World Bean Outlook 2015

32

Transcript of World Bean Outlook 2015

Competitive Factors

Pulse income premium gone

Weak grains, strong oilseeds

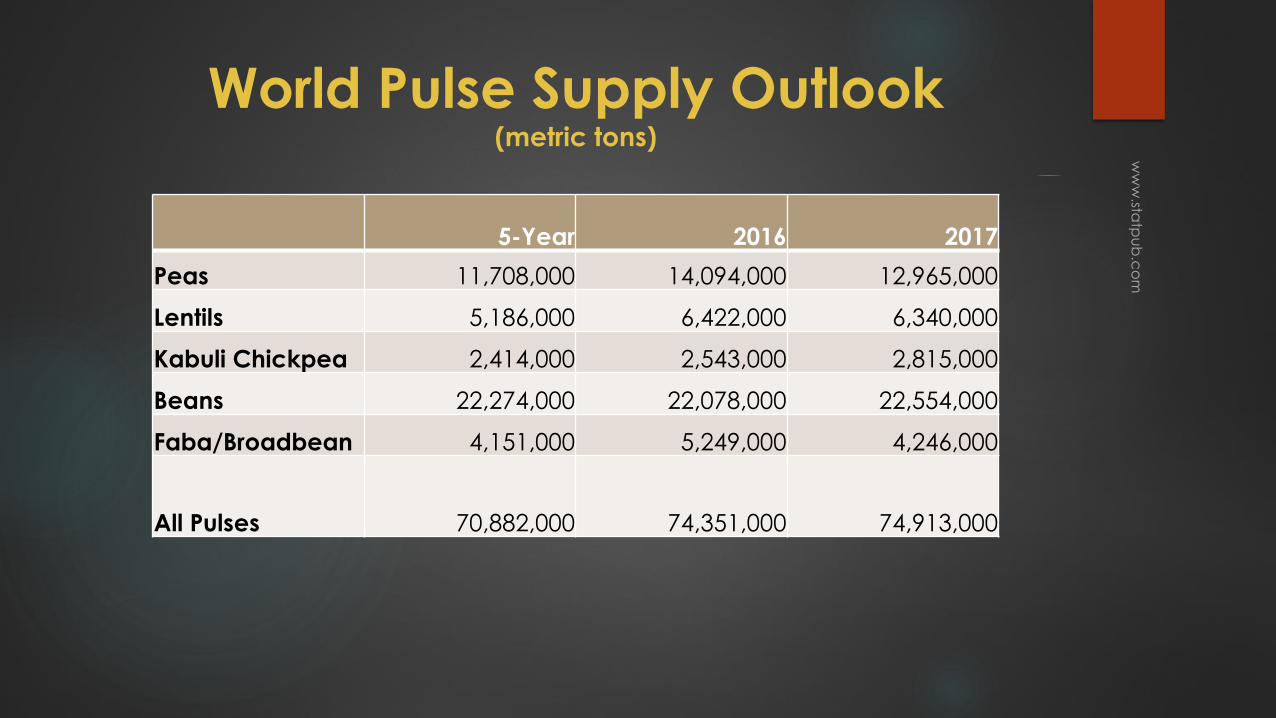

World Pulse Supply Outlook(metric tons)

5-Year 2016 2017

Peas 11,708,000 14,094,000 12,965,000

Lentils 5,186,000 6,422,000 6,340,000

Kabuli Chickpea 2,414,000 2,543,000 2,815,000

Beans 22,274,000 22,078,000 22,554,000

Faba/Broadbean 4,151,000 5,249,000 4,246,000

All Pulses 70,882,000 74,351,000 74,913,000

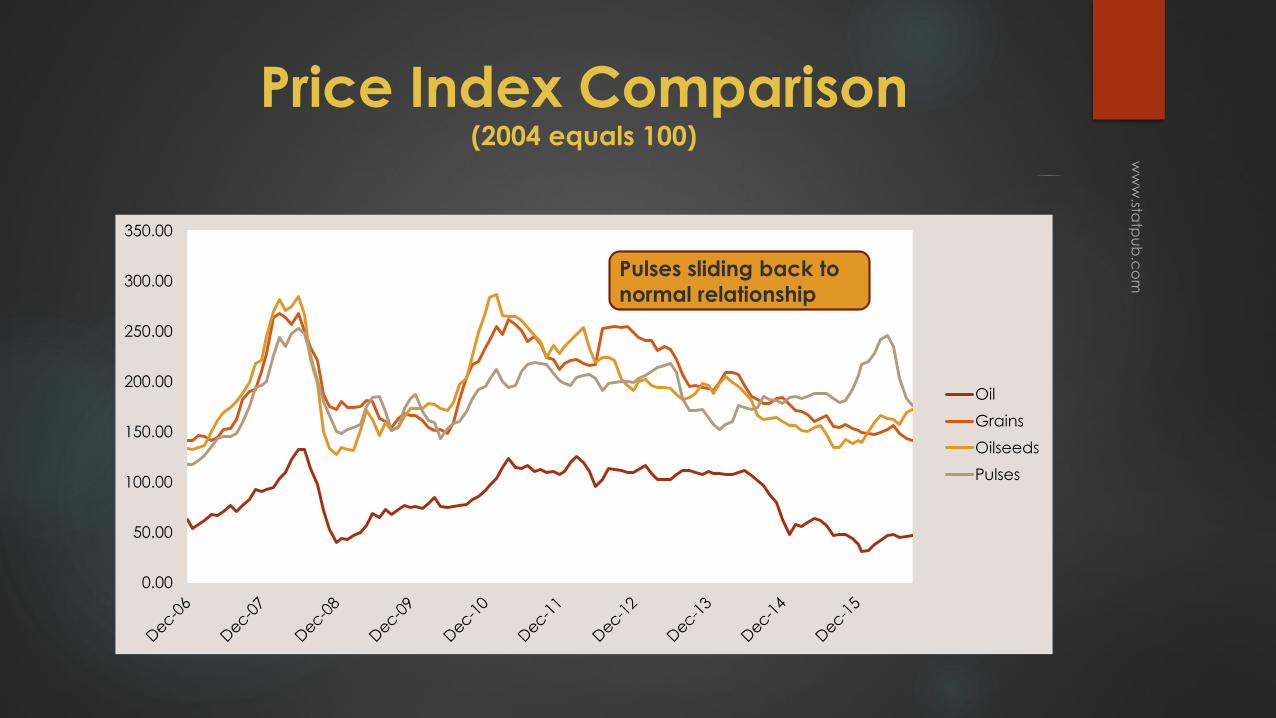

Price Index Comparison(2004 equals 100)

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

Oil

Grains

Oilseeds

Pulses

Pulses sliding back to

normal relationship

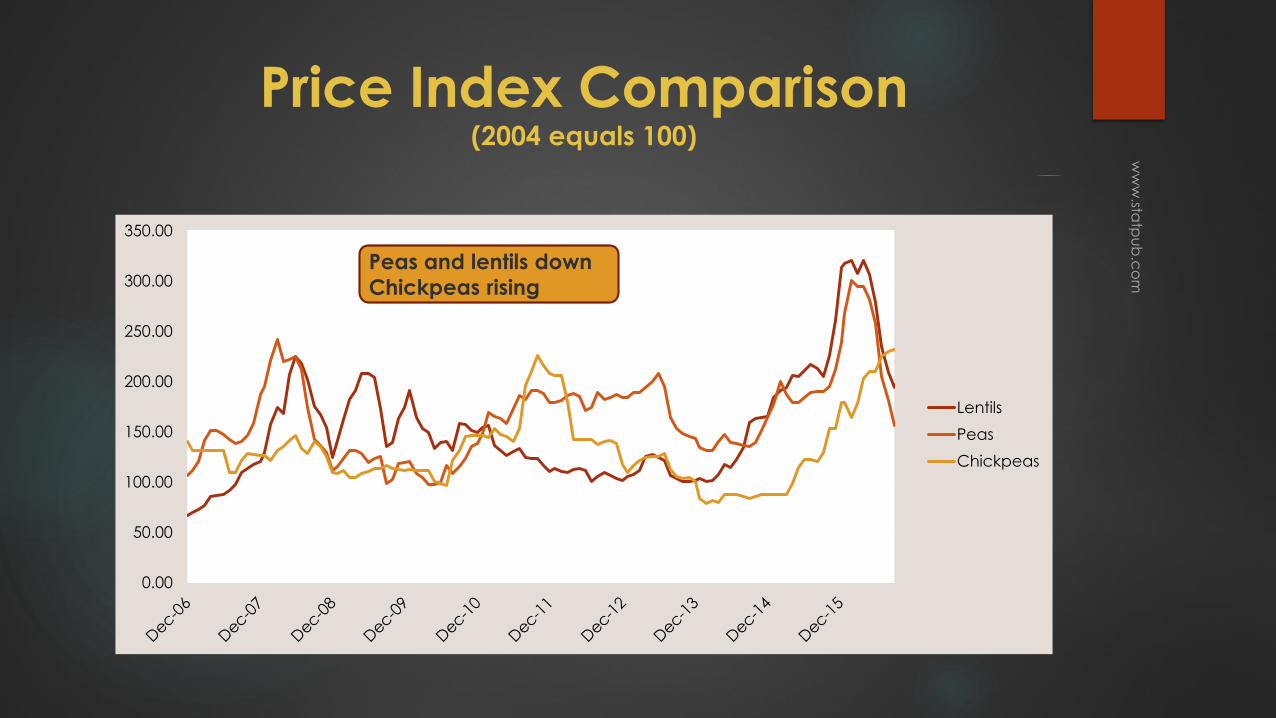

Price Index Comparison(2004 equals 100)

