Your FWO October 2013 Issue One

12

1. RETIREMENT PLANNING - SELF MANAGED SUPER FUND CASE STUDY 2. USING A LOW TAX SUPERANNUATION ENVIRONMENT FOR YOUR RETIREMENT 3. FWO WEBINARS 4. INSURANCE 5. PLANNING FOR YOUR FUTURE - WHERE DO YOU WANT TO BE IN 10 YEARS Your FW

-

Upload

fwo-chartered-accountants -

Category

Documents

-

view

229 -

download

0

description

Â

Transcript of Your FWO October 2013 Issue One

1. RETIREMENT PLANNING - SELF MANAGED SUPER FUND CASE STUDY

2. USING A LOW TAX SUPERANNUATION ENVIRONMENT FOR YOUR RETIREMENT

3. FWO WEBINARS

4. INSURANCE

5. PLANNING FOR YOUR FUTURE - WHERE DO YOU WANT TO BE IN 10 YEARS

Your FW

Hello and welcome to the first edition of the FWO Client e-zine.

It seems that you are all keen to receive constant information about ways to becoming Financially Well Organised - or at least that’s what you keep telling us

Hence, we have created this impressive e-zine for you - YOUR FWO.

The idea behind the e-zine is to share our knowledge with you in order to help support and guide you to achieve your goals.

We want to make your journey to becoming Financially Well Organised a smooth one.

Introduction

ii www.financiallywellorganised.com Your FWO IssueOne

OutcomeRefinanced $450K of undrawn equity in business and made 3 year roll-

up non-concessional contributions to SMSF for 1 member.

Used savings outside SMSF to make 3 year roll-up non-concessional

contributions of $450K to SMSF for the other member.

SMSF borrowed $2M from bank under LRBA plus existing cash

and non-concessional contributions received to purchase business

premises for $3M.

SMSF rents business premises to the Husband and Wife’s business for

$340K pa with 4% rent increases each year.

Business will make maximum $25K pa concessional contributions each

for Husband and Wife to SMSF.

After 7 years, SMSF bank loan reduced to $1.4M and Net Assets of

SMSF have grown from $300K to $2.8M.

SMSF bank loan will be paid out in 17 years.

Husband and Wife no longer paying lost rent of $280K pa increasing by

4% each year and effectively own their own business premises.

Will probably sell property in 20 years time when Husband and Wife are

in pension phase.

A very good chance that they will make a sizeable capital gain when

they sell business property in 20 years time.

Based on current rules, the Husband and Wife’s SMSF will not pay any

tax on capital gain when sold in 20 years time when they are receiving a

retirement income stream from the SMSF.

Retirement Planning

CASE STUDY ONE SMSF - Business Property Purchase with Limited recourse Borrowing Arrangement (LRBA)

Facts

• 2 members of SMSF Husband and Wife

• Sole Asset in SMSF Cash of $300k

• Currently renting business premises for $280K pa

• Wanting to buy own business premises for $3M

• Savings outside SMSF of $500K

• Undrawn equity in business

1www.financiallywellorganised.com Your FWO IssueOne

In March 2012, Rice Warner Actuaries prepared a report commissioned

by the Financial Services Council (FSC) to estimate the Retirement

Savings Gap (RSG) in Australia as at 30 June 2011. The RSG is the value

for the working population of the shortfall they will have in building an

adequate (reasonable) retirement benefit.

Rice Warner estimated that there was a RSG of some $836 billion at 30

June 2011.

So it is pretty clear that most of us will have a Gap. Some of us are

closer to retirement than others – but we all think about it!

We may not want to retire, however one thing is certain – one day we

will stop working by choice or otherwise – so we need to have a plan on

how to close the gap between what we have now and what we will need

when we retire.

Accumulating savings is the way to close the Gap, and accumulating

savings through superannuation has been the most effective way to

save.

Business Owners and employees can use contributions into

superannuation as a tax effective way to save.

Superannuation generally only taxes contributions and earnings at

15% and capital gains on investments at 10%, if held for longer than

12 months. Because these tax rates are much lower than tax rates on

income and capital gains made outside of superannuation, a greater

after-tax amount of investments are re-invested in the superannuation

environment that will grow at a faster rate over the longer term

than equivalent investments taxed at a higher rate outside the

superannuation environment.

