Xbrane Biopharma Corporate Presentation April 2019 · Board & Management Team Jointly Involved In...

41

1 Xbrane Biopharma Corporate Presentation April 2019

Transcript of Xbrane Biopharma Corporate Presentation April 2019 · Board & Management Team Jointly Involved In...

1

Xbrane Biopharma Corporate Presentation April 2019

2

Important Information

You must read the following before continuing. The following applies to this document and the information provided in this presentation by Xbrane Biopharma AB (publ) (the “Company”) or any person on behalf of the Company and any other material distributed or statements made in connection with such presentation (the “Information”), and you are therefore advised to carefully read the statements below before reading, accessing or making any other use of the Information. In accessing the Information, you agree to be bound by the following terms and conditions.

The Information does not constitute or form part of, and should not be construed as, an offer or invitation to subscribe for, underwrite or otherwise acquire, any securities of the Company or a successor entity or any existing or future subsidiary or affiliate of the Company, nor should it or any part of it form the basis of, or be relied on in connection with, any contract to purchase or subscribe for any securities of the Company or any of such subsidiaries or affiliates nor shall it or any part of it form the basis of or be relied on in connection with any contract or commitment whatsoever. Specifically, this presentation does not constitute a “prospectus” within the meaning of the U.S. Securities Act of 1933, as amended.

The Information may not be reproduced, redistributed, published or passed on to any other person, directly or in directly, in whole or in part, for any purpose. The Information is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of, or located in, any locality, state, country or other jurisdiction where such distribution or use would be contrary to law or regulation or which would require any registration or licensing within such jurisdiction. The Information is not for publication, release or distribution in the United States, the United Kingdom, Australia, Canada or Japan, or any other jurisdiction in which the distribution or release would be unlawful.

All of the Information herein has been prepared by the Company solely for use in this presentation. The Information contained in this presentation has not been independently verified. No representation, warranty or undertaking, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the Information or the opinions contained herein. The Information contained in this presentation should be considered in the context of the circumstances prevailing at that time and has not been, and will not be, updated to reflect material developments which may occur after the date of the presentation. The Company may alter, modify or otherwise change in any manner the content of this presentation, without obligation to notify any person of such revision or changes.

This presentation may contain certain forward-looking statements and forecasts which relate to events and depend on circumstances that will occur in the future and which, by their nature, will have an impact on the Company’s operations, financial position and earnings. The terms “anticipates”, “assumes”, “believes”, “can”, “could”, “estimates”, “expects”, “forecasts”, “intends”, “may”, “might”, “plans”, “should”, “projects”, “will”, “would” or, in each case, their negative, or other variations or comparable terminology are used to identify forward-looking statements. There are a number of factors that could cause actual results and developments to differ materially from those expressed or implied in a forward-looking statement or affect the extent to which a particular projection is realised. Factors that could cause these differences include, but are not limited to, implementation of the Company’s strategy and its ability to further grow, risks associated with the development and of the Company’s products, ongoing research and development, the ability to commercialize the Company’s products, technology changes and new products in the Company’s potential market and industry, the ability to develop new products, the impact of competition, changes in general economy and industry conditions and legislative, regulatory and political factors. While the Company always intends to express its best judgment when making statements about what it believes will occur in the future, and although the Company bases these statements on assumptions that it believe to be reasonable when made, these forward-looking statements are not a guarantee of its performance, and you should not place undue reliance on such statements. Forward-looking statements are subject to many risks, uncertainties and other variable circumstances. Such risks and uncertainties may cause the statements to be inaccurate and readers are cautioned not to place undue reliance on such statements. Many of these risks are outside of the Company’s control and could cause its actual results to differ materially from those it thought would occur. The forward-looking statements included in this presentation are made only as of the date hereof. The Company does not undertake, and specifically decline, any obligation to update any such statements or to publicly announce the results of any revisions to any of such statements to reflect future events or developments.

3

Table of Contents

Presenters

Martin ÅmarkCEO

Anders Tullgren

Chairman of the Board

1. Xbrane Biopharma Overview

2. The Biosimilar Market

3. The VGEF Market & The Unmet Medical Need

4. Lead Product Xlucane

5. Summary & Investment Highlights

4

Xbrane - Biosimilar Developer With Patented High Yield Technology

Lead Product Xlucane In Phase III With Commercial Partner STADA. Annual Sales Target Of €350 M. Income Of €100 M For Xbrane After COGS, SG&A And Partner Profit Sharing.

Addressing Attractive Biosimilar Market Opportunity. The Fastest Growing Segment Within Pharma Combined With Low Technical Risk

Patented Innovative High-yield Technology Platform Resulting In Low Production Costs

Strong Product Pipeline Targeting +€ 11 B In Originator Sales. Only Public Biosimilar Developments To Opdivo® And Cimzia®

Listed At Nasdaq First North With € 35 M* Market Cap – Up-Listing To Main Market During 2019

*As of 2019-04-18

5

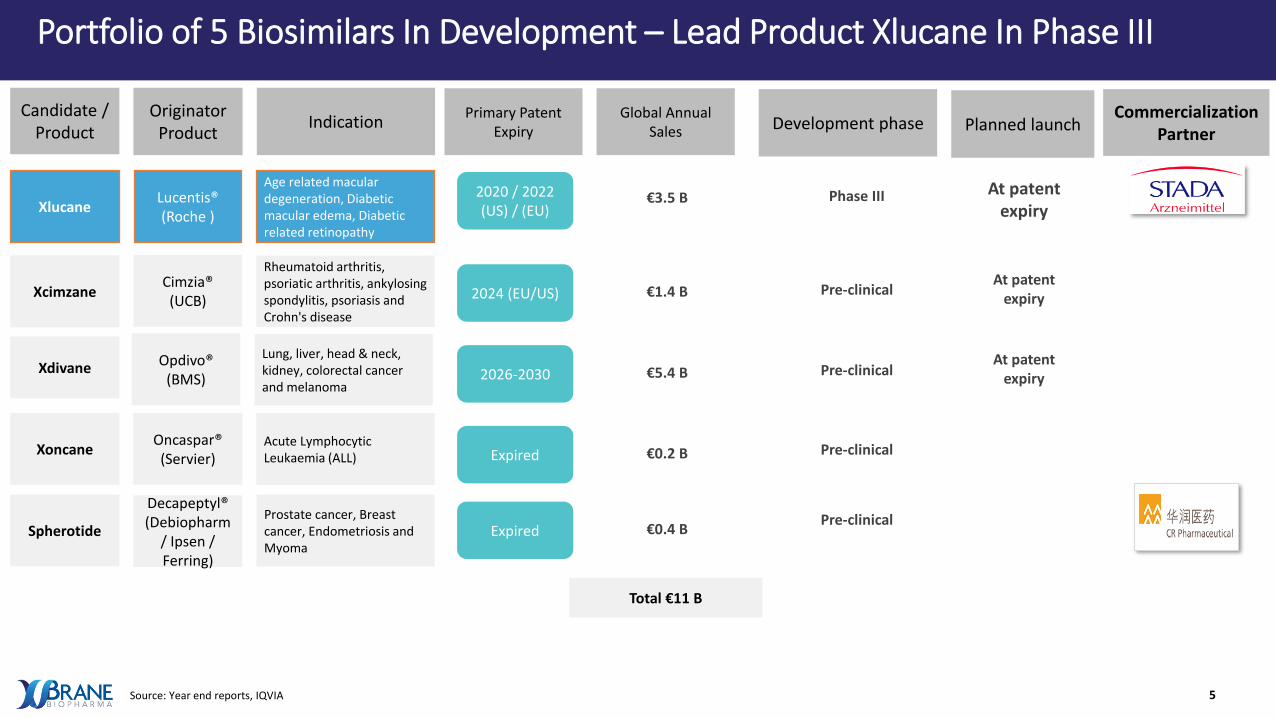

Portfolio of 5 Biosimilars In Development – Lead Product Xlucane In Phase III

Commercialization Partner

o

Candidate / Product

Originator Product

Indication Development phase Planned launch

Xlucane

Xcimzane

Xoncane

Spherotide

Xdivane

Lucentis®(Roche )

Cimzia®(UCB)

Oncaspar®(Servier)

Decapeptyl®(Debiopharm

/ Ipsen / Ferring)

Age related macular degeneration, Diabetic macular edema, Diabetic related retinopathy

Rheumatoid arthritis, psoriatic arthritis, ankylosing spondylitis, psoriasis and Crohn's disease

Acute Lymphocytic Leukaemia (ALL)

Prostate cancer, Breast cancer, Endometriosis and Myoma

At patent expiry

Opdivo®(BMS)

Lung, liver, head & neck, kidney, colorectal cancer and melanoma

Primary Patent Expiry

2020 / 2022 (US) / (EU)

2024 (EU/US)