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

Lentils

Peas

Chickpeas

Peas and lentils down

Chickpeas rising

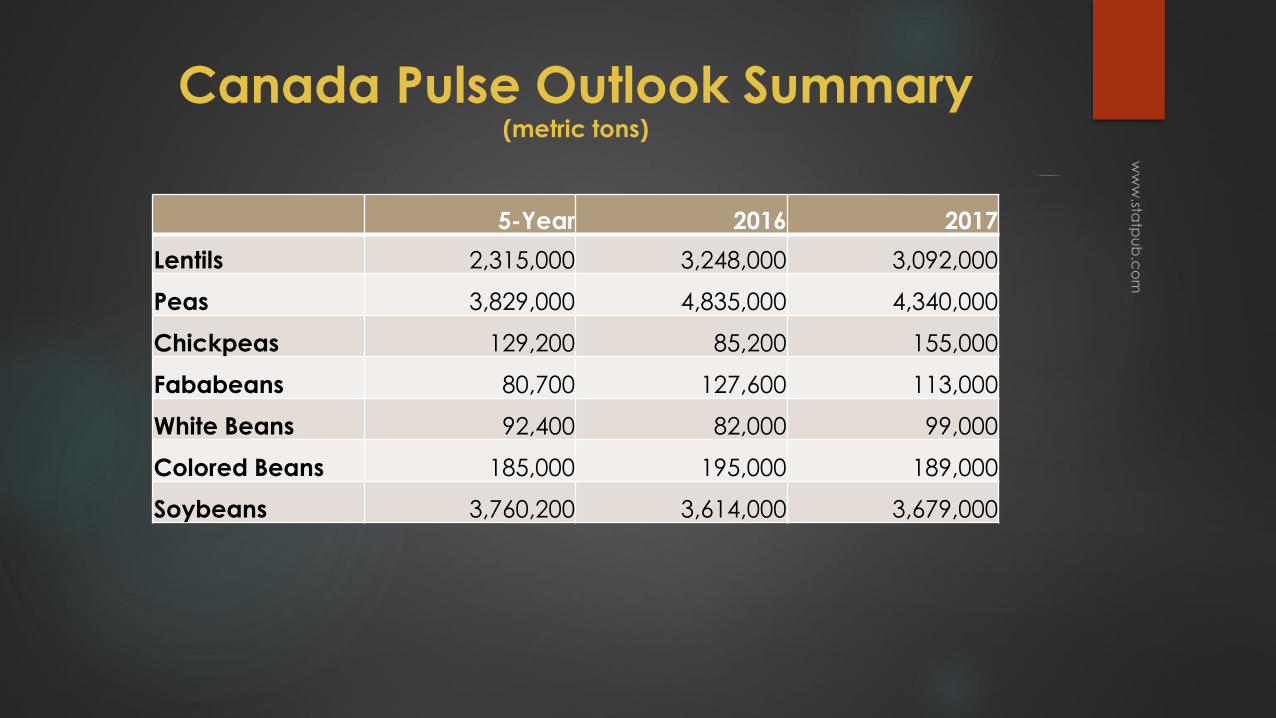

Canada Pulse Outlook Summary(metric tons)

5-Year 2016 2017

Lentils 2,315,000 3,248,000 3,092,000

Peas 3,829,000 4,835,000 4,340,000

Chickpeas 129,200 85,200 155,000

Fababeans 80,700 127,600 113,000

White Beans 92,400 82,000 99,000

Colored Beans 185,000 195,000 189,000

Soybeans 3,760,200 3,614,000 3,679,000

Red Lentils

Supply and demand pressures

Canadian area should fall

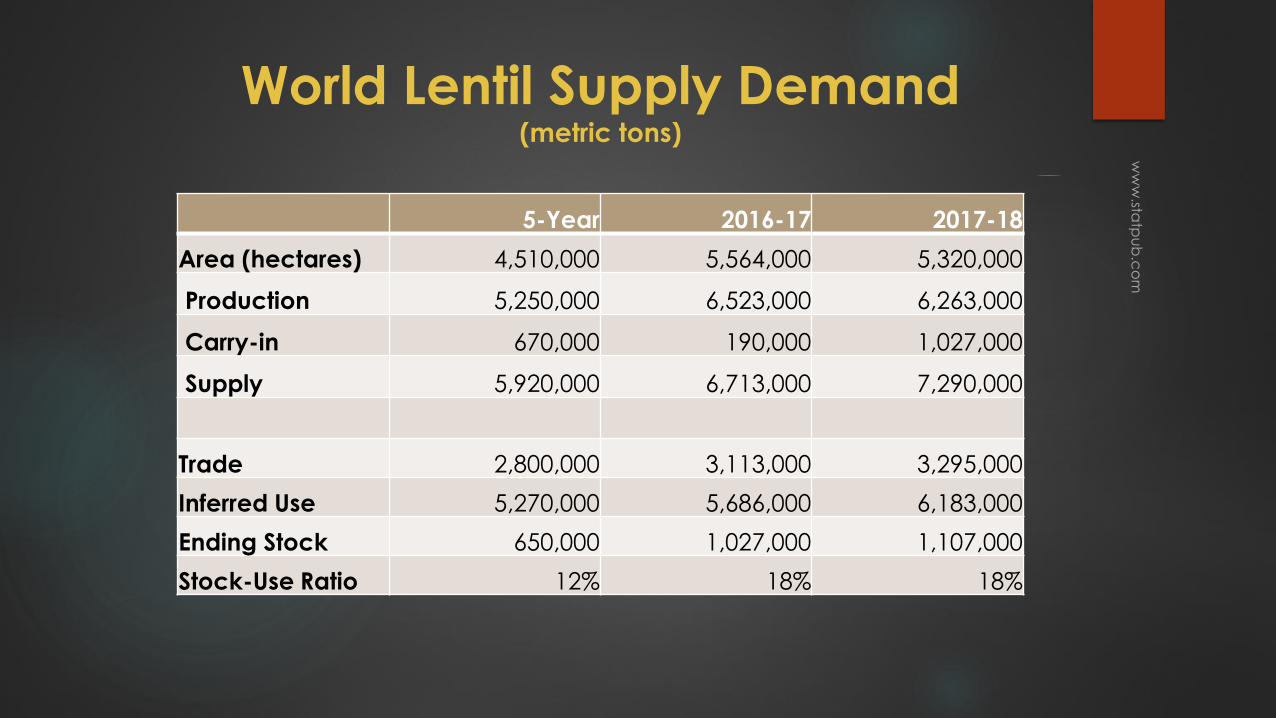

World Lentil Supply Demand(metric tons)

5-Year 2016-17 2017-18

Area (hectares) 4,510,000 5,564,000 5,320,000

Production 5,250,000 6,523,000 6,263,000

Carry-in 670,000 190,000 1,027,000

Supply 5,920,000 6,713,000 7,290,000

Trade 2,800,000 3,113,000 3,295,000

Inferred Use 5,270,000 5,686,000 6,183,000

Ending Stock 650,000 1,027,000 1,107,000

Stock-Use Ratio 12% 18% 18%

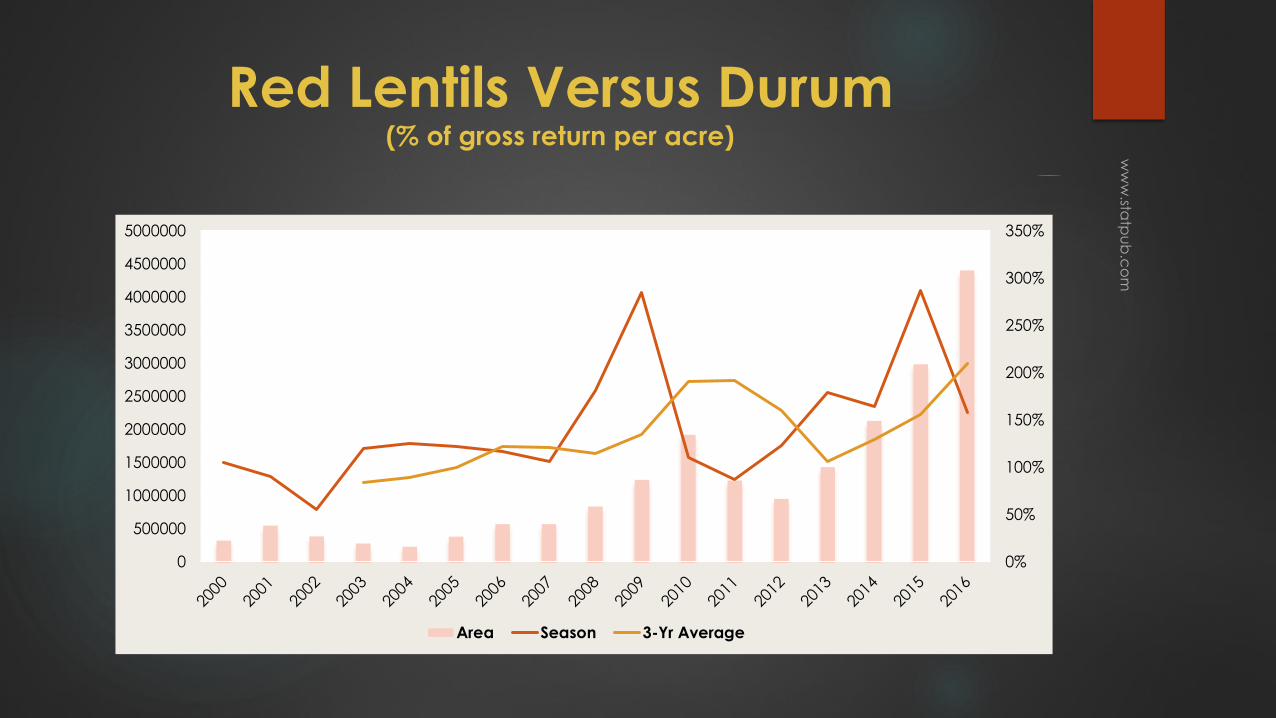

Red Lentils Versus Durum(% of gross return per acre)