In May 2010, the Australian Government legislated an increase in the

Superannuation Guarantee contribution rate from 9% to 12% from 2013

to 2019 which will help increase superannuation savings for employees.

MIND THE GAPUsing a low tax superannuation environment for your retirement

Many people have a gap between how much they will need to comfortably retire and what they have now. We call this - THE GAP.

2 www.financiallywellorganised.com Your FWO IssueOne

For Business Owners, many have established their own Self-Managed

Superannuation Fund (SMSF) to be their wealth creation vehicle due

to the low tax rates on offer and the increase in control over their

investment decisions it gives them.

Concessional (tax deductible) contributions from the business entity to

the SMSF for the business owner have been a way to reduce tax and

accumulate savings at a faster rate in a SMSF low tax environment.

Currently, concessional contributions are capped at $35,000 per annum

for a person aged 59 years or over on 30 June 2013 and $25,000 for

everyone else.

A person can also make non-concessional (not tax deductible)

contributions into a superannuation fund each year up to a

current $150,000 limit. These contributions are not taxable to the

superannuation fund.

Concessional and non-concessional contributions have been a way of

transferring savings into the low tax superannuation environment to re-

invest and grow faster.

SMSF’s have offered business owners very flexible ways to reduce tax

and grow their wealth for future retirement in a way that still suits their

business requirements.

We will discuss some of these flexible ways in the next edition of Your

FWO.

3www.financiallywellorganised.com Your FWO IssueOne

SMSF’s offer business owners very flexible ways to reduce tax and grow their wealth for future retirement...

FWO Client WebinarsOur team is committed to guiding your Financially Well Organised future.

We have designed a new series of bi-monthly client webinars to help keep you informed with the added convenience of not leaving your office.

Our webinars will cover a variety of topics that will help guide to you becoming Financially Well Organised.

To register for our next FWO Client Webinar please visit our website here for further information.

5www.financiallywellorganised.com Your FWO IssueOne

The NDIS is aimed at providing long term, high quality support for people who have a permanent disability that significantly affects their communication, social interaction, learning, mobility, self-care or self management.

Support may be provided if the disablement is permanent or where early intervention can mitigate the impact on the individual’s ability to function. Those accepted to participate in the scheme will have a personalised support plan developed and the necessary funding provided.

The government intends to partially fund the DisabilityCare scheme through an increase to the Medicare levy of 0.5%. Even with the recent change in government, the scheme has received ongoing support from the coalition.

To date, South Australia, New South Wales, ACT, Northern Territory and Queensland have signed up to the full DisabilityCare Scheme, agreeing to ensure full implementation by 2018-19. Upon full implementation the scheme will provide support for approximately 460,000 individuals

1.

This is a fraction of the four million Australians who suffer some type of disablement and the 1.25 million Australians with severe or profound disablement according to the ABS

2.

Why personal life insurance is still important

The DisablityCare Scheme will not cover people for loss of income nor assist with other living expenses such as paying for rent or mortgage.

Personal Life Insurance is primarily concerned with whether the insured person meets the defined event and policy terms regardless of the level of support available to them through their families, carers or the community in general.

Income Protection can provide individuals with a regular income while temporarily unable to work and may also include payment of rehabilitation expenses.

Critical Illness or total and permanent disablement insurance gives individuals greater flexibility over how they use their lump sum benefit.

Lump sum benefits can be used to support rehabilitation, pay for necessary aids or future medical costs or to provide an income over the long term.

DisabilityCare is a step in the right direction and will assist many people, however it is no substitute for having comprehensive personal insurance.

INSURANCEDisabilityCare is not a substitute for comprehensive personal insurance.In May 2013 the government announced that it would be implementing the National Disability Insurance Scheme (NDIS) or DisabilityCare. We have taken the opportunity to look at the program in more detail.

1. www.budget.gov.au

(Budget Overview – May 2013) 2.

