WESTERMAN BALL EDERER MILLER Hearing: August...

22

WESTERMAN BALL EDERER MILLER Hearing: August 5, 2016, 10:00 a.m. (ET) ZUCKER & SHARFSTEIN, LLP 1201 RXR Plaza Uniondale, New York 11556 Telephone: (516) 622-9200 Eric G. Waxman III, Esq. Richard F. Harrison, Esq. Attorneys for River Birch Capital LLC UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK -----------------------------------------------------------------------x In re: MOTORS LIQUIDATION COMPANY, f/k/a GENERAL MOTORS CORPORATION, et al., Debtors. -----------------------------------------------------------------------x Chapter 11 Case No. 09-50026 (MG) (Jointly Administered) Adversary Proceeding Case No. 11-09406 (MG) LIMITED OBJECTION TO THE JOINT MOTION OF THE AVOIDANCE ACTION TRUST AND COMMITTEE FOR, AMONG OTHER THINGS, AN ORDER APPROVING THE SETTLEMENT OF THE ALLOCATION DISPUTE, INCLUDING THE LITIGATION COST ADVANCE AGREEMENT 1 River Birch Capital LLC, as the Investment Manager with authority for River Birch Master Fund, LP (“Private Funder”) files this Limited Objection and reservation of rights to the Joint Motion of Motors Liquidation Company Avoidance Action Trust (“Avoidance Action Trust” or “Trust”) and the Official Committee of Unsecured Creditors (“Committee” and together with the Avoidance Action Trust, “Joint Movants”), by which the Joint Movants seek entry of an Order that, among other things, approves the integrated settlement of the Allocation 1 Joint Motion of Motors Liquidation Company Avoidance Action Trust and Official Committee of Unsecured Creditors for Entry of (A) Stipulation and Agreed Order (I) Settling Disputed Entitlements of Debtor-in-Possession Lenders and Official Committee of Unsecured Creditors to Potential Term Loan Avoidance Action Proceeds and (II) Modifying Avoidance Action Trust Agreement to Implement Settlement, and (B) Order (I) Approving Settlement of the Allocation Dispute, (II) Approving Amendments to the Avoidance Action Trust Agreement, and (III) Authorizing the Avoidance Action Trust to Grant an Lien to the DIP Lenders, dated July 15, 2016 [Bankr. Dkt. No. 13688] (“Joint Motion”). Capitalized terms not otherwise defined have the meanings ascribed to them in the Joint Motion. 11-09406-mg Doc 44 Filed 07/28/16 Entered 07/28/16 16:50:59 Main Document Pg 1 of 6

-

Upload

hoangduong -

Category

Documents

-

view

215 -

download

0

Transcript of WESTERMAN BALL EDERER MILLER Hearing: August...

WESTERMAN BALL EDERER MILLER Hearing: August 5, 2016, 10:00 a.m. (ET) ZUCKER & SHARFSTEIN, LLP 1201 RXR Plaza Uniondale, New York 11556 Telephone: (516) 622-9200 Eric G. Waxman III, Esq. Richard F. Harrison, Esq. Attorneys for River Birch Capital LLC UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK

-----------------------------------------------------------------------x In re: MOTORS LIQUIDATION COMPANY, f/k/a GENERAL MOTORS CORPORATION, et al.,

Debtors. -----------------------------------------------------------------------x

Chapter 11

Case No. 09-50026 (MG) (Jointly Administered)

Adversary Proceeding Case No. 11-09406 (MG)

LIMITED OBJECTION TO THE JOINT MOTION OF THE AVOIDANCE ACTION TRUST AND COMMITTEE FOR, AMONG OTHER THINGS, AN

ORDER APPROVING THE SETTLEMENT OF THE ALLOCATION DISPUTE, INCLUDING THE LITIGATION COST ADVANCE AGREEMENT1

River Birch Capital LLC, as the Investment Manager with authority for River Birch

Master Fund, LP (“Private Funder”) files this Limited Objection and reservation of rights to the

Joint Motion of Motors Liquidation Company Avoidance Action Trust (“Avoidance Action

Trust” or “Trust”) and the Official Committee of Unsecured Creditors (“Committee” and

together with the Avoidance Action Trust, “Joint Movants”), by which the Joint Movants seek

entry of an Order that, among other things, approves the integrated settlement of the Allocation

1 Joint Motion of Motors Liquidation Company Avoidance Action Trust and Official Committee of Unsecured Creditors for Entry of (A) Stipulation and Agreed Order (I) Settling Disputed Entitlements of Debtor-in-Possession Lenders and Official Committee of Unsecured Creditors to Potential Term Loan Avoidance Action Proceeds and (II) Modifying Avoidance Action Trust Agreement to Implement Settlement, and (B) Order (I) Approving Settlement of the Allocation Dispute, (II) Approving Amendments to the Avoidance Action Trust Agreement, and (III) Authorizing the Avoidance Action Trust to Grant an Lien to the DIP Lenders, dated July 15, 2016 [Bankr. Dkt. No. 13688] (“Joint Motion”). Capitalized terms not otherwise defined have the meanings ascribed to them in the Joint Motion.