0%

50%

100%

150%

200%

250%

300%

350%

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

5000000

Area Season 3-Yr Average

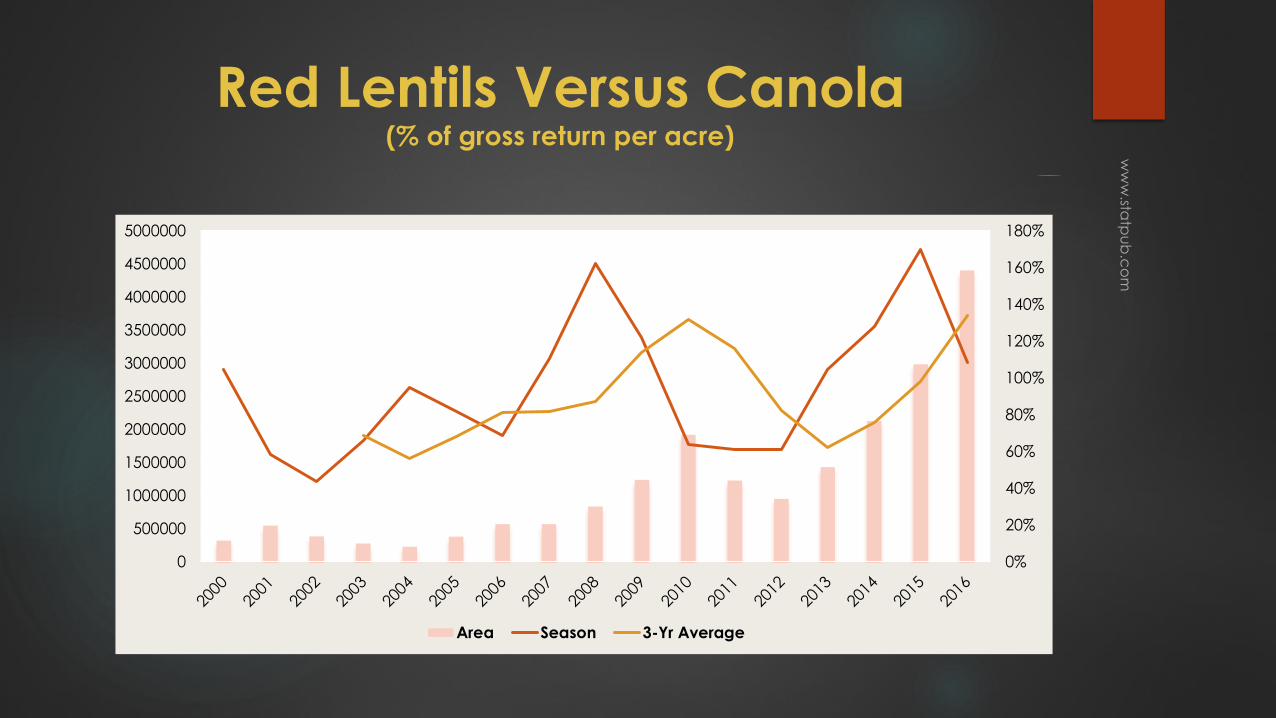

Red Lentils Versus Canola(% of gross return per acre)

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

5000000

Area Season 3-Yr Average

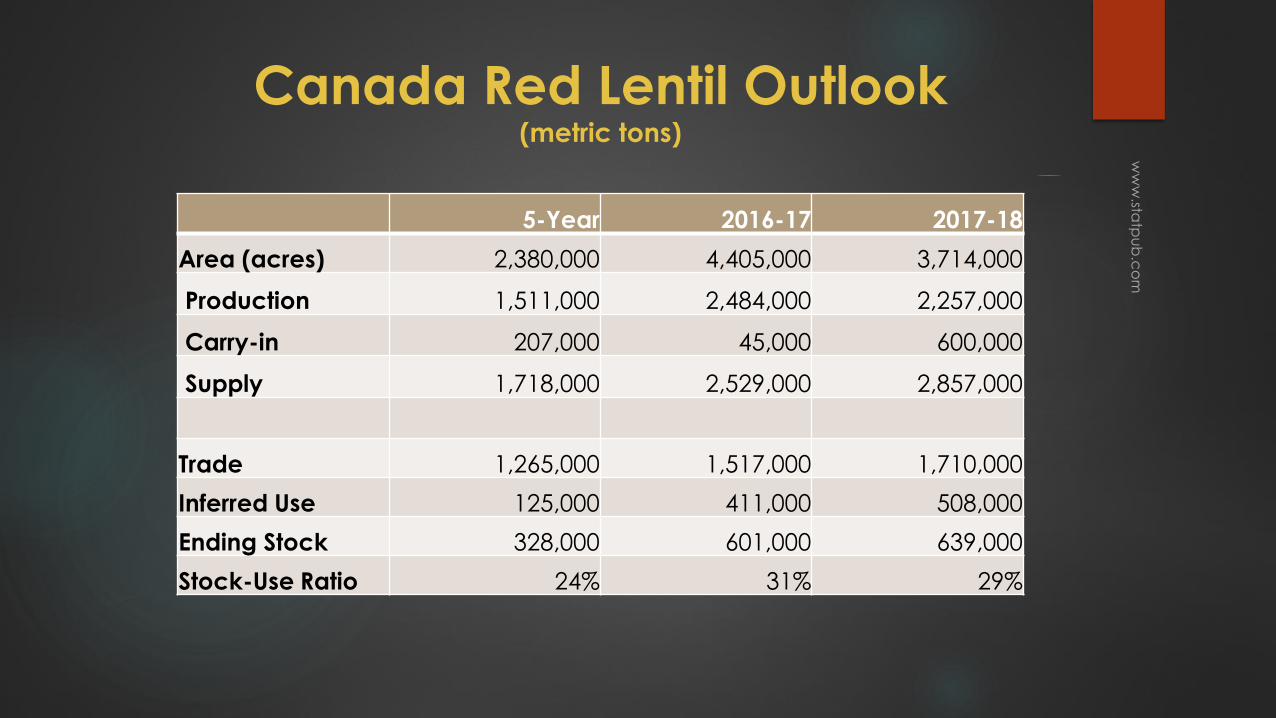

Canada Red Lentil Outlook(metric tons)

5-Year 2016-17 2017-18

Area (acres) 2,380,000 4,405,000 3,714,000

Production 1,511,000 2,484,000 2,257,000

Carry-in 207,000 45,000 600,000

Supply 1,718,000 2,529,000 2,857,000

Trade 1,265,000 1,517,000 1,710,000

Inferred Use 125,000 411,000 508,000

Ending Stock 328,000 601,000 639,000

Stock-Use Ratio 24% 31% 29%

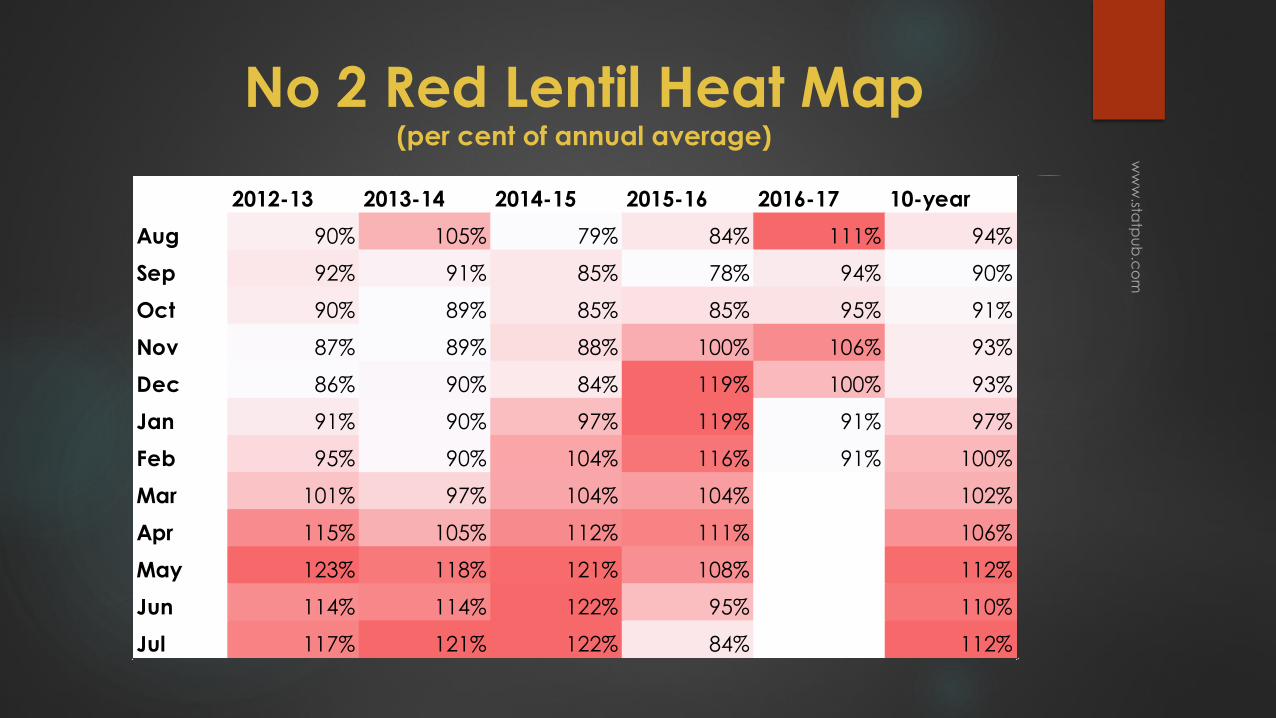

No 2 Red Lentil Heat Map (per cent of annual average)

