Working Paper 101 - The Global Financial Crisis and ......Office of the Chief Economist AFRICAN...

43

N° 101 - July 2009 The Global Financial Crisis and Domestic Resource Mobilization in Africa

Transcript of Working Paper 101 - The Global Financial Crisis and ......Office of the Chief Economist AFRICAN...

N° 101 - July 2009

The Global Financial Crisis and DomesticResource Mobilization in Africa

ISBN - 978 - 9973 - 071 - 25 - 5

Correct citation : Ernest Aryeetey (2009), The Global Financial Crisis and Domestic Resource Mobilization inAfrica, Working Papers Series N°101, African Development Bank, Tunis, Tunisia. 37 pp.

Editorial Committee

Kamara, Abdul B. (Chair)Anyanwu, John C.Aly, Hassan YoussefRajhi, TaoufikVencatachellum, Desire J. M.

Coordinators

Salami, AdelekeMoummi, Ahmed

Copyright © 2009Africain Development BankAngle des trois rues: Avenue du Ghana,Rue Pierre de Coubertin, Rue Hédi NouiraBP 323 - 1002 TUNIS belvédère (Tunisia)Tél: +216 71 333 511 / 71 103 450Fax: +216 71 351 933E-mail: [email protected]

Rights and Permissions

All rights reserved.

The text and data in this publication may bereproduced as long as the source is cited.Reproduction for commercial purposes isforbidden.

The Working Paper Series (WPS) are produc-ced by the Development ResearchDepartment of the African Development Bank.The WPS disseminates the findings of work inprogress, preliminary research results, anddevelopment experience and lessons, toencourage the exchange of ideas and innova-tive thinking among researchers, developmentpractitioners, policymakers, and donors. Thefindings, interpretations, and conclusionsexpressed in the Bank’s WPS are entirelythose of the author(s) and do not necessarilyrepresent the view of the African DevelopmentBank, its Board of Directors, or the countriesthey represent.

Working Papers are available online athttp:/www.afdb.org/

Office of the Chief Economist

AFRICAN DEVELOPMENT BANK GROUP

Working Paper No. 101July 2009

The Global Financial Crisis and DomesticResource Mobilization in Africa1

(1)This Working Paper is published from a consultancy report prepared by Ernest Aryeetey, presented at aworkshop on the Global Financial Crisis hosted by the African Development Bank on 10 April 2009 in Tunis,Tunisia.

As access to foreign resources has becomeincreasingly difficult, in the wake of the globalfinancial crisis, the use of domestic resourcesfor development purposes is becoming moreand more important. Ironically, however, thereare possibilities of the financial crisis also affec-ting the mobilization of domestic resources. Theglobal financial crisis affected the capacity ofthe public sector to mobilize tax revenues. Theintroduction of such new taxes as VAT, the ratio-nalization of trade tariffs, the strengthening oftax offices, the reform of incentive structures,reduction and removal of subsidies have thepotential to improve domestic resource mobili-zation.

Another significant challenge that African coun-tries face is how to strengthen their financialsystems in order to make them deliver thenecessary financial resources to be used forboosting investments and facilitate employmentcreation. Reforms in this area will enhance thepolicy environment for financial institutions andprovide incentives for them to become morecompetitive. Despite the effort, studies of finan-cial systems performance in most African coun-tries over the last two decades have often sug-gested that the reforms have generally had limi-ted success in effectively mobilizing domesticresources and channeling these into productiveinvestments.

While the African financial sector remains mar-ginally integrated in global financial market, it isgenerally true that in knowing that they couldborrow from international markets to supple-ment whatever resources were available to themfrom domestic markets encouraged Africanfinancial institutions to be a lot more out-goingin terms of the development of new instrumentsin recent years. But going back old ways wherethere was little interest in new instruments andnew clients, opting for safer government busi-ness only, will not be beneficial in the long-term.Reforms to enhance the continent’s integrationinto the global market are therefore important.

This paper attempts to answer some importantquestions: Whether the mobilization of domesticresources is counter-cyclical and whether exter-nal shocks will lead to improvements in domes-tic resource mobilization? The paper argues thatif there should be any interruptions in the flowof domestic resources, this may not be easilyattributable to the onset of the financial crisis,rather it is argued that the structural and institu-tional constraints that have hindered resourcemobilization for a long time will continue tomake it difficult for the financial systems torespond adequately to any interruptions inexternal resource flows. The paper highlights anumber of suggestions for countries to improvedomestic resources mobilization.

Abstract

Ernest Aryeetey, University of Ghana

Keywords: Financial crisis, saving, domestic resource mobilization JEL classification: G00, G14, G19

1. Introduction2. The Problem with Domestic Resource Mobilization in Africa

2.1 Trends in Savings Mobilization2.2 Credit Availability and Domestic Investment in SSA2.3 Taxation and Public Investments

3. The Financial Crisis and Domestic Resource Mobilization in Africa3.1 The Crisis and Savings Mobilization3.2 The Financial Crisis and Credit Availability3.3 The Financial Crisis and Tax Revenues

4. African Responses to Global Financial Crisis and Implications forDomestic Resource Mobilization

5. Moving Forward: Mobilizing Additional Domestic Resources5.1 Enhancing Savings Mobilization and Lending

6. Summary and ConclusionsReferencesFiguresFigure 1: Cross domestic savings by developing regions, 1960-2004Figure 2: Financial Deepening, M2/GDP RatioTablesTable 1: Distribution of savings rates in Africa, 2000-2005Table 2: Gross Fixed Capital Formation/GDP

144

101216171819

2122233435

59

510

Contents

1. Introduction

The use of domestic resources for deve-lopment purposes is becoming more andmore important as access to foreignresources becomes increasingly difficult.It is the current global financial crisis andthe subsequent recession that are gene-rally expected to make access to foreignresources more difficult. Ironically, howe-ver, there are possibilities of the financialcrisis also affecting the mobilization ofdomestic resources. “Domestic resourcemobilization refers to the generation ofsavings from domestic resources andtheir allocation to socially productiveinvestments” (Culpeper 2008). Suchresource mobilization can come from boththe public sector and the private sector.The public sector does this through taxa-tion and other forms of public revenuegeneration. The private sector mobilizesresources through household and busi-ness savings, working through financialintermediaries to convert these into pro-ductive assets.

The global financial crisis will affect thecapacity of the public sector to mobilizetax revenues if it affects the incomes ofresidents or has an impact on trade withoutsiders which will affect trade taxes. It isobserved that many African countrieshave pursued a number of reforms aimedat strengthening the mobilization of taxrevenues. The introduction of such new

taxes as VAT, the rationalization of tradetariffs, the strengthening of tax offices, thereform of incentive structures, reductionand removal of subsidies, etc. are someof the reforms associated with the fiscalsector in a number of countries withvaried outcomes. In Ghana, for example,government revenues have increasedsteadily as a share of GDP over the lasttwo decades at an average rate of 4 per-cent per annum. While this has happenedpublic expenditures have also climbedsteadily, albeit somewhat faster, leaving agrowing deficit. The quality of such expen-ditures in delivering socially productiveoutcomes has been questioned (Killick2008). The situation is not different inmost countries.

Another significant challenge that Africancountries face is how to strengthen theirfinancial systems in order to make themdeliver the necessary financial resourcesto be used for boosting investments andfacilitating employment creation. The lasttwo decades have seen several reformsintended to deal with various bottlenecksin the system for the purpose. Most of thereforms have been designed to enhancethe policy environment for financial institu-tions and provide incentives for them tobecome more competitive. They have alsobeen intended to build the institutionalcapacity to handle the growing demand fordifferent types of financial services comingfrom a more diversified clientele.

1

Despite the effort, studies of financial sys-tems performance in most African coun-tries over the last two decades have oftensuggested that the reforms have generallyhad limited success in effectively mobili-zing domestic resources and channelingthese into productive investments.Savings mobilization has been slow inmany countries and lending to the privatesector has always been problematic,especially for small borrowers. In somecountries, weak financial systems havefacilitated considerable capital flight tomore modern economies. In trying tostem the problem, a number of countrieshave devoted considerable resources tostrengthening regulatory regimes, withvaried results coming out of the effort.