11-09406-mg Doc 44 Filed 07/28/16 Entered 07/28/16 16:50:59 Main Document Pg 1 of 6

2

Dispute2 and implements a Litigation Cost Advance Agreement by which the DIP Lenders loan

$15 million to the Avoidance Action Trust. The Private Funder objects and respectfully states as

follows:

OBJECTION

1. By the Private Litigation Funding Agreement,3 Private Funder agreed to invest

$15 million to provide funding to the Avoidance Action Trust to continue its prosecution of the

Term Loan Avoidance Action (“TLA Action”).4 In exchange, the Private Funder would receive

a return calculated as the greater of (a) 4.75 percent of the aggregate proceeds of the TLA Action

or (b) 2.25 times the amount of the investment drawn by the Avoidance Action Trust.

2. The Private Litigation Funding Agreement is an exclusive agreement with only

limited termination rights in favor of the Avoidance Action Trust. As the agreement was the

result of extensive competitive bidding and arms’ length negotiations, it is not subject to higher

and better offers and does not contain a “fiduciary out.” The Private Litigation Funding

Agreement does permit termination, but only if the DIP Lenders timely provide funding “on

terms materially more favorable to the Trust than those provided by the Investors under this

[Private Litigation Funding] Agreement.”5

2 Official Comm. of Unsecured Creditors of Motors Liquidation Co. v. U.S. Dep’t of Treasury (In re Motors Liquidation Co.), Adv. Pro. No. 11-09406, Dkt. No. 1 (Bankr.S.D.N.Y. June 6, 2011). 3 Funding Agreement dated as of May 19, 2016 among the Avoidance Action Trust, Investors, and U.S. Bank National Association, as Administrative Agent and Collateral Agent (“U.S. Bank”), a copy of which is attached as Exhibit B [Bankr. Dkt. No. 13650-2] to the Motion of the Avoidance Action Trust for an Order Approving the Private Litigation Funding Agreement, dated June 23, 2016 [Bankr. Dkt. No. 13650] (“Private Funding Approval Motion”), and subsequently withdrawn by the Avoidance Action Trust. See Letter to the Court from Counsel to the Avoidance Action Trust, dated July 15, 2016 [Bankr. Dkt. No. 13690]. 4 Motors Liquidation Company Avoidance Action Trust v. JPMorgan Chase Bank, N.A. (In re Motors Liquidation Co.), Adv. Pro. No. 09-00504 (Bankr.S.D.N.Y. July 31, 2009) [Adv. Pro. Dkt. No. 1] (“TLA Action”). 5 See Definition of “Permitted Alternative Funding Event,” Private Litigation Funding Agreement, § 1.1 (emphasis added).

11-09406-mg Doc 44 Filed 07/28/16 Entered 07/28/16 16:50:59 Main Document Pg 2 of 6

3

3. The Joint Motion seeks approval of alternative funding through a $15 million loan

from the DIP Lenders under the Litigation Cost Advance Agreement that is “inextricably linked

to (and conditioned on)” the allocation settlement.6 While the Avoidance Action Trust claims

that a Permitted Alternative Funding Event has occurred under the Private Litigation Funding

Agreement and has acted to terminate that agreement,7 the Private Funder rejects the Trust’s

claim as it is clear that the Litigation Cost Advance Agreement is in no sense “free.” In fact, it is

considerably more expensive than the financing under the Private Litigation Funding Agreement.

4. Critically, the DIP Lenders’ Litigation Cost Advance Agreement is explicitly

conditioned upon approval of the settlement of the Allocation Dispute by which the DIP Lenders

shall receive 30 percent of the proceeds of the TLA Action (after payment of, among other

things, the Litigation Cost Advance). If there is no approval of the 30 percent allocation, there is

no funding. The Joint Movants offer no explanation or rationale for the bundling of the

Litigation Cost Advance Agreement and the Allocation Dispute settlement, but it is clear by the

fact that the cost advance is conditioned on the settlement consideration that some portion of the

settlement payment is being used to pay for the cost advance.8

6 See Joint Motion, ¶ 5, 51 Ex. C. 7 See Letter dated July 15, 2016 from Avoidance Action Trust to Private Funder and U.S., a copy of which is attached as Exhibit A to this Objection. The Private Funder rejects the Avoidance Action Trust’s assertion that a Permitted Alternative Funding Event has occurred. See note 10, infra. 8 The Private Funder requested that both the Avoidance Action Trust and the Committee (a) to provide their analysis of the cost of the Litigation Cost Advance Agreement from the DIP Lenders, including how much the DIP Lenders’ advance would cost if it were unbundled from the Allocation Dispute settlement and (b) whether the DIP Lenders are willing to provide the cost advance on a stand-alone basis. See Letter dated July 21, 2016 from the Private Funder to the Trust and Letter dated July 22, 2016 from the Private Funder to counsel for the Committee, copies of which are attached as Exhibits B and C to this Objection. The Trust responded by Letter dated July 25, 2016 to the Private Funder, a copy of which is attached as Exhibit D to this Objection (“Trust Letter Response”).The Committee responded by letter dated July 27, 2016, a copy of which is attached as Exhibit E to this Objection (the “Committee Response”).

11-09406-mg Doc 44 Filed 07/28/16 Entered 07/28/16 16:50:59 Main Document Pg 3 of 6

4

5. The Trust would have the Court and interested parties believe that “the DIP

Lenders are providing the Trust money at no cost,”9 but this fiction is belied by the DIP Lenders’

requirement that they receive a substantial portion of the TLA Action proceeds in exchange for

the Litigation Cost Advance Agreement. The Joint Movants cannot have it both ways – either

the cost of the Litigation Cost Advance Agreement is all or a meaningful portion of the TLA

Action proceeds or the DIP Lenders should commit to making the Litigation Cost Advance

Agreement even if the Allocation Dispute settlement is rejected.