Expired

Expired

Global Annual Sales

€3.5 B

€1.4 B

€0.2 B

€0.4 B

2026-2030 €5.4 B

At patent expiry

At patent expiry

Phase III

Pre-clinical

Pre-clinical

Pre-clinical

Pre-clinical

Total €11 B

Source: Year end reports, IQVIA

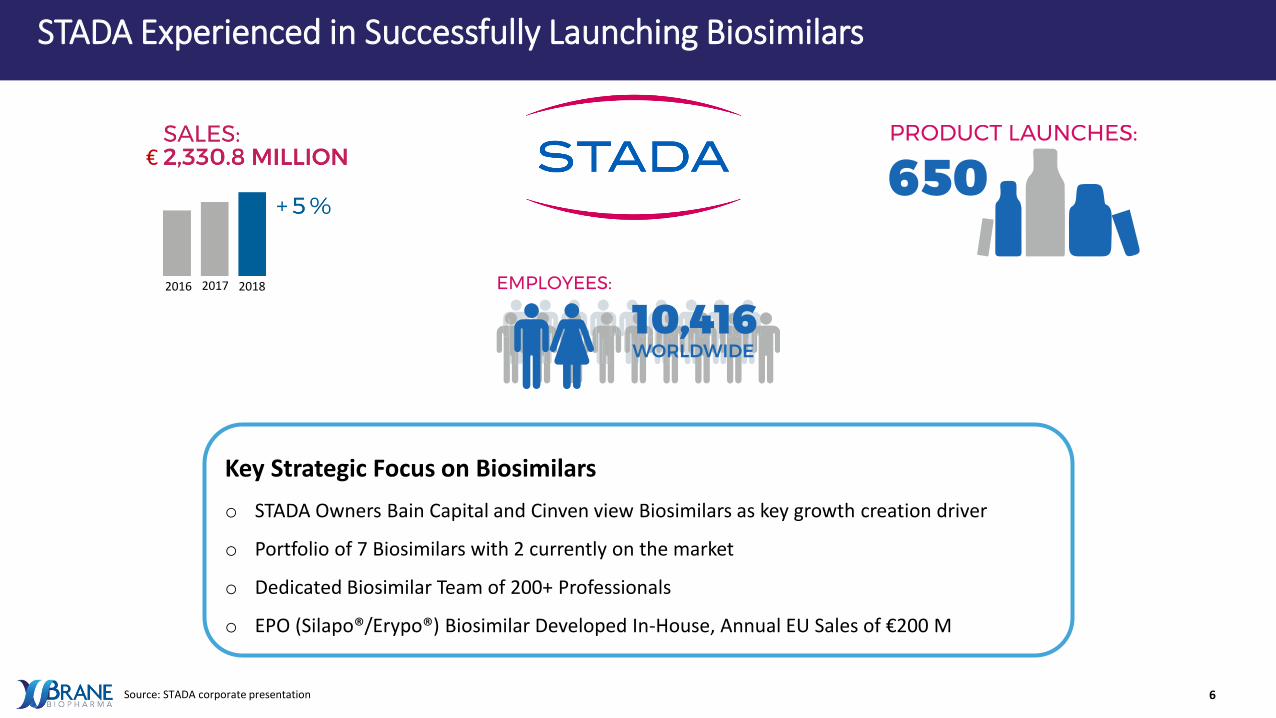

6Source: STADA corporate presentation

STADA Experienced in Successfully Launching Biosimilars

Key Strategic Focus on Biosimilars

o STADA Owners Bain Capital and Cinven view Biosimilars as key growth creation driver

o Portfolio of 7 Biosimilars with 2 currently on the market

o Dedicated Biosimilar Team of 200+ Professionals

o EPO (Silapo®/Erypo®) Biosimilar Developed In-House, Annual EU Sales of €200 M

201820172016

€

7

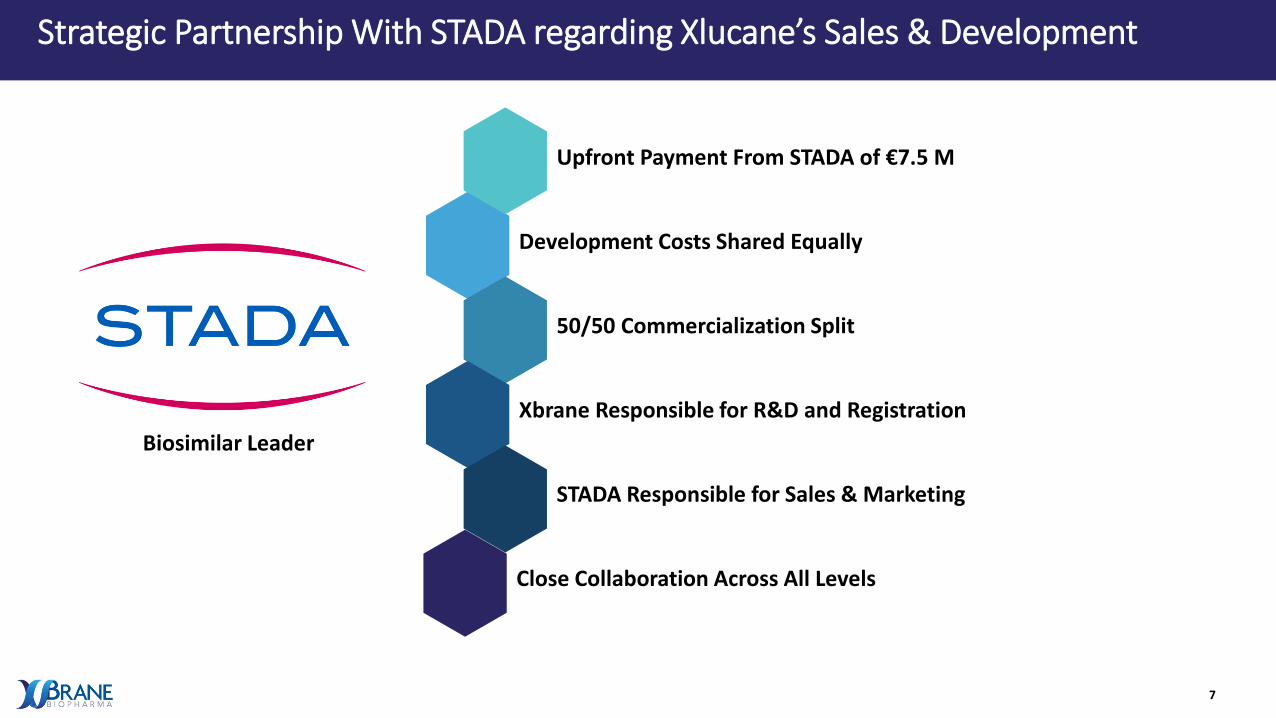

Strategic Partnership With STADA regarding Xlucane’s Sales & Development

Upfront Payment From STADA of €7.5 M

Development Costs Shared Equally

50/50 Commercialization Split

Xbrane Responsible for R&D and Registration

STADA Responsible for Sales & Marketing

Close Collaboration Across All Levels

Biosimilar Leader

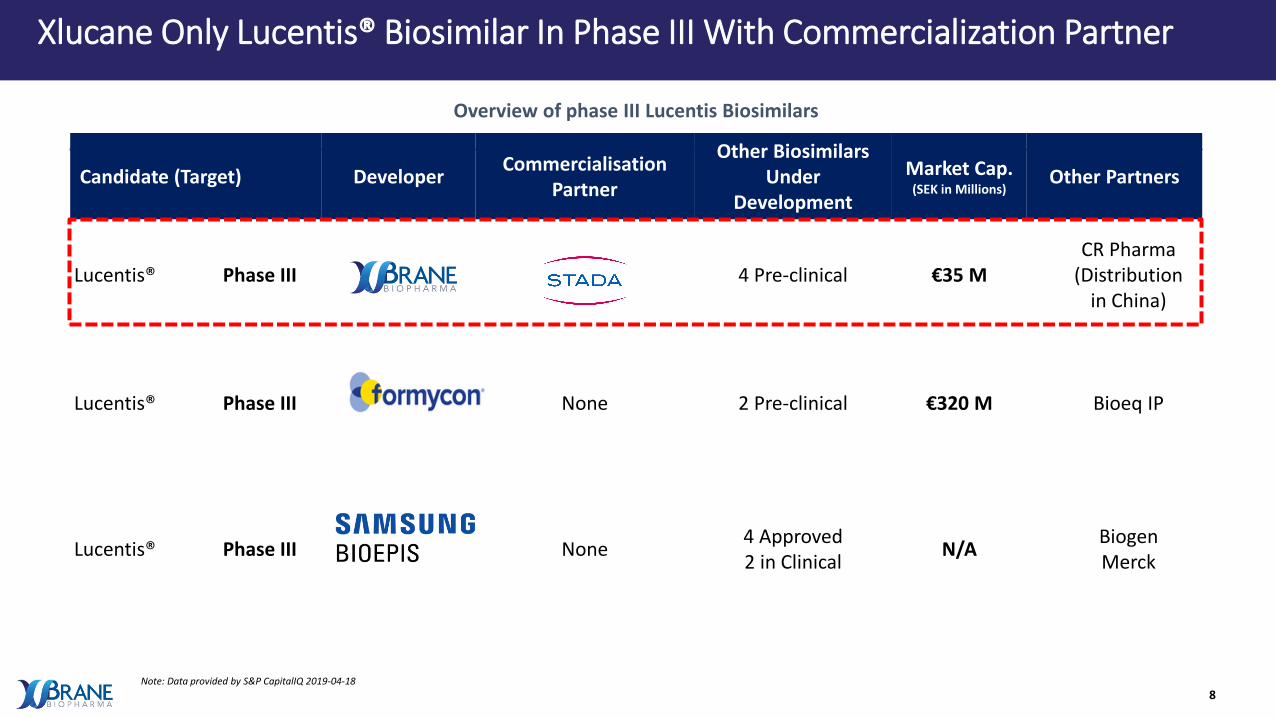

8Note: Data provided by S&P CapitalIQ 2019-04-18

Candidate (Target) DeveloperCommercialisation

Partner

Other Biosimilars Under

Development

Market Cap. (SEK in Millions)

Other Partners

Lucentis® Phase III 4 Pre-clinical €35 MCR Pharma

(Distribution in China)

