Wireless Telephone Service Providers Rachel Yan Bennet Heidenreich Lindsey Ludwig Lucas Hartman.

50

Wireless Telephone Service Providers Rachel Yan Bennet Heidenreich Lindsey Ludwig Lucas Hartman

-

Upload

russell-knight -

Category

Documents

-

view

219 -

download

0

Transcript of Wireless Telephone Service Providers Rachel Yan Bennet Heidenreich Lindsey Ludwig Lucas Hartman.

Wireless Telephone Service Providers

Rachel YanBennet HeidenreichLindsey LudwigLucas Hartman

Quick Question…

That’s Why!

Why?• Strongly influenced by technological progress• Rapid growth over the past 5 years• Information good• Highly concentrated• Interest pricing patterns• Tacit collusion pattern• Recent news about mergers and acquisitions

Industry Structure

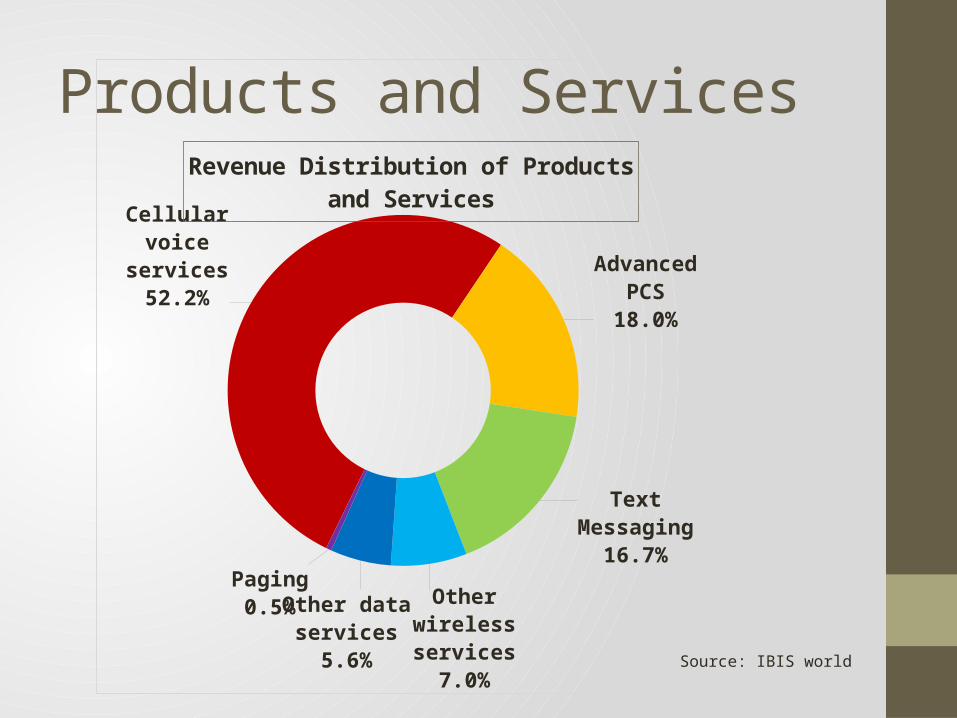

Products and Services

Cellular voice services52.2% Advanced PCS

18.0%

Text Messaging16.7%

Other wireless services

7.0%

Other data services

5.6%

Paging0.5%

Revenue Distribution of Products and Services

Source: IBIS world

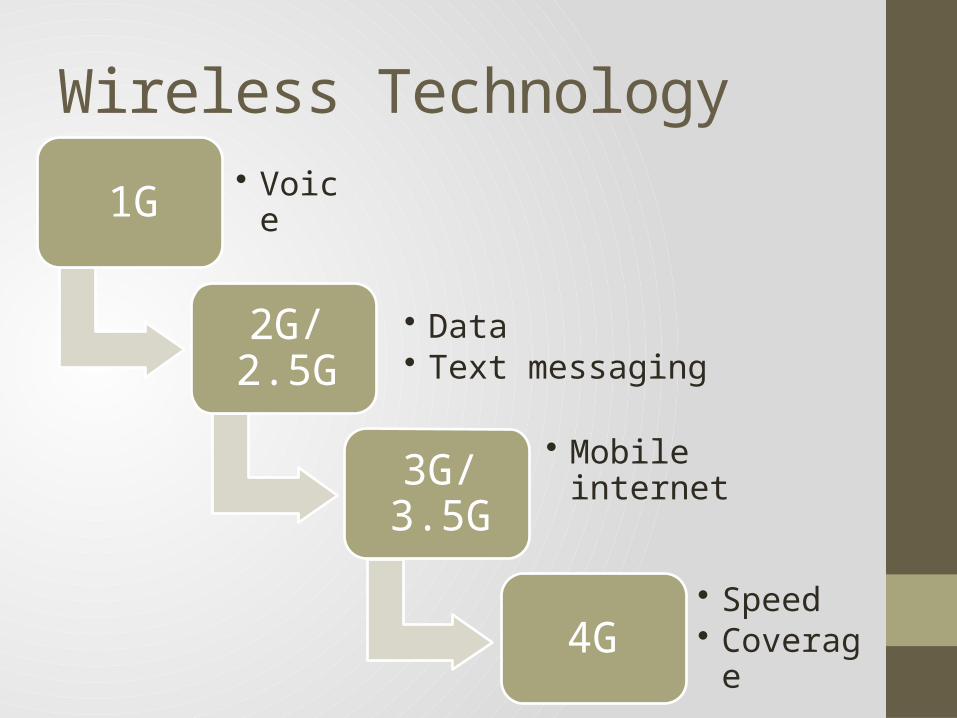

Wireless Technology

1G • Voice

2G/2.5G• Data• Text messaging

3G/3.5G• Mobile internet

4G• Speed• Coverage

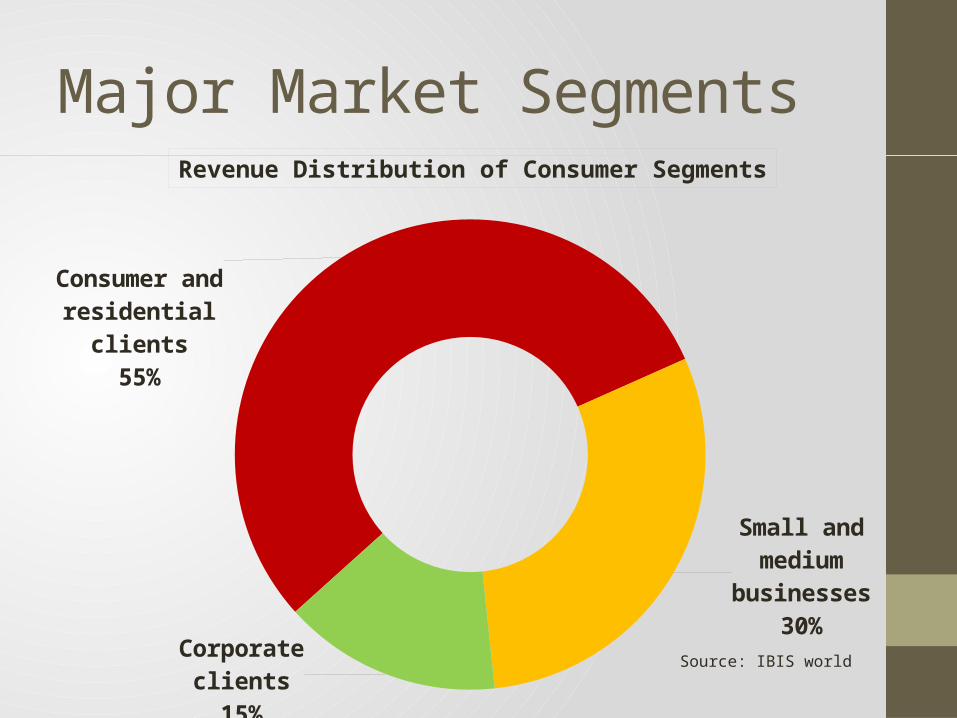

Major Market Segments

Consumer and res-idential clients

55%

Small and medium businesses

30%

Corporate clients15%

Source: IBIS world

Revenue Distribution of Consumer Segments

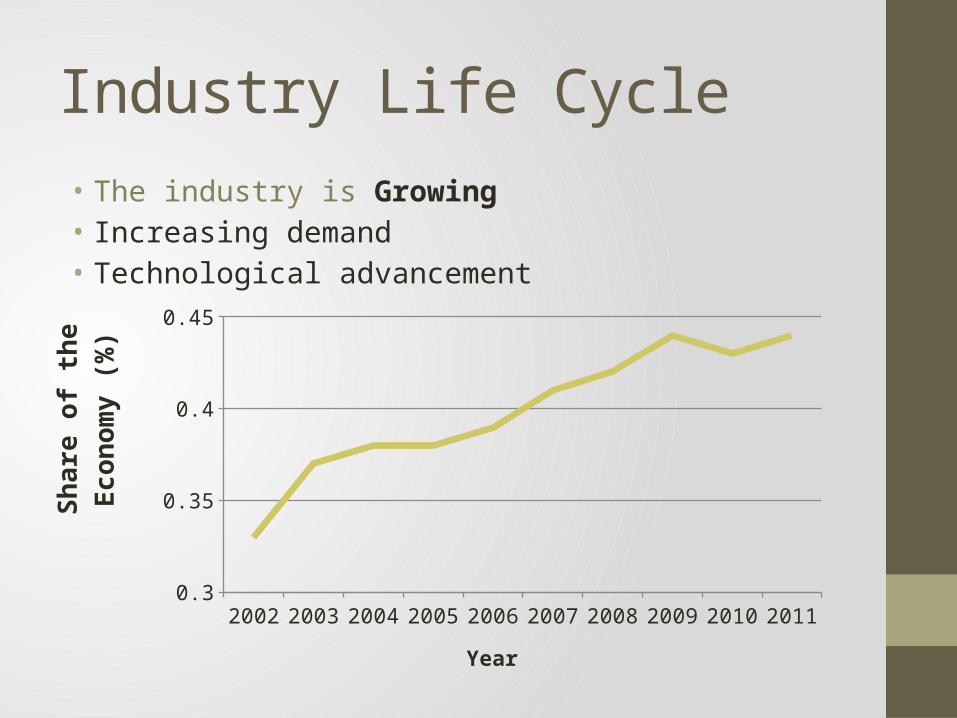

Industry Life Cycle• The industry is Growing• Increasing demand• Technological advancement

2002 2003 2004 2005 2006 2007 2008 2009 2010 20110.3

0.35

0.4

0.45

Year

Shar

e of

the

Econ

omy

(%)

