World Energy Outlook 2011 WEO-2012 Colation... · © OECD/IEA 2011 World Energy Outlook 2011 Laura...

9

© OECD/IEA 2011 World Energy Outlook 2011 Laura Cozzi Deputy Head, Office of the Chief Economist Coalition for energy savings -Brussels, 26 April 2012

Transcript of World Energy Outlook 2011 WEO-2012 Colation... · © OECD/IEA 2011 World Energy Outlook 2011 Laura...

© OECD/IEA 2011

World Energy Outlook 2011

Laura Cozzi Deputy Head, Office of the Chief Economist

Coalition for energy savings -Brussels, 26 April 2012

© OECD/IEA 2011

The EU in the future global energy landscape

In a world full of uncertainty, one thing is sure: rising incomes & population will push energy needs higher

EU is already the largest importer of natural gas; a competitive, integrated market remains the best bet for gas security.

EU becomes the largest oil importer around 2015 (until overtaken by China in the 2020), a shift with clear geopolitical implications

Power sector investment will become increasingly capital intensive with the rising share of renewables

Great potential for energy efficiency, but are the right policies in place?

Steps in the right direction, but the door to 2oC is closing

© OECD/IEA 2011

0

50

100

150

200

250

300

350

400

450

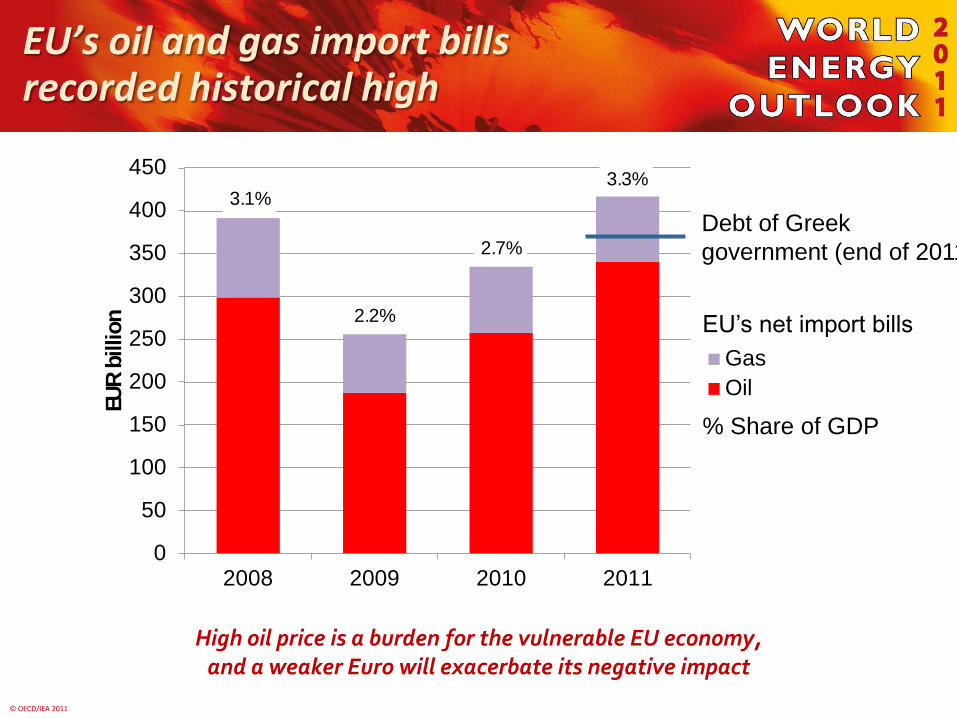

2008 2009 2010 2011

EUR

billion

Gas

Oil

3.1%

2.2%

2.7%

3.3%

EU’s oil and gas import bills recorded historical high

High oil price is a burden for the vulnerable EU economy, and a weaker Euro will exacerbate its negative impact

EU’s net import bills

% Share of GDP

Debt of Greek

government (end of 2011)