6. While neither the Trust nor the Committee has conducted any comparative

analysis of the two funding transactions,10 the Motion hints that the DIP Lenders’ loan is, at

best, no better than the Private Litigation Funding Agreement.11 Further, the Committee admits

that it never considered the cost of the Litigation Advance Agreement unbundled from the

settlement, or whether the DIP Lenders would even provide financing that was not being paid for

by the settlement.12 This is a remarkable admission considering the Committee knew that

competitive stand-alone litigation funding was being proposed to the Trust when the Committee

started to consider a bundled proposal from the DIP Lenders.

9 See Trust Letter Response in which the Trust claims that the DIP Lenders’ loan is “at no cost,” baldly asserts that the proceeds of the TLA Action are not “additional consideration” for the loan, and concedes that it has not conducted any “comparative analysis of the two [funding] transactions.” 10 See Exhibit D, Trust Letter Response, and Exhibit E, Committee Response. 11 See Joint Motion at ¶ 50 (the Committee submits that the “cost” of the Allocation Dispute settlement (30%) should be reduced by the cost of litigation funding provided by the DIP Lenders, which the Committee suggests should be calculated at 5 percent -- the approximate cost of the Private Litigation Funding Agreement. 12 See Exhibit E, Committee Response, fn. 2.

11-09406-mg Doc 44 Filed 07/28/16 Entered 07/28/16 16:50:59 Main Document Pg 4 of 6

5

7. The Private Funder has prepared a comparison of the financing costs under both

proposals,13 and in virtually all recovery outcomes under the TLA Action, the DIP Lenders’ cost

advance is materially more expensive than the Private Litigation Funding Agreement -- in

many cases, hundreds of millions of dollars more expensive. Under no reasonable analysis for

recoveries in excess of $77.5 Million, are the terms of the alternative funding “more favorable”

to the Avoidance Action Trust.

13 See AAT Funding Agreement Comparisons attached as Exhibit F to this Objection, comparing payments to the Private Funder and the DIP Lenders under different TLA Action recoveries.

11-09406-mg Doc 44 Filed 07/28/16 Entered 07/28/16 16:50:59 Main Document Pg 5 of 6

6

CONCLUSION AND RESERVATION OF RIGHTS

8. Consequently, a Permitted Alternative Funding Event has not occurred, the

Avoidance Action Trust is not authorized to terminate the Private Litigation Funding Agreement,

and approval of the DIP Lenders’ Litigation Cost Advance Agreement could expose the

Avoidance Action Trust to, among other things, breach of contract claims. The Court should

consider that risk as it evaluates the Joint Motion.

9. The Private Funder reserves all of its rights and remedies and those of the Agent

under the Private Litigation Funding Agreement and applicable law.

Dated: Uniondale, New York July 27, 2016

WESTERMAN BALL EDERER MILLER ZUCKER & SHARFSTEIN, LLP By: /s/Eric G. Waxman III, Esq.

Eric G. Waxman III, Esq. Richard F. Harrison, Esq. 1201 RXR Plaza Uniondale, New York 11556 Telephone: (516) 622-9200 Attorneys for River Birch Capital LLC

1409877.6

11-09406-mg Doc 44 Filed 07/28/16 Entered 07/28/16 16:50:59 Main Document Pg 6 of 6

EXHIBIT A

11-09406-mg Doc 44-1 Filed 07/28/16 Entered 07/28/16 16:50:59 Exhibit A to Objection Pg 1 of 2

Motors Liquidation Company Avoidance Action Trust Wilmington Trust Company, Trustee

1100 N. Market Street Wilmington, DE 19890

July 15, 2016

River Birch Master Fund, LP Grace Building 1114 Avenue of the Americas, 41' Floor New York, NY 10036 Attn: James P. Seery, Jr,

U.S. Bank National Association 214 N. Tryon Street, 27 th Floor Charlotte, NC 28202 Attention: James A. Hanley

Re: Termination of Funding Agreement

Gentlemen:

Reference is made to that certain Funding Agreement, dated as of May 19, 2016 (the "Funding Agreement"), among Motors Liquidation Company Avoidance Action Trust (the "Trust"), the Investors party thereto from time to time (the "Investors"), and U.S. Bank National Association, as Administrative Agent and Collateral Agent (the "Agent"). The purpose of this letter is to provide notice to the Investors and the Agent of (i) the occurrence of a Permitted Alternative Funding Event (as defined in the Funding Agreement) and (ii) the Trust's exercise of the right to terminate the Funding Agreement pursuant to Section 8.1(c) of the Funding Agreement. Pursuant to Section 8.1(c)(i) of the Funding Agreement, the Funding Agreement is hereby terminated and shall be of no further force and effect, with the exception that the Trust shall remain obligated to pay the Closing Expense Payment (as defined in the Funding Agreement) in accordance with the terms of the Funding Agreement.

Sincerely,

MOTORS LIQUIDATION COMPANY AVOIDANCE ACTION TRUST By: Wilmington Trust Company,

acting solely in its capacity as T st Administr for and Trustee

By: — , t ,--..--.17 Name: David A. Vanaskey Jr, Title: Vice President

cc: Arthur J. Gonzalez, Esq. Eric B. Fisher, Esq.

