Find Out How Banks Calculate How Much Mortgage They Will be Giving You

5

11/29/2016 www.greatcalgaryrealestate.com/blog/how-much-real-estate-can-you-afford/print.html http://www.greatcalgaryrealestate.com/blog/how-much-real-estate-can-you-afford/print.html 1/5 How Much Real Estate Can You Afford? Posted by Joe Samson on Wednesday, September 21st, 2016 at 10:25am. One of the first things that you should be doing when buying a home is figuring out how much you can comfortably afford without putting any stress on your monthly budget. Once you have settled into your new home it's going to be rather difficult and costly to change your mind about the home you have just bought. By reading this article, you will be able to figure out how much real estate you can truly afford to buy. Questions to keep in mind when setting a real estate budget: Is it going to change my lifestyle? Can I live within my means? What is the maximum mortgage payment that I feel comfortable with? Have I created a monthly budget? Is it going to cause stress or peace in my life? It’s fairly easy and straightforward to find out whether you even qualify for a mortgage. A responsible and well planned home buying process must start out with getting a mortgage pre-approval so that you can benchmark your decision based on your purchasing power. Yes, as weird or perhaps somewhat belittling it may sound - we all have certain financial limitations that we need to keep in mind and not to exceed. Even the elite home buyers need to draw the line in the sand when they are looking at luxury homes in their local real estate market. In my years of experience of working with all categories of home buyers, I have found that those who have stayed within their means, turned out to be the most satisfied with their home purchase. Owning a home comes with many aspects of responsibilities, including the financial burden that buyers must keep in mind before they sign on the dotted line. Monthly mortgage payments, property taxes, insurance fees, common maintenance costs can add up really quickly. Not having enough money set aside in your budget to allow you to enjoy a certain level of lifestyle could really dampen your entire home ownership experience. Life Beyond Owning Real Estate It’s so easy to get depressed these days with all the negative news that we’re seeing on TV every day. A home should be a place where we go to find shelter, to relax and to reenergize ourselves, perhaps to have a bit of

-

Upload

joe-samson -

Category

Real Estate

-

view

38 -

download

0

Transcript of Find Out How Banks Calculate How Much Mortgage They Will be Giving You

11/29/2016 www.greatcalgaryrealestate.com/blog/how-much-real-estate-can-you-afford/print.html

http://www.greatcalgaryrealestate.com/blog/how-much-real-estate-can-you-afford/print.html 1/5

How Much Real Estate Can You Afford?Posted by Joe Samson on Wednesday, September 21st, 2016 at 10:25am.

One of the first things that you should bedoing when buying a home is figuring outhow much you can comfortably affordwithout putting any stress on your monthlybudget. Once you have settled into yournew home it's going to be rather difficultand costly to change your mind about thehome you have just bought. By reading thisarticle, you will be able to figure out howmuch real estate you can truly afford tobuy.

Questions to keep in mind when setting areal estate budget:

Is it going to change my lifestyle?Can I live within my means?What is the maximum mortgagepayment that I feel comfortable with?Have I created a monthly budget?Is it going to cause stress or peace inmy life?

It’s fairly easy and straightforward to findout whether you even qualify for amortgage. A responsible and well plannedhome buying process must start out withgetting a mortgage pre-approval so that youcan benchmark your decision based on yourpurchasing power.

Yes, as weird or perhaps somewhatbelittling it may sound - we all have certainfinancial limitations that we need to keep inmind and not to exceed. Even the elitehome buyers need to draw the line in thesand when they are looking at luxury homes in their local real estate market. In my years of experience ofworking with all categories of home buyers, I have found that those who have stayed within their means,turned out to be the most satisfied with their home purchase.

Owning a home comes with many aspects of responsibilities, including the financial burden that buyers mustkeep in mind before they sign on the dotted line. Monthly mortgage payments, property taxes, insurance fees,common maintenance costs can add up really quickly. Not having enough money set aside in your budget toallow you to enjoy a certain level of lifestyle could really dampen your entire home ownership experience.

Life Beyond Owning Real Estate

It’s so easy to get depressed these days with all the negative news that we’re seeing on TV every day. A homeshould be a place where we go to find shelter, to relax and to reenergize ourselves, perhaps to have a bit of

11/29/2016 www.greatcalgaryrealestate.com/blog/how-much-real-estate-can-you-afford/print.html

http://www.greatcalgaryrealestate.com/blog/how-much-real-estate-can-you-afford/print.html 2/5

fun and to invite friends and family over.

I’ve been in far too many homes which were by no means entry level homes, yet I’d found that while itlooked great on the outside, the owners had minimal furniture inside the house. It’s quite demoralizing tovisit a home where the owners can’t afford to have sufficient amount of furniture to make it feel like anenjoyable place to be in.