A number of studies into the problems ofmobilizing domestic resources have focu-sed on the nature and extent of financialdevelopment in the light of reforms.Nissanke and Aryeetey (2008) argued thatthe situation of difficult financial interme-diation is the consequence of having frag-mented financial markets which have diffi-culty minimizing transaction costs the wayefficient markets do. As a result of thefragmentation, the different elements ofthe market serve different groups andinterests and do not afford them the bene-fits from a competitive market. The mar-kets have difficulty mobilizing depositsfrom surplus units and making these avai-lable to deficit units. This is best reflectedby the presence of many informal and

semi-formal operators who are fairly inde-pendent of the formal financial system.

With the current global financial crisis,the view has generally been that sinceAfrican financial markets were not closelyintegrated into global financial systemsthey would be spared the worst of theeffects on financial markets. It is arguedthat African banks generally have Africanownership and therefore the problems ofthe European and American banks arenot likely to be transferred to the Africanbanks through ownership structures. Evenwhere there is some foreign ownership,and this has increased with reforms, theassets and liabilities of these institutionsare fairly well decoupled. Another argu-ment has also been that African bankshave limited exposure to the internationalfinancial markets. Their borrowing fromthese markets has been limited and theyhave not had much interaction with theso-called toxic assets of the foreign insti-tutions. While these may very well begenerally true, the fact also remains thatin knowing that they could borrow frominternational markets to supplement wha-tever resources were available to themfrom domestic markets encouragedAfrican financial institutions to be a lotmore out-going in terms of the develop-ment of new instruments in recent years.There is certainly a worry now that thebanks would go back to their old ways,showing extremely little interest in newinstruments and new clients, opting forsafer government business only.

2

It is important to note that even if Africaninstitutional arrangements for the mobili-zation of domestic resources are not clo-sely integrated into international arrange-ments, the various economic agents whouse the financial systems may be affectedby their own interaction with the interna-tional goods and other markets, which inturn would affect their incomes and hencetheir ability to engage with tax authoritiesand the financial systems as appropriate.

The global financial crisis is expected toreduce external inflows into African eco-nomies. FDI, aid, export earnings, remit-tances, etc. are all expected to be affec-ted by the financial crisis. Moreover, thecrisis is making it more difficult and moreexpensive to attract private capital thanbefore. Indeed it will require more effort toaccess the same level or even lowerlevels of external resources than before.There have been long held views thatefforts to attract foreign resources alwaystake away from initiatives to mobilizedomestic resources for African develop-ment (Adam and O’Connell, 1997).Hence, there is a growing concern thatthe search for external support in this per-iod of challenges will lead to reducedattention to domestic resource mobiliza-tion. The main thrust of this paper therefo-re is essentially to show that while thedirect effects of a financial crisis will notbe immediately observed in a significantway in the functioning of African financialsystems, despite the reduced flows, they

will lead to a slowdown in the productiveactivities of African countries through theirreal sectors. In order to offset this redu-ced flow and also in order to promote longterm growth and development throughsustained production, it is essential thatAfrican countries mobilize additionaldomestic resources.

This paper on the impact of the globalfinancial crisis essentially looks at trendsin the mobilization of domestic resourcesfocusing on savings mobilization and cre-dit to the private sector, as well as theproblems with the mobilization of taxes.One issue considered is whether themobilization of domestic resources iscounter-cyclical. Are they expected to risein the face of external shocks? The paperargues that if there should be any inter-ruptions in the flow of domestic resources,this may not be easily attributable to theonset of the financial crisis. While trying toidentify how the current global financialcrisis may affect the performance ofAfrican countries in the area of resourcemobilization, it is argued that the structu-ral and institutional constraints that havehindered resource mobilization for a longtime will continue to make it difficult forthe financial systems to respond adequa-tely to any interruptions in external resour-ce flows. It is further argued that theeffects of the crisis on domestic resourcemobilization can be identified mostlythrough indirect channels. The paperhighlights a number of suggestions that

3

have been made for countries to mobilizedomestic resources and then concludes.

2. The Problem withDomestic ResourceMobilization in Africa

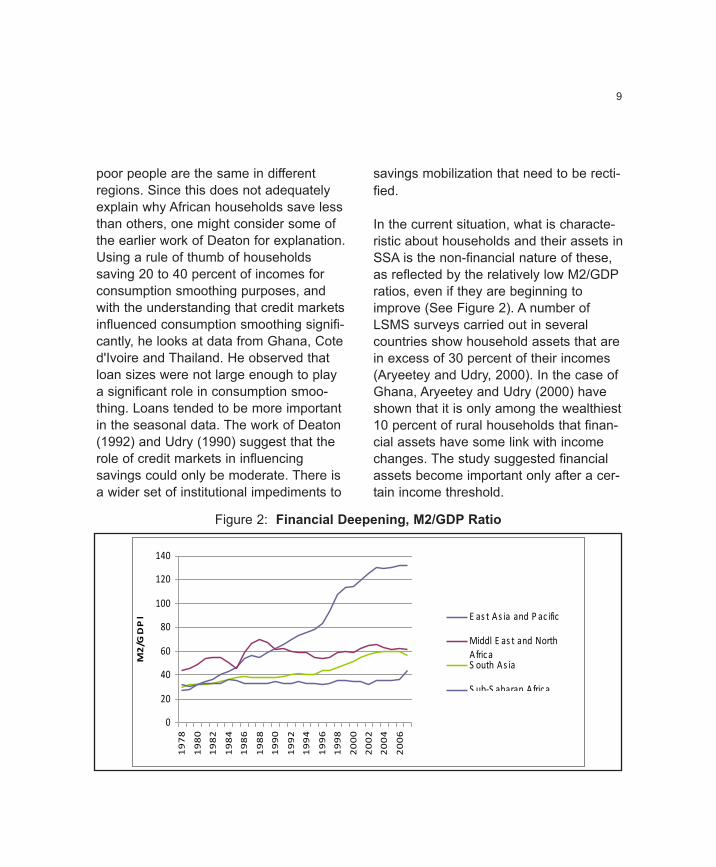

The main problem with domestic resourcemobilization in Africa has been that notenough savings are being generated tofacilitate the required investment(Aryeetey, 2004). Also, the types ofsavings available do not easily makefinancial intermediation possible. Africancountries’ low and stagnant savings rateshave not compared well with those ofAsia, giving Sub-Saharan Africa thelowest savings rate among the developingregions. The most available measure ofsavings performance is the gross domes-tic savings (GDS). GDS in Sub-SaharanAfrica amounted to 17.6 percent of GDPin 2006, compared with 26.0 percent inSouth Asia, 24.0 percent in Latin Americaand the Caribbean, and nearly 42.9 per-cent in East Asia and Pacific countries(World Bank, 2007) (See Figure 1). Themuch lower level of savings in Sub-Saharan Africa may explain much of thelower level of economic activity in theregion and the slower pace of growth.

2.1 Trends in Savings Mobilization

But the above low figures for SSA hideimportant differences across the region.

While gross domestic savings in someparts of Africa were as low as -20 percentof GDP in 2005 (e.g., in Eritrea and SaoTome and Principe), indicating dissavings,in other places, including Algeria and theRepublic of Congo, domestic savingsrates were as high as 50 percent of GDP(World Bank, 2006). Angola experiencedan average rate of growth for domesticsavings of 28 percent in 1980-96 andGabon with an average saving rate of 38percent for the same period, and theserose to 40.6 percent and 55.4 percentrespectively in 2007. The very high ratesfor the major oil exporting countries is notsurprising in a region where most coun-tries have domestic saving rates of lessthan 15 percent of GDP. Not surprisingly,in these high savings economies, thepublic sector tends to dominate savings.

The savings rate for Sub-Saharan Africahas broadly evolved over the years in thefollowing pattern. From 1960 to 1974, itincreased steadily from 17.5 percent to24.3 percent of GDP (World Bank, 2007).It then experienced much higher volatilitybefore reaching its highest rate (nearly 26percent) in 1980. In 1992, savings inAfrica basically collapsed, reaching an all-time low of 15 percent and generallyremained that way, albeit with a slightrecovery at 17.6 percent in 2005 (WorldBank, 2007). Table 1 below shows thetrend in saving rates in SSA for the period2000-2005, with a majority of the coun-tries showing very low rates.

4

The savings trends for SSA diverge signi-ficantly from that of other developingregions, especially after 1980. While SSA

saving rates have fallen, Latin America’shave stagnated and East Asia’s rateshave soared (See Figure 1).