0118917505,1

11-09406-mg Doc 44-1 Filed 07/28/16 Entered 07/28/16 16:50:59 Exhibit A to Objection Pg 2 of 2

EXHIBIT B

11-09406-mg Doc 44-2 Filed 07/28/16 Entered 07/28/16 16:50:59 Errata B to Objection Pg 1 of 3

RIVER BIRCH CAPITAL LLC Grace Building

1114 Avenue of the Americas, 4 V FL New York, New York 10036

July 21, 2016

Mr. David Vanaskey Motors Liquidation Company Avoidance Action Trust Wilmington Trust Company, Trustee 1100 N. Market Street Wilmington, DE 19890 Fax: 302-636-4140 [email protected]

Re: Funding Agreement dated as of May 18, 2016 ("Funding Agreement")

David:

Further to our discussion of Monday, July 18 and my email of that same morning, we are in receipt of your July 15, 2016 letter claiming to terminate the Funding Agreement as a result of a purported Permitted Alternative Funding Event. Based on the limited information provided in the joint motion of the Trust and the Committee of Unsecured Creditors (the "Motion"), it does not appear to us that the conditions for a Permitted Alternative Funding Event have occurred. Accordingly, we do not believe the Trust has the right to terminate the Funding Agreement,

In my conversations with you and Eric, as well as in the Motion, the Trust claims that the DIP Lenders have agreed to provide a "$15 million (interest free) Litigation Cost Advance." However, the cost advance is "inextricably linked to (and conditioned on)" additional valuable consideration being paid to the DIP Lenders. In our view, that additional consideration makes the proposed Litigation Cost Advance materially less favorable to the Trust than the funding provided under the Funding Agreement. In fact, in every Term Loan Avoidance Action outcome in excess of $77.5 million, the DIP Lender's Litigation Cost Advance is more expensive -- and in most eases hundreds of millions of dollars more expensive.... than the funding provided under the Funding Agreement.

Because the Trust, the DIP Lenders and the Committee have chosen to bundle the Litigation Cost Advance and the Allocation Dispute settlement, the exact cost of the advance is obscured. Nonetheless, the Motion effectively admits that the cost advance is not "free," We therefore request that you provide us with the Trust's (and if you have it the Committee's) analysis of the cost of the Litigation Cost Advance, including how much the cost advance would cost if it were unbundled from the settlement. In addition, please provide us with detail on the DIP Lenders' willingness to provide the Litigation Cost Advance on a stand-alone.

Our agreement requires that a Permitted Alternative Funding Event occurs only if the alternative funding is on terms "materially more favorable to the Trust" than those provided under the Funding Agreement. Based on our analysis, the proposed Litigation Cost Advance could cost the Trust nearly $400 million more than the financing under the Funding Agreement. That

11-09406-mg Doc 44-2 Filed 07/28/16 Entered 07/28/16 16:50:59 Errata B to Objection Pg 2 of 3

proposal does not satisfy the conditions required to terminate our agreement. We therefore reserve all of our rights and the rights of the Agent under the Agreement.

Best Re

Ja s P. Seery, Jr.

Partner [email protected]

Cc: Arthur J. Gonzalez Eric B. Fisher James A. Hanley

2

11-09406-mg Doc 44-2 Filed 07/28/16 Entered 07/28/16 16:50:59 Errata B to Objection Pg 3 of 3

EXHIBIT C

11-09406-mg Doc 44-3 Filed 07/28/16 Entered 07/28/16 16:50:59 Exhibit C to Objection Pg 1 of 3

RIVER BIRCH CAPITAL LLC Grace Building

1114 Avenue of the Americas, 41“ New York, New York 10036

July 22, 2016

Robert T. Schmidt, Esq. Kramer Levin Naftalis & Frankel LLP 1177 Avenue of the Americas New York, New York 10036

Re: Funding Agreement dated as of May 18, 2016 ("Funding Agreement")

Bob:

Further to our discussion of Monday, July 18, we received a letter from Wilmington Trust, dated July 15, 2016, claiming to terminate the Funding Agreement as a result of a purported Permitted Alternative Funding Event. Based on the limited information provided in the joint motion of the Trust and the Committee of Unsecured Creditors (the "Motion"), it does not appear to us that the conditions for a Permitted Alternative Funding Event under the Funding Agreement have occurred. Accordingly, we do not believe the Avoidance Action Trust has effectively terminated the Funding Agreement, and the alternative financing that is part of your settlement and attached to the Motion conflicts with our Funding Agreement.

My conversations with Eric as well the Motion indicate that the Trust claims that the DIP Lenders have agreed to provide a "$15 million (interest free) Litigation Cost Advance." However, the cost advance is "inextricably linked to (and conditioned on)" additional valuable consideration being paid to the DIP Lenders. In our view, that additional consideration makes the proposed Litigation Cost Advance materially less favorable to the Trust than the funding provided under the Funding Agreement In fact, in every Term Loan Avoidance Action outcome in excess of $77.5 million, the DIP Lender's Litigation Cost Advance is more expensive -- and in most cases hundreds of millions of dollars more expensive — than the funding provided under the Funding Agreement,

Because the Trust, the DIP Lenders and the Committee have chosen to bundle the Litigation Cost Advance and the Allocation Dispute settlement, the exact cost of the advance is obscured. Nonetheless, the Motion effectively admits that the cost advance is not "free," and the DIP Lenders would not provide the cost advance without the significant additional consideration.

