Mysterious connection of Elizabeth Riley ... - John Riley, Sr.

2007 Annual Report

We’ll help you get

THERE

Getting THERE can start here. One of the biggest obstacles to getting there issimply making sense of all the options.MassMutual’s Web site is a great first step youcan take on your own. Not only can you learnabout our products, services and people, you canuse some innovative tools to help make sense oflife insurance, retirement savings and more. And you can do it all quickly, from anywhere,anytime – which takes care of a couple of other obstacles.

Some things you can do at MassMutual.com:• Discover the “Top 10 Questions” to help you

get there.

• Take the next step after major events such aschanging jobs, buying a home, losing a loved one orstarting a business.

• View and manage your MassMutual retirementsavings account.

• Calculate how much life insurance you might need.

• Study up on financial markets.

• Learn some financial strategies for your business.

• Investigate a career with MassMutual.

• Find a MassMutual financial professional officenear you.

1

There is a place where you feel good about your future. Where you’re confidentthat you’re taking smart steps today, for tomorrow. Where you’re comfortablethat you’re doing all you can for yourself and the people you care about.

When it comes to your financial life, getting there doesn’t mean reaching somefar-off destination. There is having peace of mind right now. Because you’re notjust thinking about the things you really should do. You’re actually doing them.

It’s a great place to be. And, at MassMutual, we’ll help you get there.

Hello. Are you

Table of ContentsLetter to Policyholders 2 MassMutual – Helping you get THERE 6 Business Highlights 20

Financial Statements 26 General Agencies and Other Offices 84 Senior Management 87

Board of Directors 88

MassMutual Financial Group is a marketing name for Massachusetts Mutual Life Insurance Company(MassMutual) and its affiliated companies and sales representatives. Securities offered throughregistered representatives of MML Investors Services, Inc., 1295 State Street, Springfield, MA 01111.

THERE

If you’re like most people, taking care of yourinsurance and retirement needs isn’t the first thingyou think of in the morning. But it may be whatkeeps you up at night.

Sometimes, no matter how badly we want to takeaction and put those worries to rest, we just can’tseem to make it happen on our own. Maybe wedon’t have enough information. Maybe we havetoo much. If you’re looking for someone to workwith you on your own terms and at your own pace, Ibelieve that MassMutual and its affiliates can helpyou move forward.

2

Stuart H. Reese, Chairman,President and Chief Executive Officer

When we say, “We’ll help you get there,” we’re nottalking about some far-off destination – we’retalking about that next step, the action you mayneed to take today to help secure your familytomorrow. Our goal is to help our clients take thenext step that’s right for them, whether thatinvolves a product purchase or not.

We do this through local financial professionalswho spend time and listen to you tell them aboutyourself and your unique financial needs. That isalso true when our client is a company. With a401(k) plan, for example, we focus onunderstanding what keeps individuals from saving for retirement, and then finding or building the right mix of tools and information to help them take action.

For example, our advanced analytics allow us tohelp plan participants manage their retirementsavings more simply and more effectively.

As a mutual company, we measureaccomplishments a little differently, because we’re owned by our members. Yes, we need todeliver strong financial results on a yearly basis,and we certainly did that in 2007.

THERE

3

“We’re here because you can’t

by yourself.”always get

For example:

• Dividends to eligible participating policyholderswere $1.37 billion, a 12 percent increase.

• Premium and other deposits totaled $29.4 billion,up 12 percent.

• All major business segments saw double-digitsales growth.

• Assets under management by MassMutual andits family of companies, which include the assetsmanaged by our subsidiaries OppenheimerFunds,Babson Capital Management and Baring AssetManagement, rose 11 percent to $505.4 billion.

• Statutory total adjusted capital totaled $10.3billion, up 9 percent.

Just as important, we continue to invest energy inmaintaining our mutual form of ownership, so wecan continue to offer you the strength, stability, andlong-term focus you have come to expect fromMassMutual. My goal is to ensure that all of ourbusinesses directly support our core insuranceoperations and reinforce a product portfoliodesigned to meet our policyholders’ and customers’needs over the long term. We work closely withour Board of Directors throughout the year insupport of our goals.

In 2007, we enhanced several of our core productslike whole life insurance, disability incomeinsurance, and retirement annuities, givingMassMutual policyholders the flexibility to useproven products – backed by our exceptionalfinancial strength – to address some of the newrisks and responsibilities of today’s economicenvironment. For example, MassMutual provides a

4

Dividends to Policyholders (in Millions)

$1,098$996

$1,155$1,226

$1,373

’07’03 ’04 ’05 ’06

Half PageA

MassMutual Financial Group’s Enterprise-wide MeasuresIn Millions 2007 2006 % ChangeAssets Under Management $505,445 $455,723 11%Worldwide Insurance In Force 502,571 472,512 6%Premium & Other Deposits 29,438 26,268 12%

Sales:U.S. Insurance Group 1,513 1,350 12%Retirement 5,953 5,023 19%

Financial Highlights

Premium & Other Deposits(in Billions)

$20$23

$25 $26$29

’07’03 ’04 ’05 ’06

Assets Under Management(in Billions)

$285$326

$396$456

$505

’07’03 ’04 ’05 ’06

Worldwide Insurance In Force(in Billions)

$415 $433 $447 $473$503

’07’03 ’04 ’05 ’06

We’ll help you get

THERESM

Financial Highlights

Consolidated Statutory Results*

In Millions 2007 2006 % Change

Dividends to Policyholders $ 1,373 $ 1,226 12%

Net Gain from Operations 656 561 17%

U.S. Whole Life Sales 269 256 5%

Life Company Assets 131,491 122,155 8%

Life Company Liabilities 123,487 115,128 7%

Total Adjusted Capital 10,294 9,428 9%

* These consolidated results of Massachusetts Mutual Life Insurance Company also include its U.S.-domiciled wholly-owned subsidiaries: MMLBay State Life Ins. Co., C.M. Life Ins. Co., CM Benefit Ins. Co. and CM Assurance Co. Copies of the separate company audited statutory financialstatements are available to policyholders upon written request. CM Benefit Ins. Co. and CM Assurance Co. were liquidated in the fourth quarter of2006. The results of these subsidiaries are included in the consolidated statutory financial statements through the date of liquidation.

Life Company Assets(in Billions)

$97$108 $114

$122$131

’07’03 ’04 ’05 ’06

Total Adjusted Capital(in Millions)

$7,753 $7,978$8,787

$9,428$10,294

’07’03 ’04 ’05 ’06

U.S. Whole Life Sales(in Millions)

$182$214 $207

$256 $269

’07’03 ’04 ’05 ’06

managed account program that allows clientsgreater flexibility to help meet their wealth andincome needs in retirement.

We continued to expand our nationwide network oflocal financial professionals, and to strengthen ourcommitment to training and supporting them. Werealize that many, if not most, of our customersneed and want a trusted ally to help them movetheir financial strategy forward. MassMutual isideally positioned to help them take that next step.

In addition to our business success, I am proud ofthe community contributions MassMutual and ourfinancial professionals make in our home officeregion, across the country and around the world.Our Corporate Responsibility Report is nowavailable at MassMutual.com and provides acomplete picture of these numerous philanthropicand community programs.

I am thankful to the MassMutual policyholders andcustomers who place their confidence inMassMutual. We are committed to doing our partto help you get there. I also thank the policyholdersand customers who let us highlight their stories inthis report. Your stories inspire us.

If you are not yet a MassMutual customer, we hopethis report motivates you to take a look at us andtake the next step – whether that means visitingMassMutual.com, contacting one of our localoffices, or simply sharing this report with someoneyou trust to get a second opinion. I believe that ifyou give MassMutual a chance to get to know youand your financial needs, you could be well on yourway to getting past the obstacles you face, andmaybe to getting a better night’s sleep.

February 22, 2008

We’ll help you get

THERE

5

Stuart H. ReeseChairman, President and Chief Executive Officer

SM

But we also see the obstacles in your way.You don’t have enough time. It’s tooconfusing. So many choices. Who do you trust?

We understand what can prevent you fromtaking action. We don’t think you or anyoneelse should let that stand in the way ofbuilding your financial future.

At MassMutual, we strive to remove thoseobstacles from your path. We help simplify theprocess and present you with meaningful,manageable next steps you can take with ease andconfidence. So you’re moving in the right direction.And you know it.

