Languages

Pages

Legal

CHAPTERCHAPTER

1

Tools for Business Decision-Making

Fifth Canadian Edition

Financial Accounting:

Prepared By:Debbie Musil

Kwantlen Polytechnic University

Copyright John Wiley & Sons Canada, Ltd.1 14

CHAPTERCHAPTER

1

CH

AP

TE

R

Performance Measurement

Study Objectives

1. Understand the concept of sustainable income and indicate how irregular items are presented.

2. Explain and apply horizontal analysis.

3. Explain and apply vertical analysis.

4. Identify and calculate ratios that are used to analyze liquidity.

5. Identify and calculate ratios that are used to analyze solvency.

6. Identify and calculate ratios that are used to analyze profitability.

7. Understand the limitations of financial analysis.

14

Copyright John Wiley & Sons Canada, Ltd.2 14

CHAPTERCHAPTER

1Sustainable Income

• The level of profit that is likely to be attainable in the future

• Differs from actual profit due to irregular revenues, expenses, gains and losses that are included in profit

• Two common types of irregular items:– Discontinued operations– Changes in accounting policy

Copyright John Wiley & Sons Canada, Ltd.3 14

CHAPTERCHAPTER

1Discontinued Operations

• Disposal, or availability for sale, of a component of an entity

– Separate major line of business or major geographical area of operations that has been disposed of or is for sale

– Must be clearly distinguishable operationally and financially

Copyright John Wiley & Sons Canada, Ltd.4 14

CHAPTERCHAPTER

1

Discontinued Operations:Statement of Financial Position

• Assets and liabilities are reported separately

• Valued and reported at lower of carrying amount and fair value, less any expected costs of disposition

– Reported as non-current assets or liabilities

Copyright John Wiley & Sons Canada, Ltd.5 14

CHAPTERCHAPTER

1

Discontinued Operations:Income Statement

• Segregated from continuing operations and reported separately on the income statement

– Shown immediately following profit/loss from continuing operations

• Consists of two parts:

– Profit (loss) from discontinued operations

– Gain (loss) on disposal of the segment

– Both components are reported net of applicable taxes

Copyright John Wiley & Sons Canada, Ltd.6 14

CHAPTERCHAPTER

1Change in Accounting Policy

• Occurs when the policy used in the current year is different from the one used in the preceding year

– Voluntary change: Allowed when new policy results in more reliable and relevant presentation

– Mandatory: Required by standard setters

Copyright John Wiley & Sons Canada, Ltd.7 14

CHAPTERCHAPTER

1

Change in Accounting Policy:Effect on Reporting

• Cumulative effect of change to prior years is reported as adjustment to opening retained earnings

– In statement of changes in equity (IFRS)

– In statement of retained earnings (ASPE)

• New policy used to report results of current year

• Prior period statements restated

• Effects of change detailed in notes

Copyright John Wiley & Sons Canada, Ltd.8 14

CHAPTERCHAPTER

1Discussion Question

Discuss the adoption of international financial reporting standards (IFRS) as a change in accounting policy.

Copyright John Wiley & Sons Canada, Ltd.9 14

CHAPTERCHAPTER

1Comparative Analysis

• Three types of comparisons:

– Intracompany basis – comparisons within a company

– Intercompany basis – comparisons between one or more competitor companies

– Industry averages

Copyright John Wiley & Sons Canada, Ltd.10 14

CHAPTERCHAPTER

1

Comparative Analysis:Three Tools

• Horizontal analysis (trend analysis)

– A technique to determine the change over time

• Percentage of base-period amount

• Percentage change for the period

• Vertical analysis (common size analysis)

