What You Should Know About Home Equity Lines of … You Should Know About Home Equity Lines of...

28

What You Should Know About Home Equity Lines of Credit and Important Terms of FlexEquity ® / Real Estate Line of Credit EFFECTIVE MAY 1, 2016

Transcript of What You Should Know About Home Equity Lines of … You Should Know About Home Equity Lines of...

What You ShouldKnow AboutHome Equity Linesof Credit andImportant Termsof FlexEquity®/Real EstateLine of Credit

EFFECTIVE MAY 1, 2016

55350_CL1570_81262_i 05.20.2016 09:03 PMM

Black

Pages 2 through 12 of this booklet were initially preparedby the Board of Governors of the Federal Reserve System.The Consumer Financial Protection Bureau (CFPB) hasmade technical updates to the booklet to reflect newmortgage rules under Title XIV of the Dodd-Frank WallStreet Reform and Consumer Protection Act (Dodd-FrankAct). A larger update of this booklet is planned in thefuture to reflect other changes under the Dodd-FrankAct and to align with other CFPB resources and toolsfor consumers as part of the CFPB’s broader mission toeducate consumers. Consumers are encouraged to visitthe CFPB’s website at consumerfinance.gov/owning-a-home to access interactive tools and resources formortgage shoppers, which are expected to be availablebeginning in 2014.

55350_CL1570_81262_ii 05.20.2016 09:03 PMM

Black

1

TABLE OF CONTENTS

Introduction..................................................................................2

Home Equity Plan Checklist...............................................3

What Is a Home Equity Line of Credit? ................................4

What Should You Look for When Shoppingfor a Plan?...............................................................................4

Costs of Establishing and Maintaininga Home Equity Line ..............................................................5

How Will You Repay Your Home Equity Plan? ............5

Line of Credit vs. Traditional SecondMortgage Loans.....................................................................6

What If the Lender Freezes or ReducesYour Line of Credit?.............................................................7

Appendix A...................................................................................8

Defined Terms.......................................................................8

Appendix B...................................................................................10

More Information ................................................................10

Appendix C................................................................................... 11

Contact Information............................................................ 11

Important Terms of Our FlexEquity® Account..................13

Important Terms of Our Real EstateLine of Credit (“RELOC”) Account....................................... 20

55350_CL1570_81262_1 05.20.2016 09:03 PMM

Black

2

INTRODUCTION

If you are in the market for credit, a home equity plan is oneof several options that might be right for you. Before makinga decision, however, you should weigh carefully the costs ofa home equity line against the benefits. Shop for the creditterms that best meet your borrowing needs without posingundue financial risks. And remember, failure to repay theamounts you’ve borrowed, plus interest, could mean theloss of your home.

55350_CL1570_81262_2 05.20.2016 09:03 PMM

Black

3

Home Equity Plan Checklist

Ask your lender to help you fill out this worksheet.

Basic Features for Comparison Plan A Plan B

Fixed Annual Percentage Rate % %

Variable Annual Percentage Rate % %

Index Used and Current Value % %

Amount of Margin

Frequency of Rate Adjustments

Amount/Length of Discount (if any)

Interest Rate Cap and Floor

Length of Plan

Draw Period

Repayment Period

Initial Fees

Appraisal Fee

Application Fee

Up-Front Charges, Including Points

Closing Costs

Repayment Terms

During the Draw Period

Interest and Principal Payments

Interest-Only Payments

Fully Amortizing Payments

When the Draw Period Ends

Balloon Payment?

Renewal Available?

Refinancing of Balance by Lender?

55350_CL1570_81262_3 05.20.2016 09:03 PMM

Black

4

WHAT IS A HOME EQUITY LINE OF CREDIT?

A home equity line of credit is a form of revolving credit in which yourhome serves as collateral. Because a home often is a consumer’smost valuable asset, many homeowners use home equity credit linesonly for major items, such as education, home improvements, ormedical bills, and choose not to use them for day-to-day expenses.

With a home equity line, you will be approved for a specific amountof credit. Many lenders set the credit limit on a home equity lineby taking a percentage (say, 75 percent) of the home’s appraisedvalue and subtracting from that the balance owed on the existingmortgage. For example:

In determining your actual credit limit, the lender will also consideryour ability to repay the loan (principal and interest) by looking atyour income, debts, and other financial obligations as well as yourcredit history.

Many home equity plans set a fixed period during which you canborrow money, such as 10 years. At the end of this “draw period,”you may be allowed to renew the credit line. If your plan does notallow renewals, you will not be able to borrow additional moneyonce the period has ended. Some plans may call for payment infull of any outstanding balance at the end of the period. Othersmay allow repayment over a fixed period (the “repayment period”),for example, 10 years.

Once approved for a home equity line of credit, you will most likely beable to borrow up to your credit limit whenever you want. Typically,you will use special checks to draw on your line. Under some plans,borrowers can use a credit card or other means to draw on the line.

There may be other limitations on how you use the line. Someplans may require you to borrow a minimum amount each timeyou draw on the line (for example, $300) or keep a minimumamount outstanding. Some plans may also require that you takean initial advance when the line is set up.

What Should You Look for WhenShopping for a Plan?If you decide to apply for a home equity line of credit, look forthe plan that best meets your particular needs. Read the creditagreement carefully, and examine the terms and conditions of variousplans, including the annual percentage rate (APR) and the costs ofestablishing the plan. Remember, though, that the APR for a homeequity line is based on the interest rate alone and will not reflectclosing costs and other fees and charges, so you’ll need to comparethese costs, as well as the APRs, among lenders.

Appraised Value of Home $100,000

Percentage x 75%

Percentage of Appraised Value = $75,000

Less Balance Owed on Mortgage – $40,000

Potential Line of Credit $35,000

55350_CL1570_81262_4 05.20.2016 09:03 PMM

Black

5

Variable Interest Rates

Home equity lines of credit typically involve variable rather thanfixed interest rates. The variable rate must be based on a publiclyavailable index (such as the prime rate published in some major dailynewspapers or a U.S. Treasury bill rate). In such cases, the interestrate you pay for the line of credit will change, mirroring changes in thevalue of the index. Most lenders cite the interest rate you will pay asthe value of the index at a particular time, plus a “margin,” such as2 percentage points. Because the cost of borrowing is tied directlyto the value of the index, it is important to find out which index isused, how often the value of the index changes, and how high it hasrisen in the past. It is also important to note the amount of the margin.

Lenders sometimes offer a temporarily discounted interest ratefor home equity lines—an “introductory” rate that is unusuallylow for a short period, such as six months.

Variable-rate plans secured by a dwelling must, by law, have a ceiling(or cap) on how much your interest rate may increase over the life ofthe plan. Some variable-rate plans limit how much your payment mayincrease and how low your interest rate may fall if the index drops.

Some lenders allow you to convert from a variable rate to a fixedrate during the life of the plan, or let you convert all or a portionof your line to a fixed-term installment loan.

Costs of Establishing and Maintaininga Home Equity LineMany of the costs of setting up a home equity line of credit aresimilar to those you pay when you get a mortgage. For example:l A fee for a property appraisal to estimate the value of your home;l An application fee, which may not be refunded if you are turned

down for credit;l Up-front charges, such as one or more “points” (one point equals

1 percent of the credit limit); andl Closing costs, including fees for attorneys, title search, mortgage

preparation and filing, property and title insurance, and taxes.