In investigating our rights under the Funding Agreement and our potential objection to the Motion, we request that you immediately provide us with the Committee's analysis of the cost of the Litigation Cost Advance, including how much the cost advance would cost if it were unbundled from the settlement. Please also provide detail as to what lower percentage of the Term Loan Avoidance Action the DIP Lenders would have agreed to if the Creditors' Committee had not required the DIP Lenders to provide the Litigation Cost Advance, In addition, please provide us with detail on the DIP Lenders' willingness to provide the Litigation Cost Advance on a stand-alone basis.

11-09406-mg Doc 44-3 Filed 07/28/16 Entered 07/28/16 16:50:59 Exhibit C to Objection Pg 2 of 3

Best

James P. Seery,

Partner [email protected]

Our Funding Agreement requires that a Permitted Alternative Funding Event occurs only if the alternative funding is on terms "materially more favorable to the Trust" than those provided under the Funding Agreement. Based on our analysis, the proposed Litigation Cost Advance could cost the Trust nearly $400 million more than the financing under the Funding Agreement. That proposal does not satisfy the conditions required to terminate our agreement. We therefore reserve all of our rights and the rights of the Agent under the Agreement as well as all rights with regard to the Motion.

Cc: Arthur J. Gonzalez Eric B. Fisher James A. Hanley

2

11-09406-mg Doc 44-3 Filed 07/28/16 Entered 07/28/16 16:50:59 Exhibit C to Objection Pg 3 of 3

EXHIBIT D

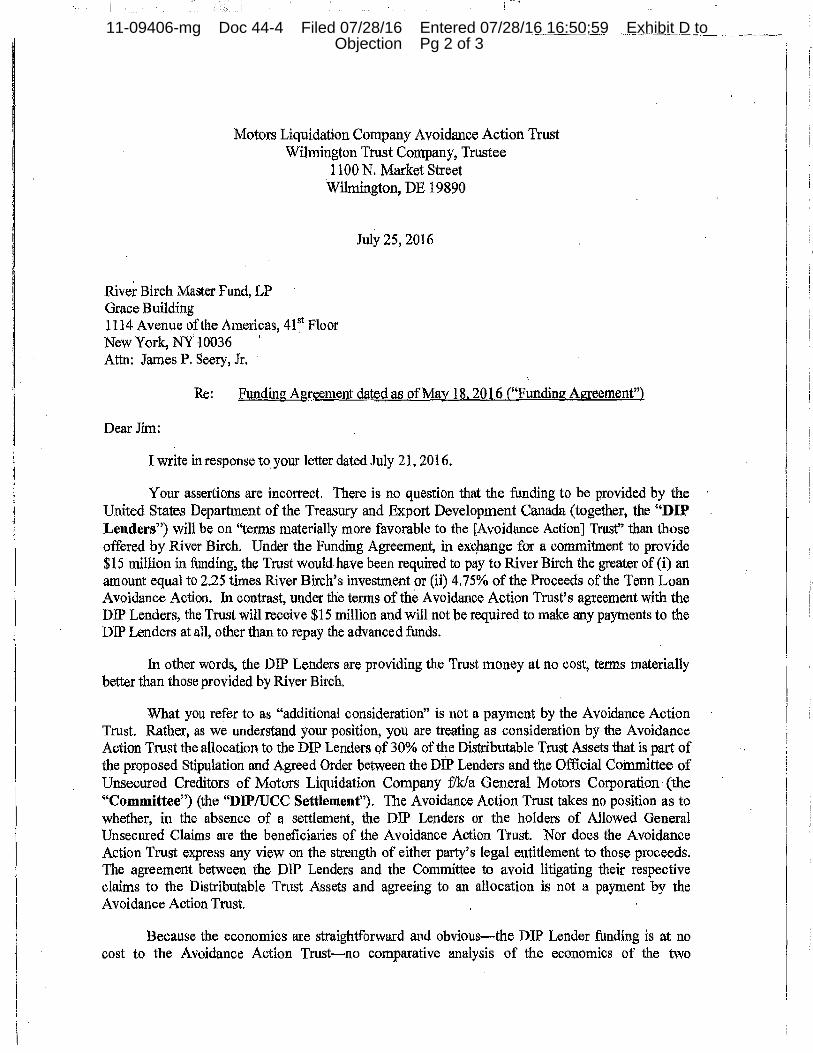

11-09406-mg Doc 44-4 Filed 07/28/16 Entered 07/28/16 16:50:59 Exhibit D to Objection Pg 1 of 3

Motors Liquidation Company Avoidance Action Trust Wilmington Trust Company, Trustee

1100 N. Market Street Wilmington, DE 19890

July 25, 2016

River Birch Master Fund, LP Grace Building 1114 Avenue of the Americas, 4V Floor New York, NY 10036 Attn: James P. Seery, Jr.

Re: Funding Agreement dated as of May 18, 2016 ("Funding Agreement")

Dear Jim:

I write in response to your letter dated July 21, 2016.