How we help you get thereExperienced people. Exceptional products. And arealistic, needs-based approach to your financialstrategy. It’s not about fitting you into a category orrushing you into a sale. We work closely with youto understand your unique situation and goals, andhelp you understand your options. Then, we helpyou focus on the right thing to do right now. Andwe work to establish a long-term relationship, sowe can continue providing help with that next stepthroughout your life.

6

Half PageB

THERE

We picture a worldwhere everyone is

MEET Mark:When Mark and Kathy Wendling met with MassMutualfinancial professional, Thomas Waring, Jr., they decided toget life insurance. They were young and healthy, building ahouse, starting a family. No one expected that only daysafter Riley was born, Kathy would die. She was 28.

Mark is now a full-time dentist, a partner in a busy dentalgroup. Riley’s kindergarten teacher says she is a delight tohave in the classroom. Later this year, Mark plans tomarry his fiancé, Katie Bajak. Riley is helping with thewedding plans.

Shown left to right: Riley and Mark Wendling, Katie Bajak.

“Riley turned five a few months

ago and began kindergarten in the

fall. It’s been a long and difficult

journey, but having the financial

freedom that life insurance

provided gave me the chance to

focus on what I love, and what was

important to me – my daughter.”

Mark S. Wendling, D.D.S.

The people helping you get thereMassMutual and its family of companies isthousands of dedicated men and womenworldwide. We’re the local financial professionalsyou can get to know and work with one-on-one.We’re the forward-thinking experts who developinnovative products and ideas. We’re thesupportive customer service representatives wholet you know you’re not alone.

We are one of the most respected life insurancecompanies in the world. And we’ve been helpingpeople like you get there since 1851. Today, weserve individuals and businesses worldwide with abroad product portfolio of life insurance, annuities,long-term care insurance, disability incomeinsurance, executive benefits, investment products,retirement plans and more.

With the right people on your side, the obstacles inyour way may not seem so big. You can get pastthem and get there. In fact, we believe everyone can.

THERE

7

We picture a worldwhere everyone is

For many, the most satisfying ”there”is knowing your family will be financially secure if you’re not around.

If you have a spouse, child, life partner, orbusiness partner, it’s natural to wonder whatwould happen to them if something happensto you. That’s life.

Knowing the people you care about are financiallyprotected – that’s life insurance. At MassMutual,we sold our first life insurance policy in 1851. Andmore than 156 years later, we’re still helping toprovide financial security to those who seek it.

Starting with LifeWhole life insurance is at the heart of our company,our strategy, our insurance portfolio, and ourmutual ownership. For many of our policyholders,whole life insurance is also at the heart of theirfinancial strategy, providing not only protection forthose left behind, but the flexibility to meet avariety of financial needs throughout their lives.

MassMutual offers a broad range of choices inaddition to whole life because choosing the right lifeinsurance is the first step to getting there. In otherwords, start here. And once you know your lovedones or your business will be protected, you canmove on to your other financial needs and goals.

8

THERENext time your child asks,

yet?”“Are we

just smile and say, “Absolutely.”

Half PageC

MEET Jason and Karen:Karen E. Smith is president of Troy Belting & Supply Co.in Watervliet, New York. Her son, Jason, is an officer ofthe company’s Board of Directors and serves as powergeneration manager. Working with MassMutualfinancial professional Todd McDonald, the Smith familyused MassMutual life insurance products to build theirbusiness succession plan.

Employing more than 70 people, Troy Belting sells powertransmission, power distribution, material handling,motor sales and service, and related specialized equipment and services to the industrial, mining andcommercial markets of the northeastern United States.

“The Monday morning after my husband

passed away, we gathered our employees

together and told them, ‘Everything will be

fine.’ I cannot express how much it meant to

be able to say that to them. George always

said, ‘We are stewards of our family’s

business for the next generation.’”

Karen E. Smith, President,

Troy Belting & Supply Co.

Making Sense of LifeThere are so many choices. And so many ways lifeinsurance can contribute to a smarter financialstrategy. But with a little help, determining theright products and coverage can be much simplerthan you think. Wherever you live or work, you cansit down with a MassMutual financial professionaland feel confident that you’re receiving helpfuladvice and service – and that you’re taking a smartfirst step.

Affording LifeWe believe even people who think they can’t affordlife insurance can’t afford to go without it. In mostcases, you can achieve a level of protection nomatter what your budget. Part of our approach is tohelp you understand the value of life insurance andfind a next step that you can manage.

MassMutual is so dedicated to this notion that in2002 we launched the innovative LifeBridgeSM FreeLife Insurance Program. The program provides free

term life insurance, paying the premiums forparents or guardians who meet certain eligibilityrequirements. If an insured parent or guardian diesduring the 10-year term, the $50,000 benefit fundsa trust serviced by our trust company to pay foreligible dependent children’s educational expenses.As of year-end 2007, we’ve given away more than$390 million worth of life insurance coveragethrough the LifeBridge program.

For a LifetimeEssentially, life insurance is a promise you make tofinancially protect your family, business or estate.And MassMutual helps you keep your promise. Our financial strength and stability through theyears is evidence you can lean on to believe we willbe there for you and your family far into the future.

9

THERENext time your child asks,

yet?”“Are we

just smile and say, “Absolutely.”

If one thing is certain today, it’s that you can’tbe certain about what will happen tomorrow.You can, however, be certain that you’vetaken action to help protect yourself and yourfamily from a number of life’s risks.

What if you become disabled?It can be remarkably comforting to know that thelifestyle you’ve worked so hard to give your familywon’t be taken away in the blink of an eye.MassMutual offers disability income insurance tohelp protect a portion of your earnings should youbecome unable to work due to the potentiallydevastating effects of disability. One ofMassMutual’s innovative products can even helpyou protect the retirement contributions you wouldhave made to your retirement savings in the eventthat you become totally disabled.

What if you or a loved one needs long-termor special care?If you or a loved one can no longer liveindependently because of a chronic, long-termmedical condition, the costs can be staggering. Thissituation is becoming more and more common ashealth care costs rise, people live longer, andfamilies take on more financial responsibility forhealth care expenses. MassMutual can cover youor a loved one, helping pay the costs of necessary

10

THERE

Where there’s a risk, there’s a

Half PageD

MEET Rick:Rick Guerra has been married 25 years and is thefather of three “beautiful daughters, who look liketheir mother.” As a new car sales manager, Rick washonored for his exceptional work in sales, training,and customer satisfaction.

Prior to Rick’s stroke, he and his wife bought theirdream house. Today, they still live there, thanks inpart to his MassMutual disability income insurance.

Rick’s unexpected challenge has changed his life.These days, he hopes his story can help others realizethe importance of preparing for the unexpectedturns life can take. So along with insurance help,MassMutual financial professional Pete Lewis isalso helping Rick share his story more broadly.

“My uncle taught me to save 10 percent of

every dollar I earned. He also said I needed

two kinds of insurance: life and disability

income. When I had a stroke at age 45, I was

really scared, but I also knew I was lucky to

have taken my uncle’s advice.”

Rick Guerra, San Antonio, TX

medical and personal care, and helping protectretirement savings and other financial assets in atime of need.

In addition, if you’re caring for a person with adisability or other special need, health issues areonly the beginning. Life’s challenges may alsoinclude earning or supplementing an income,creating a safe and accessible living environment,fulfilling special equipment needs, and increasingpersonal independence. MassMutual’s SpecialCareSM

program provides access to information, specialistsand financial solutions through our nationalnetwork of trained Special Care Planners.

What if you have employees to look out for?If you’re a business owner or employer, you knowthe determination and passion it takes to besuccessful. Building an enterprise and guiding itthrough the ups and downs of today’s businessclimate is a heroic undertaking. MassMutual canhelp along the way. Through our network offinancial professionals, we can help you build long-term succession plans and provide benefits for

employees. Plus, our Executive Benefits programincludes insurance solutions that can help attractand retain talented professionals, as well asaddress the more complicated financial needs ofyour executives.

What if your needs change?Most MassMutual insurance products are with youfor the long haul. Our goal is to build and maintaina product suite that is in touch with the manyneeds of our customers. Additionally, we train ourfinancial professionals to look after your needsthroughout your life, helping you navigate whateverchanges may come your way.