Disability, Ageing and carers, Australia: Summary of findings (ABS 2009)

6 www.financiallywellorganised.com Your FWO IssueOne

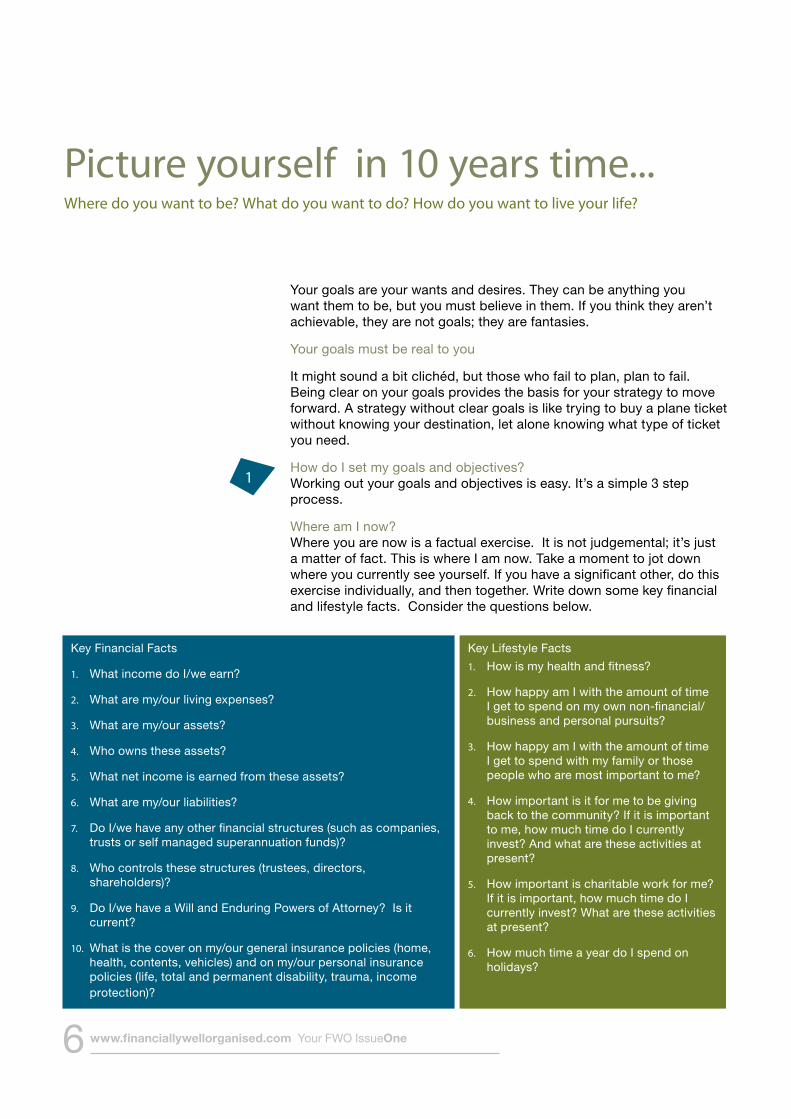

Your goals are your wants and desires. They can be anything you want them to be, but you must believe in them. If you think they aren’t achievable, they are not goals; they are fantasies.

Your goals must be real to you

It might sound a bit clichéd, but those who fail to plan, plan to fail. Being clear on your goals provides the basis for your strategy to move forward. A strategy without clear goals is like trying to buy a plane ticket without knowing your destination, let alone knowing what type of ticket you need.

How do I set my goals and objectives? Working out your goals and objectives is easy. It’s a simple 3 step process.

Where am I now? Where you are now is a factual exercise. It is not judgemental; it’s just a matter of fact. This is where I am now. Take a moment to jot down where you currently see yourself. If you have a significant other, do this exercise individually, and then together. Write down some key financial and lifestyle facts. Consider the questions below.

1

Picture yourself in 10 years time...Where do you want to be? What do you want to do? How do you want to live your life?

Key Financial Facts

1. What income do I/we earn?

2. What are my/our living expenses?

3. What are my/our assets?

4. Who owns these assets?

5. What net income is earned from these assets?

6. What are my/our liabilities?

7. Do I/we have any other financial structures (such as companies, trusts or self managed superannuation funds)?

8. Who controls these structures (trustees, directors, shareholders)?

9. Do I/we have a Will and Enduring Powers of Attorney? Is it current?

10. What is the cover on my/our general insurance policies (home, health, contents, vehicles) and on my/our personal insurance policies (life, total and permanent disability, trauma, income protection)?