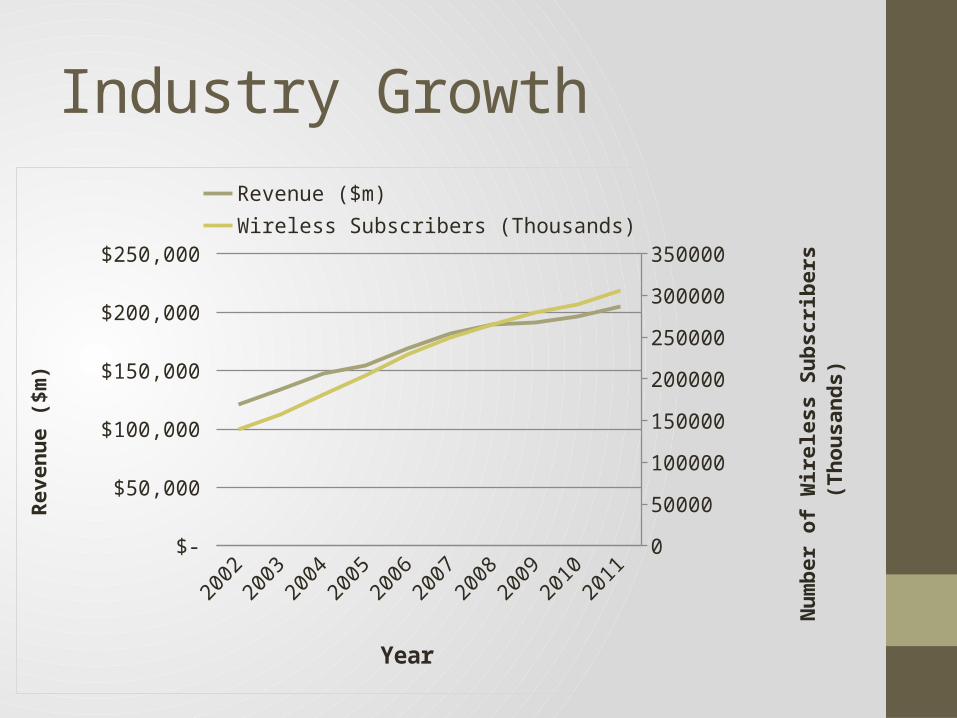

Industry Growth

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 $-

$50,000

$100,000

$150,000

$200,000

$250,000

0

50000

100000

150000

200000

250000

300000

350000

Revenue ($m) Wireless Subscribers (Thousands)

Year

Reve

nue

($m

)

Num

ber o

f Wire

less

Sub

scrib

ers (

Thou

sand

s)

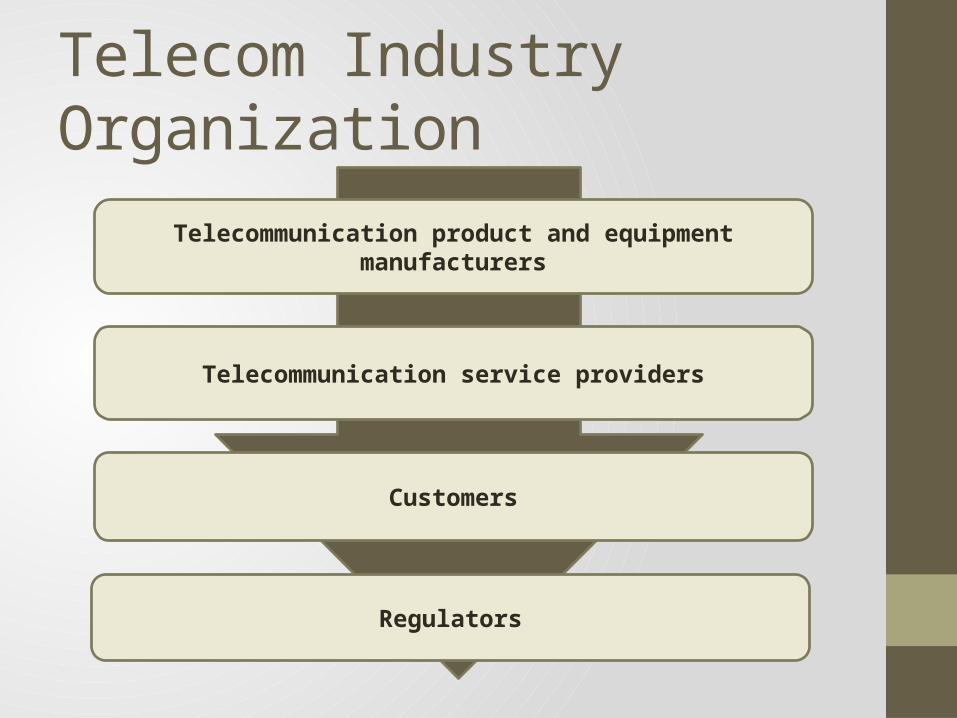

Telecom Industry Organization

Telecommunication product and equipment manufacturers

Telecommunication service providers

Customers

Regulators

Regulation• Medium Level• Federal Communications Commission (FCC)

Functions:• Promote competition• Ensure customers are given sufficient information

about charges• Improve quality of services• Encourage rapid deployment of new technologies

Competition

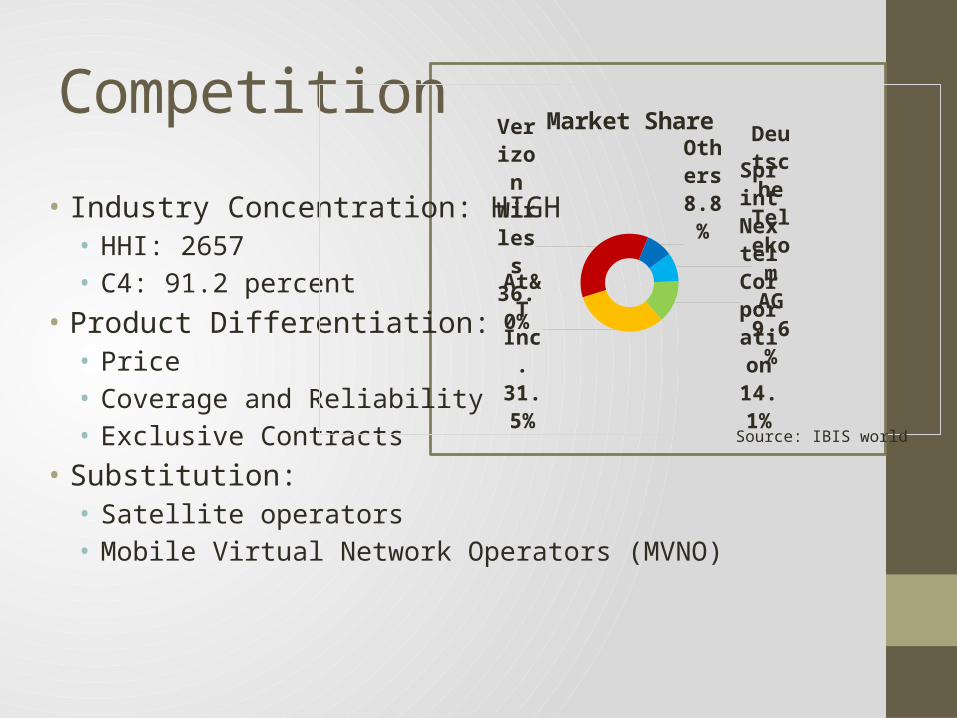

• Industry Concentration: HIGH• HHI: 2657• C4: 91.2 percent

• Product Differentiation:• Price• Coverage and Reliability• Exclusive Contracts

• Substitution:• Satellite operators• Mobile Virtual Network Operators (MVNO)

Deutsche Telekom

AG9.6%

Sprint Nextel

Corpora-tion

14.1%At&T Inc.31.5%

Verizon Wirless36.0%

Others8.8%

Market Share

Source: IBIS world

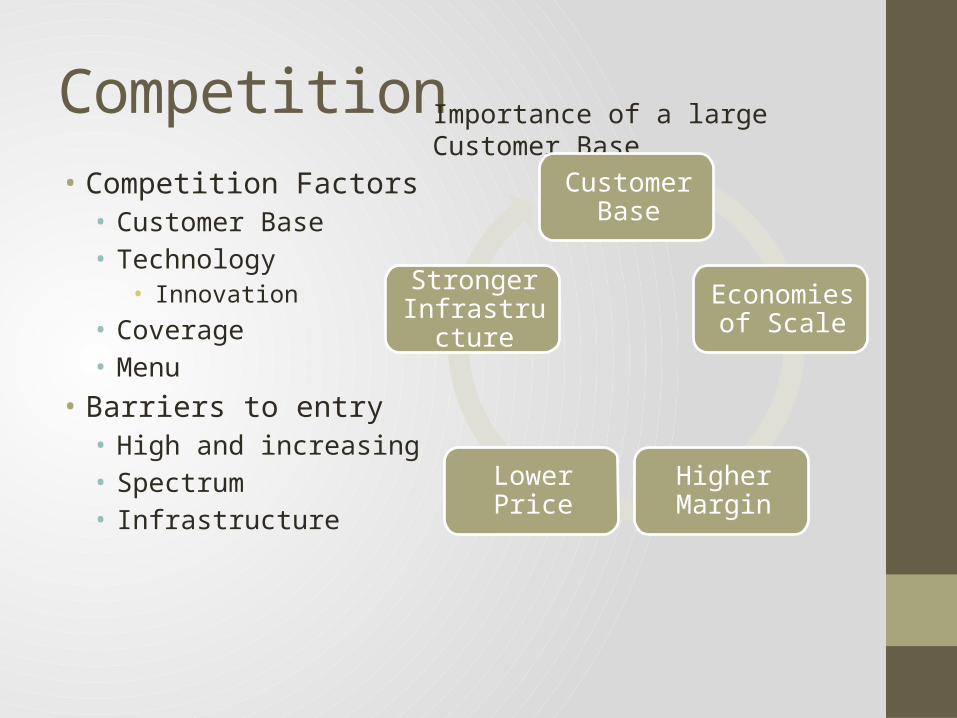

Competition• Competition Factors• Customer Base• Technology

• Innovation• Coverage• Menu

• Barriers to entry• High and increasing• Spectrum• Infrastructure

Importance of a large Customer Base

Customer Base

Economies of Scale

Higher MarginLower Price

Stronger Infrastructure

Major companies

• Verizon• AT&T• Sprint• T-Mobile

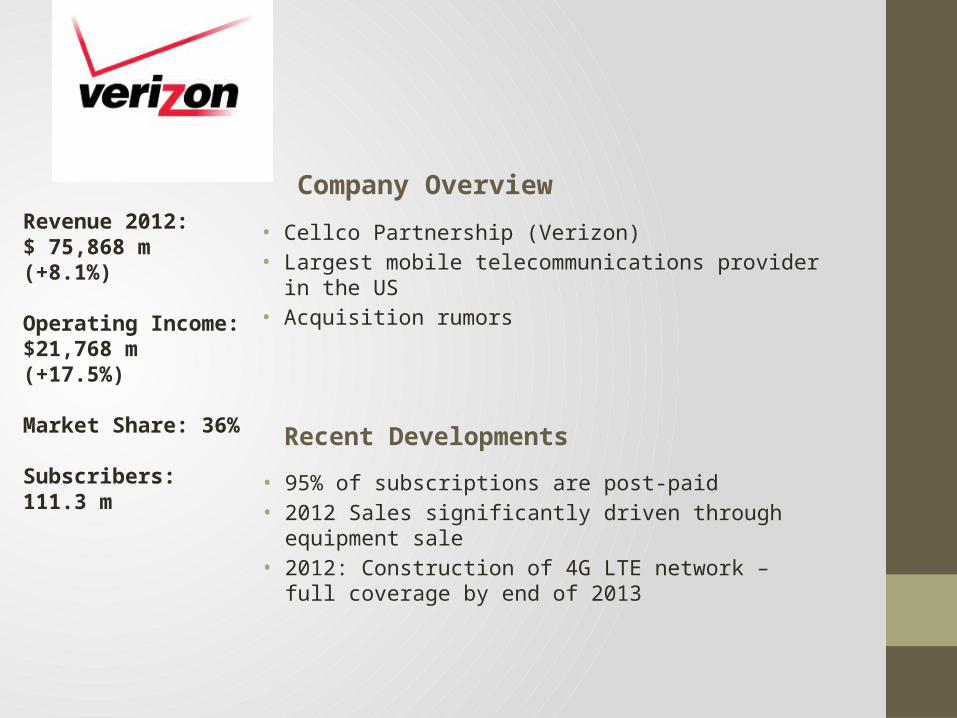

Revenue 2012: $ 75,868 m (+8.1%)

Operating Income: $21,768 m (+17.5%)