11

THERE

Where there’s a risk, there’s a

Retirement can seem so far away. And whenyou consider how much you’ll need to save, itcan appear even more distant. But that’s okay.Because you don’t get to retirement in onegiant leap. You keep taking deliberate, smartsteps in the right direction – steps that makeyou feel confident you have a good plan inplace. That’s when you’re truly there.

MotivatingAbove all else, MassMutual strives to help you actnow. Our products and people will help demystifyretirement planning through every stage of your life.So obstacles fade. Your next step becomes clear.And planning for retirement is no longer somethingyou just think about. It’s something you do.

EmpoweringGenerally, you take advantage of MassMutual’sretirement products, including 401(k) plans andpension plans, through your employer. So it’s ourjob to work closely with retirement plan advisorswho assist business owners and benefits managersat companies of all shapes and sizes. We equipthese professionals with quality products,dedicated support services and innovativeeducational materials so they can, in turn, helpemployees become actively involved in retirementplanning decisions.

12

THEREisn’t arriving at your retirement destination.

It’s being on the right path.

Half PageE

MEET Bill and Jennie:Bill Karns and Jennie Wine oversee Rodda Paint'sbenefits and 401(k) plan. Rodda employs more than350 people in 45 locations throughout Oregon,Washington, Alaska and Idaho.

Working collaboratively, MassMutual and the plan'sthird-party financial advisor deliver personalized, one-on-one enrollment assistance and investmenteducation to Rodda Paint employees.

Shown left to right: Bill Karns, Jennie Wine,MassMutual’s Mitch Haber.

“We knew that our employees' own

retirement savings would be vital to their

overall success in meeting their retirement

needs, but they just weren't saving enough.

Today, nearly 90 percent of Rodda Paint

employees are participating in our

plan – compared to 47 percent six years

ago. Better still, the average savings rate

has also increased.”

Bill Karns, Human Resources Director, Rodda Paint

LearningHow do we help turn thoughts into action? We’vemade it a top priority to better understand howpeople think, and act, when saving for retirement.Through research we’ve sponsored, we betterunderstand the challenges people face. Whatobstacles are in the way. What it will take to getyou to begin. And what will keep you engagedgoing forward. As a result, the products we offerand the tools we use to communicate with you arecustomized to your needs and aimed at making thewhole process easier.

For example, we launched a new paper-based Gapand Income Statement for retirement planparticipants that uses your individual personal dataand assumptions to estimate whether you will havea sufficient account balance, combined with aSocial Security benefit, to replace 90 percent ofyour current income at normal retirement age. Wealso developed plan participant uses for a first-of-its-kind hand-held enrollment device called thee4SM. It allows you to explore your options andenroll in your company’s retirement plan at the pushof a button.

Our online retirement planning program, TheJourneySM, puts account management tools andinvestment information right at your fingertips. It’sdesigned to give you just what you need to moveforward – whether you want to steer your plan allby yourself, get a detailed road map or let us domost of the driving.

13

THEREisn’t arriving at your retirement destination.

It’s being on the right path.

At the point of retirement, there’s a dramaticchange of gears financially. After years andyears of working for your money, you switchto years and years of your money working foryou. It’s a critical moment. And, atMassMutual, we’re right there with you.

Your RetirementWill you sit back and relax, surrounded by family, orembark on a more active and adventurous lifestyle?Will you move into your dream home or walk into asecond career? Will you do all of the above?Retirement is like starting a whole new financiallife, complete with new priorities, needs and goals.And just like when you first started saving for theretirement of your dreams, MassMutual can helpyou take the next steps in funding the retirement ofyour reality.

14

THERE

When you realize your retirementsavings will pay off, you’re

Half PageF

MEET Carey:Carey Ann Smith is a retired nurse educator too energetic to simply stop working. This natural nurturer now provides house-sitting, errand andnanny/babysitting services.

To prepare her for a new stage in life, Carey'sMassMutual financial professional did a thoroughfinancial review. Because she had a pension, Careyneeded less – not more – income from her IRA whenshe retired. MassMutual has tools that evaluate manyoptions to help determine the best fit for each client’sneeds. So instead of receiving unnecessary income,Carey adjusted her IRA withdrawal rate in order tobetter meet her current income needs.

And, if Carey decides to pursue a new direction, she can adjust her income plan accordingly.

“When I retired, I knew I needed help.

I met with my financial professional to

help figure out my future income needs.

I also told her that I needed a new car.

She helped me to figure out my income

plan and I was even able to buy the car

within my budget.”

Carey Ann Smith, retired

Your Income So many things have changed in your life since youfirst started saving. The result is, your incomeneeds may be different than you anticipated. And itcan be difficult to determine exactly how muchyou’ll need and for how long. MassMutual willwork closely with you and your financialprofessional as you approach and enter intoretirement. We offer a number of programs andservices that can help you generate a steady,reliable stream of income for your needs today andfor years to come, including help managing accountwithdrawals over the length of your retirement.This innovative suite of offerings gives youflexibility and choices, not just when you’re savingfor your retirement, but also when you get there.And if you haven’t quite reached your accumulationgoal, we can help with that, too.

Your Future Changing savings into income isn’t a one-time deal.We’ll stay with you throughout your retirement years,so as your needs change, your income plan can aswell. One of our investment advisor programs guidesyou throughout your retirement by recommending theright withdrawals to help keep pace with your needsover the years. And we can help you take care ofother important financial needs after retirement, likeensuring your loved one has income or leaving alegacy for your children.

15

THERE

When you realize your retirementsavings will pay off, you’re

When you choose to work with a specificfinancial professional and company, you’reputting quite a bit of trust in their ability toperform for you today and stay with you forthe long term. It’s a big decision. So when wesay, “We’ll help you get there,” why shouldyou believe it?

ExperienceNot many companies have been around for 156years. We’re proud of what that says about ourexperience and our stability. We’ve grown andthrived – surviving wars, depressions, recessionsand changing market conditions. And while we’veadapted and expanded our offerings along theway, our main focus has never wavered. We are acompany that helps people like you take the nextstep toward a more secure financial future. And our rich history is proof that this approach is effective.

16

Half PageG

THEREWe’ve been here helping people get

for 156 years.

MEET THE Dickersons:Andrew Jackson Dickerson, “Jack,” met Gwen whenthey were 12. They married at 18 and had four children.He became a board certified surgeon, and when theymoved to Waynesville, North Carolina, he was the firstsurgeon in the area.

Over the years, Dr. Dickerson gave back to his family,his community, and the world. He volunteered forHabitat for Humanity and Rotary International.

As a medical student in 1950, he bought his first wholelife insurance policies from Joe Mickey. Fifty-sevenyears later, Joe’s son, John, a third-generationMassMutual agent, handled the claims.

Shown left to right: Beverly, Gwen and Marty Dickerson.

“Daddy left a legacy in so many ways. He

was a surgeon in a small town who treated

everyone with dignity. I remember he once

performed an appendectomy in trade for a

pony for me. And I didn’t even know until

recently that he’d bought a life insurance

policy so he could leave a legacy to

Bowman Gray Medical School.”

Marty Dickerson, daughter of

Dr. Andrew J. Dickerson

StrengthWhy should you care about our financial strengthratings? Because they’re a key indicator of our abilityto deliver on our long-term promises to you, likepaying a life insurance benefit or an annuity payment.And they can give you reason to believe the moneyyou entrust with us is being handled expertly. We’reproud that our ratings1 are among the highest of anycompany in any industry.

A.M. Best Company: A++ (Superior)

Fitch Ratings: AAA (Exceptionally Strong)

Moody's Investors Service: Aa1 (Excellent)

Standard & Poor's: AAA (Extremely Strong)

MutualMutual is not just part of our name. It’s part of ourhistory, our future and our everyday commitment toyou. In simplest terms, if you have a participatinglife insurance policy issued by MassMutual, youshare in the ownership of the company. AtMassMutual, we ensure that your interests aretaken very seriously and that declared dividendsare paid to eligible policyholders and notshareholders. In short, it’s just one more wayMassMutual maintains its strength, stability andcontinuity for you.

17

THEREWe’ve been here helping people get

for 156 years.

1 Ratings are subject to change. This information is current as of February 22, 2008. Ratings apply to Massachusetts Mutual Life InsuranceCompany and its subsidiaries, C.M. Life Insurance Company and MML Bay State Life Insurance Company.

