Workshop dec 2012

27

Legal and Institutional Frameworks for Secured Lending Moscow December 2012

Transcript of Workshop dec 2012

Legal and Institutional Frameworks for Secured Lending

Moscow

December 2012

Antecedent Work on Reform

• EBRD critique and recommendations on Codification Committee’s 2010 draft amendments to Chapter 23 of Civil Code

• Identified positive changes in draft and numerous remaining deficiencies

• Developed proposed amendments to draft that is now before Duma (without those amendments)

Determine Approach to Reform• Amend existing law or replace? The question

needs to be considered

• Start by describing the desired end state, by whatever route it is reached

• At the highest abstract level, end state must fit core concepts of modern secured lending, to be addressed serially as:– Comprehensive coverage

– Functional approach

– Flexibility and autonomy of parties

– Simplicity

Comprehensive Coverage

• One set of rules for all arrangements in which an obligation (monetary or otherwise) is secured by a legal interest in movable property

• All types of:

– Parties – natural and juridical

– Legal forms of security

– Movable property

Functional Approach

• Not defined by narrow rules of specific legal forms of interest in movable property

• Concerned with what the transaction does, not what name we use for it

• Approach does not require abolishment of legal forms, only that they be treated with one set of rules with regard to coverage of this law

Flexibility and Party Autonomy

• Principally with respect to description of the obligation and property

• Also with respect to other terms of agreement such as definition of terms of default

• General idea is that parties should be free to frame their own agreements within broad scope of the law

Simplicity

• No requirements that are not necessary to core purpose of law

• Eliminate formalities, e.g. notarization of agreements

• Eliminate need for paper in registration

• KISS rule as guiding mantra

Legal Framework

Framework must have four major components – may be in different legal sources, e.g. CC, special law, regulation

• Creation of security interest

• Priority scheme and requirements

• Registration and registry

• Enforcement

Will address each in turn

Component 1 – Creation of Security Interest

• Parties make security agreement

• Agreement in writing – any tangible medium

• Parties set own terms – no unnecessary requirements in law

• Binding on parties upon conclusion of agreement – no registration required

A Security Interest May:

Secure one or more obligations that may:

• Be described specifically or generally

• Be monetary or non-monetary

• Be pre-existing, present or future; or a line of credit

Description of Collateral

• Description may be specific or general; may include future collateral

• Must reasonably identify collateral

• “All equipment” or “all accounts receivable” is sufficient description

• Purchase money exception – specific description necessary

Types of Interests Covered

• Pledge

• Chattel mortgage

• Sale with retained title

• Installment seller’s right to re-take

• Finance lease

• Other interest in movables that secures an obligation

Types of Movables• Equipment• Inventory and raw goods• Cash-flows (receivables & secured sales

contracts)• Intangibles and documents (e.g.

securities, warehouse receipts, instruments, contract rights, intellectual property, etc.)

• Crops and livestock• Fixtures – movables fixed to real estate• Consumer goods• Cash & deposit accounts• Minerals and timber to be severed from land

