ZCCM Investments Holdings Plc - Novi Insight … · ZCCM Investments Holdings Plc 5 ZCCM...

98

Transcript of ZCCM Investments Holdings Plc - Novi Insight … · ZCCM Investments Holdings Plc 5 ZCCM...

ZCCM Investments Holdings PlcAnnual report and financial statements

for the year ended 31 March 2013

ZCCM Investments Holdings Plc

Annual report and financial statements for the year ended 31 March 2013

ZCCM Investments Holdings PlcZCCM Investments Holdings PlcAnnual Reportfor the year ended 31 March 2013

Contents Page

Directorate and administration 1

Management committee 2-3

Chairman’s statement 4 - 6

Report of the directors 7 - 10

Operations report

Subsidiary companies’ performance 11 - 12

Associate companies and other investments’ performance 13 - 21

Corporate social responsibility and environmental review 22

Directors’ responsibilities in respect of the preparation of financial statements 23

Report of the independent auditors 24 - 25

Consolidated and company statements of comprehensive income 26 - 27

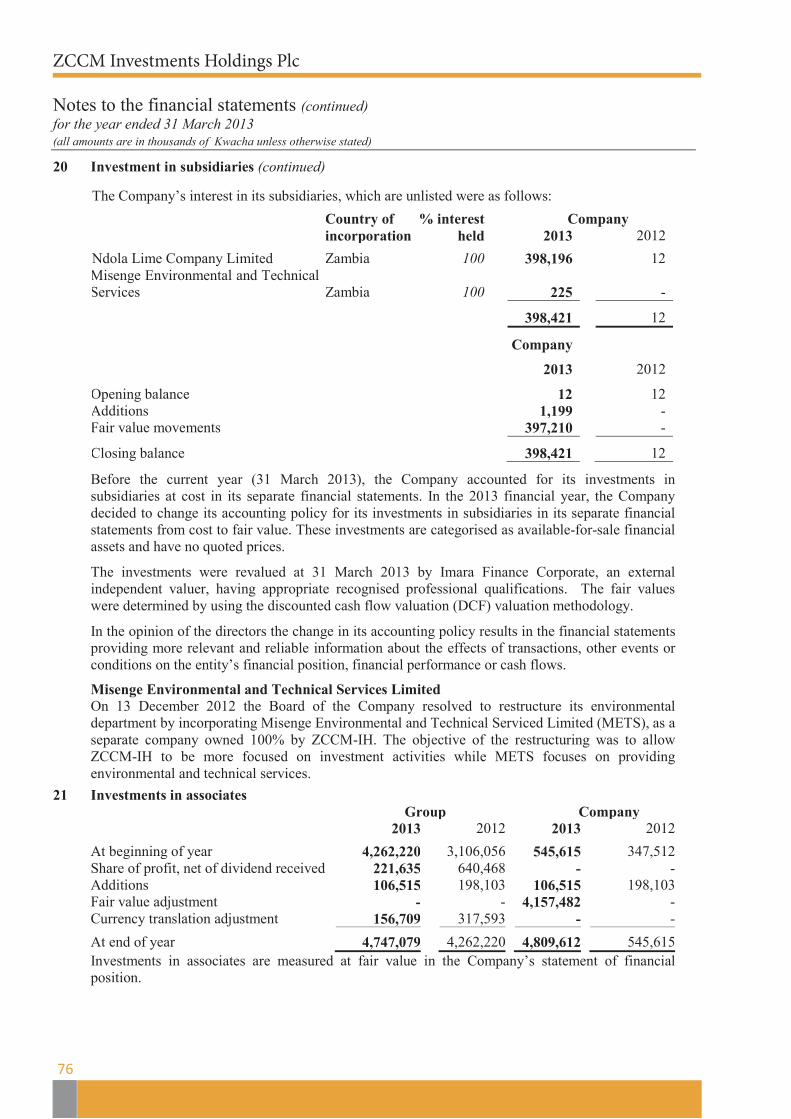

Consolidated and company statements of financial position 28 - 29

Consolidated and company statements of changes in equity 30 - 31

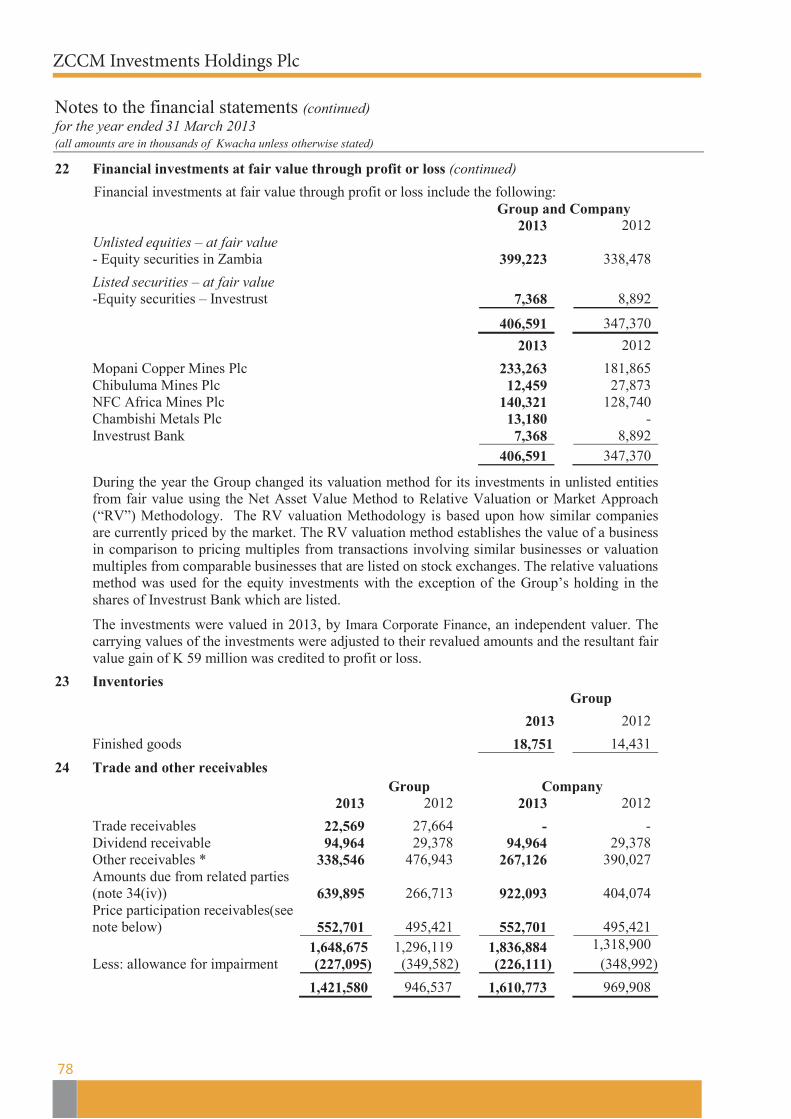

Consolidated and company statements of cash flows 32 - 33

Notes to the financial statements 34 - 93

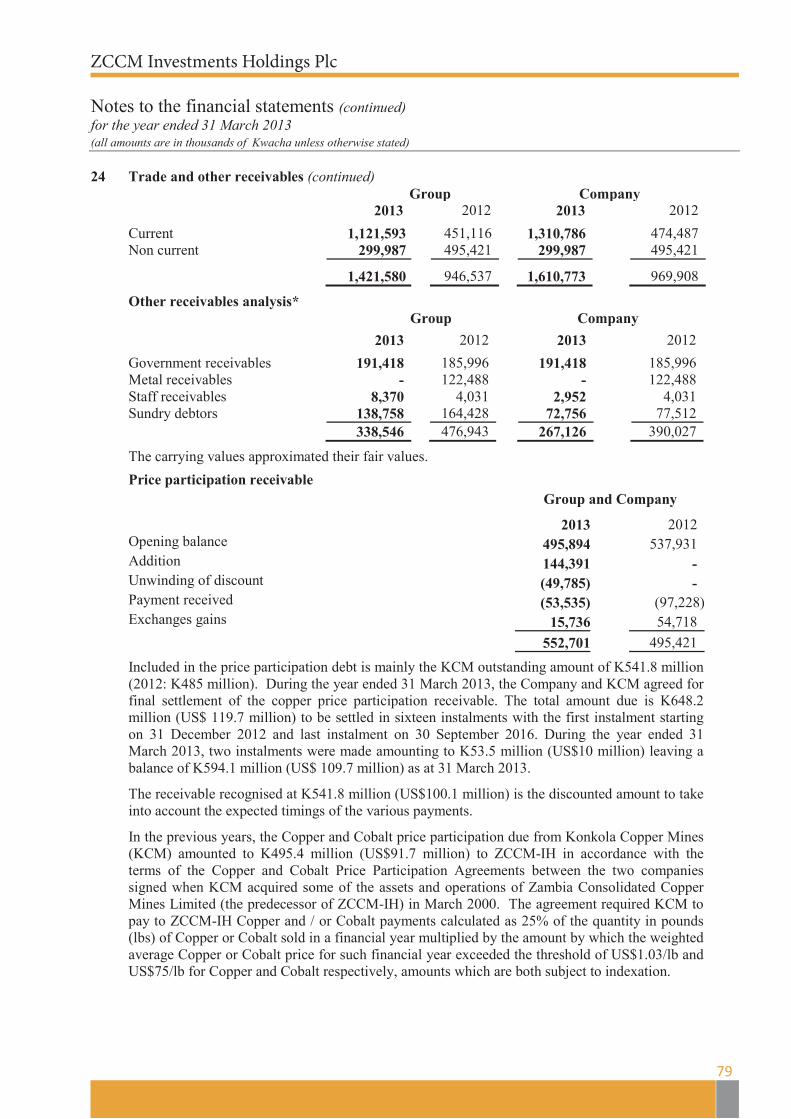

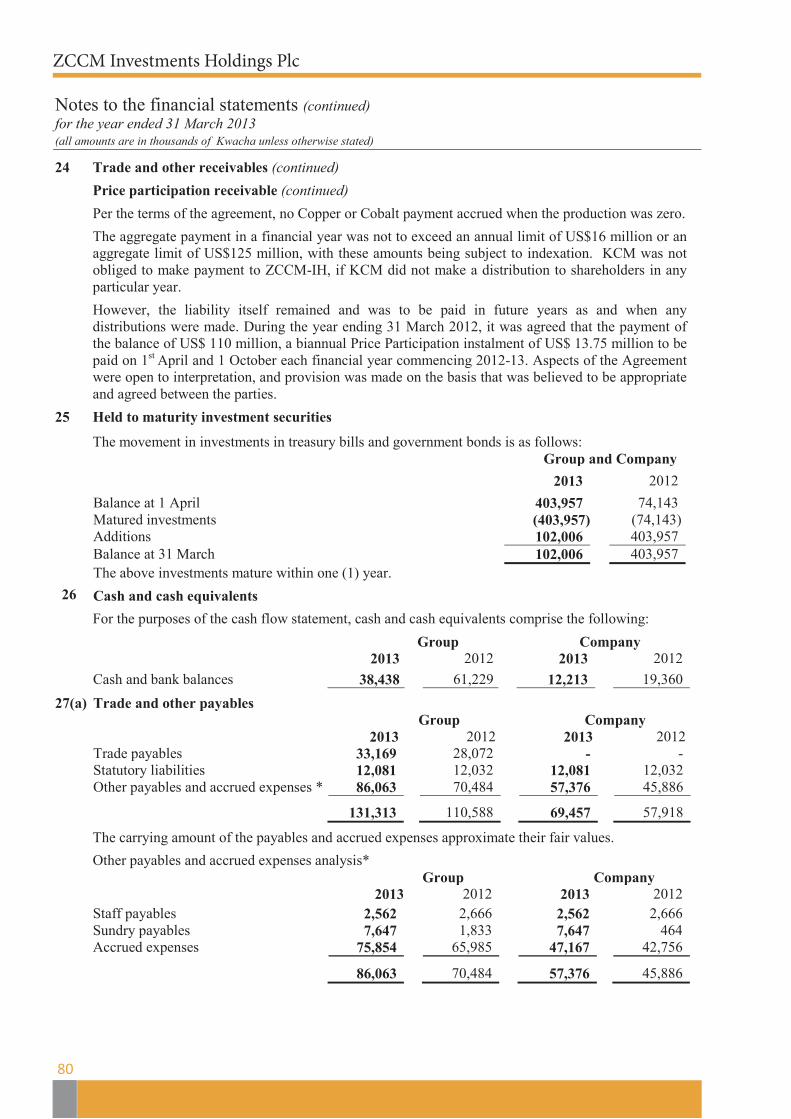

Corporate information 94 - 95

12 - 21

2 - 3

ZCCM Investments Holdings Plc

1

ZCCM Investments Holdings Plc Annual Report (continued) for the year ended 31 March 2013 DIRECTORATE AND ADMINISTRATION DIRECTORS The Directors who held office during the period to 31 March 2013 were: Mr. W D Mung’omba Executive Chairman of the Board Mr. J M D Patterson Non Executive Director Mr.C Mwananshiku Non Executive Director Ms. S Mutemba Non Executive Director Dr. V Mutambo Non Executive Director Dr. B K E Ng’andu Non Executive Director Appointed 02 April 2012 Mrs. P C Kabamba Non Executive Director Appointed 15 January 2013 Dr. A Mwenda Non Executive Director Retired 30 June 2012 The Directors who held office as at the date of approval of this report (08 November 2013) were: Mr. W D Mung’omba (Executive Chairman) Mr. J M D Patterson (Non-executive Director) Mr. C Mwananshiku (Non-executive Director) Ms. S Mutemba (Non-executive Director) Dr. V Mutambo (Non-executive Director) Dr. B K E Ng’andu (Non-executive Director) Mrs. P C Kabamba (Non-executive Director)