5

Figure 1: Gross domestic savings by developing regions, 1960-2004(Percentage of GDP)

Source: World Development Indicators, 2007.

Source: World Development Indicators, 2007.

Table 1: Distribution of savings rates in Africa, 2000-2005(Number of countries)

11 14 13 7 5

Negative 0-10-% of GDP 10-20-% of GDP 20-30% of GDP Over 30% of GDP

Aside from saving rates, stability overtime is crucial for smooth and predictableinvestment, and Africa again fares worsethan other developing regions in this area.A major reason for this is the volatility ofthe sources of income, which is higher inAfrica than in other developing regions,due mainly to exogenous shocks relatedto primary commodity dependence.

By and large, these trends reflect the eco-nomic performance of these regions overthe past four decades or so. It is thereforenot surprising that in Asia, most of thecountries that were on a similar economicfooting as Sub-Saharan countries in theearly 1960s, have made significant stridesin their development, while Sub-SaharanAfrica has deteriorated.

Explaining the Low Saving Ratesin Africa

A number of studies have been conductedin the last decade to explain low savingsrates in Africa. There are those that havebeen done using macroeconometricapproaches and the more micro-levelanalysis. An example of some of the ear-lier broad econometric work is that carriedout by Hadjimichael et.al. (1995) who sug-gested that sustained reform programsand positive per capita growth generallyled to faster growth of private savings. Inthose faster growing economies that theylooked at, they measured a cumulativechange of 5.7 percentage points between

1986 and 1993 of private savings as ashare of GDP compared to –2.7 percenta-ge points for slower reforming and gro-wing economies in the region. Eventhough they argued that the maintenanceof structural adjustment policies led toimprovements in macroeconomicbalances and low inflation, a number ofother studies (including Nissanke andAryeetey, 1998), found little evidence ofreforms having such an impact on savingsperformance. It is also interesting that theWorld Bank (1994) had earlier noted thatthere was little evidence that economicreforms in many African countries hadhad a major impact on savings andinvestments. Over the reform period, onlya couple of serious reformers saw somemodest improvements in their savingsperformance.

The Hadjimichael et.al (1995) study alsosuggested that increased official inflowsled to improvements in governmentsavings and investment as well as fastergrowth in private savings and investmentin several of those countries. They usedtheir empirical testing of the relationshipbetween macroeconomic performanceand growth, savings and investment tosuggest that a conducive macroeconomicenvironment was necessary for growth,savings and investment. Despite whatthey saw as significant improvements inthe countries they studied in SSA, theyacknowledged that savings and invest-ment ratios in the region were “significant-

6

ly lower than for other developing coun-tries and still too low to support a sustai-nable expansion in output and employ-ment” (pp.27).

Other macro studies include that ofMwega (1997). He did a comparative ana-lysis using life-cycle and permanent inco-me intertemporal models of average pri-vate savings rates in 33 countries, inclu-ding 15 African countries and found evi-dence that saving rates were generallylower than in other developing countries.He found a positive and highly significantcoefficient on per capita income whichdecreased as income increased, a positi-ve and highly significant coefficient ongrowth of per capita income, a negativeand highly significant coefficient on publicsaving, a positive and highly significantcoefficient on the degree of financialdepth (M2/GDP), and an insignificantcoefficient on financial constraints.Focusing on the African countries alone,Mwega (1997) shows that private savingsis determined largely by the dependencyratio, level of per capita income, economicgrowth, terms of trade and public savingsrates. His conclusion generally was thatthe low savings rate in Africa was aconsequence of both the private savingsfunction and initial economic conditions.

It is generally anticipated that terms oftrade shocks will affect savings, and thisis important to SSA, particularly in thistime of a global crisis. Interestingly, the

study by Hadjimichael et.al (1995) did notfind any significant relationship betweenchanges in the terms of trade andsavings. Mwega (1997) on the other handfound a significant negative relationshipbetween terms of trade and savings.

The World Bank’s (1994) study suggestedthat savings performance in SSA was dri-ven largely by the performance of publicsavings. This was quite different from thesituation that Srinivasan (1993) had repor-ted about Asia. Following this observation,there have been discussions of whetherthe public sector tends to crowd out theprivate sector in SSA. Kelly and Mavrotas(2003) modeled the relationship betweenpublic and private savings and suggestedthat the two have a relationship thatreflects Ricardian equivalence effectsalong the lines of Barro (1974) andFeldstein (1982). This finding is differentfrom that by Hadjimichael et.al. (1995)who observed a strong positive relation-ship between them. In this case it is sug-gested that public investments generateprivate capital accumulation and econo-mic growth through positive externalities.Aryeetey (2004) has argued that publicsavings and private savings have differenteffects on investments and this is moreimportant in terms of employment crea-tion. Considering that both are low inSSA, the desirable thing at this stage inSSA development is to have both growingand having their differentiated impacts oninvestment and employment.

7

It is usual to consider the link betweendemographic characteristics and savingsby incorporating the dependency ratio intoa model. Hadjimichael et.al. (1995) obser-ved a strong negative relationship bet-ween the two. Mwega (1997) also foundthat the dependency ratio had a signifi-cantly negative effect on private savings.It is reasonable however to argue that theissue of the link between the two is stillfar from settled.

The study by Nissanke and Aryeetey(1998) presents one of the most compre-hensive assessments of savings mobiliza-tion following liberalization of the financialsystem. The fact that reforms did not leadto enhanced savings mobilization hasalso been observed by many others. Theylead to a general conclusion that structu-ral and institutional issues are very impor-tant for savings mobilization. Kelly andMavrotas (2003) made the point that dra-wing any specific conclusions about howliberalization affects savings mobilizationis futile since one has to consider thefinancial sector and its structures in totali-ty. Nissanke and Aryeetey (1998) havediscussed a number of structural and ins-titutional constraints to the mobilization ofsavings, particularly from poor house-holds. They suggest that financial marketsin Africa are highly fragmented and thatthe high transaction costs for economicagents trying to move across differentsegments act as a disincentive in savingsmobilization. They relate these structural

features to various institutional constraintsof the formal sector, noting, for example,that savings mobilization from rural areasis very costly and that banks in Africahave not been designed to counter thisthrough innovative approaches in savingsmobilization. The answer does not simplylie in having more rural outlets for com-mercial banks, as they indicate that ruralsavings mobilization is not necessarilypositively correlated with the number ofbank outlets. Indeed, many of the ruraloutlets turn out to be unsustainable,hence the tendency to close many ofthem with financial sector reforms.Nissanke and Aryeetey (1998) suggestthat there have been few innovativesavings instruments developed with aview to reaching untapped segments ofthe financial market.

There have also been quite a fewattempts to explain savings behaviorthrough micro analysis. Deaton (1997)worked on the life-cycle hypothesis usingIvorian LSS and Thai household data, loo-king at consumption and saving bycohorts. They showed hardly any eviden-ce of life-cycle considerations for saving.His work showed that over the long-term,consumption and income were closelycorrelated. He observed consumption tobe tracking income and leaving no evi-dence of life-cycle saving in Cote d'Ivoire.This observation is corroborated by thework of Collins (1991) whose work sug-gests that the motivations to save among

8

poor people are the same in differentregions. Since this does not adequatelyexplain why African households save lessthan others, one might consider some ofthe earlier work of Deaton for explanation.Using a rule of thumb of householdssaving 20 to 40 percent of incomes forconsumption smoothing purposes, andwith the understanding that credit marketsinfluenced consumption smoothing signifi-cantly, he looks at data from Ghana, Coted'Ivoire and Thailand. He observed thatloan sizes were not large enough to playa significant role in consumption smoo-thing. Loans tended to be more importantin the seasonal data. The work of Deaton(1992) and Udry (1990) suggest that therole of credit markets in influencingsavings could only be moderate. There isa wider set of institutional impediments to

savings mobilization that need to be recti-fied.

In the current situation, what is characte-ristic about households and their assets inSSA is the non-financial nature of these,as reflected by the relatively low M2/GDPratios, even if they are beginning toimprove (See Figure 2). A number ofLSMS surveys carried out in severalcountries show household assets that arein excess of 30 percent of their incomes(Aryeetey and Udry, 2000). In the case ofGhana, Aryeetey and Udry (2000) haveshown that it is only among the wealthiest10 percent of rural households that finan-cial assets have some link with incomechanges. The study suggested financialassets become important only after a cer-tain income threshold.

