (145,463) 35.3%

Depreciation and amortization (524,606) (344,689) 52.2%

Total (3,094,283) (3,005,602) 3.0%

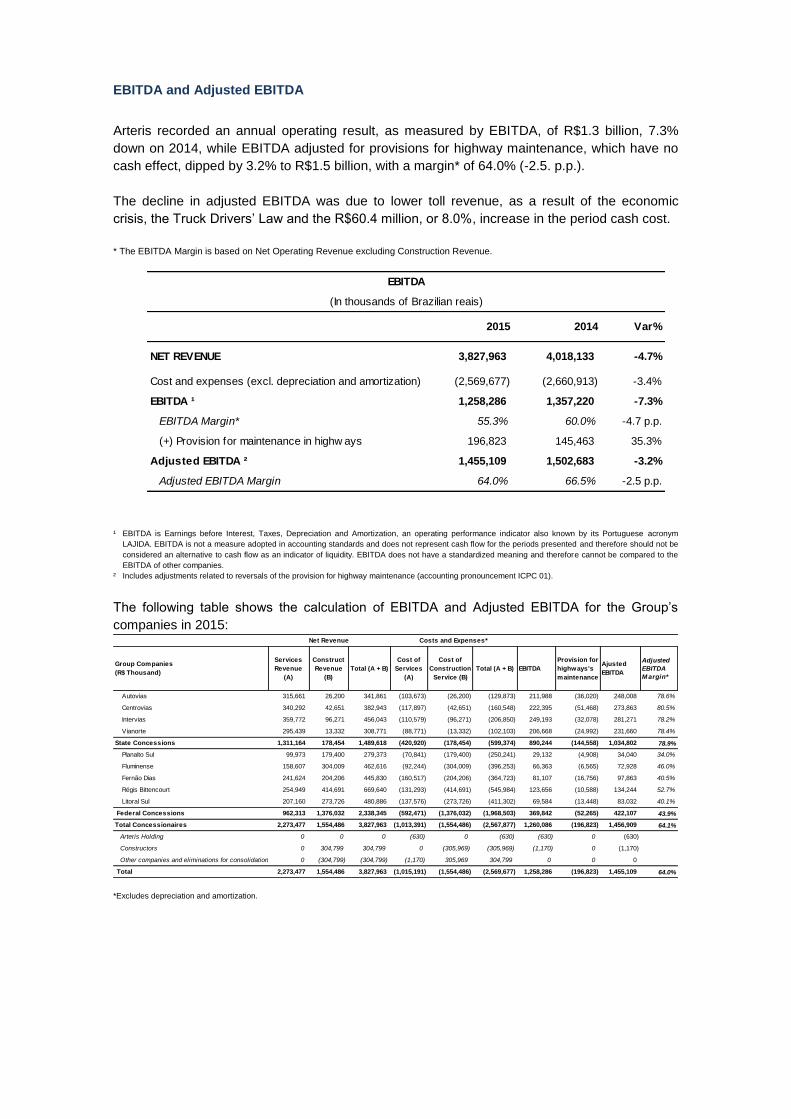

EBITDA and Adjusted EBITDA

Arteris recorded an annual operating result, as measured by EBITDA, of R$1.3 billion, 7.3%

down on 2014, while EBITDA adjusted for provisions for highway maintenance, which have no

cash effect, dipped by 3.2% to R$1.5 billion, with a margin* of 64.0% (-2.5. p.p.).

The decline in adjusted EBITDA was due to lower toll revenue, as a result of the economic

crisis, the Truck Drivers’ Law and the R$60.4 million, or 8.0%, increase in the period cash cost.

* The EBITDA Margin is based on Net Operating Revenue excluding Construction Revenue.

¹ EBITDA is Earnings before Interest, Taxes, Depreciation and Amortization, an operating performance indicator also known by its Portuguese acronym

LAJIDA. EBITDA is not a measure adopted in accounting standards and does not represent cash flow for the periods presented and therefore should not be

considered an alternative to cash flow as an indicator of liquidity. EBITDA does not have a standardized meaning and therefore cannot be compared to the

EBITDA of other companies.

² Includes adjustments related to reversals of the provision for highway maintenance (accounting pronouncement ICPC 01).

The following table shows the calculation of EBITDA and Adjusted EBITDA for the Group’s

companies in 2015:

*Excludes depreciation and amortization.

2015 2014 Var%

NET REVENUE 3,827,963 4,018,133 -4.7%

Cost and expenses (excl. depreciation and amortization) (2,569,677) (2,660,913) -3.4%

EBITDA ¹ 1,258,286 1,357,220 -7.3%

EBITDA Margin* 55.3% 60.0% -4.7 p.p.

(+) Provision for maintenance in highw ays 196,823 145,463 35.3%

Adjusted EBITDA ² 1,455,109 1,502,683 -3.2%

Adjusted EBITDA Margin 64.0% 66.5% -2.5 p.p.

EBITDA

(In thousands of Brazilian reais)

Group Companies

(R$ Thousand)

Services

Revenue

(A)

Construct

Revenue

(B)

Total (A + B)

Cost of

Services

(A)

Cost of

Construction

Service (B)

Total (A + B) EBITDA

Provision for

highways's

maintenance

Ajusted

EBITDA

Adjusted

EBITDA

M argin*

Autovias 315,661 26,200 341,861 (103,673) (26,200) (129,873) 211,988 (36,020) 248,008 78.6%

Centrovias 340,292 42,651 382,943 (117,897) (42,651) (160,548) 222,395 (51,468) 273,863 80.5%

Intervias 359,772 96,271 456,043 (110,579) (96,271) (206,850) 249,193 (32,078) 281,271 78.2%

Vianorte 295,439 13,332 308,771 (88,771) (13,332) (102,103) 206,668 (24,992) 231,660 78.4%

State Concessions 1,311,164 178,454 1,489,618 (420,920) (178,454) (599,374) 890,244 (144,558) 1,034,802 78.9%

Planalto Sul 99,973 179,400 279,373 (70,841) (179,400) (250,241) 29,132 (4,908) 34,040 34.0%

Fluminense 158,607 304,009 462,616 (92,244) (304,009) (396,253) 66,363 (6,565) 72,928 46.0%

Fernão Dias 241,624 204,206 445,830 (160,517) (204,206) (364,723) 81,107 (16,756) 97,863 40.5%

Régis Bittencourt 254,949 414,691 669,640 (131,293) (414,691) (545,984) 123,656 (10,588) 134,244 52.7%

Litoral Sul 207,160 273,726 480,886 (137,576) (273,726) (411,302) 69,584 (13,448) 83,032 40.1%

Federal Concessions 962,313 1,376,032 2,338,345 (592,471) (1,376,032) (1,968,503) 369,842 (52,265) 422,107 43.9%

Total Concessionaires 2,273,477 1,554,486 3,827,963 (1,013,391) (1,554,486) (2,567,877) 1,260,086 (196,823) 1,456,909 64.1%

Arteris Holding 0 0 0 (630) 0 (630) (630) 0 (630)

Constructors 0 304,799 304,799 0 (305,969) (305,969) (1,170) 0 (1,170)

Other companies and eliminations for consolidation 0 (304,799) (304,799) (1,170) 305,969 304,799 0 0 0

Total 2,273,477 1,554,486 3,827,963 (1,015,191) (1,554,486) (2,569,677) 1,258,286 (196,823) 1,455,109 64.0%

Net Revenue Costs and Expenses*

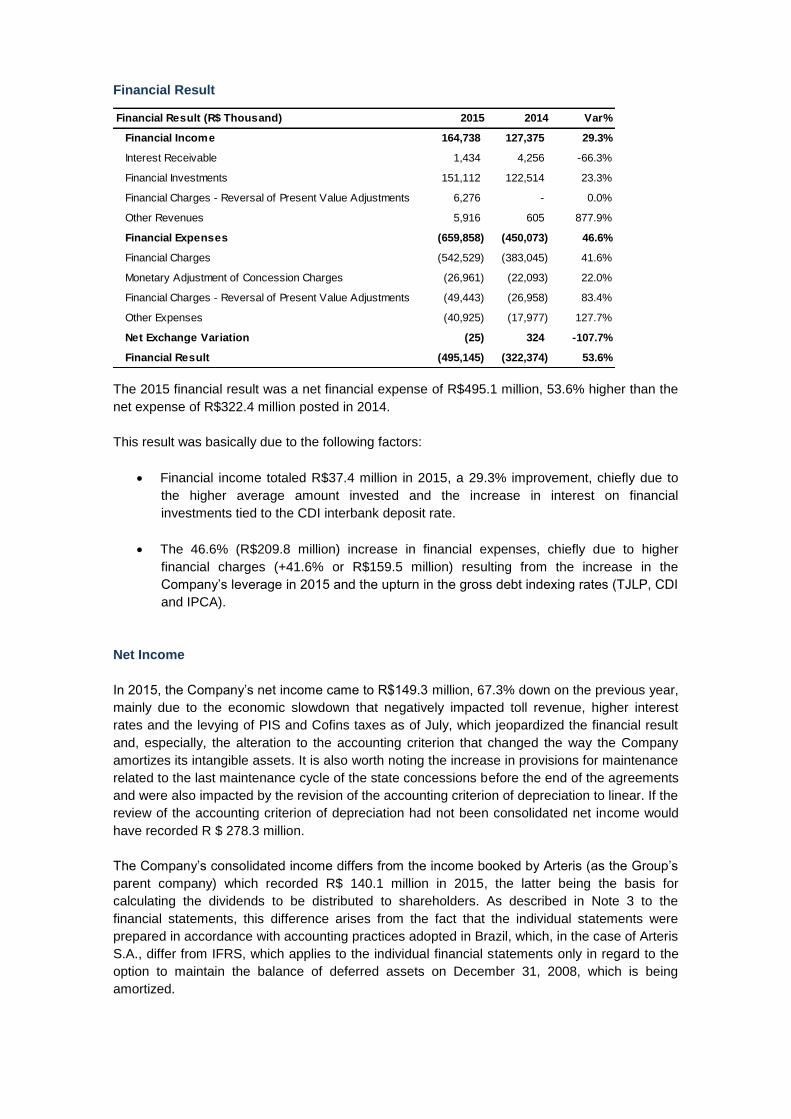

Financial Result

The 2015 financial result was a net financial expense of R$495.1 million, 53.6% higher than the

net expense of R$322.4 million posted in 2014.

This result was basically due to the following factors:

Financial income totaled R$37.4 million in 2015, a 29.3% improvement, chiefly due to

the higher average amount invested and the increase in interest on financial

investments tied to the CDI interbank deposit rate.

The 46.6% (R$209.8 million) increase in financial expenses, chiefly due to higher

financial charges (+41.6% or R$159.5 million) resulting from the increase in the

Company’s leverage in 2015 and the upturn in the gross debt indexing rates (TJLP, CDI

and IPCA).

Net Income

In 2015, the Company’s net income came to R$149.3 million, 67.3% down on the previous year,

mainly due to the economic slowdown that negatively impacted toll revenue, higher interest

rates and the levying of PIS and Cofins taxes as of July, which jeopardized the financial result

and, especially, the alteration to the accounting criterion that changed the way the Company

amortizes its intangible assets. It is also worth noting the increase in provisions for maintenance

related to the last maintenance cycle of the state concessions before the end of the agreements

and were also impacted by the revision of the accounting criterion of depreciation to linear. If the

review of the accounting criterion of depreciation had not been consolidated net income would

have recorded R $ 278.3 million.

The Company’s consolidated income differs from the income booked by Arteris (as the Group’s

parent company) which recorded R$ 140.1 million in 2015, the latter being the basis for

calculating the dividends to be distributed to shareholders. As described in Note 3 to the

financial statements, this difference arises from the fact that the individual statements were

prepared in accordance with accounting practices adopted in Brazil, which, in the case of Arteris

S.A., differ from IFRS, which applies to the individual financial statements only in regard to the

option to maintain the balance of deferred assets on December 31, 2008, which is being

amortized.

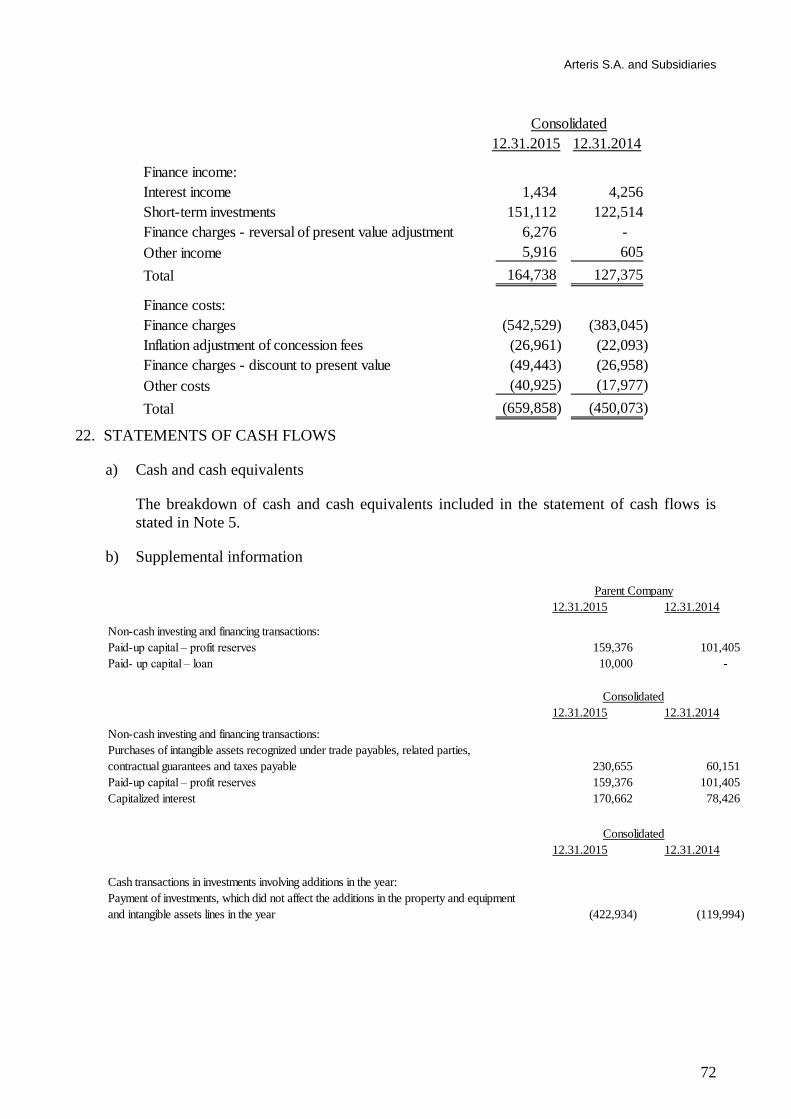

Financial Result (R$ Thousand) 2015 2014 Var%

Financial Income 164,738 127,375 29.3%

Interest Receivable 1,434 4,256 -66.3%

Financial Investments 151,112 122,514 23.3%

Financial Charges - Reversal of Present Value Adjustments 6,276 - 0.0%

Other Revenues 5,916 605 877.9%

Financial Expenses (659,858) (450,073) 46.6%

Financial Charges (542,529) (383,045) 41.6%

Monetary Adjustment of Concession Charges (26,961) (22,093) 22.0%

Financial Charges - Reversal of Present Value Adjustments (49,443) (26,958) 83.4%

Other Expenses (40,925) (17,977) 127.7%

Net Exchange Variation (25) 324 -107.7%

Financial Result (495,145) (322,374) 53.6%

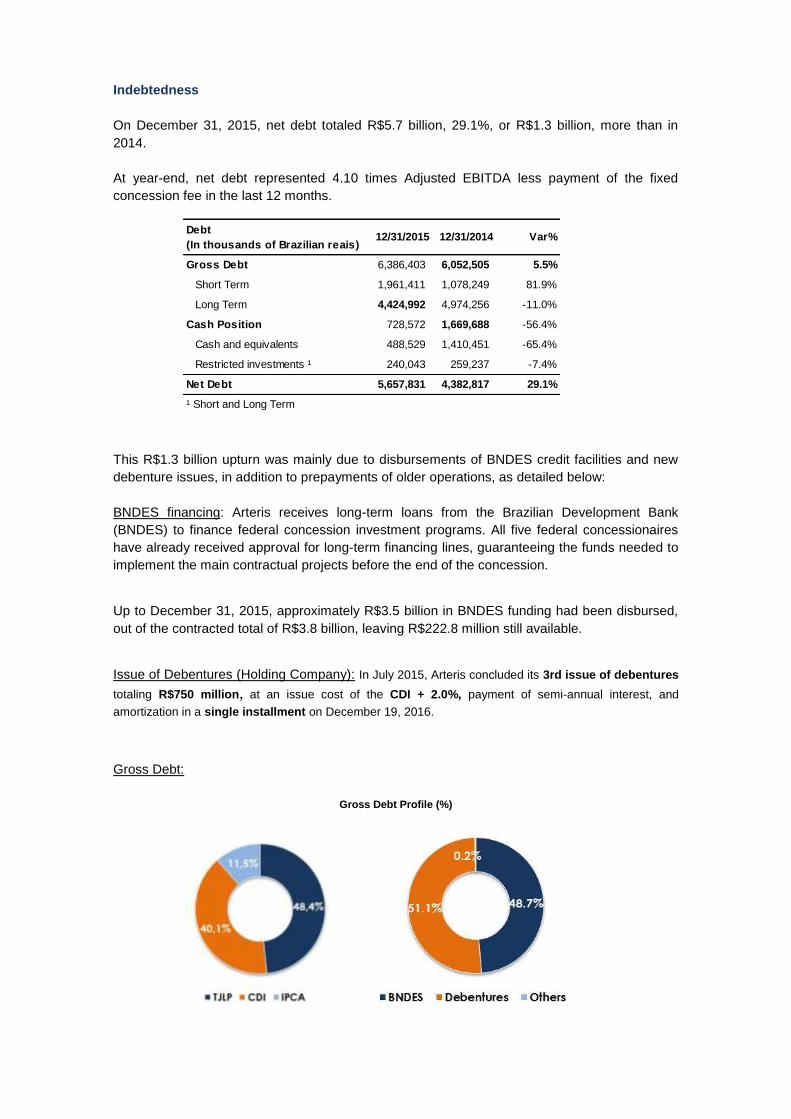

Indebtedness

On December 31, 2015, net debt totaled R$5.7 billion, 29.1%, or R$1.3 billion, more than in

2014.