ZCCM Investments Holdings Plc

2

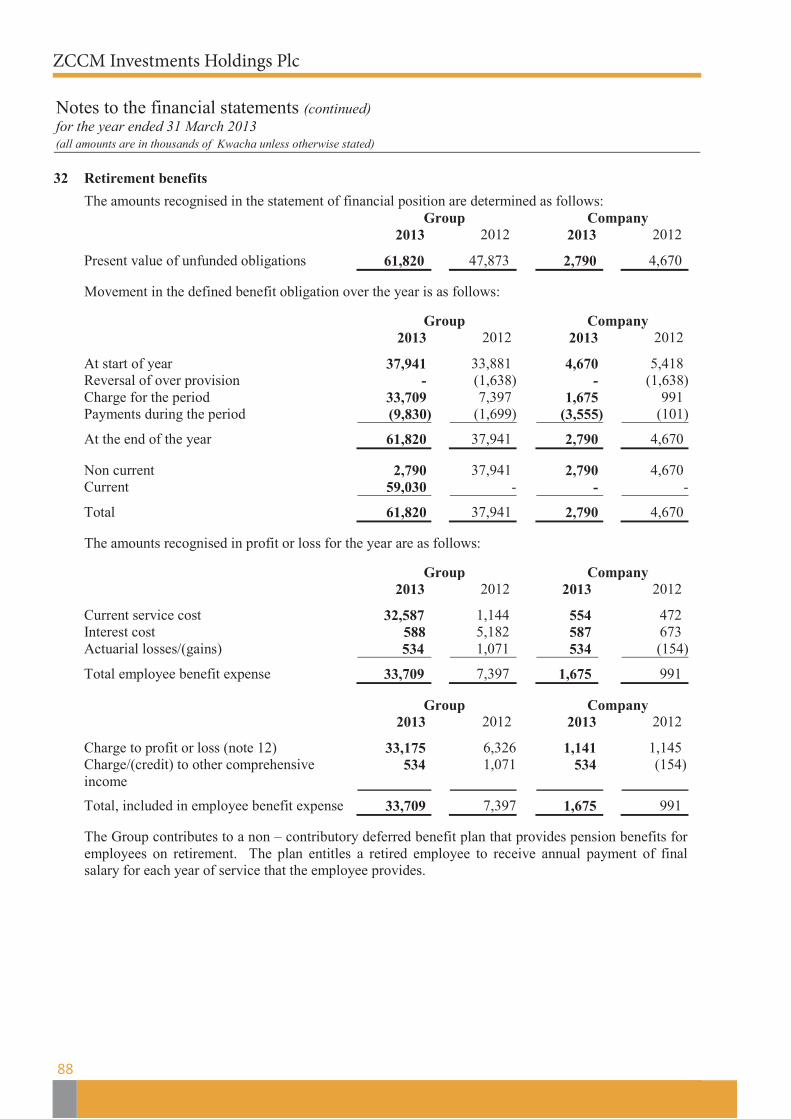

ZCCM Investments Holdings Plc Annual Report (continued) for the year ended 31 March 2013 MANAGEMENT COMMITTEE Management officials who held office during the year to 31 March 2013 were: Mr. W D Mung’omba Executive Chairman of the Board Mr. M Muyunda Chief Executive Officer Mr. C Chabala Company Secretary Ms. M Chanda Chief Operating Officer (Appointed 01 February 2013) Mr. M T Chipata Chief Financial Officer ( Appointed 1 July 2012) Ms. Y Mkandawire Acting Legal Manager (Appointed 21 November 2012) Mr. Moses Chilambe Acting Technical Manager (Appointed 21 August 2012) Mr C Mjumphi Corporate Officer (Appointed 07 January 2013) Mr. B F Shamalavu Head, Human Resources Ms. W Mangambwa Head, Risk and Internal Audit Mr. J Makumba Environmental Manager (separated 28 February 2013) Mr. M Mbewe Investments Manager (separated 02 November 2012) Mr. J K Kaite Legal Manager (separated 31 October 2012) Mr. M Khunga Corporate Officer (separated 24 September 2012) Mr. W K Katoto Technical Manager (separated 30 June 2012)

ZCCM Investments Holdings Plc

3

ZCCM Investments Holdings Plc Annual Report (continued) for the year ended 31 March 2013 MANAGEMENT COMMITTEE (continued) Management officials who held office as at the date of approval of this report (08 November 2013) were: Mr. W D Mung’omba Executive Chairman of the Board

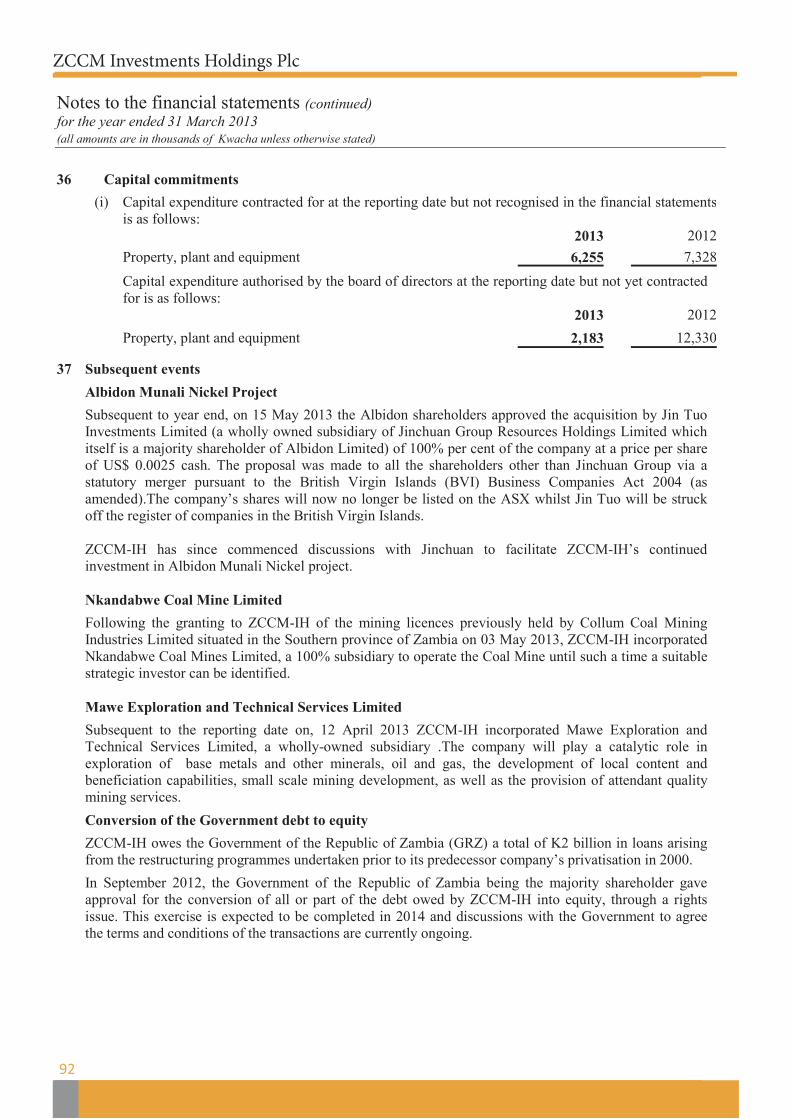

Mr. M Muyunda Chief Executive Officer

Mr. C Chabala Chief Corporate Services Officer /Company Secretary

Ms. M Chanda Chief Operating Officer

Mr. M T Chipata Chief Financial Officer

Ms. Y Mkandawire Deputy General Counsel

Ms. W Mangambwa Head, Risk and Internal Audit

Mr C Mjumphi Corporate Officer

ZCCM Investments Holdings Plc

4

ZCCM Investments Holdings Plc Annual Report (continued) for the year ended 31 March 2013 CHAIRMAN’S STATEMENT During the period under review the global economy continued to record sluggish growth and continuing volatility. Uncertainty across the major economic regions ranging from the post election fiscal cliff in the United States of America, the Chinese leadership transition, to reforms in the Eurozone area continued to impact the global economy. Global copper demand marginally increased by 3.1% (2012:3.2%), while copper production increased by 4.5% (2012: Nil). Copper prices declined 9.4%, from US$8,318 per tonne at the beginning of the year to US$7,540 per tonne at the close of the financial year. Despite the scenario above, the Zambian economy recorded growth of 7.2% in 2013 (2012:6.6%), 0.5% lower than forecast due to lower than budgeted performance in the mining sector and the weaker global economy. Financial performance For the Group, investment in productive capacity, efforts to reposition and enhance efficiencies continued. Investment in Ndola Lime Company Limited continued and this was expected to improve the production capacity of lime and the Group’s business. Other investee companies continued with their growth strategies premised on the prospect of recovery in global demand and improved investments in power projects intended to remove bottlenecks in electricity supply. Growth in output is expected in 2014-15 as investments continue in Lubambe Copper Mine Plc, Konkola Copper Mines Plc as well as First Quantum Minerals Limited’s new Trident Mine. The Group recorded turnover of K520 million (2012: K257 million) and operating profit of K417 million (2012: K367 million). Improved dividend payments from investee companies impacted positively on Group performance. The Group reported a profit before tax of K654 million (2012: K1, 053 million). The Group recorded a profit after tax of K762 million (2012: K1, 238 million). The Group’s share of profit of equity accounted investees reduced to K222 million (2012: K640 million). The Group’s retained earnings as at 31 March 2013 were positive at K4, 018 million (2012: K3, 256 million).The Company’s retained earnings became positive for the first time to K511 million (2012: negative K57 million). Strategic and new investments Ndola Lime Company Limited continued with the rehabilitation of the plant as part of the recapitalisation project of the company. The electrostatic precipitator on the rotary kiln was re-commissioned and a new dust abatement unit on the vertical kiln was installed. ZCCM-IH provided an additional loan of K133 million (2012: K137 million) for the recapitalisation project expected to be commissioned in December 2013.

ZCCM Investments Holdings Plc

5

ZCCM Investments Holdings Plc Annual Report (continued) for the year ended 31 March 2013 CHAIRMAN’S STATEMENT (continued) In September 2012, the Government of the Republic of Zambia (GRZ) gave approval for the conversion of all or part of the GRZ debt owed by ZCCM-IH amounting to K 1.9 billion (approximately US$352 million) into equity through a rights issue. As at 31st March 2013, implementation modalities involving the appointment of the Lead Financial Advisors to undertake the rights issue had progressed. As part of this exercise, a valuation of ZCCM-IH and its investments was conducted to ascertain the appropriate value of ZCCM-IH shares. The valuation has been incorporated in these financial statements. The whole balance sheet restructuring exercise is expected to be completed in 2014. During the period under review, ZCCM-IH and Konkola Copper Mines Plc (KCM) entered into a Settlement Agreement pursuant to which certain outstanding payments owed by KCM to ZCCM-IH and certain contingent amounts payable, under the then existing Price Participation Arrangements (PPAs) which dated back to March 2000 were settled. The PPAs were concurrently terminated. Under the settlement agreement, US$46.3 million was required to be paid by KCM (in instalments) to ZCCM-IH on or before 31 August 2013, and a further US$73.4 million (in instalments) on or before 30 September 2016.

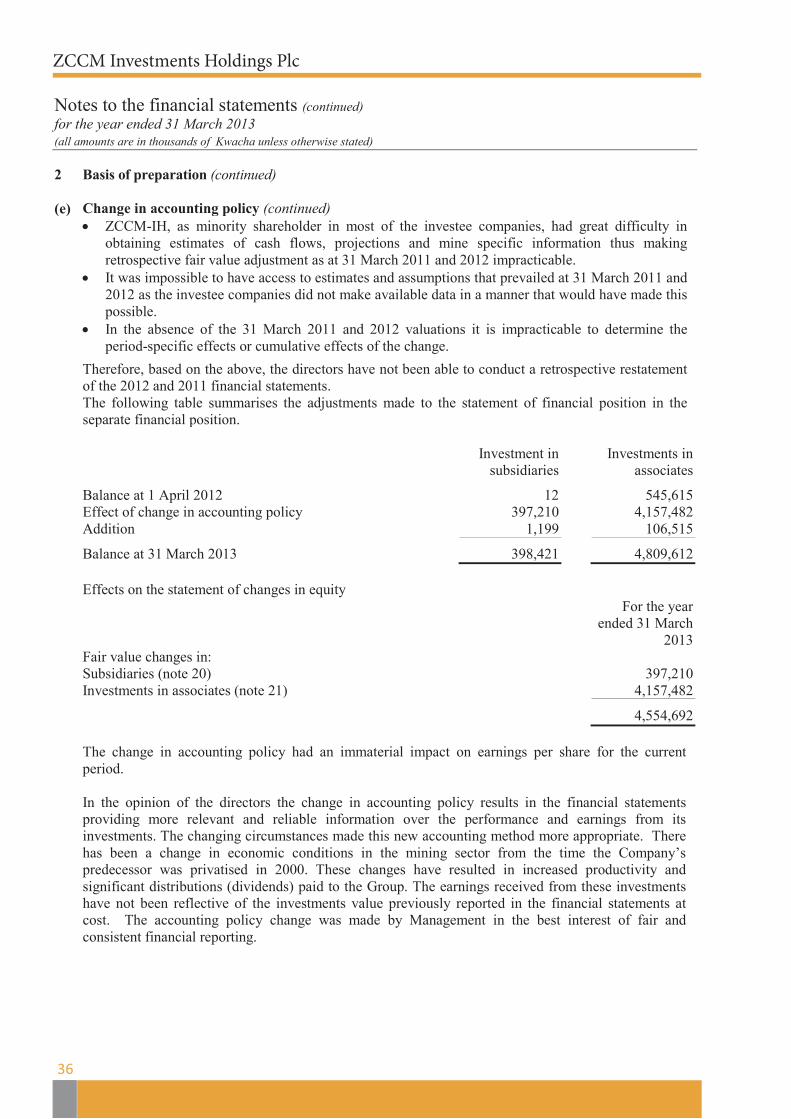

During the financial year under review, GRZ announced the cancellation of the Small Scale Mining Licenses issued to Collum Coal Mining Industries Limited (Collum) situated in Sinazongwe District in the Southern Province of Zambia. Following the cancellation of the licenses, ZCCM-IH applied for and was issued with licences for the coal mine. ZCCM-IH has incorporated Nkandabwe Coal Mine Limited, a 100% subsidiary to operate the coal mine. ZCCM-IH intends to look for strategic partners to work with and develop the mine. Albidon Zambia Ltd was placed under care and maintenance during the financial year under review so as to maintain the investment at Munali. On 28 March 2013, the Board of Albidon Limited announced, that Jin Tuo Investment Limited (a wholly owned subsidiary of Jinchuan Group Resources Holdings Limited, which is itself a majority shareholder of Albidon Limited) had proposed to acquire 100 per cent of the Albidon Limited at a cash price per share of US$0.0025. Subsequent to the financial year under review, the proposal was made to all shareholders other than the Jinchuan Group via a Statutory Merger pursuant to the British Virgin Islands Business Companies Act 2004 (as amended). During the year, the Board of ZCCM-IH resolved to restructure and reorganise the Legal Department. The objective of the restructuring was to separate all legacy matters from current and future business so that the internal legal counsel would focus on current and future business while legacy matters could be handled by external legal counsel. The other objective was to downsize and enhance efficiencies. In this regard, all legacy (historical) related conveyancing and litigation matters were outsourced to an external law firm. As a result of the restructuring the number of staff in the legal department reduced from 26 to 3. Further restructuring decisions were made to the Environment Department. The restructuring of the Environment Department resulted in the formation of a subsidiary company called Misenge Environmental and Technical Services Limited (METS), The objective of the restructuring was to allow ZCCM-IH to be more focused on investment activities while METS would provide environmental management services to ZCCM-IH including taking over all outstanding and future environmental obligations for ZCCM-IH. METS would also provide environment management services to other clients. METS officially commenced operations on 1 February 2013.