Lucentis® Phase III Formycon AG None 2 Pre-clinical €320 M Bioeq IP

Lucentis® Phase IIISamsung Bioepis

None4 Approved2 in Clinical

N/ABiogenMerck

Overview of phase III Lucentis Biosimilars

Xlucane Only Lucentis® Biosimilar In Phase III With Commercialization Partner

9

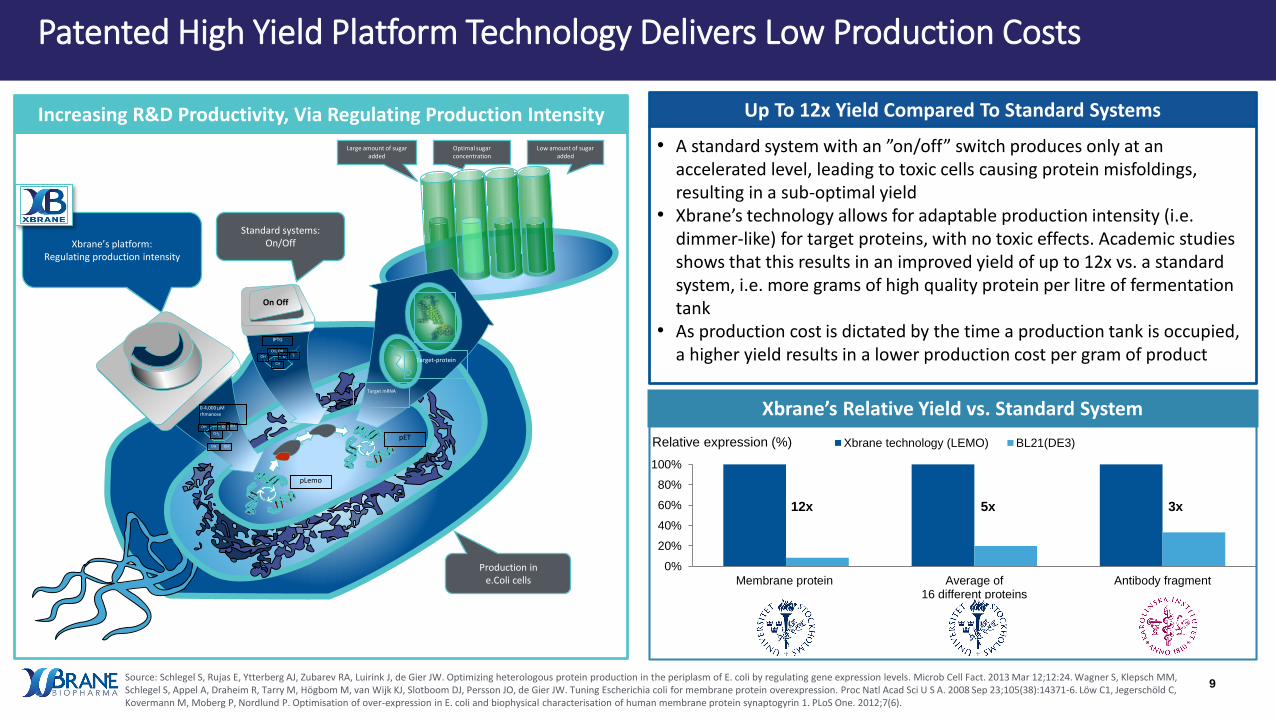

Patented High Yield Platform Technology Delivers Low Production Costs

Increasing R&D Productivity, Via Regulating Production Intensity

On Off

Xbrane’s platform: Regulating production intensity

Standard systems: On/Off

Production in e.Coli cells

pLemo

pET

0-4,000 µM rhmanose

OHOH

OHOH oCH2

IPTG

SOH o

CH

CH2 OH

Target mRNA

Target-protein

Large amount of sugar added

Optimal sugar concentration

Low amount of sugar added

o

• Source: Schlegel S, Rujas E, Ytterberg AJ, Zubarev RA, Luirink J, de Gier JW. Optimizing heterologous protein production in the periplasm of E. coli by regulating gene expression levels. Microb Cell Fact. 2013 Mar 12;12:24. Wagner S, Klepsch MM, Schlegel S, Appel A, Draheim R, Tarry M, Högbom M, van Wijk KJ, Slotboom DJ, Persson JO, de Gier JW. Tuning Escherichia coli for membrane protein overexpression. Proc Natl Acad Sci U S A. 2008 Sep 23;105(38):14371-6. Löw C1, Jegerschöld C, Kovermann M, Moberg P, Nordlund P. Optimisation of over-expression in E. coli and biophysical characterisation of human membrane protein synaptogyrin 1. PLoS One. 2012;7(6).

Up To 12x Yield Compared To Standard Systems

• A standard system with an ”on/off” switch produces only at an accelerated level, leading to toxic cells causing protein misfoldings, resulting in a sub-optimal yield

• Xbrane’s technology allows for adaptable production intensity (i.e. dimmer-like) for target proteins, with no toxic effects. Academic studies shows that this results in an improved yield of up to 12x vs. a standard system, i.e. more grams of high quality protein per litre of fermentation tank

• As production cost is dictated by the time a production tank is occupied, a higher yield results in a lower production cost per gram of product

Xbrane’s Relative Yield vs. Standard System

0%

20%

40%

60%

80%

100%

Membrane protein Average of16 different proteins

Antibody fragment

Xbrane technology (LEMO) BL21(DE3)Relative expression (%)

12x 5x 3x

10

Jointly involved in development of

over 25 marketed pharmaceuticals

ChaAnders

Tullgren

M.Sc.

Chairman

Saeid

Esmaeilzadeh

Ph.D.

Board Member

Maris Hartmanis

Ph.D.

Board Member

Peter Edman

Ph.D.

Board Member

Karin Wingstrand

M.Sc.

Board Member

Alessandro Sidoli

M.Sc.

Board Member

Giorgio Chirivi

M.Sc.

Board Member

Board & Management Team Jointly Involved In Development Of Over 35 Marketed Pharmaceuticals

Board of Directors Management And Core Development Team

Jointly involved in development of over 10 marketed pharmaceuticals

CEO

Martin Åmark

M.Sc./MBA

Head of Biosimilars

Siavash Bashiri

M.Sc.

CFO

Susanna Helgesen

M.Sc.

Head of Long acting

injectables

Paolo Sarmientos

Ph.D.

CTO

David Vikström

Ph.D.

Head of Clinical Affairs

Dina Jurman

M.Sc.

Head of Regulatory

Maria Edebrink

M.Sc.

Head of Analytics

Per Edebrink

Ph.D

Patrik Samuelsson

Head of Upstream

Ph.D

Nurzian Ismail

Head of Downstream

Ph.D

Anders Wallström

Head of Supply-Chain

M.Sc.

Ilaria Sammartino

Quality Assurance

11

Company History

Xbrane BipharmaFounded at Stockholm

University

2008

Acquired Primm Pharma

with the product Spherotide

2015

GMP Approval Xbrane obtains GMP

approval for its facility for the production of Spherotide

2016 2017

Commercialization agreement

for Sphetodite in China signed with the country’s second largest

pharmaceutical distribute CR Pharma

2018

Xbrane partners with STADA for the development and

commercialization of Xlucane

First patient inIn Xlucane phase III trial

2019

CTA Approval from FDA

for initiation of pivotal phase III study with

Xlucane

Xbrane IPO’son Nasdaq First North and raised SEK 100 M

Establishment of biosimilar pilot

facilityin Stockholm

Patent approval of E.coli platform

Xbrane E.coli expression technology patent approved

in Europe

Mammalian cell based platform

establishedand development of

Xdivane (Opdivo) accelerated

12

Table of Contents

1. Xbrane Biopharma Overview

2. The Biosimilar Market

3. The VGEF Market & The Unmet Medical Need

4. Lead Product Xlucane

5. Summary & Investment Highlights

Presenters

Martin ÅmarkCEO

Anders Tullgren

Chairman of the Board

13

Biosimilars: Follow-On Biologics Launched When Originator Product Patent Expires

Source: 1FDA; CancerNet Dictionary

Based on living cells, with complex molecular structures requiring high-level development and production yet have the advantages of fewer side effects and enhanced efficacy

Based on chemical substances, made by combining specific chemical ingredients in an ordered process, creating a well-

defined chemical structure. Can usually be analyzed to determine all its various components

GENERICS

• Identical copy of originator active ingredient

• Bioequivalence demonstrated clinically

PHARMACEUTICALS

SMALL MOLECULES BIOLOGICS

BIOSIMILARS

• Highly similar molecule as originator

• Analytical similarity demonstrated with +20 methods

• Equivalent efficacy and safety demonstrated clinically (Phase I and Phase III)

Living cellChemicalsubstance

14Note: Exchange rate EUR/USD = 1.2003 as of December 31 2017. Source: 1) Tufts Center for the Study of Drug Development (CSDD); 2) Informa Pharma’s Biomedtracker database, based on 108 tracked biosimilardevelopment programs and over 10,000 novel product development programs; 3) IQVIA - The impact of biosimilar competition in Europe.

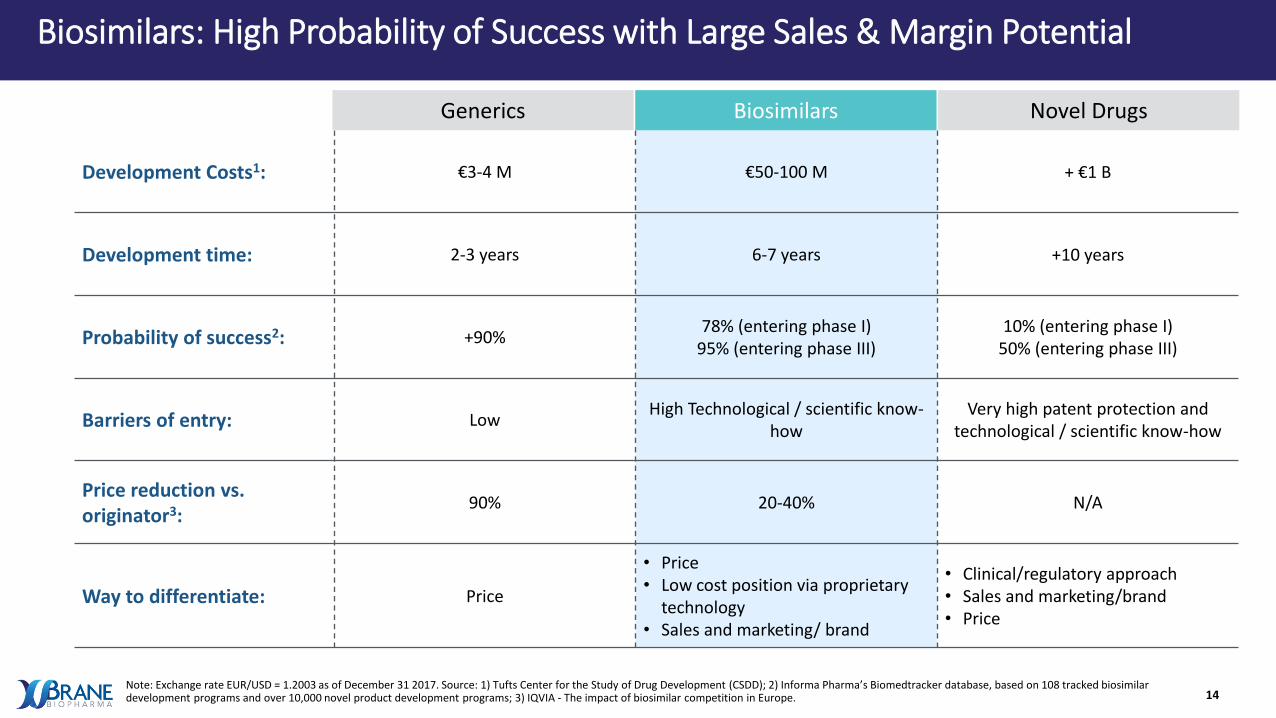

Biosimilars: High Probability of Success with Large Sales & Margin Potential

Development Costs1: €3-4 M €50-100 M + €1 B

Development time: 2-3 years 6-7 years +10 years

Probability of success2: +90%78% (entering phase I)

