Languages

Pages

Legal

Accounting Education: The Real Facts about Who Teaches, Who

Studies?

Bruce Behn, David Leslie, and Susan Crosson

Front page

news…….

Supply of and demand for Accounting faculty

• The number of Accounting faculty has declined.

• The number of Accounting students has risen.

• The number of Ph.D.’s produced is lagging far behind prospective retirements.

Table 1: Total number of faculty by type of institution, 1993 – 2004

Accounting

1993 2004 Rate of change

Research/Doctoral 4501 4100 -9%

4-Year 7400 6806 -8%

2-Year 8400 6800 -19%

Total 20301 17706 -13%

Other business

Total +19%

All other fields

Total +22%

Figure 24: Enrollment of (full-time) undergraduate and (all) graduate accounting students, by type of institution, 1990 - 2000.

0

10

20

30

40

50

60

70

80

90

Res./Doct. 4-Year. Public 2-Year

Nu

mb

er in

100

0's

Total 1990

Total 2000

Figure 1b: Linear trends in transformed numbers (estimated) of Accounting faculty and students, 1993 - 2008.

4

4.1

4.2

4.3

4.4

4.5

4.6

4.7

4.8

4.9

1993 1996 2000 2003 2008

Tra

ns

form

ed s

cale

Linear (Students 2-year)

Linear (Students4-year)

Linear (Faculty2-year)

Linear (Faculty4-year)

Figure 14: Average annual production of Ph.D.s in accounting, 1980 - 2005

0

20

40

60

80

100

120

140

160

180

200

1980–84 1985–89 1990–94 1995–99 2000-04 2005

Ave

rag

e an

nu

al n

um

ber

of

Ph

.D.s

140 PhDs in Accounting were awarded in 2008, per Survey of Earned PhDs.

The age profile of accounting faculty suggests as many as 500 – 700 retirements per year in the foreseeable future, which, even if too high, suggests that there will not be enough new Ph.D.’s to replace them one-for-one. Plumlee’s (2005) survey of supply and demand for Ph.D. accounting faculty estimates demand at 350 – 590 per year between 2005 and 2007, and estimates there is supply to fill abut 50% of that demand, with supply unevenly matched to subspecialties.

Competition for Accounting talent.

• Half of new Ph.D.’s are foreign born.

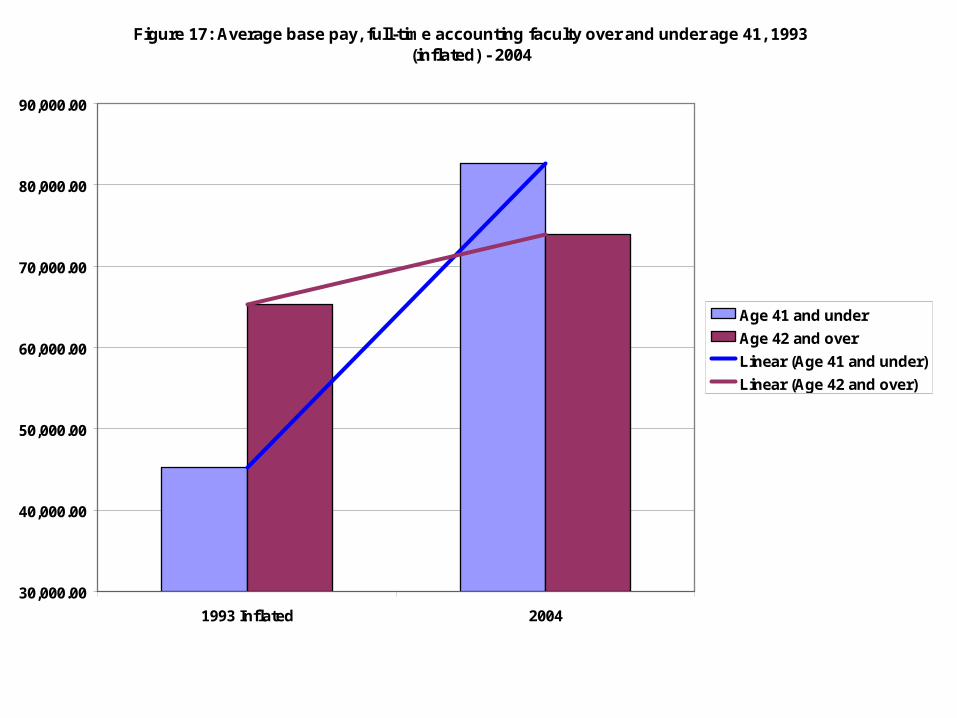

• Salary inversion signals inadequate supply, competing opportunties, less attractive working conditions.