In addition, you may be subject to certain fees during the plan period,such as annual membership or maintenance fees and a transactionfee every time you draw on the credit line.

You could find yourself paying hundreds of dollars to establishthe plan. And if you were to draw only a small amount againstyour credit line, those initial charges would substantially increasethe cost of the funds borrowed. On the other hand, because thelender’s risk is lower than for other forms of credit, as your homeserves as collateral, annual percentage rates for home equity linesare generally lower than rates for other types of credit. The interestyou save could offset the costs of establishing and maintaining theline. Moreover, some lenders waive some or all of the closing costs.

How Will You Repay Your Home Equity Plan?Before entering into a plan, consider how you will pay back themoney you borrow. Some plans set a minimum monthly paymentthat includes a portion of the principal (the amount you borrow) plusaccrued interest. But, unlike with typical installment loan agreements,the portion of your payment that goes toward principal may not beenough to repay the principal by the end of the term. Other plans

55350_CL1570_81262_5 05.20.2016 09:03 PMM

Black

6

may allow payment of only the interest during the life of the plan,which means that you pay nothing toward the principal. If you borrow$10,000, you will owe that amount when the payment plan ends.

Regardless of the minimum required payment on your homeequity line, you may choose to pay more, and many lenders offera choice of payment options. However, some lenders may requireyou to pay special fees or penalties if you choose to pay more, socheck with your lender. Many consumers choose to pay down theprincipal regularly as they do with other loans. For example, if youuse your line to buy a boat, you may want to pay it off as you woulda typical boat loan.

Whatever your payment arrangements during the life of theplan—whether you pay some, a little, or none of the principalamount of the loan—when the plan ends, you may have to pay theentire balance owed, all at once. You must be prepared to make this“balloon payment” by refinancing it with the lender, by obtaining aloan from another lender, or by some other means. If you are unableto make the balloon payment, you could lose your home.

If your plan has a variable interest rate, your monthly paymentsmay change. Assume, for example, that you borrow $10,000under a plan that calls for interest-only payments. At a 10 percentinterest rate, your monthly payments would be $83. If the raterises over time to 15 percent, your monthly payments will increaseto $125. Similarly, if you are making payments that cover interestplus some portion of the principal, your monthly payments mayincrease, unless your agreement calls for keeping payments thesame throughout the plan period.

If you sell your home, you will probably be required to pay off yourhome equity line in full immediately. If you are likely to sell your homein the near future, consider whether it makes sense to pay the up-frontcosts of setting up a line of credit. Also keep in mind that renting yourhome may be prohibited under the terms of your agreement.

Line of Credit vs. Traditional SecondMortgage LoansIf you are thinking about a home equity line of credit, you mightalso want to consider a traditional second mortgage loan. This typeof loan provides you with a fixed amount of money, repayable overa fixed period. In most cases, the payment schedule calls for equalpayments that pay off the entire loan within the loan period. Youmight consider a second mortgage instead of a home equity line if,for example, you need a set amount for a specific purpose, such asan addition to your home.

In deciding which type of loan best suits your needs, consider thecosts under the two alternatives. Look at both the APR and othercharges. Do not, however, simply compare the APRs, because theAPRs on the two types of loans are figured differently:l The APR for a traditional second mortgage loan takes into account

the interest rate charged plus points and other finance charges.l The APR for a home equity line of credit is based on the periodic

interest rate alone. It does not include points or other charges.

55350_CL1570_81262_6 05.20.2016 09:03 PMM

Black

7

Disclosures from Lenders

The federal Truth in Lending Act requires lenders to disclose theimportant terms and costs of their home equity plans, including theAPR, miscellaneous charges, the payment terms, and informationabout any variable-rate feature. And in general, neither the lendernor anyone else may charge a fee until after you have receivedthis information. You usually get these disclosures when youreceive an application form, and you will get additional disclosuresbefore the plan is opened. If any term (other than a variable-ratefeature) changes before the plan is opened, the lender mustreturn all fees if you decide not to enter into the plan because ofthe change. Lenders are also required to provide you with a list ofhomeownership counseling organizations in your area.

When you open a home equity line, the transaction puts your homeat risk. If the home involved is your principal dwelling, the Truthin Lending Act gives you three days from the day the account wasopened to cancel the credit line. This right allows you to changeyour mind for any reason. You simply inform the lender in writingwithin the three-day period. The lender must then cancel itssecurity interest in your home and return all fees—including anyapplication and appraisal fees—paid to open the account.

The Home Ownership and Equity Protection Act of 1994 (HOEPA)addresses certain unfair practices and establishes requirements forcertain loans with high rates and fees, including certain additionaldisclosures. HOEPA now covers some HELOCs. You can find outmore information by contacting the CFPB at the website address andphone number listed in the Contact Information appendix, below.

What If the Lender Freezes or Reduces YourLine of Credit?Plans generally permit lenders to freeze or reduce a credit lineif the value of the home “declines significantly” or when thelender “reasonably believes” that you will be unable to makeyour payments due to a “material change” in your financialcircumstances. If this happens, you may want to:l Talk with your lender. Find out what caused the lender to freeze or

reduce your credit line and what, if anything, you can do to restoreit. You may be able to provide additional information to restore yourline of credit, such as documentation showing that your house hasretained its value or that there has not been a “material change” inyour financial circumstances. You may want to get copies of yourcredit reports (go to the CFPB’s website at consumerfinance.gov/askcfpb/5/can-i-review-my-credit-report.html for informationabout how to get free copies of your credit reports) to make sure allthe information in them is correct. If your lender suggests getting anew appraisal, be sure you discuss appraisal firms in advance sothat you know they will accept the new appraisal as valid.

l Shop around for another line of credit. If your lender does not wantto restore your line of credit, shop around to see what other lendershave to offer. If another lender is willing to offer you a line of credit,you may be able to pay off your original line of credit and take outanother one. Keep in mind, however, that you may need to pay someof the same application fees you paid for your original line of credit.

55350_CL1570_81262_7 05.20.2016 09:03 PMM

Black

8

APPENDIX A

Defined Terms

This glossary provides general definitions for terms commonlyused in the real estate market. They may have different legalmeanings depending on the context.

DEFINED TERM

ANNUALMEMBERSHIP ORMAINTENANCE FEE

An annual charge for access to afinancial product such as a line ofcredit, credit card, or account. The feeis charged regardless of whether or notthe product is used.

ANNUALPERCENTAGERATE (APR)

The cost of credit, expressed as ayearly rate. For closed-end credit,such as car loans or mortgages, theAPR includes the interest rate, points,broker fees, and other credit chargesthat the borrower is required to pay.An APR, or an equivalent rate, is notused in leasing agreements.

APPLICATION FEE

Fees charged when you apply for a loanor other credit. These fees may includecharges for property appraisal and acredit report.

BALLOON PAYMENTA large extra payment that may becharged at the end of a mortgage loanor lease.

CAP(INTEREST RATE)

A limit on the amount that yourinterest rate can increase. Two typesof interest-rate caps exist. Periodicadjustment caps limit the interest-rateincrease from one adjustment periodto the next. Lifetime caps limit theinterest-rate increase over the life ofthe loan. By law, all adjustable-ratemortgages have an overall cap.

