What to do when duties have been imposed? How to Avoid ... to Avoid Circumvention and Fraud to...

22

www.mcguirewoods.com What to do when duties have been imposed? How to Avoid Circumvention and Fraud to Customs Origin Before the Delegation of the Ministry of Industry and Trade of the Socialist Republic of Vietnam 24 June 2014

Transcript of What to do when duties have been imposed? How to Avoid ... to Avoid Circumvention and Fraud to...

www.mcguirewoods.com

What to do when duties have been imposed? How to Avoid Circumvention and Fraud to Customs Origin

Before the Delegation of the Ministry of Industry and Trade of the Socialist Republic of Vietnam 24 June 2014

2 | McGuireWoods

Meet McGuireWoods: Our speakers today

Yves Melin [email protected] +32 2 629 42 26 Rue des Colonies 56 b.3 1000 Brussels

Yongqing Bao [email protected] +32 2 629 42 24 www.mcguirewoods.com

3 | McGuireWoods

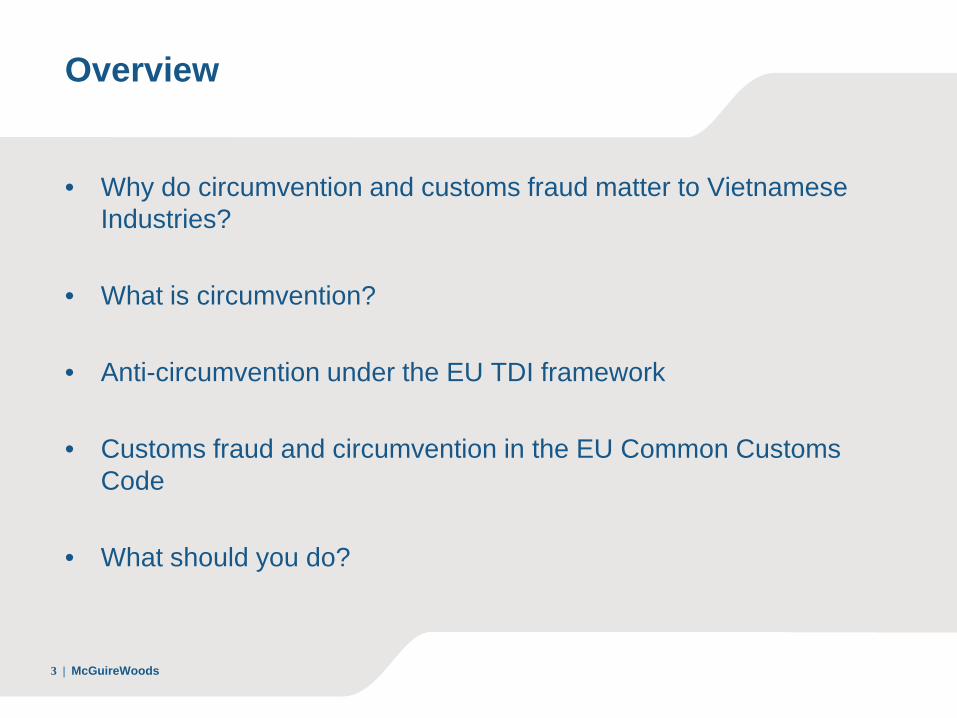

Overview

• Why do circumvention and customs fraud matter to Vietnamese Industries?

• What is circumvention?

• Anti-circumvention under the EU TDI framework

• Customs fraud and circumvention in the EU Common Customs Code

• What should you do?

4 | McGuireWoods

Why do circumvention and customs fraud matter to Vietnamese Industries?

• Application of anti-circumvention rules by the European Commission under the TDI framework – Investigation of nine months – Customs registration of imports and possible retroactive imposition of

anti-dumping/anti-subsidy duties – Extension of residual highest duty initially applied to other countries – Disturbance of export to the EU onwards

• Application of rules of origin by OLAF and EU customs authorities – Investigation of customs fraud – Retroactive collection of customs duties due on imports in the past three

years + interests of the duties unpaid – Likely fines on top of the duties – Possible criminal prosecution in certain Member States

• Conclusion: Enormous legal and commercial exposure

5 | McGuireWoods

What is circumvention?