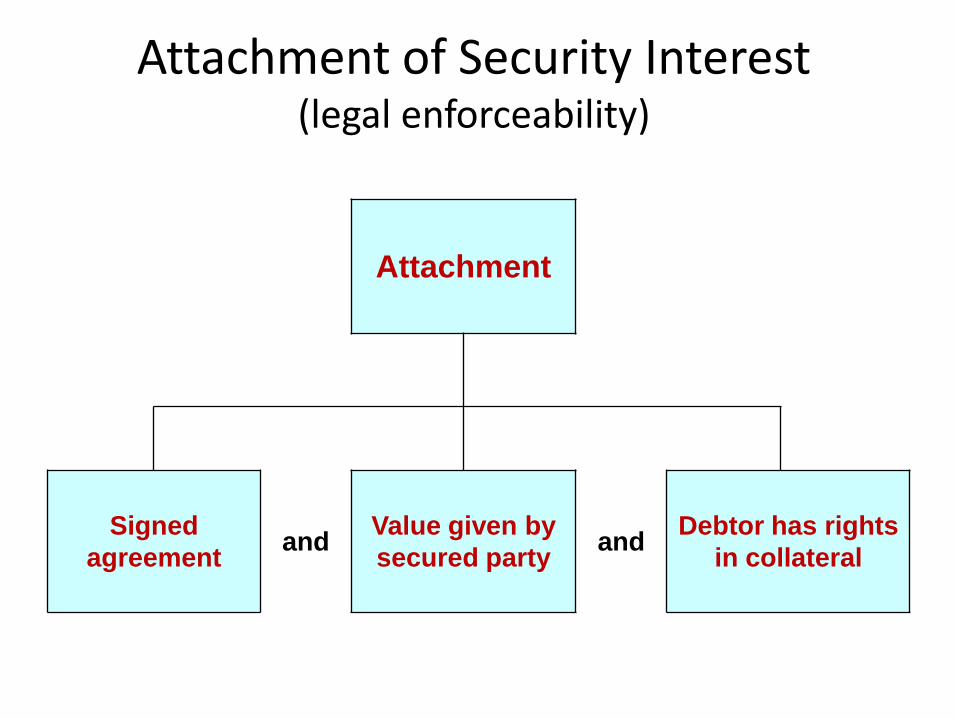

Attachment (Effectiveness between Parties) of Security Interest

Attachment relates to making the security interest enforceable between the parties

Three requisites:

• Security agreement signed by debtor

• Secured party has given value

• Debtor has rights in the collateral (not necessarily ownership)

A security interest attaches to proceeds of original collateral

Attachment of Security Interest(legal enforceability)

Attachment

Signed

agreementand

Value given by

secured partyand

Debtor has rights

in collateral

Continuity of Security Interest

• General Rule: Security interest continues in collateral even if sold, leased, licensed or otherwise disposed

• Exceptions are laid out in Law

Component 2 – Priority Scheme

• General principle – priority determined by when security interest is made transparent, e.g. by registration, possession or control

• Exceptions:

–Purchase money

–Proceeds

–Purchase in ordinary course of business

Perfection a/k/a Completion or Third Party Effectiveness

• Perfection means optimization of secured creditor’s rights against third parties

• Generally achieved by making security interest transparent

• Requires attachment and means of perfection

• Four means of perfection:– Registering notice in registry

– Possession

– Control

– Automatic (purchase money, proceeds)

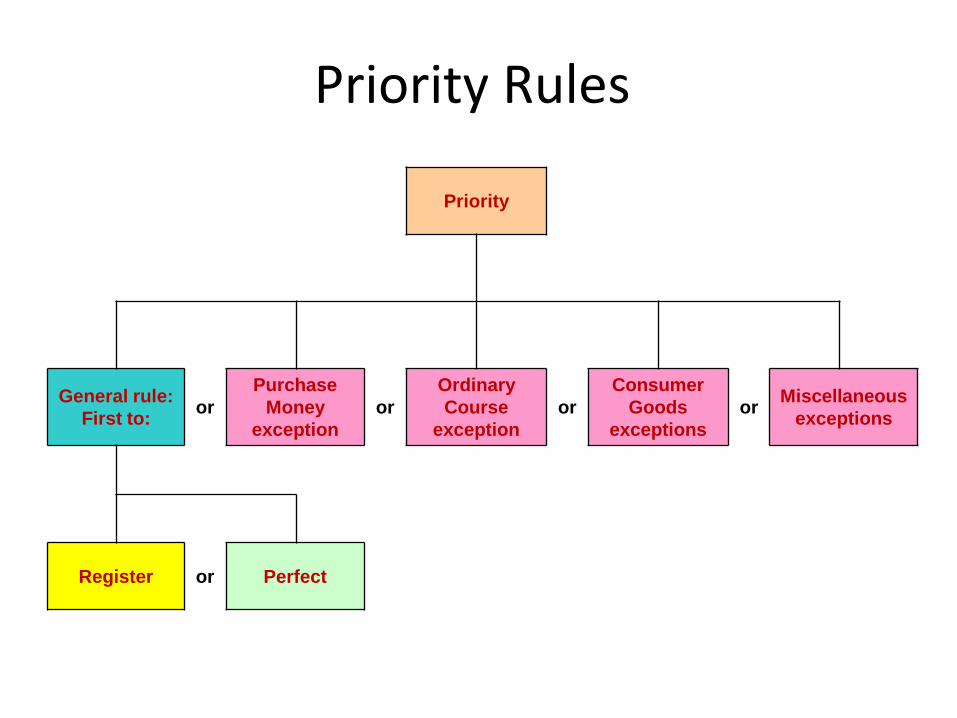

Priority Rules

Priority

General rule:

First to:or

Purchase

Money

exception

or

Ordinary

Course

exception

or

Consumer

Goods

exceptions

orMiscellaneous

exceptions

Register or Perfect

Priority Is Against Following:

• Buyers of collateral

• Unsecured creditors

• Other secured creditors

• Lessors of equipment

• Bankruptcy liquidator

• Other interests (government and judgment liens, etc.) if politically possible to include in law

Special Priority Provisions Facilitate MSME and Agricultural Financing

• Purchase money security interest has priority over security interest in a class of movables; enables business to use second financer for purchase of a specific asset

• Interest in crops, growing or to be grown has priority over interests in the land

• Interest in crops or livestock for costs of production has priority over a general security interest in crops or livestock

Component 3 – Registration and Registry

• Secured party registers only a notice, not the security agreement

• Notice includes only:–Debtor name or identification number

– Secured party name and address

–Description of collateral – general or specific

• No formalities required – notice does not create rights; it only publicizes the interest

Purpose of Registry

• To give notice of the secured creditor’s interest in the collateral

• To establish the secured creditor’s priority by time of registration of the notice

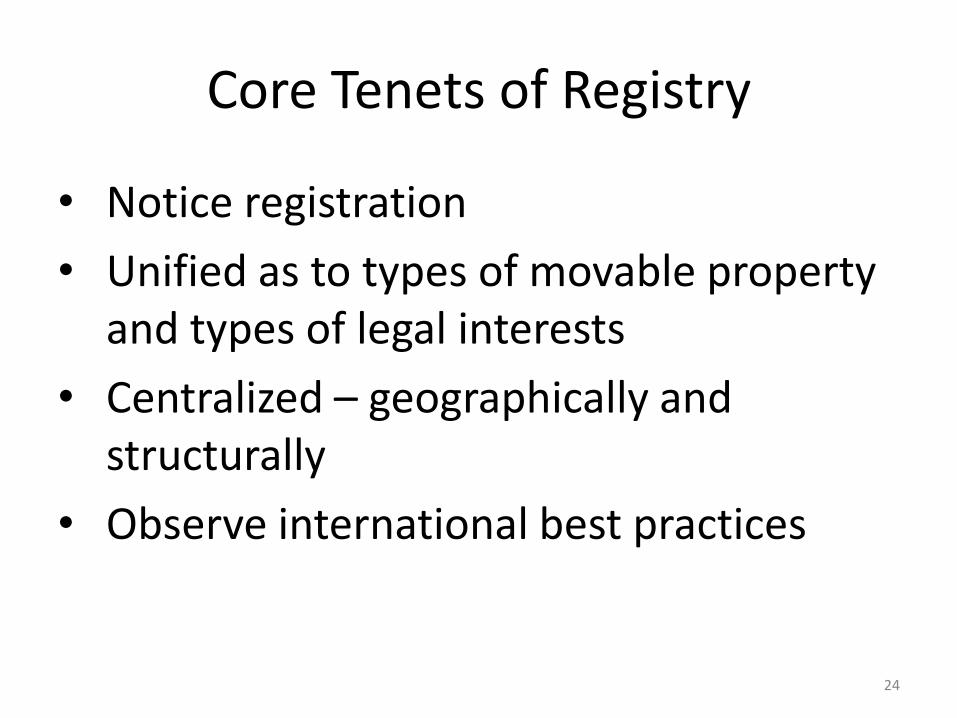

Core Tenets of Registry

• Notice registration

• Unified as to types of movable property and types of legal interests

• Centralized – geographically and structurally

• Observe international best practices

24

• Accuracy – capture exactly information presented

• Speed – speed of registration and searching

• Accessibility – any time, from any place

• Cost effectiveness – fees cover costs of operation; not general revenue source for government

• Simplicity – reduce risk of error and encourage use

• Limited to purposes of registration – give notice and establish priority

• Rule-based decision-making – no bureaucratic discretion in registration and searching