CLOSING ORSETTLEMENT COSTS

Fees paid when you close (or settle) on aloan. These fees may include applicationfees; title examination, abstract of title,title insurance, and property survey fees;fees for preparing deeds, mortgages, andsettlement documents; attorneys’ fees;recording fees; estimated costs of taxesand insurance; and notary, appraisal, andcredit report fees. Under the Real EstateSettlement Procedures Act, the borrowerreceives a good faith estimate of closingcosts within three days of application.The good faith estimate lists eachexpected cost as an amount or a range.

55350_CL1570_81262_8 05.20.2016 09:03 PMM

Black

9

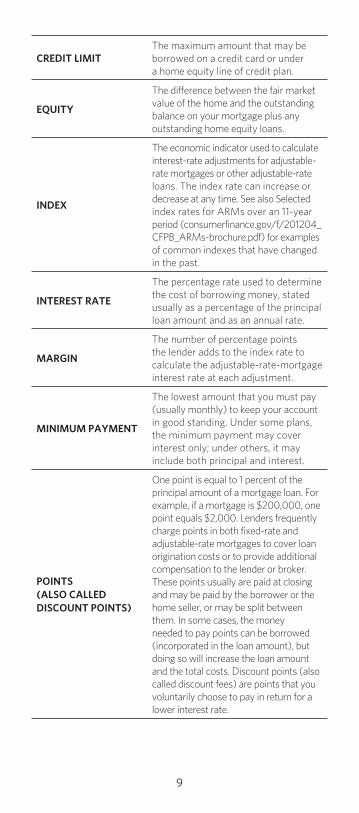

CREDIT LIMITThe maximum amount that may beborrowed on a credit card or undera home equity line of credit plan.

EQUITY

The difference between the fair marketvalue of the home and the outstandingbalance on your mortgage plus anyoutstanding home equity loans.

INDEX

The economic indicator used to calculateinterest-rate adjustments for adjustable-rate mortgages or other adjustable-rateloans. The index rate can increase ordecrease at any time. See also Selectedindex rates for ARMs over an 11-yearperiod (consumerfinance.gov/f/201204_CFPB_ARMs-brochure.pdf) for examplesof common indexes that have changedin the past.

INTEREST RATE

The percentage rate used to determinethe cost of borrowing money, statedusually as a percentage of the principalloan amount and as an annual rate.

MARGIN

The number of percentage pointsthe lender adds to the index rate tocalculate the adjustable-rate-mortgageinterest rate at each adjustment.

MINIMUM PAYMENT

The lowest amount that you must pay(usually monthly) to keep your accountin good standing. Under some plans,the minimum payment may coverinterest only; under others, it mayinclude both principal and interest.

POINTS(ALSO CALLEDDISCOUNT POINTS)

One point is equal to 1 percent of theprincipal amount of a mortgage loan. Forexample, if a mortgage is $200,000, onepoint equals $2,000. Lenders frequentlycharge points in both fixed-rate andadjustable-rate mortgages to cover loanorigination costs or to provide additionalcompensation to the lender or broker.These points usually are paid at closingand may be paid by the borrower or thehome seller, or may be split betweenthem. In some cases, the moneyneeded to pay points can be borrowed(incorporated in the loan amount), butdoing so will increase the loan amountand the total costs. Discount points (alsocalled discount fees) are points that youvoluntarily choose to pay in return for alower interest rate.

55350_CL1570_81262_9 05.20.2016 09:03 PMM

Black

10

SECURITY INTEREST

If stated in your credit agreement, acreditor, lessor, or assignee’s legalright to your property (such as yourhome, stocks, or bonds) that securespayment of your obligation under thecredit agreement. The property thatsecures payment of your obligation isreferred to as “collateral.”

TRANSACTION FEE

Fee charged each time a withdrawalor other specified transaction is madeon a line of credit, such as a balancetransfer fee or a cash advance fee.

VARIABLE RATE

An interest rate that changesperiodically in relation to an index,such as the prime rate. Payments mayincrease or decrease accordingly.

APPENDIX B

More InformationFor more information about mortgages, including home equitylines of credit, visit consumerfinance.gov/mortgage. For answersto questions about mortgages and other financial topics, visitconsumerfinance.gov/askcfpb. You may also visit the CFPB’swebsite at consumerfinance.gov/owning-a-home to accessinteractive tools and resources for mortgage shoppers, whichare expected to be available beginning in 2014.

Housing counselors can be very helpful, especially for first-timehome buyers or if you’re having trouble paying your mortgage.The U.S. Department of Housing and Urban Development (HUD)supports housing counseling agencies throughout the countrythat can provide free or low-cost advice. You can search for HUD-approved housing counseling agencies in your area on the CFPB’sweb site at consumerfinance.gov/find-a-housing-counselor or bycalling HUD’s interactive toll-free number at 800-569-4287.

The company that collects your mortgage payments is your loanservicer. This may not be the same company as your lender. If youhave concerns about how your loan is being serviced or anotheraspect of your mortgage, you may wish to submit a complaintto the CFPB at consumerfinance.gov/complaint or by calling(855) 411-CFPB (2372).

When you submit a complaint to the CFPB, the CFPB will forwardyour complaint to the company and work to get a response.Companies have 15 days to respond to you and the CFPB. You canreview the company’s response and give feedback to the CFPB.

55350_CL1570_81262_10 05.20.2016 09:03 PMM

Black

11

APPENDIX C

Contact InformationFor additional information or to submit a complaint, you can contactthe CFPB or one of the other federal agencies listed below, dependingon the type of institution. If you are not sure which agency to contact,you can submit a complaint to the CFPB and if the CFPB determinesthat another agency would be better able to assist you, the CFPB willrefer your complaint to that agency and let you know.

Regulatory Agency Regulated EntitiesContactInformation

Consumer FinancialProtection Bureau (CFPB)P.O. Box 4503Iowa City, IA 52244

Insured depositoryinstitutions and creditunions with assetsgreater than $10 billion(and their affiliates),and non-bank providersof consumer financialproducts and services,including mortgages,credit cards, debtcollection, consumerreports, prepaid cards,private education loans,and payday lending

(855) 411-CFPB (2372)consumerfinance.govconsumerfinance.gov/complaint

Board of Governors of theFederal Reserve System(FRB)Consumer HelpP.O. Box 1200Minneapolis, MN 55480

Federally insuredstate-charteredbank members ofthe Federal ReserveSystem

(888) 851-1920federalreserveconsumerhelp.gov

Office of the Comptrollerof the Currency (OCC)Customer Assistance Group1301 McKinney StreetSuite 3450Houston, TX 77010

National banks andfederally charteredsavings banks/associations

(800) 613-6743occ.treas.govhelpwithmybank.gov

Federal Deposit InsuranceCorporation (FDIC)Consumer Response Center1100 Walnut StreetBox #11Kansas City, MO 64106

Federally insuredstate-chartered banksthat are not membersof the Federal ReserveSystem

(877) ASK-FDIC or(877) 275-3342fdic.govfdic.gov/consumers

Federal Housing FinanceAgency (FHFA)Consumer CommunicationsConstitution Center400 7th Street, S.W.Washington, DC 20219