95% (entering phase III)10% (entering phase I)

50% (entering phase III)

Barriers of entry: LowHigh Technological / scientific know-

howVery high patent protection and

technological / scientific know-how

Price reduction vs. originator3:

90% 20-40% N/A

Way to differentiate: Price

• Price• Low cost position via proprietary

technology• Sales and marketing/ brand

• Clinical/regulatory approach• Sales and marketing/brand• Price

Generics Biosimilars Novel Drugs

15

11 of Global Top 15 Drugs Are Biologics

Source: IGEA

Position ProductAnnual Sales 2017

(€ Billion)Category

1 Humira® €16,2 Biologic

2 Revlimid® €7,2 Small Molecule

3 Rituxan® €7,1 Biologic

4 Enbrel® €7,0 Biologic

5 Herceptin® €6,6 Biologic

6 Eliquis® €6,5 Small Molecule

7 Avastin® €6,3 Biologic

8 Remicade® €6,3 Biologic

9 Xarelto® €5,8 Small Molecule

10 Eylea® €5,5 Biologic

11 Januvia® €5,2 Small Molecule

12 Lantus® €5,0 Biologic

13 Prevnar® €4,9 Biologic

14 Opdivo® €4,4 Biologic

15 Neulasta® €4,0 Biologic

16

US & EU Biosimilar Market Expected To Grow from €2.6 B to €11.8 B in 2025

Loss of Exclusivity of Originators

+€ 100B additional originator sales to be exposed 2022

Regulatory Clarity

44 biosimilars approved in Europe, 19 in US

Payor, Physician and Patient Adoption

Biosimilar penetration on filgrastim up to 90% in Europe

Source: BCC research. IQVIA; Morgan Stanley

Growth drivers

0,91,7 2,3

3,14,0

6,16,9

7,7

1,7

3,0

3,6

3,7

4,2

4,34,2

4,2

2,6

4,7

5,9

6,9

8,2

10,411,1

11,8

-1,0

1,0

3,0

5,0

7,0

9,0

11,0

13,0

15,0

2018 2019 2020 2021 2022 2023 2024 2025

Biosimilar Market (€ Billion)

US EU

17

By Year Three Biosimilars Reached 50-75% Market Share – Faster Uptake In Recent Launches

0%

25%

50%

75%

100%

0 1 2 3 4 5 6 7 8 9

Years After Launch

EPO

GCSF

HGH

Infliximab

Etanercept

Rituximab

Traztuzumab

Adalimumab

Average Biosimilar Volume Market Share vs. Originator In Europe

91%

8 years

51%

3 years

67%

9 years

41%

8 years

60%

1 years

35%

4 months 40%

2 years10%

2 months

Laun

chseq

uen

ce

Source: IQVIA, - The impact of biosimilar competition in Europe, Morgaon Stanley – Biosimilars infancy to Youth

0%

25%

50%

75%

100%

0 1 2 3

Years After Launch

GCSF

InsulinGlargine

Average Biosimilar Volume Market Share Vs. Originator In US

75%

3 years

26%

1,5 years

6%

1 year

Agressiveportfolio rebatedefense by J&J

Laun

chseq

uen

ce

18

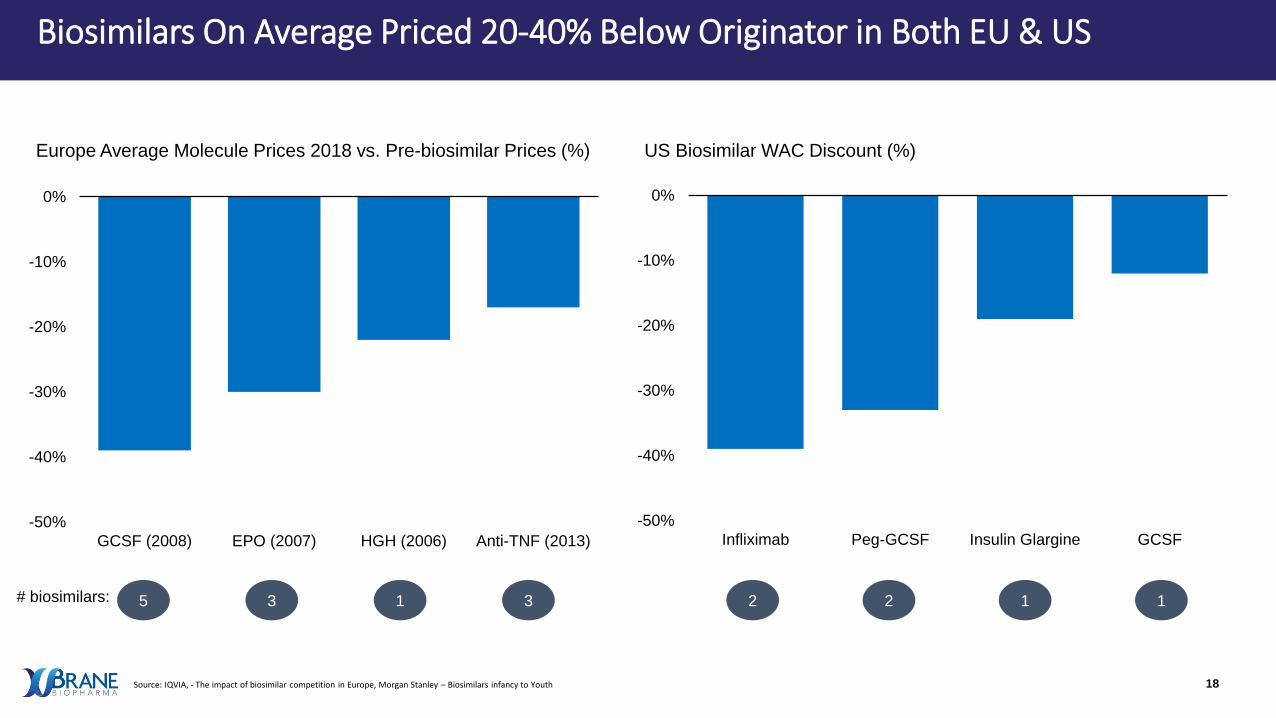

Europe Average Molecule Prices 2018 vs. Pre-biosimilar Prices (%)

-50%

-40%

-30%

-20%

-10%

0%

GCSF (2008) EPO (2007) HGH (2006) Anti-TNF (2013)

# biosimilars: 5 3 1 3

-50%

-40%

-30%

-20%

-10%

0%

Infliximab Peg-GCSF Insulin Glargine GCSF

US Biosimilar WAC Discount (%)

Biosimilars On Average Priced 20-40% Below Originator in Both EU & US

2 2 1 1

Source: IQVIA, - The impact of biosimilar competition in Europe, Morgan Stanley – Biosimilars infancy to Youth

19

Biosimilars Generated Annual Sales Of €300-600 Million

0

100

200

300

400

500

600

700

Basalgar Inflectra Benepali Truxima Remsima

Annual Sales 2018 Select Biosimilars (€ M)

Europe US

Launch: US 2017EU 2016

US 2016EU 2015

2016 2017 2015

Truxima And Remsima DevelopedBy Celltrion - Generating 65% OfRevenue From Biosimilars With55% Operating Margin In 2018

Source: IQVIA, - The impact of biosimilar competition in Europe, Morgan Stanley – Biosimilars infancy to Youth