9

0

20

40

60

80

100

120

140

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

M2/G

DPl E as t As ia and P ac ific

Middl E as t and NorthAfricaS outh As ia

S ub-S aharan Africa

Figure 2: Financial Deepening, M2/GDP Ratio

2.2 Credit Availability and DomesticInvestment in SSA

The last two decades have seen a gro-wing reliance by African countries onexternal resources to finance investments.With Gross Domestic Savings at over 25percent of GDP in 1980 and GrossDomestic Investment at 22 percent ofGDP, there was hardly a gap to be filled.Foreign direct investment came to only0.7 percent of GDP. The East Asia andPacific region invested 32 percent of GDPand saved 30 percent of GDP at the time.As savings figures have dropped in SSA,

they have left a growing gap to be filledby foreign resources. But the period hasalso seen a significant decline in invest-ments as shown by data on gross fixedcapital formation in Table 2 below. Thereality is that SSA countries are not inves-ting as much as is necessary and most ofthe investment done has, for a long time,been with public resources. The verysignificant use of public investment wouldalso explain why employment generationhas not been a major outcome of theassociated growth processes (Ndulu etal., 2008).

10

Source: African Development Indicators, 2007-08, Tunis

Table 2: Gross Fixed Capital Formation/GDPYear Sub-Saharan Africa

1980199419951996199719981999200020012002200320042005

1980-891990-992000-05

22.217.918.418.217.719

18.417

17.918.218.619.519.418.917.718.9

Not surprisingly the low rate of invest-ments, especially private investment, isattributed, even if partially only, to thedearth of credit to the private sector inSSA countries (Honohan and Beck,2007). Honohan and Beck (2007) showthat by 2005 the claims that banks in SSAhad on the private sector was less than30 percent of their total assets comparedto more than 60 percent in East Asia andthe Pacific and also in South Asia. In LatinAmerica this was almost 70 percent oftotal assets. The ratio of private credit toGDP was only about 18 percent in SSA in2005. In South Asia this was as much as30 percent. For the low-income countriesin SSA the ratio of private credit to GDPfalls to as low as 11 percent (Honohanand Beck, 2007). African financial sys-tems are reported to show a low interme-diation ratio. This means they have a lowshare of deposits going into private sectorcredit.

Honohan and Beck (2007) also show thateven though all indicators of financialdepth indicate SSA to have the lowestachievements, there are signs that thesehave improved significantly in the lastdecade. The median value of real privatesector credit has doubled in the period. Asmany as 80 percent of all SSA countriesshowed this improvement, and in Ghanacredit to the private sector moved from 14percent of GDP in 2000 to 27.4 percent in2007. Honohan and Beck (2007) have

suggested that the significant improve-ments in many countries suggest thatthere is a lot of room for further improve-ment simply by restructuring institutions.They use the Tanzanian situation toexemplify the potential after credit to theprivate sector moved up from 2.8 percentin 1996 to about 10 percent in 2005 follo-wing a restructuring of the largest bank.Clearly, despite the improvements there isstill a significant gap between the perfor-mance of African banks and what hasbeen achieved in other developingregions.

There are a number of explanations forthe low level of credit to the private sector.These have been studied several timesand many reasons have been assignedfor the situation. Most of the explanationsare related to the perceived high risk envi-ronment of SSA economies. Nissankeand Aryeetey (2008) have explained thatwith the fragmented nature of the financialsystems, the flow of information acrossthe different units is very limited thusmaking it difficult and costly for banks andother lenders to acquire the necessaryuseful information about potential clients.The fragmentation makes banking uncom-petitive and inefficient. Information asym-metry is seen to be at the bottom of alllending decision making. Honohan andBeck (2007) explain that the problems oflow competition and efficiency also havean effect on the interest rate margins,

11

costs and profitability of banks. Banks areable to raise their profits largely by avoi-ding small borrowers, about whom verylittle information may be found, and thenconcentrate on lending to public entitiesand other high net worth customers atpremium rates.

But there have also been macroeconomicfactors. Governments have used variousmonetary policy tools to control their eco-nomies. Borrowing extensively from thebanking system to finance growing defi-cits has always pushed up interest ratesthat have effectively led to a rationing ofcredit to the private sector. But, untilrecently, the steady borrowing in manycountries also contributed to rapid deterio-ration in inflation conditions which contri-buted to banks further raising their baserates.

In sum, SSA financial systems have a lotof difficulty mobilizing deposits andthrough intermediation, making theseavailable to potential investors. The resultis that very little of such investment inSSA is done with bank credit or otherforms of credit.

2.3 Taxation and Public Investments

Tax revenue is a major domestic financialresource in all economies. Indeed taxesaccount for most of government revenuein the majority of African countries, but

they do not generate enough, particularlywhen compared to other regions. Theamount of tax revenue as a percentage ofGDP in Africa was 22 percent in 2002(World Bank, 2005), which was far lowerthan the average for developed countries.The tax ratio is considerably lower in Sub-Saharan Africa (20 percent) than in NorthAfrica (25 percent). Furthermore, thereare major differences among countries inthe region with regard to their tax perfor-mance. Tax as a share of GDP in 2002ranged from more than 38 percent inAlgeria and Angola to less than 10 per-cent in Chad, Niger and Sudan (WorldBank, 2005). The tax-to-GDP ratio in agiven economy is broadly determined bya set of structural features such as theper capita income, urbanization, literacy,the shares of the industrial, agriculturaland mining sectors, as well as the level oftrade. In Sub-Saharan Africa, the maindeterminants of the tax-to-GDP ratio havebeen observed to be per capita income,trade levels, and the shares of agricultureand mining in the economy (World Bank,2005). Per capita income reflects not onlythe taxable capacity of the population; italso serves as an indicator for generaldevelopment in an economy.

A recent study by Le et.al (2008) providesan interesting insight into how Africancountries are doing in the area of taxmobilization. They employed a cross-country approach to estimate tax capacity

12

from a sample of 104 countries, includingseveral African countries, for the period1994-2003. They used their estimationresults as benchmarks to comparetaxable capacity and tax effort in the diffe-rent countries. They defined taxable capa-city as the predicted tax-GDP ratio thatcould be estimated with the regression,after taking into account a country’s speci-fic economic, demographic, and institutio-nal features. They also defined tax effortas an index of the ratio between the shareof the actual tax collection in grossdomestic product and the predictedtaxable capacity. Following this they clas-sified countries into four groups by theirlevel of actual tax collection and attainedtax effort(2). The analysis provides guidan-ce for countries with various levels of taxcollection and tax effort.

Interestingly most of the African countriesin the sample fell into two categories,namely Group 1: Low Collection and LowEffort and Group 2: Low Collection andHigh Effort. Countries in the first groupwere mainly from the developing world,and about 75 percent of them were ran-ked as low-income or lower-middle-inco-me countries. The majority of them wereobserved to have several problems inboth tax policy and tax administration.Some of them including Cameroon and

Madagascar were mentioned as having“their tax policies riddled with overly com-plex structures and multiple —largely ad-hoc— incentives that narrow the alreadylimited tax base, create more loopholesfor tax avoidance and evasion, intensifythe public perception of unfairness oftaxes, and generate opportunity for cor-ruption”. The researchers report thatsome countries have opted to retaingenerous tax incentives to compensatefor their relatively high statutory rates oncorporate income in order to attract priva-te foreign capital. An example mentionedin the study is Cameroon but this couldeasily have been many other countries.The researchers suggest that “such com-plex tax regimes combined with the exis-ting weak revenue administration capacityhave led to chronic low tax collection athigh administrative and compliancecosts”.

For the countries listed in the LowCollection and High Effort group, there isstill a large number of African countries,including Cote d’Ivoire, Ethiopia, Ghana,Kenya, Senegal, Uganda and Zambia. Leet.al (2008) noted that in these countries,“administration capacity is notably low andthe tax regime is highly unstable. Theyhave low collections, whereas high taxefforts are usually achieved by either

13

(2) The classification was based on the benchmark of the global average of tax collection and a tax effort indexof 1 when tax collection is exactly the same as the estimated taxable capacity.

enforcing easy taxes (particular tradetaxes) or imposing high taxes on the for-mal sector, or both. Uganda is the case inpoint”. Uganda’s tax system is reported tobe one that could be considered as asignificant impediment to investment andformality (Chen et al., 2001). It is notedthat revenue collection has stagnated atabout 12 percent since the early 2000s. Indescribing the recent tax policy reformstrategies, they are noted to have beenlargely inconsistent with an increase ofstatutory rates in some major taxes at thesame time as an introduction of newexemptions and zero rates in the VAT.Uganda is reported to rely heavily on dis-torting trade taxes. As in many othercountries “a high tax burden is imposedon a limited number of taxpayers, andmedium sized firms which already beardisproportionately high share of taxes(Gauthier et al., 2006).