Fannie Mae,Freddie Mac, andthe Federal HomeLoan Banks

Consumer Helpline(202) 649-3811fhfa.govwww.fhfa.gov/AboutUs/Contact

55350_CL1570_81262_11 05.20.2016 09:03 PMM

Black

12

Regulatory Agency Regulated EntitiesContactInformation

National Credit UnionAdministration (NCUA)Consumer Assistance1775 Duke StreetAlexandria, VA 22314

Federally charteredcredit unions

(800) 755-1030ncua.govmycreditunion.gov

Federal TradeCommission (FTC)Consumer Response Center600 Pennsylvania Ave.,N.W.Washington, DC 20580

Finance companies,retail stores, autodealers, mortgagecompanies and otherlenders, and creditbureaus

(877) FTC-HELP or(877) 382-4357ftc.govftc.gov/bcp

Securities and ExchangeCommission (SEC)Complaint Center100 F Street, N.E.Washington, DC 20549

Brokerage firms, mutualfund companies, andinvestment advisers

(202) 551-6551sec.govsec.gov/complaint/select.shtml

Farm Credit AdministrationOffice of Congressionaland Public Affairs1501 Farm Credit DriveMcLean, VA 22102

Agricultural lenders (703) 883-4056fca.gov

Small BusinessAdministration (SBA)Consumer Affairs409 3rd Street, S.W.Washington, DC 20416

Small business lenders (800) U-ASK-SBA or(800) 827-5722sba.gov

Commodity FuturesTrading Commission(CFTC)1155 21st Street, N.W.Washington, DC 20581

Commodity brokers,commodity tradingadvisers, commoditypools, and introducingbrokers

(866) 366-2382www.cftc.gov/ConsumerProtection/index.htm

U.S. Department ofJustice (DOJ)Civil Rights Division950 Pennsylvania Ave., N.W.Housing and CivilEnforcement SectionWashington, DC 20530

Fair lending andhousing issues

(202) 514-4713TTY (202) 305-1882FAX (202) 514-1116To report an incident ofhousing discrimination:(800) [email protected]

Department of Housingand Urban Development(HUD)Office of Fair Housing/Equal Opportunity451 7th Street, S.W.Washington, DC 20410

Fair lending andhousing issues

(800) 669-9777hud.gov/complaints

55350_CL1570_81262_12 05.20.2016 09:03 PMM

Black

13

IMPORTANT TERMS OF OURFLEXEQUITY®ACCOUNT

This disclosure contains important information about our FlexEquityline of credit account (the “Account”). You should read it carefullyand keep a copy for your records.

1. Availability of TermsAll of the terms described below are subject to change. If theseterms change (other than a change in the Annual PercentageRate that results from a change in the index value) and, as aresult, you decide not to enter into an agreement with us, youare entitled to a refund of any fees you paid to us or to anyoneelse in connection with your application.

2. Security InterestWe will take a deed of trust on your home. You could lose yourhome if you do not meet the obligations in your agreement with us.

3. Possible Actions We Can Take(a) Termination. If any of the following events occur, we may

terminate your Account, accelerate the Maturity Date andthe Account Balance and require you to pay us the entireoutstanding Account Balance in one payment, or take otherlesser action and charge you certain fees: (i) you engage infraud or material misrepresentation in connection with theAccount; (ii) you do not meet the repayment terms of theAccount; or (iii) your action or inaction adversely affectsthe property securing the Account or our rights in thatproperty.

(b) Suspension. We can temporarily suspend credit privileges foryour Account, refuse to make additional extensions of credit,or reduce your credit limit if: (i) the value of the propertysecuring the Account declines significantly below theappraised value of the appraisal obtained when the Accountwas opened; (ii) we reasonably believe you will not be able tomeet the repayment requirements for the Account due to amaterial change in your financial circumstances; (iii) you arein default of a material obligation in the Account Agreement;(iv) government action (a) prevents us from imposingthe Annual Percentage Rate provided for in the AccountAgreement, or (b) impairs our security interest in your homesuch that the value of our interest in your home is less than120 percent of the credit limit; (v) a regulatory agency hasnotified us that continued advances would constitute anunsafe and unsound practice; or (vi) the maximum AnnualPercentage Rate is reached.

(c) Other Changes. The initial Agreement permits us to makecertain changes to the terms of the Agreement at specifiedtimes or upon the occurrence of specified events.

Upon your request, we will provide you with more specificinformation about when we can take these actions.

55350_CL1570_81262_13 05.20.2016 09:03 PMM

Black

14

4. Draw Period and Repayment PeriodYour rights and obligations under the Account will differdepending on whether your Account is in the “Draw Period” orthe “Repayment Period.” The Draw Period is a 120-month periodduring which you may obtain credit advances subject to the termsof the Account Agreement. The Repayment Period is a 240-monthperiod (or such shorter period as you select) that follows the DrawPeriod and during which you can no longer obtain credit advances.

5. Fixed-Rate Option PlansDuring the Draw Period, your Account balance will be subject toa “Variable Rate Plan” under which a finance charge will accrueat a variable interest rate, except that you may transfer all or aportion of the Account balance to up to four (4) fixed-interest sub-accounts (each, a “Fixed Rate Option Plan”), subject to applicableprovisions of the Account Agreement. You may make such atransfer only once in any 365-day period during the Draw Period.

You may use any one of the following transfer options: (i) you maytransfer all or a portion of your Variable Rate Plan balance to anew Fixed Rate Option Plan; (ii) you may transfer all or a portion ofyour Variable Rate Plan balance to any existing Fixed Rate OptionPlan; (iii) you may combine all or a portion of your Variable RatePlan balance and one or more Fixed Rate Option Plan balances intoone Fixed Rate Option Plan balance; or (iv) you may combine theoutstanding balances under one or more Fixed Rate Option Plansinto a single Fixed Rate Option Plan.

If any portion of the Account balance is subject to the VariableRate Plan as of the expiration of the Draw Period, that portion ofthe balance automatically will be converted to a new Fixed RateOption Plan on the day following the expiration of the Draw Period.This may result in up to five Fixed Rate Option Plans that you arerequired to repay during the Repayment Period.

Any day that a portion of your Account balance is transferred toa new or existing Fixed Rate Option Plan is a “Fixed Rate OptionTransfer Date.”

6. Promotional PricingYou may be eligible to receive a promotional rate for a fixedperiod of time during the Draw Period. During this period, theVariable Rate Plan Portion of your FlexEquity account will besubject to a promotional rate for the first 6 or 12 months of theFlexEquity Agreement. The promotional rate will not be basedon the sum of the index and margin, and will be fixed during thepromotional period. At the end of the promotional period, yourrate will be subject to requirements of the Variable Rate Plan asdescribed in Section 12. The promotional rate is only valid forthe specified 6- or 12-month period and no other discounts areapplicable during this period. The promotional rate may be belowthe Minimum Rate of 3.24% as described in Section 13.