All of us at MassMutual share a strong beliefthat doing business the right way will help uscontinue to serve our customers far into thefuture. As an industry leader, we strive to seta good example for our peers by being anexceptional corporate citizen. We want you tohave both confidence and pride in thecompany you call your own.

Ethical StandardsSo many rely on us for their financial future, and wetake that responsibility very seriously. You musttrust us for the relationship to work. So we strictlyadhere to the laws and regulations that govern ourbusiness. We instill high ethical standards in ouremployees. And we strive to act with the utmostintegrity across all areas of our business.

Giving BackMassMutual supported a number of local andnational charities through monetary donations andcorporate sponsorships of nearly $6 million in 2007.We also give back in a number of other ways. Forinstance, we provide free life insurance for eligibleparents and guardians through the LifeBridgeSM FreeLife Insurance Program. Our education programsprovide scholarships to deserving students. And wemotivate and empower our financial professionalsacross the country to get involved in their localcommunities, too, so they can make a differencewhere you live.

18

Being GreenToday, being environmentally responsible is morethan just a good idea. It’s essential to ourcompany’s long-term growth and stability. We’rededicated to reducing our “environmental footprint”through activities such as recycling and utilizingenergy-efficient building materials and practices.We encourage conservation in the workplace,engaging employees to share and pursue their own“green” ideas.

We also strive to be an industry leader inintroducing technologies that can reduce paper use,such as online forms and “electronic” policies. Forexample, with help from The Conservation Fund’s GoZeroSM program, MassMutual is driving awarenessof its electronic prospectus delivery option availableto retirement plan sponsors and participants. Forevery plan sponsor who replaced paper deliverywith e-prospectus delivery in 2007, MassMutualmade a donation to The Conservation Fund to planta tree in a protected forest on their behalf.

A Great Place to WorkOur success and our ability to serve your needsdepend on having talented, dedicated andmotivated employees. Which is why we’veconstructed a workplace experience that hasearned us national recognition as a WorkingMother 100 Best Company (October 2007) and thatranks us among America’s Most AdmiredCompanies® in our industry category according toFortune magazine (April 30, 2007).

19

THEREHelping you get

is a great responsibility.

� 42% Education

� 19% Health and Human Services

� 17% Matching Gifts

� 14% Civic and Community

� 8% Arts and Culture

MassMutual’s 2007 Community Contribution

2007 Business HighlightsInsurance• Dividends to eligible participating policyholders

were $1.37 billion, a 12 percent increase and thelargest ever for the company since it was foundedin 1851.

• Introduced a flexible new entry in the whole lifeinsurance marketplace, further expanding ourportfolio and continuing to offer product optionsthat help our customers take action in addressingtheir financial needs and the needs of those whodepend on them.

• Further strengthened our leading position in theexecutive protection market by enhancing ourdisability income insurance products to provideadditional flexibility and increased coverage limits.

• Underwent a rigorous, independent assessmentof individually owned life insurance, annuitiesand long term care products by an impartial thirdparty in renewing our membership in theInsurance Marketplace Standards Association,the premier standards-setting organization for the life insurance marketplace.

• Approximately 1.8 million domestic individual lifeinsurance policies in force at year-end.

• More than $356 billion of individual life insurance coverage in force.

• More than $1.3 billion in death benefit claims paid.

• MassMutual continued as DALBAR’s top-rankedsite for financial professionals, while earning the“Excellent” designation for its consumer Web site– MassMutual.com.

• MassMutual’s continued support of its CareerAgency distribution system helped grow thenumber of financial professionals to more than4,400 in 2007, a 7 percent increase over theprevious year.

• The number of women in our network of financialprofessionals increased by 9 percent asMassMutual continues to empower women to achieve success with their personal andbusiness finances.

20

Retirement• MassMutual announced sponsorship of the PBS

documentary – “Retirement Revolution®” –which aims to raise awareness of retirementpreparation for Americans.

• MassMutual released a study revealing fixedincome annuities as a new asset class for creatingretirement income plans, and also introduced twonew annuities to the market in 2007.

• As of January 2008, MassMutual had leadingfinancial strength ratings when compared toother companies that issue variable annuitieswith a full suite of living benefits features.

• MassMutual offers a program that combinesinvestments, annuities and withdrawal guidancein one integrated package to deliver lifetimeretirement income in a single account – one ofthe few programs of this type in the industry.

• The company expanded its institutionalretirement sales and service team to supportboth strong growth and its network of strategicdistribution relationships.

• MassMutual earned a 2007 Annual Call CenterExcellence Award in the “Best in Class CallCenter” category (staff of less than 500). Theaward, sponsored by the International Quality &Productivity Center, recognizes superior thinking,creativity, and execution.

• Introduced a new bundled small plan producttargeting defined contribution retirement planswith $1 million-to-$5 million in assets. The newplan helps optimize participation and savingsbehavior with simplified administration for theplan sponsor.

• Introduced the SmartArchitectureSM InvestmentProgram, supported by a robust third-partycertification program, and a Fiduciary Warranty,all designed to offer plan sponsors and financialadvisors help in fulfilling their fiduciaryresponsibilities.

• Developed MassMutual RetireSmartSM, a suite ofautomatic features (automatic enrollment, assetallocation, and deferral increase) that helpsretirement plan participants get closer to theirretirement goals with enhanced simplicity.

21

Investment Management The MassMutual Financial Group of companiesincludes a number of respected investmentmanagement companies. If you have an insurancepolicy or retirement plan with us, your money isoften managed by these industry leaders. Or, theycan serve you and other investors independently.Their presence in the MassMutual FinancialGroup enhances our overall financial strength and stability.

OppenheimerFunds, Inc.One of the nation’s largest and most respectedinvestment management companies,OppenheimerFunds has been helping investorsrealize their financial goals for nearly a half century.OppenheimerFunds and its controlled affiliates offera broad range of products and services toindividuals, corporations and institutions.

• In October 2007, OppenheimerFunds Chairmanand CEO John V. Murphy was named Chairman ofthe Investment Company Institute (ICI), thenational association of U.S. investmentcompanies, including mutual funds, closed-endfunds, exchange-traded funds (ETFs), and unitinvestment trusts (UITs).

• Four portfolio managers were named to Barron’sannual Top 100 Portfolio Manager rankings inAugust 2007, marking the ninth consecutive yearfour or more managers have been named to thisprestigious list.2

22

2 OppenheimerFunds, Inc. has had at least four portfolio managers ranked in Barron's/Value Line annual survey "Top 100 Fund Managers"for each of the past nine years. Surveys were published 8/13/07, 8/14/06, 8/15/05, 8/16/04, 8/4/03, 7/29/02, 7/23/01, 7/17/00 and 7/19/99.Surveys are of qualifying portfolio managers; scores assigned based on performance and volatility of the Fund managed, versus peergroup. Barron's is a trademark of Dow Jones, L.P.

Investment Management Sales(in Millions)

$28,609$38,222

$62,967

$79,487

$104,950

’07’03 ’04 ’05 ’06

Babson Capital Management LLCBabson Capital is a full-service investment advisorthat creates investment strategies and solutions forinstitutions and other sophisticated investors.

• In a year where the industry saw significantvolatility, and specifically the challenges in thecredit markets, Babson Capital had another strongsales year, growing assets managed and servicedby 10 percent to $120.2 billion.

• Babson’s Mezzanine and Private Equity Groupcompleted its 100th realization since its inception15 years ago.

Baring Asset Management LimitedBaring is an international investment managementfirm with investment skills, clients and businesslocations spanning world markets.

• Baring’s exceptional year-over-year earningsgrowth measured over 100 percent.

• In 2007, Baring won more than 60 newinstitutional clients worldwide.

Cornerstone Real Estate Advisers LLCCornerstone, MassMutual’s real estate managementand advisory firm, manages real estate assets forinsurance companies, public and corporate pensionplans, Taft-Hartley plans, endowments and foundations.

• Launched a global real estate securities fund aspart of its initiative to expand into global realestate markets.

• Completed sales of assets from CornerstoneRotational Venture, which had invested in officeand apartment projects in selected U.S. marketsstarting in 2004, returning all capital to investors inaddition to returns that exceeded projections.