ZCCM Investments Holdings Plc

6

ZCCM Investments Holdings Plc Annual Report (continued) for the year ended 31 March 2013 CHAIRMAN’S STATEMENT (continued) Capital market The ZCCM-IH share price on the Lusaka Stock Exchange closed the year at K12.5 (2011; K12.5). The market capitalisation as at 31 March 2013 was K1, 116 million (2012; K1, 116 million). To strengthen corporate governance in investee companies, ZCCM-IH adopted a new policy for the appointment of Representative Directors intended to tap best talent to represent ZCCM-IH on the Boards of Directors of its investee companies. This was done by advertising in the national media for applicants who would be interested in taking up directorships in ZCCM-IH’s investee companies. The applicants were subjected to interviews before selection. To this effect, new ZCCM-IH’s Representative Directors were appointed on the Boards of investee companies in September 2012. Outlook ZCCM-IH remains confident about the fundamentals of the mining industry in general and those of copper in particular. While continued volatility is expected in the short term, the long-term fundamentals for copper are expected to remain strong on the back of continued urbanization in China, India, South East Asia and Africa. The Zambian economy is expected to continue to grow at higher rates than most of the economies in Sub-Saharan Africa premised on increased execution of development projects, investment in transport infrastructure, private investment in existing and new mining operations, and power projects. ZCCM-IH is well positioned to maximise returns from its existing investments currently concentrated in copper mining, as well as pursuing value adding opportunities in other minerals and mining related opportunities. Directorate During the year, there were changes to the Directorate as follows: Dr B K E Ng’andu Appointed 02 April 2012 Non Executive Director Mrs P C Kabamba Appointed 15 January 2013 Non Executive Director Dr A Mwenda Retired 30 June 2012 Non Executive Director Appreciation I extend my gratitude to my fellow Board members, the Management and Staff of ZCCM-IH for their commitment and hard work during the past financial year. I further extend my gratitude to the investee companies for their efforts and contributions in the year. Wila D Mung’omba Executive Chairman of the Board

ZCCM Investments Holdings Plc

7

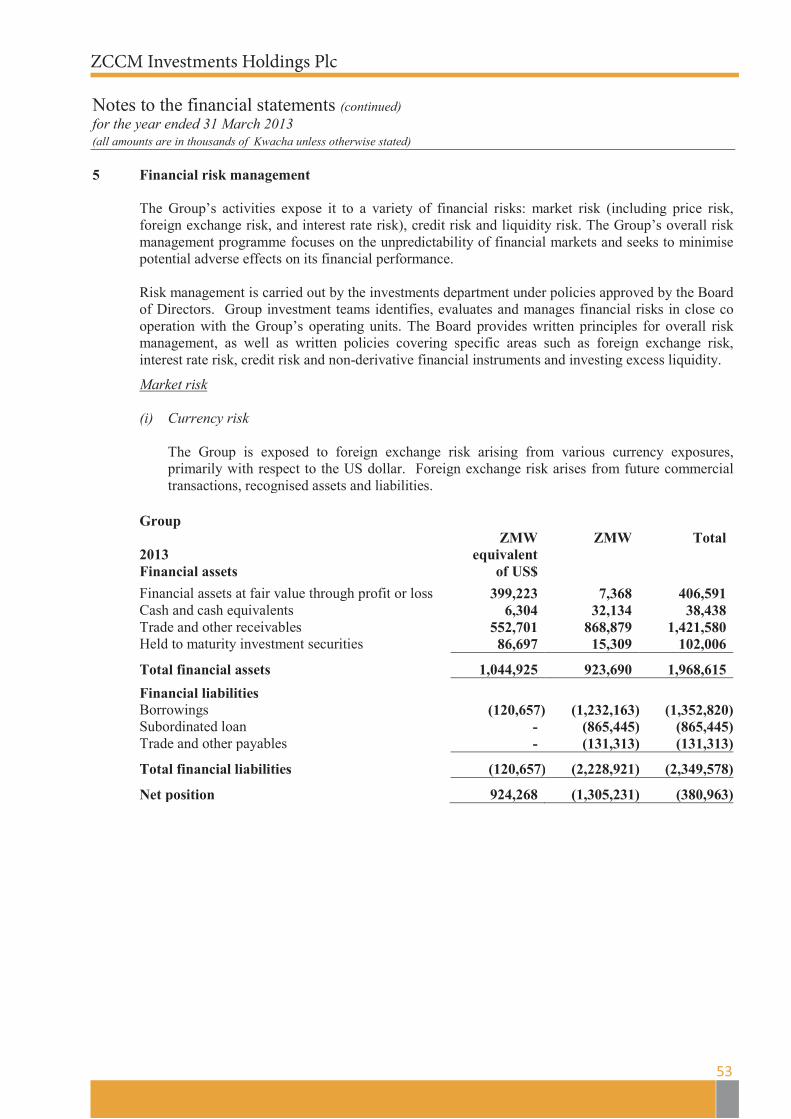

ZCCM Investments Holdings Plc Annual Report (continued) for the year ended 31 March 2013 REPORT OF THE DIRECTORS The Directors submit their report together with the audited financial statements for the year ended 31 March 2013, which disclose the state of affairs of ZCCM Investments Holdings Plc (‘the Company’) and its subsidiaries (together “the Group”). Shareholding The Group has the following interests in the undernoted companies:

1 Ndola Lime Company Limited 2 Misenge Environmental and Technical Services Ltd 3 Kariba Minerals Limited

100.00% 100.00% 50.00%

4 Maamba Collieries Limited 35.00% 5 Konkola Copper Mines Plc 20.60% 6 Kansanshi Mining Plc 20.00% 7 Copperbelt Energy Corporation Plc 20.00% 8 Lubambe Copper Mine Plc 20.00% 9 Luanshya Copper Mines Plc 20.00% 10 NFC Africa Mining Plc 15.00% 11 Chibuluma Mines Plc 15.00% 12 Investrust Bank Plc 10.60% 13 Chambishi Metals Plc 10.00% 14 Mopani Copper Mines Plc 10.00% 15 Albidon Limited 0.98%

Share capital

The authorised share capital of the Company remained unchanged at K 900 000 divided as follows:

54,000,000 “A” Ordinary Shares of K 0.01 each; and 36,000,000 “B” Ordinary Shares of K 0.01 each.

There were no changes in the issued share capital of 89,296,428 shares with a nominal value of K892,964 during the year which remained as detailed below:

Number of shares

Amount K

At beginning and end of year 89,296,428 892,964

ZCCM Investments Holdings Plc

8

ZCCM Investments Holdings Plc Annual Report (continued) for the year ended 31 March 2013 REPORT OF THE DIRECTORS (continued) The shares are held as follows Number of

shares Amount

K “A” shares - Ministry of Finance and National Planning on behalf of the Government of the Republic of Zambia (GRZ)

53,825,808

538,258

“B” shares - Ministry of Finance and National Planning on behalf of the Government of the Republic of Zambia (GRZ)

24,329,828

243,298

“B” Shares - Others 11,140,792 111,408

89,296,428 892,964 The 11,140,792 “B” Ordinary Shares are thinly spread and as at 31 March 2013 were held by 2,317 non-controlling shareholders. Currency rebasing

With effect from 1 January 2013, the Zambian Kwacha was rebased by dividing the currency by a thousand. As part of the process the currency code was changed from ZMK to ZMW although the currency symbol “K” remained unchanged. Consequently, the financial statements are presented in the rebased currency.

ZCCM Investments Holdings Plc

9

ZCCM Investments Holdings Plc Annual Report (continued) for the year ended 31 March 2013 REPORT OF THE DIRECTORS (continued)

PRINCIPAL ACTIVITIES

ZCCM–IH (“ the Company’’) is an investments holdings company which has a primary listing on the Lusaka Stock Exchange and secondary listings on London and Euronext Stock Exchanges. The Company has the majority of its investments held in the copper mining sector of Zambia. Its principal activities include managing the Zambian Government’s stake in the mining sector. Other activities include: Undertaking investment analysis and aligning company operations towards maximising

returns to shareholders; Pursuing investee companies to consistently declare reasonable dividends and company

growth; Ensuring effective representation on the boards of the investee companies; Establishing and securing joint venture partnerships for projects assessed to be viable; and Promoting Zambian ownership and management in mining assets.

Functions and performance of the Group

In its transformed state as an investments holding company, the main functions of the Company are as follows:

to monitor the performance of the investee companies with respect to production and metal prices in order to ensure that commitments agreed upon relating to disbursements are fulfilled on a timely basis;

to continue monitoring production and cost levels in the associate companies. In addition, to ensure collection of price participation payments due;

to anticipate the receipt of deferred sale considerations and ensure that these are received on a timely basis and in the correct amounts;

to ensure that ZCCM-IH environmental obligations under the transaction documents are complied with;

to ensure that environmental obligations continued to be attended to through different levels of participation. The Company undertook remedial environmental measures through its Environmental Department up to 31 January 2013 when provision of environmental services was outsourced to METS; and

to liaise with prospective greenfield investors in the mining and minerals industry who will enter into agreements with the Government. The Group has continued to liaise with greenfield investors.

CORPORATE GOVERNANCE

The Group continued to operate by enforcing good corporate governance practices and observing the separation of powers between the Directors and Management on one hand and the Chairman of the Board and the Chief Executive Officer on the other. All Directors on the Board except for the Chairman were non-executive during the financial year.

Activities were further streamlined by the full utilisation of the existing Audit, Remuneration and Investments Committees of the Board whose membership as at the date of this report (08 November 2013) is indicated below:

ZCCM Investments Holdings Plc

10

ZCCM Investments Holdings Plc Annual Report (continued) for the year ended 31 March 2013 REPORT OF THE DIRECTORS (continued)

CORPORATE GOVERNANCE (continued)

Audit Committee

Remuneration Committee

Mr. C Mwananshiku (Chairperson) Mr. J M D Patterson Ms. S Mutemba Mrs. P C Kabamba

Dr.B K E Ng’andu (Chairperson) Ms. S Mutemba Mr.C Mwananshiku Dr.V Mutambo

Investments Committee

Mr. J M D Patterson Mrs P C Kabamba Dr.V Mutambo Dr. B K E Ng’andu Mr.M Muyunda Mr. M T Chipata Ms. M Chanda Mr.C Mpundu Mr.B Nundwe Mr.A Chimpwende

Chairperson Chief Executive Officer Chief Financial Officer Chief Operating Officer Co-opted Investments Expert Co-opted Investments Expert Co-opted Investments Expert

Average number and remuneration of employees

The total remuneration of employees during the year amounted to K90.6 million (2012: K53.9 million) for the Group and K28 million (2012: K23.2 million) for the Company. The average number of employees was as follows:

Month Subsidiaries Company Group Month Subsidiaries Company Group

April 2012 455 85 540 October 2012 457 87 544 May 2012 455 87 542 November 2012 448 64 512 June 2012 453 86 539 December 2012 443 64 507 July 2012 454 85 539 January 2013 444 65 509 August 2012 438 86 524 February 2013 468 58 526 September 2012 436 86 522 March 2013 465 60 525

Staff expenses 2013 2012

Subsidiary Companies 62,577 30,711 ZCCM-IH 27,981 23,157 90,558 53,868

Signed on their behalf by: ........................................ ......................................... Director Director

ZCCM Investments Holdings Plc

11

ZCCM Investments Holdings Plc Annual Report (continued) for the year ended 31 March 2013 OPERATIONS REPORT

(A) Subsidiary Companies’ Performance

The performance of the subsidiary companies for the year ended 31 March 2013 is summarised below: 1 Ndola Lime Company Limited

Total revenue for the financial year ended 31 March 2013 was K214.6 million (2012:K177.6 million). The company reported a loss before tax of K 30.5 million (2012:profit K 5.4 million). The loss after tax was K 22.9 million (2012:loss K 6.2 million).

The company also exported goods amounting to K 23.4 million (2012: K 40.6million).

During the year, the company strengthened its mining operations by purchasing two terex dump trucks and water bowsers. The electrostatic precipitator on the rotary kiln was recommissioned and operations were satisfactory. A new dust abatement unit was installed on the vertical kiln and is at commissioning stage.