Market Share: 36%

Subscribers: 111.3 m

Company Overview

• Cellco Partnership (Verizon)• Largest mobile telecommunications provider in the US• Acquisition rumors

• 95% of subscriptions are post-paid• 2012 Sales significantly driven through equipment sale• 2012: Construction of 4G LTE network – full coverage by end

of 2013

Recent Developments

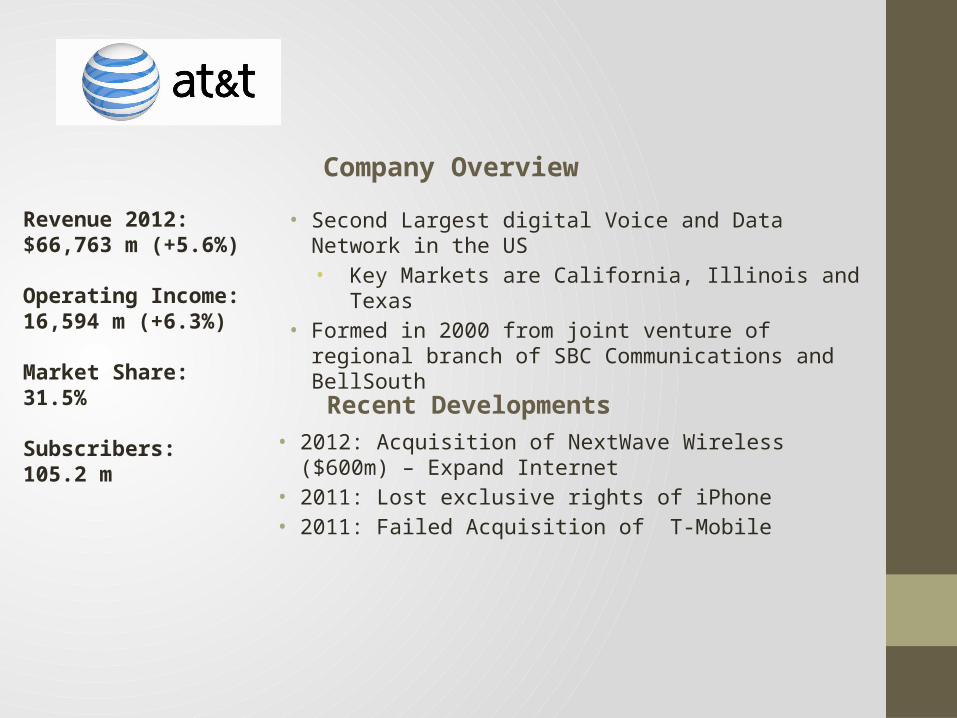

Company Overview

• Second Largest digital Voice and Data Network in the US• Key Markets are California, Illinois and Texas

• Formed in 2000 from joint venture of regional branch of SBC Communications and BellSouth

Revenue 2012:$66,763 m (+5.6%)

Operating Income: 16,594 m (+6.3%)

Market Share: 31.5%

Subscribers: 105.2 mRecent Developments

• 2012: Acquisition of NextWave Wireless ($600m) – Expand Internet

• 2011: Lost exclusive rights of iPhone• 2011: Failed Acquisition of T-Mobile

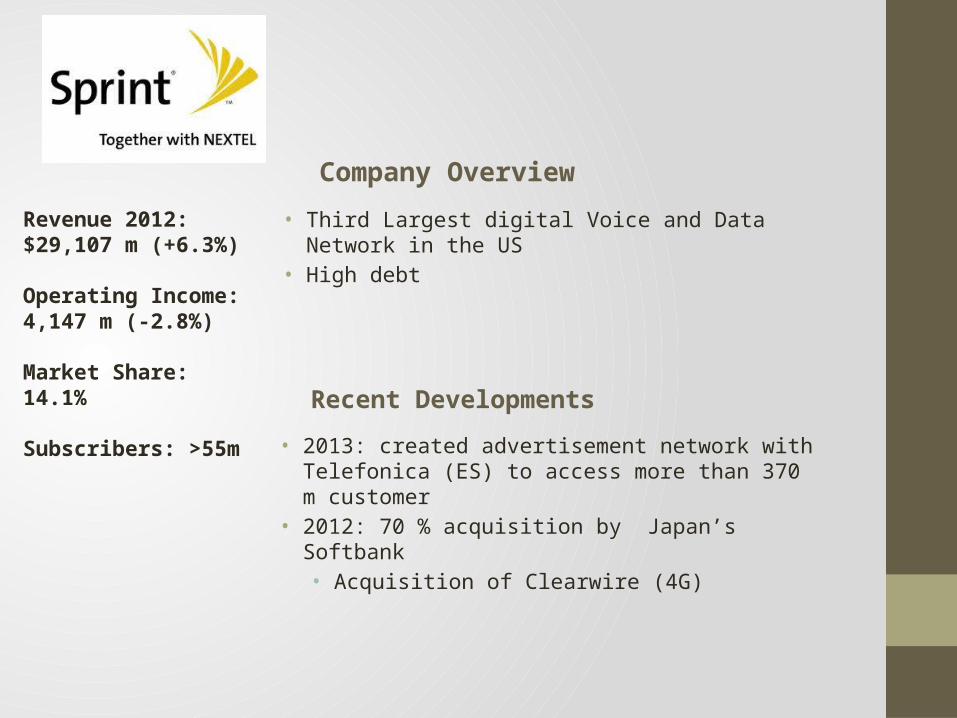

Company Overview

• Third Largest digital Voice and Data Network in the US• High debt

Revenue 2012:$29,107 m (+6.3%)

Operating Income: 4,147 m (-2.8%)

Market Share: 14.1%

Subscribers: >55m Recent Developments

• 2013: created advertisement network with Telefonica (ES) to access more than 370 m customer

• 2012: 70 % acquisition by Japan’s Softbank• Acquisition of Clearwire (4G)

Company Overview

• Subsidiary of Germany-based Deutsche TelekomFocuses on metropolitan markets• Relative small network coverage

• Operates largest carrier-owned Wi-Fi network through T-Mobile hotspots

• Offers low rates

Revenue 2012:19,875 m (+7.5%)

Operating Income: -9,770 m

Market Share: 9.6%

Subscribers: 24.8m

Recent Developments• 2012: Agreed to acquire Metro PCS• April 12th

• 2013: Begin LTE operations with investment of $4 bn.

Pricing Strategies

Outline• Importance and

Pricing Goal• 2nd Degree Pricing• 3rd Degree Pricing• Verizon and AT&T• Sprint and T-Mobile• Advertising Wars • Survey Data Analysis

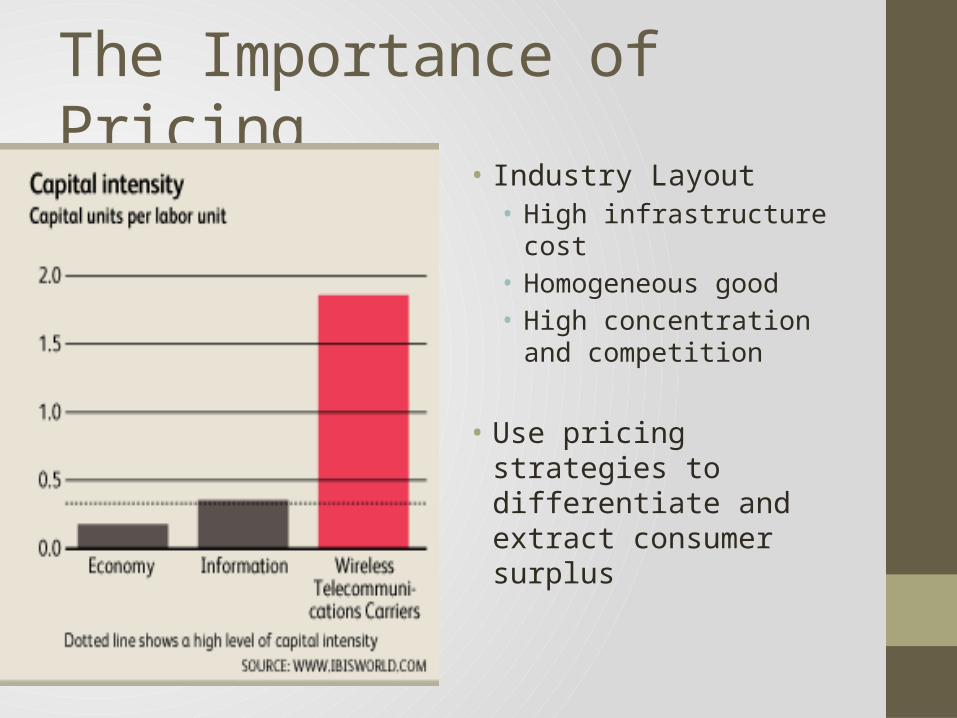

The Importance of Pricing

• Industry Layout • High infrastructure cost• Homogeneous good• High concentration and

competition

• Use pricing strategies to differentiate and extract consumer surplus

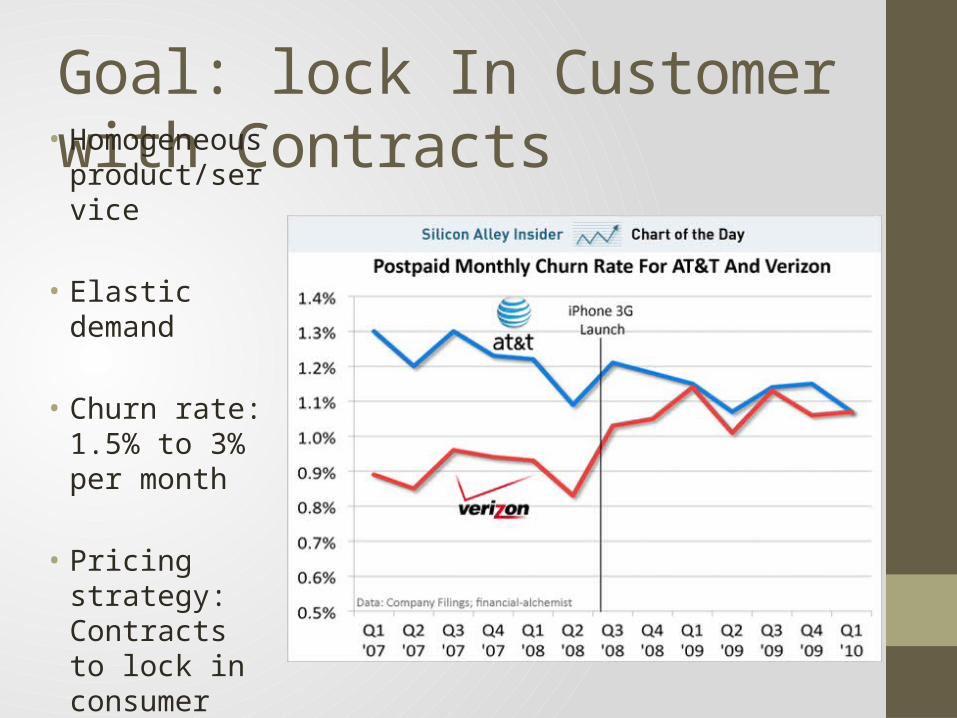

Goal: lock In Customer with Contracts• Homogeneous

product/service

• Elastic demand

• Churn rate: 1.5% to 3% per month

• Pricing strategy: Contracts to lock in consumer

Prepaid Strategies • No contracts, pay before use • Battle churn rate and declining average revenue per user