But not having enough furniture inside a house is only a first world problem. Making sure that you can stillhave enough money for clothes and entertainment is going to be a great contributor to the level of satisfactionyou’ll have in life.

Embrace Living Within Your Means

For many new homebuyers in today’s real estate market the phrase “living within your means” is asforeign as the authentic hair on Donald Trump’s head. While our parents used to live with the belief ofsaving first and then spending what you’ve got - today’s generation is trying to live their parent’s dream byspending first and then paying for it later.

Unfortunately this type of thinking often gets homebuyers into financial problems and creates extraordinarystress in their lives. Money problems usually snowball into other kinds of problems like having issues withrelationships and the stress could also lead to health challenges if you are not careful about calculating howmuch real estate you can afford.

While you may easily afford your monthly mortgage payments while you’re having a well paying job - whatwould happen if that income source would stop all of a sudden? Can you go on and make the mortgagepayments for two, six or maybe 12 months if needed?

Having peace of mind knowing that you can easily afford your home is going to serve you well. Especiallyknowing that you have enough savings set aside when unexpected financial challenges happen.

How Banks Calculate Mortgage Approvals?

For many decades now, banks have come up with a formula to calculate people’s affordability levels. Thisformula is called the GDSR (Gross debt service ratio) and TDSR (Total debt service ratio). Banks havestatistically proven that if they purposely limit how much financial debt people take on, then thelikeliness of them defaulting on their mortgage is significantly reduced.

The GDSR takes into account all of the monthly expenses associated with the property and compares it toyour monthly income before taxes. Banks and conventional lenders like to make sure that homeowners don’tspend more than 32% of their gross monthly income on housing costs.

What is included in the GDSR calculation? When the gross debt service ratio is used, it takes intoconsideration the following expenses: 50% of all condo fees (if applicable), heating costs, property taxes andmortgage payments.

TDSR - total debt service ratio is another formula that lenders use when someone applies for a mortgage. Asthe name of the formula suggests, it adds up all the debt that you may have in addition to the expenses ofowning a home. The TDSR formula includes all credit card, car loan payments and any other types of loansthat you may be responsible for. The maximum amount that banks prefer limiting their client’s mortgagepayment amount is to be below 42% of the borrower’s gross monthly income.

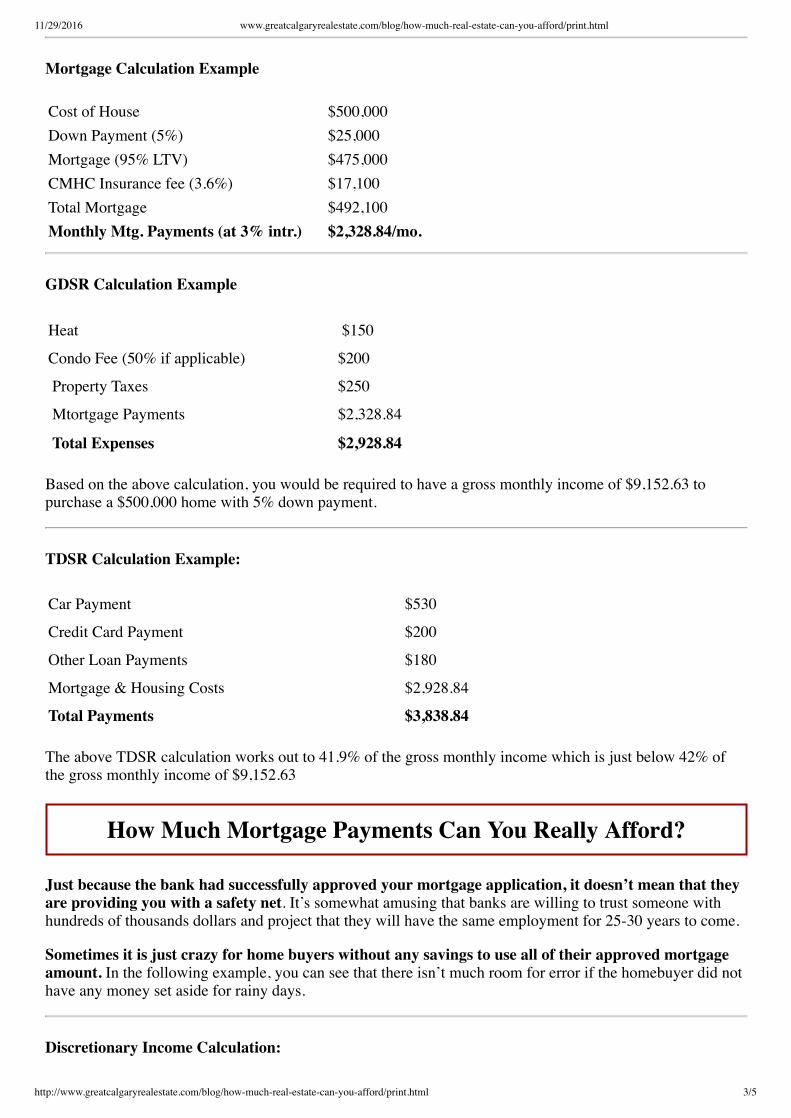

Assuming that you have sound employment and a good credit history, along with a decent credit score, youshould be able to easily figure approximately what mortgage amount the banks will consider approving youfor. Below is a quick example of how banks may approach your mortgage application.