At year-end, net debt represented 4.10 times Adjusted EBITDA less payment of the fixed

concession fee in the last 12 months.

This R$1.3 billion upturn was mainly due to disbursements of BNDES credit facilities and new

debenture issues, in addition to prepayments of older operations, as detailed below:

BNDES financing: Arteris receives long-term loans from the Brazilian Development Bank

(BNDES) to finance federal concession investment programs. All five federal concessionaires

have already received approval for long-term financing lines, guaranteeing the funds needed to

implement the main contractual projects before the end of the concession.

Up to December 31, 2015, approximately R$3.5 billion in BNDES funding had been disbursed,

out of the contracted total of R$3.8 billion, leaving R$222.8 million still available.

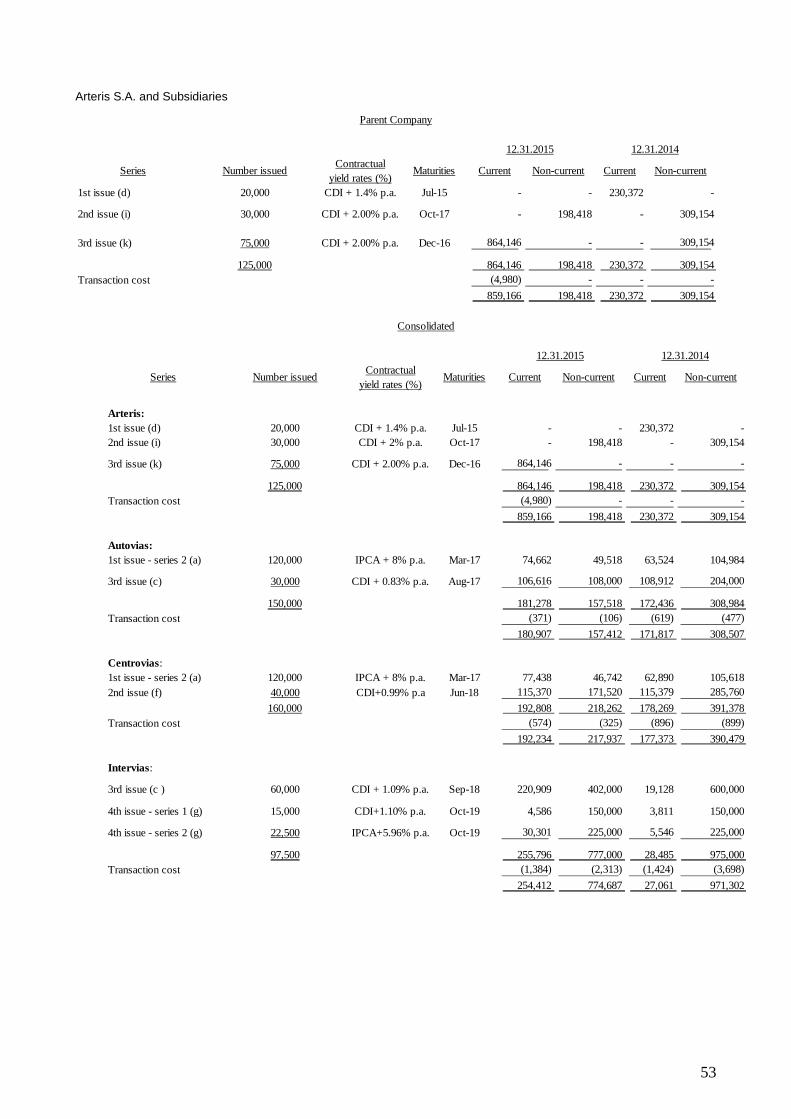

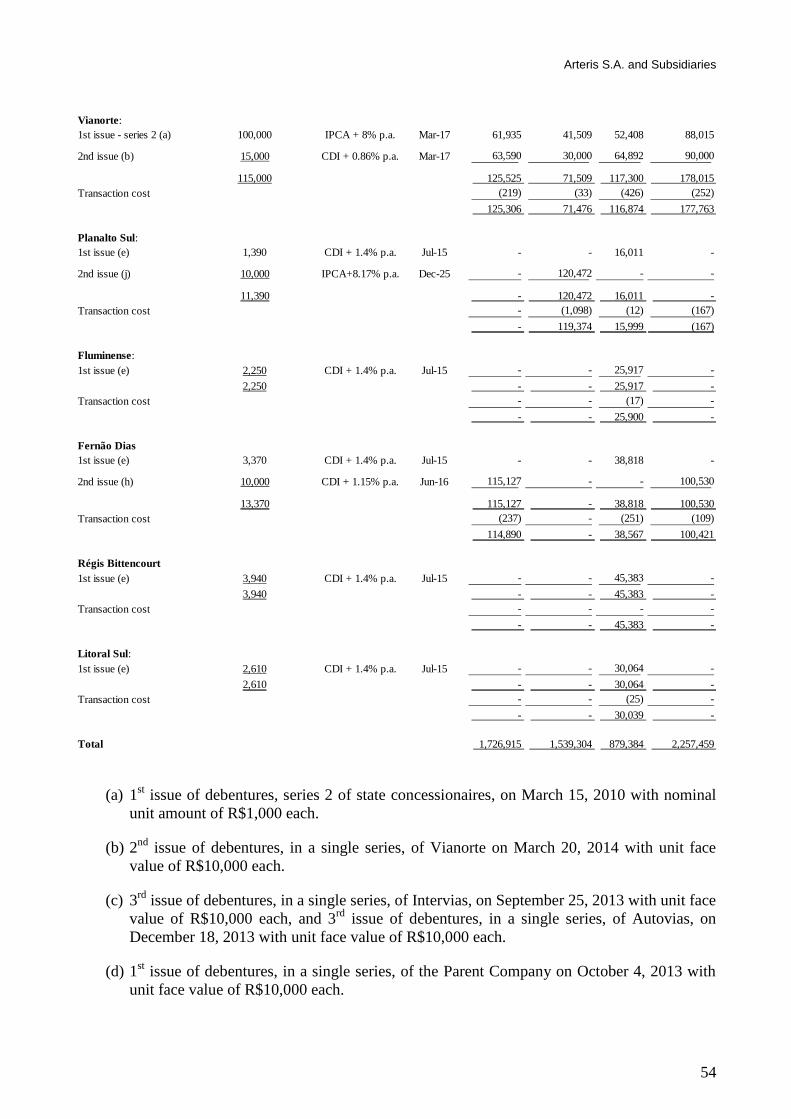

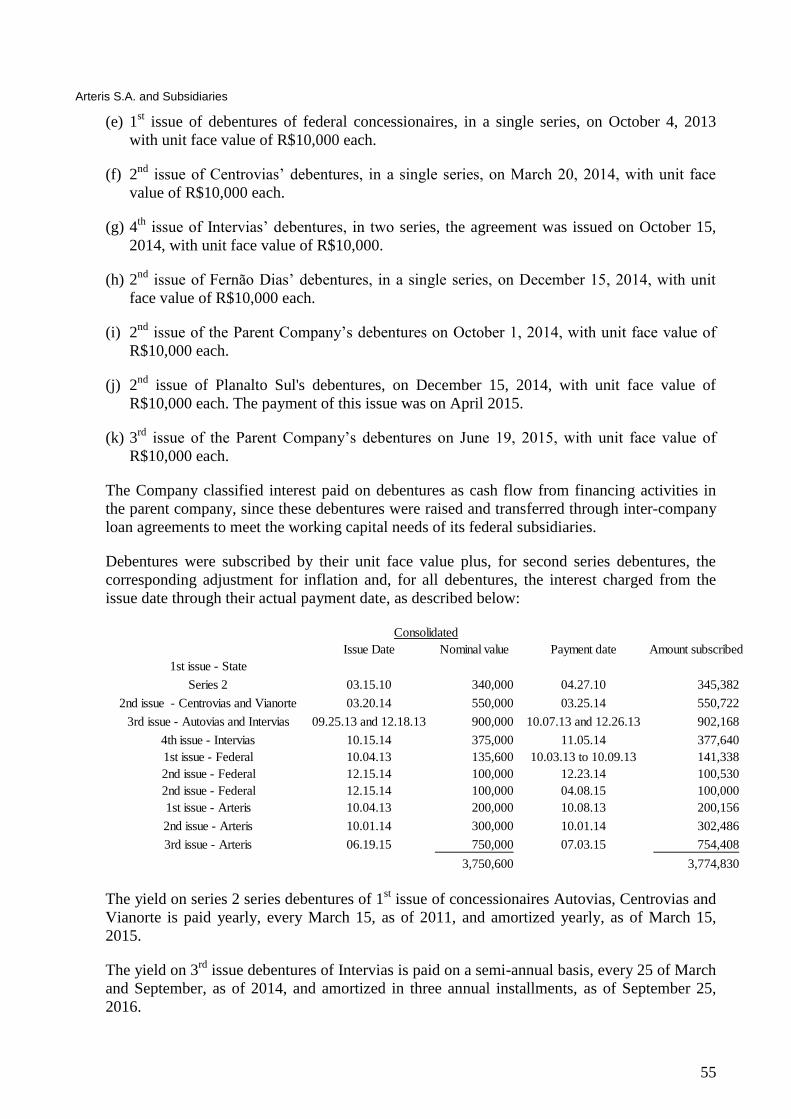

Issue of Debentures (Holding Company): In July 2015, Arteris concluded its 3rd issue of debentures

totaling R$750 million, at an issue cost of the CDI + 2.0%, payment of semi-annual interest, and

amortization in a single installment on December 19, 2016.

Gross Debt:

Gross Debt Profile (%)

Debt

(In thousands of Brazilian reais)12/31/2015 12/31/2014 Var%

Gross Debt 6,386,403 6,052,505 5.5%

Short Term 1,961,411 1,078,249 81.9%

Long Term 4,424,992 4,974,256 -11.0%

Cash Position 728,572 1,669,688 -56.4%

Cash and equivalents 488,529 1,410,451 -65.4%

Restricted investments ¹ 240,043 259,237 -7.4%

Net Debt 5,657,831 4,382,817 29.1%

¹ Short and Long Term

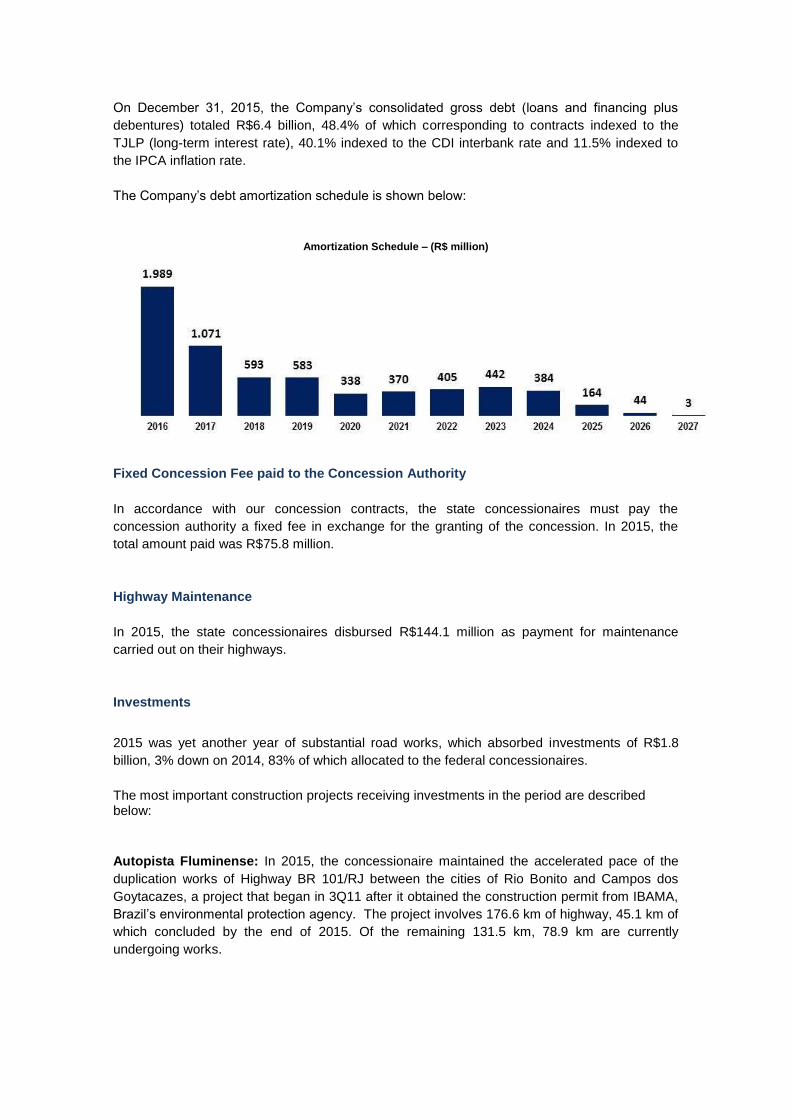

On December 31, 2015, the Company’s consolidated gross debt (loans and financing plus

debentures) totaled R$6.4 billion, 48.4% of which corresponding to contracts indexed to the

TJLP (long-term interest rate), 40.1% indexed to the CDI interbank rate and 11.5% indexed to

the IPCA inflation rate.

The Company’s debt amortization schedule is shown below:

Amortization Schedule – (R$ million)

Fixed Concession Fee paid to the Concession Authority

In accordance with our concession contracts, the state concessionaires must pay the

concession authority a fixed fee in exchange for the granting of the concession. In 2015, the

total amount paid was R$75.8 million.

Highway Maintenance

In 2015, the state concessionaires disbursed R$144.1 million as payment for maintenance

carried out on their highways.

Investments

2015 was yet another year of substantial road works, which absorbed investments of R$1.8

billion, 3% down on 2014, 83% of which allocated to the federal concessionaires.

The most important construction projects receiving investments in the period are described below:

Autopista Fluminense: In 2015, the concessionaire maintained the accelerated pace of the

duplication works of Highway BR 101/RJ between the cities of Rio Bonito and Campos dos

Goytacazes, a project that began in 3Q11 after it obtained the construction permit from IBAMA,

Brazil’s environmental protection agency. The project involves 176.6 km of highway, 45.1 km of

which concluded by the end of 2015. Of the remaining 131.5 km, 78.9 km are currently

undergoing works.

In August 2015, the Company concluded the duplication works of Avenida do Contorno, in the

city of Niterói, including an extension of 2.2 km. The project increased the safety of highway

users, due to the expansion of the road’s capacity.

Autopista Fernão Dias: After having completed the implantation of the 8.1 kilometer Betim

Beltway (MG) in 2013, creating an alternative for long-distance highway traffic, which used to

pass through the city, the concessionaire concluded its main contractual works.

However, other improvements have been implemented on the highway, including the

construction of 22 km of side roads in Atibaia (SP), Extrema (MG) and Camanducaia (MG), 2.6

km of side roads in the city of Betim (MG) and the improvement of three access ways at km

887+450, km 902+000 and km 947+880.

Autopista Régis Bittencourt: The Serra do Cafezal (BR-116/SP) project, the concessionaire’s

main construction work, continues to move ahead. The Company has already concluded and

delivered 17.9 km of the duplication of a total of 30.5 km, including two interchanges. In

December 2014, the ANTT approved the necessary contractual rebalancing for the continuation

of the works, which include the construction of four tunnels, all of which in progress, and 42

bridges and overpasses (11 concluded, 22 in progress and 9 not yet started).

Other improvements are being implemented on the highway, including the conclusion of the

construction of 10.6 km of side roads.

Autopista Planalto Sul: The concessionaire’s main project is the duplication of 25.4 km of the

BR-116/PR between Curitiba (PR) and Mandirituba (PR), whose construction permit has

already been obtained from IBAMA. Of this total, 9.8 km between Curitiba and Fazenda Rio

Grande (PR) have already been concluded and freed for traffic, and the remainder, up to

Mandirituba (PR), is under construction.

In 2015, an underpass was constructed at km 128.6, in the city of Fazenda Rio Grande/PR, as

well as two raised interchanges at km 127.5 and km 131.8, in Fazenda Rio Grande (PR).

Additionally, the Vila Pompéia Interchange was concluded at km 117.7, in Curitiba/PR.

Autopista Litoral Sul: The Florianópolis Beltway project, one of the most important works in

the region, began in May 2014, immediately after IBAMA had granted the installation license for

a 14 km stretch. In May 2015, the Company obtained a rectifying Environmental License

covering a total extension of 47 km. The northern and intermediate stretches are currently

undergoing works, including one raised interchange at km 215+380 and four underpasses.

In 2015, the Concessionaire also concluded the construction of 5 km of side roads, five

overpasses and one underpass at km 169+650, in Tijucas (SC).

Autovias: In September 2014 Autovias began duplicating 13.6 km of the SP 318 between km

235 and 249, in the São Carlos region. This is a new project which will be added to the

concession agreement, resulting in a six-month extension of the concession term until May

2019, in accordance with the marginal cash flow method for the economic and financial

rebalancing of the agreement.

Intervias: In February 2016, the implementation of the second 5 km stage of the Mogi Mirim

Beltway was concluded.

The concessionaire is also duplicating the SP 147 between Mogi Mirim and Engenheiro Coelho,

a project that began in September 2014.