MassMutual International LLCMassMutual International (MMI) is the holdingcompany for MassMutual’s international insuranceand selected investment subsidiaries. MMI hasexpanded over the past decade through theacquisition of several well-established firms and nowoffers insurance and other financial products to morethan 1.9 million people in Japan, Taiwan, Hong Kong,Macau, Luxembourg and Chile.

• Total insurance sales of more than $2.4 billion.

• More than $22 billion in assets undermanagement, up 25 percent over 2006.

• Total premium over $4.6 billion, a 15 percentincrease over 2006.

23

Investment PhilosophyMassMutual’s seasoned investmentprofessionals apply a value-driven investmentapproach to identify investment opportunities.Their broad expertise allows us to consider awide range of asset types. Our goal is toprovide exceptional results for our policyholdersdespite the unpredictable market conditionsthat may prevail.

We believe that diversification – both across andwithin asset types – is extremely important andlimits exposure to any particular asset type oreconomic event at any point in time. We anticipatethat adherence to our disciplined investmentapproach and a long-term focus will continue toprovide for the best interests of our policyholders.

BondsMassMutual invests in public and private bonds,resulting in a portfolio that is well diversified acrossindustries and issuers to help reduce credit risk.Private bonds and loans diversify across differentissuers and provide considerable value to theportfolio as most offer some combination of higheryields, protective covenants and call-protectionfeatures. Almost 91 percent of the bond portfolio isinvestment grade based on ratings by the NationalAssociation of Insurance Commissioners (NAIC).

24

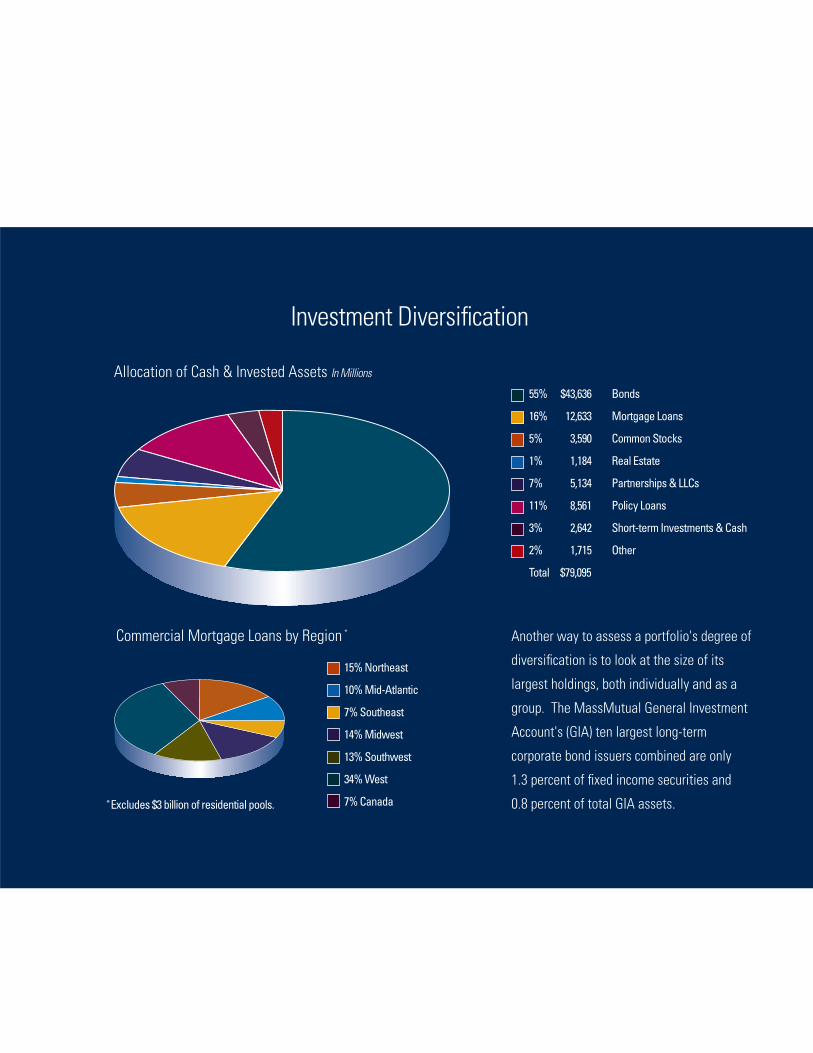

Half PageH

Investment Diversification

Another way to assess a portfolio's degree of

diversification is to look at the size of its

largest holdings, both individually and as a

group. The MassMutual General Investment

Account's (GIA) ten largest long-term

corporate bond issuers combined are only

1.3 percent of fixed income securities and

0.8 percent of total GIA assets.

Allocation of Cash & Invested Assets In Millions

55% $43,636 Bonds

16% 12,633 Mortgage Loans

5% 3,590 Common Stocks

1% 1,184 Real Estate

7% 5,134 Partnerships & LLCs

11% 8,561 Policy Loans

3% 2,642 Short-term Investments & Cash

2% 1,715 Other

Total $79,095

Commercial Mortgage Loans by Region *

15% Northeast

10% Mid-Atlantic

7% Southeast

14% Midwest

13% Southwest

34% West

7% Canada*Excludes $3 billion of residential pools.

Credit Quality* In Millions

Statement Value %

Aaa/Aa/A $29,244 67.0%

Baa 10,376 23.8%

Ba 1,783 4.1%

B 1,748 4.0%

Caa & lower 410 0.9%

In or near default 75 0.2%

Total $43,636 100.0%

* Public rating agency equivalents based on NAIC classifications.

Investment Quality

Allocation of Bonds In Millions

90.8% $39,620 Investment Grade

9.2% 4,016 Non-Investment Grade

Commercial Mortgage LoansOur direct lending expertise in commercialmortgages serves us well in identifyingopportunities. Commercial mortgage loans arediversified geographically and by property type, with most of the loans on buildings such as offices,apartments, shopping malls and hotels.MassMutual’s commercial mortgage loan portfolioperformed well during 2007 and at year-end therewere no loans in default.

Equities and Real EstatePublic and private equities are held directly andthrough partnerships, limited liability companies,and funds. Private equity in particular has providedsignificant benefits to the portfolio for many years,both directly through ownership and indirectlythrough attractive lending opportunities that arisefrom these business relationships.

Directly owned real estate is diversifiedgeographically to insulate the portfolio fromdownturns in local or regional economies.Commercial real estate historically has producedgood cash flow and enjoys certain tax advantages.In addition to directly owned real estate,MassMutual invests in real estate funds,partnerships, and real estate investment trusts.

Investment Risk ManagementInvestment risk management is a high priority. We monitor and analyze exposures to variousinvestment risks, employing a rigorous managementprocess for our assets to optimize policyholdervalue while ensuring our ability to meet ourobligations. In keeping with our obligation toprovide timely payment, MassMutual maintains astrong liquidity position. Liquidity is routinelyaddressed as part of the ongoing managementprocess and through periodic liquidity stress testing.

25

The management of Massachusetts Mutual LifeInsurance Company (MassMutual) is responsible forthe integrity and objectivity of the accompanyingconsolidated statutory financial statements ofMassMutual and its United States of America-domiciled life insurance subsidiaries (the Company),including estimates and judgments reflected inthem, and believes they fairly present theconsolidated financial condition of the Company inaccordance with statutory accounting principles.The Company engages independent publicaccountants to audit the fair presentation of itsfinancial statements and disclosures. Copies of theseparate company audited statutory financialstatements can be obtained by contactingMassachusetts Mutual Life Insurance Company,Corporate Communications, 1295 State Street,Springfield, MA 01111.

Management is responsible for the design andimplementation of the internal controls designed toprovide reasonable assurance that assets aresafeguarded, financial transactions are properlyrecorded and relevant matters are appropriatelydisclosed. These controls include appropriateseparation of duties, specified delegation ofauthority, and established policies and procedures

that are clearly communicated throughout theCompany.

Based on financial reporting risk assessments,management updates process documentation,identifies key controls and performs tests of theoperating effectiveness of the key controls. Inaddition, MassMutual’s professional staff ofinternal auditors monitors and evaluates theCompany’s control structure through periodicreviews and tests of the control aspects ofaccounting, financial, and operating activities.

An Audit Committee of the Board of Directors ofMassMutual, consisting of directors who are notofficers or employees of the Company, meetsperiodically with management, the independentpublic accountants, and the internal auditors toexercise its oversight responsibilities with respectto accounting controls, preparation of financialstatements, and the roles of the independent publicaccountants and the internal auditors.