• Ratio analysis

Copyright John Wiley & Sons Canada, Ltd.11 14

CHAPTER

1

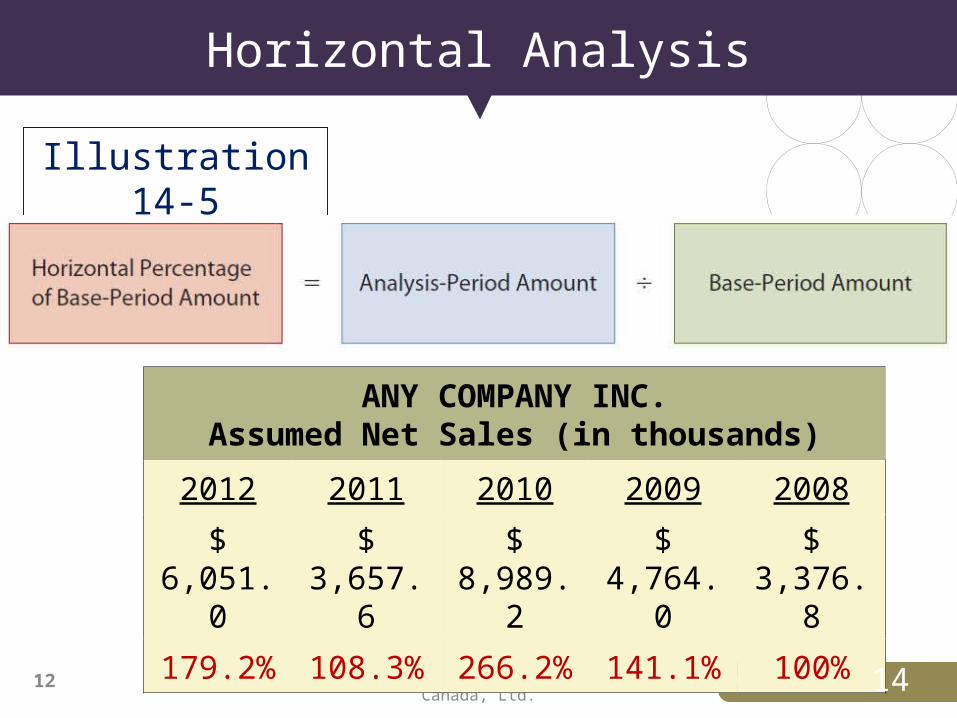

Horizontal Analysis

Copyright John Wiley & Sons Canada, Ltd.12

Illustration 14-5

ANY COMPANY INC.Assumed Net Sales (in thousands)

2012 2011 2010 2009 2008

$ 6,051.0 $ 3,657.6 $ 8,989.2 $ 4,764.0 $ 3,376.8

179.2% 108.3% 266.2% 141.1% 100%

14

CHAPTER

1

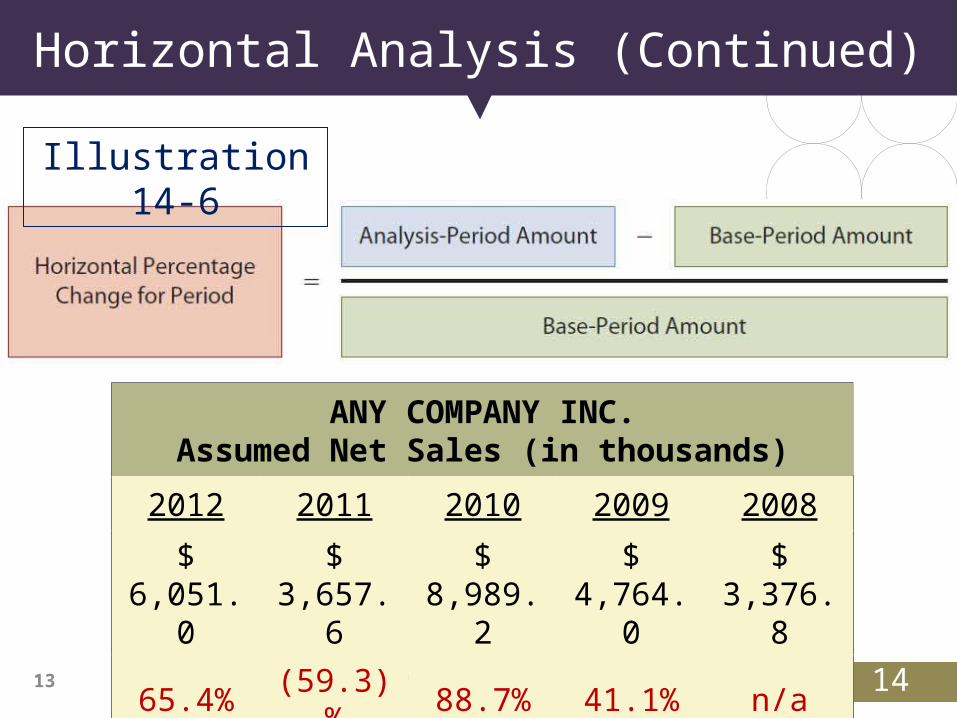

Horizontal Analysis (Continued)

Copyright John Wiley & Sons Canada, Ltd.13 14

ANY COMPANY INC.Assumed Net Sales (in thousands)