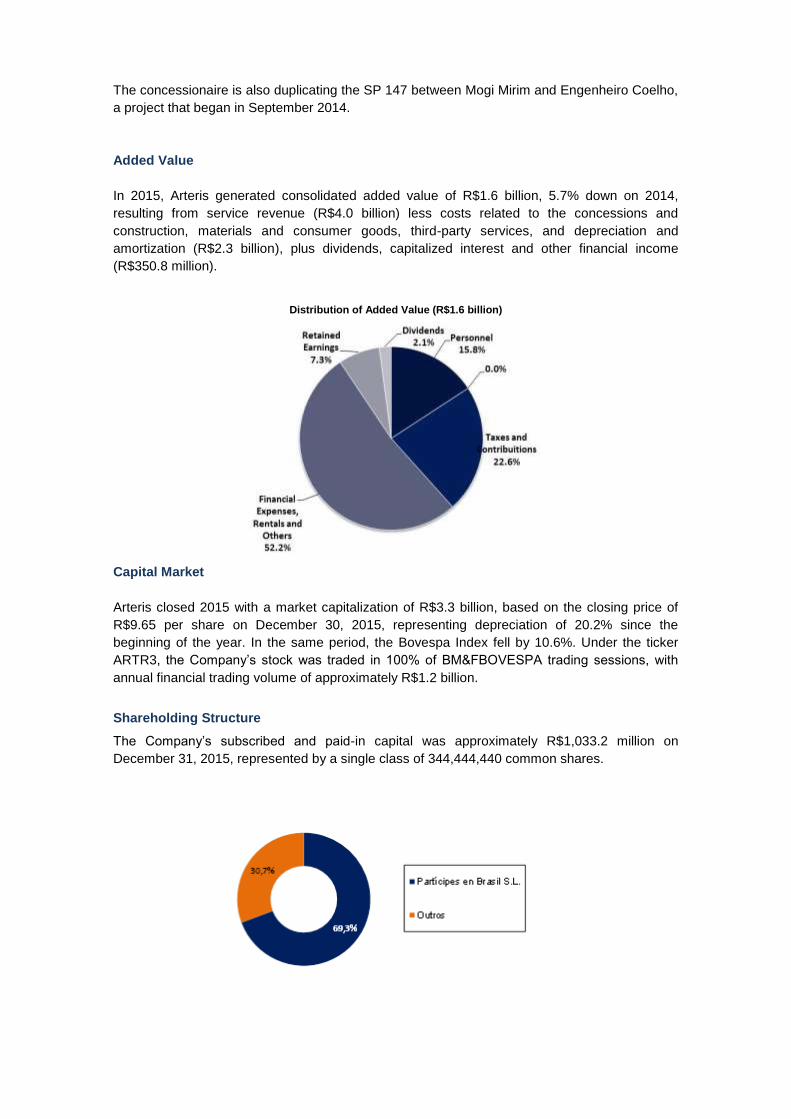

Added Value

In 2015, Arteris generated consolidated added value of R$1.6 billion, 5.7% down on 2014,

resulting from service revenue (R$4.0 billion) less costs related to the concessions and

construction, materials and consumer goods, third-party services, and depreciation and

amortization (R$2.3 billion), plus dividends, capitalized interest and other financial income

(R$350.8 million).

Distribution of Added Value (R$1.6 billion)

Capital Market

Arteris closed 2015 with a market capitalization of R$3.3 billion, based on the closing price of

R$9.65 per share on December 30, 2015, representing depreciation of 20.2% since the

beginning of the year. In the same period, the Bovespa Index fell by 10.6%. Under the ticker

ARTR3, the Company’s stock was traded in 100% of BM&FBOVESPA trading sessions, with

annual financial trading volume of approximately R$1.2 billion.

Shareholding Structure

The Company’s subscribed and paid-in capital was approximately R$1,033.2 million on

December 31, 2015, represented by a single class of 344,444,440 common shares.

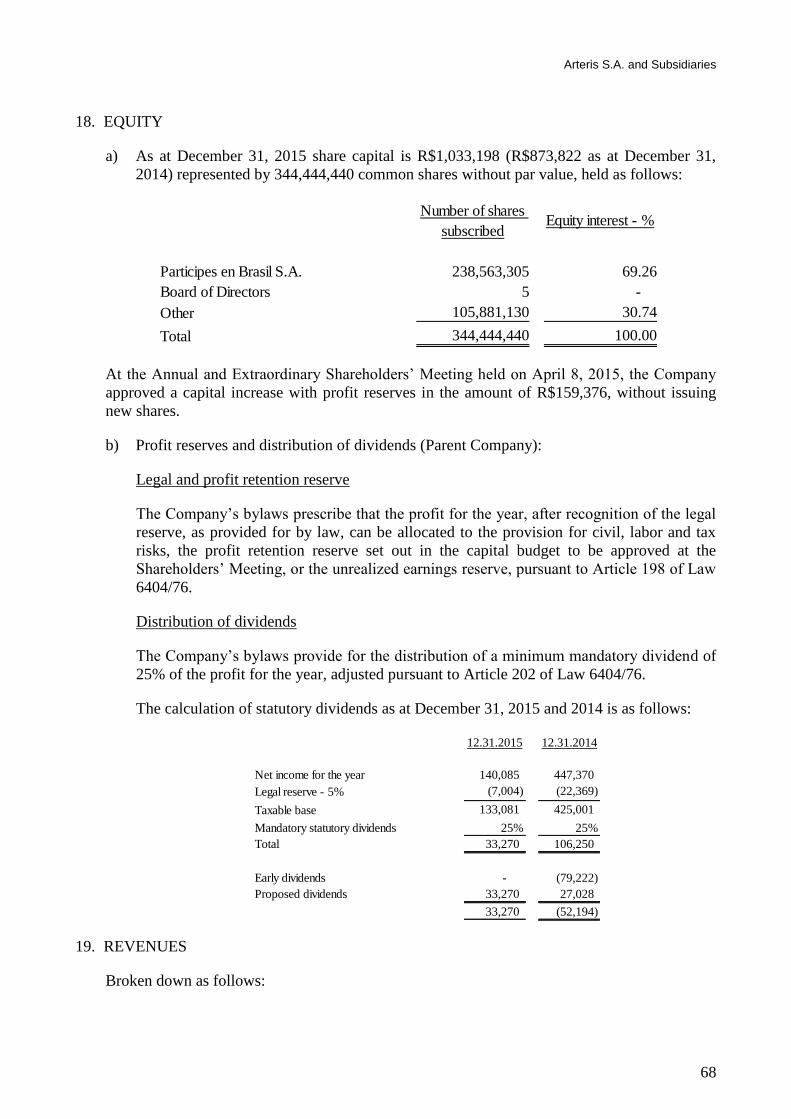

Dividends

Shareholders are entitled to receive minimum mandatory dividends of 25% of annual net

income, adjusted in accordance with Article 202 of Brazilian Corporation Law.

The Company paid dividends of R$106.2 million on 2014 net income, corresponding to R$0.31

per share and representing a payout of 25%.

The Company did not pay interim dividends on net income for the fiscal year ended December

31, 2015. The payment of dividends for 2015 will be resolved at the Annual Shareholders’

Meeting, to be held on April 29, 2016.

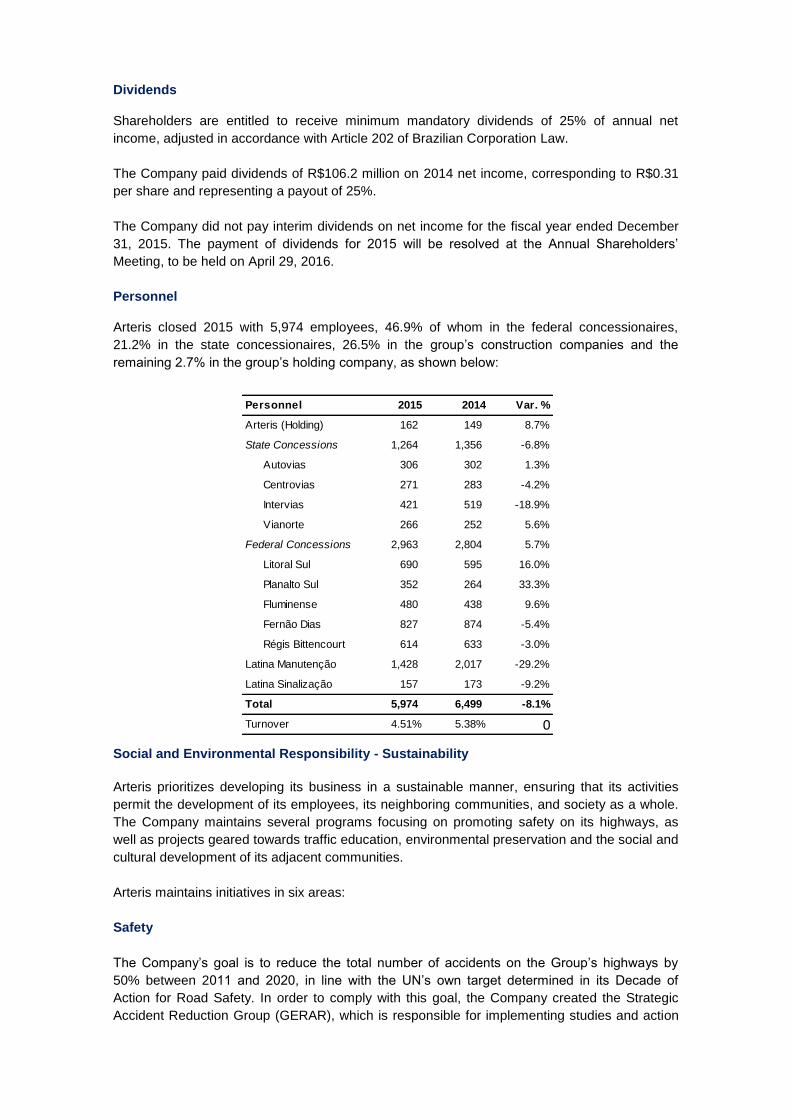

Personnel

Arteris closed 2015 with 5,974 employees, 46.9% of whom in the federal concessionaires,

21.2% in the state concessionaires, 26.5% in the group’s construction companies and the

remaining 2.7% in the group’s holding company, as shown below:

Social and Environmental Responsibility - Sustainability

Arteris prioritizes developing its business in a sustainable manner, ensuring that its activities

permit the development of its employees, its neighboring communities, and society as a whole.

The Company maintains several programs focusing on promoting safety on its highways, as

well as projects geared towards traffic education, environmental preservation and the social and

cultural development of its adjacent communities.

Arteris maintains initiatives in six areas:

Safety

The Company’s goal is to reduce the total number of accidents on the Group’s highways by

50% between 2011 and 2020, in line with the UN’s own target determined in its Decade of

Action for Road Safety. In order to comply with this goal, the Company created the Strategic

Accident Reduction Group (GERAR), which is responsible for implementing studies and action

Personnel 2015 2014 Var. %

Arteris (Holding) 162 149 8.7%

State Concessions 1,264 1,356 -6.8%

Autovias 306 302 1.3%

Centrovias 271 283 -4.2%

Intervias 421 519 -18.9%

Vianorte 266 252 5.6%

Federal Concessions 2,963 2,804 5.7%

Litoral Sul 690 595 16.0%

Planalto Sul 352 264 33.3%

Fluminense 480 438 9.6%

Fernão Dias 827 874 -5.4%

Régis Bittencourt 614 633 -3.0%

Latina Manutenção 1,428 2,017 -29.2%

Latina Sinalização 157 173 -9.2%

Total 5,974 6,499 -8.1%

Turnover 4.51% 5.38% 0

plans to preserve life in traffic. Since September 2014, the Company has been holding the

Arteris Safety Month, a pioneer initiative in the highway concession sector to raise the

awareness of drivers, employees and society in general of the importance of remaining

conscientious in traffic. In 2015, the initiative raised the awareness of nearly one million people

and began with the 2nd

Arteris Safety Forum, with the presence of representatives from

transport regulation agencies, the Ministry of Health, highway police authorities, research

institutions and NGOs.

Education

Traffic humanization is the Company’s priority in the education area, exemplified by the School

Project (Projeto Escola), a 15-year initiative that prepares teachers for the adoption of traffic

safety activities with public school students. The initiative is recognized as good practice by

UNICEF (United Nations Children’s Fund). The same strategy is used to prepare these teachers

in relation to environmental issues through the Long Live Environment program (Viva Meio

Ambiente).

The Company also develops specific initiatives through the Passarela Viva (for pedestrians in

the adjacent communities), Viva Ciclista and Viva Motociclista programs in order to raise the

awareness of these users on the importance of adopting a responsible attitude in traffic.

Health

The Saúde na Boleia program has already benefited more than 100,000 truck drivers through

provision of advice on health and safety, as well as free medical exams and vaccination

programs. The objective of this initiative is to raise professional drivers’ awareness of the need

to preserve their quality of life, since they frequently lack appropriate conditions to take care of

their health. The program has a preventive approach, which encourages them to undergo

medical exams.

The Environment

Business sustainability is a priority for Arteris, influencing the way the Company carries out the

infrastructure works estimated in the concession agreements. Arteris develops projects related

to reforestation and the recovery of degraded areas, the planting of native tree seedlings and

environmental education initiatives in the surrounding communities. The Environmental

Management System is the mechanism through which Arteris and its concessionaires monitor

the execution of initiatives in this area. It also controls and recycles garbage, and maintains

agreements with several state and federal universities to control wildlife.

Cultural, social and sporting projects

The Company prioritizes the sponsorship of important sporting, cultural, social and health

projects in the regions where its concessionaires operate, and promotes partnerships with

leading cultural institutions to sponsor exhibitions by internationally renowned artists in Brazil. In

2014, it sponsored a Salvador Dalí exhibition, the most complete exhibition of his work ever to

come to Brazil. Shown in Rio de Janeiro and São Paulo, it attracted more than 1.5 million

visitors. In 2015, an exhibition of the work of Joan Miró was shown in São Paulo and

Florianópolis. The Company also formed partnerships with institutions that care for children with

special needs as well as other organizations, so that people who normally would not have

access to this type of cultural event, could attend the exhibition.

Volunteer Program

The Company’s employees are encouraged to maintain close relations with their surrounding

communities by developing a transformational approach in order to help build a more just

society. At the same time as it helps develop employees’ personal skills, the initiative also adds

value to the business and strengthens the Company’s image.

Arbitration Clause

The Company is subject to arbitration under the Market Arbitration Chamber, pursuant to the

arbitration clause in its Bylaws.

Final Considerations Relations with the Independent Auditors

In accordance with CVM Instruction 381/03, the Company hereby declares that, during the fiscal

year ended December 31, 2015, it did not hire Deloitte Touche Tohmatsu Auditores

Independentes for any services beyond those related to the external audit. In its relations with

the independent auditors, the Company seeks to evaluate conflicts of interest in regard to non-

audit-related services based on the following precepts: the auditors must not (a) audit their own

work, (b) exercise managerial functions in the Company or (c) promote the Company’s interests.

Declaration by the Board of Executive Officers Pursuant to Article 25 of CVM Instruction 480/09 of December 7, 2009, the Company’s

executive officers hereby declare that they have discussed, reviewed and are in full agreement

with (i) the opinions expressed in the report drawn up by Deloitte Touche Tohmatsu Auditores

Independentes; and (ii) the financial statements for the fiscal year ended December 31, 2015.

São Paulo, March 29, 2016.

Board of Executive Officers David Antonio Díaz Almazán Chief Executive Officer Felipe Ezquerra Plasencia Vice Chief Executive Officer and Administrative and Finance Officer Alessandro Scotoni Levy Investor Relations Officer Maria de Castro Michielin Legal Officer Angelo Luiz Lodi Executive Officer Paulo Pacheco Fernandes Executive Officer Board of Directors

Luiz Ildefonso Simões Lopes Chairman Benjamin Michael Vaughan Member David Antonio Díaz Almazan Member Eduardo de Salles Bartolomeo Independent Member Fernando Martinez Caro Member Francisco José Aljaro Navarro Member Francisco Miguel Reynés Massanet Member Josep Lluis Giménez Sevilla Member Marta Casas Caba Member Marcos Pinto Almeida Member Sérgio Silva de Freitas Independent Member

Deloitte Touche Tohmatsu

Av. Dr. José Bonifácio Coutinho Nogueira, 150 - 5º andar

Campinas - SP - 13091-611 Brasil

Tel: + 55 (19) 3707-3000

Fax:+ 55 (19) 3707-3001

www.deloitte.com.br

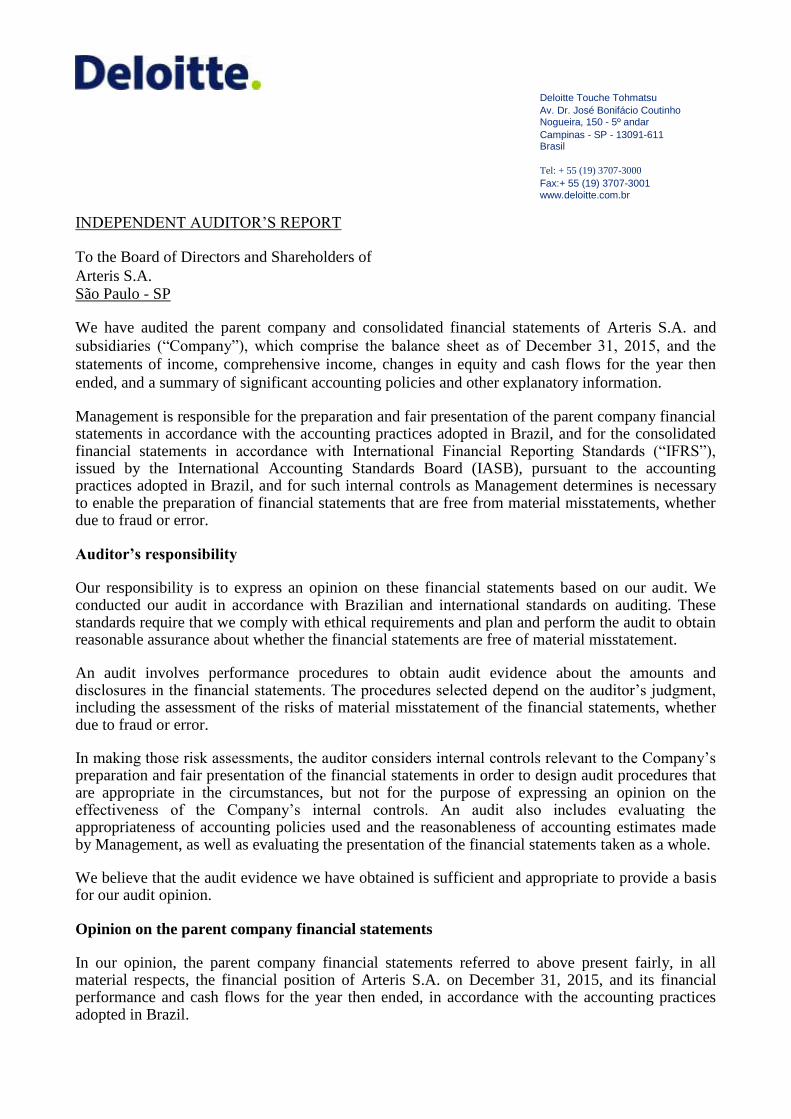

INDEPENDENT AUDITOR’S REPORT

To the Board of Directors and Shareholders of

Arteris S.A. São Paulo - SP

We have audited the parent company and consolidated financial statements of Arteris S.A. and

subsidiaries (“Company”), which comprise the balance sheet as of December 31, 2015, and the

statements of income, comprehensive income, changes in equity and cash flows for the year then

ended, and a summary of significant accounting policies and other explanatory information.