Your assertions are incorrect. There is no question that the funding to be provided by the United States Department of the Treasury and Export Development Canada (together, the "DIP Lenders") will be on "terms materially more favorable to the [Avoidance Action] Trust" than those offered by River Birch. Under the Funding Agreement, in exchange for a commitment to provide $15 million in funding, the Trust would have been required to pay to River Birch the greater of (i) an amount equal to 225 times River Birch's investment or (ii) 4,75% of the Proceeds of the Term Loan Avoidance Action. In contrast, under the terms of the Avoidance Action Trust's agreement with the DIP Lenders, the Trust will receive $15 million and will not be required to make any payments to the DIP Lenders at all, other than to repay the advanced funds.

In other words, the DIP Lenders are providing the Trust money at no cost, terms materially better than those provided by River Birch.

What you refer to as "additional consideration" is not a payment by the Avoidance Action Trust, Rather, as we understand your position, you are treating as consideration by the Avoidance Action Trust the allocation to the DIP Lenders of 30% of the Distributable Trust Assets that is part of the proposed Stipulation and Agreed Order between the DIP Lenders and the Official Committee of Unsecured Creditors of Motors Liquidation Company flkla General Motors Corporation (the "Committee") (the "DIP/UCC Settlement"). The Avoidance Action Trust takes no position as to whether, in the absence of a settlement, the DIP Lenders or the holders of Allowed General Unsecured Claims are the beneficiaries of the Avoidance Action Trust. Nor does the Avoidance Action Trust express any view on the strength of either party's legal entitlement to those proceeds. The agreement between the DIP Lenders and the Committee to avoid litigating their respective claims to the Distributable Trust Assets and agreeing to an allocation is not a payment by the Avoidance Action Trust.

Because the economics are straightforward and obvious—the DIP Lender funding is at no cost to the Avoidance Action Trust—no comparative analysis of the economics of the two

11-09406-mg Doc 44-4 Filed 07/28/16 Entered 07/28/16 16:50:59 Exhibit D to Objection Pg 2 of 3

transactions was required. Further, the Avoidance Action Trust does not have non-privileged documents concerning the considerations that caused the Avoidance Action Trust to decide to enter into its agreement with the DIP Lenders.

The Avoidance Action Trust reserves all rights.

Sincerely, MOTORS LIQUIDATION COMPANY AVOIDANCE ACTION TRUST By: Wi mington Trust Company, as

Tru t Administri or and Trust

cc: Arthur J. Gonzalez, Esq. Eric B. Fisher, Esq.

By: - — Name: David A. Vanaskey Jr. Title: Vice President

2

11-09406-mg Doc 44-4 Filed 07/28/16 Entered 07/28/16 16:50:59 Exhibit D to Objection Pg 3 of 3

11-09406-mg Doc 44-5 Filed 07/28/16 Entered 07/28/16 16:50:59 Exhibit E to Objection Pg 1 of 3

K R A M E R L E V I N N A F T A L I S & F R A N K E L L L P

1177 Avenue of the Americas New York NY 10036-2714 Phone 212.715.9100 Fax 212.715.8000 990 Marsh Road Menlo Park CA 94025-1949 Phone 650.752.1700 Fax 650.752.1800

47 Avenue Hoche 75008 Paris France Phone (33-1) 44 09 46 00 Fax (33-1) 44 09 46 01 www.kramerlevin.com

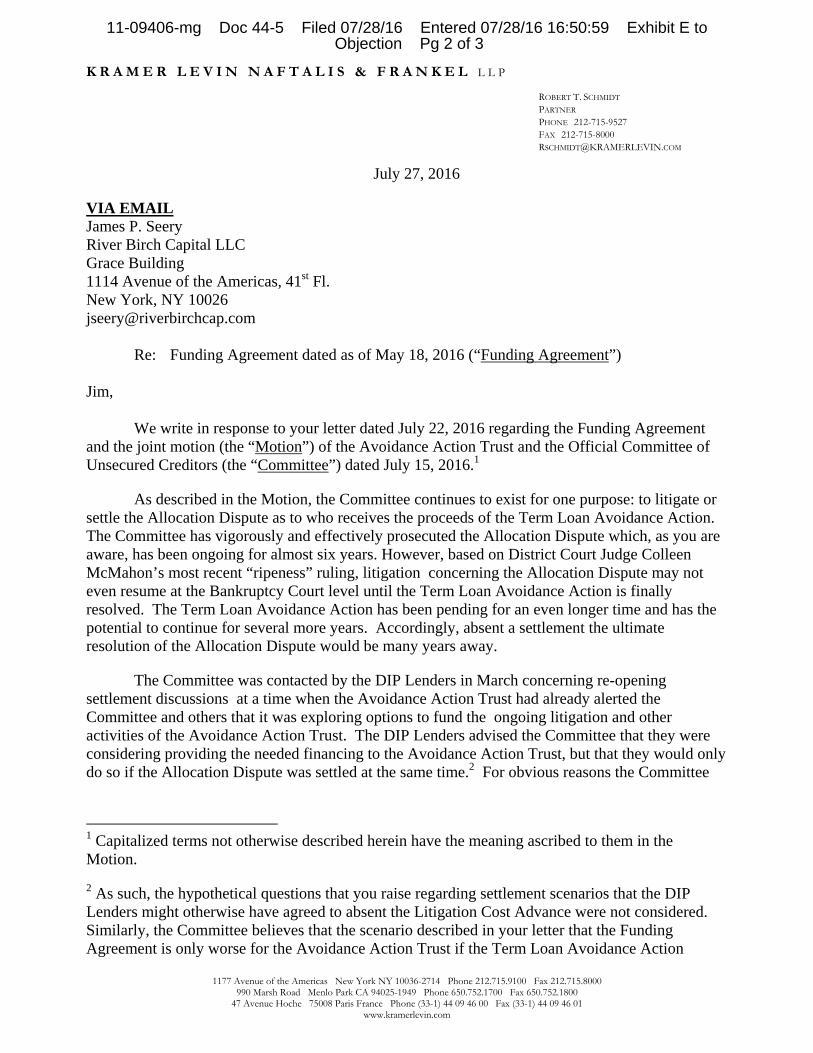

July 27, 2016

VIA EMAIL James P. Seery River Birch Capital LLC Grace Building 1114 Avenue of the Americas, 41st Fl. New York, NY 10026 [email protected]