2012 2011 2010 2009 2008

$ 6,051.0 $ 3,657.6 $ 8,989.2 $ 4,764.0 $ 3,376.8

65.4% (59.3)% 88.7% 41.1% n/a

Illustration 14-6

CHAPTER

1

Vertical Analysis

Copyright John Wiley & Sons Canada, Ltd.14

Expresses each item in a financial statement as a percent of a base amount (total assets or net sales)

Illustration 14-9

14

CHAPTER

1

Vertical Analysis (Continued)

Copyright John Wiley & Sons Canada, Ltd.15 14

ANY COMPANY INC.Condensed Statement of Financial Position

December 31 (in thousands)

2012 2011

Assets Amount Percent Amount Percent

Current Assets $ 2,139.9 20.3% $ 2,271.7 25.1%

Property, Plant, and Equipment 8,062.7 76.3% 6,413.3 70.9%

Other Assets 363.1 3.4% 359.9 4.0%

Total Assets $ 10,565.7 100% $ 9,044.9 100%

CHAPTERCHAPTER

1Discussion Question

Identify some situations when a horizontal or vertical percentage cannot be calculated or is not meaningful.

Copyright John Wiley & Sons Canada, Ltd.16 14

CHAPTERCHAPTER

1Ratio Analysis

• Liquidity Ratios: Measure short-term ability of the company to pay its maturing obligations and to meet unexpected needs for cash

• Solvency Ratios: Measure the ability of the company to survive over a long period of time

• Profitability Ratios: Measure the earnings or operating success of a company for a given period of time

Copyright John Wiley & Sons Canada, Ltd.17 14

CHAPTERCHAPTER

1Liquidity Ratios

• Working capital

• Current ratio

• Cash current debt coverage

• Receivables turnover

• Average collection period

• Inventory turnover

• Days in inventory

Copyright John Wiley & Sons Canada, Ltd.18 14

CHAPTERCHAPTER

1Working Capital

• Measures short-term debt paying ability

Working Capital = Current Assets – Current Liabilities

Copyright John Wiley & Sons Canada, Ltd.19 14

Higher is better

CHAPTERCHAPTER

1Current Ratio

• Measures short-term debt paying ability

Copyright John Wiley & Sons Canada, Ltd.20 14

Current Ratio = Current Assets Current Liabilities

Higher is normally (but not always) better. Be cautious about influences of slow moving

inventory and receivables on this ratio.

CHAPTERCHAPTER

1Cash Current Debt Coverage

• Measures short-term debt-paying ability (cash basis)

Copyright John Wiley & Sons Canada, Ltd.21 14

Cash Current Debt Coverage =

Cash Provided (Used) by Operating

ActivitiesAverage Current

Liabilities

Higher is better

CHAPTERCHAPTER

1Receivables Turnover

• Measures liquidity of receivables

Copyright John Wiley & Sons Canada, Ltd.22 14

Receivables Turnover =

Net Credit SalesAverage Gross Receivables

Higher is better

CHAPTERCHAPTER

1Average Collection Period

• Measures number of days receivables are outstanding

Copyright John Wiley & Sons Canada, Ltd.23 14

Average Collection

Period =

365 DaysReceivables Turnover

Lower is better

CHAPTERCHAPTER

1Inventory Turnover

• Measures liquidity of inventory

Copyright John Wiley & Sons Canada, Ltd.24 14

Inventory

Turnover =

Cost of Goods SoldAverage Inventory

Higher is better

CHAPTERCHAPTER

1Days in Inventory

• Measures number of days inventory is on hand

Copyright John Wiley & Sons Canada, Ltd.25 14

Days in Inventory =365 Days

Inventory Turnover

Lower is better

CHAPTERCHAPTER

1Solvency Ratios

• Debt to total assets• Times interest earned• Cash total debt coverage• Free cash flow

Copyright John Wiley & Sons Canada, Ltd.26 14

CHAPTERCHAPTER

1Debt to Total Assets Ratio

• Measures % of total assets provided by creditors

Copyright John Wiley & Sons Canada, Ltd.27 14

Debt to Total Assets =Total Liabilities

Total Assets

Lower is better

CHAPTERCHAPTER

1Times Interest Earned

• Measures ability to meet interest payments as they come due

Copyright John Wiley & Sons Canada, Ltd.28 14

Times Interest Earned =

Profit + Interest Expense + Income Tax

Expense (EBIT)Interest Expense

Higher is better

CHAPTERCHAPTER

1Cash Total Debt Coverage

• Measures long-term debt-paying ability (cash basis)