Construction of Vertical Kiln and Anxiliary Plants, and the new Hydrator

The Company obtained an additional loan of K133 million from ZCCM Investments Holdings Plc for the completion of the recapitalisation project. Civil works for the new vertical kiln were completed and mechanical erection commenced in February 2013. Hot commissioning of the vertical kiln is expected to commence in December 2013.

Through certification audits conducted by the British Standards Institute (BSI), Ndola Lime Company was recommended for certification to the internationally recognised ISO14001:2004 and OHSAS 18001:2007 for Environmental Management System and Occupational Health and Safety respectively.

There were no dividends paid during the year (2012: Nil).

ZCCM Investments Holdings Plc

12

ZCCM Investments Holdings Plc Annual Report (continued) for the year ended 31 March 2013 OPERATIONS REPORT (continued) (A) Subsidiary Companies’ Performance (continued)

2 Misenge Environmental and Technical Services Limited

Misenge Environmental and Technical Services Limited (METS) officially commenced operations on 1 February 2013. METS realised total revenue of K203, 903 during the two months of operation in February and March 2013.

The company has started preparing a strategic plan for the period 2013 to 2016 for the provision of environmental and technical services to ZCCM-IH and other clients. The main focus during the strategic period will be to grow the revenue to K 51.5 million which translates into a growth of 8% annually.

There were no dividends paid during the year (2012: Nil).

(B) Associate Companies’ Performance

The performance of investee companies for the year ended 31 March 2013 is summarised below:

1 Kariba Minerals Limited (KML)

For the financial period ended 31 March 2013, Kariba Minerals Limited (KML) had a turnover of K2.6 million (2012: K7.8 million) with a loss after tax for the year of K 6.7 million. ZCCM-IH and Gemfields advanced a total of US$2.5 million (K13.5 million) loan to the company to finance acquisition of mining equipment and working capital requirements. The equipment has been commissioned. ZCCM-IH advanced a loan balance of US$1.25 million (K6.6 million) from the above amount as at end of year.

With the arrival of new mining equipment and washing plant, the operations are expected to be more mechanised and cost efficient requiring less manpower and therefore in line with the company’s business plan, the workforce has been reduced from 224 to 164 as at 31 March 2013 and all benefits for the separated employees have since been paid.

There were no dividends paid during the year (2012: Nil).

2 Maamba Collieries Limited (MCL)

During the year to 31 March 2013, Maamba Collieries Limited (MCL) reported a total revenue of K15.1 million (2012: K1.5 million) and a net loss of K55.5 million (2012: K8.8 million). The strategic thrust remains in power generation using thermal grade coal to add value to the mining function as a path to viability. MCL has retained ABSA Capital Consortium (ABSA) as the mandated lead arranger to arrange up to US$ 508 million through International Commercial Banks and Development Financial Institutions (DFIs) to partially finance the integrated coal mine revamping and thermal power plant projects. ABSA circulated the Project Information Memorandum (PIM) to all shortlisted prospective lenders.

ZCCM Investments Holdings Plc

13

ZCCM Investments Holdings Plc

Annual Report (continued) for the year ended 31 March 2013

OPERATIONS REPORT (continued) (B) Associate Companies’ Performance (continued)

2 Maamba Collieries Limited (MCL) (continued)

Ongoing construction at Maamba Power Plant

Some of the issues for project finance from likely financiers include the credit enhancement mechanism for receivables and the lack of progress on grid up-gradation work by Zambia Electricity Supply Corporation Limited (ZESCO). MCL is also exploring options other than those loans backed by Sinosure support (ECA) and by DFIs. These options include loans from commercial banks backed by Political Risk Insurance (PRI) cover. MCL expects financial closure to occur by February 2014, assuming that the external concerns on the Escrow arrangement and the grid up-gradation works of ZESCO are resolved to the lenders’ satisfaction. MCL has received the detailed indicative term sheet from the lenders advisor, which would undergo some changes based on the terms approved by the credit committee of each of the banks.

There were no dividends paid during the year (2012: Nil).

3 Konkola Copper Mines Plc (KCM)

KCM’s medium-long term outlook remains dependent on the Konkola Ore Body Expansion (KOBE) Project. The objective of the project is to ensure continuity of mining at Konkola Mine, expand production from the current 2 million metric tonnes of ore per annum to final ramp up level of 7.5 million metric tonnes per annum and extend the life of the mine by up to 30 years. Finished copper production will increase from the current level of approximately 50,000 tonnes per annum to approximately 210,000 tonnes per annum.

On 11 February 2013, ZCCM-IH Plc and Konkola Copper Mines Plc (KCM) entered into a settlement agreement, pursuant to which certain outstanding payments owed by KCM to ZCCM-IH and certain contingent amounts payable under the then existing Price Participation Arrangements (PPAs) which dated back to March 2000 were settled. The PPAs were concurrently terminated. Under the settlement agreement, US$46.3 million was required to be paid by KCM (in instalments) to ZCCM-IH on or before 31 August 2013, and a further US$73.4 million (in instalments) on or before 30 September 2016.

KCM declared a total of K400.37 million (US$75 million) as dividend on 20 October 2012 in respect of the financial year ended 31 March 2013 (2012: Nil). The amount payable to ZCCM-IH was K82.6 million (2012: K8.5 million).

ZCCM Investments Holdings Plc

14

ZCCM Investments Holdings Plc Annual Report (continued) for the year ended 31 March 2013 OPERATIONS REPORT (continued)

(B) Associate Companies’ Performance (continued)

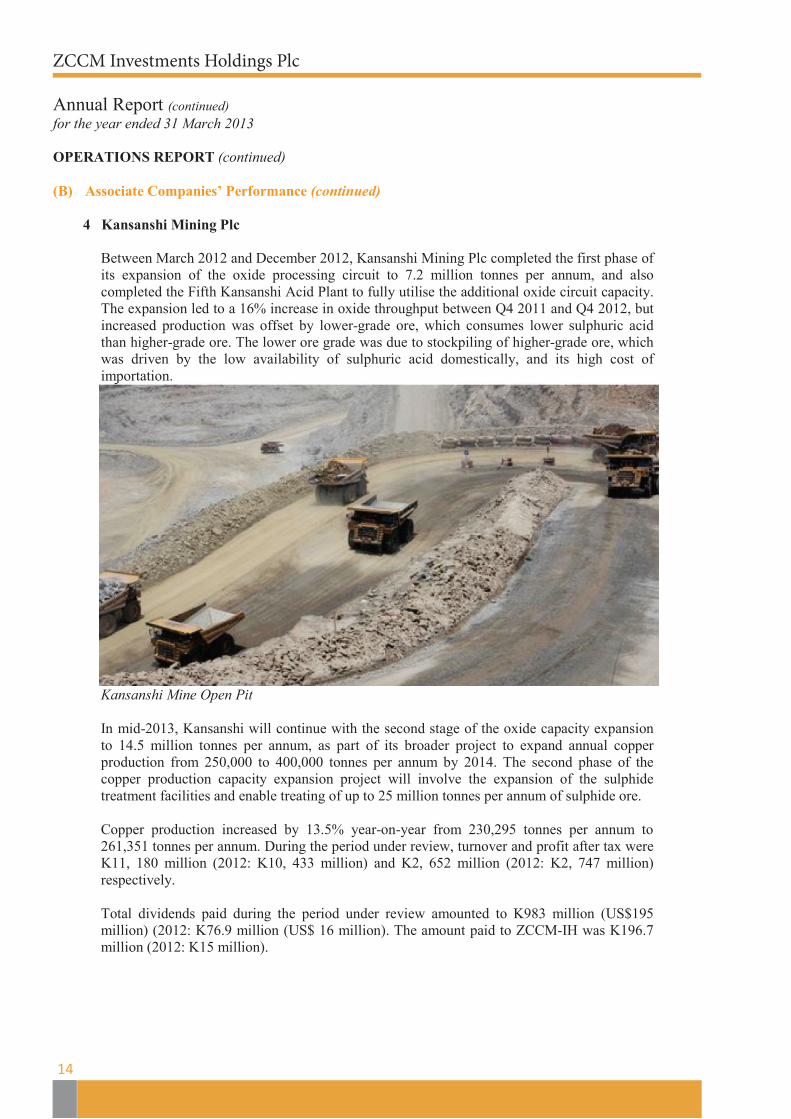

4 Kansanshi Mining Plc

Between March 2012 and December 2012, Kansanshi Mining Plc completed the first phase of its expansion of the oxide processing circuit to 7.2 million tonnes per annum, and also completed the Fifth Kansanshi Acid Plant to fully utilise the additional oxide circuit capacity. The expansion led to a 16% increase in oxide throughput between Q4 2011 and Q4 2012, but increased production was offset by lower-grade ore, which consumes lower sulphuric acid than higher-grade ore. The lower ore grade was due to stockpiling of higher-grade ore, which was driven by the low availability of sulphuric acid domestically, and its high cost of importation.

Kansanshi Mine Open Pit In mid-2013, Kansanshi will continue with the second stage of the oxide capacity expansion to 14.5 million tonnes per annum, as part of its broader project to expand annual copper production from 250,000 to 400,000 tonnes per annum by 2014. The second phase of the copper production capacity expansion project will involve the expansion of the sulphide treatment facilities and enable treating of up to 25 million tonnes per annum of sulphide ore.

Copper production increased by 13.5% year-on-year from 230,295 tonnes per annum to 261,351 tonnes per annum. During the period under review, turnover and profit after tax were K11, 180 million (2012: K10, 433 million) and K2, 652 million (2012: K2, 747 million) respectively. Total dividends paid during the period under review amounted to K983 million (US$195 million) (2012: K76.9 million (US$ 16 million). The amount paid to ZCCM-IH was K196.7 million (2012: K15 million).

ZCCM Investments Holdings Plc

15

ZCCM Investments Holdings Plc

Annual Report (continued) for the year ended 31 March 2013 OPERATIONS REPORT (continued) (B) Associate Companies’ Performance (continued)

5 Copperbelt Energy Corporation Plc (CEC)

Copperbelt Energy Corporation Plc (CEC) revenue increased from K 1,172 million for the period to 31 March 2012 to K 1,353 million for the period to 31 March 2013. The net profit to 31 March 2013 was K 111 million (2012: K 115 million). The feasibility study of the Kabompo Hydro Power Project (KHPP) was completed during the year, and the Environmental Impact Assessment was conditionally approved by the Zambia Environmental Management Agency. Sinohydro Corporation Limited emerged as the preferred contractor with the Engineering, Procurement and Construction contract initialized. The project is expected to reach financial closure in the third quarter of 2013, after which construction is expected to commence.

Part of CEC Infrastructure The company also incorporated CEC Africa Limited (Mauritius), in which it will retain a partial equity stake, and which vehicle will drive its Africa growth strategy. Pilot investments will include the acquisition of 60% of the Abuja Electricity Distribution Company (“AEDC”) in the Abuja district of Nigeria and the development of a 120MW Heavy Fuel Oil Power Plant in Arandis, Namibia. The Sale and Purchase Agreement for the AEDC was signed on 21st February 2013, for a purchase consideration of US$ 164 million for a 60% stake in the company. The average maximum demand for the year ended December 2012 increased by 9.6% from 481.2MW in 2011 to 527.4MW in 2012. Collectively, the NFC South East Project (additional 45MW in 2013), the Mopani Synclinorium Project (additional 25MW in 2013), China Copper Mines (5MW in Q1 2013) and Lubambe Copper Mine (additional 15MW) are expected to add an additional 90MW of load in the medium-term.

ZCCM Investments Holdings Plc

16

ZCCM Investments Holdings Plc

Annual Report (continued) for the year ended 31 March 2013

OPERATIONS REPORT (continued)

(B) Associate Companies’ Performance (continued) 5 Copperbelt Energy Corporation Plc (CEC) (continued)

The CEC Plc’s share price on the LuSE increased from K 0.65 as at end of April 2012 to K0.83 at end of March 2013, representing a 27.9% capital gain year-on-year. CEC Plc paid dividends of K 55 million during the period under review. The amount paid to ZCCM-IH was K11 million (2012: K12 million).

6 Lubambe Copper Mine Ltd

In July 2012 the Konkola North Project Copper Mines (Konnoco) was renamed Lubambe Copper Mine Plc (LCM). The mine is a modern facility, with fully mechanised underground operations, that was completed two months ahead of schedule and delivered the first copper concentrate in October 2012. The mine is expected to produce 45,000 tonnes of contained copper by 2015 at a steady pace and employ 1,500 people. The total cost of the project is US$456 million. Construction of the concentrator plant was completed in September 2012 which was also completed two months ahead of schedule. Copper concentrate produced by Lubambe will be sold for smelting and refining within Zambia. All the copper concentrate sale agreements have been agreed and signed and the first concentrate was sold in October 2012.

The extension of the LCM includes the expansion of operations into an area six kilometres south of the current mine and within the allocated Large-scale Mining License area. A feasibility study into the viability of the extension is forecast to be completed by the first half of 2014. There were no dividends paid during the year (2012: Nil).

7 CNMC Luanshya Copper Mines plc

Turnover for the period to 31 March 2013 was K1, 093 million and the loss after tax was K7.9 million. The Muliashi Project was commissioned in March 2012. However, low oxide ore grades and below-capacity production led to sub-optimal production performance. The Ore grades were low at 1%, whilst production levels were at 20% capacity. The capacity constraint occurred owing to the natural overlay of friable ore over competent ore, which warrants that friable ore is mined first in order to obtain competent ore. In addition, the delay in the completion of a Heap Leach System to process competent ore further impeded production.