20

Table of Contents

1. Xbrane Biopharma Overview

2. The Biosimilar Market

3. The VGEF Market & The Unmet Medical Need

4. Lead Product Xlucane

5. Summary & Investment Highlights

Presenters

Martin ÅmarkCEO

Anders Tullgren

Chairman of the Board

21

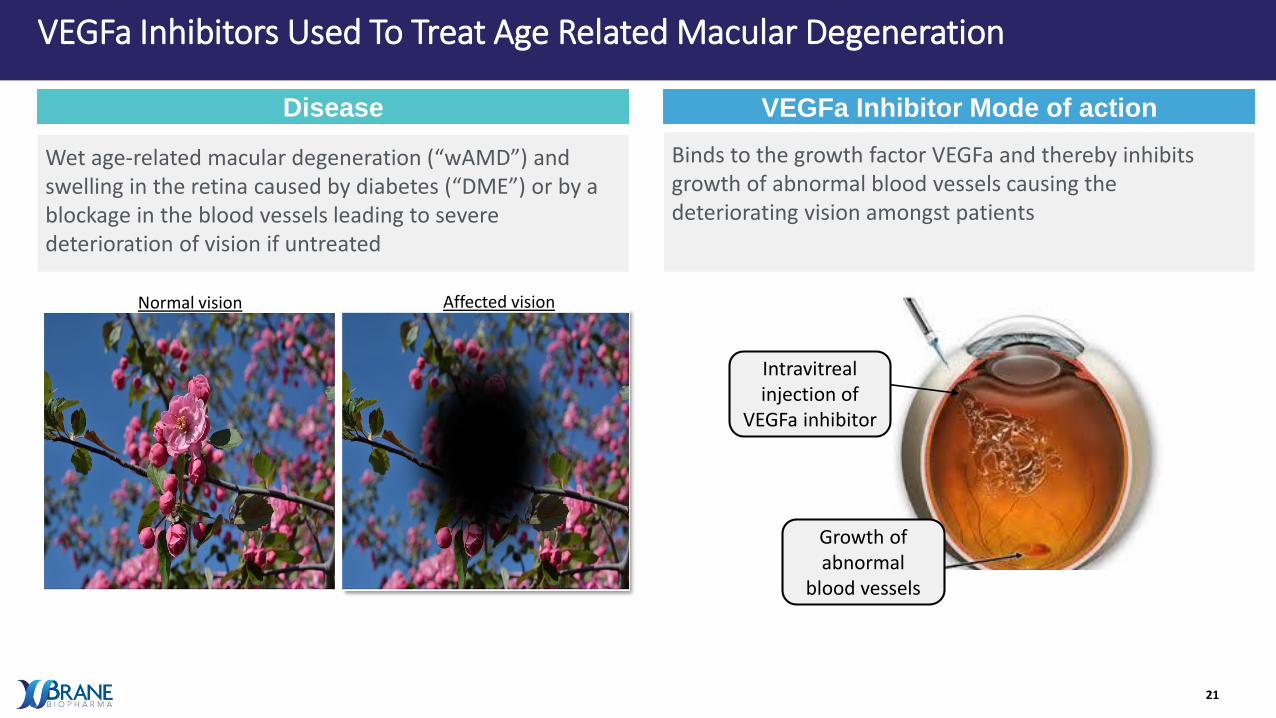

VEGFa Inhibitors Used To Treat Age Related Macular Degeneration

Wet age-related macular degeneration (“wAMD”) and swelling in the retina caused by diabetes (“DME”) or by a blockage in the blood vessels leading to severe deterioration of vision if untreated

Binds to the growth factor VEGFa and thereby inhibits growth of abnormal blood vessels causing the deteriorating vision amongst patients

Disease VEGFa Inhibitor Mode of action

Normal vision Affected vision

Growth ofabnormal

blood vessels

Intravitrealinjection of

VEGFa inhibitor

2222Source: 1) HARBOR, ANCHOR, MARINA, PrONTO trials; 2) VIEW1 and VIEW2 trials; On average treatment initiated at 60 letters baseline, normal vision at about 90 letters 3) CATT trial, Pharmacies; Assuming price discount of 30-40% vs. reference product; Based on real world data from Swedish Macular Registry. Exchange rate EUR/SEK=10.4638 as of June 30 2018.

Avastin®Lucentis®

Lucentis® & Eylea® Only Approved VEGFa Inhibitors For Ophtalmic Use

Treatment

Efficacy(vision improvement after

12 months)

Safety

Average

Cost(Per patient

per year)

US

EU

• 7 – 11 letters (on average 1/3 of vision recovered)1

• Generally well tolerated 1

• Designed to treat macular degenerations

• 7 – 11 letters 1• Non-inferiority to Lucentis

demonstrated 2

• Similar safety profile as Lucentis demonstrated2

• Anti-body used to treat different

types of cancers (off-label)

• Non-inferiority to Lucentis demonstrated 3

• Various safety issues

EUR 9 600

EUR 4 200

EUR 9 760

EUR 4 453

EUR 900

EUR 1 020

Off-label

usage

• Designed to treat macular degenerations

Eylea®

23

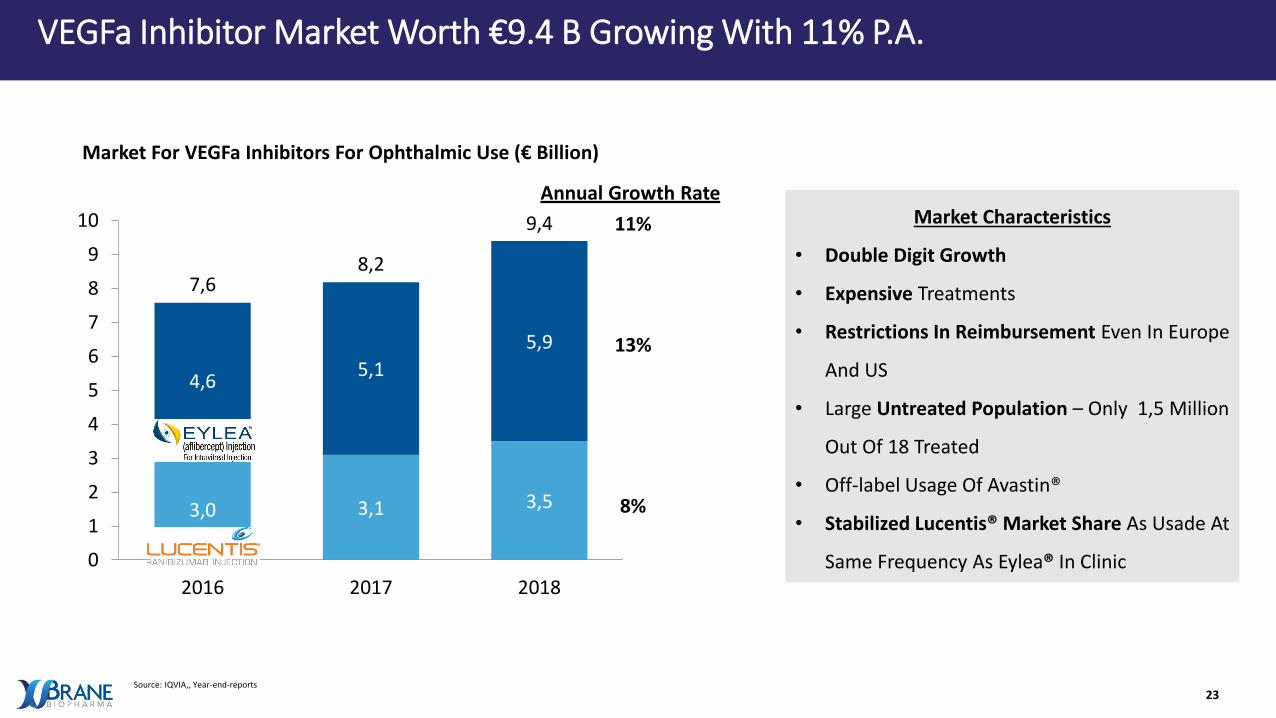

VEGFa Inhibitor Market Worth €9.4 B Growing With 11% P.A.

3,0 3,1 3,5

4,65,1

5,9

7,68,2

9,4

0

1

2

3

4

5

6

7

8

9

10

2016 2017 2018

Market For VEGFa Inhibitors For Ophthalmic Use (€ Billion)

Annual Growth Rate

13%

8%

11% Market Characteristics

• Double Digit Growth

• Expensive Treatments

• Restrictions In Reimbursement Even In Europe

And US

• Large Untreated Population – Only 1,5 Million

Out Of 18 Treated

• Off-label Usage Of Avastin®

• Stabilized Lucentis® Market Share As Usade At

Same Frequency As Eylea® In Clinic

Source: IQVIA,, Year-end-reports

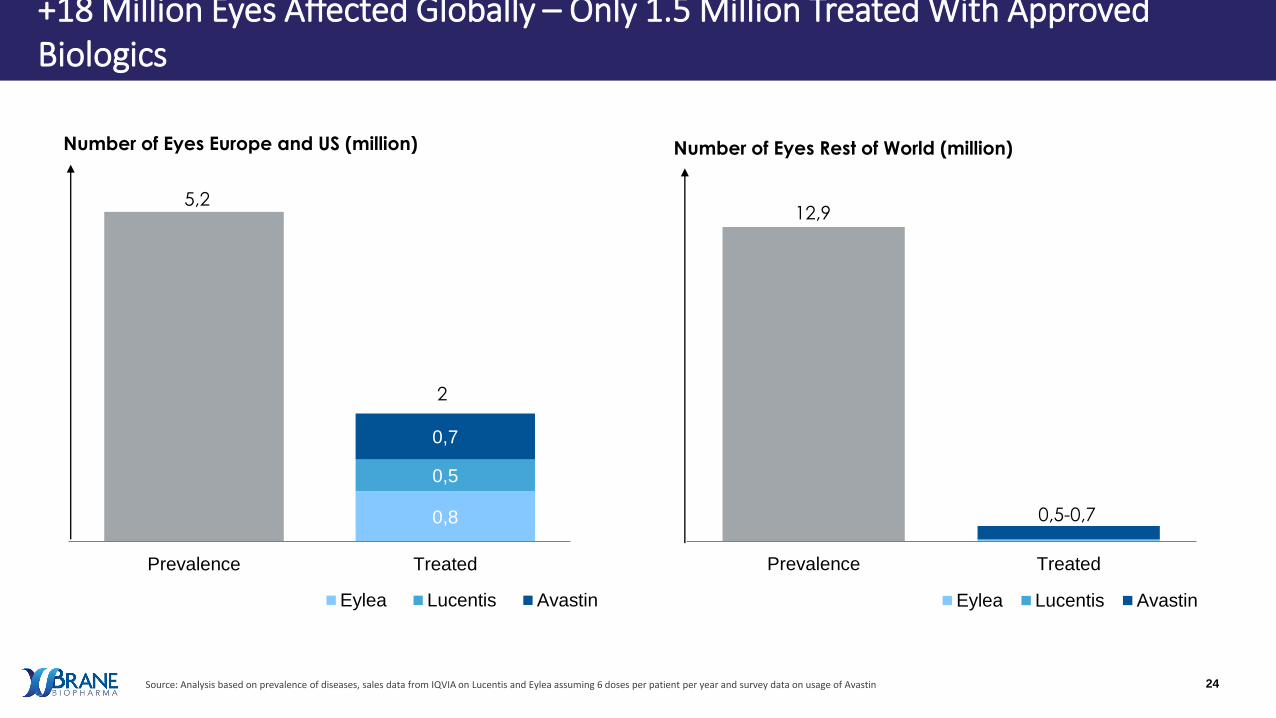

24Source: Analysis based on prevalence of diseases, sales data from IQVIA on Lucentis and Eylea assuming 6 doses per patient per year and survey data on usage of Avastin

