Yole Equipment Materials for 3DIC Wafer Level Packaging Sample October 2012

21

© 2012 Equipment & Materials for 3DIC and Wafer-Level-Packaging The second complete REPORT and exhaustive DATABASE analyzing in details the equipment and materials tool-box for packaging at the wafer scale November - 2012 SUSS Brewer Science DuPont SPTS PlanOptikt EVG

-

Upload

wirebonder -

Category

Documents

-

view

287 -

download

8

description

3D IC Market Report Sample

Transcript of Yole Equipment Materials for 3DIC Wafer Level Packaging Sample October 2012

© 2012

Equipment & Materials for 3DIC and Wafer-Level-Packaging

The second complete REPORT and exhaustive DATABASE analyzing in details

the equipment and materials tool-box for packaging at the wafer scale

November - 2012

SUSS Brewer Science DuPont SPTS PlanOptikt EVG

© 2012 • 2

Copyrights © Yole Développement SA. All rights reserved.

Table of Content

• Scope of the report & definitions ..……. 4 – Objectives, key features, glossary

• Executive Summary ….………………… 11

1) 3DIC & WLP Equipment & Materials

2011 – 2017 market forecasts ...………. 41 – Equipment market forecasts (in units and M$ revenues)

…………………………………………………....…… 48

o Breakdown details for Wafer Bonders / die bonders /

C2W Bonders / DRIE etching & other drilling tools /

CVD / PVD / ECD Plating / Exposure & Lithography /

Spray coating / Cleaning / Temporary Bonding & De-

Bonding / Grinding-Thinning-CMP / Wafer-molding /

Inspection & Metrology / Test tools

– Competitive landscape and market share of main

equipment suppliers detailed

– Materials market forecasts (in M$ revenues)

…………………………………………………......….. 86

o Breakdown details for Photoresist & coatings /

Adhesive tapes / pre-applied & wafer-level underfills /

Molding compounds / Plating & cleaning chemistries /

Slurries for CMP / Temporary bonding materials/ Gas

& precursors / sputtering targets

– Competitive landscape and market share of main

material suppliers detailed

2) 3DIC & WLP technologies process flows &

manufacturing trends analysis ……...... 110 – Focus on Flip-chip wafer bumping …………….. 112

o Introduction & background

o Typical manufacturing process flows

o Equipment & Materials suppliers involved

o Key process challenges and issues

– Focus on WL CSP packaging …………………... 118

– Focus on FO WLP packaging ………………...... 136

– Focus on 2.5D silicon interposers ................... 148

– Focus on 3D WLP …………………..…………….. 162

– Focus on 3DIC & TSV „Via Middle‟ …………….. 170

– Focus on “Via first” TSV

for WLP MEMS Oscillator with TSV……………..205

3) DATABASE in excel format …...……...… 275 – Detailed analysis of the activity of the 375+ key

equipment & material suppliers of the wafer-level-

packaging tool-box solutions (activity profiling & key contacts)

• Conclusions & Perspectives …...……... 281

• Appendix ………………….……....…….…. 286

© 2012 • 3

Copyrights © Yole Développement SA. All rights reserved.

Scope of this report coverage

Wafer-level-packaging Platforms

Wafer-Level Electrical Redistribution

Flip-chip & Wafer-Level Stacking / Integration

WL CSP ‘Fan-in’

FOWLP ‘Fan-Out’

Glass / Silicon

Flip-chip wafer bumping

on BGA

3D IC

& TSV

Embedded IC in PCB / laminate

Wafer-Level Interface / Encapsulation

3D WLP For MEMS & sensors

(also called 3D SiP sometimes)

2.5D

interposers

Complete Equipment & Materials Tool-Box covered in this report!