Management is responsible for the preparation and fair presentation of the parent company financial statements in accordance with the accounting practices adopted in Brazil, and for the consolidated financial statements in accordance with International Financial Reporting Standards (“IFRS”), issued by the International Accounting Standards Board (IASB), pursuant to the accounting practices adopted in Brazil, and for such internal controls as Management determines is necessary to enable the preparation of financial statements that are free from material misstatements, whether due to fraud or error.

Auditor’s responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Brazilian and international standards on auditing. These standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement.

An audit involves performance procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error.

In making those risk assessments, the auditor considers internal controls relevant to the Company’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal controls. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by Management, as well as evaluating the presentation of the financial statements taken as a whole.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion on the parent company financial statements

In our opinion, the parent company financial statements referred to above present fairly, in all material respects, the financial position of Arteris S.A. on December 31, 2015, and its financial performance and cash flows for the year then ended, in accordance with the accounting practices adopted in Brazil.

© 2016 Deloitte Touche Tohmatsu. All rights reserved. 3

Opinion on the consolidated financial statements

In our opinion, the consolidated financial statements referred to above present fairly, in all material

respects, the consolidated financial position of Arteris S.A. on December 31, 2015, and its

consolidated financial performance and its consolidated cash flows for the year then ended, in

accordance with International Financial Reporting Standards (“IFRS”), issued by the International

Accounting Standards Board (IASB) and the accounting practices adopted in Brazil.

Emphasis of matter

As described in Note 3, the parent company financial statements were prepared in accordance with

accounting practices adopted in Brazil, which, in the case of Arteris S.A., differ from IFRS, which

applies to the parent company financial statements, only with respect to the option to maintain the

balance of deferred assets on December 31, 2008, which is being amortized. Our opinion on this

matter is unqualified.

Other matters

Statements of value added

We have also audited the parent company and consolidated statements of value added (DVA) for

the year ended December 31, 2015, prepared under the responsibility of the Company’s

Management, the disclosure of which is required by Brazilian Corporation Law for publicly-held

companies, and considered as additional information under the IFRS, which do not require this

disclosure. These statements were submitted to the same audit procedures previously described

and, based on our opinion, they are fairly presented, in all material respects, in line with the

financial statements taken as a whole.

Audit of figures corresponding to the prior year

The figures corresponding to the parent company and consolidated financial statement for the year

ended December 31, 2014, originally prepared prior to the reclassifications carried out in the

statements of consolidated cash flows described in Note 5, were audited by other auditors, who

issued an audit report containing an emphasis of matter paragraph regarding the fact that the parent

company financial statements were prepared in accordance with the accounting practices adopted in

Brazil which, in the case of Arteris S.A., differ from the IFRS only with respect to the option to

maintain the balance of deferred assets, which has been amortized, existing on December 31, 2009,

dated February 25, 2015. As part of our audit of the parent company and consolidated financial

statements for 2015, we have also audited the reclassifications described in Note 5, carried out to

change the consolidated financial statements of December 31, 2014. We have not been engaged to

audit, review or apply any other procedures to the parent company and consolidated financial

statements for 2014 and, therefore, we do not expresses an opinion or any other form of assurance

on the 2014 parent company and consolidated financial statements taken as a whole.

Campinas, March 29, 2016

DELOITTE TOUCHE TOHMATSU Edgar Jabbour

Auditores Independentes Engagement Partner

CRC n. 2 SP 011609/O-8 CRC n. 1 SP 156465/O-9

2

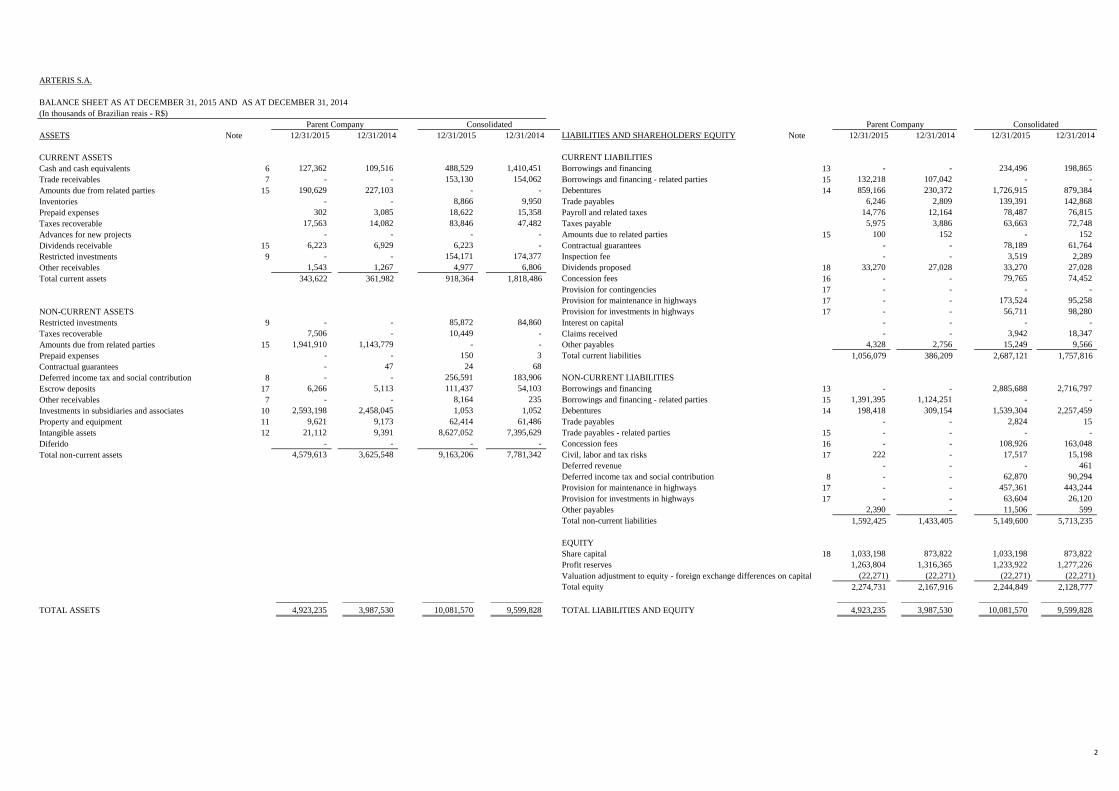

ARTERIS S.A.

(In thousands of Brazilian reais - R$)

ASSETS Note 12/31/2015 12/31/2014 12/31/2015 12/31/2014 LIABILITIES AND SHAREHOLDERS' EQUITY Note 12/31/2015 12/31/2014 12/31/2015 12/31/2014

CURRENT ASSETS CURRENT LIABILITIESCash and cash equivalents 6 127,362 109,516 488,529 1,410,451 Borrowings and financing 13 - - 234,496 198,865 Trade receivables 7 - - 153,130 154,062 Borrowings and financing - related parties 15 132,218 107,042 - - Amounts due from related parties 15 190,629 227,103 - - Debentures 14 859,166 230,372 1,726,915 879,384 Inventories - - 8,866 9,950 Trade payables 6,246 2,809 139,391 142,868 Prepaid expenses 302 3,085 18,622 15,358 Payroll and related taxes 14,776 12,164 78,487 76,815 Taxes recoverable 17,563 14,082 83,846 47,482 Taxes payable 5,975 3,886 63,663 72,748 Advances for new projects - - - - Amounts due to related parties 15 100 152 - 152 Dividends receivable 15 6,223 6,929 6,223 - Contractual guarantees - - 78,189 61,764 Restricted investments 9 - - 154,171 174,377 Inspection fee - - 3,519 2,289 Other receivables 1,543 1,267 4,977 6,806 Dividends proposed 18 33,270 27,028 33,270 27,028 Total current assets 343,622 361,982 918,364 1,818,486 Concession fees 16 - - 79,765 74,452

Provision for contingencies 17 - - - - Provision for maintenance in highways 17 - - 173,524 95,258

NON-CURRENT ASSETS Provision for investments in highways 17 - - 56,711 98,280 Restricted investments 9 - - 85,872 84,860 Interest on capital - - - - Taxes recoverable 7,506 - 10,449 - Claims received - - 3,942 18,347 Amounts due from related parties 15 1,941,910 1,143,779 - - Other payables 4,328 2,756 15,249 9,566 Prepaid expenses - - 150 3 Total current liabilities 1,056,079 386,209 2,687,121 1,757,816Contractual guarantees - 47 24 68 Deferred income tax and social contribution 8 - - 256,591 183,906 NON-CURRENT LIABILITIESEscrow deposits 17 6,266 5,113 111,437 54,103 Borrowings and financing 13 - - 2,885,688 2,716,797 Other receivables 7 - - 8,164 235 Borrowings and financing - related parties 15 1,391,395 1,124,251 - - Investments in subsidiaries and associates 10 2,593,198 2,458,045 1,053 1,052 Debentures 14 198,418 309,154 1,539,304 2,257,459 Property and equipment 11 9,621 9,173 62,414 61,486 Trade payables - - 2,824 15 Intangible assets 12 21,112 9,391 8,627,052 7,395,629 Trade payables - related parties 15 - - - - Diferido - - - - Concession fees 16 - - 108,926 163,048 Total non-current assets 4,579,613 3,625,548 9,163,206 7,781,342 Civil, labor and tax risks 17 222 - 17,517 15,198

Deferred revenue - - - 461 Deferred income tax and social contribution 8 - - 62,870 90,294 Provision for maintenance in highways 17 - - 457,361 443,244 Provision for investments in highways 17 - - 63,604 26,120 Other payables 2,390 - 11,506 599 Total non-current liabilities 1,592,425 1,433,405 5,149,600 5,713,235

EQUITYShare capital 18 1,033,198 873,822 1,033,198 873,822 Profit reserves 1,263,804 1,316,365 1,233,922 1,277,226 Valuation adjustment to equity - foreign exchange differences on capital (22,271) (22,271) (22,271) (22,271) Total equity 2,274,731 2,167,916 2,244,849 2,128,777

TOTAL ASSETS 4,923,235 3,987,530 10,081,570 9,599,828 TOTAL LIABILITIES AND EQUITY 4,923,235 3,987,530 10,081,570 9,599,828

Parent Company Parent Company

BALANCE SHEET AS AT DECEMBER 31, 2015 AND AS AT DECEMBER 31, 2014

Consolidated Consolidated

3

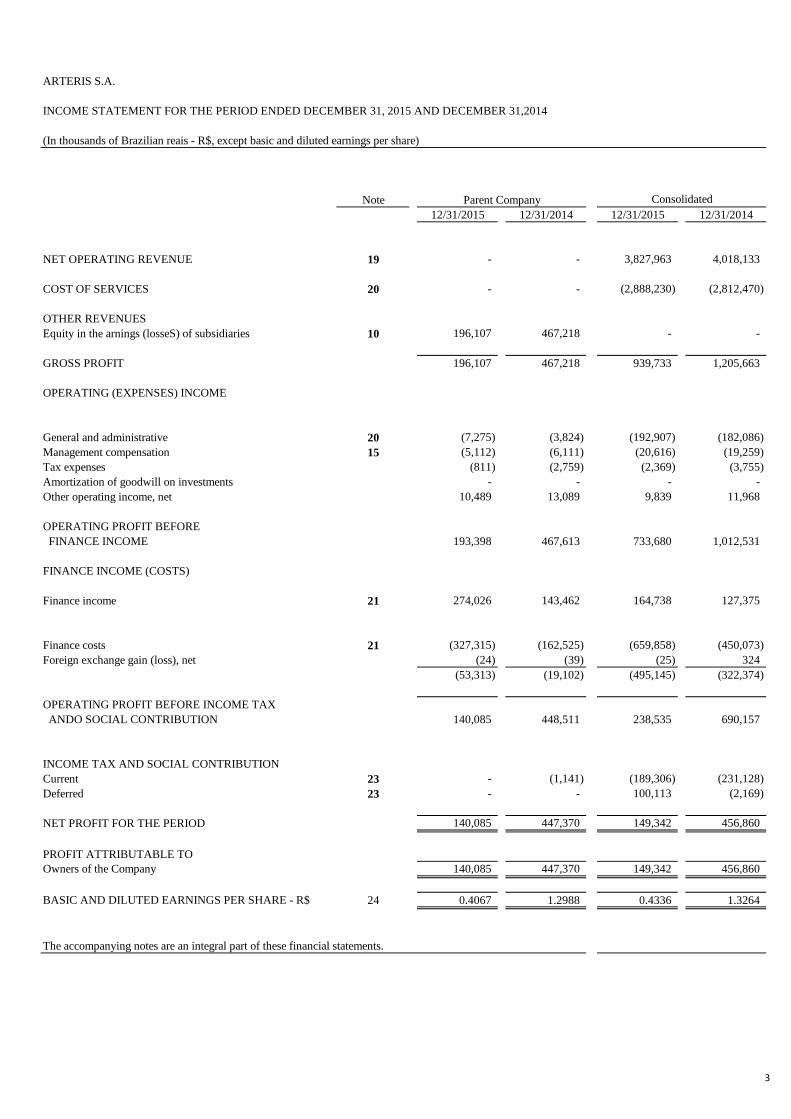

ARTERIS S.A.

INCOME STATEMENT FOR THE PERIOD ENDED DECEMBER 31, 2015 AND DECEMBER 31,2014

(In thousands of Brazilian reais - R$, except basic and diluted earnings per share)

Note12/31/2015 12/31/2014 12/31/2015 12/31/2014

NET OPERATING REVENUE 19 - - 3,827,963 4,018,133

COST OF SERVICES 20 - - (2,888,230) (2,812,470)

OTHER REVENUESEquity in the arnings (losseS) of subsidiaries 10 196,107 467,218 - -

GROSS PROFIT 196,107 467,218 939,733 1,205,663

OPERATING (EXPENSES) INCOME

General and administrative 20 (7,275) (3,824) (192,907) (182,086) Management compensation 15 (5,112) (6,111) (20,616) (19,259) Tax expenses (811) (2,759) (2,369) (3,755) Amortization of goodwill on investments - - - - Other operating income, net 10,489 13,089 9,839 11,968

OPERATING PROFIT BEFORE FINANCE INCOME 193,398 467,613 733,680 1,012,531

FINANCE INCOME (COSTS)

Finance income 21 274,026 143,462 164,738 127,375

Finance costs 21 (327,315) (162,525) (659,858) (450,073) Foreign exchange gain (loss), net (24) (39) (25) 324

(53,313) (19,102) (495,145) (322,374)

OPERATING PROFIT BEFORE INCOME TAX ANDO SOCIAL CONTRIBUTION 140,085 448,511 238,535 690,157

INCOME TAX AND SOCIAL CONTRIBUTIONCurrent 23 - (1,141) (189,306) (231,128) Deferred 23 - - 100,113 (2,169)

NET PROFIT FOR THE PERIOD 140,085 447,370 149,342 456,860

PROFIT ATTRIBUTABLE TOOwners of the Company 140,085 447,370 149,342 456,860

BASIC AND DILUTED EARNINGS PER SHARE - R$ 24 0.4067 1.2988 0.4336 1.3264

The accompanying notes are an integral part of these financial statements.

Parent Company Consolidated

4

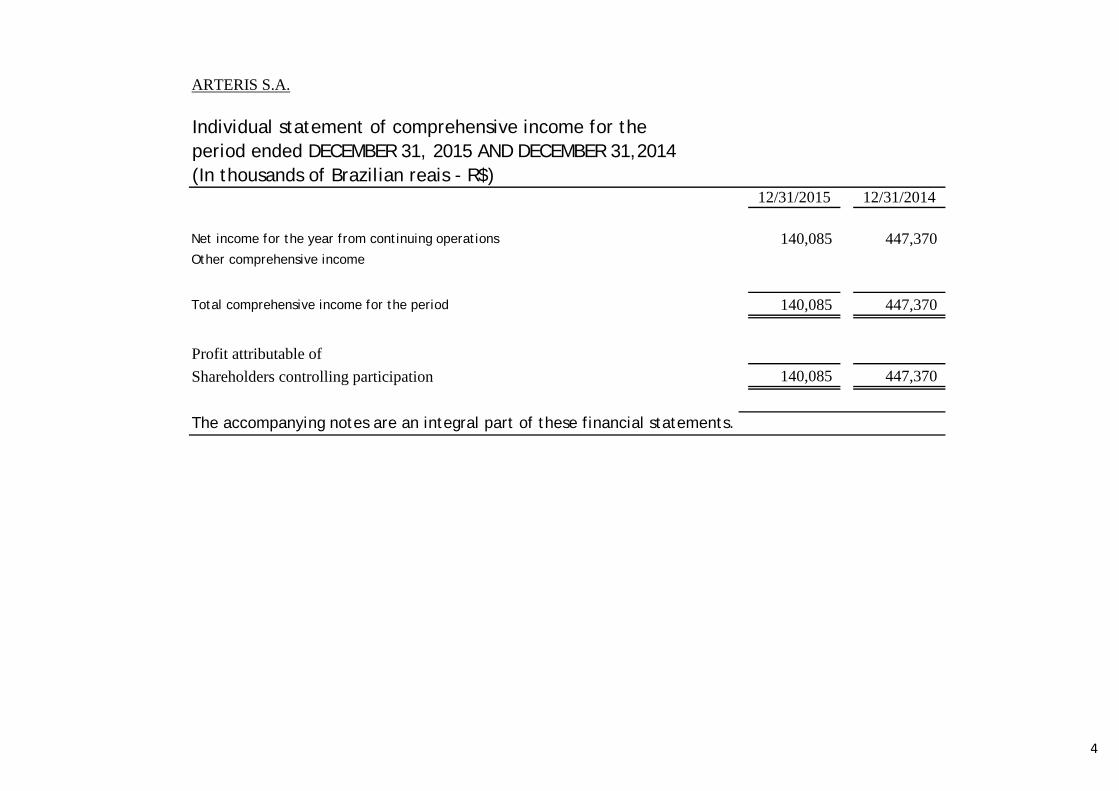

ARTERIS S.A.