There have been a number of studies intowhy taxation is difficult in African econo-mies. Fjeldstad and Rakner (2003) haveargued that “most Sub-Saharan countriesface a trilemma with respect to taxation:(1) There is an urgent and obvious needfor more revenues to enable resourcepoor states to provide and maintain eventhe most basic public services. (2) Thereality is, however, that those with politicalpower and economic ability are few anddo not want to pay tax. (3) Moreover,those without political power are many,

have almost nothing to tax, and do alsoresist paying taxes”. In light of thesegeneral difficulties, the challenge thatgovernments in the region face is how “toraise domestic revenues from consentingcitizens in poor and increasingly openeconomies”. Fjelstad and Rakner (2003)believe that as governments increasinglybecome elected they have to confront the“hard choices about taxation”. In weakdemocracies it is very difficult to introducenew taxes without fear of difficult politicalrepercussions.

Fjeldstad and Rakner (2003) further sug-gest that tax systems may be assessedusing a number of criteria, including theability to raise revenues, effects on eco-nomic efficiency, equity implications andadministrative feasibility. Based on thesecriteria they assess tax systems in manyAfrican countries to be scoring low onmost. They argue that the weaknessesare partially derived from the nature of thereforms that have been pursued in light ofstructural adjustment. “In most cases thisinvolves the introduction of measures to(broaden) the tax base while simulta-neously flattening the tax rates”, just as isgenerally the case in more advancedcountries. It is argued that the socio-cultu-ral characteristics of environments do notappear to have been taken into account inthese reforms. The reforms have general-ly involved the following:

14

• introduction of the value-added tax;• lower personal and corporate income

taxes;• simplification of the tax bands and

broadening of the bases for personaland corporate income taxes;

• reduction of import duties andsimplification of the rate structure;

• simplification of the excise dutystructure; and

• abolition of export taxes.

In spite of the reforms, it is assessed thattax systems in many African countriescurrently “show an excessive number ofdifferent taxes with rate structures that aredifficult for taxpayers to understand”.Fjelstad and Rakner (2003) suggest thatthe language used in tax laws is usuallyconfusing and there are no manuals to beconsulted. The consequence is that theygenerally lead to considerable discretiona-ry powers for tax enforcers, includingseveral related to the provision of taxexemptions, determination of tax liabili-ties, selection of audits, litigation, etc.They further suggest that a number ofadministrative procedures, including theprocedures for reporting tax revenues,lack transparency and are difficult tomonitor. The result is that tax systems arecomplicated and lack transparency. Theseviews about the tax systems in SSA arenot very different from those of Adam andO’Connell (1997) who have suggestedthat tax distortions have been high and

volatile in Africa. They have pointed outthat poor systems influence the allocationof national wealth and they can reduceboth the level and productivity of domesticinvestment. For them, however, the poorcomposition of domestic investment maybe more important in explaining poorgrowth in the region than the level ofdomestic investment.

The difficulties of the tax system are notonly found at the national level. They areeven more difficult at the local govern-ment level. In the study by Fjelstad andRakner (2003) they conclude that manylocal taxes tend to have “a distortingeffect on resource allocation decisions,and an inhibiting effect on the start- up ofnew enterprises”. They argue that theseeffects come about as a result of theconsiderable variation in effective taxrates between different goods that are tra-ded. They indicate that license fees tendto be too high for small enterprises thatare beginning operations, and this is amajor disincentive for local businesses.Local taxes are assessed to lead to ahigher tax burden on the poor than on thenon-poor. A difficult local government taxsystem is not only costly but is seen toease corruption and encourage mismana-gement.

Adam and O’Connell (1997) have lookedat how taxes in SSA impact different sec-tors of the economy. They observe that

15

while taxes on international trade areadministratively easy to collect they tendto make up a declining share of total reve-nues as per capita income rises.International trade taxes accounted for anaverage of 35 percent of total revenues inthe mid-1980s, as compared with 23 and17 percent in Asia and Latin America/Caribbean. SSA has been associated withhigh average tax rates on African trade.Thus, despite declining tariffs in the wakeof trade liberalization in the mid-1980s,the median tax rate for SSA still exceededthat for other developing countries by 50percent. Adam and O’Connell (1997) alsoargue that, real exchange rate overvalua-tion provides a measure of the implicittaxation of export-oriented production infavor of production for the home market.“The overvaluation “tax” on exporters isadditional to that implied by low producerprices paid by monopsony national mar-keting boards.”

Another area of major taxation is the agri-cultural sector which has been assessedby Adam and O’Connell (1997) to havehas also faced an “unusually heavy taxburden in some African countries”. Schiffand Valdes (1991) reported from a studyof 26 commodities that a combination ofexport taxes, low producer prices, protec-tion of manufactured inputs, and exchan-ge rate overvaluation produced an avera-ge nominal protection rate of -52 percentfor the three African countries in the

sample (Cote d’Ivoire, Ghana andZambia). For the other 15 developingcountries in the sample, this was only -30percent.

In effect, the capacity of African econo-mies to mobilize domestic resourcesthrough taxation is not only hampered bywidespread poverty, but largely a conse-quence of institutional failures that needto be addressed.

3. The Financial Crisis andDomestic ResourceMobilization in Africa

The discussion in section three will sug-gest that the performance of savingsmobilization and lending by banks in mostAfrican countries have relatively little to dowith the performance of global financialmarkets, but more with how the marketsin Africa are organized. But before the cri-sis began, the global financial marketswere beginning to exert some influenceon resource mobilization in SSA byincreasingly providing standards thatcould be used to measure the performan-ce of financial institutions. For example, inthe wake of the Asian crisis in 1997, theresulting tightening of standards andregulations in financial markets throu-ghout the world was also extended tofinancial institutions in SSA. The adoption

16

of the International Financial ReportingStandards (IFSR) by banks in the regionwas significant in this regard. After theimprovements in the regulatory environ-ment for African institutions, there emer-ged the beginnings of interaction betweenthe financial markets of African econo-mies and those in Europe. A few Africangovernments began to issue sovereignbonds in 2007 that were assigned throughconsortia of local and international finan-cial institutions, and this development wasgenerally seen as marking a new entran-ce onto the global financial system. Whilethat development may have been curtai-led as a result of the global financial cri-sis, even more important was the fact thatbanking in Africa was being modeledincreasingly along those of banks inadvanced economies. This may be lostwith the financial crisis. This section of thepaper discusses what developments therehave been in savings mobilization andlending by African banking systems sincethe crisis broke, using developments froma handful of African banking systems forillustrative purposes only.

3.1 The Crisis and SavingsMobilization

In the absence of aggregated data thatwill show the flow of savings in the periodsince the crisis broke the paper relieshere on data and reports from a few

African central banks with relevant infor-mation on the performance of savings.

The Bank of Ghana (2009) has indicatedthat at the end of the last quarter of 2008,total deposits of the banking system stoodat GH¢6,949 million which was 65 percentof total liabilities compared to 63 percentin 2007. Also in the last quarter of 2008there was an increase of 11.4 percent inthe total deposits of the banking systemover the previous quarter’s figures andthis compares with an increase of 14.3percent over the same period in 2007.The difference in the rate of increase inthe last quarter of both years is judged tobe not statistically significant. What isinteresting about the growth of deposits inthe Ghanaian banking system in 2008 isthat it occurred when the share of totalborrowings in the banks’ liabilities decli-ned by 0.8 percentage point. The share ofshareholders’ funds in the liabilities didnot change in the period, remaining at10.4 percent. Thus, deposits have remai-ned fairly robust even if the banking sys-tem’s holding of deposits is not verywidespread.

In Nigeria, the Monetary Policy Commit-tee of the Central Bank of Nigeria met inDecember 2008 and reported that broadmoney growth had moderated somewhatin the last quarter based on figures up tothe end of October 2008. In Kenya, theGovernor of central bank has recently

17

18

reported that the global crisis has notaffected significantly the performance ofthe banking system, and so indeed havesimilar reports from the Bank of Tanzania.It is safe to conclude that central banks inthe region do not anticipate any majorchanges in the savings outcomes as aresult of the crisis.