ZCCM Investments Holdings Plc

17

ZCCM Investments Holdings Plc

Annual Report (continued) for the year ended 31 March 2013

OPERATIONS REPORT (continued)

(C) Associate Companies’ Performance (continued)

7 CNMC Luanshya Copper Mines plc (continued)

CLM infrastructure As at 31 March 2013 US$391.29 million was invested in Muliashi. At the same date, only 3,945 tonnes of copper metal in concentrate was produced, finishing 20.76%, lagging behind the quarterly plan. The failure is attributed to two key factors. Firstly, the mining condition is not favourable; especially with loose rocks and bad hangings. In the first quarter, some areas underground collapsed which affected production. Secondly, Baluba mine is a marginal mine with low-grade resources, thus negatively affecting the copper metal yield. Overall profitability remained low owing to low production levels at both the Muliashi and Baluba mines. Going forward, mining at Baluba will still prove to be difficult owing to the high operating costs and the low ore grade. The Muliashi mine has insufficient competent ore whilst the high competent fine ore will increase the burden of agitation and adversely impact the leaching rate of heap leaching and high power cost from electrical heating. There were no dividends paid during the year (2012: Nil).

(C) Associate Companies’ Performance (continued)

ZCCM Investments Holdings Plc

18

ZCCM Investments Holdings Plc

Annual Report (continued) for the year ended 31 March 2013

OPERATIONS REPORT (continued) (C) Other Investments

1 NFC Africa Mining Plc (NFCA)

At NFC Africa, capital expenditure in the financial year ended December 2012 amounted to US$ 26.91 million on the South East Ore body project. It is expected that the total investment will reach approximately US$830 million, with construction over a period of 5 years, and with a labour-force of 5,000.

NFCA Infrastructure Loan financing of US$ 548 million will be acquired from the Export-Import Bank of China to part-finance the South East Ore body project.

There were no dividends paid during the year (2012: Nil).

2 Chibuluma Mines Plc

Chibuluma Mines Plc (CMP) current mining reserves will be exhausted by 2017. Currently, exploration works are progressing at: • Chifupu, where deposit mineral resources have been doubled by additional drilling at

depth in 2011 and 2012. Early indications point to an increase of 800,000 tons, with drilling completion planned for May 2013;

• Chibuluma West Mine, no ore intersections have been recorded in the first two holes drilled in the Kalulushi Anticline region, to the south-west of the West Chibuluma mine;

• Deepening of the South Mine, where drilling was completed in Q3 and confirmed that the Chibuluma South ore-body has pinched out at 600 meters, with no further work planned; and

ZCCM Investments Holdings Plc

19

ZCCM Investments Holdings Plc

Annual Report (continued) for the year ended 31 March 2013

OPERATIONS REPORT (continued)

(C) Other Investments (continued)

3 Chibuluma (continued)

• Chibuluma has been awarded an exploration licence in the area between the

Chibuluma South and West mining licences areas.

For the financial year ended 31 December 2012, CMP had revenue of US$142.6 million, a 2.7% drop from the US$$146.6 million achieved the previous year. The profit for the year was US$30.3 million (2011: US$22.1 million). Chibuluma paid a total of K101 million (K186.8 million in 2012) in dividends for the period to 31 March 2013. The amount paid to ZCCM-IH was K15.2 million (2012: K20 million).

4 Investrust Bank Plc

During the year, the Bank embarked on an ambitious branch expansion programme. It completed and opened the Levy Business Park Branch in April 2012 and initiated works on construction of Kabwe Branch (completed in January 2013), Lusaka Mumbwa Road Agency, branches in Ndola, Choma and Mongu. The Bank also rolled out its branding program and installed state-of-the-art signage at head office and a number of existing and new branch locations. The Bank also re-organised and improved on its credit function by introducing a Credit Risk Management unit alongside the Credit Control unit and strengthened its credit underwriting, review and control processes. The Corporate and Investment Banking unit was also augmented by the appointment of the Head Corporate and Investment Banking and the appointment of additional Relationship Managers. The Bank introduced more products onto its portfolio and launched InvestMobile and extended the use of InvestNet to payment of selected utility bills. The Bank aggressively marketed and popularised the use of its VISA Green Card and recorded massive improvement in its utilisation rate. In 2013 and beyond the Bank will continue its systematic expansion programme and consolidation of its existing operations in all new business units to prop up levels of efficiencies and effectiveness to boost overall bank profitability. The Bank did not declare any dividends in the period under review. The Bank’s share price on the LuSE closed the period under review at K 14.90 (2012: K18.00). There were no dividends paid during the year (2012: Nil).

ZCCM Investments Holdings Plc

20

ZCCM Investments Holdings Plc

Annual Report (continued) for the year ended 31 March 2013

OPERATIONS REPORT (continued)

(C) Other Investments (continued)

5 Chambishi Metals Plc

At Chambishi Metals Plc (Chambishi), losses persisted owing to the delay of the installation of a new roaster, which is expected to increase processing capacity to 55,000 tonnes per annum. However, following the successful installation of additional Solvent Extraction and Electrowinning (SE/EW) capacity in 2012, copper processing is expected to surge from 6,900 tons to between 20,000 tonnes and 25,000 tonnes in 2013.

Chambishi Metals Plc Infrastructure Power shortages affected the quality of production and repair costs. A voltage regulator will be installed in 2013 to minimize damages to equipment and in turn reduce repair costs. The installation of a second roaster is expected to be completed in 2014. This is expected to aid future profitability at Chambishi. Feasibility studies have commenced in this regard, and the second roaster is expected to increase copper production capacity from 35,000 tonnes per annum to 55,000 tonnes per annum, with the Frontier and BOSS mines in the Democratic Republic of Congo providing the concentrates to meet the additional capacity.

There were no dividends paid during the year (2012: Nil).

ZCCM Investments Holdings Plc

21

ZCCM Investments Holdings Plc

Annual Report (continued) for the year ended 31 March 2013

OPERATIONS REPORT (continued)

(C) Other Investments (continued)

6 Mopani Copper Mines Plc

During the year ended December 2012, US$ 53 million was spent on the new Synclinorium shaft with major milestones completed this year including starting the construction of the permanent Winder House and the start of the vent shaft pre-sink. The project continues to remain on target to be completed at a total cost of approximately US$ 323 million by the end of 2015 and will significantly extend the economic life of Mopani's operations. In 2012, Mopani announced that the smelter upgrade project (including improving SO2 emission capture to above 97%) is expected to be completed by December 2013, 18 months ahead of schedule. Mopani recorded a decline in revenue from US$ 1,152 million for the year ended December 2011 to US$1,053 million in 2012. Profit after tax in 2012 was US$31million (2011:US$111.7 million). Over the same period, Mopani processed 187,100 tonnes of copper representing a 2% decline year-on-year, and it produced 99,000 tonnes of copper representing an 8% decline year-on-year. The remaining 88,100 tonnes of copper processed was sourced from third parties. The decline in production resulted from the temporary suspension of the heap leach process earlier in the year There were no dividends paid during the year (2012: Nil).

7 Albidon Limited (Munali Nickel project)

Albidon Zambia Ltd was placed under care and maintenance in the period under review so as to maintain the investment at Munali. All staff at the Company were given notices of their redundancies in line with the Zambian law. On the US$12 million tax liability, a delegation from Albidon was advised by the Zambia Revenue Authority (ZRA) that whilst an arrangement could be entered into with the ZRA with respect to a deferred payment plan for the tax, the only way that the liability could be extinguished would be by way of a ‘Statutory Instrument’ (SI) issued by the GRZ.

As there remained ongoing uncertainty as to the Company’s financial future, the Company’s securities remained in voluntary suspension on the Australian Securities Exchange.

ZCCM Investments Holdings Plc

22

ZCCM Investments Holdings Plc Annual Report (continued) for the year ended 31 March 2013

Corporate social responsibility and environmental review (A) Corporate Social Responsibility

The Company’s focus on meeting its social obligations continued during the year, and was to be undertaken through completion of implementation of environmental programmes by the Company’s Environmental Department up to 31 January 2013 and thereafter through METS.

(B) Environmental Review

The two subprojects on the Copperbelt which had not been completed before closure of the Copperbelt Environment Project (CEP) on 31 March 2011 were still not completed in the financial year ended 31 March 2013. The following are the major highlights of environmental activities undertaken during the year:

i) ZCCM-IH successfully disposed, in an environmentally sound manner, the stock of

redundant chemicals which were collected from privatised mines in 2000 and kept in interim storage.

ii) During the year, implementation of the Integrated Case Management (ICM) of children with elevated blood lead levels continued with household interviews, standardized physical examination and treatment at health centers. In addition, an outreach programme involving all parts of the community, providing guidance and education on minimizing exposure to lead continued in identified areas in Kabwe.

iii) A Knowledge, Attitude, Beliefs and Practise (KABP) survey phase 2 was conducted during the year to assess behavioural changes in the lead impacted communities of Kabwe.

iv) Monitoring of the physical integrity of Tailings Dams (TD) and overburden dumps

continued during the year and where necessary, minor maintenance works were done. Feasibility studies by SINO Metals Plc to establish potential for reprocessing of two TDS in Mufulira (TD10 and TD8) continued during the year.

v) ZCCM-IH transferred the responsibility of managing open pits numbers 1, 2 and a

combination of pits 5 and 6 at Kabwe Mine site to Enviro Props Limited after the mine licences area was transferred to the new owners.

Mukela Muyunda Lusaka Chief Executive Officer November 2013

ZCCM Investments Holdings Plc

23

ZCCM Investments Holdings Plc Directors' responsibilities in respect of the preparation of financial statements The directors are responsible for the preparation and fair presentation of the consolidated and separate annual financial statements of ZCCM Investments Holdings Plc, comprising the statements of financial position at 31 March 2013, the statements of comprehensive income, changes in equity and cash flows for the year then ended, and the notes to the financial statements, which include a summary of significant accounting policies and other explanatory notes, in accordance with International Financial Reporting Standards and the requirements of the Companies Act of Zambia. In addition, the directors are responsible for preparing the chairman and directors’ report. The directors are also responsible for such internal controls as they determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error and for maintaining adequate accounting records and an effective system of risk management. The directors have made an assessment of the company and its subsidiaries to continue as going concerns and have no reason to believe the business will not be going concerns in the year ahead. The auditor is responsible for reporting on whether the consolidated and separate financial statements are fairly presented in accordance with the applicable financial reporting framework. Approval of the financial statements The consolidated and separate annual financial statements of ZCCM Investments Holdings Plc, as identified in the first paragraph, were approved by the board of directors on 25 November 2013 and signed on its behalf by: .............................................. ............................................. Director Director

ZCCM Investments Holdings PlcZCCM Investments Holding Plc

24 KPMG Chartered Accountants, a Zambian Partnership, is a

member firm of the KPMG network of independent member firms affiliated with KPMG International cooperative (“KPMG International”), .a Swiss entity. All rights reserved.

Partners: A list of the partners is available at the above mentioned address

Independent auditor’s report to the shareholders of ZCCM Investments Holdings Plc Report on the financial statements

We have audited the consolidated and separate financial statements of ZCCM Investments Holdings Plc, which comprise the statements of financial position as at 31 March 2013, and the statements of comprehensive income, changes in equity and cash flows for the year then ended, and the notes to the financial statements which include a summary of significant accounting policies and other explanatory notes as set out on pages 26 to 93.

Directors’ responsibility for the financial statements

The Company’s Directors are responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards and the requirements of the Companies Act of Zambia, and for such internal control as the directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgement, including the assessment of the risk of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, we consider internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

KPMG Chartered Accountants First Floor, Elunda Two Addis Ababa Roundabout Rhodes Park, P.O Box 31282 Lusaka Zambia

Telephone +260 2 11372900

Website www.kpmg.com/zm

ZCCM Investments Holdings Plc

25

Opinion

In our opinion, these financial statements present fairly, in all material respects, the consolidated and separate financial position of ZCCM Investments Holdings Plc as at 31 March 2013, and its consolidated and separate financial performance and consolidated and separate cash flows for the year then ended in accordance with International Financial Reporting Standards and the requirements of the Companies Act of Zambia.

Report on other legal and regulatory requirements

In accordance with Section 173 (3) of the Companies Act of Zambia, we report that, in our opinion, the required accounting records, other records and registers have been properly kept in accordance with the Act. KPMG Chartered Accountants 2013 Lusaka, Zambia

Jason Kazilimani, Jr Partner

ZCCM Investments Holdings Plc

26

ZCCM Investments Holdings Plc

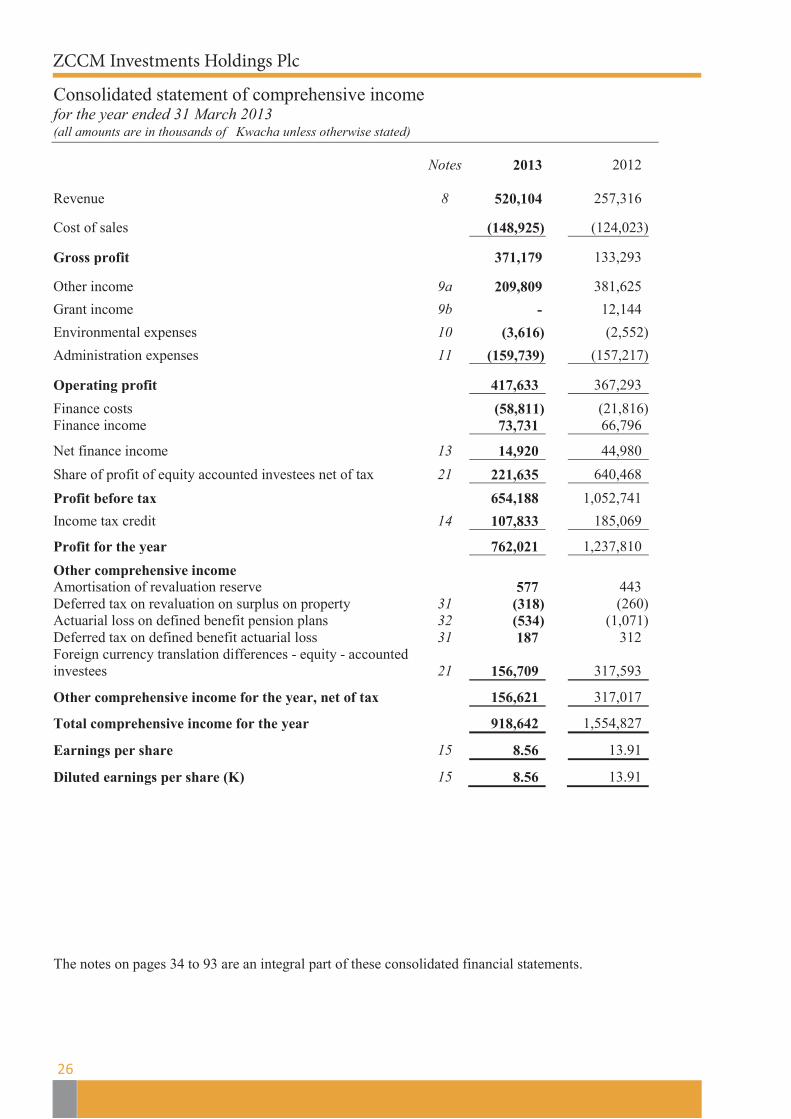

Consolidated statement of comprehensive income for the year ended 31 March 2013 (all amounts are in thousands of Kwacha unless otherwise stated)