2012-13 2013-14 2014-15 2015-16 2016-17 10-year

Aug 90% 105% 79% 84% 111% 94%

Sep 92% 91% 85% 78% 94% 90%

Oct 90% 89% 85% 85% 95% 91%

Nov 87% 89% 88% 100% 106% 93%

Dec 86% 90% 84% 119% 100% 93%

Jan 91% 90% 97% 119% 91% 97%

Feb 95% 90% 104% 116% 91% 100%

Mar 101% 97% 104% 104% 102%

Apr 115% 105% 112% 111% 106%

May 123% 118% 121% 108% 112%

Jun 114% 114% 122% 95% 110%

Jul 117% 121% 122% 84% 112%

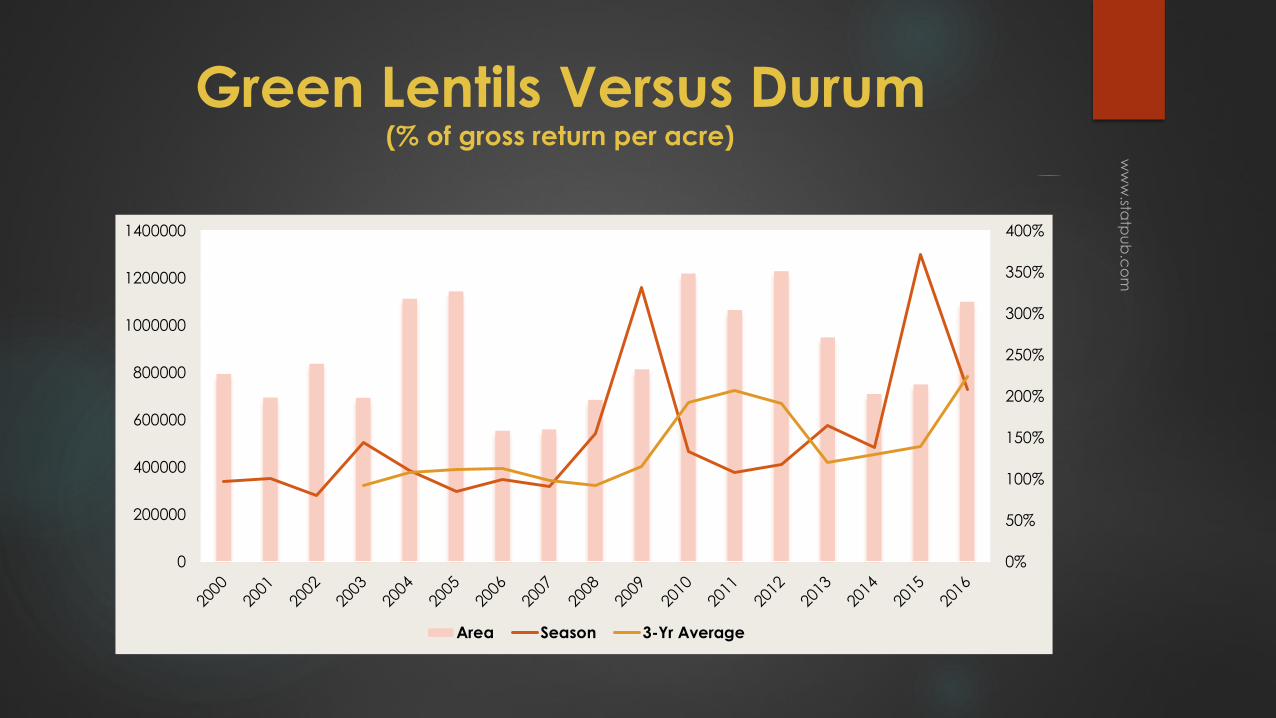

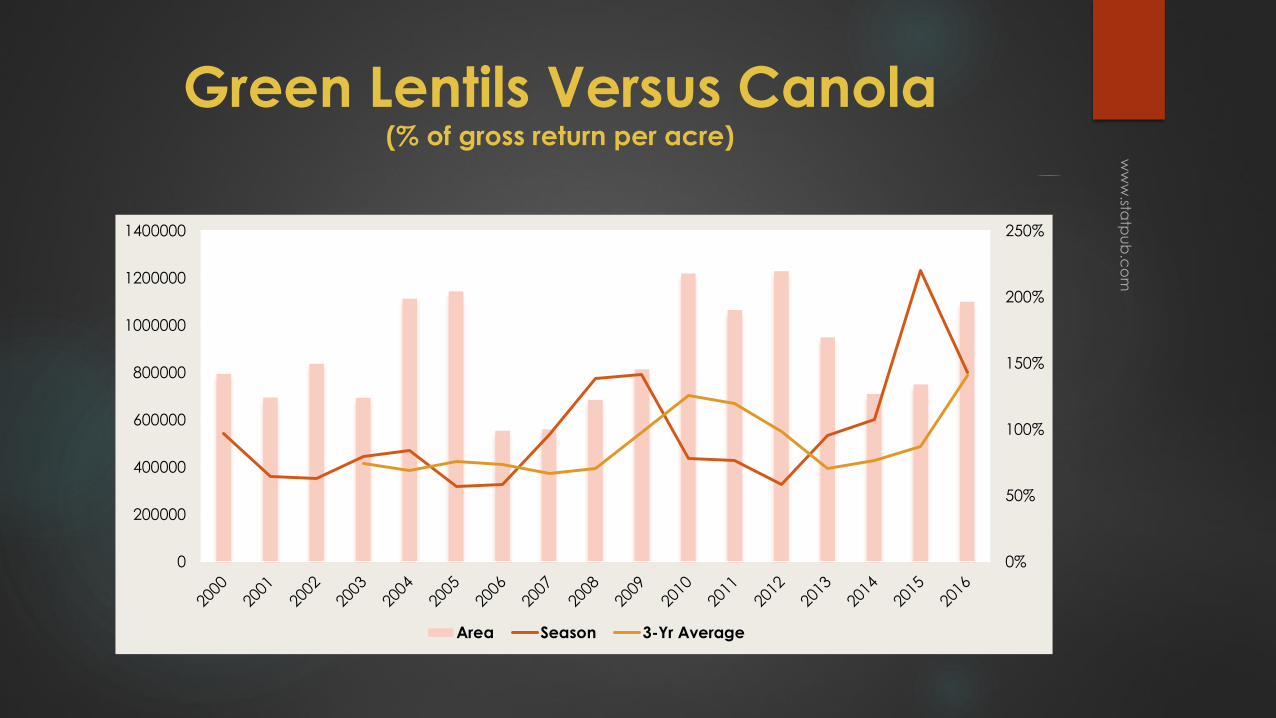

Green Lentils

Quality problems abound

Strong prices for quality

Green Lentils Versus Durum(% of gross return per acre)

0%

50%

100%

150%

200%

250%

300%

350%

400%

0

200000

400000

600000

800000

1000000

1200000

1400000

Area Season 3-Yr Average

Green Lentils Versus Canola(% of gross return per acre)

0%

50%

100%

150%

200%

250%

0

200000

400000

600000

800000

1000000

1200000

1400000

Area Season 3-Yr Average

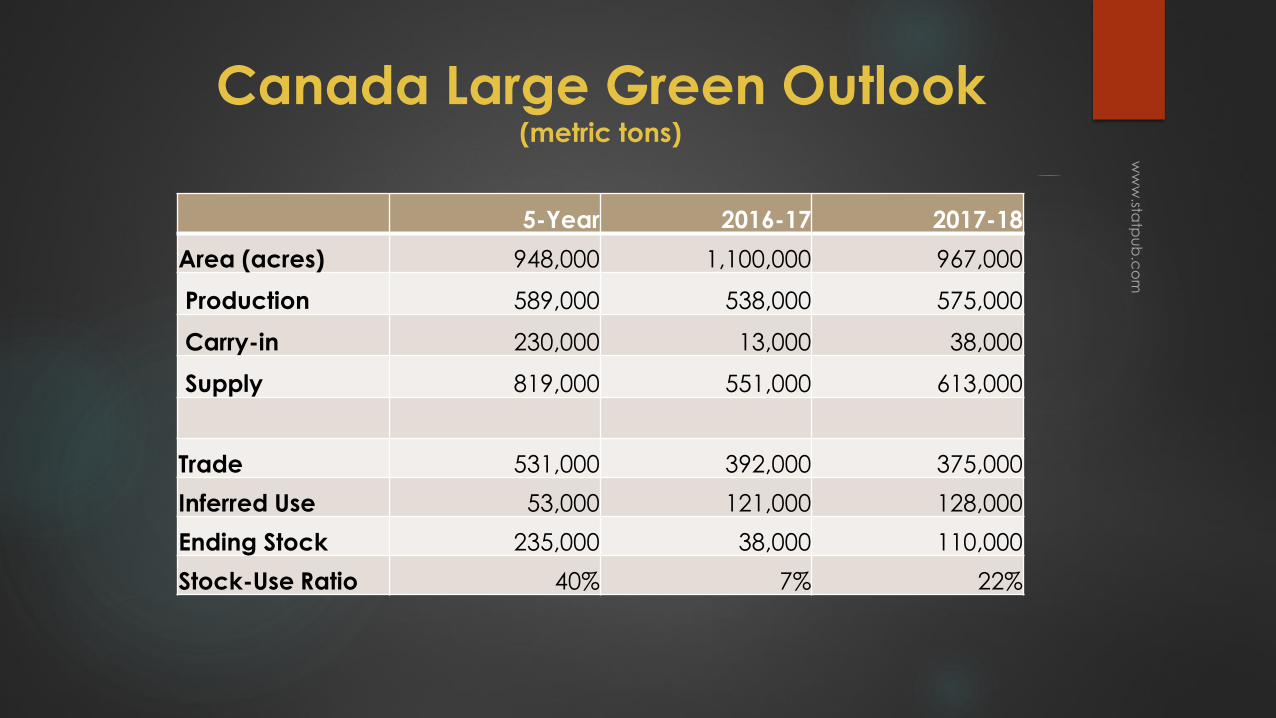

Canada Large Green Outlook(metric tons)