It is not surprising that savings outcomesare not expected to change. This isbecause, as earlier pointed out, theissues relating to savings and depositsare more of an institutional and structuralnature, after having dealt with many of thepolicy issues through financial sectorreform programs. The factors that impactmost on savings have not been affectedyet by the global crisis, and this situationwill not change much in the very nearfuture. What this means is that the lowsavings in the region cannot be immedia-tely blamed on the crisis directly. On theother hand if it should lead to deteriora-tion of household incomes in the future,as well as in the profits of private enter-prises, there is every reason to expectthat the holding of financial assets will bereduced.

3.2 The Financial Crisis and CreditAvailability

The picture with the availability of credit isquite similar to that of deposits mobiliza-tion. There is no real indication of a dis-

cernible change in the usual pattern. Forinstance, the Bank of Ghana has reportedthat the last three months of 2008 saw atightening of credit supply by banks. Morethan 35 percent of banks reported suchtightening in December, compared to justover 25 percent in October. The main rea-son for the new stance was the rising costof funds and the changing expectationsabout economic activity in the country.The data showed that in the last quarterof 2008, the availability of credit to smalland medium sized enterprises increasedbut the increase was smaller than it wasin the third quarter. The difference was,however marginal.

Unlike SMEs, credit to households forhouse purchase in Ghana declined signifi-cantly in the last quarter of 2008 and thiswas attributed by banks to concernsabout the economic outlook. Even thoughhouseholds received more consumer cre-dit in the last quarter, the increase wasless than had been observed in the thirdand earlier quarters in the year. The cen-tral bank in Ghana argues that the neteasing of consumer credit could be attri-buted to competition among banks. Whatis also interesting is the fact that the num-ber of applications being presented tobanks for loans also went down in the lastquarter, particularly for SMEs. On theother hand larger enterprises submittedmore applications in the last quarter thanthey had previously done. Not surprisin-

gly, the demand for long term loans drop-ped significantly in the last quarter. Whatthe above picture signifies is a mixed bagof developments with no clear patternemerging. While the drop in demand forlong-term credit may be significant, it isassociated more with firms’ views aboutglobal demand for their products asexporters than with the global financial cri-sis itself. Many of these were exportingfirms, thus confirming the idea that anylinks between domestic resource mobili-zation and the global financial crisis worksmore directly through the changes in thereal economy worldwide. It is also note-worthy that interest rates began to risemuch faster in the last quarter largely inresponse to worsening macroeconomicconditions.

In Kenya, the flow of credit to the privatesector increased by 7.4 percent in thethird quarter of 2008 but this dropped to2.5 percent in the last quarter. In thesecond quarter the growth had been 5.2percent. The ups and downs in the flow in2008 are not comparable to the situationin 2007. In the last quarter of 2007 thegrowth of credit to the private sector wasas high as 9.6 percent compared to thethird quarter increase of 3.9 percent. The2007 trends were more like what hadbeen observed in earlier years. Thus,clearly the sharp drop in credit flow to theprivate sector in the last quarter of 2008stood out.

For many African countries, the storyappears to be quite mixed on the creditfront. Banks appear to have generallyreduced credit supply in the last quarter of2008, in particular for SMEs and house-holds as they expected more difficult eco-nomic conditions in the face of a growingglobal financial crisis. This is in spite ofthe fact that households dominate thereceipt of credit from the banking sys-tems.

In Nigeria, the report of the MonetaryPolicy Committee of the Central Bank ofNigeria in December 2008 observed thatthe “growth in M2 has continued to be dri-ven mainly by credit to the core privatesector, which grew by 52.5 percent (or63.3 percent annualized) as at end-October 2008”. Again what is referred toas the core private sector is the group oflarger enterprises that continued to recei-ve credit in other countries also. Thegrowth in credit was also reflected by thelarger profitability of banks in Nigeria asthe MPC of the central bank noted that“whereas many banks abroad have beenmaking losses and faced with potentialbankruptcies, Nigerian banks have in factbeen posting profits”.

3.3 The Financial Crisis and TaxRevenues

The situation with tax revenues in mostcountries is not expected to have chan-

19

ged much in the wake of the crisis but thefinancial crisis will affect tax revenues inthe medium term by affecting their deter-minants. Generally, tax revenues areexpected to fall given that the total reve-nues depend on the level of income andeconomic activities. The financial crisis isexpected to reduce Africa’s GDP growthto only 3.25 percent in 2009, depresstrade and diminish investment by corpora-te entities. This means that if tax rates(income tax rate, consumption tax rate,corporate tax rate and trade tax rate)remain at the current levels, the amountof revenue collection for 2009 and beyondby governments would decline.

The implication is that in the face of theglobal financial crisis, many African coun-tries will have to significantly improve theirtax effort in order to maintain the samelevel of revenue collection. More impor-tantly, the countries will have to ensurehigh efficiency of government spendingsince it is an essential part of makingdomestic resources the engine of deve-lopment. With the financial crisis in fullswing, the opportunity cost of each unit ofspending is very high.

In Ghana, figures published by thegovernment suggest that tax revenueexceeded the target significantly. Total taxrevenue in 2008 was about 24.4 percentof GDP and was almost 30 percent higherthan in 2007. Of this, direct taxes, made

up of personal income tax, company tax,etc. constituted 29 percent of total taxrevenue and exceeded the target by 11.7percent. Government attributed the betterthan expected performance to the intro-duction of a new pay-as-you-earn arran-gement for personal income taxes.Interestingly, international trade taxes yiel-ded an amount that was less than the tar-get but exceeded the figure for 2007.Other taxes that saw drops in their intakeinclude petroleum tax that yielded lessthan the outturn for 2007 and was 21.2percent less than budgeted. This hasbeen attributed to a reduction in the ratein the wake of the petroleum price risesearlier.

In Kenya, tax revenue increased by 14.3percent between 2007 and 2008. Theincrease was driven largely by thealmost18 percent increase in income tax.The slowest growth came from importduties and excise duties. It stands to rea-son that incomes had not been necessari-ly affected in 2008 and this would explainwhy income taxes rose significantly in theabsence of any changes in the rates.

As earlier suggested, the main problemwith tax systems in Africa remains the factthat the governments are focusing onreforms that ensure larger and larger col-lections from the same sources and littleeffort to enlarge the net and to rationalizethe taxes.

20

4. African Responses toGlobal Financial Crisis andImplications for DomesticResource Mobilization

Sub-Saharan African governments gene-rally recognize the fact that they are likelyto be affected significantly by the fact thatwhat began as a financial crisis has tur-ned into a significant global economic cri-sis and sharp drops in demand. The effecton most domestic resources, as seenabove, will come largely through indirectchannels or not through the first-roundeffects. But African institutions have gene-rally recognized the point that when theimpact is felt in the real sectors of theireconomies, the effects could be long-las-ting and have greater consequences forlong-term growth and development thanwould be the case elsewhere.

At the meeting of the Committee ofFinance Ministers and Central BankGovernors held in Cape Town in January2009, the point was made that tradereceipts would suffer significantly asimporters of African goods went into arecession. Additionally trade financingwas expected to decline sharply as theprivate agents who handled and financedtrade experienced increasing difficulty inaccessing their financiers. Private foreigninvestments were also expected to decli-ne significantly as such investors found it

more and more difficult to access funds inEuropean and US banks and other capitalmarkets. It was recognized that remit-tances will decline significantly as manymore African migrants lost their jobs in thedownsizing and restructuring of Europeanand US companies. It was anticipated thatthe developed world might adopt protec-tionist positions and also renege on com-mitments to provide development assis-tance. The meeting was told that “Themajor concern in terms of the impact ofthe financial crisis on the real economy isthe adverse effect on domestic demand,namely consumption, investment, exportsand government spending. Any substan-tial decline in domestic demand will redu-ce income which will in turn affect employ-ment and consequently growth”. It wasanticipated that any worsening of thesituation would have negative conse-quences for poverty reduction.