The accompanying financial statements include theresults of MassMutual, C.M. Life InsuranceCompany, MML Bay State Life Insurance Company,CM Assurance Company, and CM Benefit InsuranceCompany.3

26

Management’s Responsibility for Financial Statements

3 The Company liquidated CM Assurance Company and CM Benefit Insurance Company in the fourth quarter of 2006. The results of thesesubsidiaries are included in the consolidated statutory financial statements through the date of liquidation.

Massachusetts Mutual Life Insurance Company and Subsidiaries CONSOLIDATED STATUTORY STATEMENTS OF FINANCIAL POSITION

December 31, 2007 2006

(In Millions)Assets:

Bonds $ 43,636 $ 43,976 Preferred stocks 167 270 Common stocks – subsidiaries and affiliates 2,786 2,684 Common stocks – unaffiliated 804 1,204 Mortgage loans 12,633 11,077 Policy loans 8,561 8,032 Real estate 1,184 1,275 Partnerships and limited liability companies 5,134 3,956 Derivatives and other invested assets 1,548 1,044 Cash, cash equivalents and short-term investments 2,642 1,015

Total invested assets 79,095 74,533

Investment income due and accrued 764 715 Other than invested assets 1,405 1,338

Total assets excluding separate accounts 81,264 76,586

Separate account assets 50,227 45,569

Total assets $ 131,491 $ 122,155

Liabilities:

Policyholders’ reserves $ 61,538 $ 59,887 Liabilities for deposit-type contracts 4,266 3,599 Contract claims and other benefits 259 248 Policyholders’ dividends 1,391 1,245 General expenses due or accrued 734 752 Federal income taxes 47 133 Asset valuation reserve 1,596 1,784 Securities sold under agreements to repurchase 2,102 1,183 Commercial paper 250 - Other liabilities 1,257 855

Total liabilities excluding separate accounts 73,440 69,686

Separate account liabilities 50,047 45,442

Total liabilities 123,487 115,128

Surplus 8,004 7,027

Total liabilities and surplus $ 131,491 $ 122,155

See notes to consolidated statutory financial statements.

27

Massachusetts Mutual Life Insurance Company and Subsidiaries CONSOLIDATED STATUTORY STATEMENTS OF INCOME

Years Ended December 31,

2007 2006(In Millions)

Revenue:

Premium income $ 13,236 $ 13,043 Net investment income 4,934 4,473 Fees and other income 574 504

Total revenue 18,744 18,020

Benefits and expenses:

Policyholders’ benefits 12,029 11,373 Change in policyholders’ reserves 2,715 3,049 General insurance expenses 1,141 1,178 Commissions 550 548 State taxes, licenses and fees 136 127

Total benefits and expenses 16,571 16,275

Net gain from operations before dividends and federal income taxes 2,173 1,745

Dividends to policyholders 1,373 1,226

Net gain from operations before federal income taxes 800 519

Federal income tax expense (benefit) 144 (42)

Net gain from operations 656 561

Net realized capital (losses) gains, after tax and transfers to interest maintenance reserve (455) 249

Net income $ 201 $ 810

See notes to consolidated statutory financial statements.

28

Massachusetts Mutual Life Insurance Company and Subsidiaries CONSOLIDATED STATUTORY STATEMENTS OF CHANGES IN SURPLUS

Years Ended December 31,

2007 2006(In Millions)

Surplus, beginning of year $ 7,027 $ 6,688

Increase (decrease) due to: Net income 201 810 Change in net unrealized capital gains (losses) 372 (10) Change in net unrealized foreign exchange capital gains 63 47 Change in asset valuation reserve 188 (266) Change in nonadmitted assets (89) (128) Change in net deferred income taxes 316 (57) Prior period adjustments (88) (57) Other 14 -

Net increase 977 339

Surplus, end of year $ 8,004 $ 7,027

See notes to consolidated statutory financial statements.

29

Massachusetts Mutual Life Insurance Company and Subsidiaries CONSOLIDATED STATUTORY STATEMENTS OF CASH FLOWS

Years Ended December 31,

2007 2006(In Millions)

Cash from operations: Premium and other income collected $ 13,819 $ 13,572 Net investment income 4,938 4,200 Benefit payments (11,878) (11,202) Net transfers to separate accounts (1,070) (1,219) Commissions and other expenses (1,839) (1,714) Dividends paid to policyholders (1,227) (1,153) Federal and foreign income taxes paid (272) (25)

Net cash from operations 2,471 2,459

Cash from investments:Proceeds from investments sold, matured, or repaid:

Bonds 15,882 15,652 Common stocks - unaffiliated 962 1,232 Mortgage loans 1,847 2,295 Real estate 382 157 Other 880 1,377

Total investment proceeds 19,953 20,713

Cost of investments acquired: Bonds (15,664) (18,194) Common stocks - unaffiliated (561) (1,205) Mortgage loans (3,311) (3,863) Real estate (189) (154) Other (2,342) (2,407)

Total investments acquired (22,067) (25,823)

Net increase in policy loans (529) (542) Net cash from investments (2,643) (5,652)

Cash from financing and other sources: Net deposits (withdrawals) on deposit-type contracts 488 (1,026) Commercial paper issued 249 - Net securities sold under agreements to repurchase 919 939 Other cash provided 151 133

Net cash from financing and other sources 1,807 46

Net change in cash, cash equivalents and short-term investments 1,635 (3,147) Cash, cash equivalents and short-term investments, beginning of year 1,015 4,162 Cash, cash equivalents and short-term investments nonadmitted (8) -Cash, cash equivalents and short-term investments, end of year $ 2,642 $ 1,015

See notes to consolidated statutory financial statements.

30

Notes to Consolidated Statutory Financial Statements

1. Nature of operations

MassMutual Financial Group (“MMFG”) is comprised of Massachusetts Mutual Life Insurance Company(“MassMutual”) and its subsidiaries. MMFG is a global, diversified financial services organization providinglife insurance, disability income insurance, long-term care insurance, annuities, retirement and savings products, investment management, mutual funds, and trust services to individual and institutional customers. MassMutual is organized as a mutual life insurance company.

2. Summary of significant accounting policies and practices

a. Basis of presentation

The consolidated statutory financial statements include the accounts of MassMutual and its wholly owned United States of America (“U.S.”) domiciled life insurance subsidiary (collectively, the “Company”): C.M. Life Insurance Company (“C.M. Life”), as well as its indirect subsidiary, MML Bay State Life InsuranceCompany, which is wholly owned by C.M. Life. Other entities comprising MMFG are accounted for under the equity method in accordance with statutory accounting principles. All intercompany transactions and balances for these consolidated entities have been eliminated. Statutory financial statements filed withregulatory authorities are not presented on a consolidated basis.

Two additional insurance subsidiaries, CM Assurance Company (“CM Assurance”) and CM Benefit Insurance Company (“CM Benefit”) had never issued any insurance policies or collected any premium. OnSeptember 29, 2006, CM Assurance and CM Benefit surrendered their Certificates of Authority and Compliance to the State of Connecticut Insurance Department. The Company liquidated these companies in the fourth quarter of 2006. The results of these subsidiaries are included in the consolidated statutory financial statements of the Company through the date of liquidation.

The consolidated statutory financial statements have been prepared in conformity with the statutoryaccounting practices of the National Association of Insurance Commissioners (“NAIC”) and the accounting practices prescribed or permitted by the Commonwealth of Massachusetts Division of Insurance (“Division”); and for the wholly owned U.S. domiciled life insurance subsidiaries, the State of Connecticut Insurance Department (“Department”).