5-Year 2016-17 2017-18

Area (acres) 948,000 1,100,000 967,000

Production 589,000 538,000 575,000

Carry-in 230,000 13,000 38,000

Supply 819,000 551,000 613,000

Trade 531,000 392,000 375,000

Inferred Use 53,000 121,000 128,000

Ending Stock 235,000 38,000 110,000

Stock-Use Ratio 40% 7% 22%

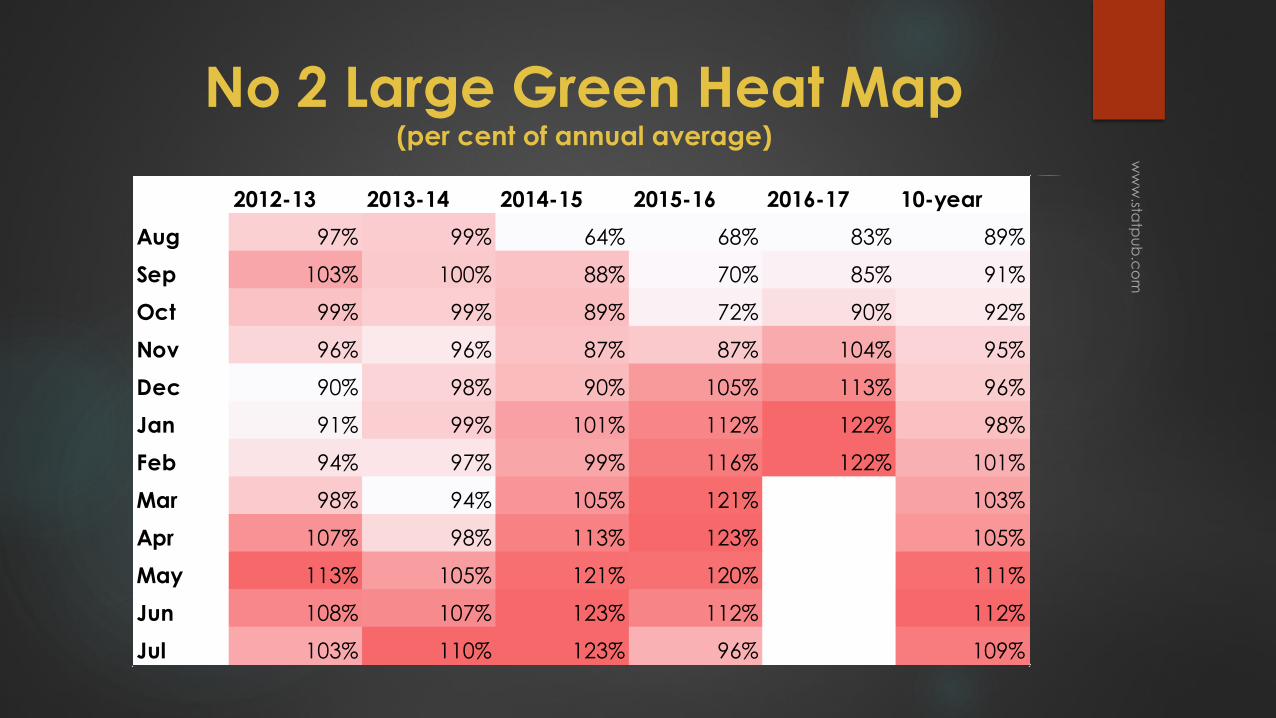

No 2 Large Green Heat Map (per cent of annual average)

2012-13 2013-14 2014-15 2015-16 2016-17 10-year

Aug 97% 99% 64% 68% 83% 89%

Sep 103% 100% 88% 70% 85% 91%

Oct 99% 99% 89% 72% 90% 92%

Nov 96% 96% 87% 87% 104% 95%

Dec 90% 98% 90% 105% 113% 96%

Jan 91% 99% 101% 112% 122% 98%

Feb 94% 97% 99% 116% 122% 101%

Mar 98% 94% 105% 121% 103%

Apr 107% 98% 113% 123% 105%

May 113% 105% 121% 120% 111%

Jun 108% 107% 123% 112% 112%

Jul 103% 110% 123% 96% 109%

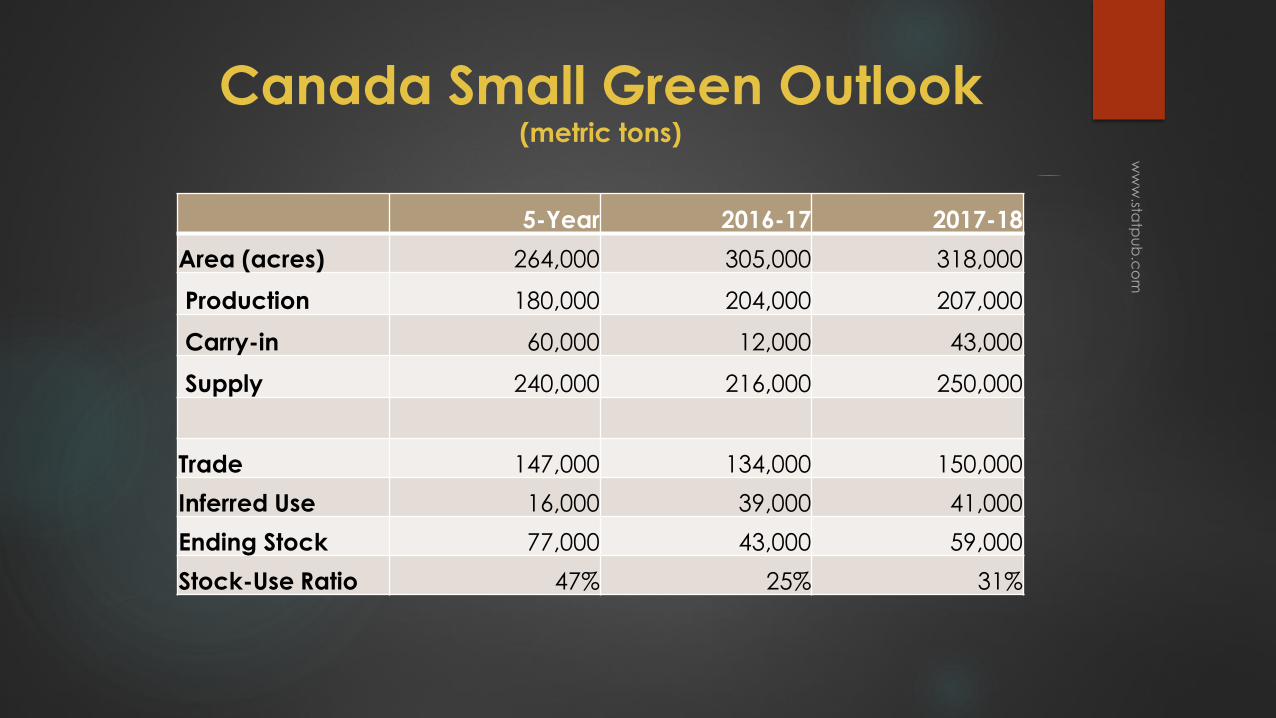

Canada Small Green Outlook(metric tons)

5-Year 2016-17 2017-18

Area (acres) 264,000 305,000 318,000

Production 180,000 204,000 207,000

Carry-in 60,000 12,000 43,000

Supply 240,000 216,000 250,000

Trade 147,000 134,000 150,000

Inferred Use 16,000 39,000 41,000

Ending Stock 77,000 43,000 59,000

Stock-Use Ratio 47% 25% 31%

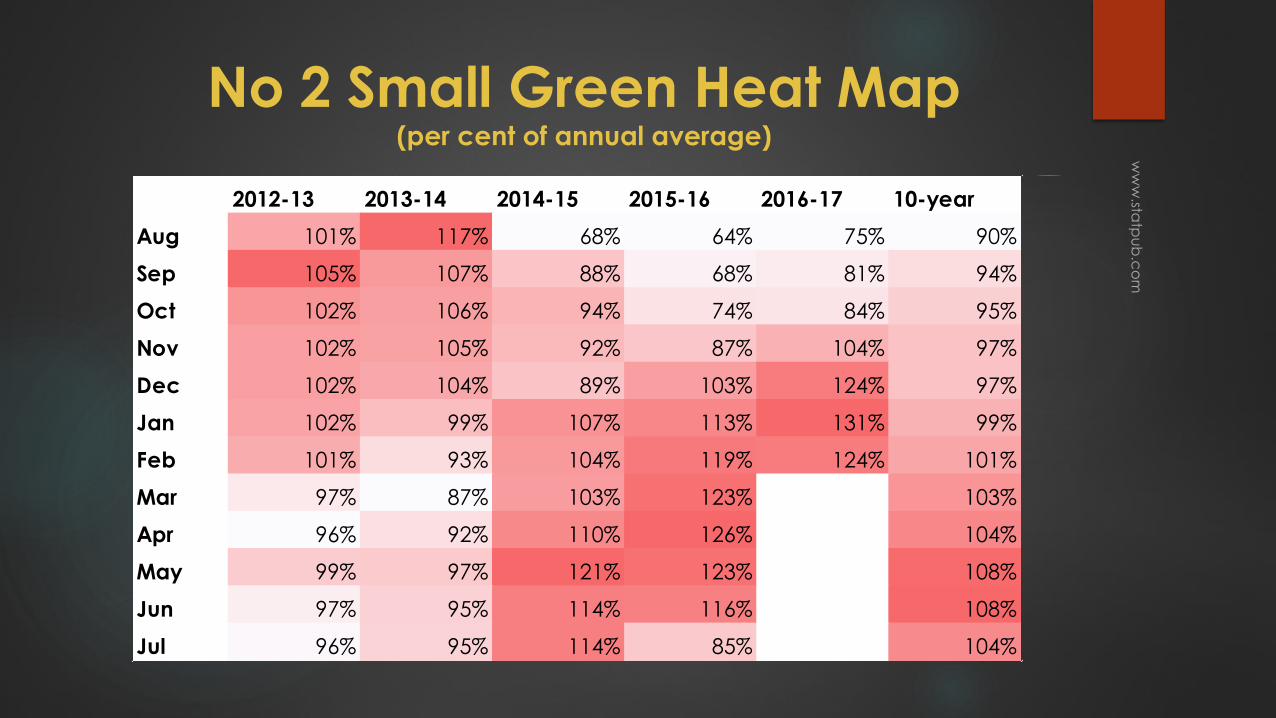

No 2 Small Green Heat Map (per cent of annual average)