• Duties (including anti-dumping/anti-subsidy duties) are calculated and imposed on certain product from certain origin (country).

• Two key elements: – Does it fall within the product scope subject to duty ? – Classification – Does it originate in the country/region/exporter subject to duty? – Rules

of origin • Ways of duty evasion/circumvention

– Modifying the product to make it fall out of the scope subject to duty – Change the product origin by:

• Consignment via third countries – Paperwork only (including Certificate of Origin or Preferential origin), e.g. Chinese product transhipped via Vietnam

• Import via the supplier benefiting the lowest duty level • Processing in a third country – Assembly / screw-driving operation in Vietnam

– Where to draw the line?

6 | McGuireWoods

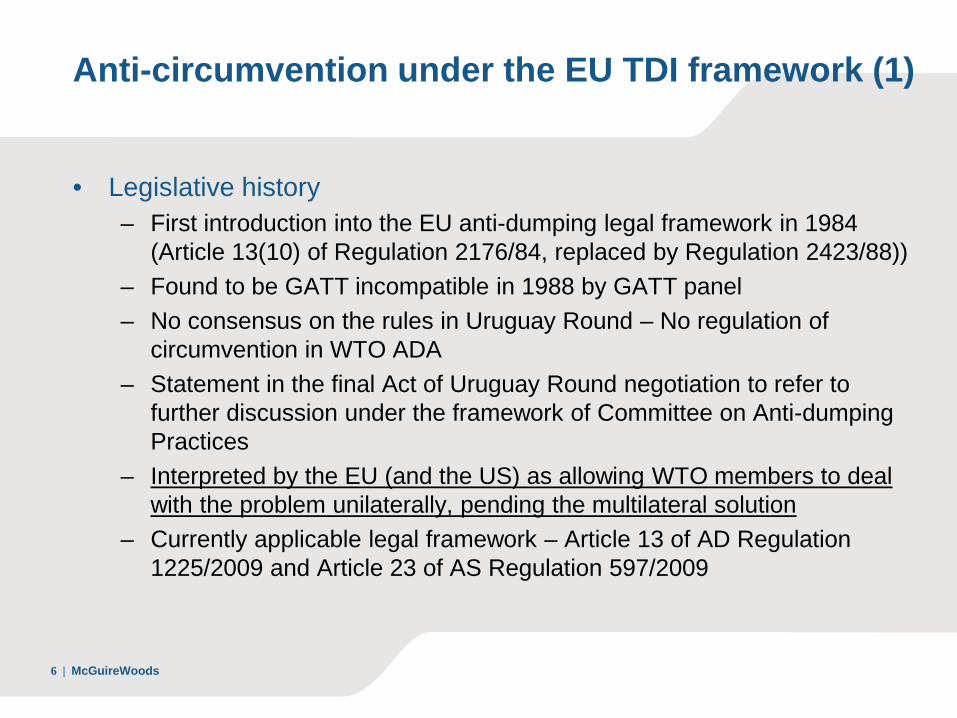

Anti-circumvention under the EU TDI framework (1)

• Legislative history – First introduction into the EU anti-dumping legal framework in 1984

(Article 13(10) of Regulation 2176/84, replaced by Regulation 2423/88)) – Found to be GATT incompatible in 1988 by GATT panel – No consensus on the rules in Uruguay Round – No regulation of

circumvention in WTO ADA – Statement in the final Act of Uruguay Round negotiation to refer to

further discussion under the framework of Committee on Anti-dumping Practices

– Interpreted by the EU (and the US) as allowing WTO members to deal with the problem unilaterally, pending the multilateral solution

