You can BANK on it!. Objectives STUDENTS WILL BE ABLE TO: Understand the different types of...

25

You can BANK on it!

-

Upload

julie-hampton -

Category

Documents

-

view

216 -

download

0

Transcript of You can BANK on it!. Objectives STUDENTS WILL BE ABLE TO: Understand the different types of...

You can BANK on it!

Objectives

STUDENTS WILL BE ABLE TO:Understand the different types of financial

institutionsCalculate how long it will take to save certain

amount of money.Calculate simple interest. Calculate compound interest. Calculate the rule of 72.

Types of Banks

Commercial Banks: For profit institution that offers checking, savings and lending. Commercial banks serve individuals and businesses.

Types of Banks

Mutual Savings banks: operate in much the same way as commercial banks; however they specialize in real-estate loans. They now offer many of the same services as commercial banks. Rates on loans are typically better than at commercial banks.

Types of Banks

Savings and Loan Associations (S&L): Historically specialized in savings and mortgages but now offer many of the same services as commercial banks.

Types of Banks

Credit Unions: Nonprofit financial institution that is owned by its members and organized for their benefit. Credit Unions offer a full range of services and rates are extremely competitive.

Non Deposit Institutions

Life Insurance Co. – Now offer investment opportunities, retirement plans and insurance products.

Investment Co. – These firms combine your money with funds from other investors in order to buy stocks, bonds, and other securities

Finance Co. – Offer higher interest loans to customers and small business.

Mortgage Co. – Specialize in home loans.

Shopping for a Bank

Checking and use of online banking must be FREE!

ATM’s for your particular bank should be all over the place!

Your bank must be near where you go to college and also near your parents/guardians.

Savings Plans

Regular Savings Account: This is just to put your money in until you move or invest it in another account. A Regular Savings Account, earns practically no interest.

Savings Plans

Certificates of Deposit: Your money is left on deposit for a stated period of time to earn a specific rate of return. Time that it is invested is called the term. The date it becomes available to you is called the maturity date.

Buying a CD

Shop for the best rate.

Decide how long you can be without your money.

Never let a financial institution “roll over” a CD.

Split your money up. Put your money in several different CD’s that mature at different times. You never know when you may need it. If you don’t need it then re-invest it.

Savings Plan

Money Market Account: this type of savings account requires a minimum balance and earns interest that varies from month to month. This account will pay more interest than a savings account but if your balance goes below the minimum you will have to pay a penalty. FDIC insures money market accounts up to 100,100

Savings Plan

U.S. Savings Bonds: Series EE bonds are puchased from the federal government in amounts that range from $25 - $5,000. All bonds have a face value. The Face value is the amount the bond is worth when it matures. All bonds have a maturity date. This is how long the bond must be held to be worth the face value.

Interest earned on Series EE Bonds is exempt from state and local taxes. You defer the federal taxes by buying HH bonds and low income family who use the interest for schooling don’t pay tax at all.

How Our Savings Grow

Simple interest: Certain account gain interest using the simple interest formula

i=prti = interest earnedp = principalr = ratet = time in years

Simple interest

Ex. 1: If Suzanne invests $5,000 in a CD that earns 7% over 5 years,

A. How much interest will Suzanne earn?

B. How much money will Suzanne have at the end of the seven years?

Compound Interest

Interest rates vary in different institutions (different banks offer different interest rates). The way interest is calculated can vary too. Interest rate is always expressed as an annual percent.

This means that if $1,000 is kept in a CD for

one year with an interest rate of 5%, you would earn $50 in simple interest. In the second year, if the CD was earning simple interest, then another $50 would be earned.

Compound Interest

However, interest is not calculated that way. All savings institutions pay compound interest, that is, interest on the principal and on the previously paid interest, assuming that the interest is left in the account. In the second year the interest calculation would look like:

1050 * .05 * 1 = $52.50 in interest if the compounding is done only

once a year.

Compound Interest

Most Banks however, compound at least semiannually. This means that at least twice a year the interest earned is added to the previous balance so the principal balance on which interest is paid grows a little faster than if the compounding were done only once a year.