(ARPU) since 2006• Attempt to win consumers in untapped markets and fight for

market share

• Virgin Mobile iPhone Commercial

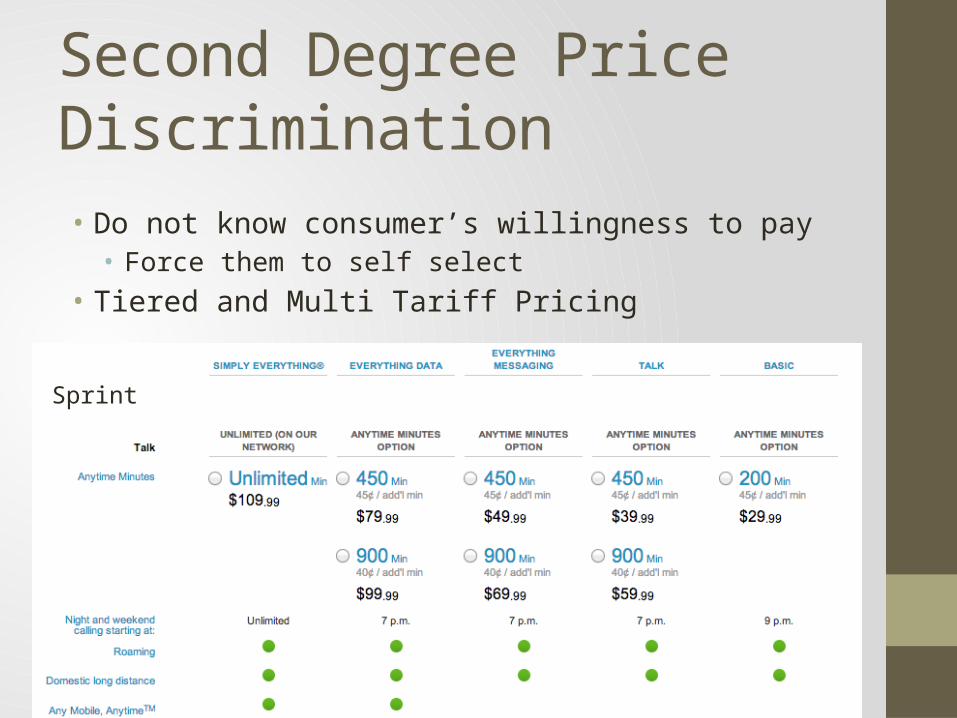

Second Degree Price Discrimination • Do not know consumer’s willingness to pay• Force them to self select

• Tiered and Multi Tariff Pricing

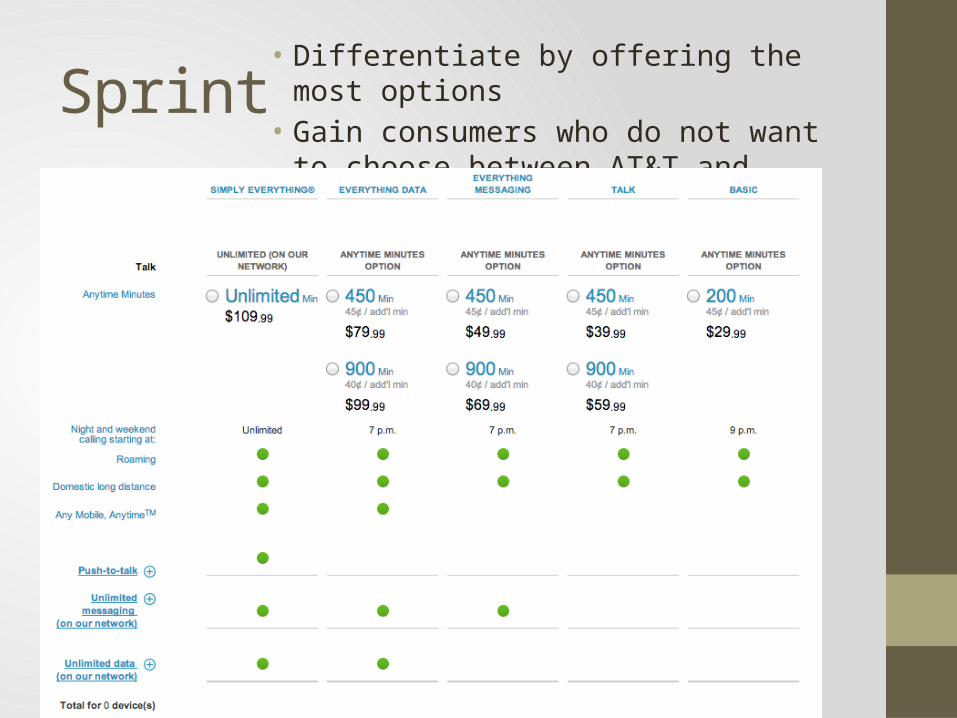

Sprint

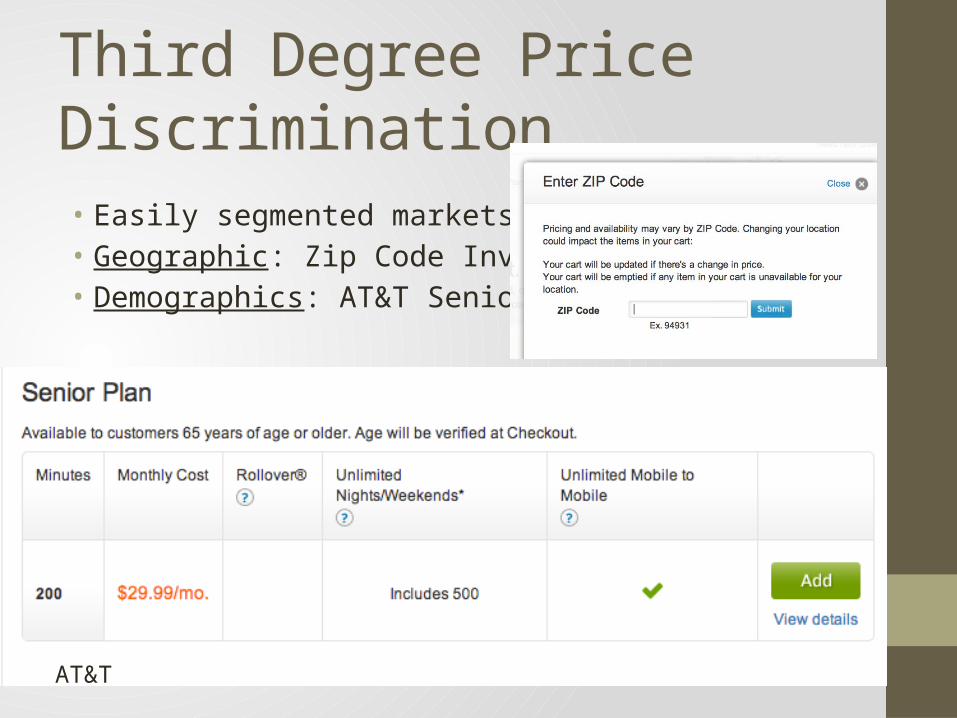

Third Degree Price Discrimination• Easily segmented markets • Geographic: Zip Code Investigation • Demographics: AT&T Senior Plan

AT&T

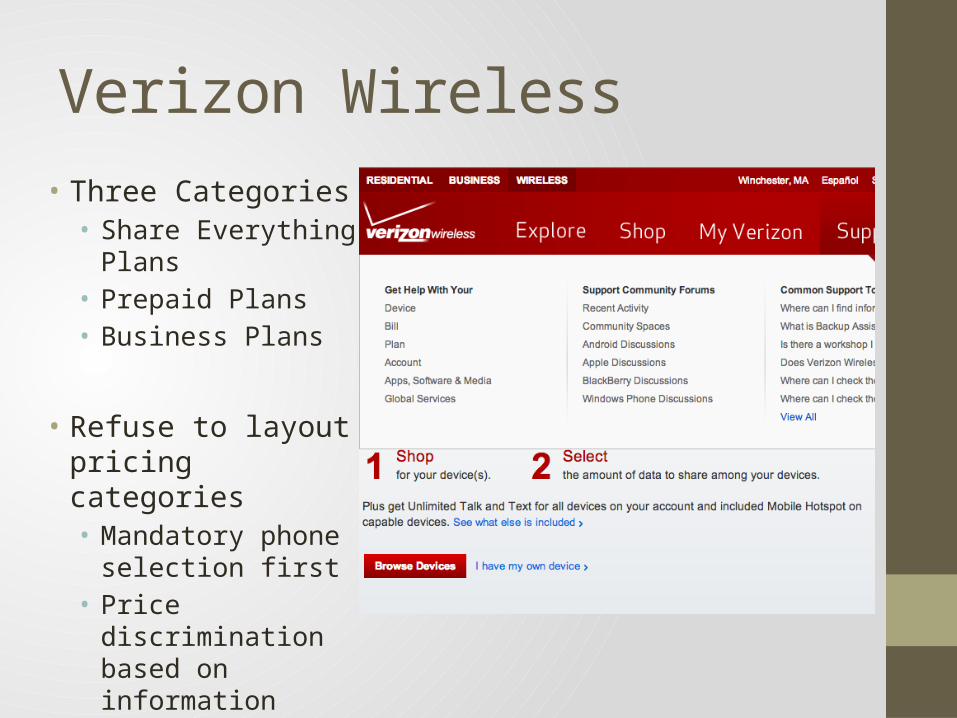

Verizon Wireless• Three Categories• Share Everything Plans• Prepaid Plans• Business Plans