Copyright John Wiley & Sons Canada, Ltd.29 14

Cash Total Debt Coverage =

Cash Provided (Used) by Operating Activities

Average Total Liabilities

Higher is better

CHAPTERCHAPTER

1Free Cash Flow

• Measures cash available for paying dividends or expanding operations

Copyright John Wiley & Sons Canada, Ltd.30 14

Net Cash Provided (Used) by Operating Activities

Net Capital Expenditures Dividends

Paid =Free Cash Flow

Higher is better

CHAPTERCHAPTER

1Profitability Ratios

Copyright John Wiley & Sons Canada, Ltd.31 14

• Return on common shareholders’ equity• Profit margin• Return on assets• Asset turnover• Gross profit margin• Earnings per share (EPS)• Price-earnings (P-E) ratio• Payout ratio• Dividend yield

CHAPTERCHAPTER

1

Return on Common Shareholders’ Equity

• Measures overall profitability of shareholders’ investment

Copyright John Wiley & Sons Canada, Ltd.32 14

Return on Common

Shareholders’ Equity =

Profit – Preferred Dividends

Average Common Shareholders’ Equity*

*Common shareholders’ equity = Total shareholders’ equity – Preferred shares

Higher is better

CHAPTERCHAPTER

1Return on Assets

• Measures overall profitability of assets– How much is earned on each dollar invested in

assets

Copyright John Wiley & Sons Canada, Ltd.33 14

Return on Assets =Profit

Average Total Assets

Higher is better

CHAPTERCHAPTER

1Profit Margin

• Measures the percentage of profit generated by each dollar of sales

Copyright John Wiley & Sons Canada, Ltd.34 14

Profit Margin =Profit

Net Sales

Higher is better

CHAPTERCHAPTER

1Asset Turnover

• Measures how efficiently assets are used to generate sales

Copyright John Wiley & Sons Canada, Ltd.35 14

Asset Turnover =Net Sales

Average Total Assets

Higher is better

CHAPTERCHAPTER

1Gross Profit Margin

• Measures margin between selling price and cost of goods sold

Copyright John Wiley & Sons Canada, Ltd.36 14

Gross Profit Margin =

Gross ProfitNet Sales

Higher is better

CHAPTER

1

Relationship Amongst Profitability Ratios

Copyright John Wiley & Sons Canada, Ltd.37

Illustration 14-15

14

CHAPTERCHAPTER

1Earnings per Share (EPS)

• Measures profit earned on each common share

Copyright John Wiley & Sons Canada, Ltd.38 14

Earnings Per Share =

Profit – Preferred Dividends

Weighted Average Number of Common

Shares

Not comparable between companies

CHAPTERCHAPTER

1Price-Earnings (P-E) Ratio

• Measures relationship between market price per share and earnings per share

Copyright John Wiley & Sons Canada, Ltd.39 14

Price-Earnings Ratio =

Share PriceEarnings Per Share

Higher indicates investors expect favourable profitability in future

CHAPTERCHAPTER

1Payout Ratio

• Measures % of profit distributed in the form of cash dividends

Copyright John Wiley & Sons Canada, Ltd.40 14

Payout Ratio =Cash Dividends

Profit

Higher is better for investors seeking income

CHAPTERCHAPTER

1Dividend Yield

• Measures rate of return earned from dividends during the year

Copyright John Wiley & Sons Canada, Ltd.41 14

Dividend Yield =Dividend per Share

Market Price per Share

Higher is better for investors seeking income

CHAPTERCHAPTER

1Discussion Question

Why are the P-E and dividend yield ratios known as market measures?

Copyright John Wiley & Sons Canada, Ltd.42 14

CHAPTERCHAPTER

1Limitations of Financial Analysis

• Can be impacted by– Alternative accounting principles– Professional judgement– Comprehensive income– Diversification – Inflation– Economic factors

Copyright John Wiley & Sons Canada, Ltd.43 14

CHAPTER

1

Comparing IFRS and ASPE

14

CHAPTERCHAPTER

1Copyright Notice

Copyright © 2012 John Wiley & Sons Canada, Ltd. All rights reserved. Reproduction or translation of this work beyond that permitted by Access Copyright (The Canadian Copyright Licensing Agency) is unlawful. Requests for further information should be addressed to the Permissions Department, John Wiley & Sons Canada, Ltd. The purchaser may make back-up copies for his or her own use only and not for distribution or resale. The author and the publisher assume no responsibility for errors, omissions, or damages caused by the use of these programs or from the use of the information contained herein.

Copyright John Wiley & Sons Canada, Ltd.45 14

Top Related