• Pay for non-tenure eligible Accounting faculty outpaces that in other fields.

• Outside income, higher ratio of part-time faculty point to competition for talent.

Basic salary from institution

Total income from the institution

Total income of respondent from all sources

N

Age in 1993

45 and under 44,744.25 48,584.44 71,418.58 2500

46 and over 65,751.48 73,323.75 99,172.30 4200

Age in 2004

45 and under 92,731.80 101,061.90 125,370.80 1500

46 and over 73,982.60 81,149.60 98,144.60 4400

[1] The age intervals were established to provide adequate cell sizes, given the NSOPF minimums.

Table 7a: Income of all Accounting faculty with Ph.D. or 1st professional degree, under/over age 45, 1993 (Inflated) – 2004[1]

Figure 17: Average base pay, full-time accounting faculty over and under age 41, 1993 (inflated) - 2004

30,000.00

40,000.00

50,000.00

60,000.00

70,000.00

80,000.00

90,000.00

1993 Inflated 2004

Age 41 and under

Age 42 and over

Linear (Age 41 and under)

Linear (Age 42 and over)

Figure 12a: Basic salary from institution, full-time NTE, 1993 (inflated) - 2004

35000

40000

45000

50000

55000

60000

1993 Inflated 2004

Con

stan

t d

olla

rs

Accounting

Other business

All other fields

Figure 12b: Basic salary from institution, part-time NTE faculty, 1993 (inflated) - 2004

6000

7000

8000

9000

10000

11000

12000

13000

1993 Inflated 2004

Con

stan

t d

olla

rs

Accounting

Other business

All other fields

Table 4: Tenure status of Accounting faculty by full- and part-time, 1993 – 2004

1993 Full-time Part-time Total

Tenured or eligible 8110 90 8200

Not eligible 2263 9837 12100

Total 10373 9927 (49%) 20300

2004 Full-time Part-time Total

Tenured or eligible 6419 281 6700

Not eligible 2191 8709 10900

Total 8610 8990 (51%) 17600

Figure 18: Average total hours worked per week reported by full-time accounting faculty at 4-year institutions, '93 - '04

47

48

49

50

51

52

53

Hours worked '93 Hours worked 04

Figure 25: Trend in Student Credit Hour productivity by type of institution and full- vs. part-time accounting faculty, 1993 - 2004.

0

200

400

600

800

1000

1200

1400

1600

Res/Doct. 4-Yr.NonDoct 2-Yr.

Ind

ex o

f S

CH

pro

du

ctio

n p

er f

acu

lty

mem

ber

.

FTSCH93

FTSCH04

PTSCH93

PTSCH04

Figure 20: Percentage of time reported on research, full-time accounting at 4-year institutions, '93 - '04

10

12

14

16

18

20

22

Time on research 93 Time on research 04

Ave

rag

e p

erce

nta

ge

of

tim

e o

n r

esea

rch

.

Figure 10a: Mean number of hours per week paid work NOT at institution, part-time NTE's.

0

5

10

15

20

25

30

35

Accounting Other business All other

Mea

n n

um

ber

of

ho

urs

1993

2004

Demographics changing

• Accounting faculty aging.

• Retirement rate accelerating.

• Fewer males, more females.