Key Lifestyle Facts

1. How is my health and fitness?

2. How happy am I with the amount of time I get to spend on my own non-financial/business and personal pursuits?

3. How happy am I with the amount of time I get to spend with my family or those people who are most important to me?

4. How important is it for me to be giving back to the community? If it is important to me, how much time do I currently invest? And what are these activities at present?

5. How important is charitable work for me? If it is important, how much time do I currently invest? What are these activities at present?

6. How much time a year do I spend on holidays?

7www.financiallywellorganised.com Your FWO IssueOne

You should also write down other financial or lifestyle facts that are relevant to you.

Step 1 Complete! You now have a clear picture of where you are now.

What’s your destination?

What’s the most common excuse for not doing what we want to be doing?

Money? What is money?

My definition of money is a commodity used to help us to achieve our personal goals. Where we go wrong, is when money becomes the be all and end all of our existence.

Don’t get me wrong, I’m not saying that money isn’t important, it is, and I’m not about to head down a righteous path and unload on you a sermon about the evils of money, but when it gets in the way of your health or family, something is seriously out of whack.

We often try to separate our financial goals from our personal goals.

Financial goals are the things you want to achieve that have a financial impact, including your business strategies, your investment strategies, your risk management strategies, and your estate planning strategies.

Your personal goals are those things that you want to do that may not have anything to do with a financial outcome, such as health and fitness, taking a decent holiday every year, spending more time with your family, being more involved with the community, undertaking more education for personal pursuits.

We forget that how we feel about our financial security impacts on how we feel about our life, and vice versa. They are inextricably interwoven.

When we develop our strategies, the financial goals always seem to come first.

This is usually because we are dependant on these to fund our lifestyle. We fail to recognise that our personal goals are actually those desires that, what may seem like a lifetime ago, our financial journey was based upon. Remember when you started working? Your pay was spent week in and week out to pay for the weekend, to save up for that holiday, buy that car you always wanted, or the ticket to the concert you couldn’t miss. But what got in the way of our lifestyle interests were responsibility, career, and the pressure of having a family. We work harder to provide and advance, but forget about ourselves and our interests.

We actually make it hard for ourselves. We put roadblocks up to make it hard to achieve our objectives.

The answer is to align your financial and personal goals. Accept that they are not two separate lists, but one, and make sure that you are consistently focusing on both without prejudice to the other.