Dry film &

adhesive tapes

Photo resist

& coatings

Mold compound

& underfills

Indirect mat. (chemistries, cleaning,

CMP slurries…)

FE / BE / LCD / PCB related equipments

(litho & exposure, etch, deposition, plating, bonding, handling,

molding, thinning , dicing, test, metrology, etc…)

…)

Substrates (carriers, cap,

interposers…)

Gas /

precursors

© 2012 • 4

Copyrights © Yole Développement SA. All rights reserved.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2011 2012 2013 2014 2015 2016 2017

Vo

lum

e (i

n M

un

its

of

30

0m

m w

afer

eq

.)

Global Wafer-Level-Packaging demand (in Munits of 300mm wafer eq.)

Yole Developpement © October 2012

The emerging flavors of the “Mid-end”

3DIC

Flip-chip

2.5D interposers

3D WLP

WL CSP

FO WLP

3D SiP

• « Mid-end » infrastructure is growing and is the main leading driver and the fastest growing

semiconductor packaging technology with more than 18% CAGR in units over the next 6 years

to come

– Wafer-level-packaging technologies are a huge business opportunity in the future: historically supported by the market

growth in flip-chip wafer bumping with electroplated gold, solder bumps and today copper pillars, wafer-level-packages are

actually coming in many different flavors, namely Fan-in WLCSP packages, 3D WLP, FO WLP packages, 2.5D Glass /

Silicon interposers and of course 3DIC integration with TSV interconnects.

– As this wafer-level-packaging industry develops over time, we are noticed that a real infrastructure has emerged by itself

into what is now being called the “Mid-end” of the semiconductor manufacturing environment. Indeed, wafer-level-

packages are true “Mid-end” technologies in the sense that they can all be served in the „blur zone‟ of overlap between the

IDMs or CMOS foundries' back-end-of-line (BEOL) wafer fabs and the back-end wafer bumping assembly facilities of the

OSATs and wafer bumping houses

© 2012 • 5

Copyrights © Yole Développement SA. All rights reserved.

Transforming IC Packaging Supply Chain*

System /

Product

Sub-Module /

Sub-systems Design & Assembly

Design of chip & package

Wafer Level

Packaging « Middle -end »

Silicon Manufacturing

« Front-end »

Package Assembly

& Final test « Back-end »

Front-end related

materials suppliers

OEMs (Original

Equipment

Makers)

FE related

equipment suppliers

BE Packaging

materials suppliers

BE Packaging

equipment suppliers

Fab-less

IC players

IDMs (Integrated Device Manufacturers)

Integrated wafer / package manufacturing foundries

OSATs (Open Source Assembly & Test houses)

WLP houses (no need for traditional substrate)

PWB suppliers (motherboard)

ODM / EMS / DMS

(electronic design &

manufacturing services)

Passive comp. & SMT materials

SMT equipment

suppliers

SiP design

houses

Package substrate

laminate suppliers

Substrate material suppliers (FR4, BT resin, Cu clad, etc…)

* Existing business models represented in red, new

business models in orange

Wafer

foundries

Fab-smart players (foundry services + focused internal investment in manufacturing & critical IP)

Wafer Bumping houses PCB / PWB houses with Embedded die capability

© 2012 • 6

Copyrights © Yole Développement SA. All rights reserved.

Detailed 3DIC & WLP Process Flow Analysis

• It‟s worth noting that there‟s a significant difference in how manufacturing is generally

performed in the front-end versus in the back-end worlds – The back-end has generally a much greater cost sensitivity but can face scaling issues with time when

semiconductor ICs continue to reduce in chip size while increasing in pin-count number

– On the other hand, front-end related technologies are more expensive initially but could be preferable

because of higher repeatability, yield, throughput and because of better perspectives in the long run when it

comes to be able to scale down the technology to smaller pitch dimension while maintaining cost pressure

• Yole‟s analysts have updated the previous

report “equipment & materials” based on the

different alternatives offered by the present

equipment and material tool-box for wafer-

level-packaging – All main scenarios are analyzed, including flip-chip

wafer bumping trends, Fan-in WLCSP, 3D WLP,

FOWLP, 2.5D silicon interposers, 3DIC Via Middle &

Via Last process scenarios

© 2012 • 7

Copyrights © Yole Développement SA. All rights reserved.