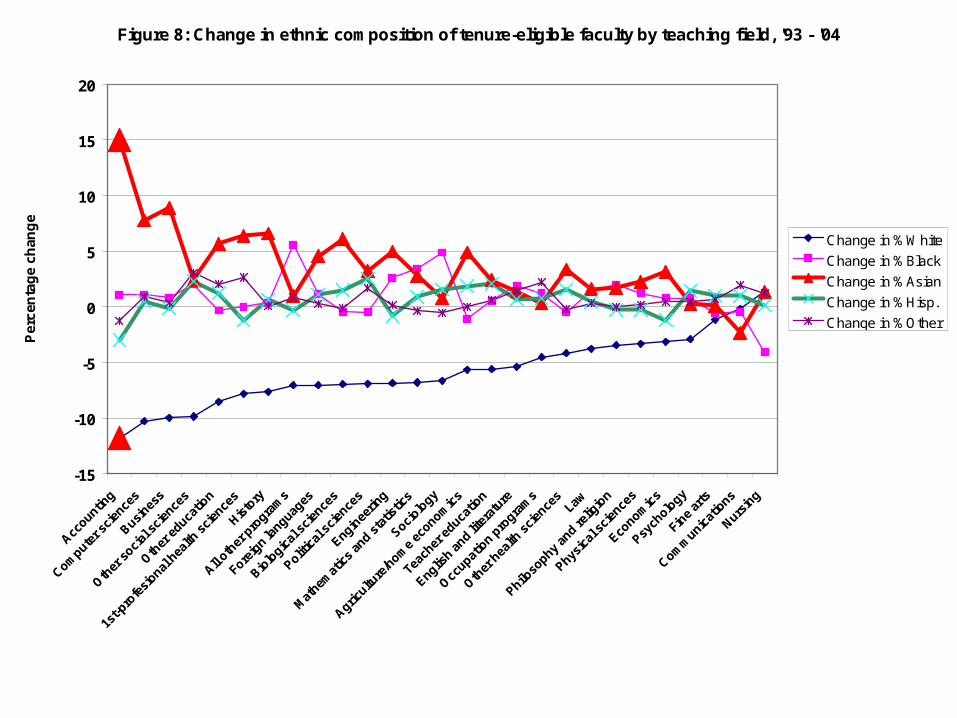

• High rate of entry by Asian-origin.

Figure 11: NSOPF estimated number (1000's) of male accounting faculty under age 40 and over age 55, 1993 - 2004

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

Males93 Males04

Under age 40

Over age 55

Linear (Under age 40)

Linear (Over age 55)

Figure 12: NSOPF estimated number (1000's) of female accounting faculty under age 40 and over age 55, 1993 - 2004.

0

0.5

1

1.5

2

2.5

Females93 Females04

Under age 40

Over age 55

Linear (Under age 40)

Linear (Over age 55)

Figure 13: Mean years to retirement, full-time accounting faculty by type of institution, 1993-2004

12

13

14

15

16

17

18

19

1993YrstoRetire 2004YrstoRetire

Me

an y

ears

to

ret

irem

ent

Res/Doct

4-Year

2-Year

Number of male and female Accounting facjulty, 1993 - 2004.

0

2000

4000

6000

8000

10000

12000

14000

16000

Male93 Female93 Male04 Female04

Nu

mb

er o

f A

cco

un

tin

g f

acu

lty

Male93

Female93

Male04

Female04

Percent of Ph.D.'s by gender, 2008

0%

10%

20%

30%

40%

50%

60%

70%

Al l fi elds Al l Business Accounting

% Female

% Male

Figure 8: Change in ethnic composition of tenure-eligible faculty by teaching field, '93 - '04

-15

-10

-5

0

5

10

15

20

Acc

ounting

Com

puter s

cien

ces

Busi

ness

Oth

er s

ocial

sci

ence

s

Oth

er e

ducatio

n

1st

-pro

fesi

onal h

ealth

sci

ence

s

His

tory

All

other

pro

gram

s

Fore

ign la

nguages

Bio

logic

al s

cien

ces

Polit

ical

sci

ence

s

Engin

eerin

g

Mat

hemat

ics

and s

tatis

tics

Soci

ology

Agric

ulture

/hom

e ec

onomic

s

Tea

cher

educa

tion

Englis

h and li

tera

ture

Occ

upatio

n pro

gram

s

Oth

er h

ealth

sci

ence

s L

aw

Philo

sophy

and re

ligio

n

Phys

ical

sci

ence

s

Eco

nomic

s

Psy

cholo

gy

Fin

e ar

ts

Com

munic

atio

ns

Nurs

ing

Per

cen

tag

e ch

ang

e

Change in %White

Change in %Black

Change in %Asian

Change in %Hisp.

Change in %Other

Over 40% of Accounting students are in community colleges.

• Mostly female.

• Older.

• Otherwise employed.

• Diverse.

• Higher “risk.”

Figure 1a: Enrollment trend, Accounting majors by type of institution, 1990 - 2008

0

50

100

150

200

250

1990 1996 2000 2008

Num

ber r

epor

ting

Acco

untin

g m

ajor

, in

1000

's.