During the Promotional Rate Period (even if your accountagreement provides for payments comprised of principaland interest), the portion of the Minimum Monthly Paymentapplicable to any outstanding Variable Rate Plan balance willbe the sum of (a) the amount of the Finance Charge assessedon the outstanding Variable Rate Plan balance during the billing

55350_CL1570_81262_14 05.20.2016 09:03 PMM

Black

15

cycle, and (b) any past-due amounts of principal and/or interest(excluding late charges and other non-interest fees or charges),but not less than $100 as described in Section 7. When thePromotional Rate Period expires, your payments will be applied asdiscussed in Section 7.

7. Minimum Payment RequirementsYour Minimum Monthly Payment will consist of the sum of:

(a) the monthly payment on the Variable Rate Plan (calculatedin the manner described below), but not less than $100 solong as the sum of the following equals or exceeds $100:(i) the monthly payment on the Variable Rate Plan, asdescribed below, plus (ii) any outstanding principal balanceon the Variable Rate Plan, and

(b) the scheduled monthly payments on all Fixed Rate OptionPlans, calculated in the manner described below.

If your Account Agreement provides for interest-only paymentson the Variable Rate Plan during the Draw Period, the portion ofthe Minimum Monthly Payment applicable to any outstandingVariable Rate Plan balance will be the sum of (a) the amount of theFinance Charge assessed on the outstanding Variable Rate Planbalance during the billing cycle, and (b) any past-due amounts ofprincipal and/or interest (excluding late charges and other non-interest fees or charges).

If your Account Agreement provides for payments comprisedof principal and interest during the Draw Period, the portion ofthe Minimum Monthly Payment applicable to any outstandingVariable Rate Plan balance will be the amount sufficient to repaythe sum of:

(a) an amount equal to the Account Balance divided by thenumber of months remaining in the Draw Period andRepayment Period combined (if your first Minimum MonthlyPayment is for less than a full month, we will divide theAccount Balance by 361), and

(b) the amount of the Finance Charge assessed on your VariableRate Plan balance, and

(c) any past-due amounts of principal and/or interest (excludinglate charges and other non-interest fees or charges).

The result of this calculation will be the new amount of yourMinimum Monthly Payment. This amount can change each monthduring the Draw Period based on the Annual Percentage Rate ineffect that month, the Variable Rate Plan Account Balance as ofthe last day of the applicable Billing Cycle, and the date you makeyour Minimum Monthly Payment. Because the term of the DrawPeriod is 10 years, but we use the number of months remainingthrough the latest Maturity Date to determine your MinimumMonthly Payment, your Minimum Monthly Payments will notbe sufficient to pay the outstanding Variable Rate Plan AccountBalance in full by the Draw Period Expiration Date.

Each Fixed Rate Option Plan monthly payment will be the amountnecessary to repay the applicable Fixed Rate Option Plan balancein substantially equal monthly payments of principal and interestover 240 months from the applicable Fixed Rate Option TransferDate (or such shorter period as you may select at your option).

55350_CL1570_81262_15 05.20.2016 09:03 PMM

Black

16

8. Minimum Payment ExampleIf you select an interest-only payment during the Draw Period,the following example applies: Assume you took a single$10,000 advance at the beginning of the Draw Period, you takeno other credit advances on your Account, you do not transferany portion of your Account balance to a Fixed Rate Option Plan,and you pay only the Minimum Monthly Payment. There wouldbe no reductions made in the outstanding principal balance ofyour Account for payments made during the Draw Period, exceptfor any principal reductions that result when the MinimumMonthly Payment exceeds the amount of the interest due in thebilling cycle. It would take a total of 360 payments to repay the$10,000. If the ANNUAL PERCENTAGE RATE during the DrawPeriod was 7.24% and the ANNUAL PERCENTAGE RATE duringthe Repayment Period was 7.24% (these APRs were effectiveas of March 1, 2016), you would make 120 monthly paymentsof $100.00 during the Draw Period, followed by 240 monthlypayments of $79.02 during the Repayment Period.

If you select a principal and interest payment during the DrawPeriod, the following example applies: Assume you took a single$10,000 advance at the beginning of the Draw Period, you takeno other credit advances on your Account, you do not transferany portion of your Account balance to a Fixed Rate OptionPlan, and you pay only the Minimum Monthly Payment. In thiscase, some but not all of the principal balance of your Accountwould be repaid by the end of the Draw Period. It would takea total of 360 payments to repay the $10,000. If the ANNUALPERCENTAGE RATE during the Draw Period was 7.24% and theANNUAL PERCENTAGE RATE during the Repayment Periodwas 7.24% (these APRs were effective as of March 1, 2016), youwould make 120 monthly payments of $100.00 during the DrawPeriod, followed by 240 monthly payments of $79.02 during theRepayment Period.

9. Fees and ChargesYou must pay an appraisal fee at the time your Account opensthat will cost from $150 up to a maximum of $450. If yourequest an Account with a credit limit exceeding $500,000,you must pay all third party fees (appraisal, title insurance,recording, etc.) to open the Account. These additional feesgenerally total between $350 -$1,200. Upon your request, wewill provide you an itemization of these fees.

If you close your Account and your Account Balance is paid in fullon or before the thirty-six (36) month anniversary of the opening ofyour Account, you will be required to pay an early termination fee.We will waive this fee if you close your Account to obtain a loanfrom us to refinance your existing home loan(s). We will refund thefee if you close the Account because you are selling the propertysecuring the Account and you obtain a new residential mortgageloan from us within six months of the date you close the Account.

We require that the property securing the Account be insured. Askus about our insurance requirements.

55350_CL1570_81262_16 05.20.2016 09:03 PMM

Black

17

10. Transaction RequirementsYou may not request an advance in an amount less than $500.

11. Tax DeductibilityYou should consult a tax advisor regarding the deductibility ofinterest and charges under your Account.

12. Variable-Rate FeatureThe Account has a variable-rate feature, and the Annual PercentageRate (corresponding to the daily periodic rate) and the MinimumMonthly Payment can change as a result. The Annual PercentageRate includes only interest and no other costs. Rate information willbe provided on or with each periodic statement.

(a) Variable Rate Plan Annual Percentage Rate. During the Draw Period,the Annual Percentage Rate for the Variable Rate Plan can changeon the first day of each billing cycle in accordance with a formulaset forth in the Account Agreement. The Annual Percentage Ratewill equal the sum of: (i) a margin value established at the timeyour Account is opened (the “Variable Rate Margin”); and (ii)the value of an index in effect on the first day of the billing cycle(the “Variable Rate Index”). The Variable Rate Index is the PrimeRate as published in the print edition of the Wall Street Journal andshown as “Prime Rate,” or substantially similar words. If more thanone rate is published, we will use the higher rate. The Variable RateMargin will be determined based on a number of factors, includingthe credit limit on your Account at the time the Account is opened(higher credit limits generally result in lower margins).

(b) Fixed Rate Option Plan Annual Percentage Rate(s). The AnnualPercentage Rate and the Minimum Monthly Payment also canchange on each Fixed Rate Option Transfer Date. The AnnualPercentage Rate on any Fixed Rate Option Plan will be the sumof: (i) a margin value established at the time your Accountis opened (the “Fixed Rate Margin”); and (ii) the value of anindex in effect as of the Sunday immediately preceding theapplicable Fixed Rate Option Transfer Date (the “Fixed RateIndex”). The Fixed Rate Index is the nominal monthly averageyield on United States Treasury Securities, adjusted to aconstant maturity of five (5) years, published by the FederalReserve Board of Governors in Federal Reserve StatisticalRelease H.15. The Fixed Rate Margin for a given Fixed RateOption Plan will be determined based on a number of factors,including the principal balance of the Fixed Rate Option Planas of the Fixed Rate Option Transfer Date (higher principalbalances generally result in lower margins). The AccountAgreement will include a schedule identifying the FixedRate Margin(s) applicable to your Account and when thosemargins will apply.