2011 2012 2013 2014 2015 2016 2017

Equipment market $869 M $646 M $867 M $1 208 M $1 725 M $2 579 M $3 773 M

Material market $596 M $714 M $890 M $1 190 M $1 503 M $1 962 M $2 186 M

$0 M

$500 M

$1 000 M

$1 500 M

$2 000 M

$2 500 M

$3 000 M

$3 500 M

$4 000 M

Sale

s fo

reca

sts

(M$

)

Global Equipment & Material market forecast for 3DIC & Wafer-Level-Packaging (in M$)

Equipment market

Material market

Yole Developpement © October 2012

• The wafer-level-packaging market remains a huge business opportunity and

shows the greatest potential for significant future growth in the semiconductor

industry.

– That can be explain by the 3D IC technology which is fundamentally changing how processing

is done and offers the opportunity for new equipment modifications and new materials

development

Market Forecasts For 3DIC / WLP equipment & materials

24%

28%

© 2012 • 8

Copyrights © Yole Développement SA. All rights reserved.

2011 Global equipment market for 3D TSV & WLP

Wafer

bonding

$52M

TB &

Debond

$43M

Spin coating/

Developer

~$100M

Spray

coating

~$15M

ECD Plating

$138M

DRIE

$30,5M CVD

~$12M PVD

~$81M

Inspection/

Metrology

~$72M

Lithography

~$134M

Others: ~$2M;

2% DNS

$8M

8%

SUSS

$30M

30%

TEL

$60M

60%

Ebara

~$35M

25%

Novellus/ LAM

Research : ~$7M; 5%

AMAT/

Semitool

$69M

50%

TEL/NEXX

~$28M

20%

LAM/ Novellu

s

$12M

39%

SPTS

$10M

33%

Others:

$3,1M;

10%

AMA

T

~$5M

18%

Rudolph

Technologi

es:~$32M

44%

Others:

~$6$; 9%

Nanometrics:

~$2M; 3%

FOGALE

~$3M; 4%

Camtek

~$26M

36%

KLA Tencor

$3M

4%

Othe

rs:

$0,6

M

TE

L/N

EX

X

~$

1M

; 1

0%

AM

AT

~$

5M

; 4

0%

SPTS

$8M;

10%

Others: ~$2M;

3%

Tango

Systems

$16M

23%

Oerlikon

$20M

28%

LAM Research/

Novellus: $0,5M

0,6%

AMAT

$24M

34%

TEL/ NEXX

$9,6M

12%

Others

~$2M;

3%

TEL

$6M

12%

SUSS

~$11

M

22%

EVG

$33M

63%

TAZM

O/ 3M

~$11M

25%

SUSS

~$11

M

25%

TEL

~$7M

5%

TOK

~$4M

15%

EVG

~$11

M

25%

SUSS

~$13

M

82%

DNS

$1M;

6%

EVG

~$2

M

12%

Ultratech

$57M

43%

ASML

~$23M

17%

SUSS

~$51M

38%

Others: ~$3M

SP

TS

~$

5M

; 1

5%

Grinding

~$27M

DISCO

~$17,6

M

65%

ACCRE

TECH

~$4,1M

15%

Okamot

o $2,7M

10%

Starsbaug

h

$1,4M; 5µ

Others: $1,4M;

5%

SA

MP

LE

TOTAL: ~$870M

© 2012 • 9

Copyrights © Yole Développement SA. All rights reserved.