Individual statement of comprehensive income for theperiod ended DECEMBER 31, 2015 AND DECEMBER 31,2014(In thousands of Brazilian reais - R$)

12/31/2015 12/31/2014

Net income for the year from continuing operations 140,085 447,370 Other comprehensive income

Total comprehensive income for the period 140,085 447,370

Profit attributable ofShareholders controlling participation 140,085 447,370

The accompanying notes are an integral part of these financial statements.

5

ARTERIS S.A.

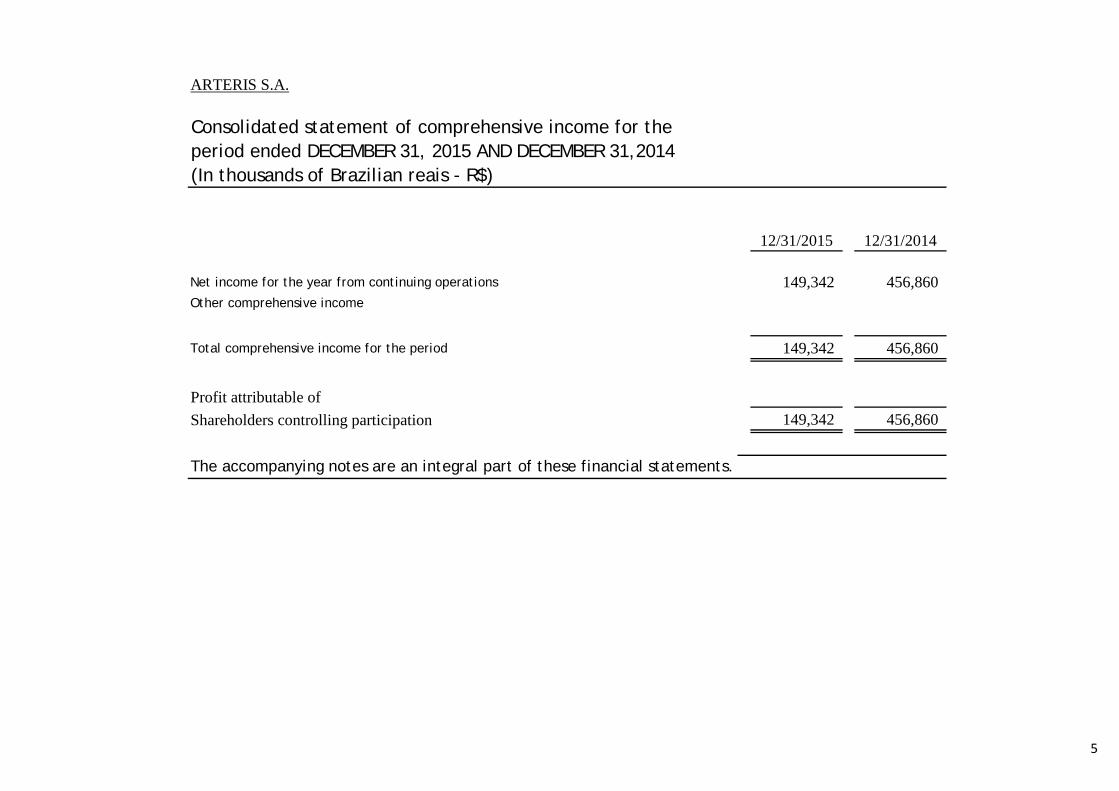

Consolidated statement of comprehensive income for theperiod ended DECEMBER 31, 2015 AND DECEMBER 31,2014(In thousands of Brazilian reais - R$)

12/31/2015 12/31/2014

Net income for the year from continuing operations 149,342 456,860 Other comprehensive income

Total comprehensive income for the period 149,342 456,860

Profit attributable ofShareholders controlling participation 149,342 456,860

The accompanying notes are an integral part of these financial statements.

6

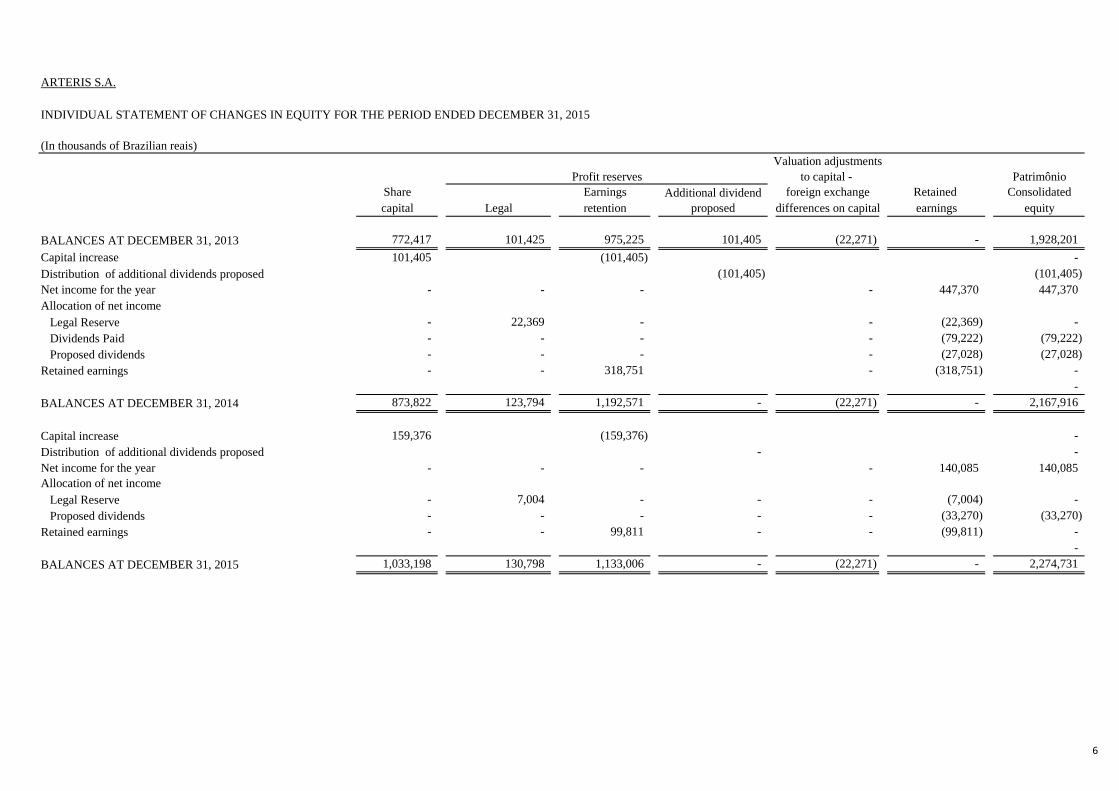

ARTERIS S.A.

(In thousands of Brazilian reais) Valuation adjustments

to capital - PatrimônioShare Earnings foreign exchange Retained Consolidatedcapital Legal retention differences on capital earnings equity

BALANCES AT DECEMBER 31, 2013 772,417 101,425 975,225 101,405 (22,271) - 1,928,201 Capital increase 101,405 (101,405) - Distribution of additional dividends proposed (101,405) (101,405) Net income for the year - - - - 447,370 447,370 Allocation of net income Legal Reserve - 22,369 - - (22,369) - Dividends Paid - - - - (79,222) (79,222) Proposed dividends - - - - (27,028) (27,028) Retained earnings - - 318,751 - (318,751) -

- BALANCES AT DECEMBER 31, 2014 873,822 123,794 1,192,571 - (22,271) - 2,167,916

Capital increase 159,376 (159,376) - Distribution of additional dividends proposed - - Net income for the year - - - - 140,085 140,085 Allocation of net income Legal Reserve - 7,004 - - - (7,004) - Proposed dividends - - - - - (33,270) (33,270) Retained earnings - - 99,811 - - (99,811) -

- BALANCES AT DECEMBER 31, 2015 1,033,198 130,798 1,133,006 - (22,271) - 2,274,731

Additional dividend proposed

Profit reserves

INDIVIDUAL STATEMENT OF CHANGES IN EQUITY FOR THE PERIOD ENDED DECEMBER 31, 2015

7

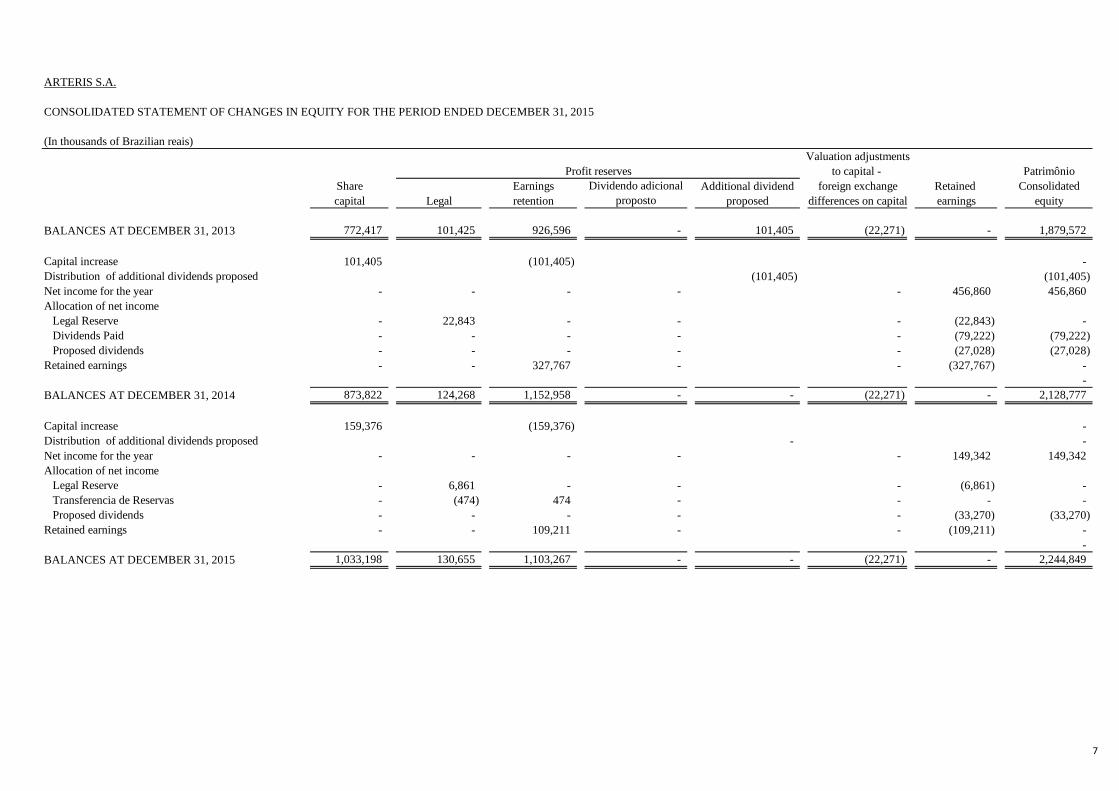

ARTERIS S.A.

(In thousands of Brazilian reais) Valuation adjustments

to capital - PatrimônioShare Earnings foreign exchange Retained Consolidatedcapital Legal retention differences on capital earnings equity

BALANCES AT DECEMBER 31, 2013 772,417 101,425 926,596 - 101,405 (22,271) - 1,879,572

Capital increase 101,405 (101,405) - Distribution of additional dividends proposed (101,405) (101,405) Net income for the year - - - - - 456,860 456,860 Allocation of net income Legal Reserve - 22,843 - - - (22,843) - Dividends Paid - - - - - (79,222) (79,222) Proposed dividends - - - - - (27,028) (27,028) Retained earnings - - 327,767 - - (327,767) -

- BALANCES AT DECEMBER 31, 2014 873,822 124,268 1,152,958 - - (22,271) - 2,128,777

Capital increase 159,376 (159,376) - Distribution of additional dividends proposed - - Net income for the year - - - - - 149,342 149,342 Allocation of net income Legal Reserve - 6,861 - - - (6,861) - Transferencia de Reservas - (474) 474 - - - - Proposed dividends - - - - - (33,270) (33,270) Retained earnings - - 109,211 - - (109,211) -

- BALANCES AT DECEMBER 31, 2015 1,033,198 130,655 1,103,267 - - (22,271) - 2,244,849

Dividendo adicional proposto

Additional dividend proposed

Profit reserves

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY FOR THE PERIOD ENDED DECEMBER 31, 2015

8

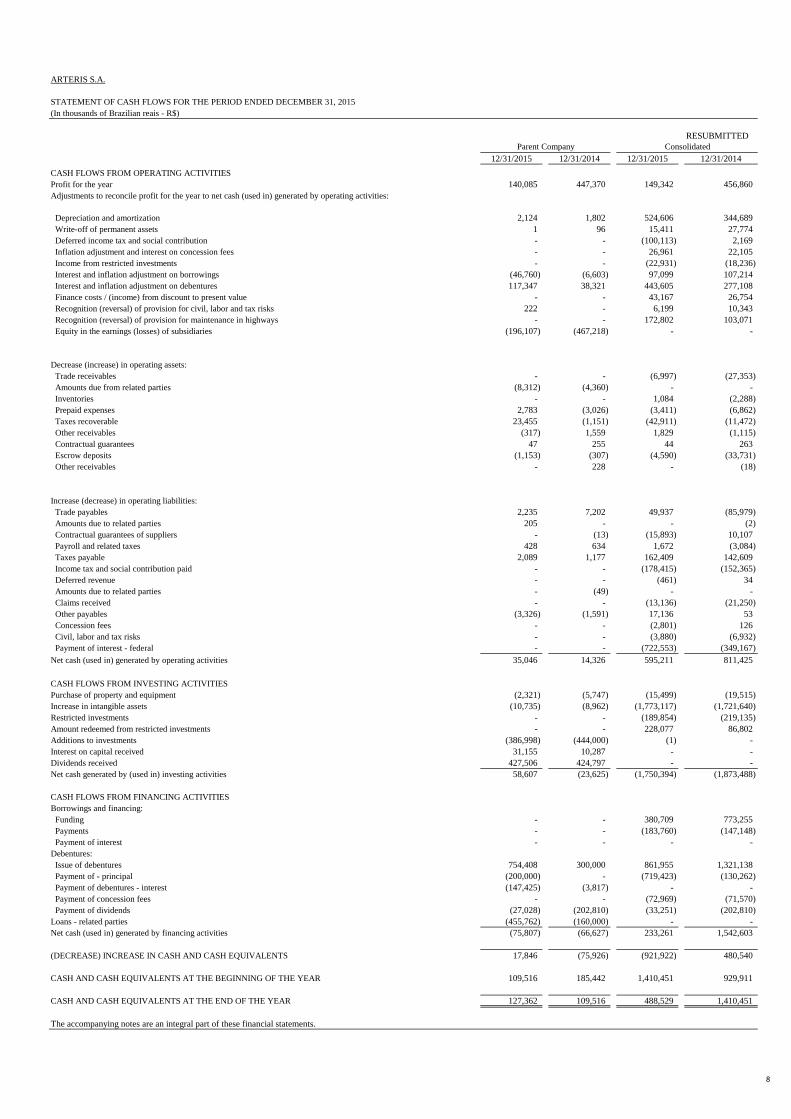

ARTERIS S.A.