The Annual Percentage Rate for any Fixed Rate Option Plan willremain fixed until any subsequent Fixed Rate Option Transfer Dateon which a portion of the Account balance is transferred to thatFixed Rate Option Plan. At that time, a new Annual PercentageRate will be established for that Fixed Rate Option Plan using theFixed Rate Index and Fixed Rate Index Margin as described above.

55350_CL1570_81262_17 05.20.2016 09:03 PMM

Black

18

We offer a 0.25% ANNUAL PERCENTAGE RATE reduction whenyou enroll to make automatic payments on your Account from aUnion Bank checking or savings account. The reduction will applyonly for the period of time payments are made by automatictransfer from such an account.

Ask us for the current Index values, margins, and AnnualPercentage Rates.

13. Minimum and Maximum RatesThe ANNUAL PERCENTAGE RATE applicable to the VariableRate Plan or to any Fixed Rate Option Plan will never be lessthan 3.24% nor more than 18.00%. Promotional rates may beavailable below the Minimum Rate of 3.24%.

14. Maximum Rate and Payment ExamplesIf you select an interest-only payment during the DrawPeriod, the following example applies: Assume the ANNUALPERCENTAGE RATE equals the maximum rate of 18.00% andyou have an outstanding balance of $10,000. The maximumrate could be reached during the first month of the Draw Period.Your Minimum Monthly Payment during the Draw Period wouldbe 120 interest payments of $147.95. Your Minimum MonthlyPayment during the Repayment Period would be 240 principaland interest payments of $154.45.

If you select a principal and interest payment during theDraw Period, the following example applies: Assume theANNUAL PERCENTAGE RATE equals the maximum rateof 18.00% and you have an outstanding balance of $10,000.The maximum rate could be reached during the first monthof the Draw Period. Your Minimum Monthly Payment duringthe Draw Period would be 120 payments ranging from$175.65 to $126.88. Your Minimum Monthly Payment duringthe Repayment Period would be 240 principal and interestpayments of $103.13.

15. Historical ExampleThe following table shows how the Annual Percentage Rateand the monthly payments for a single $10,000 credit advancewould have changed based on changes in the Variable RateIndex and the Fixed Rate Index over the past 15 years. The tableis based on the values in effect for the respective indices as ofMarch 1 of each year, but index values and payment amountswould have varied during each year. The table assumes that noadditional credit advances were taken, that only the MinimumMonthly Payments were made, and that the rate remainedconstant during each year. While only one payment amount peryear is shown, payments comprised of principal and interestwould have varied during each year for the term of the DrawPeriod. The table does not necessarily indicate how the indicesor payments will change in the future.

55350_CL1570_81262_18 05.20.2016 09:03 PMM

Black

19

Rate History Table – Standard Rate

Draw Period

Year index% Margin1

(%Points)

AnnualPercentageRate

MinimumMonthlyPayment2

(InterestOnly)

MinimumMonthlyPayment2

(Principal &Interest)

2002 4.75% 2.24% 6.99% $100.00 $100.00

2003 4.25% 2.24% 6.49% $100.00 $100.00

2004 4.00% 2.24% 6.24% $100.00 $100.00

2005 5.50% 2.24% 7.74% $100.00 $100.00

2006 7.50% 2.24% 9.74% $100.00 $107.83

2007 8.25% 2.24% 10.49% $100.00 $114.00

2008 6.00% 2.24% 8.24% $100.00 $100.00

2009 3.25% 2.24% 5.49% $100.00 $100.00

2010 3.25% 2.24% 5.49% $100.00 $100.00

2011 3.25% 2.24% 5.49% $100.00 $100.00

RepaymentPeriod

2012 0.84% 8.75% 9.60% $93.84 $93.84

2013 0.81% 8.75% 9.57% $93.65 $93.65

2014 1.65% 8.75% 10.41% $99.21 $99.21

2015 1.39% 8.75% 10.15% $97.48 $97.48

2016 1.22% 8.75% 9.98% $96.35 $96.351 This is a margin we have used recently.2 Some payments reflect the required minimum payment of $100.

Rate History Table – Promotional Rate

Draw Period

Year index% Margin1

(%Points)

AnnualPercentageRate

MinimumMonthlyPayment2

(InterestOnly)

MinimumMonthlyPayment2

(Principal &Interest)

2002 4.75% 2.24% 2.49%3 $100.00 $100.004

2003 4.25% 2.24% 6.49% $100.00 $100.00

2004 4.00% 2.24% 6.24% $100.00 $100.00

2005 5.50% 2.24% 7.74% $100.00 $100.00

2006 7.50% 2.24% 9.74% $100.00 $107.83

2007 8.25% 2.24% 10.49% $100.00 $114.00

2008 6.00% 2.24% 8.24% $100.00 $100.00

2009 3.25% 2.24% 5.49% $100.00 $100.00

2010 3.25% 2.24% 5.49% $100.00 $100.00

2011 3.25% 2.24% 5.49% $100.00 $100.00

RepaymentPeriod

2012 0.84% 8.75% 9.60% $93.84 $93.84

2013 0.81% 8.75% 9.57% $93.65 $93.65

2014 1.65% 8.75% 10.41% $99.21 $99.21

2015 1.39% 8.75% 10.15% $97.48 $97.48

2016 1.22% 8.75% 9.98% $96.35 $96.351 This is a margin we have used recently.2 Some payments reflect the required minimum payment of $100.3 This rate reflects a promotional rate that we have offered recently; your planmight be subject to a different discount amount.

4 During the promotional period, the minimum payment will be applied as describedin Section 6 above.

55350_CL1570_81262_19 05.20.2016 09:03 PMM

Black

20

IMPORTANT TERMS OF OUR REAL ESTATELINE OF CREDIT (“RELOC”) ACCOUNT

This disclosure contains important information about our RELOCaccount (the “Account”). You should read it carefully and keep acopy for your records.

1. Availability of TermsAll of the terms described below are subject to change. If theseterms change (other than a change in the Annual PercentageRate that results from a change in the index value) and, as aresult, you decide not to enter into an agreement with us, youare entitled to a refund of any fees you paid to us or to anyoneelse in connection with your application.

2. Security InterestWe will take a deed of trust on your home. You could lose yourhome if you do not meet the obligations in your agreement with us.

3. Possible Actions We Can Take(a) Termination. If any of the following events occur, we may

terminate your Account, accelerate the Maturity Date andthe Account Balance and require you to pay us the entireoutstanding Account Balance in one payment, or take otherlesser action and charge you certain fees: (i) you engage infraud or material misrepresentation in connection with theAccount; (ii) you do not meet the repayment terms of theAccount; or (iii) your action or inaction adversely affects theproperty securing the Account or our rights in that property.