2011 Global materials market for 3D TSV & WLP

Others

$14M

13%

JSR Micro

$4M; 4%

Sumito Bakelite/

Promerus

$7M; 7%

Fujifilm

$23M; 22%

HD Microsystems/

Dupont

$28M

26%

DOW Chemical

$26M

25%

AZ Electronis Materials

$3M; 3%

Others

$3,3M

30%

Nagase

$7,7M

70%

Others $5M; 5%

Indium

$7M

15%

Sekisui

Chemicals

$14M

30%

Nippon

Micrometal

$9M

20%

Mitsubishi

Materials

$14M

30%

OM Group Ultra

Pure Chemicals

$10M

20%

ATOTECH

$19M

40%

Enthone

(Cookson Elect)

$14M

30%

Others

$4,8M

10% Hitachi Chemi

$1M; 2%

Cabot Micro

$36M

75%

AGC

~$6M

12%

Air Products

~$5M

10%

Others; $0,5$

Honeywell

$5,0M; 8%

Zeon Chemicals

$16M

25%

Dynaloy

$16M

25%

AZ Electronis

Materials

$6; 10%

Others: $1,2M; 2%

OM Group Ultra

Pure Chemicals

$12M

20%

Shin-Etsu Chemical

$6M

10%

TOK

$26M

20%

AZ Electronis Materials

$39M

30%

JSR Micro

$52M

40%

Dupont $3M; 2%

Dow electronic materials

$3M; 2%

Shin-Etsu Chemical; $4M

3%

Shin-Etsu Micro Si

$4M; 3%

Permanent dielectric

resists

$106,2M

Wafer Molding

compound

$11M

Solder paste

$46M

Plating

chemistries

$48M

Slurries for CMP

$48M

Cleaning chemistries

$62M Strippable plating resists

$130M

TOTAL: ~$590M

© 2012 • 10

Copyrights © Yole Développement SA. All rights reserved.

TEL (Tokyo Electron LTD.)

$60.0 M 60%

SUSS Microtec $30.0 M

30%

Dai Nippon SCREEN $8.0 M

8%

Others* $2.3 M

2%

Spin coating & Developer equipment for 3D & WLP 2011 Market Share Breakdown by supplier (in M$)

Yole Developpement © October 2012

* SSEC, EVG, TAZMO, TOK, Toray engineering, Ushio

2011 Spin-Coater/ Developer Equipment Market

3D & WLP Market share per equipment supplier

• Total market related to the spin coater & developer equipment market is assessed at $100M in 2011.

• The key providers active in spin coating & developer equipment are:

– TEL, SUSS MicroTec and Dai Nippon Screen

TEL has strong leadership in the middle-end packaging market especially related to the coating + developer

track equipment set

SUSS Micro is a key leader in spinc oater dedicated to WLP applications

TOT ~ 100 M$

© 2012 • 11

Copyrights © Yole Développement SA. All rights reserved.