STATEMENT OF CASH FLOWS FOR THE PERIOD ENDED DECEMBER 31, 2015(In thousands of Brazilian reais - R$)

RESUBMITTED

12/31/2015 12/31/2014 12/31/2015 12/31/2014CASH FLOWS FROM OPERATING ACTIVITIESProfit for the year 140,085 447,370 149,342 456,860 Adjustments to reconcile profit for the year to net cash (used in) generated by operating activities:

Depreciation and amortization 2,124 1,802 524,606 344,689 Write-off of permanent assets 1 96 15,411 27,774 Deferred income tax and social contribution - - (100,113) 2,169 Inflation adjustment and interest on concession fees - - 26,961 22,105 Income from restricted investments - - (22,931) (18,236) Interest and inflation adjustment on borrowings (46,760) (6,603) 97,099 107,214 Interest and inflation adjustment on debentures 117,347 38,321 443,605 277,108 Finance costs / (income) from discount to present value - - 43,167 26,754 Recognition (reversal) of provision for civil, labor and tax risks 222 - 6,199 10,343 Recognition (reversal) of provision for maintenance in highways - - 172,802 103,071 Equity in the earnings (losses) of subsidiaries (196,107) (467,218) - -

Decrease (increase) in operating assets: Trade receivables - - (6,997) (27,353) Amounts due from related parties (8,312) (4,360) - - Inventories - - 1,084 (2,288) Prepaid expenses 2,783 (3,026) (3,411) (6,862) Taxes recoverable 23,455 (1,151) (42,911) (11,472) Other receivables (317) 1,559 1,829 (1,115) Contractual guarantees 47 255 44 263 Escrow deposits (1,153) (307) (4,590) (33,731) Other receivables - 228 - (18)

Increase (decrease) in operating liabilities: Trade payables 2,235 7,202 49,937 (85,979) Amounts due to related parties 205 - - (2) Contractual guarantees of suppliers - (13) (15,893) 10,107 Payroll and related taxes 428 634 1,672 (3,084) Taxes payable 2,089 1,177 162,409 142,609 Income tax and social contribution paid - - (178,415) (152,365) Deferred revenue - - (461) 34 Amounts due to related parties - (49) - - Claims received - - (13,136) (21,250) Other payables (3,326) (1,591) 17,136 53 Concession fees - - (2,801) 126 Civil, labor and tax risks - - (3,880) (6,932) Payment of interest - federal - - (722,553) (349,167) Net cash (used in) generated by operating activities 35,046 14,326 595,211 811,425

CASH FLOWS FROM INVESTING ACTIVITIESPurchase of property and equipment (2,321) (5,747) (15,499) (19,515) Increase in intangible assets (10,735) (8,962) (1,773,117) (1,721,640) Restricted investments - - (189,854) (219,135) Amount redeemed from restricted investments - - 228,077 86,802 Additions to investments (386,998) (444,000) (1) - Interest on capital received 31,155 10,287 - - Dividends received 427,506 424,797 - - Net cash generated by (used in) investing activities 58,607 (23,625) (1,750,394) (1,873,488)

CASH FLOWS FROM FINANCING ACTIVITIESBorrowings and financing: Funding - - 380,709 773,255 Payments - - (183,760) (147,148) Payment of interest - - - - Debentures: Issue of debentures 754,408 300,000 861,955 1,321,138 Payment of - principal (200,000) - (719,423) (130,262) Payment of debentures - interest (147,425) (3,817) - - Payment of concession fees - - (72,969) (71,570) Payment of dividends (27,028) (202,810) (33,251) (202,810) Loans - related parties (455,762) (160,000) - - Net cash (used in) generated by financing activities (75,807) (66,627) 233,261 1,542,603

(DECREASE) INCREASE IN CASH AND CASH EQUIVALENTS 17,846 (75,926) (921,922) 480,540

CASH AND CASH EQUIVALENTS AT THE BEGINNING OF THE YEAR 109,516 185,442 1,410,451 929,911

CASH AND CASH EQUIVALENTS AT THE END OF THE YEAR 127,362 109,516 488,529 1,410,451

The accompanying notes are an integral part of these financial statements.

Parent Company Consolidated

9

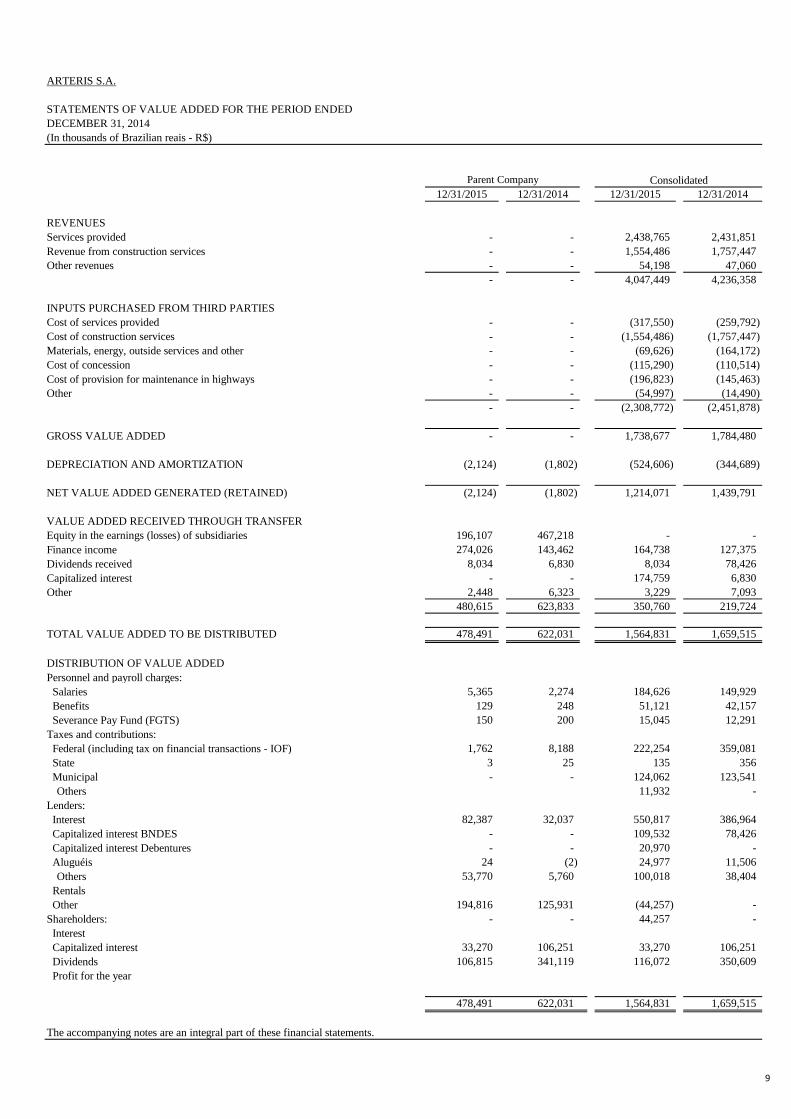

ARTERIS S.A.

STATEMENTS OF VALUE ADDED FOR THE PERIOD ENDEDDECEMBER 31, 2014(In thousands of Brazilian reais - R$)

12/31/2015 12/31/2014 12/31/2015 12/31/2014

REVENUESServices provided - - 2,438,765 2,431,851 Revenue from construction services - - 1,554,486 1,757,447 Other revenues - - 54,198 47,060

- - 4,047,449 4,236,358

INPUTS PURCHASED FROM THIRD PARTIESCost of services provided - - (317,550) (259,792) Cost of construction services - - (1,554,486) (1,757,447) Materials, energy, outside services and other - - (69,626) (164,172) Cost of concession - - (115,290) (110,514) Cost of provision for maintenance in highways - - (196,823) (145,463) Other - - (54,997) (14,490)

- - (2,308,772) (2,451,878)

GROSS VALUE ADDED - - 1,738,677 1,784,480

DEPRECIATION AND AMORTIZATION (2,124) (1,802) (524,606) (344,689)

NET VALUE ADDED GENERATED (RETAINED) (2,124) (1,802) 1,214,071 1,439,791

VALUE ADDED RECEIVED THROUGH TRANSFEREquity in the earnings (losses) of subsidiaries 196,107 467,218 - - Finance income 274,026 143,462 164,738 127,375 Dividends received 8,034 6,830 8,034 78,426 Capitalized interest - - 174,759 6,830 Other 2,448 6,323 3,229 7,093

480,615 623,833 350,760 219,724

TOTAL VALUE ADDED TO BE DISTRIBUTED 478,491 622,031 1,564,831 1,659,515

DISTRIBUTION OF VALUE ADDEDPersonnel and payroll charges: Salaries 5,365 2,274 184,626 149,929 Benefits 129 248 51,121 42,157 Severance Pay Fund (FGTS) 150 200 15,045 12,291 Taxes and contributions: Federal (including tax on financial transactions - IOF) 1,762 8,188 222,254 359,081 State 3 25 135 356 Municipal - - 124,062 123,541

Others 11,932 - Lenders: Interest 82,387 32,037 550,817 386,964 Capitalized interest BNDES - - 109,532 78,426 Capitalized interest Debentures - - 20,970 - Aluguéis 24 (2) 24,977 11,506

Others 53,770 5,760 100,018 38,404 Rentals Other 194,816 125,931 (44,257) - Shareholders: - - 44,257 - Interest Capitalized interest 33,270 106,251 33,270 106,251 Dividends 106,815 341,119 116,072 350,609 Profit for the year

478,491 622,031 1,564,831 1,659,515

The accompanying notes are an integral part of these financial statements.

Parent Company Consolidated

Arteris S.A. and

Subsidiaries

Parent Company and Consolidated

Financia Statements for the Year

Ended December 31, 2015

Deloitte Touche Tohmatsu Auditores Independentes

ARTERIS S.A. AND SUBSIDIARIES

FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31, 2015 AND

INDEPENDENT AUDITOR’S REPORT ON THE FINANCIAL STATEMENTS

TABLE OF CONTENTS

1. OPERATIONS ........................................................................................................................... 10

2. CONCESSIONS ......................................................................................................................... 11

3. BASIS OF PREPARATION ...................................................................................................... 22

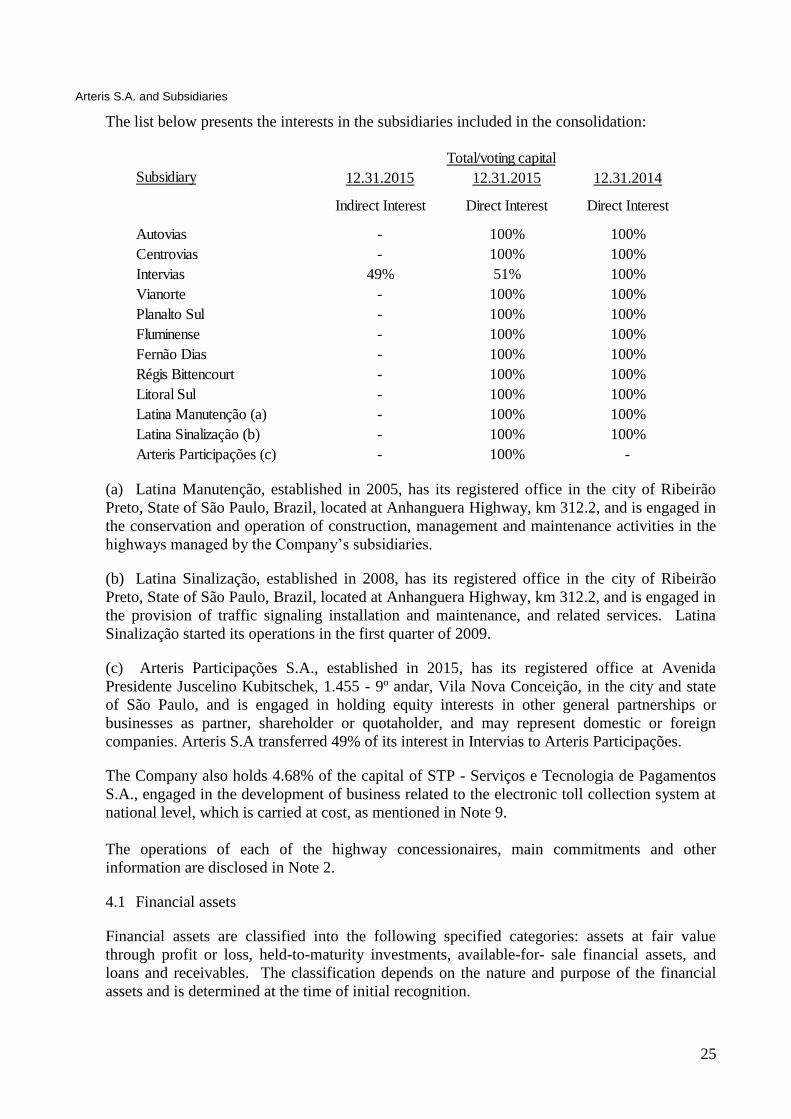

4. SIGNIFICANT ACCOUNTING POLICES .............................................................................. 24

5. RESTATEMENT OF THE STATEMENTS OF CASH FLOWS ............................................. 35

6. CASH AND CASH EQUIVALENTS ....................................................................................... 38

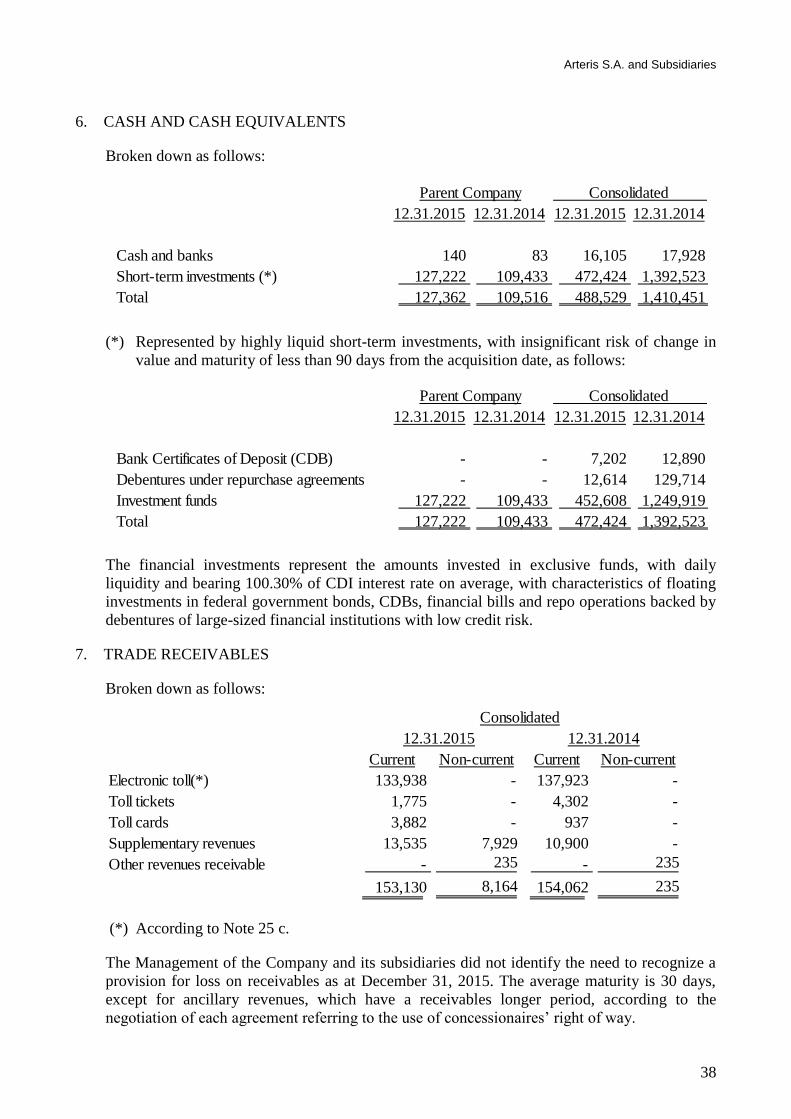

7. TRADE RECEIVABLES ........................................................................................................... 38