Notes 2013

2012

Revenue 8 520,104 257,316 Cost of sales (148,925) (124,023) Gross profit 371,179 133,293 Other income 9a 209,809 381,625

Grant income 9b - 12,144

Environmental expenses 10 (3,616) (2,552)

Administration expenses 11 (159,739) (157,217) Operating profit 417,633 367,293

Finance costs (58,811) (21,816) Finance income 73,731 66,796

Net finance income 13 14,920 44,980

Share of profit of equity accounted investees net of tax 21 221,635 640,468

Profit before tax 654,188 1,052,741

Income tax credit 14 107,833 185,069

Profit for the year 762,021 1,237,810

Other comprehensive income Amortisation of revaluation reserve 577 443 Deferred tax on revaluation on surplus on property 31 (318) (260) Actuarial loss on defined benefit pension plans 32 (534) (1,071) Deferred tax on defined benefit actuarial loss 31 187 312 Foreign currency translation differences - equity - accounted investees 21 156,709 317,593

Other comprehensive income for the year, net of tax 156,621 317,017

Total comprehensive income for the year 918,642 1,554,827

Earnings per share 15 8.56 13.91

Diluted earnings per share (K) 15 8.56 13.91 The notes on pages 34 to 93 are an integral part of these consolidated financial statements.

ZCCM Investments Holdings Plc

27

ZCC M Investments Holdings Plc

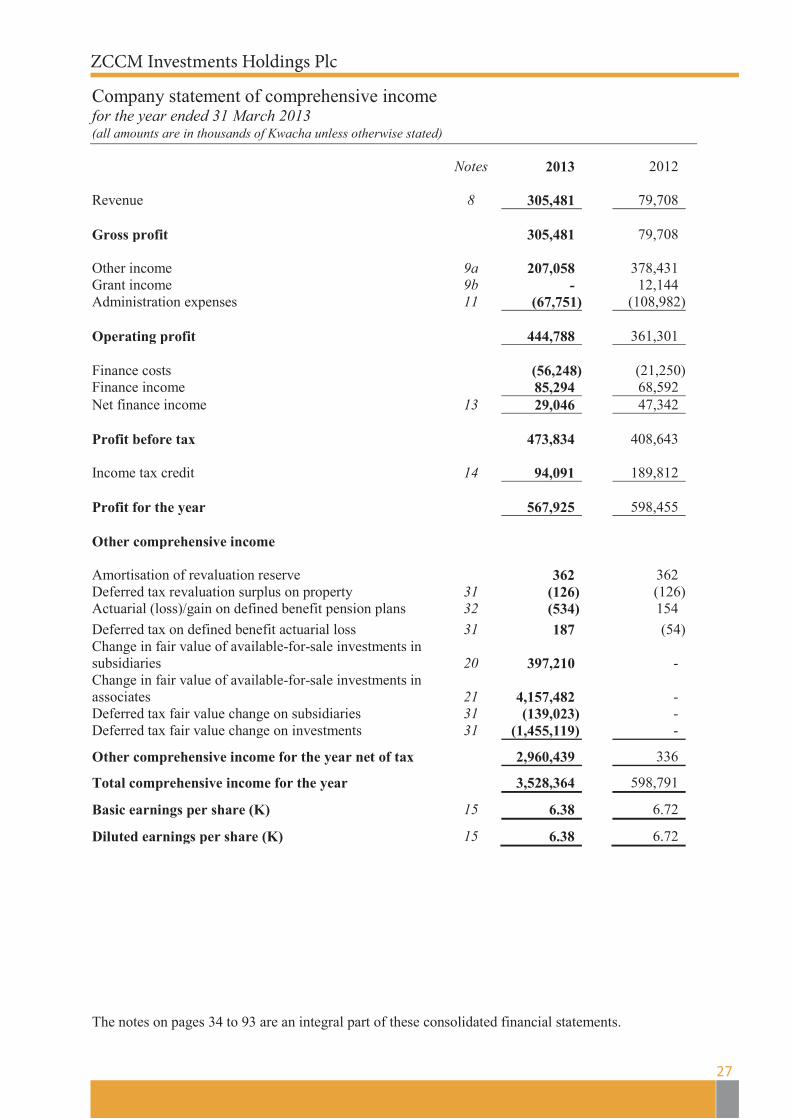

Company statement of comprehensive income for the year ended 31 March 2013 (all amounts are in thousands of Kwacha unless otherwise stated) Notes 2013

2012

Revenue 8 305,481 79,708 Gross profit 305,481 79,708 Other income 9a 207,058 378,431 Grant income 9b - 12,144 Administration expenses 11 (67,751) (108,982) Operating profit 444,788 361,301 Finance costs (56,248) (21,250) Finance income 85,294 68,592 Net finance income 13 29,046 47,342 Profit before tax 473,834 408,643 Income tax credit 14 94,091 189,812 Profit for the year 567,925 598,455 Other comprehensive income Amortisation of revaluation reserve 362 362 Deferred tax revaluation surplus on property 31 (126) (126) Actuarial (loss)/gain on defined benefit pension plans 32 (534) 154 Deferred tax on defined benefit actuarial loss 31 187 (54) Change in fair value of available-for-sale investments in subsidiaries 20 397,210 - Change in fair value of available-for-sale investments in associates 21 4,157,482 - Deferred tax fair value change on subsidiaries 31 (139,023) - Deferred tax fair value change on investments 31 (1,455,119) -

Other comprehensive income for the year net of tax 2,960,439 336

Total comprehensive income for the year 3,528,364 598,791

Basic earnings per share (K) 15 6.38 6.72

Diluted earnings per share (K) 15 6.38 6.72 The notes on pages 34 to 93 are an integral part of these consolidated financial statements.

ZCCM Investments Holdings Plc

28

ZCC M Investments Holdings Plc

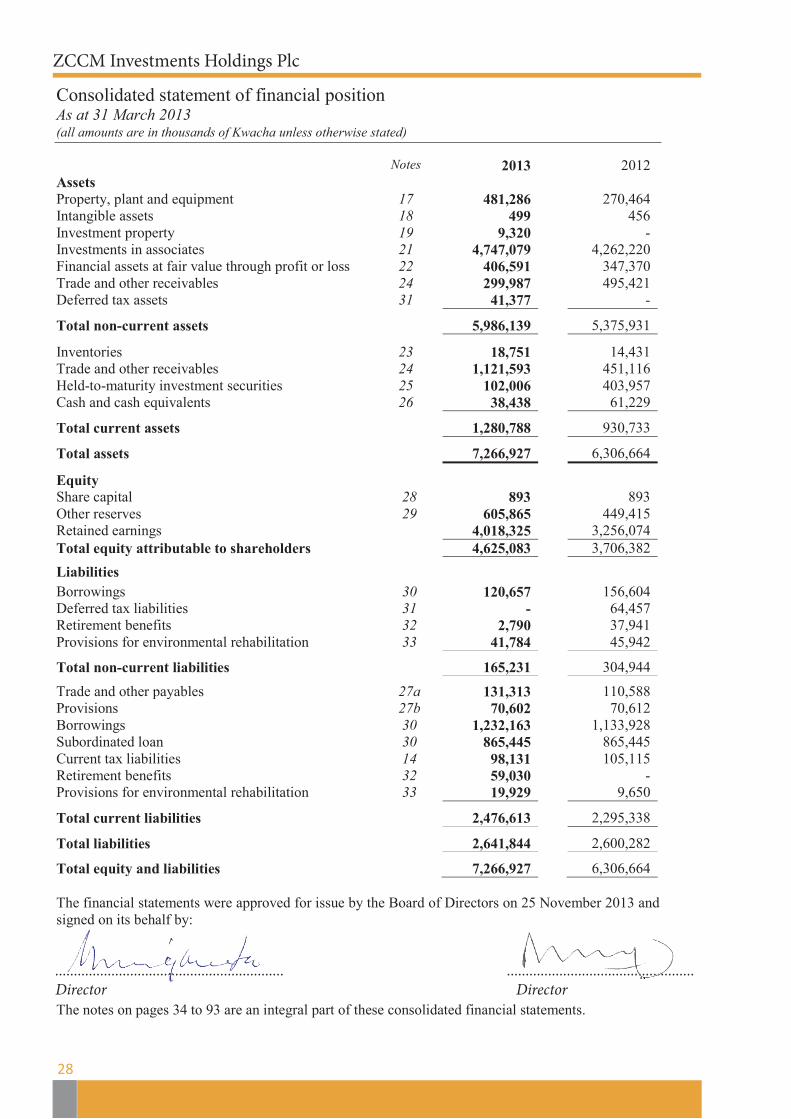

Consolidated statement of financial position As at 31 March 2013 (all amounts are in thousands of Kwacha unless otherwise stated) Notes 2013 2012 Assets Property, plant and equipment 17 481,286 270,464 Intangible assets 18 499 456 Investment property 19 9,320 - Investments in associates 21 4,747,079 4,262,220 Financial assets at fair value through profit or loss 22 406,591 347,370 Trade and other receivables 24 299,987 495,421 Deferred tax assets 31 41,377 -

Total non-current assets 5,986,139 5,375,931

Inventories 23 18,751 14,431 Trade and other receivables 24 1,121,593 451,116 Held-to-maturity investment securities 25 102,006 403,957 Cash and cash equivalents 26 38,438 61,229

Total current assets 1,280,788 930,733

Total assets 7,266,927 6,306,664

Equity Share capital 28 893 893 Other reserves 29 605,865 449,415 Retained earnings 4,018,325 3,256,074 Total equity attributable to shareholders 4,625,083 3,706,382

Liabilities Borrowings 30 120,657 156,604 Deferred tax liabilities 31 - 64,457 Retirement benefits 32 2,790 37,941 Provisions for environmental rehabilitation 33 41,784 45,942

Total non-current liabilities 165,231 304,944

Trade and other payables 27a 131,313 110,588 Provisions 27b 70,602 70,612 Borrowings 30 1,232,163 1,133,928 Subordinated loan 30 865,445 865,445 Current tax liabilities 14 98,131 105,115 Retirement benefits 32 59,030 - Provisions for environmental rehabilitation 33 19,929 9,650

Total current liabilities 2,476,613 2,295,338

Total liabilities 2,641,844 2,600,282

Total equity and liabilities 7,266,927 6,306,664 The financial statements were approved for issue by the Board of Directors on 25 November 2013 and signed on its behalf by:

……………………………. ……………………………. Director Director The notes on pages 34 to 93 are an integral part of these consolidated financial statements.

............................................................. ..................................................Director Director

ZCCM Investments Holdings Plc

29

ZCC M Investments Holdings Plc

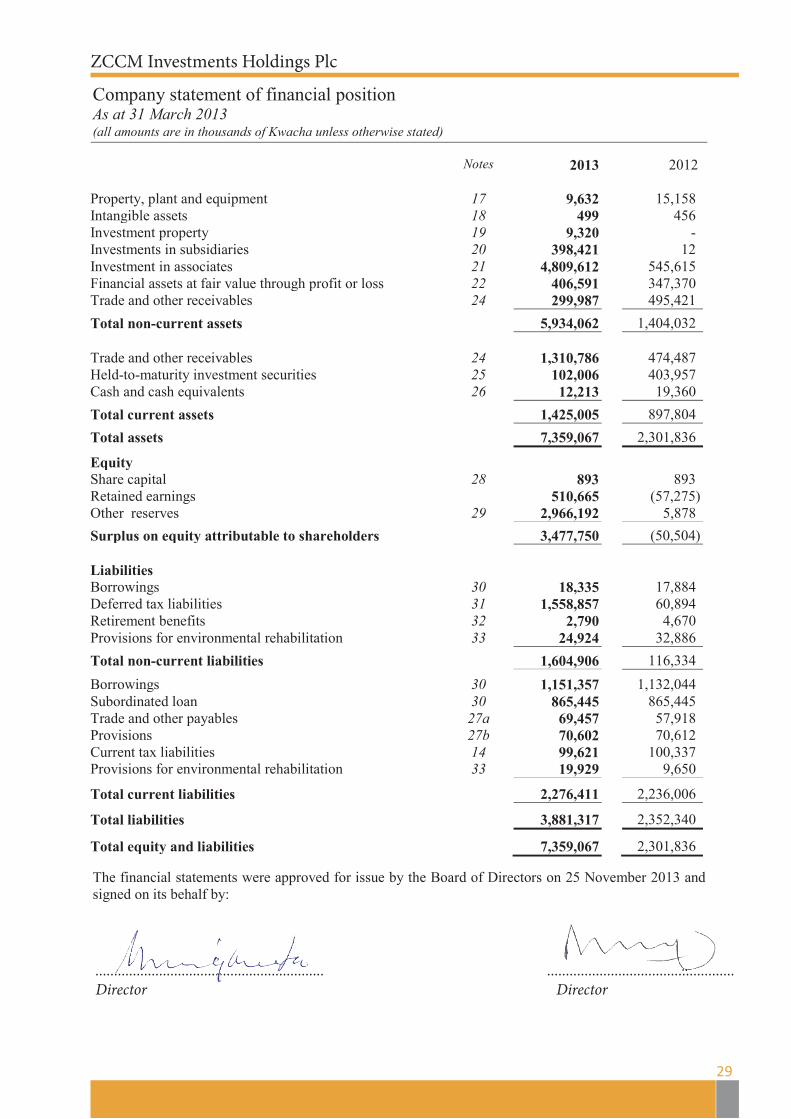

Company statement of financial position As at 31 March 2013 (all amounts are in thousands of Kwacha unless otherwise stated) Notes 2013