2

8 www.financiallywellorganised.com Your FWO IssueOne

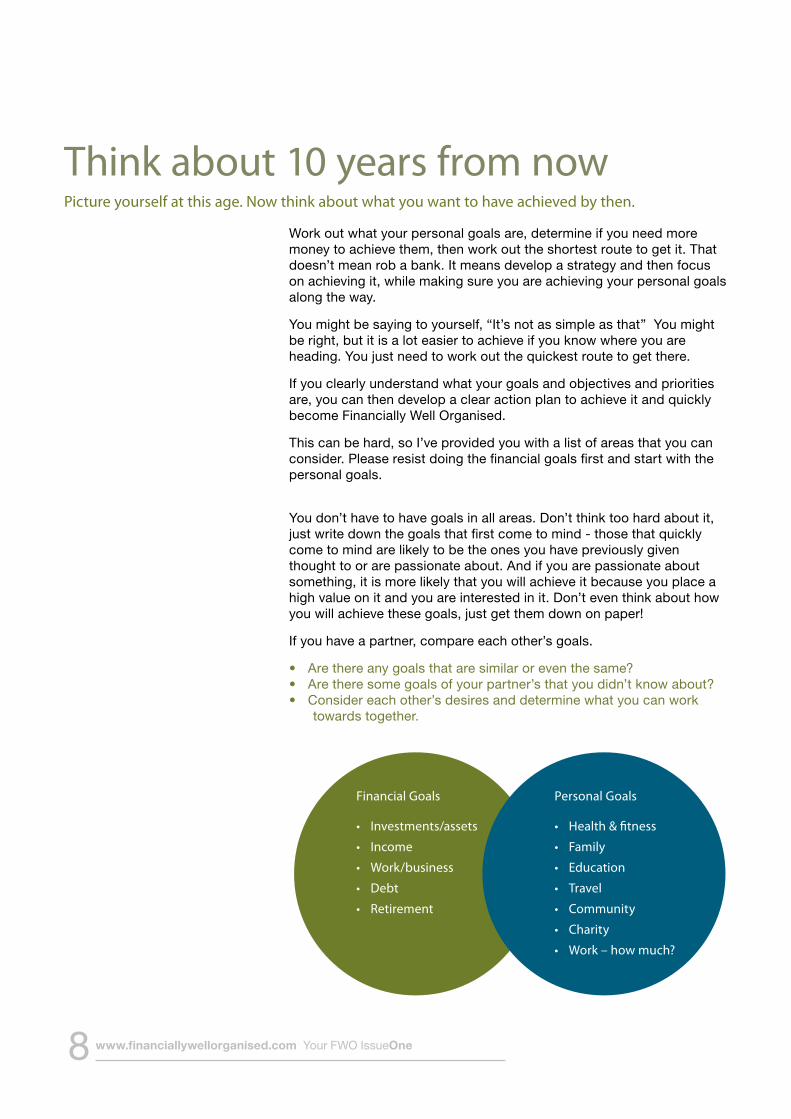

Work out what your personal goals are, determine if you need more money to achieve them, then work out the shortest route to get it. That doesn’t mean rob a bank. It means develop a strategy and then focus on achieving it, while making sure you are achieving your personal goals along the way.

You might be saying to yourself, “It’s not as simple as that” You might be right, but it is a lot easier to achieve if you know where you are heading. You just need to work out the quickest route to get there.

If you clearly understand what your goals and objectives and priorities are, you can then develop a clear action plan to achieve it and quickly become Financially Well Organised.

This can be hard, so I’ve provided you with a list of areas that you can consider. Please resist doing the financial goals first and start with the personal goals.

You don’t have to have goals in all areas. Don’t think too hard about it, just write down the goals that first come to mind - those that quickly come to mind are likely to be the ones you have previously given thought to or are passionate about. And if you are passionate about something, it is more likely that you will achieve it because you place a high value on it and you are interested in it. Don’t even think about how you will achieve these goals, just get them down on paper!

If you have a partner, compare each other’s goals.

• Arethereanygoalsthataresimilaroreventhesame?• Aretheresomegoalsofyourpartner’sthatyoudidn’tknowabout?• Considereachother’sdesiresanddeterminewhatyoucanwork

towards together.

Financial Goals • Investments/assets

• Income

• Work/business

• Debt

• Retirement

Personal Goals

• Health & fitness

• Family

• Education

• Travel

• Community

• Charity

• Work – how much?

Think about 10 years from nowPicture yourself at this age. Now think about what you want to have achieved by then.

9www.financiallywellorganised.com Your FWO IssueOne

Then think about three years time

In three years, which of these goals must have you achieved? These goals can be joint or individual goals, but they share the same timeline, and you must have these achieved in the next three years. It might mean you can achieve them next week, or it might take all of three years to do so, it doesn’t matter, it’s just about working out what you want to make sure you have done it in the next three years. Three years is far enough away to achieve significant outcomes and soon enough to make short term tangible differences. You are committing to yourself or to each other, whichever is relevant to your situation, that you will achieve these in three years.

Step 2 Complete! You have identified your destination.

Work out the action plan to get there

After you have determined your goals and objectives, there are nine key ‘how you get there’ areas that lead you to being Financially Well Organised. These nine key areas ensure that your strategy aligns with your personal and financial goals, and provides you with a step by step process to achieve your goals.

Being Financially Well Organised is as simple or complex as you want to make it. The key is to understand that what being Financially Well Organised means to you will be different from your partner, your family, your friends and your work colleagues. It is what is relevant for you in your situation. There is no one way – every situation is unique.

3

become financially well organised.

If you clearly understand what your goals and objectives and priorities are, you can then develop a clear action plan to achieve it...

Ground Floor, Green Square North Tower515 St Paul’s Terrace, Fortitude Valley QLD 4006

GPO Box 81, Brisbane QLD 4001

www.financiallywellorganised.com

Ph: 07 3833 3999 Fax: 07 3833 3900