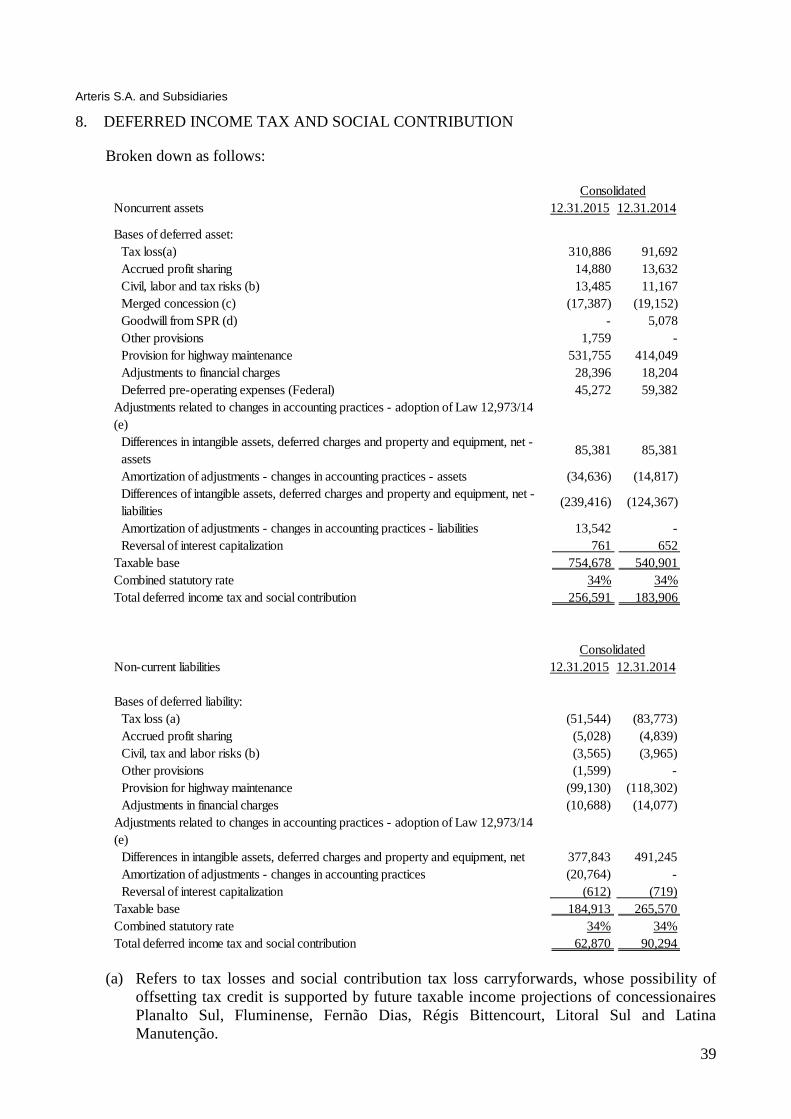

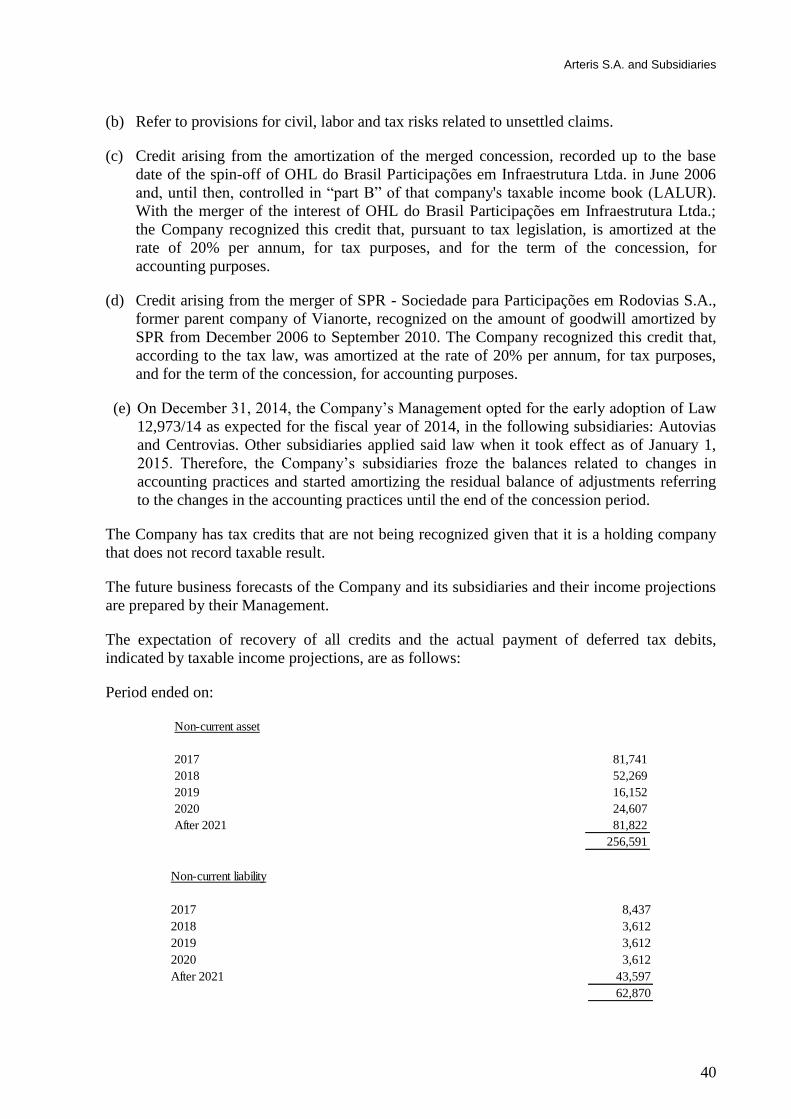

8. DEFERRED INCOME TAX AND SOCIAL CONTRIBUTION ............................................. 39

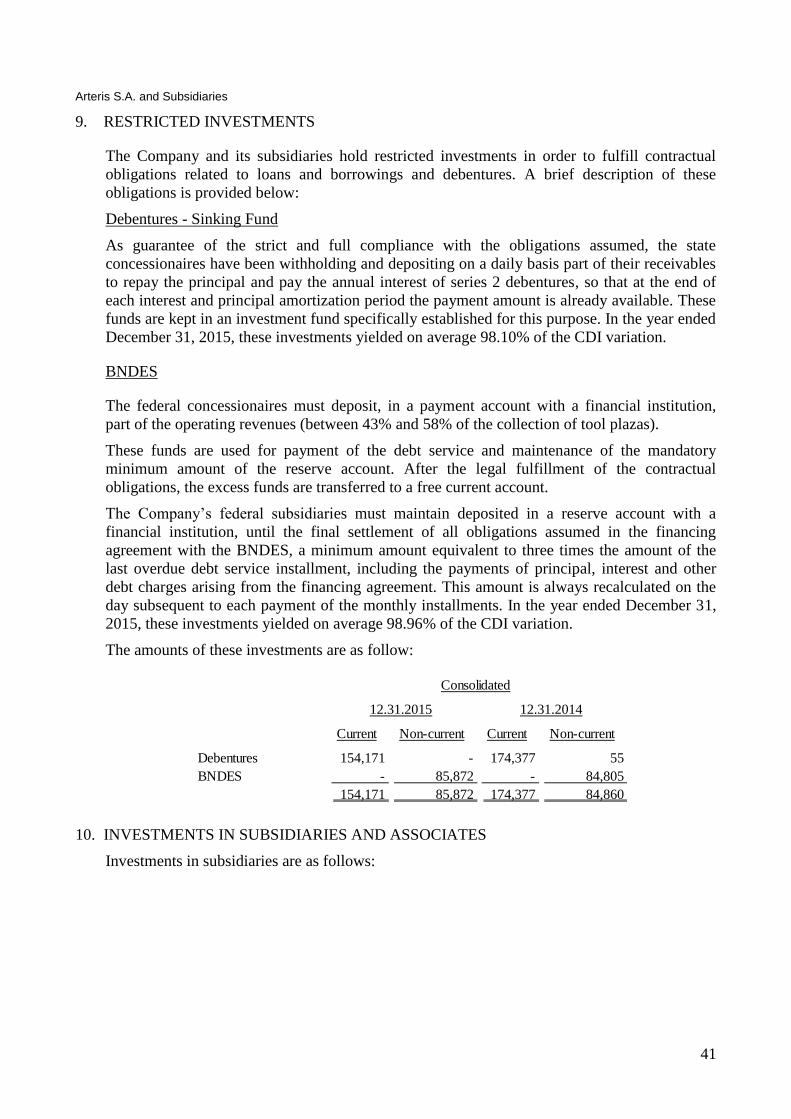

9. RESTRICTED INVESTMENTS ............................................................................................... 41

10. INVESTMENTS IN SUBSIDIARIES AND ASSOCIATES .................................................... 41

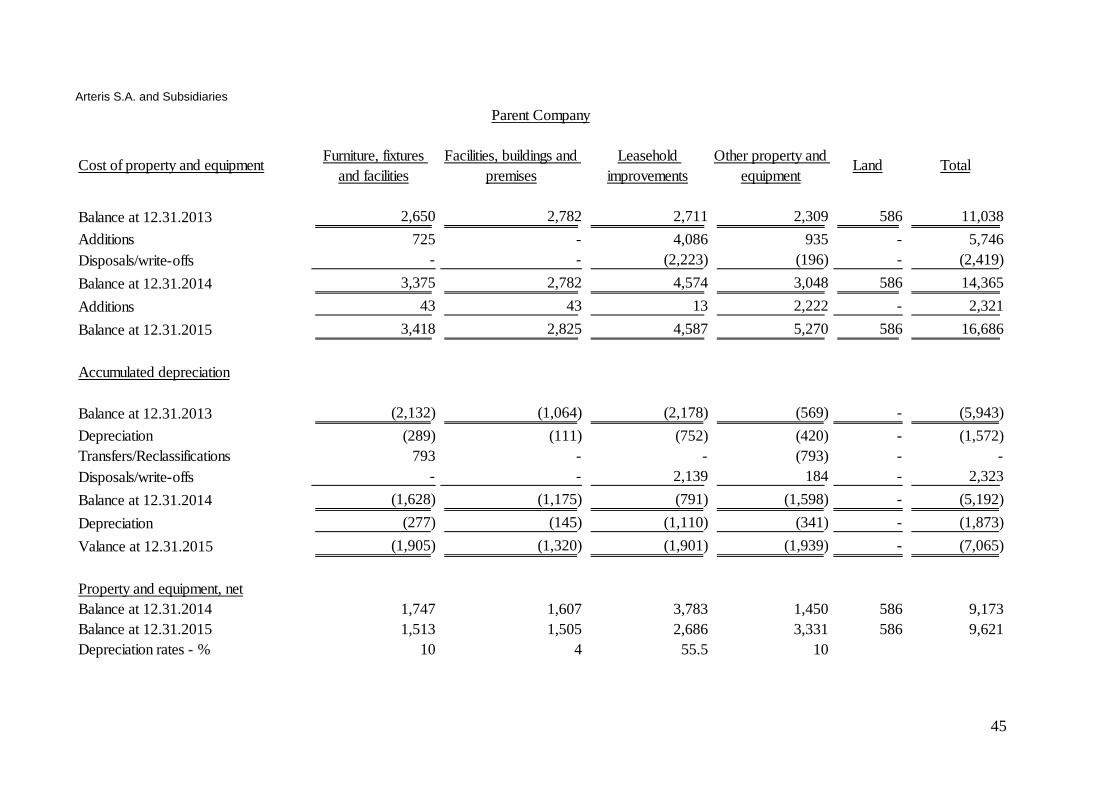

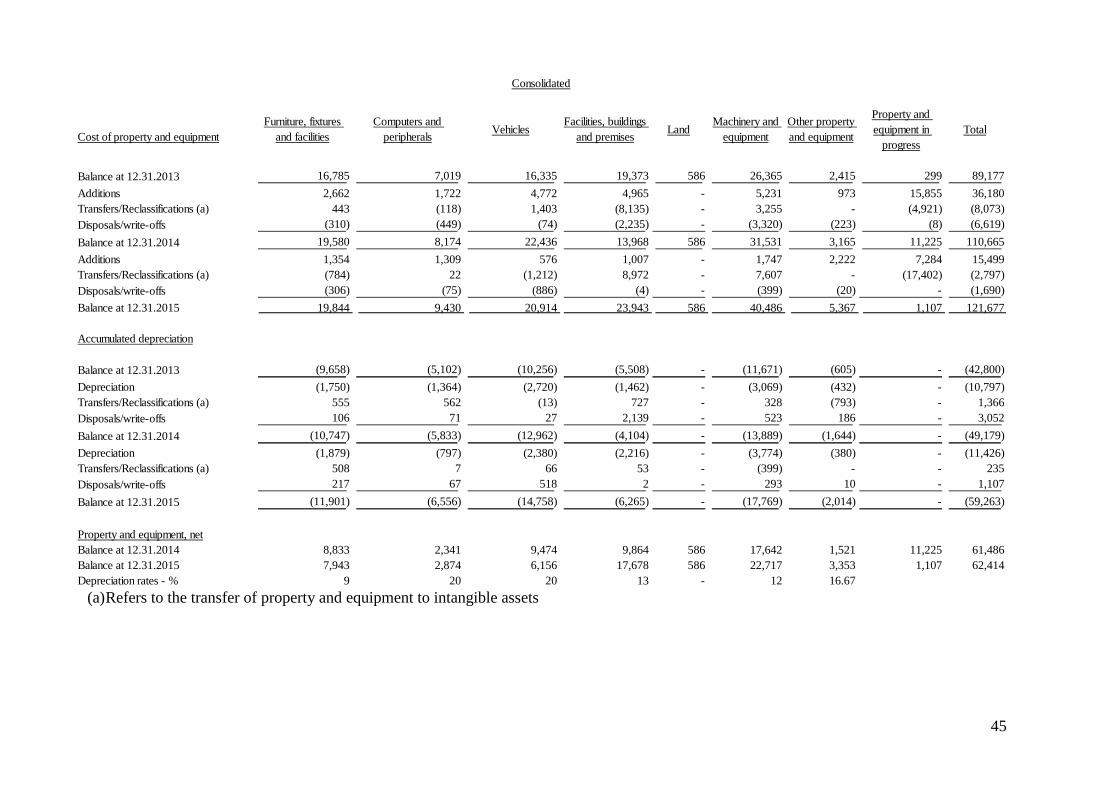

11. PROPERTY AND EQUIPAMENT ........................................................................................... 44

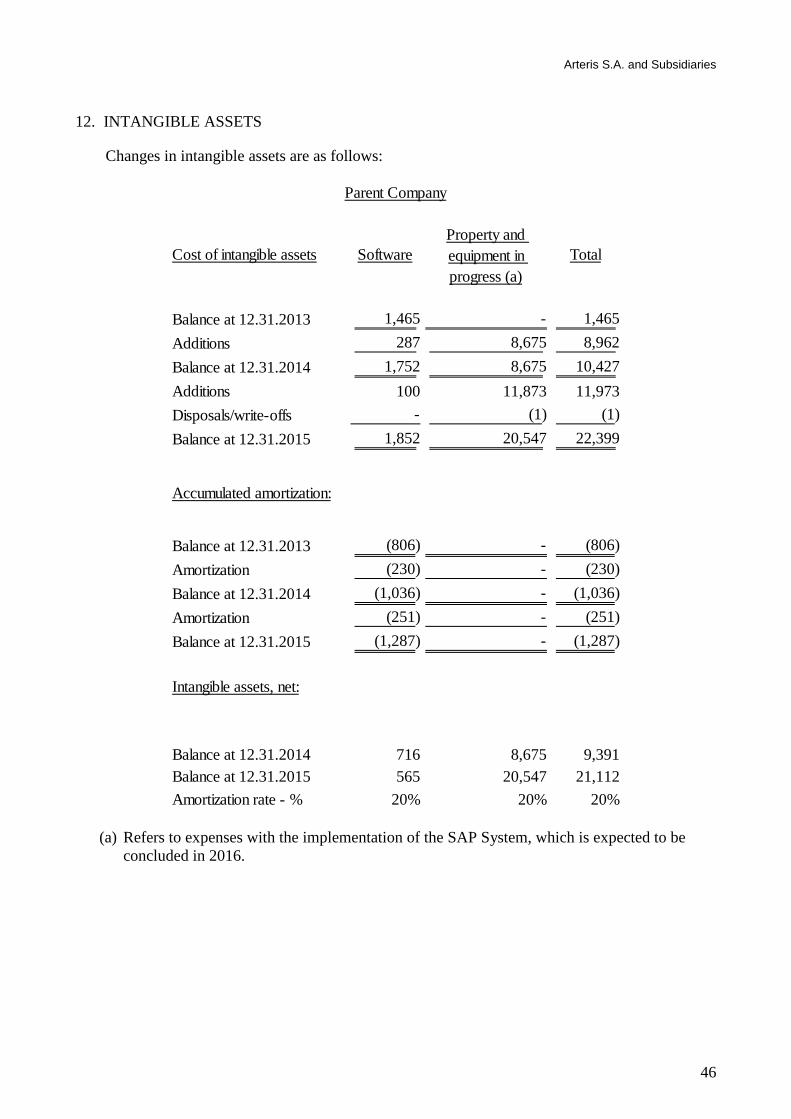

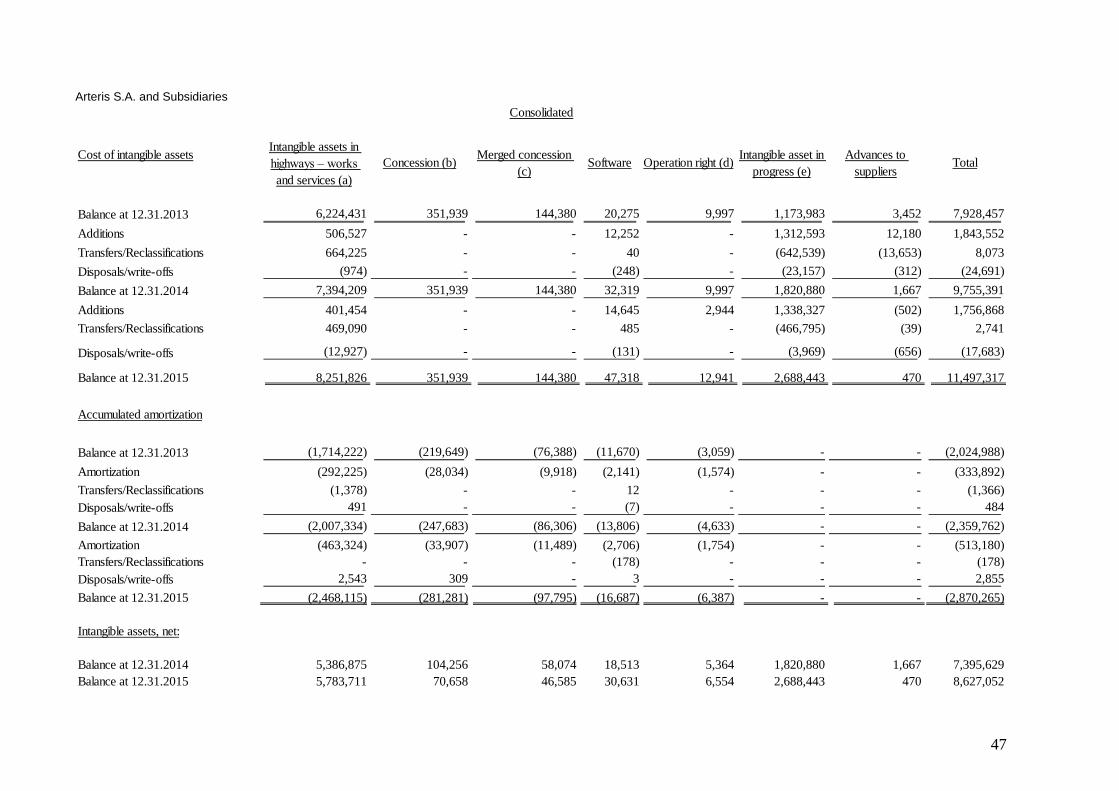

12. INTANGIBLE ASSETS ............................................................................................................ 46