2012

Property, plant and equipment 17 9,632 15,158 Intangible assets 18 499 456 Investment property 19 9,320 - Investments in subsidiaries 20 398,421 12 Investment in associates 21 4,809,612 545,615 Financial assets at fair value through profit or loss 22 406,591 347,370 Trade and other receivables 24 299,987 495,421 Total non-current assets 5,934,062 1,404,032 Trade and other receivables 24 1,310,786 474,487 Held-to-maturity investment securities 25 102,006 403,957 Cash and cash equivalents 26 12,213 19,360 Total current assets 1,425,005 897,804 Total assets 7,359,067 2,301,836

Equity Share capital 28 893 893 Retained earnings 510,665 (57,275) Other reserves 29 2,966,192 5,878 Surplus on equity attributable to shareholders 3,477,750 (50,504) Liabilities Borrowings 30 18,335 17,884 Deferred tax liabilities 31 1,558,857 60,894 Retirement benefits 32 2,790 4,670 Provisions for environmental rehabilitation 33 24,924 32,886 Total non-current liabilities 1,604,906 116,334

Borrowings 30 1,151,357 1,132,044 Subordinated loan 30 865,445 865,445 Trade and other payables 27a 69,457 57,918 Provisions 27b 70,602 70,612 Current tax liabilities 14 99,621 100,337 Provisions for environmental rehabilitation 33 19,929 9,650

Total current liabilities 2,276,411 2,236,006

Total liabilities 3,881,317 2,352,340

Total equity and liabilities 7,359,067 2,301,836 The financial statements were approved for issue by the Board of Directors on 25 November 2013 and signed on its behalf by: …………………………… ……………………………….. Director Director The notes on pages 34 to 93 are an integral part of these consolidated financial statements.

............................................................. ..................................................Director Director

ZCC

M In

vest

men

ts H

oldi

ng P

lc

30

ZCC

M In

vest

men

ts H

oldi

ngs P

lc

Con

solid

ated

stat

emen

t of c

hang

es in

equ

ity

for t

he y

ear e

nded

31

Mar

ch 2

013

(all

amou

nts a

re in

thou

sand

s of K

wac

ha u

nles

s oth

erw

ise st

ated

) 20

12

N

otes

Sh

are

capi

tal

R

eval

uatio

n re

serv

e

T

rans

latio

n re

serv

e

R

etai

ned

earn

ings

T

otal

B

alan

ce a

s at 3

1 M

arch

201

1

893

9,24

2 12

2,76

3 2,

018,

580

2,15

1,47

8 T

otal

com

preh

ensi

ve in

com

e fo

r th

e ye

ar

Prof

it fo

r the

yea

r

- -

- 1,

237,

810

1,23

7,81

0 O

ther

com

preh

ensi

ve in

com

e ne

t of t

ax:

Cur

renc

y tra

nsla

tion

– eq

uity

acc

ount

ed in

vest

ees

21

- -

317,

593

- 31

7,59

3 A

mor

tisat

ion

of re

valu

atio

n

-

(443

) -

443

- D

efer

red

tax

on re

valu

atio

n

31

- 26

0 -

- 26

0 A

ctua

rial g

ain

on d

efin

ed b

enef

it

32

- -

- (1

,071

) (1

,071

) D

efer

red

tax

on d

efin

ed b

enef

it ac

tuar

ial g

ains

31

-

- -

312

312

Tot

al o

ther

com

preh

ensi

ve in

com

e fo

r th

e ye

ar

-

(183

) 31

7,59

3 (3

16)

317,

094

Bal

ance

as a

t 31

Mar

ch 2

012

893

9,05

9 44

0,35

6 3,

256,

074

3,70

6,38

2 20

13

Bal

ance

as a

t 1 A

pril

2012

893

9,05

9 44

0,35

6 3,

256,

074

3,70

6,38

2 T

otal

com

preh

ensi

ve in

com

e fo

r th

e ye

ar

Prof

it fo

r the

yea

r

O

ther

com

preh

ensi

ve in

com

e ne

t of t

ax:

-

- -

762,

021

762,

021

Cur

renc

y tra

nsla

tion

– eq

uity

acc

ount

ed in

vest

ees

21

- -

156,

709

- 15

6,70

9 A

mor

tisat

ion

of re

valu

atio

n su

rplu

s 29

-

(577

) -

577

- D

efer

red

tax

on re

valu

atio

n re

serv

e 31

-

318

- -

318

Act

uaria

l los

s on

defin

ed b

enef

it 32

-

- -

(534

) (5

34)

Def

erre

d ta

x on

def

ined

ben

efit

actu

aria

l los

s 31

-

- -

187

187

Tot

al o

ther

com

preh

ensi

ve in

com

e fo

r th

e ye

ar

-

(259

) 15

6,70

9 23

0 15

6,68

0

At 3

1 M

arch

201

3

893

8,80

0 59

7,06

5 4,

018,

325

4,62

5,08

3 R

etai

ned

earn

ings

are

the

carr

ied

forw

ard

reco

gnis

ed in

com

e, n

et o

f exp

ense

s, of

the

Gro

up p

lus c

urre

nt p

erio

d pr

ofit

attri

buta

ble

to sh

areh

olde

rs.

The

note

s on

page

s 34

to 9

3 ar

e an

inte

gral

par

t of t

hese

con

solid

ated

fina

ncia

l sta

tem

ents

.

ZCC

M In

vest

men

ts H

oldi

ng P

lc

31

ZCC

M In

vest

men

ts H

oldi

ngs P

lc

Com

pany

stat

emen

t of c

hang

es in

equ

ity

for t

he y

ear e

nded

31

Mar

ch 2

013

(all

amou

nts a

re in

thou

sand

s of K

wac

ha u

nles

s oth

erw

ise st

ated

)

2012

N

otes

Sh

are

capi

tal

Rev

alua

tion

rese

rve

Fair

val

ue

rese

rve

Ret

aine

d ea

rnin

g

Tot

al

Bal

ance

as a

t 1 A

pril

2011

893

6,11

4 -

(656

,192

) (6

49,1

85)

Prof

it fo

r the

yea

r

- -

59

8,45

5 59

8,45

5 O

ther

com

preh

ensi

ve in

com

e ne

t of t

ax

Am

ortis

atio

n of

reva

luat

ion

surp

lus

29

- (3

62)

36

2 -

Def

erre

d ta

x on

reva

luat

ion

surp

lus

31

- 12

6

- 12

6 A

ctua

rial g

ain

on d

efin

ed b

enef

it

32

- -

15

4 15

4 D

efer

red

tax

on d

efin

ed b

enef

it ac

tuar

ial g

ain

31

- -

(5

4)

(54)

O

ther

com

preh

ensi

ve in

com

e ne

t of t

ax

-

(236

) -

462

226

Tota

l com

preh

ensi

ve in

com

e fo

r the

yea

r

- (2

36)

59

8,91

7 59

8,68

1

Bal

ance

at 3

1 M

arch

201

2 as

rest

ated

893

5

,878

-

(57,

275)

(5

0,50

4)

2013

B

alan

ce a

s at 1

Apr

il 20

12

89

3 5,

878

- (5

7,27

5)

(50,

504)

T

otal

com

preh

ensi

ve in

com

e fo

r th

e ye

ar

Prof

it fo

r the

yea

r

- -

- 56

7,92

5 56

7,92

5 O

ther

com

preh

ensi

ve in

com

e ne

t of t

ax

Am

ortis

atio

n of

reva

luat

ion

surp

lus

-

(362

) -

362

- D

efer

red

tax

on re

valu

atio

n re

serv

e 31

-

126

-

-

12

6 A

ctua

rial g

ain

on d

efin

ed b

enef

it

32

- -

- (5

34)

(534

) D

efer

red

tax

on d

efin

ed b

enef

it ac

tuar

ial g

ain

31

- -

- 18

7 18

7 C

hang

e in

fair

valu

e of

ava

ilabl

e-fo

r-sal

e in

vest

men

ts in

subs

idia

ries

20

- -

397,

210

- 39

7,21

0 D

efer

red

tax

fair

valu

e ch

ange

on

subs

idia

ries

31

- -

(139

,023

) -

(139

,023

) C

hang

e in

fair

valu

e of

ava

ilabl

e-fo

r-sal

e in

vest

men

ts in

ass

ocia

tes

21

- -

4,15

7,48

2 -

4,15

7,48

2 D

efer

red

tax

fair

valu

e ch

ange

on

inve

stm

ents

31

-

- (1

,455

,119

) -

(1,4

55,1

19)

Tot

al o

ther

com

preh

ensi

ve in

com

e fo

r th

e ye

ar

-

(236

)

2,9

60,5

50

15

2,96

0,32

9

Tot

al c

ompr

ehen

sive

inco

me

for

the

year

- (2

36)

2

,960

,550

567,

940

3,

528,

254

At 3

1 M

arch

201

3

893

5,

642

2,9

60,5

50

51

0,66

5

3,47

7,75

0

Ret

aine

d ea

rnin

gs a

re th

e ca

rrie

d fo

rwar

d re

cogn

ised

inco

me,

net

of e

xpen

ses,

of th

e C

ompa

ny p

lus c

urre

nt p

erio

d pr

ofit

attri

buta

ble

to sh

areh

olde

rs.

The

note

s on

page

s 34

to 9

3 ar

e an

inte

gral

par

t of t

hese

con

solid

ated

fina

ncia

l sta

tem

ents

.