2012-13 2013-14 2014-15 2015-16 2016-17 10-year

Aug 101% 117% 68% 64% 75% 90%

Sep 105% 107% 88% 68% 81% 94%

Oct 102% 106% 94% 74% 84% 95%

Nov 102% 105% 92% 87% 104% 97%

Dec 102% 104% 89% 103% 124% 97%

Jan 102% 99% 107% 113% 131% 99%

Feb 101% 93% 104% 119% 124% 101%

Mar 97% 87% 103% 123% 103%

Apr 96% 92% 110% 126% 104%

May 99% 97% 121% 123% 108%

Jun 97% 95% 114% 116% 108%

Jul 96% 95% 114% 85% 104%

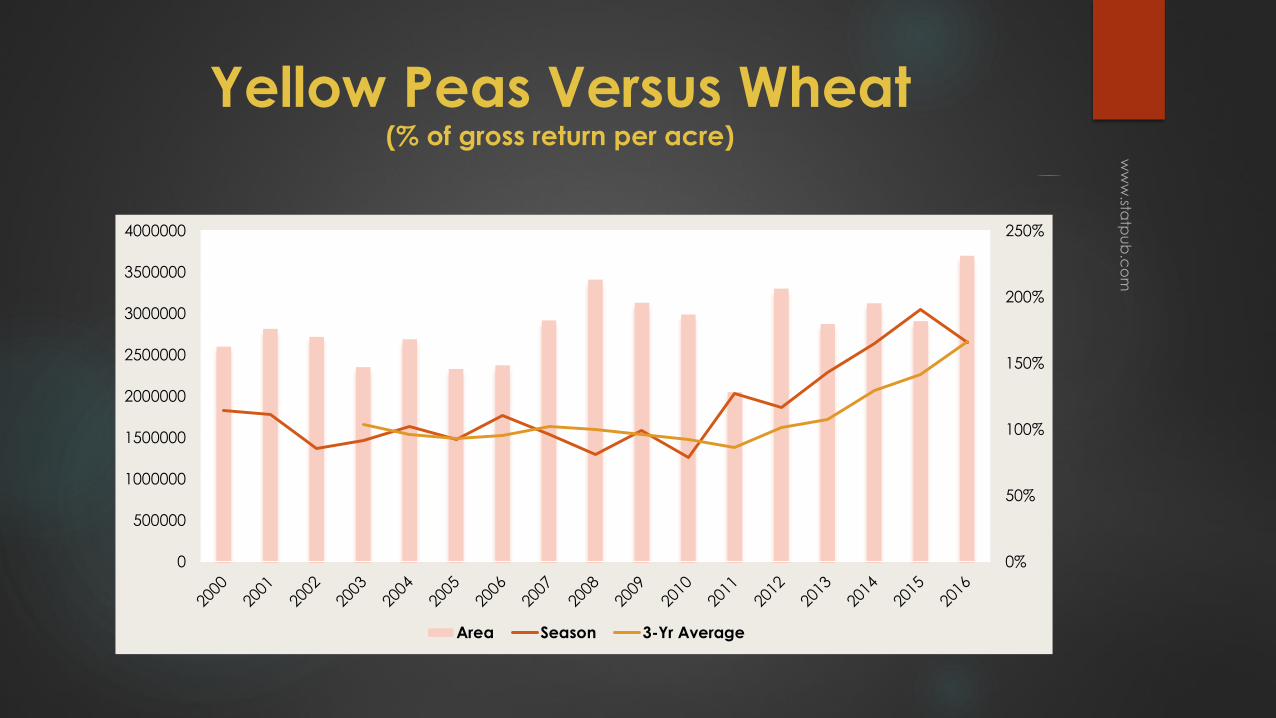

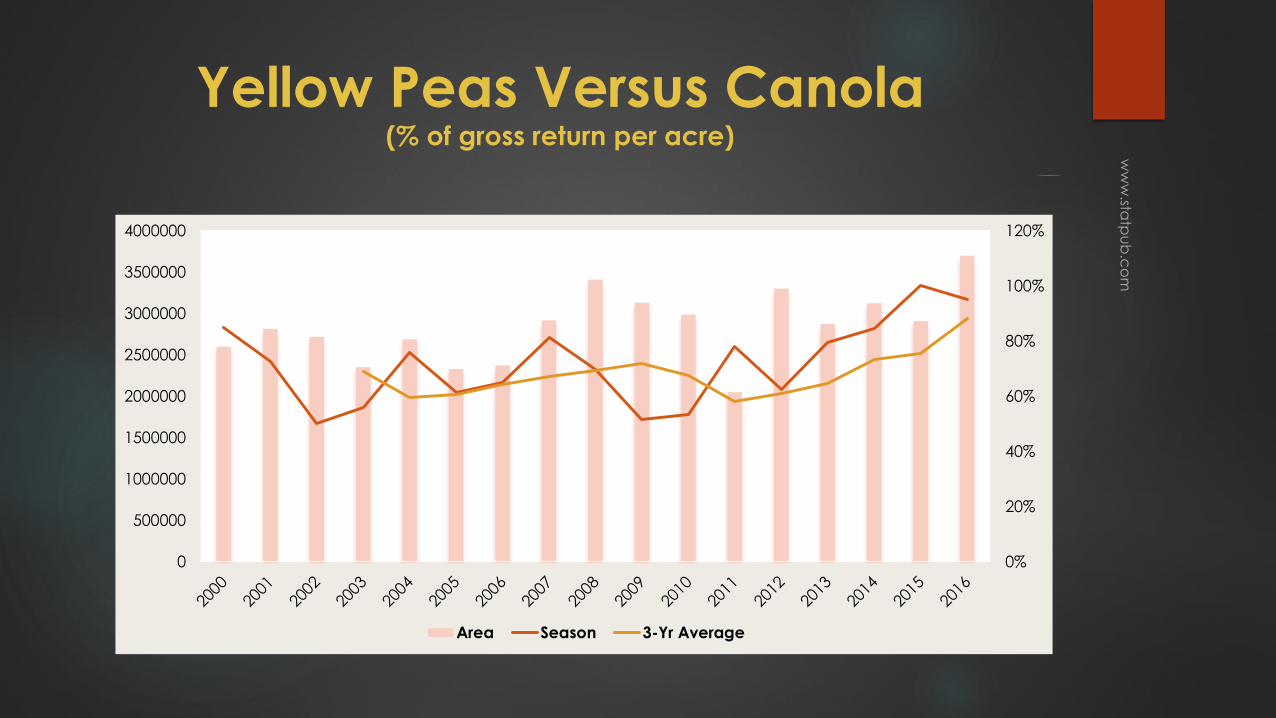

Yellow Peas

Excellent movement

Still competitive for area

Yellow Peas Versus Wheat(% of gross return per acre)

0%

50%

100%

150%

200%

250%

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

Area Season 3-Yr Average

Yellow Peas Versus Canola(% of gross return per acre)