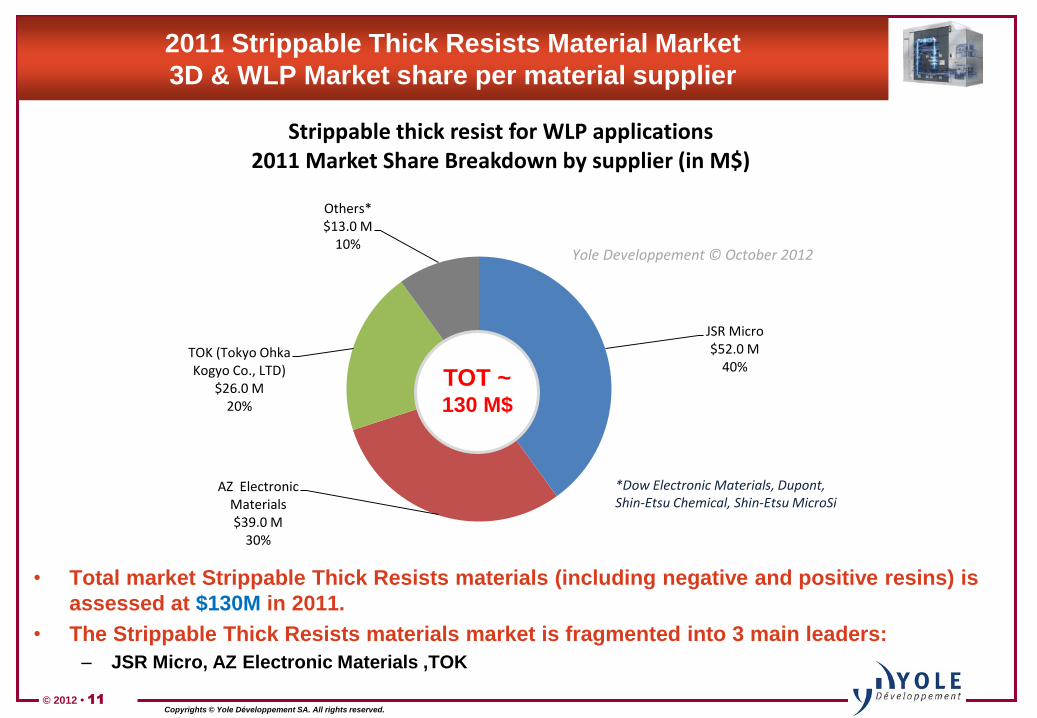

2011 Strippable Thick Resists Material Market

3D & WLP Market share per material supplier

• Total market Strippable Thick Resists materials (including negative and positive resins) is

assessed at $130M in 2011.

• The Strippable Thick Resists materials market is fragmented into 3 main leaders:

– JSR Micro, AZ Electronic Materials ,TOK

JSR Micro $52.0 M

40%

AZ Electronic Materials $39.0 M

30%

TOK (Tokyo Ohka Kogyo Co., LTD)

$26.0 M 20%

Others* $13.0 M

10%

Strippable thick resist for WLP applications 2011 Market Share Breakdown by supplier (in M$)

*Dow Electronic Materials, Dupont, Shin-Etsu Chemical, Shin-Etsu MicroSi

Yole Developpement © October 2012

TOT ~ 130 M$

© 2012 • 12

Copyrights © Yole Développement SA. All rights reserved.

More slides extracts (1/1)

© 2012 • 13

Copyrights © Yole Développement SA. All rights reserved.

DATABASE with 375+ key Equipment & Material

Suppliers for 3DIC / WLP

• The database wad steadily updated with new key equipment & materials suppliers – Along with this new research and updated report, Yole is delivering an excel database screening and

profiling the detailed activity of more than 375+ small to medium to giant equipment & material suppliers

coming either from Front-end, Back-end assembly, PCB, LCD or Solar industries and providing actual

solutions for the 3DIC & wafer-level-packaging tool-box

• One of the main move this year was the acquisition of NEXX by TEL, Tokyo

Electron, in March 2012, enabling the company to expand and enhance their

position in advanced packaging by being involved in electrochemical deposition

(ECD) and physical vapor deposition (PVD) systems.

© 2012 • 14

Copyrights © Yole Développement SA. All rights reserved.

375+ companies cited in this Report / Database

3M, 3MTS, 4Pico, Ablestik, ACCRETECH, ADEKA CORPORATION, Adtec Engineering, Advanced Chemical Company , Advanced Inquiry Systems,

Advantest, AGC, AI TEchnology Inc, Aimsolder, AIR LIQUIDE, Air Products, AJI – dvanced Jisso Technology, Ajinomoto Fine Techno Co Inc., Akrion

systems, AkroMetrix LLC, Alchimer, ALSI, Altatech Semiconductor, AMEC, Amicra Microtechnologies GmbH, AML, Anji Microelectronics, Applied

Materials, Applied Relay Testing, Applied Spectra, Asahi Kasei E-Materials Corporation, ASM Pacific Technologies, ASML Netherlands B.V.,

Assembleon, AST (Samurai), ASYS GmbH, ATI, ATMI, ATOTECH, Auros Tech, Austin American Technology Corp, Axcelis Technologies, Ayumi

Industry Co. Ltd., AZ Electronic Materials, Azores Corp, Barth Electronics, BASF, Bergquist Company, Berliner Glass, Blue-M, Boschman

Technologies B.V., Brewer Science, Bruker AXS , Cabot electronics, CAMTEK USA, Canon ANELVA, Cascade Microtech, CHAPMAN, Chomerics,

Corning, Corning Incorporated, CSM Instruments, Cyantek, Cyber-Technologies, Daxin Materials Corporation, Datacon Technology GmbH (BESI),