0,8

0,5

0,7

Prevalence Treated

Eylea Lucentis Avastin

Number of Eyes Europe and US (million)

5,2

2

Prevalence Treated

Eylea Lucentis Avastin

12,9

0,5-0,7

+18 Million Eyes Affected Globally – Only 1.5 Million Treated With Approved Biologics

Number of Eyes Rest of World (million)

25

Table of Contents

1. Xbrane Biopharma Overview

2. The Biosimilar Market

3. The VGEF Market & The Unmet Medical Need

4. Lead Product Xlucane

5. Summary & Investment Highlights

Presenters

Martin ÅmarkCEO

Anders TullgrenChairman of the

Board

26

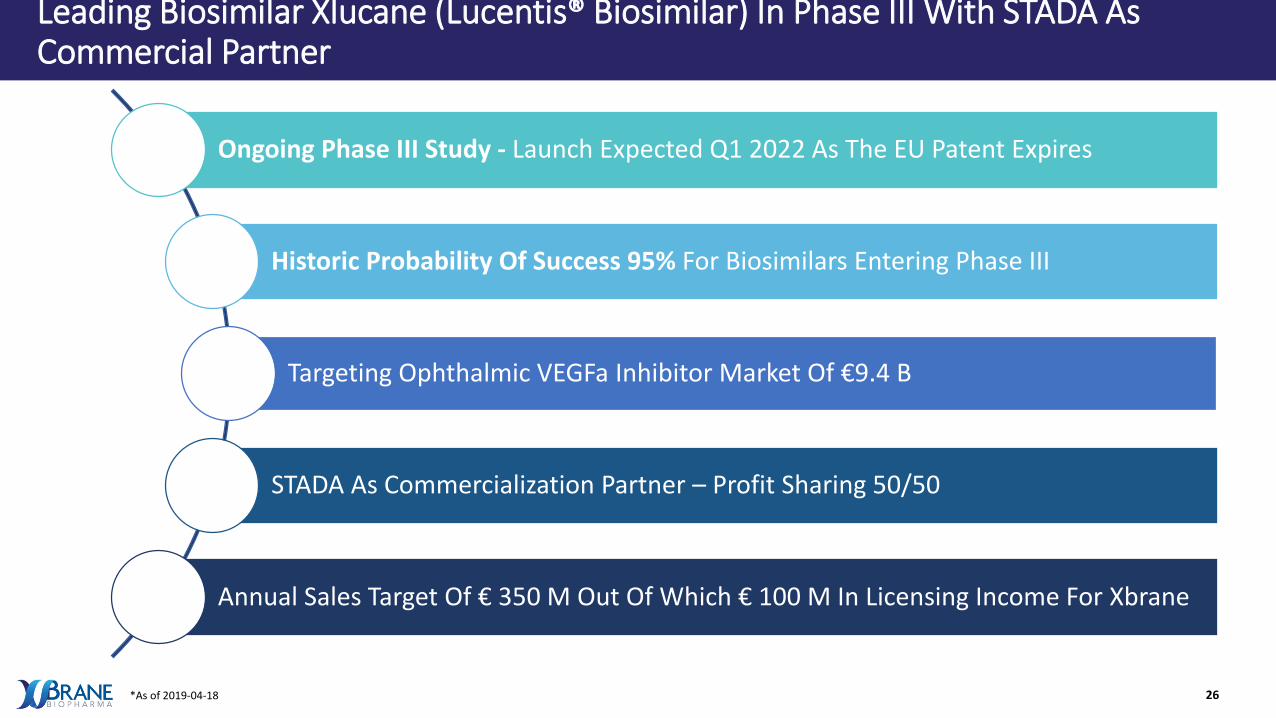

Leading Biosimilar Xlucane (Lucentis® Biosimilar) In Phase III With STADA As Commercial Partner

Ongoing Phase III Study - Launch Expected Q1 2022 As The EU Patent Expires

Historic Probability Of Success 95% For Biosimilars Entering Phase III

Targeting Ophthalmic VEGFa Inhibitor Market Of €9.4 B

STADA As Commercialization Partner – Profit Sharing 50/50

Annual Sales Target Of € 350 M Out Of Which € 100 M In Licensing Income For Xbrane

*As of 2019-04-18

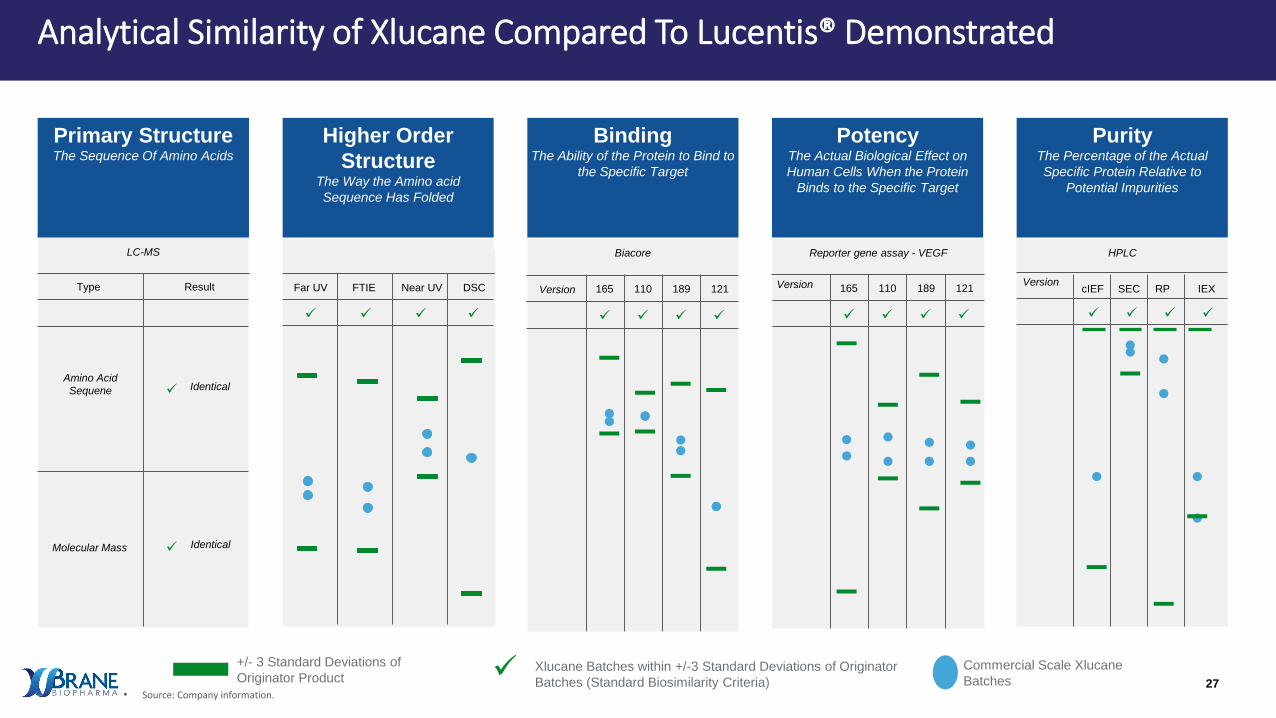

27• Source: Company information.

+/- 3 Standard Deviations of

Originator ProductCommercial Scale Xlucane

BatchesXlucane Batches within +/-3 Standard Deviations of Originator

Batches (Standard Biosimilarity Criteria) ✓

LC-MS

Amino Acid

Sequene

Molecular Mass

Identical

Identical✓

✓

Type Result

Reporter gene assay - VEGF

✓ ✓ ✓ ✓

165 110 189 121Version

Biacore

✓ ✓ ✓ ✓

165 110 189 121Version

HPLC

Version

✓ ✓ ✓ ✓

cIEF SEC RP IEX

✓ ✓ ✓ ✓

Far UV FTIE Near UV DSC

BindingThe Ability of the Protein to Bind to

the Specific Target

PotencyThe Actual Biological Effect on

Human Cells When the Protein

Binds to the Specific Target

Higher Order

StructureThe Way the Amino acid

Sequence Has Folded

PurityThe Percentage of the Actual

Specific Protein Relative to

Potential Impurities

Primary StructureThe Sequence Of Amino Acids

Analytical Similarity of Xlucane Compared To Lucentis® Demonstrated

28

• Two Groups with 8 Rabbits (16 Eyes) In Each Group Recieving Intravitral Injection of Xlucane and Lucentis Respectively

• Serum Concentration of Ranibizumab Analyzed at Hour 4, 8 And 48

• Eye Inflammations Observed Throughout the Duration of The Study

Tolerability1 Pharmacokinetic Profile

Candidate Minimal Mild Moderate Total

Xlucane 1/4 0/4 0/4 1/4

Lucentis 1/4 1/4 1/4 3/4

1

10

100

0 8 16 24 32 40 48

Mea

n (

ng

/mL)

Time (hr)

1 mg/total Lucentis 1 mg/total Xlucane

Study Design

Note: 1) Measured via microscopic evaluation on ocular tissues from animals euthanized on Day 28. Eye inflammation defined as mononuclear cell infiltration in the vitreous body, ciliary body, anterior chamber, optic disc, conjunctiva, retina and/or choroid. Source: A Pharmacokinetics Study of Two Formulations of Ranibizumab following a Single Bilateral Intravitreal Injection in the New Zealand White Rabbit (Study No. 5701026), performed by Charles River Montreal under GLP conditions with Xbrane Biopharma as sponsor.