– Currently applicable legal framework – Article 13 of AD Regulation 1225/2009 and Article 23 of AS Regulation 597/2009

7 | McGuireWoods

Anti-circumvention under the EU TDI framework (2)

• Conditions for applying anti-circumvention measures – Article 13.1 of the AD Regulation (Article 23.3 of the AS Regulation) – Change in the trade pattern between Vietnam and the EU or between

individual companies in Vietnam and the EU – Practice, process or work without sufficient due cause or economic

justification other than the imposition of the duty – Evidence of injury or that the remedial effects of the duty are being

undermined in terms of the prices and/or quantities of the like product – Evidence of dumping in relation to the normal values previously

established for the like product

8 | McGuireWoods

Anti-circumvention under the EU TDI framework (3)

• Practice, process or work: – Slight modification of the product concerned to make it fall out of the

scope subject to the duty, provided that the modification does not alter its essential characteristics

– Consignment of the product subject to duty via Vietnam – Reorganisation of patterns and channels of sales in Vietnam in order to

eventually have their products exported to the EU through producers benefiting from a lower duty level

– Assembly operation in the EU or Vietnam

9 | McGuireWoods

Anti-circumvention under the EU TDI framework (4)

• Definition of assembly under anti-circumvention rules – Article 13.2 of the AD Regulation – Timing of the start/substantial increase of the operation – Numerical threshold:

• Not less than 60% of value of the parts imported from the country subject to duty

• Less than 25% of added value to the parts – Undermines remedial effect of the duty and evidence of dumping

10 | McGuireWoods

Anti-circumvention under the EU TDI framework (5)

• Anti-circumvention investigation procedure – Initiation ex officio or at the request of Member State or interested party

(complainant) – Immediate customs registration of import since initiation – Investigation and decision making process are similar to normal TDI

investigations – Investigation lasts for nine months – Outcome of investigation: change of product scope / extension of duty

to Vietnam / termination – Possible application for exemption from registration or extension of duty

by genuine Vietnamese producer (Article 13.4 of the AD Regulation and Articles 23.5 and 23.6 of the AS Regulation)

• Affiliation to the producers already subject to duty (e.g. Chinese invested) is relevant but not decisive

11 | McGuireWoods

Anti-circumvention under the EU TDI framework (6)

• Anti-circumvention cases per year

• Total 49 cases since 1995

0

1

2

3

4

5

6

7

8

1995 1996 1997 1998 1999 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

12 | McGuireWoods

Anti-circumvention under the EU TDI framework (7)

• Anti-circumvention cases per original country subject to duty

0

5

10

15

20

25

30

35

40

Belarus Brazil China India Japan Russia Singapore Taiwan Ukraine USA

13 | McGuireWoods

Anti-circumvention under the EU TDI framework (8)

• Anti-circumvention cases per type of circumvention practice

8

1

5 1

65

Slightly modified

Wrong declaration of product

Assembly operation in the EU

Export through lowest duty company

Consignment through third country

14 | McGuireWoods

Anti-circumvention under the EU TDI framework (9)