DCG Systems, DEK semiconductor, DELO, Delta Design, Denka, Disco Corporation, DJ DevCorp, Dai Nippon SCREEN, Dongjin Semichem Co.,

Doublecheck Semiconductors, Dow Corning Corporation, Dow Electronic Materials, DRY PLASMA SYSTEMS, D-Tek Technology Co.,Ltd, DuPont

Electronic Technologies, Dynaloy, DYNATEX International, Eastman Chemical, EBARA Technologies Corp., Ebina Denka, ECI Technology, EEJA,

Electroglas Inc, ENF Technology Co .Ltd, Enterprix, Enthone (Cookson Electronics), Epoxy Technology Inc., ERS – gmbh, ESEC AG, ESI, Etched in

Time Inc, EV Group, Evest Corp., EXCICO, Exelsius, FASSE CO., LTD., Fico molding (BESI), Finetech, FOGALE Nanotech, Frontier Semiconductor, Frt

Of America, FSI International, Fuji Polymers, FUJIFILM Electronic Materials, Furukawa America GE Sensing & Inspection, Gore, GPD Global, Inc.,

Hamamatsu, HamaTech APE GmbH & Co. KG, HD MicroSystems, Henkel Corporation, Heraeus GmbH, Hesse & Knipps, Hitachi Chemical Co., Ltd.,

Hitachi High Technologies Corporation, Honeywell Electronic Materials, HORIBA Semiconductor, Hoya, IceMOS Technology, ICOS Vision Systems

NV, Ikonix Imaging, Indium Corporation, Ishihara Chemical , Ismeca Europe Semiconductor SA, JENOPTIK, Jet Metal, JSR Micro, Kester, KiyoKawa

Plating industry, KLA-TENCOR, Koh Young Technology Inc., Kulicke & Soffa, Kyzen Corporation, Laird Technologies, LAM Research Corporation ,

Laserod, Lasertec Corporation, Lauffer Presses, Leybold Optics USA Inc, LG Chem., Ltd., Life Bioscience, LincoTec, Linde Gas, Lintec, Loadpoint,

LORD Corporation, Mapper Lithography, Materion, Mattson Technology, Mechatronic Systemtechnik, MECO, MEMC Electronic Materials, Inc. ,

Metryx, MicroChem, MicroFab Technologies Inc, Micronic Laser Systems AB, Micronics Japan Co., Mitshubishi Gas Chemical, Mitsubishi Chemical

Corporation, Mitsubishi Electric, Mitsubishi Heavy Industry (MHI), Mitsubishi Materials, Mitsubishi Materials Corporation, Mitsui Chemicals,

Momentive performance material, MSG Lithoglas AG, MTK Co, Ltd., Mühlbauer, Nagase & Co., Ltd., Namics, Nanda Tech GmbH, NANOPLAS,

Nanovea, NEC / SCHOTT, Newport, NEXX Systems, Nikko Metal, Nikon Corporation, Nippon Electric Glass – NEG, Nippon Kayaku Co., Ltd., Nippon

Sheet Glass – NSG, Nissan Chemical Industries, Nitta Haas Inc., Nitto Denko Corporation, Norcom Systems Inc, Nordson ASYMTEK, Inc., Nordson

dage, Nordson March, NOVELLUS, nScrypt Inc., Nusil Silicone Technology, Nypro Inc., oak-mitsui technologies, OEM group, Oerlikon, Okmetic,

Olympus-ITA, Inc., OM Group Ultra Pure Chemicals Pte. Ltd., OPµS, Orbotech Ltd., Oxford Instrument, Pac Tech, Palomar Technologies Inc.,

Panasonic Denko, PANASONIC Factory Solutions, Philips Applied Technologies, picoDRILL, Plan Optik AG GmbH, Polymatech, Potomac Laser,

Praxair.com, Promerus LLC, Protavic America, Inc., PVA TePla AG, Ramgraber GmbH, rasco, REC Silicon, RENA GmbH, Replisaurus Technologies,