(b) Suspension. We can temporarily suspend credit privilegesfor your Account, refuse to make additional extensionsof credit, or reduce your credit limit if: (i) the value of theproperty securing the Account declines significantly below theappraised value of the appraisal obtained when the Accountwas opened; (ii) we reasonably believe you will not be able tomeet the repayment requirements for the Account due to amaterial change in your financial circumstances; (iii) you are indefault of a material obligation in the Account Agreement;(iv) government action (a) prevents us from imposingthe Annual Percentage Rate provided for in the AccountAgreement, or (b) impairs our security interest in your homesuch that the value of our interest in your home is less than120 percent of the credit limit; (v) a regulatory agency hasnotified us that continued advances would constitute anunsafe and unsound practice; or (vi) the maximum AnnualPercentage Rate is reached.

(c) Other Changes. The initial Agreement permits us to makecertain changes to the terms of the Agreement at specifiedtimes or upon the occurrence of specified events.

Upon your request, we will provide you with more specificinformation about when we can take these actions.

55350_CL1570_81262_20 05.20.2016 09:03 PMM

Black

21

4. Draw Period and Repayment PeriodYour rights and obligations under the Account will differ dependingon whether your Account is in the “Draw Period” or the “RepaymentPeriod.” The Draw Period is a 120-month period during which youmay obtain credit advances subject to the terms of the AccountAgreement. The Repayment Period is a 240-month period (orsuch shorter period as you select) that follows the Draw Periodand during which you can no longer obtain credit advances.

5. Fixed-Rate Option PlanDuring the Draw Period, your Account balance will be subject toa “Variable Rate Plan” under which a finance charge will accrueat a variable interest rate, except that you may transfer all or aportion of the Account balance to a fixed-interest sub-account(the “Fixed Rate Option Plan”), subject to applicable provisionsof the Account Agreement. You may make such a transfer onlyonce in any 365-day period during the Draw Period.

You may use any one of the following transfer options: (i) if thereis no existing Fixed Rate Option Plan, you may transfer all or aportion of your Variable Rate Plan balance to a newly establishedFixed Rate Option Plan; or (ii) if there is an existing Fixed RateOption Plan, you may transfer all or a portion of your Variable RatePlan balance to that Fixed Rate Option Plan.

If any portion of the Account balance is subject to the VariableRate Plan as of the expiration of the Draw Period, that portion ofthe balance automatically will be converted to a new Fixed RateOption Plan on the day following the expiration of the Draw Period.This may result in up to two Fixed Rate Option Plans that you arerequired to repay during the Repayment Period.

Any day that a portion of your Account balance is transferred toa new or existing Fixed Rate Option Plan is a “Fixed Rate OptionTransfer Date.”

6. Minimum Payment RequirementsYour Minimum Monthly Payment will consist of the sum of:

(a) the monthly payment on the Variable Rate Plan (calculated in themanner described below), if any, but not less than $100 so long asthe sum of the following equals or exceeds $100: (i) the monthlypayment on the Variable Rate Plan, as described below, plus (ii)any outstanding principal balance on the Variable Rate Plan, and

(b) the scheduled monthly payments on each Fixed Rate Option Plan,if any (calculated in the manner described below).

If your Account Agreement provides for interest-only payments on theVariable Rate Plan during the Draw Period, the portion of the MinimumMonthly Payment applicable to any outstanding Variable Rate Planbalance will be the sum of (a) the amount of the Finance Chargeassessed on the outstanding Variable Rate Plan balance during thebilling cycle, and (b) any past-due amounts of principal and/or interest(excluding late charges and other non-interest fees or charges).

If your Account Agreement provides for payments comprised ofprincipal and interest during the Draw Period, the portion of theMinimum Monthly Payment applicable to any outstanding VariableRate Plan balance will be the amount sufficient to repay the sum of:

55350_CL1570_81262_21 05.20.2016 09:03 PMM

Black

22

(a) an amount equal to the Account Balance divided by the numberof months remaining in the Draw Period and Repayment Periodcombined (if your first Minimum Monthly Payment is for less thana full month, we will divide the Account Balance by 361), and

(b) the amount of the Finance Charge assessed on your Variable RatePlan balance, and

(c) any past-due amounts of principal and/or interest (excluding latecharges and other non-interest fees or charges).

The result of this calculation will be the new amount of your MinimumMonthly Payment. This amount can change each month during theDraw Period based on the Annual Percentage Rate in effect thatmonth, the Variable Rate Plan Account Balance as of the last day of theapplicable Billing Cycle, and the date you make your Minimum MonthlyPayment. Because the term of the Draw Period is 10 years, but we usethe number of months remaining through the latest Maturity Date todetermine your Minimum Monthly Payment, your Minimum MonthlyPayments will not be sufficient to pay the outstanding Variable RatePlan Account Balance in full by the Draw Period Expiration Date.

The Fixed Rate Option Plan monthly payment will be the amountnecessary to repay the Fixed Rate Option Plan balance in substantiallyequal monthly payments of principal and interest over 240 monthsfrom the applicable Fixed Rate Option Transfer Date (or such shorterperiod as you may select at your option).

7. Minimum Payment ExampleIf you select an interest-only payment during the Draw Period,the following example applies: Assume you took a single $10,000advance at the beginning of the Draw Period, you take no othercredit advances on your Account, you do not transfer any portionof your Account balance to a Fixed Rate Option Plan, and youpay only the Minimum Monthly Payment. There would be noreductions made in the outstanding principal balance of yourAccount for payments made during the Draw Period, except forany principal reductions that result when the Minimum MonthlyPayment exceeds the amount of the interest due in the billingcycle. It would take a total of 360 payments to repay the $10,000.If the ANNUAL PERCENTAGE RATE during the Draw Periodwas 8.75% and the ANNUAL PERCENTAGE RATE during theRepayment Period was 8.24% (these APRs were effective asof March 1, 2016), you would make 120 monthly payments of$100.00 during the Draw Period, followed by 240 monthlypayments of $85.19 during the Repayment Period.

If you select a principal and interest payment during the Draw Period,the following example applies: Assume you took a single $10,000advance at the beginning of the Draw Period, you take no othercredit advances on your Account, you do not transfer any portionof your Account balance to a Fixed Rate Option Plan, and you payonly the Minimum Monthly Payment. In this case, some but not allof the principal balance of your Account would be repaid by the endof the Draw Period. It would take a total of 360 payments to repaythe $10,000. If the ANNUAL PERCENTAGE RATE during the DrawPeriod was 8.75% and the ANNUAL PERCENTAGE RATE duringthe Repayment Period was 8.24% (these APRs were effectiveas of March 1, 2016), you would make 120 monthly payments

55350_CL1570_81262_22 05.20.2016 09:03 PMM

Black

23

of $100.00 during the Draw Period, followed by 240 monthlypayments of $85.19 during the Repayment Period.

8. Fees and ChargesYou must pay an appraisal fee at the time your Account opens thatwill cost from $150 up to a maximum of $450. If you request anAccount with a credit limit exceeding $500,000, you must pay allthird party fees (appraisal, title insurance, recording, etc.) to openthe Account. These additional fees generally total between $350-$1,200. Upon your request, we will provide you an itemization ofthese fees.