Statutory accounting practices are different in some respects from financial statements prepared in accordance with U.S. generally accepted accounting principles (“GAAP”). The more significant differences between statutory accounting principles and GAAP are as follows: (a) certain acquisition costs,such as commissions and other variable costs, that are directly related to acquiring new business, are charged to current operations as incurred, whereas GAAP generally capitalizes these expenses and amortizes them based on profit emergence over the expected life of the policies or over the premium payment period; (b) statutory policy reserves are based upon the Commissioners’ Reserve ValuationMethod or net level premium method and prescribed statutory mortality, morbidity and interest assumptions, whereas GAAP reserves would generally be based upon the net level premium method or theestimated gross margin method, with estimates of future mortality, morbidity and interest assumptions; (c) bonds are generally carried at amortized cost, whereas GAAP generally reports bonds at fair value; (d)deferred income taxes, which provide for book versus tax temporary differences, are subject to limitation and are charged to surplus, whereas GAAP would generally include the change in deferred taxes in net income; (e) payments received for universal and variable life insurance products and variable annuities arereported as premium income and changes in reserves, whereas GAAP would treat these payments asdeposits to policyholders’ account balances; (f) majority-owned non-insurance subsidiaries and variable interest entities where the company is the primary beneficiary and certain controlled entities are accounted for using the equity method, whereas GAAP would consolidate these entities; (g) surplus notes are reportedin surplus, whereas GAAP would report these notes as liabilities; (h) assets are reported at “admitted asset” value and “nonadmitted assets” are excluded through a charge against surplus, whereas GAAP records these assets net of any valuation allowance; (i) reinsurance reserve credits are reported as a reduction of policyholders’ reserves and liabilities for deposit-type contracts, whereas GAAP would report these balances as an asset; (j) an asset valuation reserve (“AVR”) is reported as a contingency reserve to stabilizesurplus against fluctuations in the carrying value of stocks, real estate investments, partnerships, limitedliability companies (“LLCs”), and certain credit related derivative instruments as well as credit-related

31

Notes to Consolidated Statutory Financial Statements (continued)

declines in the value of bonds and mortgage loans, whereas GAAP does not record this reserve; (k) after-tax realized capital gains and losses which result from changes in the overall level of interest rates for alltypes of fixed-income investments and interest-related hedging activities are deferred into the interestmaintenance reserve (“IMR”) and amortized into revenue, whereas GAAP reports these gains and losses asrevenue; (l) changes in the fair value of derivative financial instruments are recorded as changes in surplus,whereas GAAP generally reports these changes as revenue unless deemed an effective hedge; (m)comprehensive income is not presented, whereas GAAP presents changes in unrealized capital gains and losses, minimum pension liability, and foreign currency translations as other comprehensive income; (n) embedded derivatives are recorded as part of the underlying contract, whereas GAAP would identify andbifurcate certain embedded derivatives from the underlying contract or security and account for themseparately; and (o) certain group annuity and universal life contracts which do not pass through allinvestment gains to contract holders are maintained in the separate accounts, whereas GAAP reports these contracts in the general account assets and liabilities of the Company.

The preparation of financial statements requires management to make estimates and assumptions that impact the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities as ofthe date of the consolidated statutory financial statements, and the reported amounts of revenues and expenses during the reporting periods. The most significant estimates include those used in determiningthe carrying values of investments, the liabilities for future policyholders’ reserves and deposit-typecontracts, and the amount of investment valuation reserves on mortgage loans, real estate held for sale, other-than-temporary impairments and the liability for taxes. Future events including, but not limited to, changes in the levels of mortality, morbidity, interest rates, persistency and asset valuations and defaults, could cause actual results to differ from the estimates used in the consolidated statutory financial statements. Although some variability is inherent in these estimates, management believes the amounts presented are appropriate.

b. Corrections of errors and reclassifications

In 2007, the Company recorded an adjustment that was attributable to the recognition of net investmentincome on partnerships and LLCs in a cumulative negative capital position for the years 2001 through2006. This adjustment reduced surplus by $100 million through prior period adjustments and increased surplus by $100 million through change in net unrealized capital gains, resulting in no net impact onsurplus.

In addition to the item noted above, changes to net surplus included a $5 million increase attributable to a correction of variable universal life reserves, a $5 million increase related to the reporting of tax settlements with the federal government, a $5 million increase attributable to the overstatement of the dividendaccumulation liability, a $4 million increase attributable to reinsurance rate errors, $1 million of various other adjustments, partially offset by a $5 million decrease attributable to annuity related reserves, and a $3 million decrease attributable to the establishment of a liability for postemployment benefits for employeeseverance plans.

As a result of this activity, the Company recorded, in the Consolidated Statutory Statements of Changes inSurplus, a net decrease of $88 million through prior period adjustments and an increase of $100 millionthrough the change in net unrealized capital gains.

During 2006, the Company recorded a net decrease to surplus of $114 million attributable to corrections ofprior year errors. The Company recorded $57 million through prior period adjustments, a component of changes in surplus, $41 million through the change in nonadmitted assets, and $16 million through the change in net unrealized capital gains. The $16 million decrease was attributable to a pricing error thatresulted in an overstatement in the carrying value of common stock and surplus as of December 31, 2005.

In 2006, prior period adjustments of $57 million included $18 million attributable to the establishment of a liability for post employment benefits for home office employee severance plans and $30 millionattributable to the correction in non-traditional life insurance reserves related to errors in a prior yearmortality study and mortality factors.

32

Notes to Consolidated Statutory Financial Statements (continued)

In 2006, the Company recorded tax corrections which decreased surplus by $48 million, of which $41million was recorded through surplus as a change in nonadmitted assets, and $7 million was recorded through prior period adjustments. In 2002 and 2003, the Company had incorrectly recorded its net deferredtax asset and federal income tax liability. The correction of these items to the net deferred tax asset in 2006 was nonadmitted. These errors relate to the reporting of tax settlements with the federal government and theadjustment to taxes following the submission of the Company’s 2001 federal income tax return.

Certain 2006 balances have been reclassified to conform to the current year presentation.

c. Bonds

Generally, bonds are valued at amortized cost using the constant yield interest method. Bond transactionsare recorded on a trade date basis, except for private placement bonds which are recorded on the fundingdate.

The fair value of bonds is based on values provided by the NAIC’s Securities Valuation Office (“SVO”) when available. If SVO values are not available, quoted market values provided by other third-partyorganizations are used. If quoted market values are unavailable, fair value is estimated by discounting expected future cash flows using current market rates applicable to yield, credit quality and maturity of the investment or using quoted market values for comparable investments.

For fixed income securities that do not have a fixed schedule of payments, such as asset-backed, mortgage-backed and structured securities, the effect on amortization or accretion is revalued quarterly based on the current estimated cash flows, using either the prospective or retrospective adjustment methodologies, consistently applied by type of security. Certain high quality fixed income securities follow the retrospective method of accounting. Under the retrospective method, the recalculated effective yieldequates the present value of the actual and anticipated cash flows, including new prepayment assumptions, to the original cost of the investment. Prepayment assumptions are based on borrower constraints andeconomic incentives such as the original term, age and coupon of the loan as affected by the interest rateenvironment. The current carrying value is then increased or decreased to the amount that would haveresulted had the revised yield been applied since inception, and investment income is correspondinglydecreased or increased. The Company has elected to use the book value as of January 1, 1994 as the costfor applying the retrospective adjustment method to securities purchased prior to that date. All other fixedsecurities, such as floating rate bonds and interest only securities follow the prospective method of accounting. Under the prospective method, the recalculated future effective yield equates the carrying value of the investment to the present value of the anticipated future cash flows.

Portfolios of asset-backed securities, including residential mortgage-backed securities, are evaluated on a periodic basis using scenarios customized by collateral type, performing sensitivity analysis on defaults as loan to values change, and on defaults as prepayments change using default curves under various scenarios. We combine scenario analysis with a monthly surveillance process in which we compare actual delinquencies and defaults to expectations established at the time securities are acquired and expectationsconsidering current market conditions, and perform a statistical review of troubled loan exposures to creditsupport on a transaction-by-transaction basis.

Management utilized a combination of external vendor prices, broker quotations and internal models for purposes of deriving fair value. Internal inputs used in the determination of fair value included estimates of prepayment speeds, default rates, discount rates, collateral values and cash flow priority, among others.Fair values resulting from internal models are those expected to be paid by a willing market participant.