Equivalent Tolerability and PK Profile of Xlucane Compared To Lucentis® Demonstrated In-Vivo

29

StartRecruitment 9 months Treatment 12 months

Xlucane290 patients

Lucentis®

290 patients

Primary end-point

Change in Visual acuity

(“BCVA”) after 8 weeks

Secondary end-points

after 12 months e.g.

Immunogenicity, BCVA,

Retina thickness

• Multi-regional clinical trial with 150 sites across 16 countries (including EU, US, India)

• Enable Marketing Authorization across key markets globally

• Partnership with highly qualified global CRO

• Clinical trial approval across most countries

• First patient in April 2019 in US

o

Global phase III trial ongoing – all patients to be recruited during 2019

30

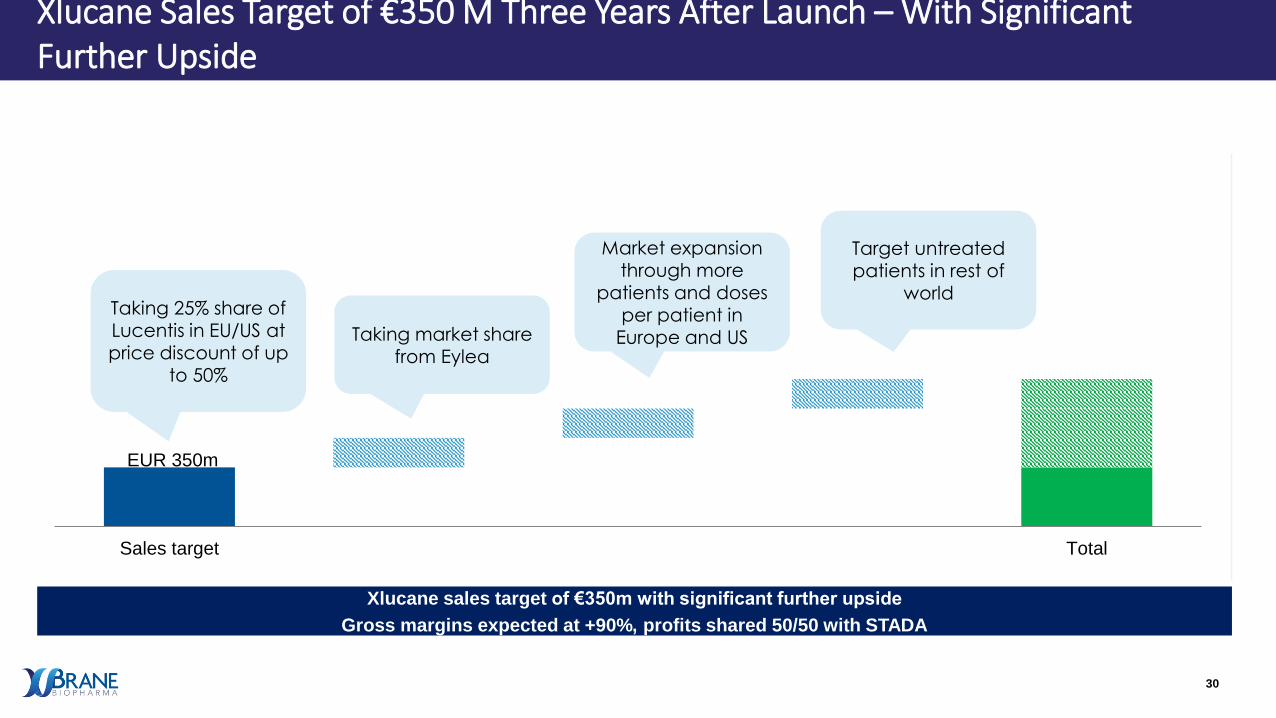

EUR 350m

Sales target Total

Xlucane sales target of €350m with significant further upside

Gross margins expected at +90%, profits shared 50/50 with STADA

Taking 25% share ofLucentis in EU/US at price discount of up

to 50%

Taking market share from Eylea

Market expansion through more

patients and doses per patient in

Europe and US

Target untreated patients in rest of

world

Xlucane Sales Target of €350 M Three Years After Launch – With SignificantFurther Upside

31

Xlucane sales

target:

Patients: 120,000*

Doses: 700,000

Sales: € 350 million*

90

55

14

Lucentis

Eylea

Xlucane target*410

190

48

75

90

23

20

25

6

10

25

6

55

50

13

Estimated number of

patients 2018

(thousands)

Xlucane €350 M Sales Target Reached With 120K Patients And 700K Doses

*Target reaching 25% volume market share of current Lucentis® market in each country at 50% price discount to originator

90

45

11

Rest of

Europe

32

European Supply-chain With Capacity For Xlucane Sales Target & Further Upside

• Drug substance manufacturer

• Manufacturing Authorization License issued

by EU EMA (expecting for FDA)

• cGMP compliant analytical development and

testing

• LOI for Xlucane supply capacity signed

• Drug product manufacturer

• Manufacturing Authorization License issued by

Swiss authorities (mutual recognition by EU).

• LOI for Xlucane supply capacity signed

33

Table of Contents

1. Xbrane Biopharma Overview

2. The Biosimilar Market

3. The VGEF Market & The Unmet Medical Need

4. Lead Product Xlucane

5. Summary & Investment Highlights

Presenters

Martin ÅmarkCEO

Anders Tullgren

Chairman of the Board

34

Significant Value Drivers Ahead

Development Timeline

100% Recruited

Phase III/Xplore

Top Line Clinical Data

Approval

Phase III/Xplore

Sales Launch

(Patent Loss)

20222020 2021H1 H22019

First Patient Recruited

Phase III/Xplore

Pre-clinical portfolio:

Xcimzane (Cimzia®)

Xdivane (Opdivo®)

Xoncane (Oncaspar®)

Spherotide (Decapeptyl®)

Partnerships and advancement of development on pre-clinical products

XlucaneOther

Candidates

Pre-Marketing

2023

25/50/75% RecruitedPhase III/Xplore

MAA/BLA Submission

35

Xbrane - Biosimilar Developer With Patented High Yield Technology

Lead Product Xlucane In Phase III With Commercial Partner STADA. Annual Sales Target Of €350 M Out Of Which €100 M In Income For Xbrane

Addressing Attractive Biosimilar Market Opportunity. The Fastest Growing Segment Within Pharma Combined With Low Technical Risk

Patented Innovative High-yield Technology Platform Resulting In Low Production Costs

Strong Product Pipeline Targeting +€ 11 B In Originator Sales. Only Public Biosimilar Developments To Opdivo® And Cimzia®

Listed At Nasdaq First North With €35 M* Market Cap – Up-listing To Main Market During 2019

*As of 2019-04-18

36

Xbrane Biopharma

Banvaktsvägen 22

17148 Solna, Sweden

Thank You

37

No Late Stage Product With Superior Efficacy Nor Safety To Lucentis Or Eylea. Preclinical Pipeline Dry.

Wet-AMD Development Pipeline and Marketed Assets

Marketed

Phase I/II

Legend

Injection Ophthalmic/Drops

Mechanisms/Targets

Route of Administration

SF0166 - SciFluor

Complement factor C3

inhibitor

*Used off-label

Phase III

Lucentis (ranibizumab) -

Novartis

Eylea (aflibercept) -

Regeneron/Bayer/Sanofi

Brolucizumab - Novartis

KH 902 (Conbercept) - Chengdu

Kanghong,

Marketed in China only

Avastin* (bevacizumab) -

Genentech

VEGF-A

Abicipar (Abicipar pegol) -

Allergan/Molecular Partners AG

ranibizumab (Lucentis) biosimilar

- Formycon/Bioeq

VEGFR-2 inhibitor

PAN 90806 - PanOptica

OPT-302 – Opthea

Faricimab – Roche

Zimura (avacincaptad pegol) –

Ophthotech Corporation

Complement factor C5 inhibitor

DE-122 (carotuximab) – Tracon

Pharmaceuticals/Santen

Anti-endoglin MAbChemokine CCL11

inhibitors

PO/Tablet

ALK 4290 – Alkahest

Phase II

ICON-1 - Iconic Therapeutics

Anti-tissue factor MAb factor VII

conjugate

ranibizumab (Lucentis) biosimilar

- Samsung Bioepis Co., Ltd.