Compound Interest

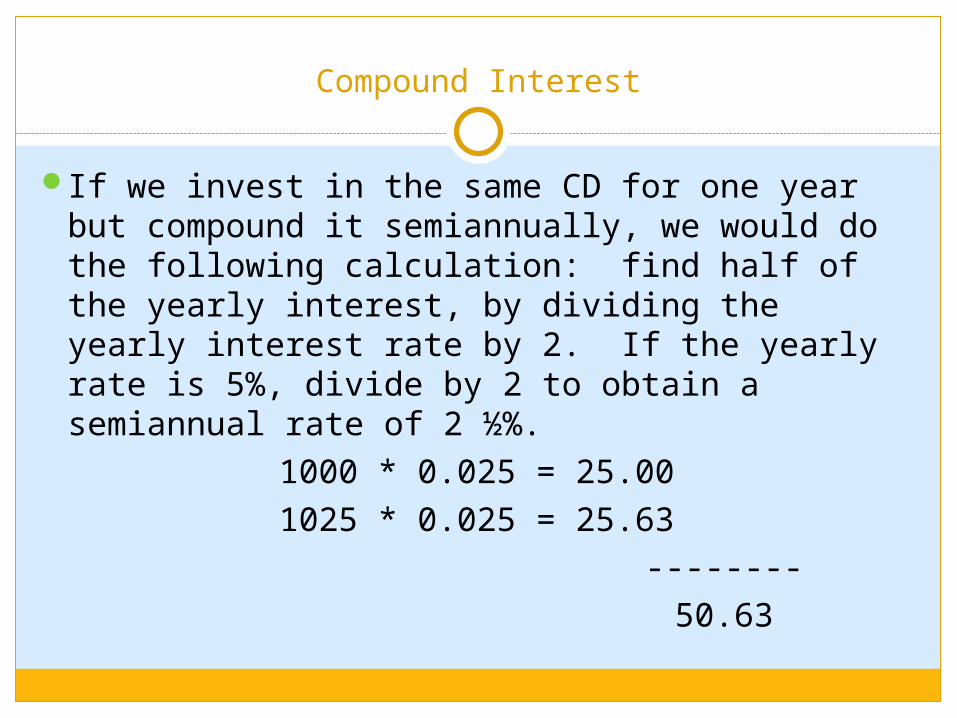

If we invest in the same CD for one year but compound it semiannually, we would do the following calculation: find half of the yearly interest, by dividing the yearly interest rate by 2. If the yearly rate is 5%, divide by 2 to obtain a semiannual rate of 2 ½%.

1000 * 0.025 = 25.001025 * 0.025 = 25.63 -------- 50.63

Compound Interest

Increasing the frequency of the compounding does not greatly increase the amount of interest that you actually get. The table below shows the total interest that you would receive over ten years on $1000 at a rate of 5% under several compounding methods.

Annually Semi Annually

Quarterly Continu-ously

Interest recieved

$628.89 $638.62 $643.62 $648.72

Compound interest Formula

A=P ( 1 + r /(n))^nt

Rule of 72

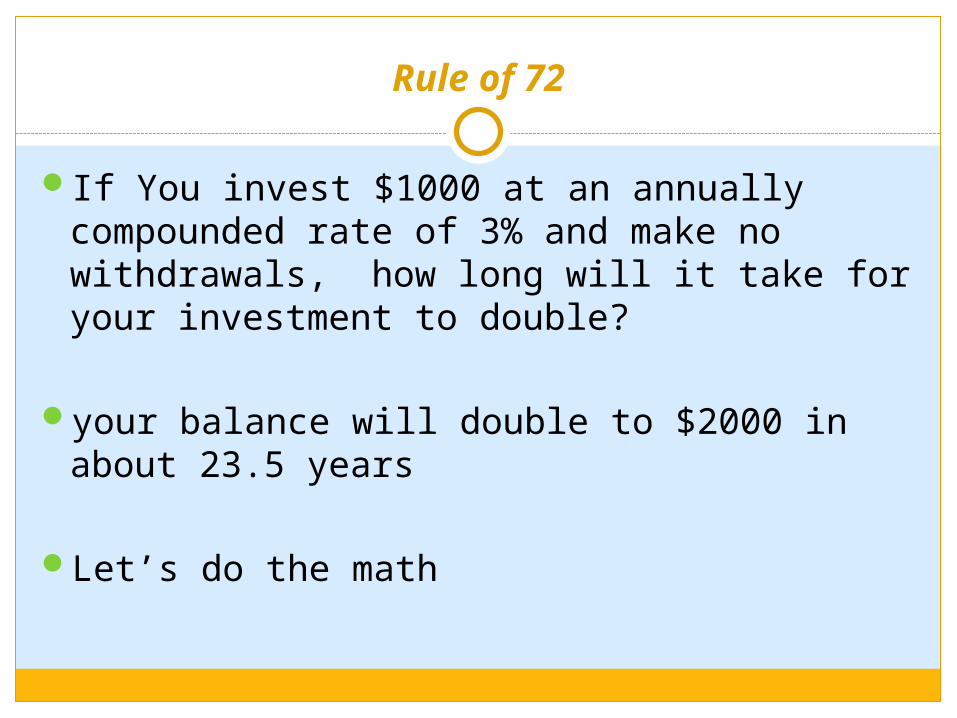

If You invest $1000 at an annually compounded rate of 3% and make no withdrawals, how long will it take for your investment to double?

your balance will double to $2000 in about 23.5 years

Let’s do the math

Rule of 72

If You invest $1000 at an annually compounded rate of 3% and make no withdrawals, your balance will double to $2000 in about 23.5 years

Let’s try the neat little RULE of 72. The RULE of

72 states that to find how long an investment will take to double, you simply

divide 72 by the interest rate *100.

MUCH EASIER!!!

Rule of 72

Pretty darn cool huh…..It’s not exact yet reasonably accurate to determine how long it will take an investment to double.

Another rule of thumb is that your investments should double in no longer than 10 years.

Class Discussion

1. What needs to be compared when selecting a bank?

2. Do we use one bank for all our financial needs?

3. What needs to be compared when selecting a CD or Money Market account?

4. Is it difficult to calculate interest?