• Refuse to layout pricing categories• Mandatory phone

selection first • Price discrimination

based on information

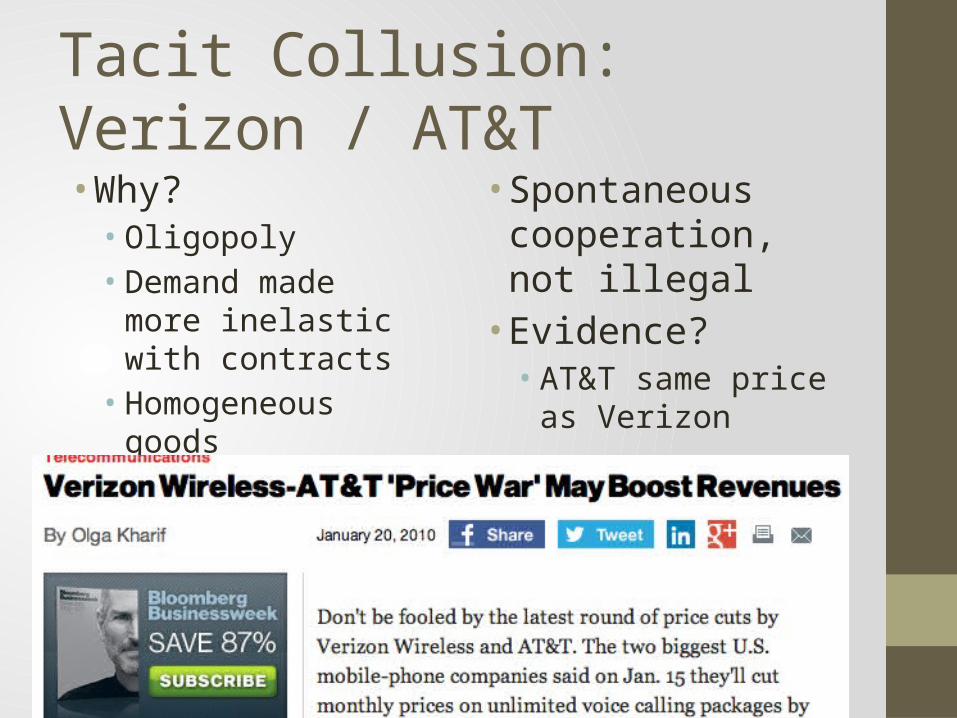

Tacit Collusion: Verizon / AT&T• Why? • Oligopoly• Demand made more

inelastic with contracts• Homogeneous goods

• Spontaneous cooperation, not illegal• Evidence?• AT&T same price as

Verizon

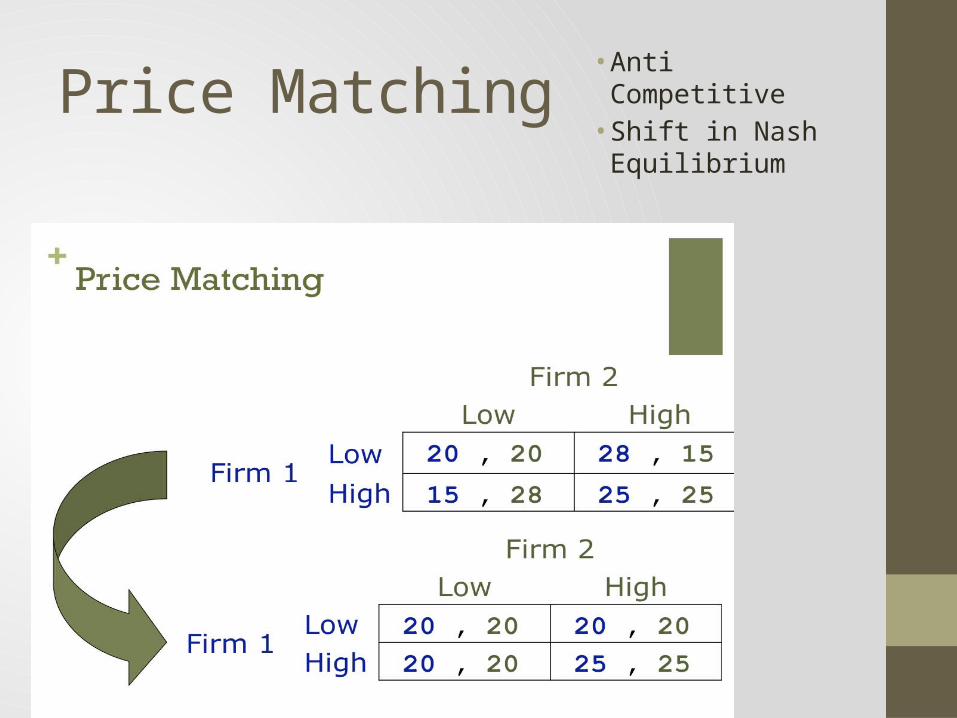

Price Matching • Anti Competitive• Shift in Nash

Equilibrium

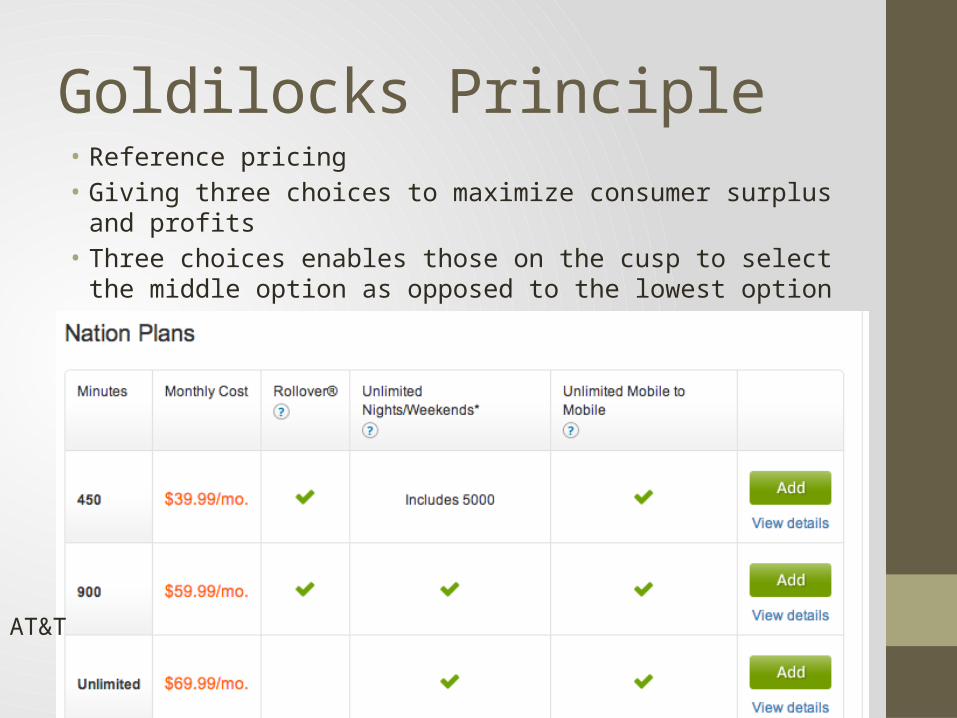

Goldilocks Principle • Reference pricing • Giving three choices to maximize consumer surplus and profits• Three choices enables those on the cusp to select the middle

option as opposed to the lowest option

AT&T

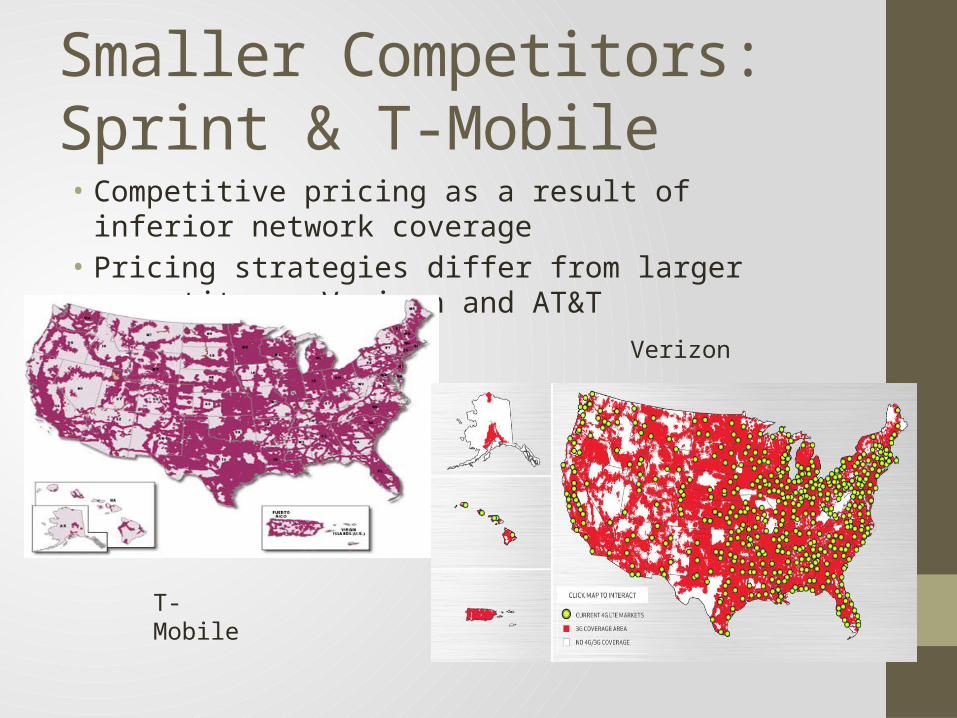

Smaller Competitors: Sprint & T-Mobile • Competitive pricing as a result of inferior network coverage• Pricing strategies differ from larger competitors: Verizon and

AT&T

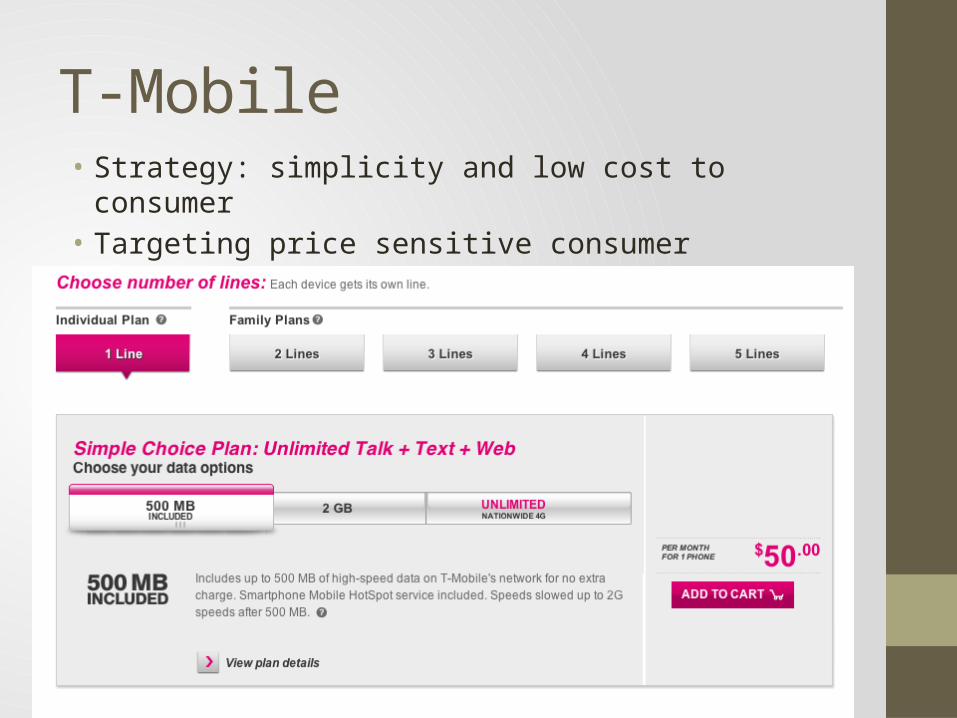

T-Mobile

Verizon

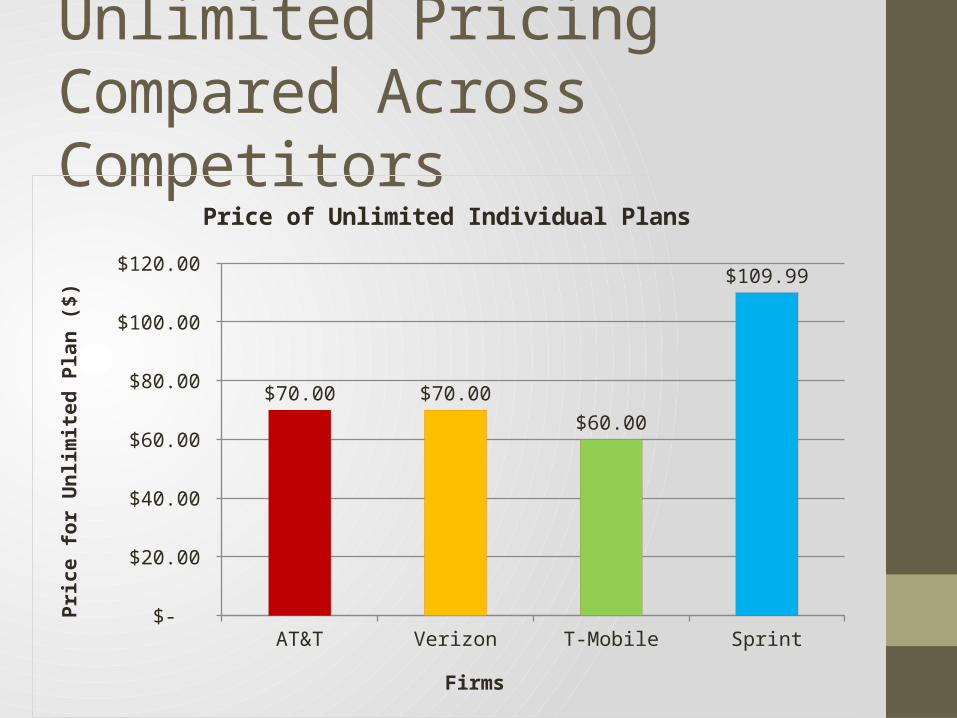

Unlimited Pricing Compared Across Competitors

AT&T Verizon T-Mobile Sprint $-

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$70.00 $70.00

$60.00

$109.99

Price of Unlimited Individual Plans

Firms

Pric

e fo

r Unl

imite

d Pl

an ($

)