Re: Funding Agreement dated as of May 18, 2016 (“Funding Agreement”) Jim,

We write in response to your letter dated July 22, 2016 regarding the Funding Agreement and the joint motion (the “Motion”) of the Avoidance Action Trust and the Official Committee of Unsecured Creditors (the “Committee”) dated July 15, 2016.1

As described in the Motion, the Committee continues to exist for one purpose: to litigate or settle the Allocation Dispute as to who receives the proceeds of the Term Loan Avoidance Action. The Committee has vigorously and effectively prosecuted the Allocation Dispute which, as you are aware, has been ongoing for almost six years. However, based on District Court Judge Colleen McMahon’s most recent “ripeness” ruling, litigation concerning the Allocation Dispute may not even resume at the Bankruptcy Court level until the Term Loan Avoidance Action is finally resolved. The Term Loan Avoidance Action has been pending for an even longer time and has the potential to continue for several more years. Accordingly, absent a settlement the ultimate resolution of the Allocation Dispute would be many years away.

The Committee was contacted by the DIP Lenders in March concerning re-opening settlement discussions at a time when the Avoidance Action Trust had already alerted the Committee and others that it was exploring options to fund the ongoing litigation and other activities of the Avoidance Action Trust. The DIP Lenders advised the Committee that they were considering providing the needed financing to the Avoidance Action Trust, but that they would only do so if the Allocation Dispute was settled at the same time.2 For obvious reasons the Committee

1 Capitalized terms not otherwise described herein have the meaning ascribed to them in the Motion.

2 As such, the hypothetical questions that you raise regarding settlement scenarios that the DIP Lenders might otherwise have agreed to absent the Litigation Cost Advance were not considered. Similarly, the Committee believes that the scenario described in your letter that the Funding Agreement is only worse for the Avoidance Action Trust if the Term Loan Avoidance Action

ROBERT T. SCHMIDT PARTNER PHONE 212-715-9527 FAX 212-715-8000 [email protected]

11-09406-mg Doc 44-5 Filed 07/28/16 Entered 07/28/16 16:50:59 Exhibit E to Objection Pg 2 of 3