Ricmar Technology GmbH, Rorze, Rudolph Technologies, Saint-Gobain, SAMCO Inc. , Schmoll Machinen, Schott AG, SCS - Speciality Coating

Systems, Sekisui Chemical Co., Ltd., Semiconductor Technologies & Instruments (ASTI), Semprius, Senju Metal Industry Co., Ltd., SENTECH

Instruments, SET - Smart Equipment Technology, Seto Engineering Co., Ltd., Shanghai Micro Electronics Equipment , Shanghai Sinyang, Shibaura

Mechatronics Corporation, Shibuya Kogyo, Shin-Etsu Chemical Co.,Ltd. , Shin-Etsu MicroSi, Inc, SHINKAWA LTD., Shinko Seiki, Silecs, Singulus,

SOITEC, Sokudo Co. Ltd., SolMateS, Solvay, SolVision, SONIX, SONOSCAN, SPP (Sumitomo Precision Products Co., Ltd.), SPTS, SSEC - Solid State

Equipment Corporation, Starfire Systems Inc., STIL SA, Strasbaugh, Sumco Corporation, Sumitomo Bakelite, Sumitomo Chemicals, Surface Science

Integartion, SUSS Microtec, Sysmelec, Takada, Takatori Ltd., Tamar Technology, Tamarack Scientific, Tango Systems, tecnisco, TEGAL, TEL (Tokyo

Electron LTD.), Teradyne, Thin materials AG, Timbre Technologies, tok, TOK (Tokyo Ohka Kogyo Co., LTD), Toray engineering Co.Ltd, Toray

Industries, Inc, TOWA Corporation, TRESKY, TRIOPTICS, Ultraspray, Ultratech , ULVAC Inc., Umicore, Uyemura Co.Ltd, Uyemura International

Corporation, Veeco, Verigy, Viscom AG, West-Bond, Inc., Xradia, YAMADA CORPORATION, Young Chang Chemical, YoungTek Electronics Corp.,

Zebra Optical, Zeon Chemicals L.P., Zetta Core, Zygo Corporation, Zymet, Inc.

© 2012 • 15

Copyrights © Yole Développement SA. All rights reserved.

About the authors of this report

Jerome Baron Jerome is leading the MEMS &

Advanced Packaging market

research at Yole Developpement.

He has been following the 3D

packaging market evolution

since its early beginnings at

device, equipment and material

levels. He was granted a Master

of Science degree in

Nanotechnologies from the

National Institute of Applied

Sciences in Lyon, France

Contact: [email protected]

Amandine Pizzagalli Amandine recently joined Yole

Development Advanced Packaging

and MEMS manufacturing teams

after graduating as an engineer in

Electronics, with a specialization in

Semiconductors and Nano

Electronics Technologies. She

worked in the past for Air Liquide

with an emphasis on CVD and ALD

processes for semiconductor

applications

Contact: [email protected]

© 2012 • 16

Copyrights © Yole Développement SA. All rights reserved.

Who should be interested in this report?

• Equipment & Material suppliers – Assess the TAM – total accessible market of

your company‟s related products in the

wafer-level-packaging areas

– Identify technology trends, challenges and

precise requirements for each 3DIC / WLP

scenarios

– Screen competition activity, identify possible

partnerships or targets for M&As in areas

close to your current business

• R&D organizations & Investors – Monitor the global activity and consolidation

currently happing in the semiconductor

equipment & material business in order to

identify new partners, targets and take the

right decision before committing to one

particular supplier

• IDMs, CMOS foundries & OSAT

players – Get an exhaustive list of the 350+

equipment & materials companies

supplying solutions in the different 3DIC

and wafer-level-packaging areas

– Understand technology trends and

benchmark several different 3DIC & WLP

scenarios including the future trends for

PANEL scale packaging based on LCD /

PCB infrastructures

• PCB substrate manufacturers – Get the complete list of semiconductor

packaging equipment & materials

companies supplying solutions in the

blooming 3DIC & wafer-level-packaging

area

– Identify technology trends, challenges

and issues for each 3D packaging

scenario

© 2012 • 17

Copyrights © Yole Développement SA. All rights reserved.