Sprint• Differentiate by offering the most options• Gain consumers who do not want to choose

between AT&T and Verizon’s three plans

T-Mobile• Strategy: simplicity and low cost to consumer • Targeting price sensitive consumer

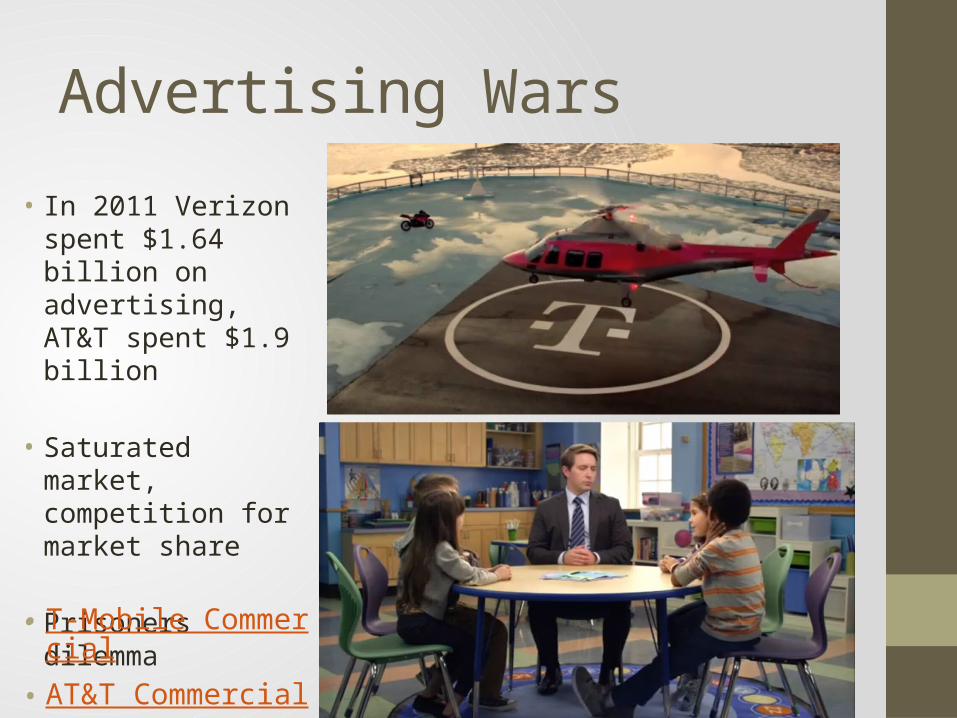

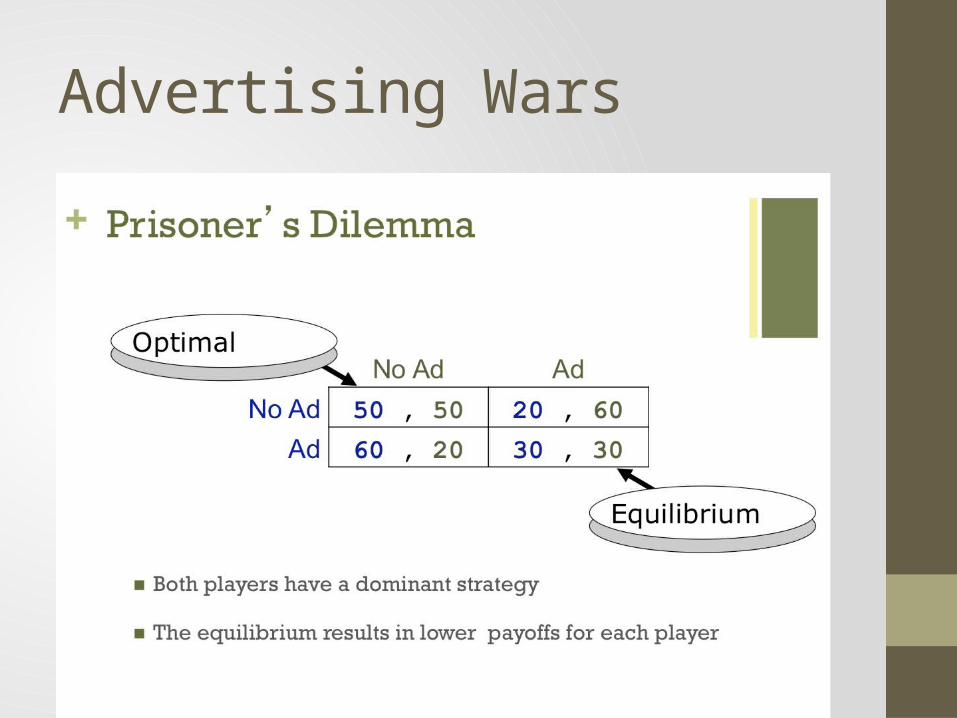

Advertising Wars

• In 2011 Verizon spent $1.64 billion on advertising, AT&T spent $1.9 billion

• Saturated market, competition for market share

• Prisoners dilemma

• T-Mobile Commercial• AT&T Commercial

Advertising Wars

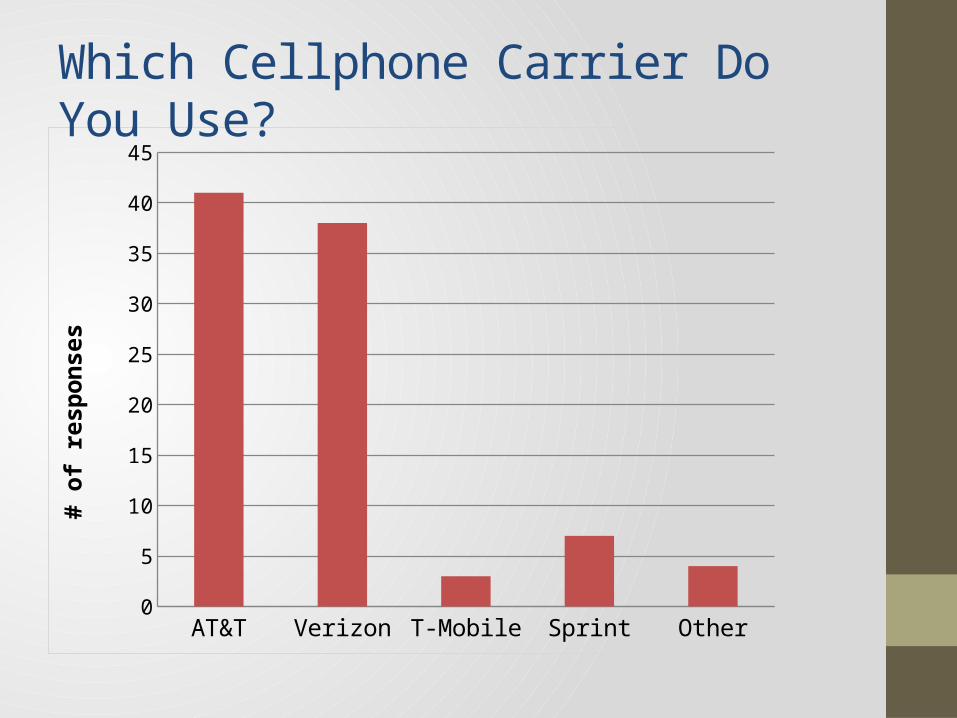

Cornell Survey

AT&T Verizon T-Mobile Sprint Other0

5

10

15

20

25

30

35

40

45

# of

resp

onse

sWhich Cellphone Carrier Do You Use?

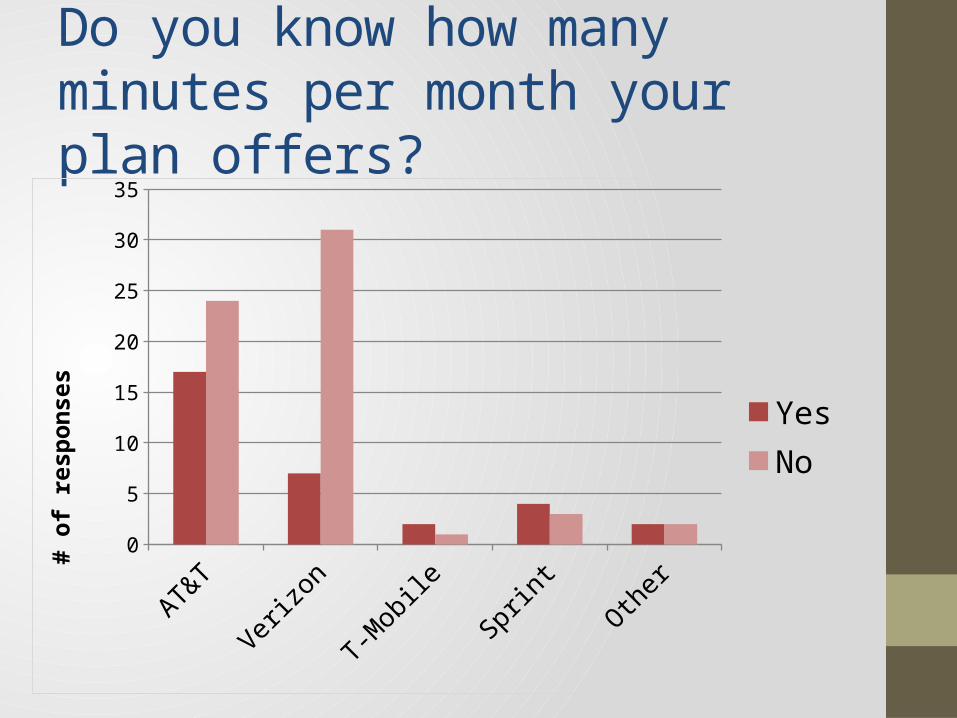

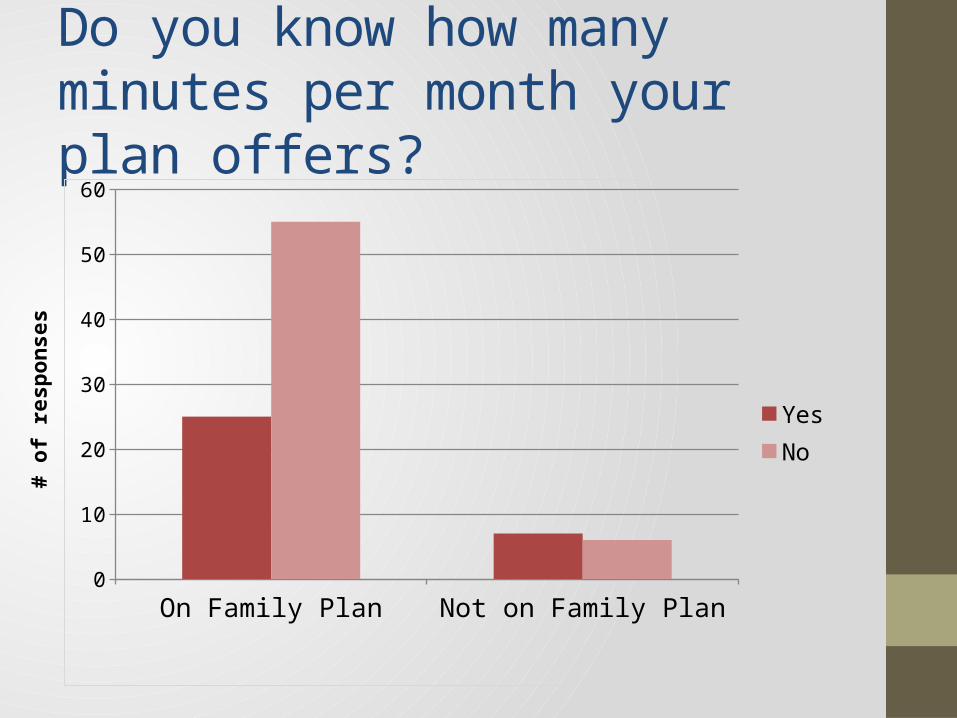

Do you know how many minutes per month your plan offers?