The carrying values of bonds, mortgage-backed and asset-backed securities are written down to fair value when a decline in value is considered to be other-than-temporary. The Company considers the followingfactors in the evaluation of whether a non-interest related decline in value is other-than-temporary: (a) the financial condition and near-term prospects of the issuer; (b) the likelihood that the Company will be ableto collect all amounts due according to the contractual terms of a debt security in effect at the date ofacquisition; (c) the Company’s ability and intent to hold the investment for a period of time sufficient toallow for an anticipated recovery in value; and (d) the period and degree to which the market value has been below cost. The Company considers the following factors in the evaluation of whether an interest

33

Notes to Consolidated Statutory Financial Statements (continued)

related decline in value is other-than-temporary: (a) the Company’s near-term intent to sell; (b) theCompany’s contractual and regulatory obligations; and (c) the Company’s ability to hold the investmentuntil anticipated recovery of the cost of the investment. The Company conducts a quarterly managementreview of all bonds including those in default, not-in-good standing, or valued below 80% of cost. The Company also considers other qualitative and quantitative factors in determining the existence of other-than-temporary impairments including, but not limited to, unrealized loss trend analysis and significant short-term changes in value. If the impairment is other-than-temporary, a direct write-down is recognized in realized capital losses and a new cost basis is established.

d. Preferred stocks

Generally, preferred stocks in good standing are valued at amortized cost. Preferred stocks not in goodstanding are valued at the lower of amortized cost or fair value. Fair values of preferred stocks are basedon published market values, where available. For preferred stocks without readily ascertainable market values, the Company has determined an estimated fair value using broker-dealer quotations or internalmodels.

e. Common stocks - subsidiaries and affiliates

Common stocks of unconsolidated subsidiaries, including MassMutual Holding LLC (“MMHLLC”), areaccounted for using the equity method. The Company accounts for the value of its investment in its subsidiary, MMHLLC, at its underlying GAAP net equity, adjusted for certain nonadmitted assets.Operating results, less dividend distributions, for MMHLLC are reflected as net unrealized capital gains inthe Consolidated Statutory Statements of Changes in Surplus. Dividend distributions by MMHLLC arerecorded in net investment income. Dividend distributions to the Company are limited to MassMutual’sequity in MMHLLC. The cost basis of common stocks - subsidiaries and affiliates is adjusted for impairments deemed to be other-than-temporary and the impairment policy is consistent with commonstocks - unaffiliated.

f. Common stocks - unaffiliated

Common stocks, including warrants, are valued at fair value with unrealized capital gains and losses included as a change in surplus. Common stock transactions are recorded on a trade date basis.

The fair value of common stocks is based on values provided by the SVO when available. If SVO values are not available, quoted market values provided by other third-party organizations are used. If quotedmarket values are unavailable, fair value is estimated by using internal models.

The cost basis of common stocks is adjusted for impairments deemed to be other-than-temporary. The Company considers the following factors in the evaluation of whether a decline in value is other-than-temporary: (a) the financial condition and near-term prospects of the issuer; (b) the Company’s ability and intent to hold the investment for a period of time sufficient to allow for an anticipated recovery in value;and (c) the period and degree to which the value has been below cost. The Company conducts a quarterly management review of issuers whose common stock is not-in-good standing or valued below 80% of cost. The Company also considers other qualitative and quantitative factors in determining the existence of other-than-temporary impairments including, but not limited to, unrealized loss trend analysis andsignificant short-term changes. If the impairment is other-than-temporary, a direct write-down to fair value is recognized in realized capital losses and a new cost basis is established.

g. Mortgage loans

Mortgage loans are valued at the unpaid principal balance of the loan, net of unamortized premium and discount, non-refundable commitment fees and mortgage interest points, and valuation allowances. Themortgage loan portfolio is comprised of commercial mortgage loans, including mezzanine loans, and residential mortgage loan pools. Mezzanine loans are loans secured by a pledge of direct or indirect equity interest in an entity that owns real estate. Residential mortgage loan pools are pools of homogeneousresidential mortgage loans substantially backed by Federal Housing Administration and VeteransAdministration guarantees.

34

Notes to Consolidated Statutory Financial Statements (continued)

The fair value of mortgage loans is estimated by discounting expected future cash flows using currentinterest rates for similar loans with similar credit risk. For non-performing loans, the fair value is the estimated collateral value of the underlying real estate.

When, based upon current information and events, it is probable that the Company will be unable to collectall amounts of principal and interest due according to the contractual terms of the mortgage loan agreement,a valuation allowance is established for the excess of the carrying value of the mortgage loan over its fair value. Collectibility and estimated recoveries are assessed on a loan-by-loan basis considering all events and conditions relevant to the loan. This evaluation is inherently subjective as it requires estimates that aresusceptible to significant revisions as more information becomes available, as changes occur in the marketor as negotiations with the borrowing entity evolve. Changes to the valuation allowance are recorded as unrealized capital losses in surplus.

When an event occurs resulting in an impairment that is other-than-temporary, a direct write-down isrecognized in realized capital losses and a new cost basis is established. An impairment is deemed other-than-temporary when foreclosure proceedings or other procedures leading to the acquisition of thecollateral are initiated, the acquisition of the collateral is probable, and a reasonable estimate of the collateral value has been determined.

Interest income earned on impaired loans is accrued on the outstanding principal balance of the loan based on the loan’s contractual coupon rate. Interest is not accrued for impaired loans more than 60 days past due, for loans delinquent more than 90 days, or when collection is improbable. The Company continuallymonitors mortgage loans where the accrual of interest has been discontinued, and will resume the accrual of interest on a mortgage loan when the facts and circumstances of the borrower and property indicate that the payments will continue to be received per the terms of the original mortgage loan agreement or modified mortgage loan agreement.

h. Policy loans

Policy loans are carried at the outstanding loan balance less amounts unsecured by the cash surrender value of the policy. At issuance, policy loans are fully secured by the cash surrender value of the policy.Unsecured amounts can occur when subsequent charges are incurred on the underlying policy without the receipt of additional premium. Unsecured amounts were $1 million as of December 31, 2007 and 2006,which were non-admitted. Policy loans earn interest calculated based upon either a fixed or a variableinterest rate. Variable rate policy loans are adjusted at least annually and their fair value approximates the carrying value. For loans issued with a fixed interest rate, fair value is estimated by discounting expected future cash flows using current interest rates for similar loans with similar credit risk. Accrued investmentincome on policy loans more than 90 days past due is included in the unpaid balance of the policy loan.

i. Real estate

Investment real estate, which the Company has the intent to hold for the production of income, and real estate occupied by the Company are carried at depreciated cost, less encumbrances. Depreciated cost is adjusted for impairments whenever events or changes in circumstances indicate the carrying amount of theasset may not be recoverable, with the impairment being included in realized capital losses. Depreciation iscalculated using the straight-line method over the estimated useful life of the real estate holding, not toexceed 40 years. Depreciation expense is included in net investment income.

Real estate held for sale is carried at the lower of depreciated cost or fair value, less selling costs. Real estate classified as held for sale is not depreciated. Adjustments to the carrying value of real estate held for sale are recorded when fair value less selling costs is below depreciated cost and are included in realized capital losses.

Real estate acquired in satisfaction of debt is recorded at the lower of cost or fair value at the date of foreclosure.

35

Notes to Consolidated Statutory Financial Statements (continued)

Fair value is generally estimated using the present value of expected future cash flows discounted at a ratecommensurate with the underlying risks. The Company also obtains external appraisals for a rotatingsample of properties on an annual basis.

j. Partnerships and limited liability companies

Partnerships and LLCs, except for investments in partnerships which generate low income housing taxcredits (“LIHTC”), are accounted for using the equity method with the change in the equity value of the underlying investment recorded in surplus. When it appears probable that the Company will be unable torecover the outstanding carrying value of an investment, or there is evidence indicating an inability of the investee to sustain earnings to justify the carrying value of the investment, an other-than-temporaryimpairment is recognized in realized capital losses for the excess of the carrying value over the estimated fair value of the investment. The estimated fair value is determined by assessing the value of the partnership or LLC’s underlying assets, cash flow, current financial condition and other market factors.Distributions not deemed to be a return of capital are recorded in net investment income when received provided there are undistributed earnings in the partnerships or LLCs.

Investments in partnerships, which generate LIHTCs, are carried at amortized cost unless consideredimpaired. Under the amortized cost method, the excess of the carrying value of the investment over itsestimated residual value is amortized into income during the period in which tax benefits are allocated. For determining impairments in partnerships which generate LIHTC, the Company uses the present value of all future benefits, the majority of which are tax credits, discounted at the risk-free rate of 4.25% and comparesthe result to its current book value. Impairments are recognized as realized capital losses.

k. Derivatives and other invested assets

Derivatives and other invested assets consist of investments in derivative financial instruments and othermiscellaneous investments.