2-year

4-year non-doctoral

4-year doctoral

Table 28: Gender of Accounting majors (percent female) by type of institution, 1990 - 2008. 1990 1996 2000 2008

2-year 68.5% 67.4% 77.8% 70.0%

4-year non-doctoral 56.9% 64.6% 63.1% 56.8%

4-year doctoral 52.6% 58.8% 51.4% 58.9%

Figure 18a: Age distribution of Accounting majors by type of institution, 2008.

0

10

20

30

40

50

60

0 to 1819 to 22

23 to 2627 to 30

31 to 3435 to 40 > 40

Age in years

Perc

ent o

f stu

dent

s in

age

inte

rval

.

2-year

4-year non-doctoral 4-year doctoral

Figure 20: Work status of Accounting students while enrolled by type of institution, 2008.

0

10

20

30

40

50

60

2-year 4-year non-doctoral 4-year doctoral

Per

cen

t o

f st

ud

ents

in in

dic

ated

job

sta

tus.

No job

Part-time

Full-time

Figure 17: Percent of 2-year Accounting students by race/ethnicity, 1990 - 2008.

0

10

20

30

40

50

60

70

80

1990 1996 2000 2008

Per

cen

t

White

Black

Hispanic

Asian/Pacific Islander

All other

68% of Accounting students at 4-year institutions were White in ’08.

Figure 22: Cumulative number of risk factors reported by Accounting students by type of institution, 2008.

0

5

10

15

20

25

30

35

40

45

Per

cen

t o

f st

ud

ents

rep

ort

ing

ris

k fa

cto

rs.

2-year

4-year non-doctoral

4-year doctoral

CC faculty differ from 4-year/research univ. faculty.

• More part-time (2/3).

• Increasingly female.

• Otherwise employed.

• Less likely to hold terminal degree.

• More likely to have highest degree in other field.

• Much heavier teaching load.

Table 6: Gender of community college accounting faculty, 1993 - 2004. 1993 2004

Percent change

Male 5300 3900 -26.4%

Female 2300 2800 +21.7%

Total 7600 6700 -11.8%

Percent male 69.7% 58.2%

Table 7: Part- and full-time status of community college Accounting faculty by gender, 1993 – 2004. 1993 2004

1993

2004

Part-time

Part-time

Percent change in part-time faculty.

Full-time

Full-time

Percent change in full-time faculty.

Male 3551 2968

-16.4%

1749 932

-46.7%

Female 1594 1459-8.5%

706 1341+89.9%

Figure 5: Age distribution of Accounting faculty in 2-year institutions by gender, 2004.

0

5

10

15

20

25

30

0 to 3031 to 34

35 to 3940 to 44

45 to 4950 to 54

55 to 59 > 60

Age in years

Per

cen

t o

f re

sp

on

de

nts

in in

terv

al

Male

Female

Table 11: Percentage of Accounting faculty at 2-year institutions reporting "other employment" than their teaching job, 1993 - 2004. 1993 2004

Part-time 88.60% 72.70%

Full-time 34.50% 21.10%

Total 71.10% 55.20%

Table 15: Percent of Accounting faculty in 2-year institutions holding indicated highest degree, 1993 – 2004.

1993 2004

Ph.D. or 1st Professional 9.60% 11.22%

Master's 60.80% 70.47%

Baccalaureate or less 29.60% 18.31%

Table 17: Field of highest degree earned, Accounting faculty in 2-year institutions, 1993 - 2004. 1993 2004

Accounting 51.3% 50.8%

Other business 31.6% 37.3%

All other fields 17.1% 11.9%

Figure 10: Mean number of classes taught by full-time Accounting faculty by type of institution, 1993 - 2004

0

1

2

3

4

5

6

1993 2004

Mea

n n

um

ber

of

clas

ses

tau

ght

2-year

4-year non-doctoral

Research/doctoral

Issues/Questions

• Accounting faculty work harder,

• Aging faster,

• Replacing slower.

• Becoming more female, more minority (esp. Asian).

• Relying on non-core (not tenured, no Ph.D., part-time, otherwise employed).

• Competing vs. other opportunities for accountants.

• Foreign-born Ph.D’s?

• Clinical or technical vs. professional content?

• Draw in allies to promote/support change, revitalization of field?

Top Related