Registry Best Practices

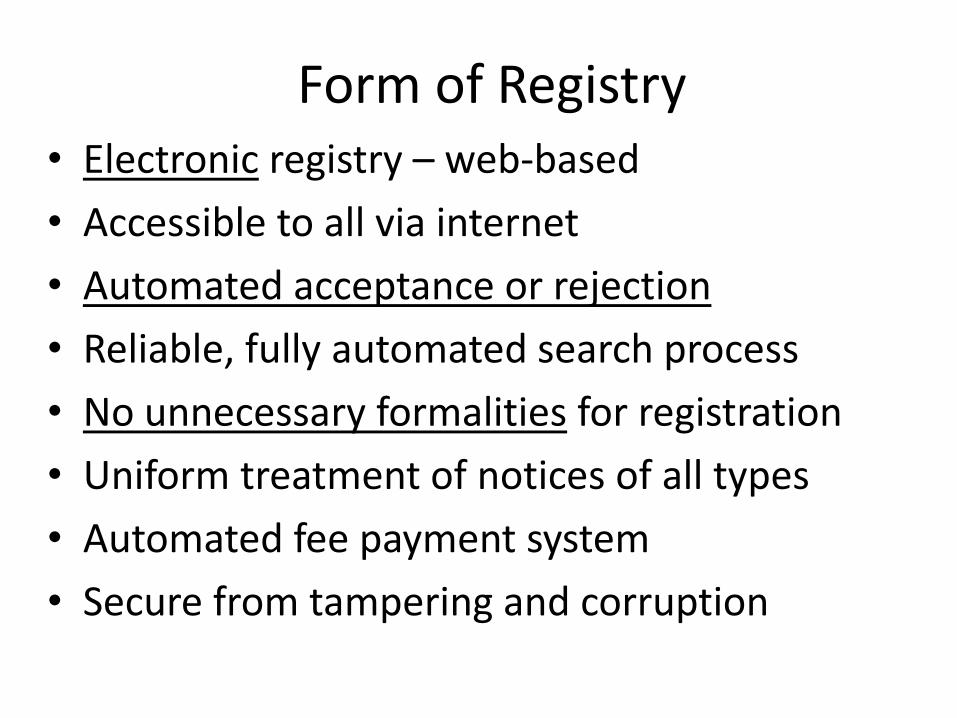

Form of Registry• Electronic registry – web-based

• Accessible to all via internet

• Automated acceptance or rejection

• Reliable, fully automated search process

• No unnecessary formalities for registration

• Uniform treatment of notices of all types

• Automated fee payment system

• Secure from tampering and corruption

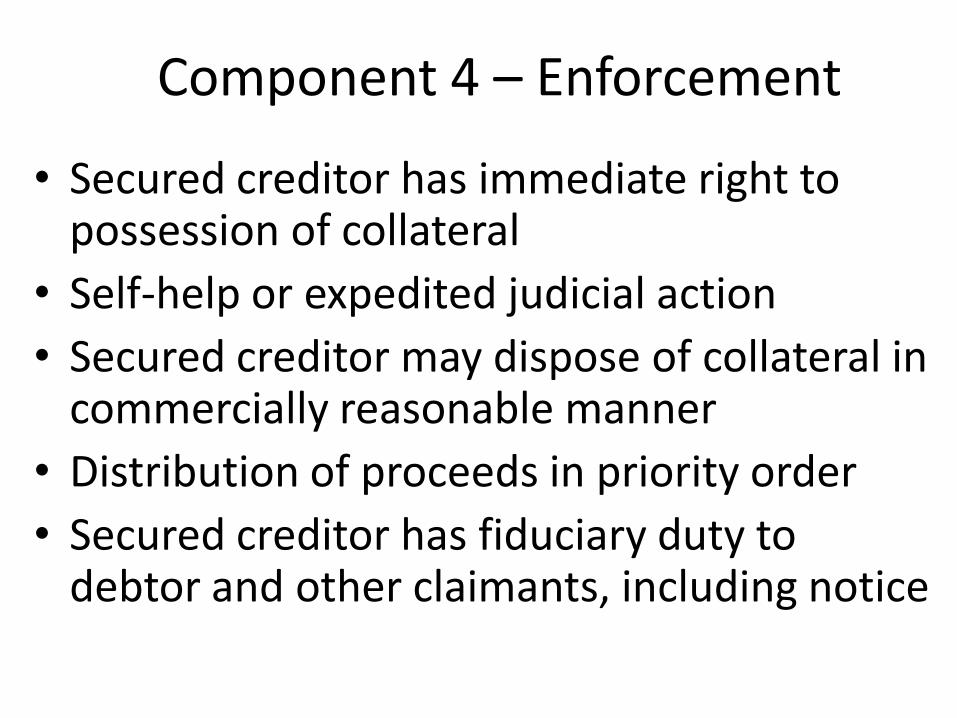

Component 4 – Enforcement

• Secured creditor has immediate right to possession of collateral

• Self-help or expedited judicial action

• Secured creditor may dispose of collateral in commercially reasonable manner

• Distribution of proceeds in priority order

• Secured creditor has fiduciary duty to debtor and other claimants, including notice