11/29/2016 www.greatcalgaryrealestate.com/blog/how-much-real-estate-can-you-afford/print.html

http://www.greatcalgaryrealestate.com/blog/how-much-real-estate-can-you-afford/print.html 3/5

Mortgage Calculation Example

Cost of House $500,000Down Payment (5%) $25,000Mortgage (95% LTV) $475,000CMHC Insurance fee (3.6%) $17,100Total Mortgage $492,100Monthly Mtg. Payments (at 3% intr.) $2,328.84/mo.

GDSR Calculation Example

Heat $150

Condo Fee (50% if applicable) $200

Property Taxes $250

Mtortgage Payments $2,328.84

Total Expenses $2,928.84

Based on the above calculation, you would be required to have a gross monthly income of $9,152.63 topurchase a $500,000 home with 5% down payment.

TDSR Calculation Example:

Car Payment $530

Credit Card Payment $200

Other Loan Payments $180

Mortgage & Housing Costs $2,928.84

Total Payments $3,838.84

The above TDSR calculation works out to 41.9% of the gross monthly income which is just below 42% ofthe gross monthly income of $9,152.63

How Much Mortgage Payments Can You Really Afford?

Just because the bank had successfully approved your mortgage application, it doesn’t mean that theyare providing you with a safety net. It’s somewhat amusing that banks are willing to trust someone withhundreds of thousands dollars and project that they will have the same employment for 25-30 years to come.

Sometimes it is just crazy for home buyers without any savings to use all of their approved mortgageamount. In the following example, you can see that there isn’t much room for error if the homebuyer did nothave any money set aside for rainy days.

Discretionary Income Calculation:

11/29/2016 www.greatcalgaryrealestate.com/blog/how-much-real-estate-can-you-afford/print.html

http://www.greatcalgaryrealestate.com/blog/how-much-real-estate-can-you-afford/print.html 4/5

Gross Monthly Income: $9,152.63Estimated Income Tax (36%) $3,294.95Mortgage & Housing Costs $2,928.84Loan & Credit Card Expenses $910Discretionary Money left to spend $2,618.84

While it may sound like life's a peach with having an income in excess of $100,000 a year - it may not bevery wise to tap out the mortgage amount that the banks might be willing to provide. After using data ofaverage housing prices, debt levels and so on, it appears that someone who is considered to be a highincome earner may end up being worse off than someone earning much less and living within hismeans.

There are other expenses that bank don’t keep in consideration, yet they play a very important role in thequality of everyone’s life. Most of us could probably live without some of these expenses, but beingaccustomed by the western world, these items below have become a normal our lives. Therefore some of thefigures in the list is an approximate estimate only to illustrate their presence in our everyday lives.

Common Monthly Expenses

Internet & TV $120Telephone $80Utilities (water & power) $200Fuel $200Car Insurance $120 Home Insurance $110Fitness $50 Dining $200 Coffee $100 New Clothes $100Kid's activities $150 Daycare $650Entertainment $150Groceries $1,000Home Maintenance $100Car Maintenance $75Vacation $250Total Expenses $3,655

To maintain a comfortable quality of life, it turns out that one might need to spend $3,655 every month aboveand beyond housing costs and other loan payments. In the above example, it turns out that based on ourcalculations, you can be at least $1,037 short at the every month if you were to buy the house that the bankhad approved you for.

Final Thoughts

It is every individual’s personal decision to figure out how much money they need to set aside to have peaceof mind. Some will want to save up enough to be able to maintain their lifestyle for many months in casethere is a disruption to their income source. Or others feel it’s important to set aside at least 10% of theirincome for future use or to invest it.

11/29/2016 www.greatcalgaryrealestate.com/blog/how-much-real-estate-can-you-afford/print.html

http://www.greatcalgaryrealestate.com/blog/how-much-real-estate-can-you-afford/print.html 5/5

There is no right or wrong answer when it comes to personal savings. But as long as you figure out your owncomfort level apart from the financial institution’s approval formula, you should be very comfortable living inyour new home knowing that you are not going to be financially stranded.