One of the meeting’s major recommenda-tions was for African governments toincreasingly turn to the use of domesticresources. It was noted that the low levelof financial development necessitatedfinancial sector and fiscal reforms in orderto raise the levels of domestic resourcemobilization. Such a reform was regardedto be essential to improving the internalconditions for mobilizing resources fordevelopment from within. The ministersconsidered the need for the establishmentof property rights, contract enforcement

21

mechanisms, and laws ensuring creditorsrights. Finding ways to make bank super-vision staff supportive of SME lendingwere suggested in view of the likelyimpact on employment generation. Otherissues discussed included the need for anefficient domestic bond market, broade-ning of the tax base as well as the intro-duction of funded pension schemes. Itwas further suggested that public financialmanagement should be a part of the pac-kage for mobilizing domestic resources asit leads to greater resource efficiency.

Since that meeting, there have been anumber of conferences and meetingsboth at the regional level and at countrylevels to discuss possible ways of dealingwith the issues. The most notable of thesehas been the adjustment of the conferen-ce organized by the Government ofTanzania and the International MonetaryFund in Dar es Salaam to discuss thelong term growth options for Africa toconsider also more pressing matters inthe light of the financial crisis and globalrecession. As at other meetings, the needfor greater attention to domestic resourcemobilization was noted.

What is problematic for many SSA coun-tries is the fact that the shock to their eco-nomies from the crisis is occurring at atime when they have significant macroe-conomic difficulties. In Ghana, forexample, a deficit of 14.9 percent of GDP

has been large enough to derail most ofthe gains from faster growth experiencedin the pervious six years. Inflation hasjumped from 12 percent from two yearsago to more than 23 percent. While thenew budget for 2009 seeks to tackle thesize of the deficit by reducing it to 9.4 per-cent of GDP in 2009, the question thisleaves is what will such a large reductionin public spending mean for aggregatedemand at a time when the need to crea-te employment is probably more acutethan ever before. This epitomizes thedilemma that many SSA governmentsface. The challenge is how to stabilize theeconomies adequately while stimulatingparts of the economy to yield improve-ments in production and productivity andalso employ more and more people.

5. Moving Forward: MobilizingAdditional DomesticResources

As noted earlier, it has long been recogni-zed that there are significant tradeoffsbetween domestic resource mobilizationand other sources of financing develop-ment such as FDI, trade promotion, aid,etc. While they ideally may complementone another, the various sources of fun-ding could also compete with another forattention and policy space, leading to thesituation in which initiatives in one area

22

may impact negatively on other areas. Forexample, high levels of aid may negative-ly impact domestic resource mobilizationby reducing recipient countries’ tax effort.In fact, the literature on the negativeeffect of increasing aid on tax effort indeveloping countries continues to grow(see Adam and O’Connell, 1997).

Unbridled trade liberalization is expectedto accelerate competitiveness and increa-se export earnings, though it has oftenresulted in reduced production and exportcapacities, even in the medium-term,apart from reducing government reve-nues. This is particularly the case in poorcountries that rely heavily on tariffs as arevenue source. In such countries, only avery small share of revenues lost – due totariff reduction – have been offset bywider indirect taxation instruments, suchas the VAT.

There are also potential tradeoffs bet-ween domestic resource mobilization anda proactive policy to attract FDI or stimu-late investment more generally, if suchefforts include tax holidays, reduced royal-ties and other incentives for foreign inves-tors. Poor countries offering such incen-tives incur huge opportunity costs in theform of foregone revenues. As a result,many are renegotiating royalty and reve-nue-sharing arrangements with foreigninvestors to garner a more significantshare of the income generated by FDI.

The need to raise domestic resourcemobilization efforts in Africa has becomevery obvious in view of the fact that thecrisis is expected to depress externalinflows and possibly have a negativeimpact on some domestic resources. Ithowever appears more prudent, especial-ly in the medium to long term, for Africa toexpend much more effort on domesticresource mobilization than on externalinflows which are unreliable, volatile andmay come with many strings attached.The question in this regard is whetherdomestic resource mobilization can ope-rate in a counter-cyclical manner and isthat desirable? Our view tends to be thatdomestic resource mobilization needs tobe pursued in its own right and can becomplemented with external resources,bearing in mind the trade-offs. It is noteasy to increase domestic resources inthe short-term and this reduces thechances for them to be treated counter-cyclically. With an effective system ofdomestic resource mobilization in place, itis easier to cope with short-term interrup-tions in the flow of external resources.

5.1 Enhancing Savings Mobilizationand Lending

The earlier discussions suggest that tryingto boost savings in Africa requires effort totackle the structural and institutional pro-blems associated with savings. The first

23

challenge is how to provide incentives forindividuals and households to hold morefinancial assets.

Making Households and IndividualsHold More Financial Assets

Aryeetey (2004) has noted that agricultu-ral production cycles and the risky envi-ronment within which many people livecreate a need for liquidity. Asset choicereflects returns on different assets, thecovariance structure of risks associatedwith them, liquidity constraints, transactioncosts, and production interactions bet-ween the different assets. The choice mayalso be affected by the cultural, demogra-phic and other socio-economic characte-ristics of communities. This need for liqui-dity puts a premium on relatively liquidassets, often dictated by the seasonalityof agricultural activity and the associatedrural household income.

Interest rates may be important but thedominance of non-financial assets in hou-sehold portfolios may not be a simpleconsequence of low expected returns toholding financial assets. Various studiesof saving in Sub-Saharan Africa havecome up with inconclusive evidence ofhow interest rates influence saving(Mwega et.al. 1990, Oshikoya 1992). It isbelieved that pervasive market failures inSSA make interest rates inappropriatetools for measuring preferences. “Market

failure forces the return on other assets toassume a greater role in asset allocation”(Aryeetey, 2004).

Households and individuals face a num-ber of options as they consider whether ornot to put wealth into particular assets.These come with costs that may be consi-dered to be intrinsic to the transaction, forexample, incomplete information. If thenature of information possessed by depo-sitors and deposit-takers as well ascontract enforcement possibilities on thefinancial markets are different a problemcould result. “If the transaction cost of hol-ding a financial asset is perceived to betoo high because there are no credibleinstitutions, other assets would be given apreference” (Aryeetey, 2004).

Trying to deal with these structural issuescan be costly for governments. The follo-wing may be considered. (See Aryeetey,2004).

• Reduce the risks associated with ruralproduction (e.g., seasonality of rainfall)possibly through improved irrigation andother infrastructure, and technologyapplication. This will reduce significantlythe higher liquidity preference of house-holds, at the same time that incomes goup in the medium term. Credit is oftenuseful for reducing the idiosyncraticrisks of poor households.

24

• Stabilize the macroeconomic environ-ment that ensures that the returns onfinancial assets are relatively stable andpredictable.

• Reduce the transaction costs of holdingfinancial assets. Developing institutionsthat are not too far away from rural hou-seholds and yet are cost-effective is themost sensible thing to do. This is what makes appropriate forms of microfinan-ce essential.

Strengthening the Banking System

The recent study by Honohan and Beck(2007) on “Making Finance Work forAfrica” provides very useful material onhow best the banking system can bemade to facilitate the flow of resources toinvestors and to poor households andsmall businesses. They emphasize theneed for them to contribute to growth andstability, improve contract enforcementand transparency of information and alsohow governments cannot be the source oflong-term funds. They also emphasize theneed for a stable macroeconomic environ-ment.

In pursuing an improvement of the ban-king system’s ability to intermediatefunds, Honohan and Beck (2007) providefor ways to improve bank lending capacityand the enhancement of contract enforce-ment. The role of prudential regulation in

all of this is very much emphasized. Onhow to improve bank lending capacity,they argue that the problem is not a lackof mobilized funds, which is a point thatNissanke and Aryeetey (1998) made adecade earlier. The problem of perceivedliquidity risk is seen to be huge at thesame time as bankers complain of a dear-th of bankable projects. Honohan andBeck (2007) conclude that “lack of banka-bility is likely the more acute and intrac-table problem” (p.74). It would appear thatthe absence of reliable information aboutprojects is one of the main obstacles toidentifying bankable projects. Not beingable to lend takes away the enthusiasm ofbanks to mobilize deposits. A solution thatis proposed for this problem is to set upcredit reference bureaus in various coun-tries that will provide the kind of informa-tion needed to make sound judgments forprojects.