AT&T Verizon T-Mobile Sprint Other0

5

10

15

20

25

30

35

Yes No

# of

resp

onse

s

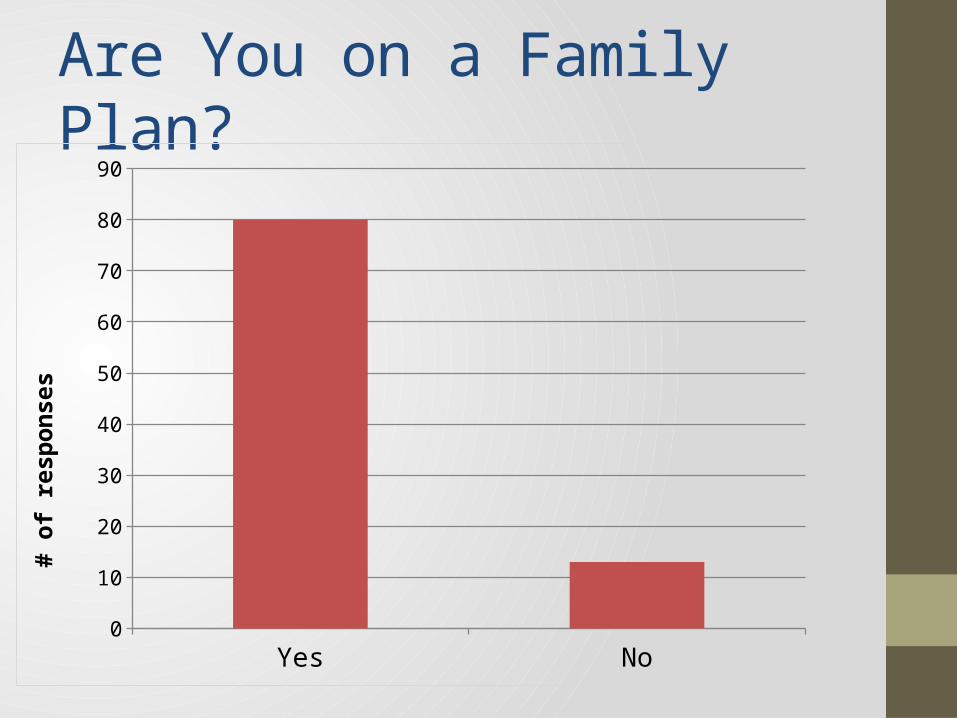

Are You on a Family Plan?

Yes No0

10

20

30

40

50

60

70

80

90

# of

resp

onse

s

Are You on a Family Plan?

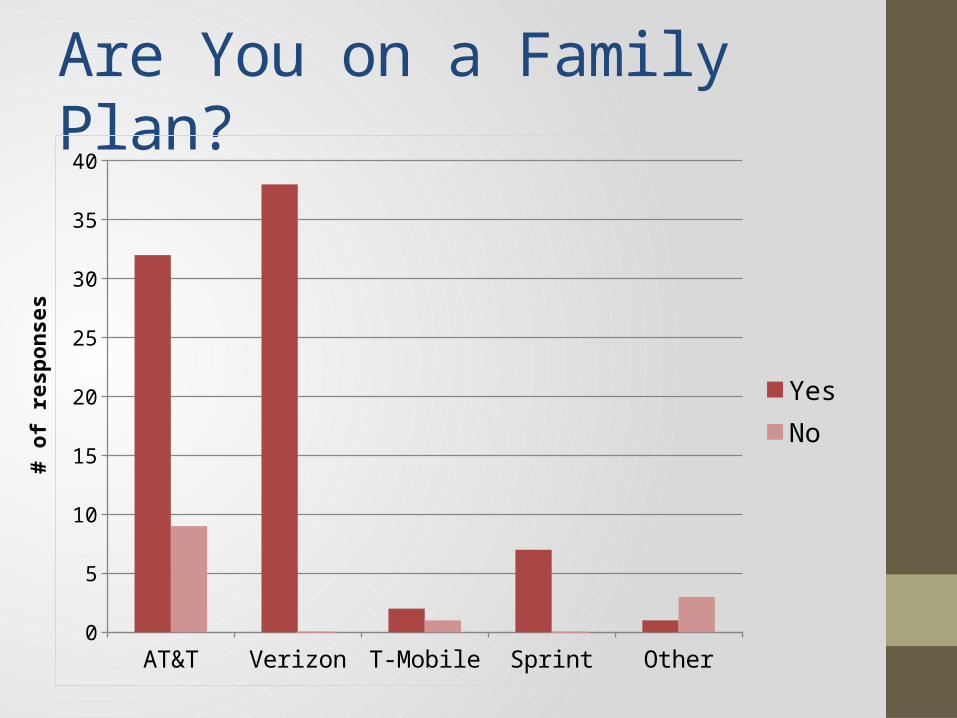

AT&T Verizon T-Mobile Sprint Other0

5

10

15

20

25

30

35

40

Yes No

# of

resp

onse

s

Do you know how many minutes per month your plan offers?

On Family Plan Not on Family Plan0

10

20

30

40

50

60

Yes No#

of re

spon

ses

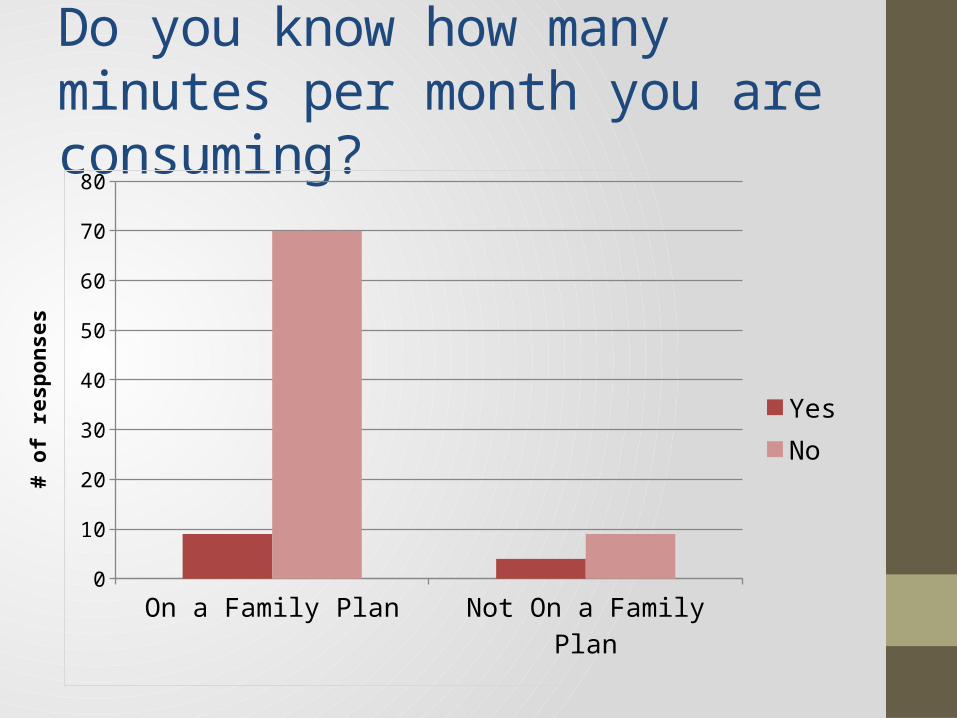

Do you know how many minutes per month you are consuming?

On a Family Plan Not On a Family Plan0

10

20

30

40

50

60

70

80

YesNo

# of

resp

onse

s

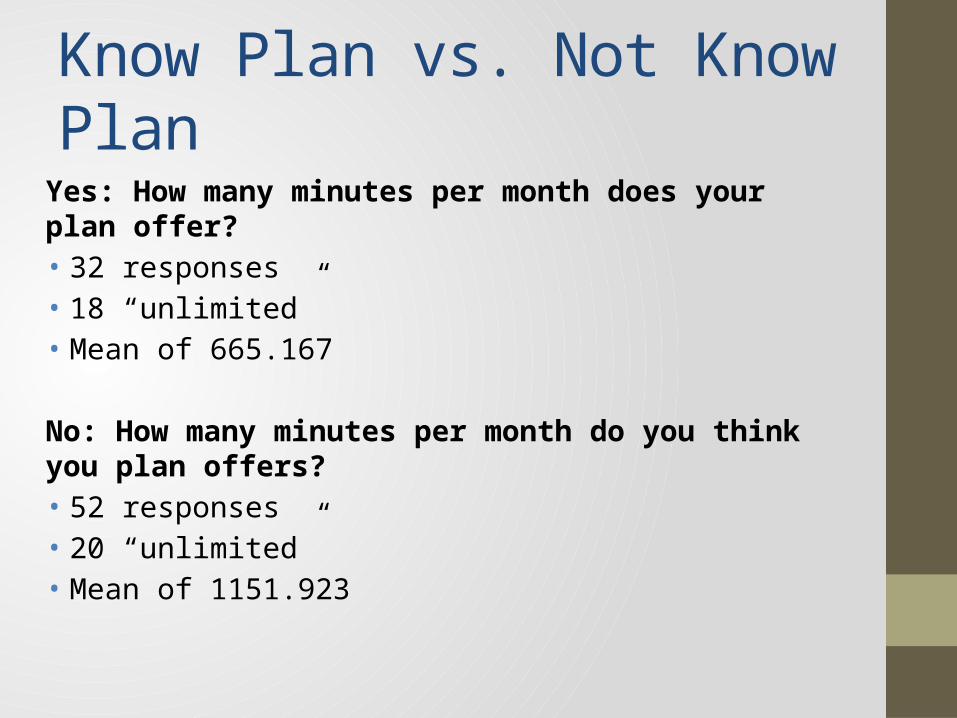

Know Plan vs. Not Know Plan

Yes: How many minutes per month does your plan offer?• 32 responses• 18 “unlimited”• Mean of 665.167

No: How many minutes per month do you think you plan offers?• 52 responses• 20 “unlimited”• Mean of 1151.923

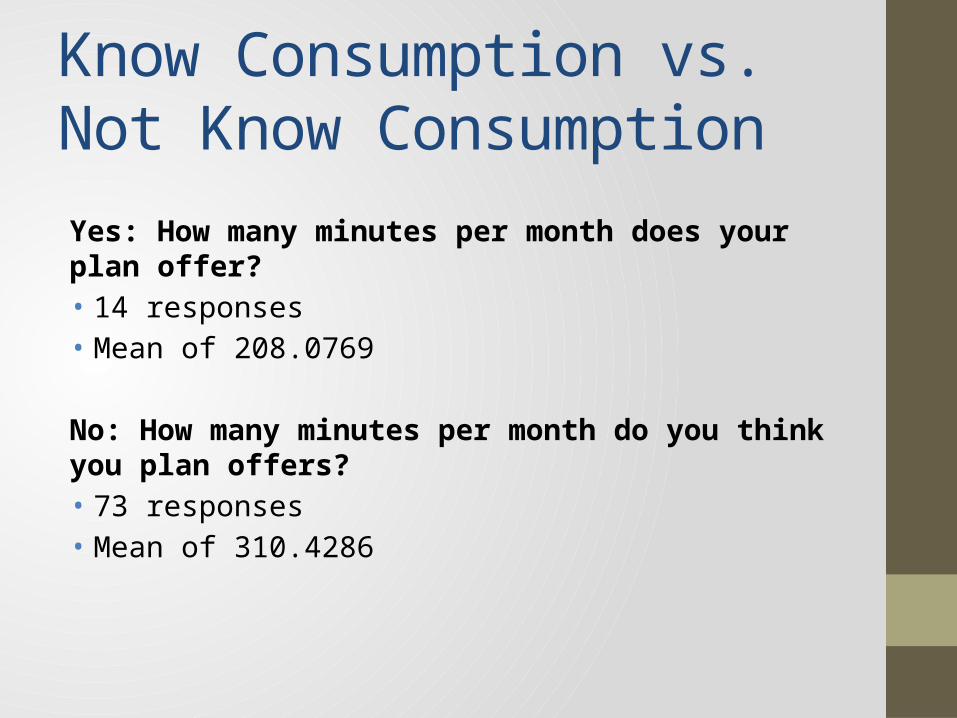

Know Consumption vs. Not Know Consumption

Yes: How many minutes per month does your plan offer?• 14 responses• Mean of 208.0769