© OECD/IEA 2011

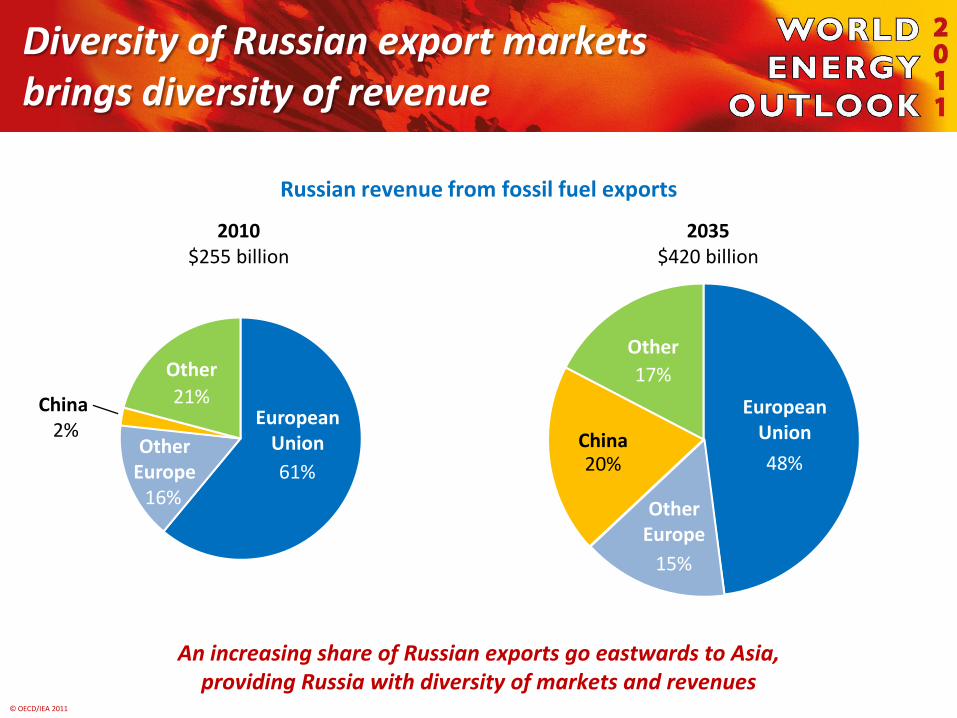

Diversity of Russian export markets brings diversity of revenue

Russian revenue from fossil fuel exports

An increasing share of Russian exports go eastwards to Asia, providing Russia with diversity of markets and revenues

2010 $255 billion

61% 16%

21%

2035 $420 billion

48%

European Union

17%

Other

20% China

15%

Other Europe

European Union Other

Europe

China 2%

Other

© OECD/IEA 2011

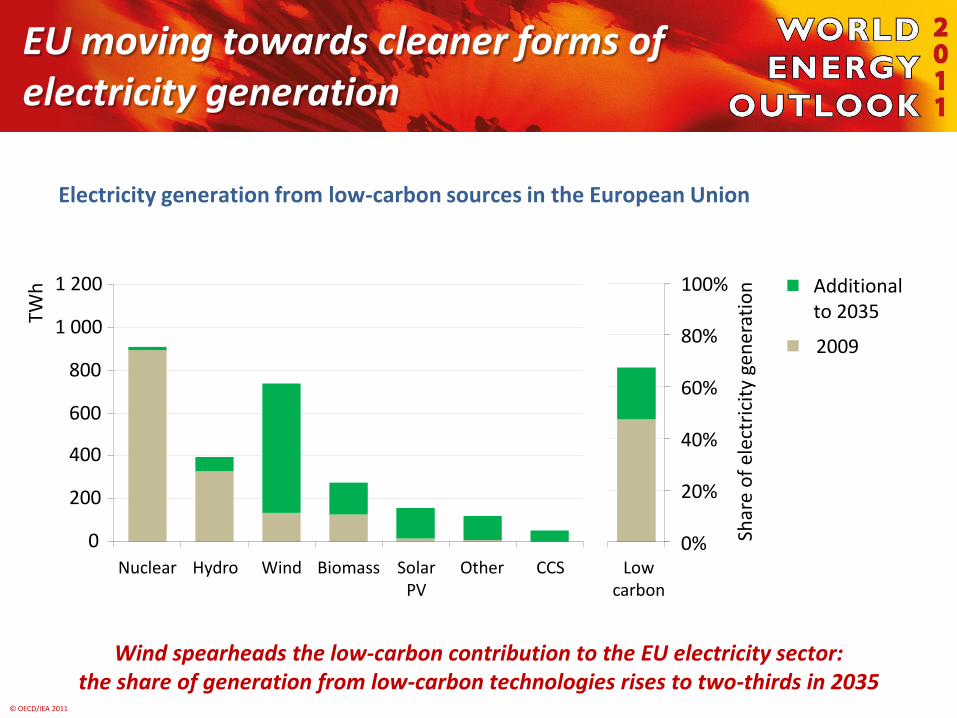

EU moving towards cleaner forms of electricity generation

Wind spearheads the low-carbon contribution to the EU electricity sector: the share of generation from low-carbon technologies rises to two-thirds in 2035