Integrin alpha 5 beta 3 inhibitor

Topical Solution

Biosimilar

APL-2 - Apellis

VEGF-C/VEGF-D

GB-102 (sunitinib) - Greybug

Vision

Molecule receptor

tyrosine kinase inhibitor

aflibercept (Eylea) biosimilar –

Mylan/Momenta

Pharmaceuticals

Implant

ranibizumab PDS– Genentech

XLUCANE ranibizumab

(Lucentis) biosimilar – Xbrane

Conbercept – Chengdu KH

Source: Xbrane research

38

Phase III

MAA/BLA

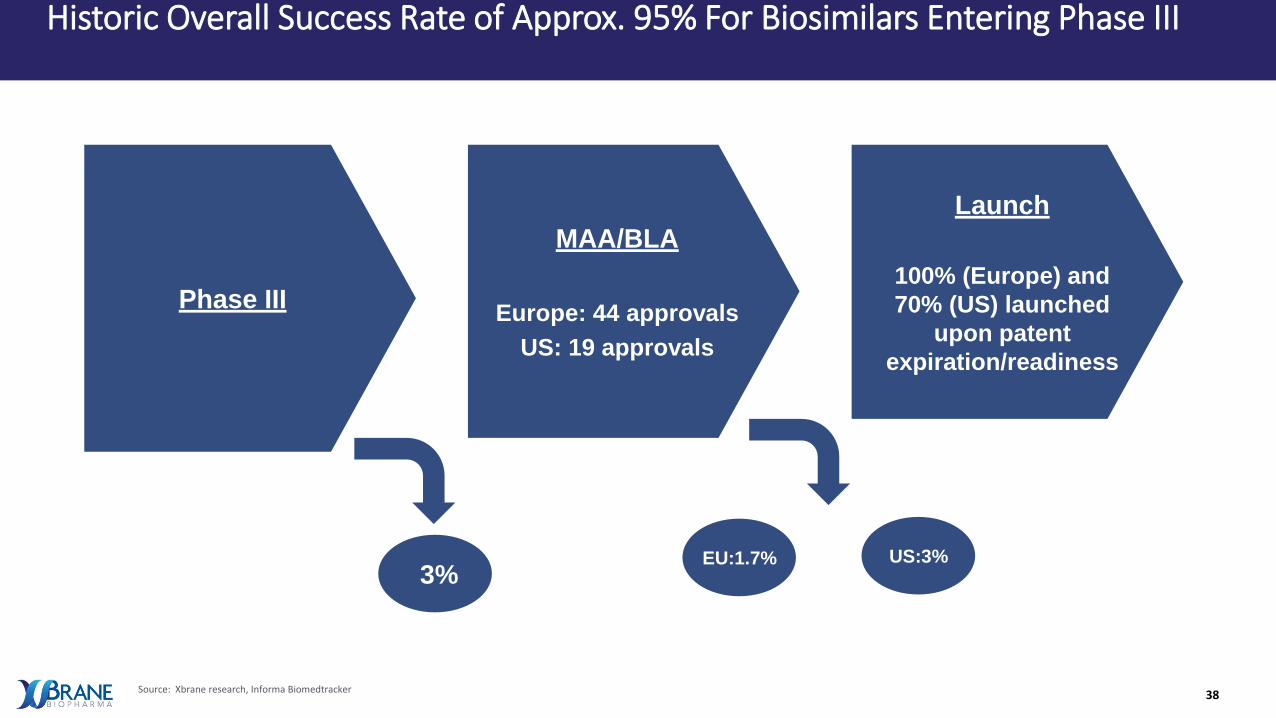

Europe: 44 approvals

US: 19 approvals

Launch

100% (Europe) and

70% (US) launched

upon patent

expiration/readiness

3%EU:1.7% US:3%

Historic Overall Success Rate of Approx. 95% For Biosimilars Entering Phase III

Source: Xbrane research, Informa Biomedtracker

39

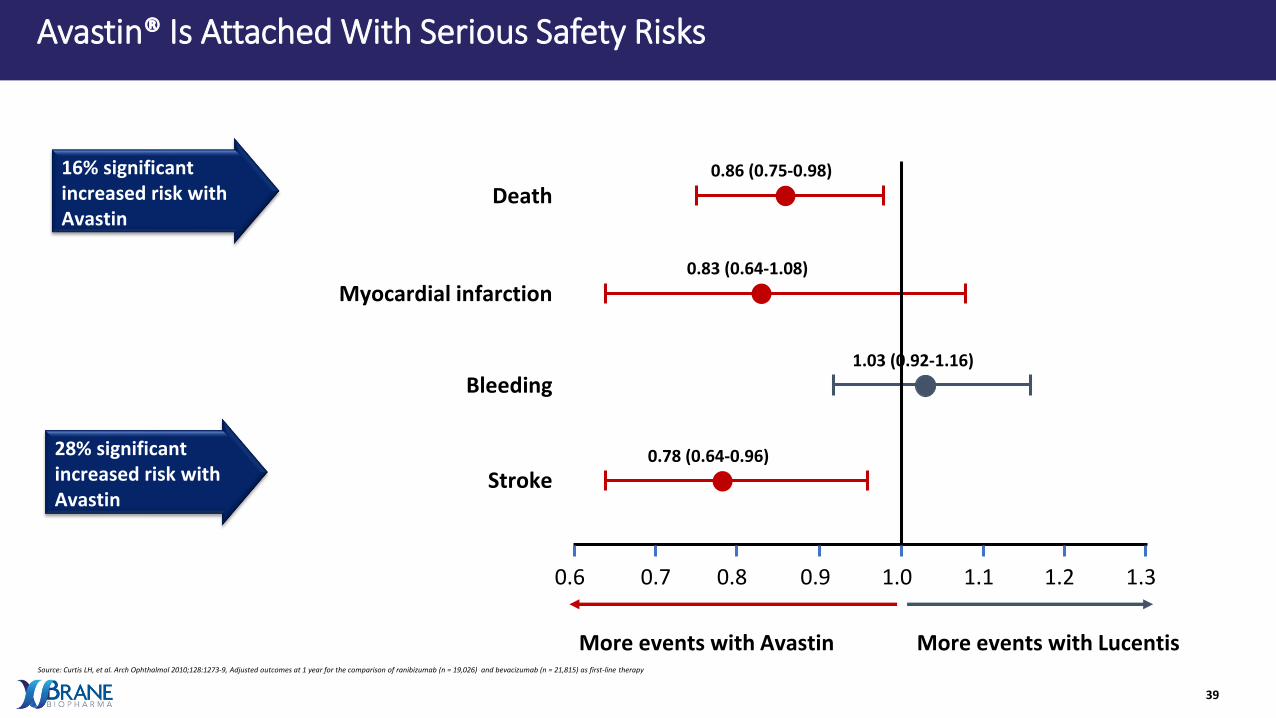

Source: Curtis LH, et al. Arch Ophthalmol 2010;128:1273-9, Adjusted outcomes at 1 year for the comparison of ranibizumab (n = 19,026) and bevacizumab (n = 21,815) as first-line therapy

Avastin® Is Attached With Serious Safety Risks

28% significant increased risk with Avastin

16% significant increased risk with Avastin

0.6 0.7 0.8 0.9 1.0 1.1 1.2 1.3

Stroke

Bleeding

Death

More events with LucentisMore events with Avastin

0.78 (0.64-0.96)

1.03 (0.92-1.16)

0.83 (0.64-1.08)

0.86 (0.75-0.98)

Myocardial infarction

40

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

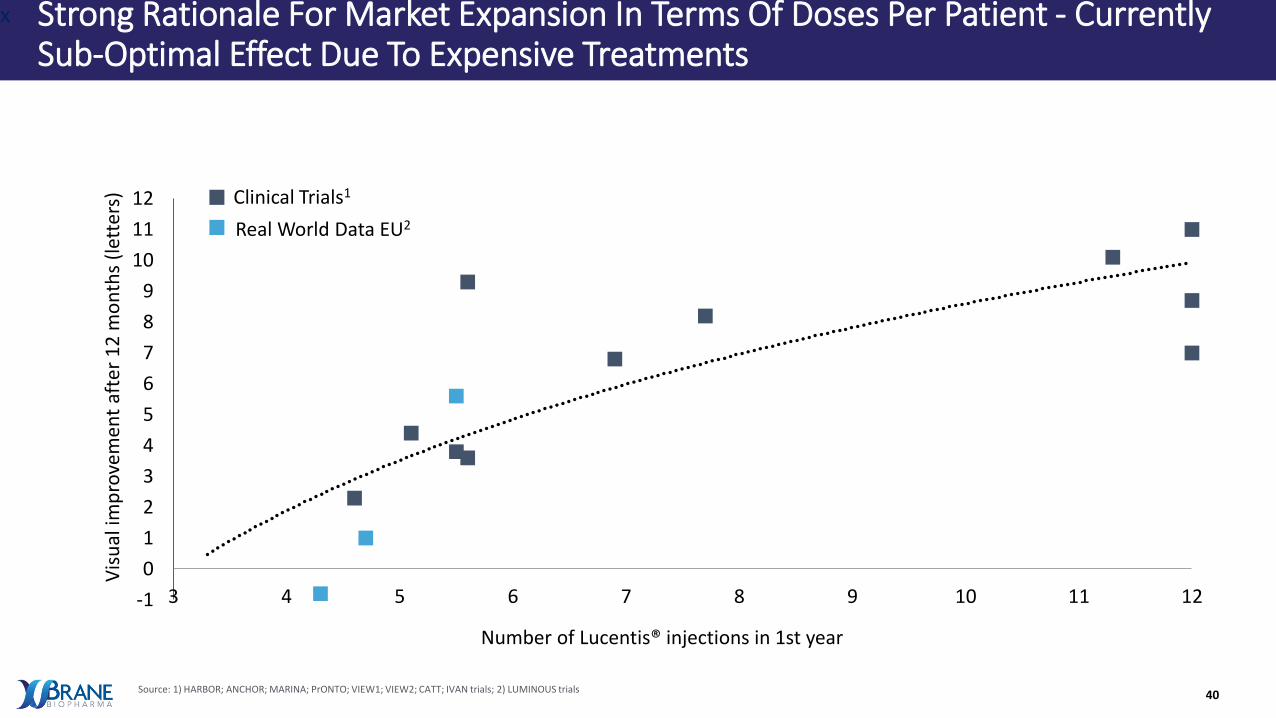

3 4 5 6 7 8 9 10 11 12

Vis

ual

imp

rove

men

t af

ter

12

mo

nth

s (l

ette

rs)

Number of Lucentis® injections in 1st year

Strong Rationale For Market Expansion In Terms Of Doses Per Patient - Currently Sub-Optimal Effect Due To Expensive Treatments

x

Real World Data EU2

Clinical Trials1

Source: 1) HARBOR; ANCHOR; MARINA; PrONTO; VIEW1; VIEW2; CATT; IVAN trials; 2) LUMINOUS trials

41

Source: IQVIA Midas

1,24 1,29 1,59

1,14 1,16

1,25

0,62 0,60

0,64

0

1

2

3

4

2016 2017 2018

US Europe Others

Lucentis® (Ranibizumab) Global Sales (€ Billion)

0,3 0,3 0,4

0,3 0,3 0,3

0,2 0,20,2

0,1 0,10,10,1 0,10,10,2 0,2

0,2

0,0

0,5

1,0

1,5

2,0

2016 2017 2018

France Germany UK Spain Italy Others

Lucentis® (Ranibizumab) Europe Sales (€ Billion)

8% P.A.

5% P.A.

Lucentis (Ranibizumab) Generates Sales of €3.5 B Growing At 8% P.A.