No: How many minutes per month do you think you plan offers?• 73 responses• Mean of 310.4286

Recommendation

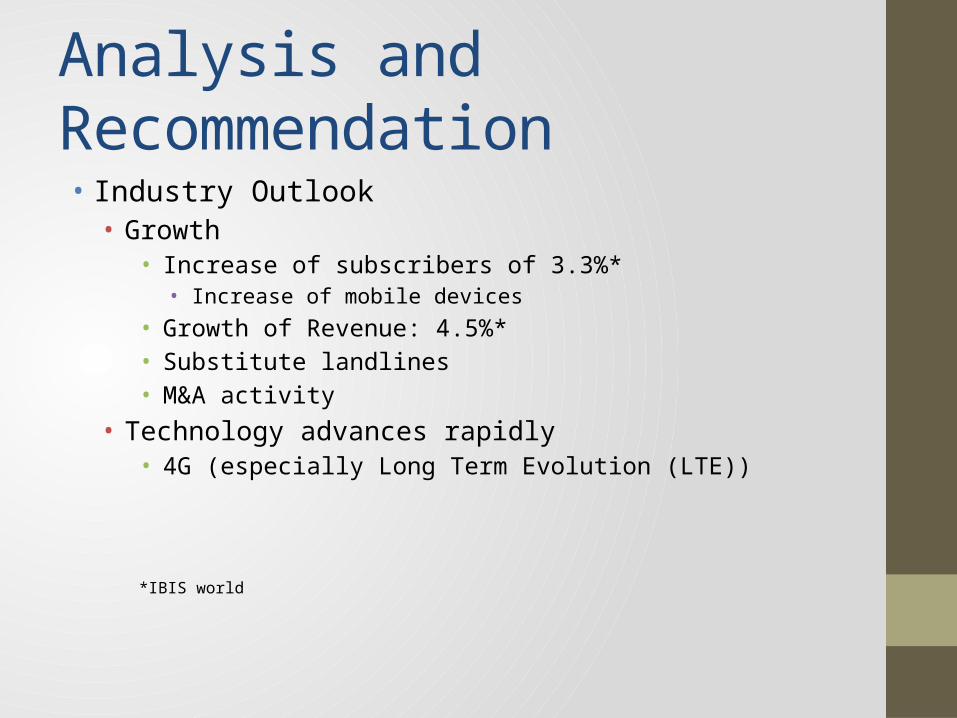

Analysis and Recommendation• Industry Outlook• Growth

• Increase of subscribers of 3.3%*• Increase of mobile devices

• Growth of Revenue: 4.5%*• Substitute landlines• M&A activity

• Technology advances rapidly• 4G (especially Long Term Evolution (LTE))

*IBIS world

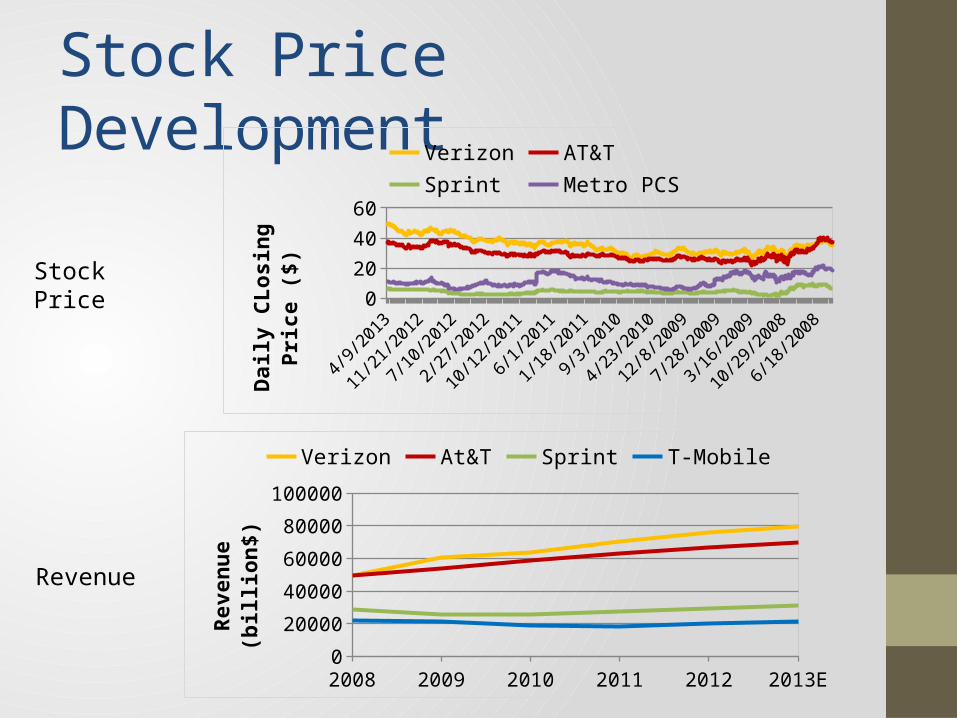

Stock Price Development

2008 2009 2010 2011 2012 2013E0

20000

40000

60000

80000

100000Verizon At&T Sprint T-Mobile

Reve

nue

(bill

ion$

)

Stock Price

Revenue

4/10/2

008

7/17/2

008

10/23/2

008

1/29/2

009

5/7/2

009

8/13/2

009

11/19/2

009

2/25/2

010

6/3/2

010

9/9/2

010

12/16/2

010

3/24/2

011

6/30/2

011

10/6/2

011

1/12/2

012

4/19/2

012

7/26/2

012

11/1/2

012

2/7/2

0130

20

40

60Verizon AT&T Sprint Metro PCS

Daily

CLo

sing

Pric

e ($

)

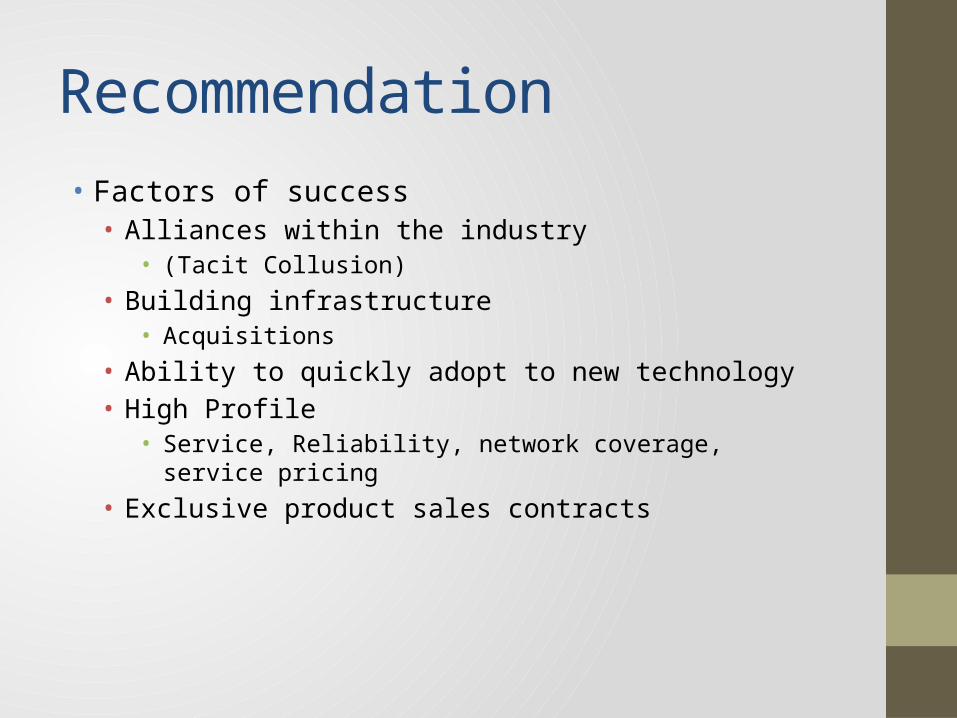

Recommendation• Factors of success• Alliances within the industry

• (Tacit Collusion)• Building infrastructure

• Acquisitions• Ability to quickly adopt to new technology• High Profile

• Service, Reliability, network coverage, service pricing• Exclusive product sales contracts

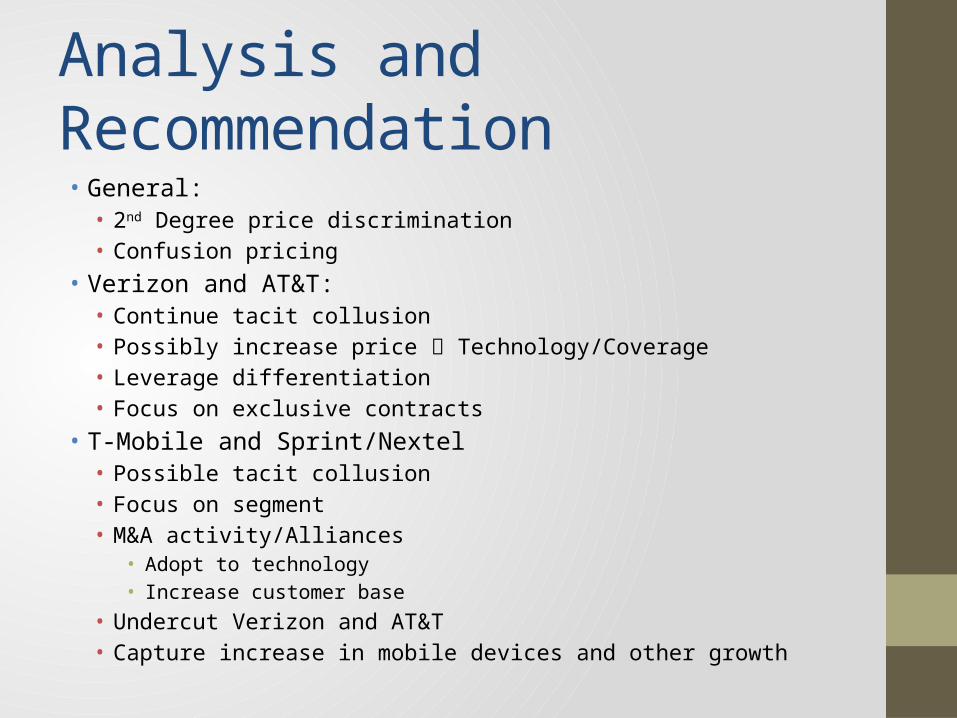

Analysis and Recommendation• General:• 2nd Degree price discrimination• Confusion pricing

• Verizon and AT&T: • Continue tacit collusion• Possibly increase price Technology/Coverage• Leverage differentiation• Focus on exclusive contracts

• T-Mobile and Sprint/Nextel• Possible tacit collusion• Focus on segment• M&A activity/Alliances

• Adopt to technology• Increase customer base

• Undercut Verizon and AT&T• Capture increase in mobile devices and other growth

The End