If you close your Account and your Account Balance is paid in fullon or before the thirty-six (36) month anniversary of the openingof your Account, you will be required to pay an early terminationfee. We will waive this fee if you close your Account to obtain a loanfrom us to refinance your existing home loan(s). We will refund thefee if you close the Account because you are selling the propertysecuring the Account and you obtain a new residential mortgageloan from us within six months of the date you close the Account.

We require that the property securing the Account be insured. Askus about our insurance requirements.

9. Transaction RequirementsYou may not request an advance in an amount less than $500.

10. Tax DeductibilityYou should consult a tax advisor regarding the deductibility ofinterest and charges under your Account.

11. Variable-Rate FeatureThe Account has a variable-rate feature, and the Annual PercentageRate (corresponding to the daily periodic rate) and the MinimumMonthly Payment can change as a result. The Annual PercentageRate includes only interest and no other costs. Rate information willbe provided on or with each periodic statement.

(a) Variable Rate Plan Annual Percentage Rate. During the DrawPeriod, the Annual Percentage Rate for the Variable Rate Plancan change on the first day of each billing cycle in accordancewith a formula set forth in the Account Agreement. TheAnnual Percentage Rate will equal the sum of: (i) a margin valueestablished at the time your Account is opened (the “VariableRate Margin”); and (ii) the value of an index in effect on thefirst day of the billing cycle (the “Variable Rate Index”). TheVariable Rate Index is the Prime Rate as published in the printedition of the Wall Street Journal and shown as “Prime Rate,” orsubstantially similar words. If more than one rate is published,we will use the higher rate. The Variable Rate Margin will bedetermined based on a number of factors, including the creditlimit on your Account at the time the Account is opened(higher credit limits generally result in lower margins).

(b) Fixed Rate Option Plan Annual Percentage Rate(s). The AnnualPercentage Rate and the Minimum Monthly Payment also canchange on each Fixed Rate Option Transfer Date. The AnnualPercentage Rate on the Fixed Rate Option Plan, including any

55350_CL1570_81262_23 05.20.2016 09:03 PMM

Black

24

Fixed Rate Option Plan established upon the expiration of theDraw Period, will be the sum of: (i) a margin value establishedat the time your Account is opened (the “Fixed Rate Margin”);and (ii) the value of an index in effect on the Fixed RateTransfer Date. The Fixed Rate Index is the Prime Rate aspublished in the print edition of the Wall Street Journal underand shown as “Prime Rate.” If more than one rate is published,we will use the higher rate. The Fixed Rate Margin for a givenFixed Rate Option Plan will be determined based on a numberof factors, including the principal balance of the Fixed RateOption Plan as of the Fixed Rate Option Transfer Date (higherprincipal balances generally result in lower margins). TheAccount Agreement will include a schedule identifying theFixed Rate Margin(s) applicable to your Account and whenthose margins will apply.

The Annual Percentage Rate will remain fixed until anysubsequent Fixed Rate Option Transfer Date for thatFixed Rate Option Plan, if any. At that time, a new AnnualPercentage Rate will be established using the Fixed RateIndex and Fixed Rate Index Margin as described above.

We offer a 0.25% ANNUAL PERCENTAGE RATE reductionwhen you enroll to make automatic payments on your Accountfrom a Union Bank checking or savings account. The reductionwill apply only for the period of time payments are made byautomatic transfer from such an account.

Ask us for the current Index values, margins, and AnnualPercentage Rates.

12. Minimum and Maximum RatesThe ANNUAL PERCENTAGE RATE applicable to the VariableRate Plan or to any Fixed Rate Option Plan will never be lessthan 3.24% nor more than 18.00%.

13. Maximum Rate and Payment ExamplesIf you select an interest-only payment during the DrawPeriod, the following example applies: Assume the ANNUALPERCENTAGE RATE equals the maximum rate of 18.00% andyou have an outstanding balance of $10,000. The maximumrate could be reached during the first month of the Draw Period.Your Minimum Monthly Payment during the Draw Period wouldbe 120 interest payments of $147.95. Your Minimum MonthlyPayment during the Repayment Period would be 240 principaland interest payments of $154.48.

If you select a principal and interest payment during the DrawPeriod, the following example applies: Assume the ANNUALPERCENTAGE RATE equals the maximum rate of 18.00% andyou have an outstanding balance of $10,000. The maximumrate could be reached during the first month of the Draw Period.Your Minimum Monthly Payment during the Draw Period wouldbe 120 payments of $175.72 to $127.23. Your Minimum MonthlyPayment during the Repayment Period would be 240 principaland interest payments of $103.41.

55350_CL1570_81262_24 05.20.2016 09:03 PMM

Black

25

14. Historical ExampleThe following table shows how the Annual Percentage Rate andthe monthly payments for a single $10,000 credit advance wouldhave changed based on changes in the Variable Rate Index andthe Fixed Rate Index over the past 15 years. The table is basedon the values in effect for the respective indices as of March 1 ofeach year, but index values and payment amounts would havevaried during each year. The table assumes that no additionalcredit advances were taken, that only the Minimum MonthlyPayments were made, and that the rate remained constant duringeach year. While only one payment amount per year is shown,payments comprised of principal and interest would have variedduring each year for the term of the Draw Period. The tabledoes not necessarily indicate how the indices or payments willchange in the future.

RELOC Rate History Table

Draw Period

Year index% Margin1

(%Points)

AnnualPercentageRate

MinimumMonthlyPayment2

(InterestOnly)

MinimumMonthlyPayment2

(Principal &Interest)

2002 4.75% 3.00% 7.75% $100.00 $100.00

2003 4.25% 3.00% 7.25% $100.00 $100.00

2004 4.00% 3.00% 7.00% $100.00 $100.00

2005 5.50% 3.00% 8.50% $100.00 $100.00

2006 7.50% 3.00% 10.50% $100.00 $114.08

2007 8.25% 3.00% 11.25% $100.00 $120.24

2008 6.00% 3.00% 9.00% $100.00 $101.75

2009 3.25% 3.00% 6.25% $100.00 $100.00

2010 3.25% 3.00% 6.25% $100.00 $100.00

2011 3.25% 3.00% 6.25% $100.00 $100.00

RepaymentPeriod

2012 3.25% 8.75% 12.01% $110.17 $110.17

2013 3.25% 8.75% 12.01% $110.17 $110.17

2014 3.25% 8.75% 12.01% $110.17 $110.17

2015 3.25% 8.75% 12.01% $110.17 $110.17

2016 3.50% 8.75% 12.26% $111.92 $111.92

1 This is a margin we have used recently.2 Some payments reflect the required minimum payment of $100.

55350_CL1570_81262_25 05.20.2016 09:03 PMM

Black

With an interest-only mortgage payment, you will not pay down theloan’s principal balance during the interest-only period. Once the interest-only period ends, your payments will increase to pay back the principaland interest. Rates are subject to increase over the life of the loan.Loans subject to credit and collateral approval. Financing available forcollateral in CA, OR, or WA. Restrictions may apply. Terms and conditionssubject to change.

©2016 MUFG Union Bank, N.A. All rights reserved. Member FDIC.Union Bank is a registered trademark and brand name ofMUFG Union Bank, N.A. unionbank.com 81262 (05/16)

55350_CL1570_81262_26 05.20.2016 09:03 PMM

Black