Nissanke and Aryeetey (1998) go wellbeyond the proposals from Honohan andBeck (2007) when they propose that thesolution to the structural and institutionalproblems facing African financial systemscan best be solved using an integratedapproach. They agree that a soundmacroeconomic environment is essentialto get a decent financial system going.They argue that most of the liberalizationpursuits of two decades ago were prema-ture since macroeconomic stability and aprudential regulatory and supervisory fra-

25

mework were missing. They suggestedthat having dealt with these two significantpolicy and institutional developmentissues effort must be made to remove thefragmentation of the financial systems. Indoing that the following are seen to beessential:

1. Measures to deepen financial marketsin the context of alternative institutionalarrangements;

2. Measures to strengthen market-suppor-ting financial infrastructure;

3. A new regulatory and incentive frame-work to advance market integration;

4. Measures to improve the financial tech-nology of both informal and formalfinance to widen the scope of their ope-rations; and

5. Measures to develop linkages amongsegments.

In terms of financial market deepening,Nissanke and Aryeetey (1998) support thedevelopment of capital markets as anextension to the system that will facilitatealternative financial instruments for poten-tial users of the system. Having differenttypes of financial institutions competingfor different types of clients appeared tothem to offer opportunities for greatercompetition. This is a view that is general-

ly very valid. While the presence of thinlytraded capital markets have not necessa-rily solved the problems of potential usersof capital, there is ample evidence thatincreased competition from non-bank ins-titutions in a number of countries is for-cing banks to pay greater attention totheir businesses (Honohan and Beck,2007).

Market-supporting financial infrastructureincludes structures that enhance the infor-mation base and the legal system. “Ourresearch findings suggest that difficultiesin obtaining reliable information andmanaging risks cause fragmentation”(Nissanke and Aryeetey, 1998). The useof well-equipped credit reference bureausis one of the means suggested to attainthis end. Essentially countries must investin enhancing the information capital baseof their economies. While the more struc-tured economies, as in South Africa, havesuch bureaus, a number of other coun-tries have only recently initiated steps toset up credit reference bureaus, as inGhana. These are still being worked on.Most other countries are yet to take thefirst steps. In terms of the legal infrastruc-ture, the idea is basically to create institu-tions that help safeguard property rightsand support the enforcement of contracts.An example of how some countries aredealing with it is to set up commercialcourts after tightening laws on commercial

26

contracts. “A special commercial courtestablished in Tanzania was greeted withenthusiasm, though —perhaps inevita-bly— early achievements were not fullymaintained. In Rwanda the time taken toresolve a dispute fell by 22 percent follo-wing the introduction of a specializedcourt for business, financial, and tax mat-ters (Honohan and Beck, 2007). But theissue of legal infrastructure is larger thansimply establishing commercial courts.There are questions about what mea-sures can be put in place to facilitate“taking collateral in forms other than lan-ded property, not only because land titleremain uncertain or not transferable inmany countries but because few smallborrowers possess land” (Nissanke andAryeetey, 1998).

On the need for new regulatory andincentive frameworks that advance marketintegration the challenge will be how touse regulation to encourage formal banksto reassess their relationships with non-banks. The growing use of microfinanceinstitutions by banks is an example ofhow such integration can be arranged(see below). As the regulatory authoritiesdevelop greater responsibility for non-banks it becomes a lot easier for banks towork with them.

In seeking to achieve integrated financialsystems, the use of appropriate financial

technology is important. This refers to theprocesses through which deposit takersand lenders gather information and pro-cess these in decision making. Withimproved technology it is possible to redu-ce the transaction cost involved in suchprocessing. Today, the use of computersand mobile phones, for example, hasintroduced a new dimension to reachingsmall depositors and borrowers in a num-ber of countries and sharing informationabout them. The M-Pesa project in Kenyafor money transfers for example, createsanother opportunity for people to be rea-ched with money. The challenge is how touse these new technologies in a morestructured manner for financial interme-diation and for the delivery of a broaderset of financial services.

In the proposals for enhancing financialtechnology, Nissanke and Aryeetey (1998)focused on devolution of decision-makingand supervision to local levels; the increa-sed application of character-based credit-worthiness criteria for small enterprisesinstead of project-based criteria; use ofinformation possessed by informal andsemi-formal financial operatives; and theuse of non-bank institutions in screeningand preparing SME loans application. Thestudy of banks and microfinance in SouthAsia shows how such arrangements haveworked and these are being consideredby many African banks.

27

Developing Capital Markets

One of the biggest challenges facing thefinancial systems in SSA is the availabilityof long term finance. In the past this camefrom the governments in view of the inabi-lity of commercial banks to deliver them.Governments created development finan-ce institutions (DFIs) to mobilize largelypublic resources and channel them tolong term projects. After their difficulties oftwo decades ago, development financehas become extremely difficult to find. Intheir place many have seen the develop-ment of capital markets as the solution tothe problems of term finance.

While capital markets offer many newopportunities to businesses in Africa theirintroduction to the region has not beenwithout its problems. Of the 15 countriesthat had stock markets in 2005, onlyNigeria and South Africa had more than100 firms listed. The remaining countrieshad an average of 24 firms listed. Themore worrying aspect of their develop-ment is the thinness of trading. With theexception of South Africa, the value tra-ded is less than 3 percent of GDP in allcountries; indeed in most countries, lessthan 1 percent of GDP. They obviouslyhave difficulty mobilizing capital. Aryeeteyand Senbet (2005) have suggested that inorder to enhance the capacity of the fled-gling capital markets to attract private

capital, it is important that steps are takento address the following:

a) Public Confidence and InformationalEfficiency: Public confidence is fosteredby an even playing field, with strict enfor-cement of existing rules. There ought tobe an independent judiciary stronglyenforcing and protecting rights. Thegovernment’s role is vital in this regard inensuring enforceability of private contractsand accounting procedures and legalstandards.

b) Efficient Capital Market Regulation: Atthe heart of capital market regulation isinvestor protection, particularly small parti-cipants in the market. Small investorsneed to be properly protected throughstrict enforcement of securities laws andregulations. African stock markets canharmonize laws and regulations towardinternational standards. Governmentregulation of securities markets should bemore of an oversight function over self-regulatory agencies, such as the stockexchanges and brokerage industry.

c) Capital Market-Based Privatization:Capital markets can be an important ave-nue for privatization. Such programsobviously contribute to the depth of thestock markets through increased supplyof listed companies. Capital market-basedprivatization provides an improved chanceof fair pricing of the enterprises, and

28

hence serves as an important means ofde-politicizing the privatization process. Inaddition, privatization through local capitalmarkets allows for local investor participa-tion and hence enhanced diversity ofownership of the economy’s resources.

d) Regionalization of Capital Markets:One way to address the thinness and illi-quidity of African capital markets is for thevarious countries to pool resources forregional co-operation and capital marketdevelopment. Regionalization of Africanstock markets should enhance mobiliza-tion of both domestic and global financialresources to fund regional companies,while injecting more liquidity into the mar-kets. The francophone example is worthlooking at.

e) Human Capital Development: Globalcapital markets have become highlysophisticated in recent years with theadvancing information technology. Theyare increasingly characterized by advan-ced and exotic securities, including avariety of derivative securities, demandingthat market participants stay abreast ofrecent developments in financial theoryand practice. Adequately trained financialmanpower should be at the centre ofcapital market development in Africa.

Developing Microfinance

In the last decade microfinance has cometo be regarded as a central part of develo-

ping country financial systems, even if litt-le progress has been achieved in terms ofwhat regulatory environment works bestfor delivering its services and protectingstakeholders. It has been shown to beeffective in delivering financial services tosmall depositors and borrowers, and thishas contributed significantly to enhanceddomestic resource mobilization. There isalso evidence of growing links betweenformal banks and microfinance institutions(MFIs) and that this link holds the key toexpanding access to microfinance ser-vices. It is becoming commonplace throu-ghout Africa to see banks set up microfi-nance operations either from within or inpartnership with MFIs. In Aryeetey (2004)the argument was made that banks andmicrofinance institutions (MFIs) that enga-ged in microfinance were most effectiveand efficient if they adopted decentralizedstructures. This allowed them to reachmarginal clients cost-effectively.Decentralization involves the maintenanceof lean structures, accountability andincentives for increasing operational effi-ciency, streamlining of operations, andoutsourcing and networking [SeeWisniwski and Hannig, (1998)].

Wisniwski and Hannig (1998) have seve-ral examples of how maintaining leanstructures can lead to substantial reduc-tions in administrative costs for banks andMFIs. This can be done while taking careof essential aspects of the business of

29