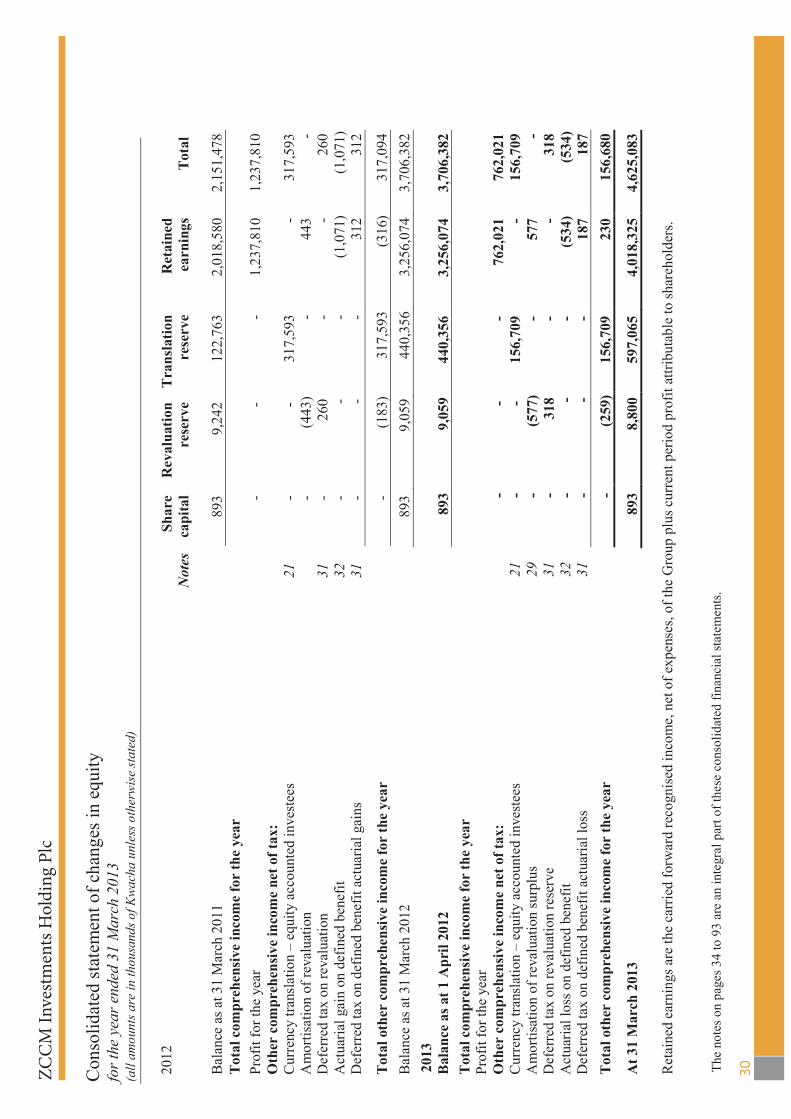

ZCCM Investments Holdings PlcZCCM Investments Holdings Plc

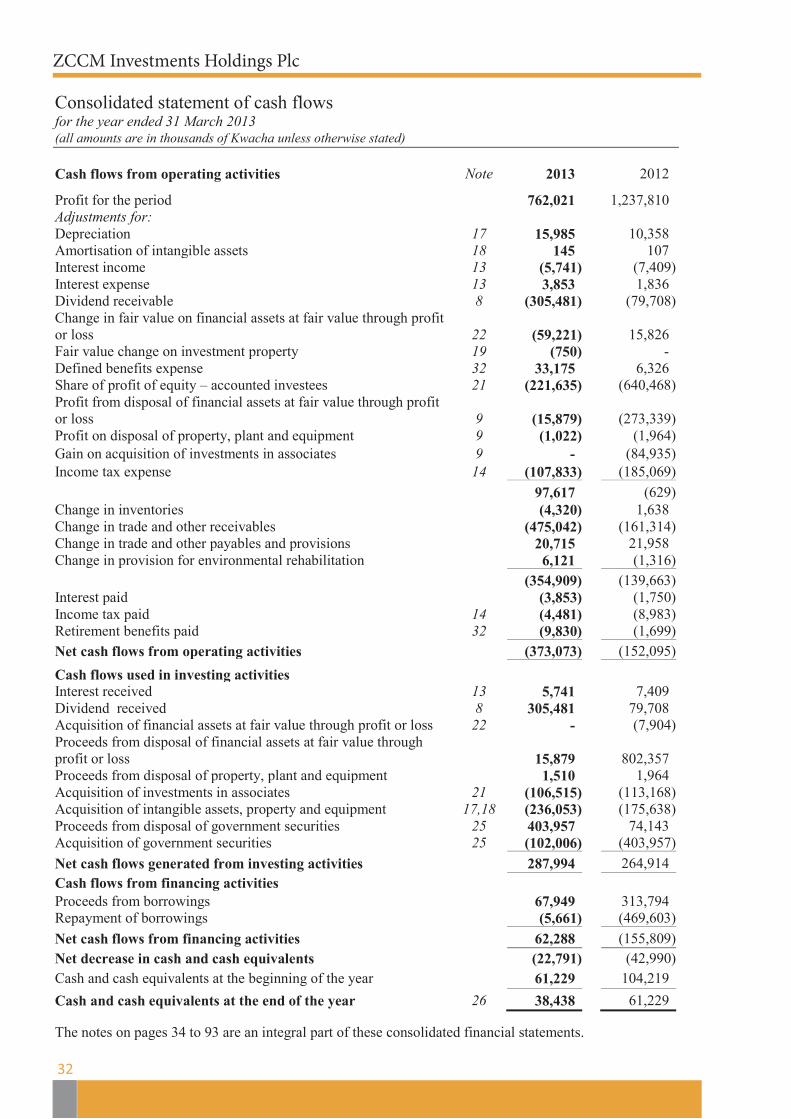

Consolidated statement of cash flows for the year ended 31 March 2013 (all amounts are in thousands of Kwacha unless otherwise stated)

32

Cash flows from operating activities Note 2013 2012

Profit for the period 762,021 1,237,810 Adjustments for: Depreciation 17 15,985 10,358 Amortisation of intangible assets 18 145 107 Interest income 13 (5,741) (7,409) Interest expense 13 3,853 1,836 Dividend receivable 8 (305,481) (79,708) Change in fair value on financial assets at fair value through profit or loss

22

(59,221)

15,826 Fair value change on investment property 19 (750) - Defined benefits expense 32 33,175 6,326 Share of profit of equity – accounted investees 21 (221,635) (640,468) Profit from disposal of financial assets at fair value through profit or loss

9

(15,879)

(273,339) Profit on disposal of property, plant and equipment 9 (1,022) (1,964) Gain on acquisition of investments in associates 9 - (84,935) Income tax expense 14 (107,833) (185,069) 97,617 (629) Change in inventories (4,320) 1,638 Change in trade and other receivables (475,042) (161,314) Change in trade and other payables and provisions 20,715 21,958 Change in provision for environmental rehabilitation 6,121 (1,316) (354,909) (139,663) Interest paid (3,853) (1,750) Income tax paid 14 (4,481) (8,983) Retirement benefits paid 32 (9,830) (1,699) Net cash flows from operating activities (373,073) (152,095)

Cash flows used in investing activities Interest received 13 5,741 7,409 Dividend received 8 305,481 79,708 Acquisition of financial assets at fair value through profit or loss 22 - (7,904) Proceeds from disposal of financial assets at fair value through profit or loss

15,879 802,357

Proceeds from disposal of property, plant and equipment 1,510 1,964 Acquisition of investments in associates 21 (106,515) (113,168) Acquisition of intangible assets, property and equipment 17,18 (236,053) (175,638) Proceeds from disposal of government securities 25 403,957 74,143 Acquisition of government securities 25 (102,006) (403,957) Net cash flows generated from investing activities 287,994 264,914 Cash flows from financing activities Proceeds from borrowings 67,949 313,794 Repayment of borrowings (5,661) (469,603) Net cash flows from financing activities 62,288 (155,809) Net decrease in cash and cash equivalents (22,791) (42,990) Cash and cash equivalents at the beginning of the year 61,229 104,219 Cash and cash equivalents at the end of the year 26 38,438 61,229

The notes on pages 34 to 93 are an integral part of these consolidated financial statements.

ZCCM Investments Holdings PlcZCCM Investments Holdings Plc

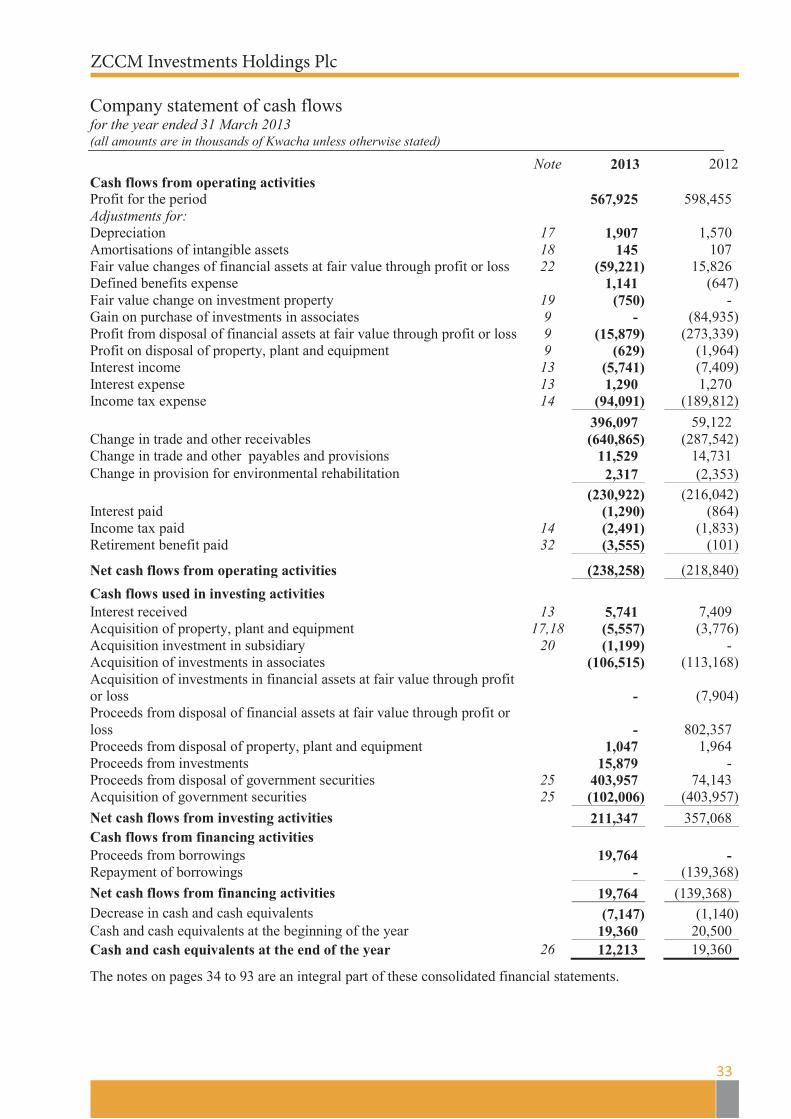

Company statement of cash flows for the year ended 31 March 2013 (all amounts are in thousands of Kwacha unless otherwise stated)

33

Note 2013 2012 Cash flows from operating activities Profit for the period 567,925 598,455 Adjustments for: Depreciation 17 1,907 1,570 Amortisations of intangible assets 18 145 107 Fair value changes of financial assets at fair value through profit or loss 22 (59,221) 15,826 Defined benefits expense 1,141 (647) Fair value change on investment property 19 (750) - Gain on purchase of investments in associates 9 - (84,935) Profit from disposal of financial assets at fair value through profit or loss 9 (15,879) (273,339) Profit on disposal of property, plant and equipment 9 (629) (1,964) Interest income 13 (5,741) (7,409) Interest expense 13 1,290 1,270 Income tax expense 14 (94,091) (189,812) 396,097 59,122 Change in trade and other receivables (640,865) (287,542) Change in trade and other payables and provisions 11,529 14,731 Change in provision for environmental rehabilitation 2,317 (2,353) (230,922) (216,042) Interest paid (1,290) (864) Income tax paid 14 (2,491) (1,833) Retirement benefit paid 32 (3,555) (101)

Net cash flows from operating activities (238,258) (218,840)

Cash flows used in investing activities Interest received 13 5,741 7,409 Acquisition of property, plant and equipment 17,18 (5,557) (3,776) Acquisition investment in subsidiary 20 (1,199) - Acquisition of investments in associates (106,515) (113,168) Acquisition of investments in financial assets at fair value through profit or loss -

(7,904)

Proceeds from disposal of financial assets at fair value through profit or loss -

802,357

Proceeds from disposal of property, plant and equipment 1,047 1,964 Proceeds from investments 15,879 - Proceeds from disposal of government securities 25 403,957 74,143 Acquisition of government securities 25 (102,006) (403,957) Net cash flows from investing activities 211,347 357,068 Cash flows from financing activities Proceeds from borrowings 19,764 - Repayment of borrowings - (139,368) Net cash flows from financing activities 19,764 (139,368) Decrease in cash and cash equivalents (7,147) (1,140) Cash and cash equivalents at the beginning of the year 19,360 20,500 Cash and cash equivalents at the end of the year 26 12,213 19,360

The notes on pages 34 to 93 are an integral part of these consolidated financial statements.

ZCCM Investments Holdings PlcZCCM Investments Holdings Plc

Notes to the financial statements for the year ended 31 March 2013

(all amounts are in thousands of Kwacha unless otherwise stated)

34

1 Reporting entity ZCCM Investments Holdings Plc (the “Company” or “ZCCM – IH”) is domiciled in Zambia. The

address of the Company is Mukuba Pension House, 5309 Dedan Kimathi Road. P.O Box 30048, Lusaka. The consolidated financial statements of the Company as of and for the year ended 31 March 2013 comprise the Company and its subsidiaries (together referred to as “the Group”) and the Group’s interest in associates. The principal activity of the Company is to manage the Zambian Government’s stake in the mining sector.

The Company’s shares are listed on the Lusaka Stock Exchange (LuSE), the London Stock Exchange and Euronext.

Where reference is made in the basis of preparation to Group it should be interpreted as being applied to the consolidated and separate financial statements as the context requires.

2 Basis of preparation

(a) Statement of compliance

The financial statements have been prepared in accordance with International Financial Reporting Standards (IFRSs) as issued by the International Accounting Standard Board (IASB) and in the manner required by the Companies Act of Zambia.

(b)

Basis of measurement

The financial statements have been prepared on the historical cost basis except for the following material items in the statement of financial position:

• Non – derivative financial instruments at fair value through profit or loss are measured at fair value.

• Investment property is measured at fair value. • The liability for the defined benefit obligation is recognised as the present value of the defined

obligation and is limited as explained in Note 3.10 (ii). • Available-for-sale investments are measured at fair value. • An investment in associates is measured at fair value in the company.

(c) Functional and presentation currency

These financial statements are presented in Zambian Kwacha, which is the Company’s functional currency. Except as otherwise indicated, financial information presented in Kwacha has been rounded to the nearest thousand. Rebasing of the Zambian Kwacha The Zambian currency (The Kwacha) was rebased effective 1 January 2013, by dividing the nominal value of the existing currency by a multiple of one thousand so that one thousand Kwacha yielded a face value of one Kwacha. All reporting entities with financial year ends after 31 December 2012 are required to prepare financial statements in the new (rebased) currency. Accordingly, the comparatives have been rebased by dividing them by 1,000.

(a) Statement of compliance

The financial statements have been prepared in accordance with International Financial Reporting Standards (IFRSs) as issued by the International Accounting Standard Board (IASB) and in the manner required by the Companies Act of Zambia.

ZCCM Investments Holdings Plc

Notes to the financial statements (continued) for the year ended 31 March 2013 (all amounts are in thousands of Kwacha unless otherwise stated)

35

2 Basis of preparation (continued)

(b) Basis of measurement

The financial statements have been prepared on the historical cost basis except for the following material items in the statement of financial position:

• Non – derivative financial instruments at fair value through profit or loss are measured at fair value.

• Investment property is measured at fair value. • The liability for the defined benefit obligation is recognised as the present value of the defined

obligation and is limited as explained in Note 3.10 (ii). • Available-for-sale investments are measured at fair value. • An investment in associates is measured at fair value in the company.

(c) Functional and presentation currency

These financial statements are presented in Zambian Kwacha, which is the Company’s functional currency. Except as otherwise indicated, financial information presented in Kwacha has been rounded to the nearest thousand.

Rebasing of the Zambian Kwacha

The Zambian currency (The Kwacha) was rebased effective 1 January 2013, by dividing the nominal value of the existing currency by a multiple of one thousand so that one thousand Kwacha yielded a face value of one Kwacha. All reporting entities with financial year ends after 31 December 2012 are required to prepare financial statements in the new (rebased) currency. Accordingly, the comparatives have been rebased by dividing them by 1,000.

(d)

Use of estimates and judgements

The preparation of financial statements in conformity with IFRSs requires management to make judgements, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimates are revised and in any future periods affected.

Information about assumptions and estimations of uncertainties that have a significant risk of resulting in material adjustment within the next financial period, and critical judgements in applying accounting policies that have the most significant effect on the amounts recognised in the financial statements is described in note 6.

(e) Change in accounting policy

In 2013, ZCCM-IH Plc decided to change its accounting policy for measuring its investments in subsidiaries and associates in the separate financial statements from cost to fair value. As a result of the change, the Group now measures its investment in subsidiaries and associates using various valuation models:

• Investments in subsidiaries are measured at fair value using a discounted cash flow valuation model.