Yole Developpement Company Presentation

© 2012 • 18

Copyrights © Yole Développement SA. All rights reserved.

Yole activities in Advanced Packaging

Media business News feed / Magazines / Webcasts

www.yole.fr

© 2009

Copyrights © Yole Développement SARL. All rights reserved.

HB-LED Packaging Technology & Market Trends

IR

Osram

Market Research

Reports

Market research, Technology & Strategy

Consulting services

© 2012 • 19

Copyrights © Yole Développement SA. All rights reserved.

Our Global Presence & Activity

Yole Inc.

Yole Développement

Lyon (HQ).

Yole Europe

Yole Japan

30% of our activity is

in North America

30% of our activity is

in Asia

40% of our activity is in

EU Countries

Yole Taiwan

Yole Korea

© 2012 • 20

Copyrights © Yole Développement SA. All rights reserved.

Supporting the Entire Value Chain

Yole consultants provide Market Analysis, Technology Evaluation and Business Plan Assessment for clients along the entire value chain

Institutions Investors

& Advocates

Integrators &

End Users

Device &

Module Makers

Material &

Equipment Suppliers

© 2012 • 21

Copyrights © Yole Développement SA. All rights reserved.

Via First / Via Last? 3D integration Scenarios

I

M

E

C

S

i

l

e

x

F

r

e

e

s

c

a

l

e

N

o

k

i

a

D

u

P

o

n

t

TSV+ Cost Analysis Tool for

your 3D IC manufacturing

3D IC & TSV 2010 Market Analysis

I

M

E

C

S

i

l

e

x

F

r

e

e

s

c

a

l

e

N

o

k

i

a

D

u

P

o

n

t

$27

7% $23

6%

$109

26%

$82%$37

9%$92%

$317%

$168

41%

TSV Scenario Cost structure breakdown

Via / Etching Drilling

Via Isolation

Via filling

Temporary bonding

Thinning

Stress release

BEOL (Pads)

Bonding

IPD - Thin-film Integrated Passive Devices

WL CSP 2012 Report update

N

o

k

i

a

2.5D Glass & Silicon

interposers - 2010 Report

© 2010

Copyrights © Yole Développement SA. All rights reserved.

MEMS Packaging Market & Technology Trends

1995

Sidebraze DIP

1996-2002

Plastic PDIP

1999 - today

SMT SOIC

& Die Down

2006

Stacked Die

QFN

~125 sq mm ~100 sq mm ~25 sq mm

6 & 6 mm

1995

Sidebraze DIP

1996-2002

Plastic PDIP

1999 - today

SMT SOIC

& Die Down

2006

Stacked Die

QFN

~125 sq mm ~100 sq mm ~25 sq mm

6 & 6 mm

Our latest advanced packaging

market research reports

© 2010

Copyrights © Yole Développement SARL. All rights reserved.

Advanced PackagingEquipment & Materials

NEC-Schott

SUSS Brewer ScienceSTSEVG

DuPont

Equipment & Materials for 3DIC & Wafer-Level-Packaging

Flip-chip 2011 Report

FO WLP & Embedded die

Wafer Packaging Fabs

DATABASE

© 2009

Copyrights © Yole Développement SARL. All rights reserved.

HB-LED Packaging Technology & Market Trends

IR

Osram

LED Packaging Market & Technology Trends

![WP91 Lucia Montanaro Kosovo State Building Conundrum 3dic[1]](https://static.fdocuments.in/doc/165x107/577d27671a28ab4e1ea3d6e5/wp91-lucia-montanaro-kosovo-state-building-conundrum-3dic1.jpg)

![Yole 3DIC & TSV Interconnects July 2012 Sample[1]](https://static.fdocuments.in/doc/165x107/54650439af795974338b4c77/yole-3dic-tsv-interconnects-july-2012-sample1.jpg)