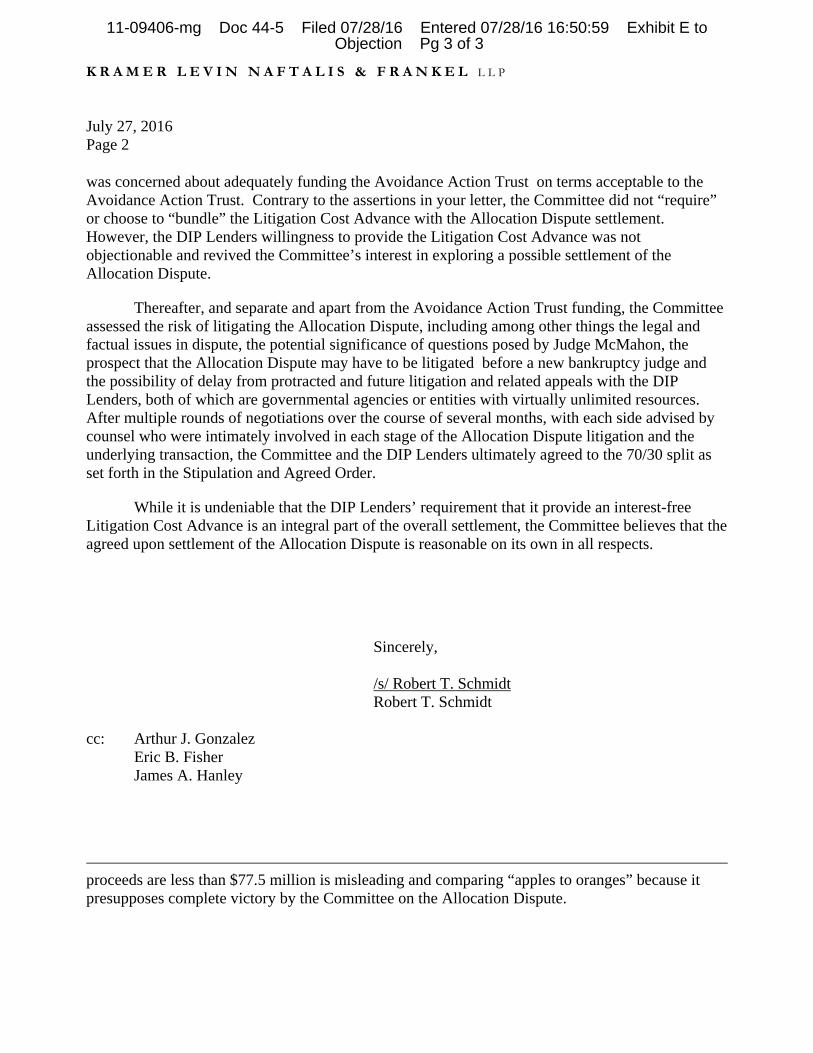

K R A M E R L E V I N N A F T A L I S & F R A N K E L L L P July 27, 2016 Page 2

was concerned about adequately funding the Avoidance Action Trust on terms acceptable to the Avoidance Action Trust. Contrary to the assertions in your letter, the Committee did not “require” or choose to “bundle” the Litigation Cost Advance with the Allocation Dispute settlement. However, the DIP Lenders willingness to provide the Litigation Cost Advance was not objectionable and revived the Committee’s interest in exploring a possible settlement of the Allocation Dispute.

Thereafter, and separate and apart from the Avoidance Action Trust funding, the Committee assessed the risk of litigating the Allocation Dispute, including among other things the legal and factual issues in dispute, the potential significance of questions posed by Judge McMahon, the prospect that the Allocation Dispute may have to be litigated before a new bankruptcy judge and the possibility of delay from protracted and future litigation and related appeals with the DIP Lenders, both of which are governmental agencies or entities with virtually unlimited resources. After multiple rounds of negotiations over the course of several months, with each side advised by counsel who were intimately involved in each stage of the Allocation Dispute litigation and the underlying transaction, the Committee and the DIP Lenders ultimately agreed to the 70/30 split as set forth in the Stipulation and Agreed Order.

While it is undeniable that the DIP Lenders’ requirement that it provide an interest-free Litigation Cost Advance is an integral part of the overall settlement, the Committee believes that the agreed upon settlement of the Allocation Dispute is reasonable on its own in all respects.

Sincerely,

/s/ Robert T. Schmidt Robert T. Schmidt

cc: Arthur J. Gonzalez Eric B. Fisher James A. Hanley

proceeds are less than $77.5 million is misleading and comparing “apples to oranges” because it presupposes complete victory by the Committee on the Allocation Dispute.

11-09406-mg Doc 44-5 Filed 07/28/16 Entered 07/28/16 16:50:59 Exhibit E to Objection Pg 3 of 3

EXHIBIT F

11-09406-mg Doc 44-6 Filed 07/28/16 Entered 07/28/16 16:50:59 Exhibit F to Objection Pg 1 of 2

AAT FUNDING DEAL COMPARISON

Term Loan Litigation Private Funder DIP Lenders Litigation Action Recovery Litigation Cost Cost

$ - $ $ $ 75,000,000.00 $ 33,750,000.00 $ 33,000,000.00

$ 100,000,000.00 $ 33,750,000.00 $ 40,500,000.00

$ 150,000,000.00 $ 33,750,000.00 $ 55,500,000.00

$ 200,000,000.00 $ 33,750,000.00 $ 70,500,000.00

$ 250,000,000.00 $ 33,750,000.00 $ 85,500,000.00

$ 300,000,000.00 $ 33,750,000.00 $ 100,500,000.00

$ 350,000,000.00 $ 33,750,000.00 $ 115,500,000.00

$ 400,000,000.00 $ 33,750,000.00 $ 130,500,000.00

$ 450,000,000.00 $ 33,750,000.00 $ 145,500,000.00

$ 500,000,000.00 $ 33,750,000.00 $ 160,500,000.00

$ 550,000,000.00 $ 33,750,000.00 $ 175,500,000.00

$ 600,000,000.00 $ 33,750,000.00 $ 190,500,000.00

$ 650,000,000.00 $ 33,750,000.00 $ 205,500,000.00

$ 700,000,000.00 $ 33,750,000.00 $ 220,500,000.00

$ 750,000,000.00 $ 35,625,000.00 $ 235,500,000.00

$ 800,000,000.00 $ 38,000,000.00 $ 250,500,000.00

$ 850,000,000,00 $ 40,375,000.00 $ 265,500,000.00

$ 900,000,000.00 $ 42,750,000.00 $ 280,500,000.00

$ 950,000,000.00 $ 45,125,000.00 $ 295,500,000.00

$ 1,000,000,000.00 $ 47,500,000.00 $ 310,500,000.00

$ 1,050,000,000.00 $ 49,875,000.00 $ 325,500,000.00

$ 1,100,000,000.00 $ 52,250,000.00 $ 340,500,000.00

$ 1,150,000,000.00 $ 54,625,000.00 $ 355,500,000.00

$ 1,200,000,000.00 $ 57,000,000.00 $ 370,500,000.00

$ 1,250,000,000.00 $ 59,375,000.00 $ 385,500,000.00

$ 1,300,000,000,00 $ 61,750,000.00 $ 400,500,000.00

$ 1,350,000,000.00 $ 64,125,000.00 $ 415,500,000.00

$ 1,400,000,000.00 $ 66,500,000.00 $ 430,500,000.00

$ 1,450,000,000.00 $ 68,875,000.00 $ 445,500,000.00

$ 1,500,000,000.00 $ 71,250,000.00 $ 460,500,000.00

11-09406-mg Doc 44-6 Filed 07/28/16 Entered 07/28/16 16:50:59 Exhibit F to Objection Pg 2 of 2