• Anti-circumvention cases per third country of consignment

0

1

2

3

4

5

6

7

8

9

15 | McGuireWoods

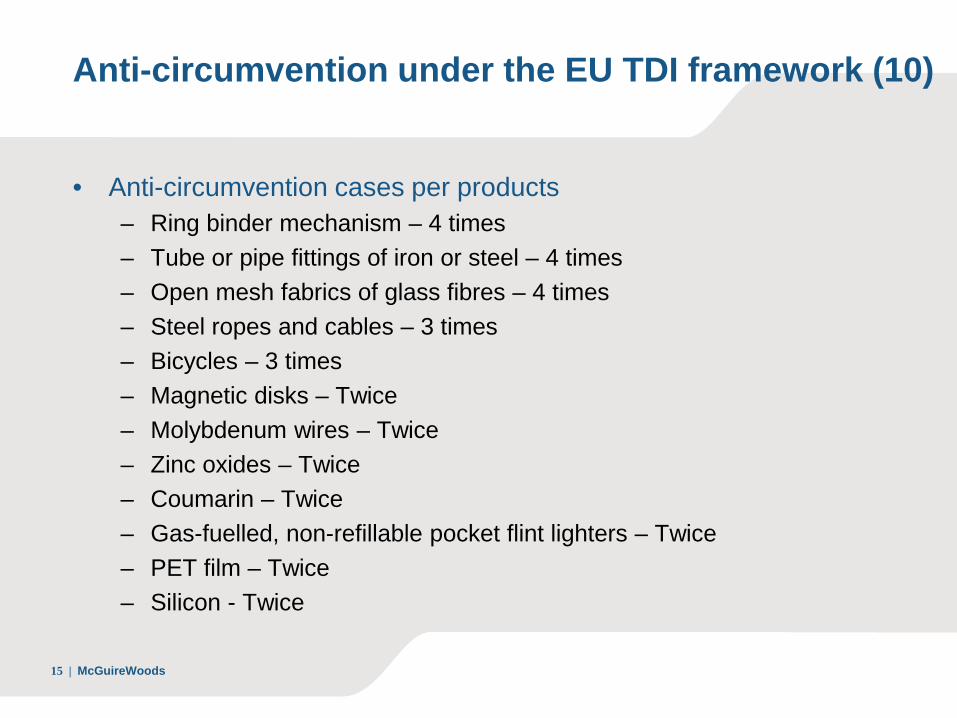

Anti-circumvention under the EU TDI framework (10)

• Anti-circumvention cases per products – Ring binder mechanism – 4 times – Tube or pipe fittings of iron or steel – 4 times – Open mesh fabrics of glass fibres – 4 times – Steel ropes and cables – 3 times – Bicycles – 3 times – Magnetic disks – Twice – Molybdenum wires – Twice – Zinc oxides – Twice – Coumarin – Twice – Gas-fuelled, non-refillable pocket flint lighters – Twice – PET film – Twice – Silicon - Twice

16 | McGuireWoods

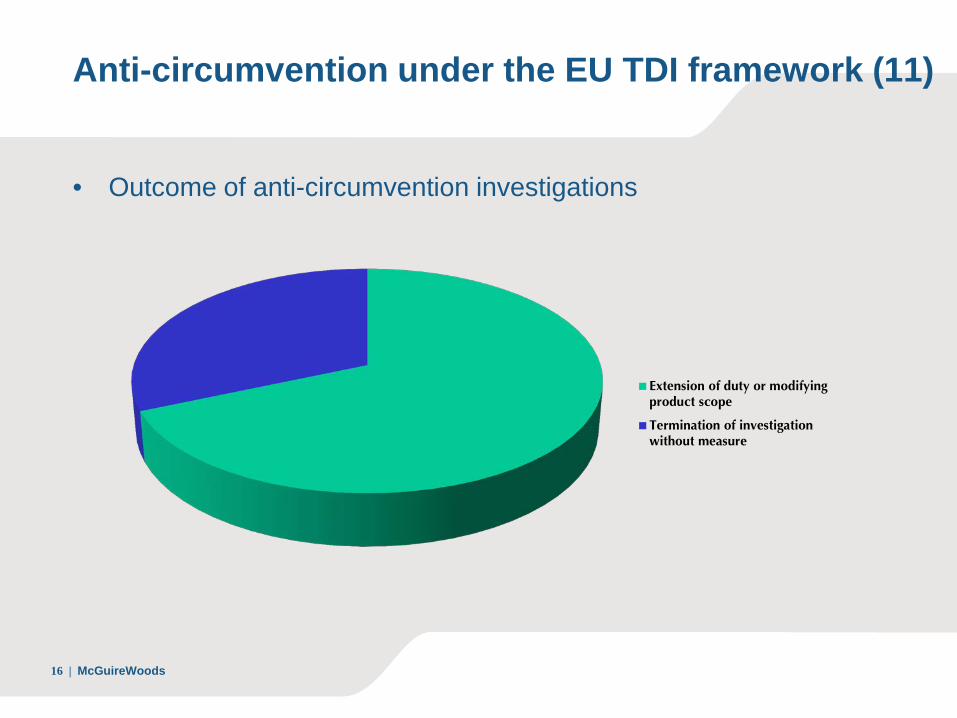

Anti-circumvention under the EU TDI framework (11)