0%

20%

40%

60%

80%

100%

120%

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

Area Season 3-Yr Average

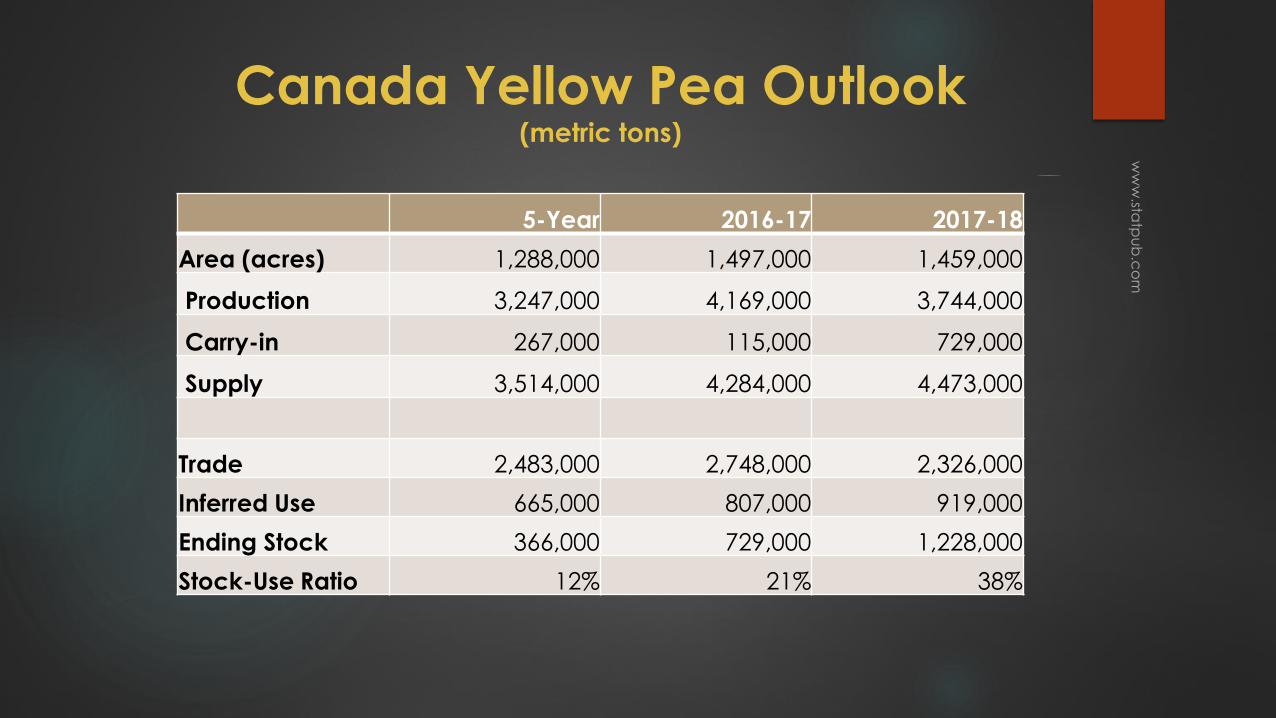

Canada Yellow Pea Outlook(metric tons)

5-Year 2016-17 2017-18

Area (acres) 1,288,000 1,497,000 1,459,000

Production 3,247,000 4,169,000 3,744,000

Carry-in 267,000 115,000 729,000

Supply 3,514,000 4,284,000 4,473,000

Trade 2,483,000 2,748,000 2,326,000

Inferred Use 665,000 807,000 919,000

Ending Stock 366,000 729,000 1,228,000

Stock-Use Ratio 12% 21% 38%

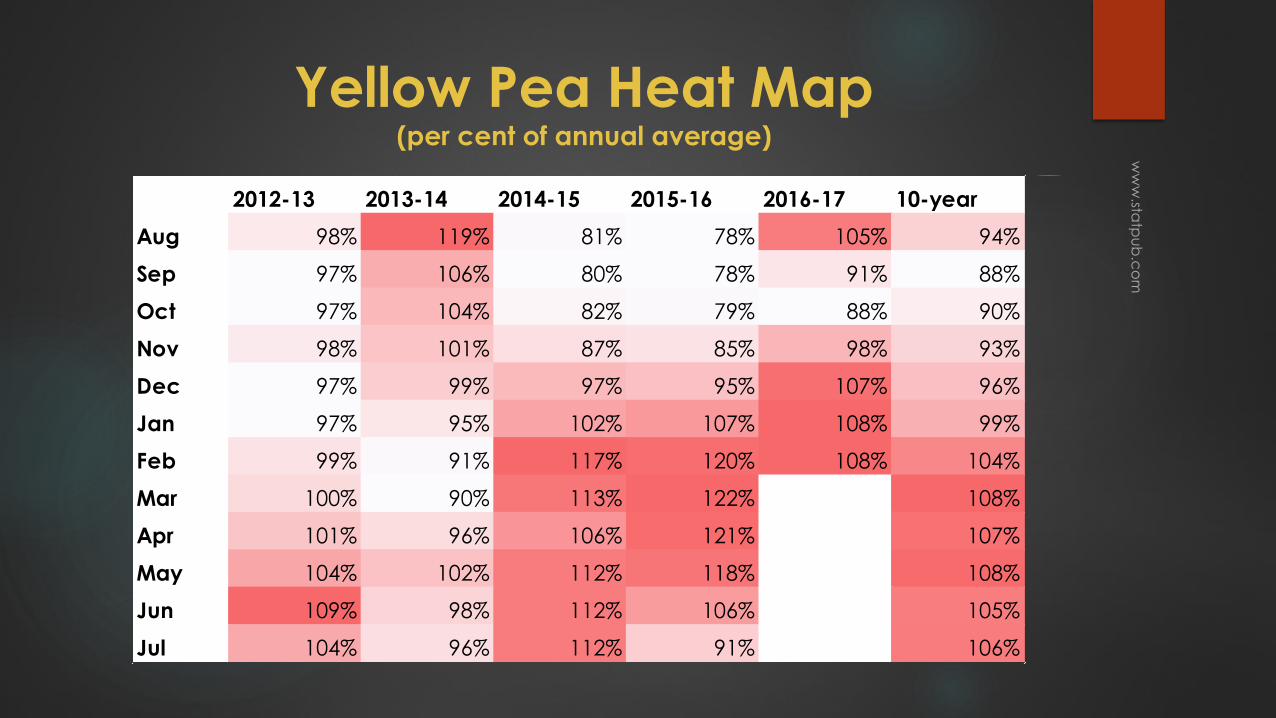

Yellow Pea Heat Map (per cent of annual average)

2012-13 2013-14 2014-15 2015-16 2016-17 10-year

Aug 98% 119% 81% 78% 105% 94%

Sep 97% 106% 80% 78% 91% 88%

Oct 97% 104% 82% 79% 88% 90%

Nov 98% 101% 87% 85% 98% 93%

Dec 97% 99% 97% 95% 107% 96%

Jan 97% 95% 102% 107% 108% 99%

Feb 99% 91% 117% 120% 108% 104%

Mar 100% 90% 113% 122% 108%

Apr 101% 96% 106% 121% 107%

May 104% 102% 112% 118% 108%

Jun 109% 98% 112% 106% 105%

Jul 104% 96% 112% 91% 106%

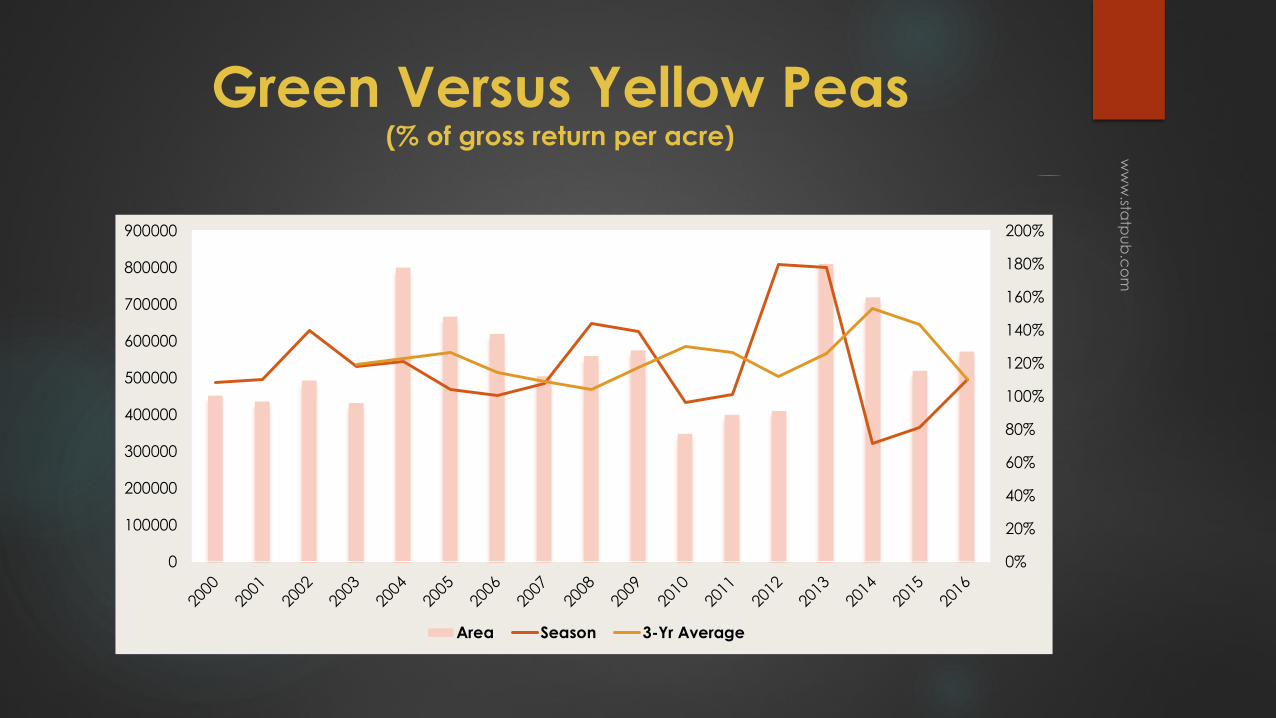

Green Peas

Yellow returns better

Still a special crop

Green Versus Yellow Peas(% of gross return per acre)