Electricity generation from low-carbon sources in the European Union

Additional to 2035

2009

0

200

400

600

800

1 000

1 200

Nuclear Hydro Wind Biomass Solar PV

Other CCS

TWh

0%

20%

40%

60%

80%

100%

Low carbon

Shar

e o

f el

ectr

icit

y ge

ner

atio

n

© OECD/IEA 2011

Efficiency gains can contribute most to EU emissions reductions

Energy efficiency measures – driven by strong policy action across all sectors – account for 50% of the cumulative CO2 abatement over the Outlook period

European Union energy-related CO2 emissions abatement in the 450 Scenario relative to the New Policies Scenario

Abatement

2020 2035

Efficiency 68% 48%

Renewables 25% 21%

Biofuels 2% 6%

Nuclear 1% 11%

CCS 3% 14%

Total (Mt CO2) 269 1032

1.5

2.0

2.5

3.0

3.5

4.0

2010 2015 2020 2025 2030 2035

Gt

New Policies Scenario

450 Scenario

© OECD/IEA 2011

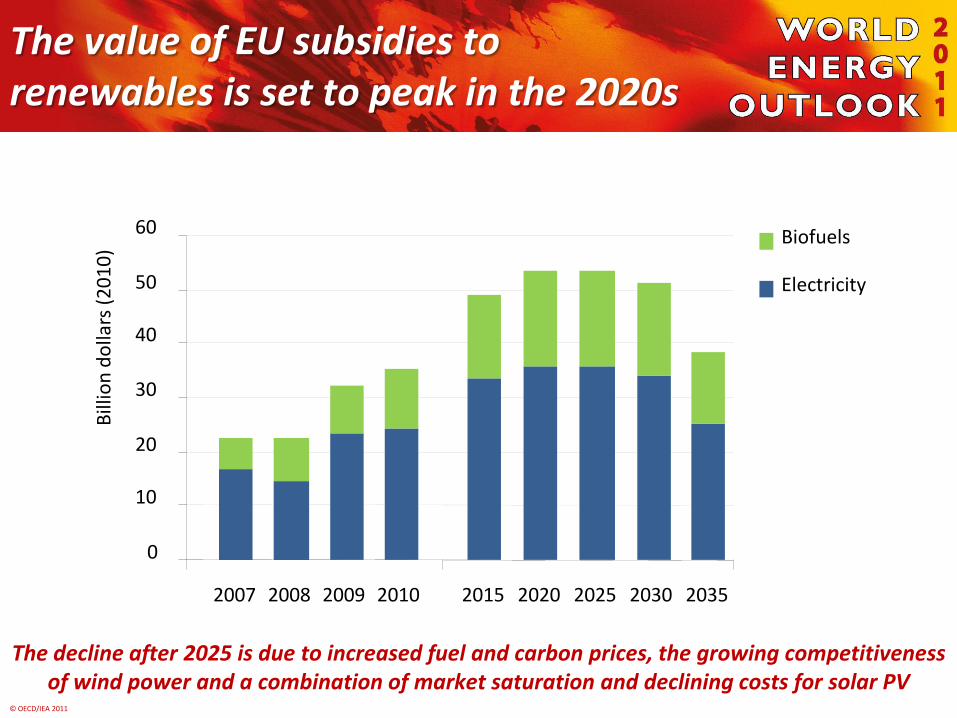

The value of EU subsidies to renewables is set to peak in the 2020s

The decline after 2025 is due to increased fuel and carbon prices, the growing competitiveness of wind power and a combination of market saturation and declining costs for solar PV

0

10

20

30

40

50

60

2007 2008 2009 2010 2015 2020 2025 2030 2035

Bill

ion

do

llars

(2

01

0)

Biofuels

Electricity

© OECD/IEA 2011

0

5

10

15

20

25

30

35

40

2010 2020 2025 2030 2035

Delay until 2017

Delay until 2015

2015

Emissions from existing infrastructure

The door to 2°C is closing, but will we be “locked-in” ?

Without further action, by 2017 all CO2 emissions permitted in the 450 Scenario will be “locked-in” by existing power plants, factories, buildings, etc

45

6°C trajectory

2°C trajectory

CO

2 e

mis

sio

ns

(gig

gato

nn

es)

© OECD/IEA 2011

Overview of WEO-2012

A full update of energy projections

by country, fuel & sector, to 2035

Objective & comprehensive analysis of topical issues

Fuel focus: energy efficiency – how to unlock the potential

climate impact on energy trends

energy-water nexus

indicators to track energy access

In addition, 2 special reports

29 May: the role of best practices (“Golden Rules”) for a Golden Age of Gas

9 October: first-ever in-depth outlook for Iraq (also included in full WEO)

Full WEO-2012 launch on 12 November