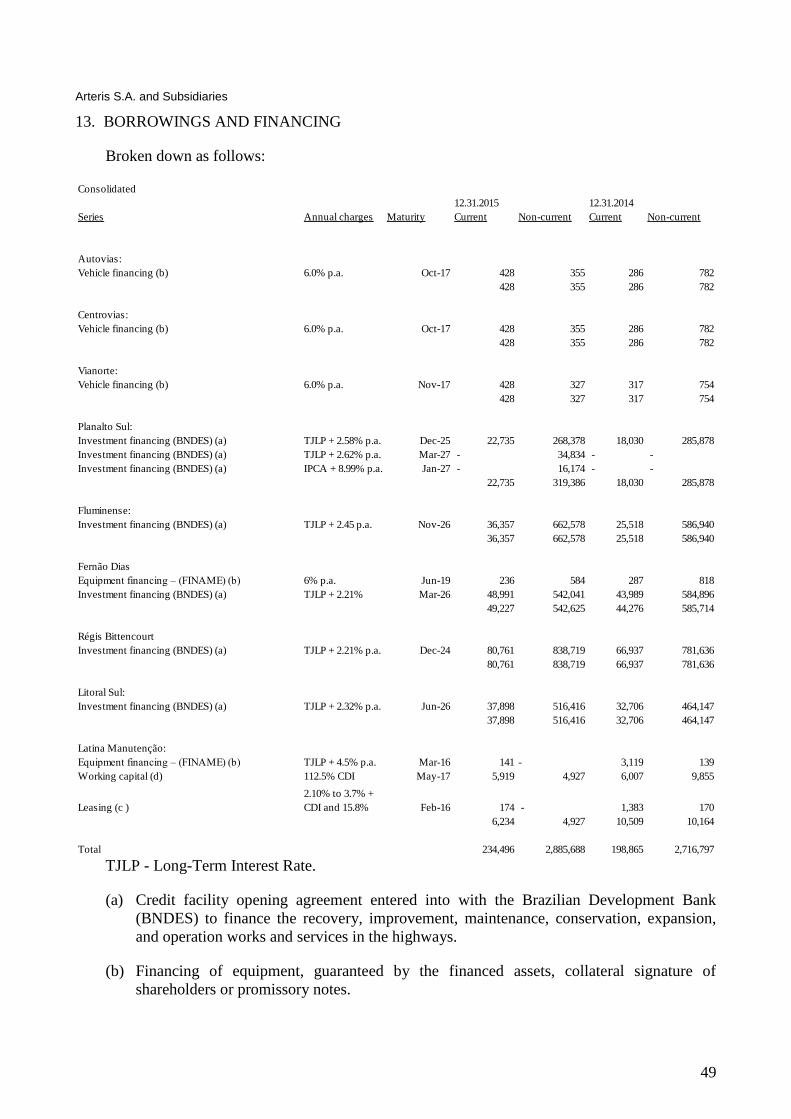

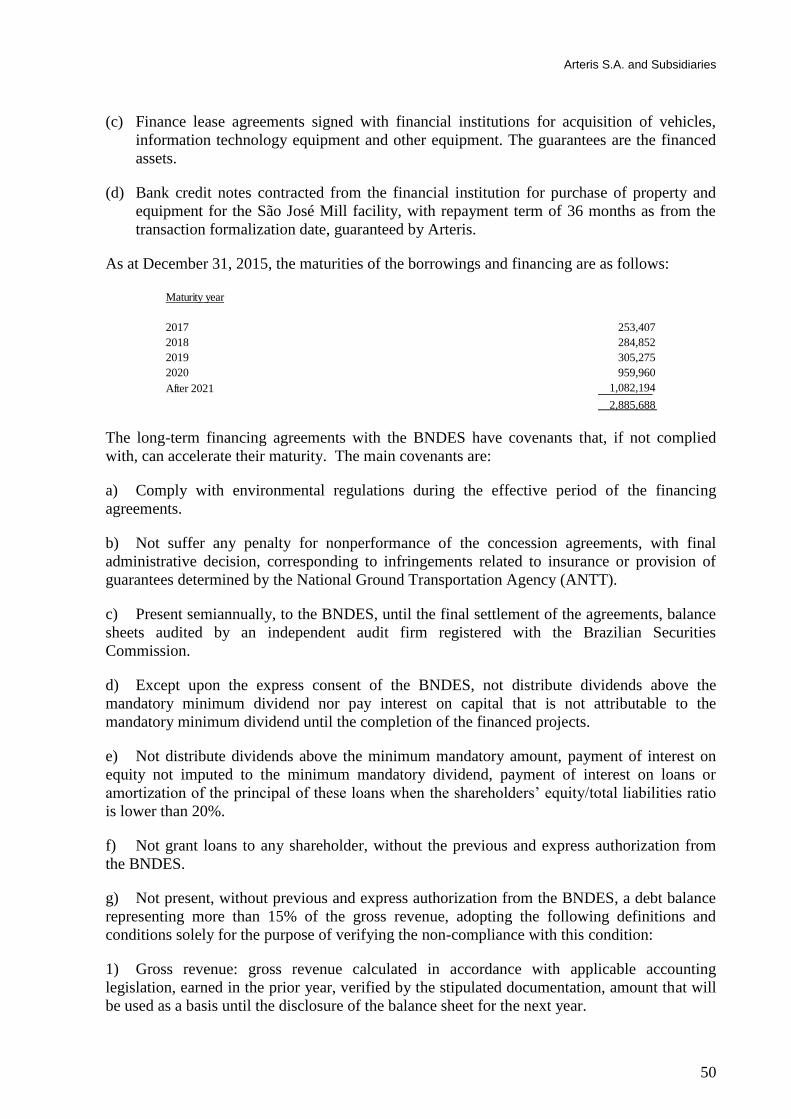

13. BORROWINGS AND FINANCING......................................................................................... 49

14. DEBENTURES .......................................................................................................................... 52

15. RELATED-PARTY TRANSACTIONS .................................................................................... 58

16. CONCESSION FEES ................................................................................................................. 63

17. PROVISIONS............................................................................................................................. 66

18. EQUITY ..................................................................................................................................... 68

19. REVENUES ............................................................................................................................... 68

20. COSTS AND EXPENSES BY NATURE ................................................................................. 70

21. FINANCE INCOME (COSTS) .................................................................................................. 71

22. STATEMENTS OF CASH FLOWS .......................................................................................... 72

23. RECONCILITION OF INCOME TAX AND SOCIAL CONTRIBUTION ............................. 73

24. EARNINGS PER SHARE ......................................................................................................... 74

25. FINANCIAL INSTRUMENTS.................................................................................................. 74

25. SEGMENT REPORTING .......................................................................................................... 77

26. GUARANTEES AND INSURANCES ...................................................................................... 80

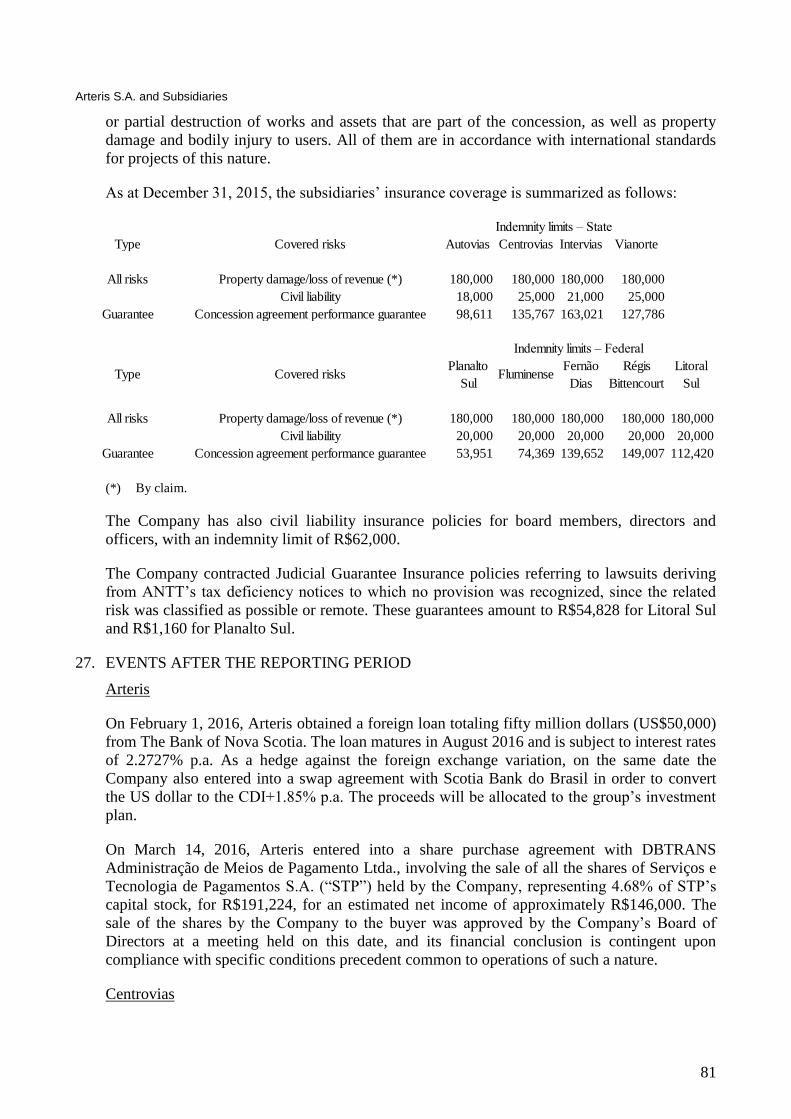

27. EVENTS AFTER THE REPORTING PERIOD ....................................................................... 81

28. MATERIAL FACTS .................................................................................................................. 83

Arteris S.A. and Subsidiaries

10

ARTERIS S.A. AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31, 2015

(Amounts in thousands of Brazilian reais - R$, unless otherwise stated)

1. OPERATIONS

Arteris S.A. (“Company”) has its registered office and principal place of business at Avenida

Presidente Juscelino Kubitschek, 1.455 - 9º andar, in the city of São Paulo, state of São Paulo,

Brazil. The Company’s parent company and consolidated financial statements for the year

ended December 31, 2015 include the Company and its subsidiaries (collectively referred to as

“Arteris Group” and individually as “Group entity”). The Company was established on

November 9, 1998 and is primarily engaged in:

• Execution by means of management, contracting or subcontracting of construction works,

including ancillary or complementary services, except the supply by the Company of

merchandise outside the location where the services are provided.

• Conducting of studies, calculations, projects, tests and supervision related to engineering and

civil construction activities.

• Performance of infrastructure works in general, including, without restriction, construction

services, earthworks in general, signaling, reinforcement, improvement, recovery, maintenance

and conservation of highways, and engineering consultancy in general.

• Direct operation and/or operation in consortiums of businesses relating to public construction

works and/or services in the infrastructure sector in general, by means of any agreement mode,

including, but not limited to, public-private partnerships, authorizations, permissions and

concessions.

• Operation and maintenance of transportation infrastructure in general.

• Holding of equity interests in other companies that develop the activities previously mentioned.

Arteris, through its subsidiaries, mainly state concessionaires, has a solid cash position, robust

capital structure and special funding sources to implement its business plan.

The Company allocates the resources generated by operating activities to meet its working

capital needs. Additionally, it accesses the capital markets and raises loans and financing with

Brazil’s major financial institutions and development agencies to complete its cash needs.

Cash generation, added to the Company’s creditworthiness, besides the funds raised through

long-term financing lines is appropriate to comply with its short-term liabilities recorded under

current liabilities, which includes the financing amortization and to maintain an appropriate

leverage level for long-term liabilities.

Once its subsidiaries’ revenue projections in the medium and long terms indicate upward and

sustainable levels through the toll traffic involvement and annual tariff increases, at the same

time the work plan is supported by the loan with the Brazilian Development Bank (BNDES)

and funds raised in the capital markets by means of the issue of infrastructure debentures or

other securities in its concessionaires and through the Company itself, Management believes

Arteris S.A. and Subsidiaries

11

that the Company and its subsidiaries have conditions to honor their current short and medium

term commitments.

On April 30, 2015, the controlling shareholder Participes em Brasil S.L. informed its intention

to hold a Public Tender Offer for the Acquisition of Arteris S.A. Shares with a view to

cancelling the Company’s registration as a category A publicly-held company and delisting it

from the Novo Mercado. The launch of the offer is contingent upon registration with the

competent regulatory agencies.

On December 31, 2015, the Company was continuing to comply with all the requirements

before the competent regulatory agencies, as described in Note 28.

The parent company and consolidated financial statements were approved by the Board of

Directors on March 29, 2016.

2. CONCESSIONS

In conformity with its corporate purposes, as at December 31, 2015, the Company holds

interests in highway concessionaires in the State of São Paulo and in federal highway

concessionaires.

State concessionaires

Autovias S.A. (“Autovias”)

Autovias is a corporation with its registered office in the city of Ribeirão Preto, State of São

Paulo, Brazil, at Anhanguera Highway, km 312.2, and started its operations on September 1,

1998 to operate, under a concession through August 31, 2018, the highway network connecting

the cities of Franca, Batatais, Ribeirão Preto, Araraquara, São Carlos and Santa Rita do Passa

Quatro and respective access routes, under the terms of the concession agreement entered into

with the São Paulo State Highway Department (DER/SP) No. 18/CIC/97/Lot 10.

By means of Addendum 19/14 of January 16, 2015, the São Paulo State Transportation

Regulatory Agency (“ARTESP” or “Granting Authority”) authorized the rebalance of the

economic and financial adequacy of the concession agreement, which was granted by

extending the concession term for another 3 months and 19 days without changing the

concession fee. Therefore, the concession operation period was extended to December 18,

2018. This term can be extended or reduced by means of an internal administrative process,

which must be concluded before the aforementioned effectiveness period starts, pursuant to

Resolution ARTESP/1 of March 25, 2013.

Autovias S.A. entered into an agreement with the São Paulo State Transportation Regulatory

Agency (“ARTESP” or “Granting Authority”) to include a new project in the concession

agreement - the duplication of 14 kilometers of the SP-318, between km 253 and 249,

involving estimated investments of R$91 million. The inclusion of the works in the agreement

and the latter’s economic and financial rebalancing will be executed through the Marginal Cash

Flow methodology, by extending the concession term of Autovias S.A. by six months, which

should end in May 2019.

Autovias assumed commitments to implement the works resulting from the concession, with

the main projects of such works already completed, as follows:

Arteris S.A. and Subsidiaries

12

SP 255 - Antônio Machado Sant’anna Highway:

• Implementation of the second lane in the stretch between kilometers 2.8 and 48.35;

• Implementation of additional lanes along the entire stretch between kilometers 48.35 and

77.

SP 318 - Engenheiro Thales de Lorena Peixoto Júnior Highway:

• Implementation of additional lanes between kilometers 257.8 and 280.

SP 330 - Anhanguera Highway:

• Implementation of side lanes in Ribeirão Preto (17.2 kilometers).

SP 334 - Cândido Portinari Highway:

• Complementation of the duplication of the stretch between kilometers 322 and 337;

• Implementation of the second lane in the stretch between kilometers 337 and 348;

• Implantation of the second lane in the stretch between kilometers 358 and 395.5.

SP 345 - Engenheiro Ronan Rocha Highway:

• Implementation of the second lane and repaving of the stretch between kilometers 10 and

36;

• Implementation of side lanes between kilometers 30 and 35, on the right side, and between

kilometers 33 and 35, on the left side.

Centrovias Sistemas Rodoviários S.A. (“Centrovias”)

Centrovias is a corporation with its registered office in the city of Itirapina, State of São Paulo,

Brazil, located at Washington Luis Highway, km 216.8, South Lane. It began operations on

June 9, 1998 under a Highway Concession Agreement signed with the Highway Department

(DER), regulated by State Decree No. 42,411 of October 30, 1997, and its exclusive objective

is to operate, under a concession, the highway system that connects the cities of São Carlos to

Cordeirópolis, Itirapina to Jaú, and Jaú to Bauru.

By means of Addendum 11 of December 21, 2006, ARTESP authorized the rebalance of the

economic and financial adequacy of the concession agreement, which was granted by

extending the concession term in another 12 months without changing the concession fee.

Therefore, the concession operation period was extended to June 19, 2019.

Centrovias assumed commitments to implement the works resulting from the concession, with

the main projects of such works already completed, as follows:

SP 225 - Engenheiro Paulo Nilo Romano and Comandante João Ribeiro de Barros Highways:

• Implementation of the second lane in the stretch between kilometers 91 + 429 and 177 +

400;

Arteris S.A. and Subsidiaries

13

• Implementation of the second lane in the stretch between kilometers 183 + 850 and 235 +

040.

Concessionária de Rodovias do Interior Paulista S.A. (“Intervias”)

Intervias is a corporation with its registered office in the city of Araras, State of São Paulo,

Brazil, located at Anhanguera Highway, km 168, South Lane. It was founded on May 28, 1999

and began operating on February 18, 2000 under a Highway Concession Agreement signed

with the State Highway Department (DER/SP 19/CIC/98), regulated by State Decree No.

42,411 of October 30, 1997. The purpose of the agreement is to operate, under a concession,

the highway system that connects the cities of Itapira, Mogi-Mirim, Limeira, Piracicaba,

Conchal, Araras, Rio Claro, Casa Branca, Porto Ferreira and São Carlos - Lot 6. The work

under the concession encompasses performance, management and inspection of the delegated

services, including operating services, conservation and expansion of the system,

complementary and non-delegated services, besides the acts required for compliance with the

object, in the manner provided by the concession agreement signed.

Under Addendum 14/06, of December 21, 2006, ARTESP authorized the revision of the

concession agreement of Intervias to ensure its financial and economic balance. As a result of

such revision, the concession period was extended for an additional 95 months without

changing current fixed concession fees. Therefore, the concession operation period was

extended to January 16, 2028.

A resolution taken by ARTESP’s Managing Board, in the exercise of the powers conferred

upon it by law, approved the inclusion in the physical and financial schedule of the concession

agreement, of work item 02 06.01.50 - SP 147 – implementation of side roads and return

connections in the industrial district of Itapira – KM 46+250 – East/West. The economic and

financial imbalance arising from the inclusion referred to above, calculated in line with the

marginal cash flow methodology, totaled R$1,053 thousand in favor of the Company, in net

present value - reference date July 1997. The estimated contractual extension for the

rebalancing of the agreements is two months and fifteen days. The concession operation was

extended to April 1, 2028.

Intervias originally assumed commitments to implement the works resulting from the

concession, with the main projects of such works already completed, as follows:

SP 147 - Engenheiro João Tosello Highway:

• Duplication of the highway in the stretch between kilometers 41.36 and 54 and between

kilometers 62.45 and 106.32.

SP 191 – Wilson Finardi Highway:

• Duplication of the highway in the stretch between kilometers 43.8 and 44.9, 45.6 and 46.9

and 49.7 and 74.72.

SP 352 - Comendador Virgolino de Oliveira Highway:

• Duplication of the highway in the stretch between kilometers 162.45 and 185.17.

SP 165/330 - Anhanguera Highway - Araras Beltway

Arteris S.A. and Subsidiaries

14

• In accordance with Addendum 06/02 and third readequacy of the work schedule of

10/08/2002, a stretch comprising 4.67 kilometers of highway, known as Araras Beltway, was

built at SP 165/330, from Km 165,225 of SP 330 - Anhanguera Highway - to Km 42,300 of SP

191 - Wilson Finardi Highway.

Vianorte S.A. (“Vianorte”)

Vianorte is a corporation with its registered office in the city of Sertãozinho, State of São

Paulo, Brazil, located at Attílio Balbo Highway, km 327.5. It started operations on March 6,