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

Area Season 3-Yr Average

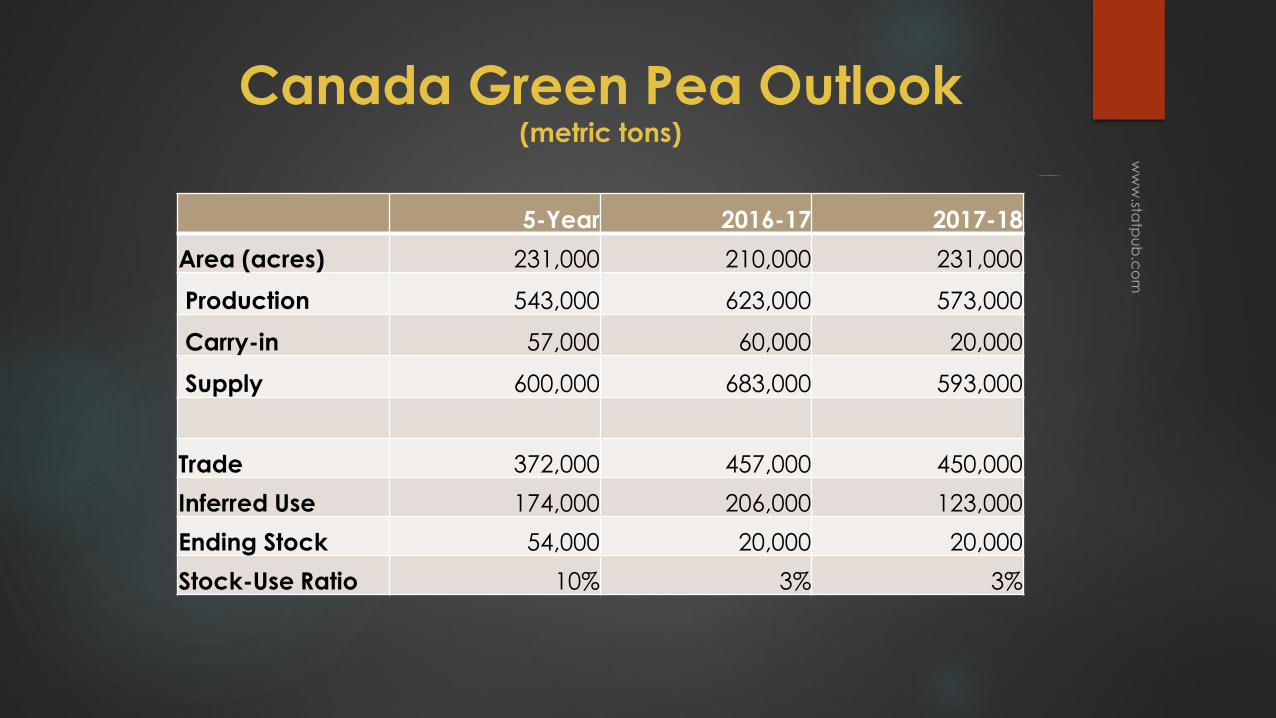

Canada Green Pea Outlook(metric tons)

5-Year 2016-17 2017-18

Area (acres) 231,000 210,000 231,000

Production 543,000 623,000 573,000

Carry-in 57,000 60,000 20,000

Supply 600,000 683,000 593,000

Trade 372,000 457,000 450,000

Inferred Use 174,000 206,000 123,000

Ending Stock 54,000 20,000 20,000

Stock-Use Ratio 10% 3% 3%

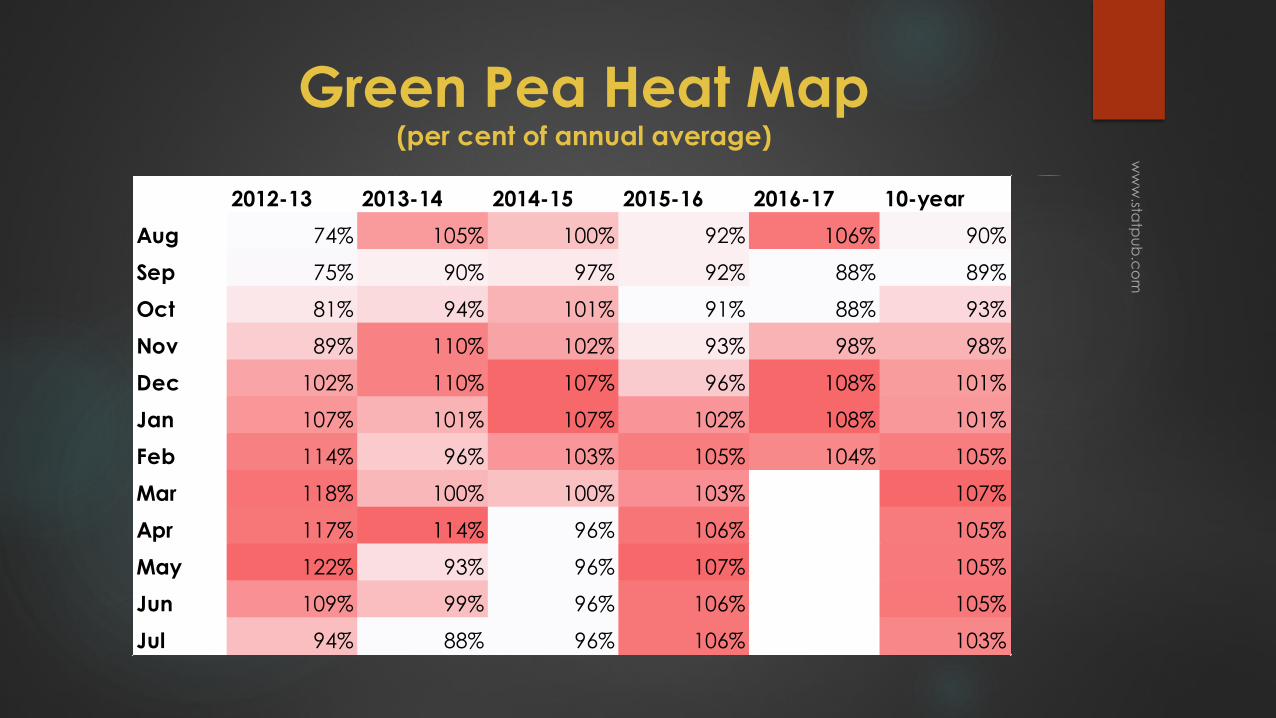

Green Pea Heat Map (per cent of annual average)

2012-13 2013-14 2014-15 2015-16 2016-17 10-year

Aug 74% 105% 100% 92% 106% 90%

Sep 75% 90% 97% 92% 88% 89%

Oct 81% 94% 101% 91% 88% 93%

Nov 89% 110% 102% 93% 98% 98%

Dec 102% 110% 107% 96% 108% 101%

Jan 107% 101% 107% 102% 108% 101%

Feb 114% 96% 103% 105% 104% 105%

Mar 118% 100% 100% 103% 107%

Apr 117% 114% 96% 106% 105%

May 122% 93% 96% 107% 105%

Jun 109% 99% 96% 106% 105%

Jul 94% 88% 96% 106% 103%

Fababeans

Egypt is only major market

The bloom is off?

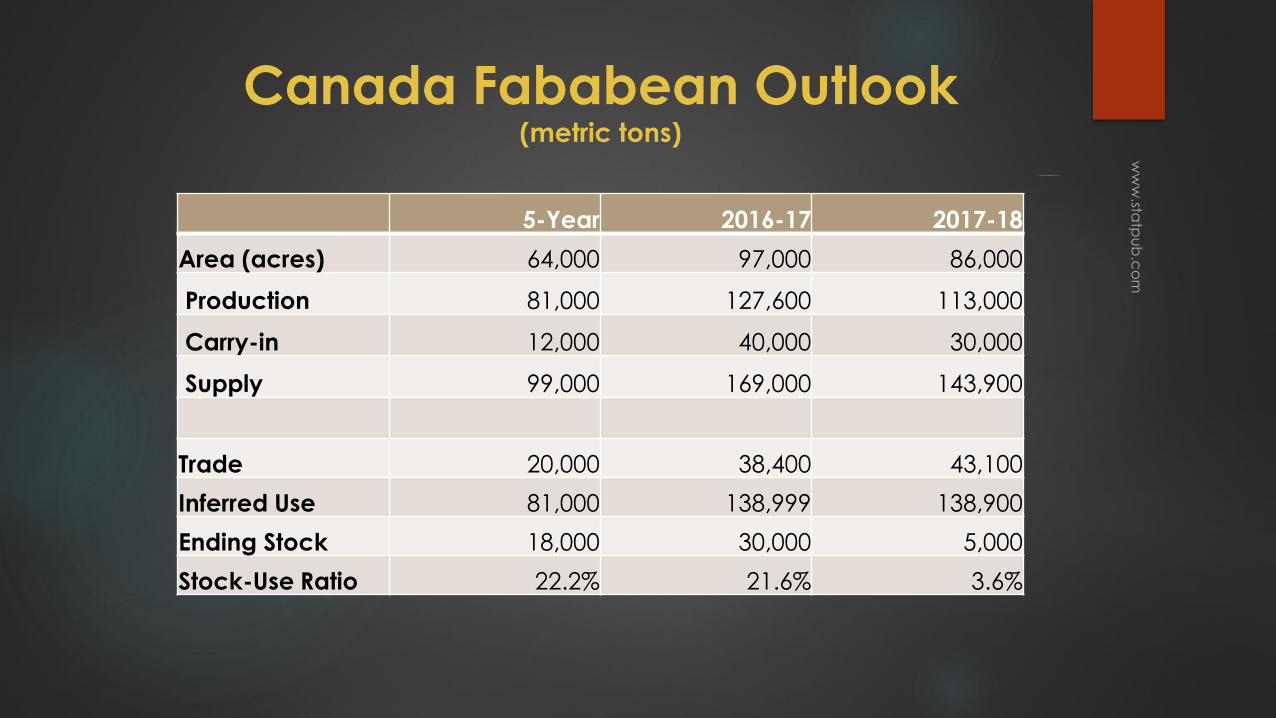

Canada Fababean Outlook(metric tons)

5-Year 2016-17 2017-18

Area (acres) 64,000 97,000 86,000

Production 81,000 127,600 113,000

Carry-in 12,000 40,000 30,000

Supply 99,000 169,000 143,900

Trade 20,000 38,400 43,100

Inferred Use 81,000 138,999 138,900

Ending Stock 18,000 30,000 5,000

Stock-Use Ratio 22.2% 21.6% 3.6%

To summarize

The pulse premium has disappeared

Area in Canada should drop

Indian demand will drop in 2017

THANK YOU