• Outcome of anti-circumvention investigations

Extension of duty or modifyingproduct scope

Termination of investigationwithout measure

17 | McGuireWoods

Anti-circumvention under the EU TDI framework (12)

• Anti-circumvention cases against Vietnam – Zinc oxides from China, consigned from Vietnam (2002) – Ring binder mechanisms from China, consigned from Vietnam (2003) – Integrated electronic compact fluorescent lamps (CFL-i) from China,

consigned from Vietnam (2004) – Gas-fuelled, non-fillable pocket flint lighters from China, consigned from

Vietnam (2012)

18 | McGuireWoods

Customs fraud and circumvention in the EU Common Customs Code (1)

• What is the imported product ? – Product classification

• What is the origin of product ? – Economic nationality of product

• Definition of origin ? – Article 23 and 24 of CCC – Wholly obtained or produced in one country – Article 23 – Production involving more than one country – Article 24

• Where the product undergoes the last, substantial, economically justified processing or working in an undertaking equipped for that purpose and resulting in the manufacture of a new product or representing an important stage of manufacture

• List rules published on the Commission’s website – Non-binding nature – Change of tariff heading – 45% added value – Specific manufacturing stage

19 | McGuireWoods

Customs fraud and circumvention in the EU Common Customs Code (2)

• Non-preferential origin and Preferential origin (e.g. GSP) – Non-preferential origin determines whether anti-dumping/anti-

subsidy duties are applicable – Preferential origin decides whether preferential duty level is

applicable – Attention: a product can aquire preferential origin (e.g., GSP), but

not acquire non-preferential origin the anti-dumping/anti-subsidy duties will apply

• Customs fraud and circumvention behaviors

– Deliberate wrong classification of products – Erroneous declaration of origin (non-preferential and/or preferential) – Undervaluation of imported products

20 | McGuireWoods

Customs fraud and circumvention in the EU Common Customs Code (3)

• Live examples of enforcement by OLAF and Member States customs authorities – Colour TV of false origin declaration (2001) – duty recovery of 18 million

EUR – Chinese bicycles declared as Philippines origin (2003) – duty recovery

of 1.5 million EUR + criminal prosecution – CFL-i lamp transhipped or assembled in third countries (2004) – 13

non-EU countries involved – duty recovery of 30 million EUR + criminal prosecution

– Ring binder mechanism consigned from three non-EU countries (2004) – duty recovery of 6 million EUR + criminal prosecution

– Fake Certificate of Origin over Chinese made textiles imported from Bangladesh (2005) – involving hundreds of importers spread in almost every Member State across the EU – duty recovery of around 30 million EUR + criminal prosecution

– Hand pallet trucks imported from Thailand (2008) – duty recovery of more than 20 million EUR + criminal prosecution

21 | McGuireWoods

What should you do?

• A priori – monitoring and alert system – When issuing Certificate of origin / Certificate of preferential origin – Regularly checking trade statistics concerning products that are

subject to TDI measures

• A posteriori – cooperate in anti-circumvention investigations – Encourage genuine Vietnamese producers to request exemption

during and after the investigation – Customs cooperation

22 | McGuireWoods

Questions or Comments?

Yves Melin [email protected] +32 2 629 42 26 Rue des Colonies 56 b.3 1000 Brussels

Yongqing Bao [email protected] +32 2 629 42 24 www.mcguirewoods.com