Weekly credit update - Danske...

34

Weekly Credit Update 21 March 2017 Important disclosures and certifications are contained from page 32 of this report Investment Research www.danskebank.com/CI This document is intended for institutional investors and is not subject to all the independence and disclosure standards applicable to debt research reports prepared for retail investors. Jonas Meyer Haseeb Syed Bendik Engebretsen Phone +47 85 40 70 79 Phone +47 85 40 54 19 Phone +47 85 40 69 14 Mobile +47 92 85 85 25 Mobile +47 97 98 78 82 Mobile +47 92 88 12 10 [email protected] [email protected] [email protected]

Transcript of Weekly credit update - Danske...

Weekly Credit Update

21 March 2017

Important disclosures and certifications are contained from page 32 of this report

Investment Researchwww.danskebank.com/CI

This document is intended for institutional investors and is not subject to all the independence and disclosure standards applicable to debt research reports prepared for retail investors.

Jonas Meyer Haseeb Syed Bendik Engebretsen

Phone +47 85 40 70 79 Phone +47 85 40 54 19 Phone +47 85 40 69 14

Mobile +47 92 85 85 25 Mobile +47 97 98 78 82 Mobile +47 92 88 12 10

22

- General credit market news and current themes

- Credit indicators

- Scandi investment grade

Contents

- Coverage universe, credit ratings and recommendations

- Scandi high yield/unrated

33

Source: Bloomberg, Danske Bank Markets (both charts)

What’s on our minds

- General credit market news

• Last week there were several international macroeconomic andpolitical events that were of high relevance to the credit markets. TheFed increased the federal funds rate by 25bp and the overallmessage from the FOMC meeting was that the Fed is on track andhas delivered one of the three hikes it projected back in December2016. Post the announcement, the USD depreciated somewhat andthe US 10-year government yield dipped 10bp to c.2.5%.

• The Dutch elections did not lead to further uncertainty and negativereactions in the European credit markets, as Geert Wilders’s PVVparty came in second after the currently ruling VVD party of PM MarkRutte. This election might have important repercussions for theupcoming French presidential election and Le Pen’s winning chances.Market sentiment improved clearly post the Dutch election and theFOMC meeting, reflected by a tightening in credit indices. ItraxxCrossover slid by 9bp to 275bp over the week, while Itraxx Maintightened 2bp to 70bp over the same period.

• Both Bank of England and Norges Bank announced in their monetarypolicy meetings that they are keeping their bank rates unchanged at0.25% and 0.50%, respectively. The news that the UK parliament hascleared PM May to move forward with Brexit did not, however, haveany material impact on credit indices.

• In the financials space, last week started with an overweight ofinvestors selling cares, though without any panic selling. Thefinancials primary market was, however, fuelled by new issuancesprinting at relatively tight levels. BNP Paribas issued for example a5.5-year senior bond with a coupon of 3M EURIBOR+85bp (c.MS+73bp).

4

Scandi HY/unrated

55

Chart 1. Relative value, indicative mid spreads Chart 2. Recent years’ LTV vs new target range

ASW spreads based on observed mid prices in market

Source: Bloomberg, Danske Bank Markets Source: Bloomberg, Danske Bank Markets

Medium credit risk – Buy Kungsleden 2019s in SEK

- Reducing leverage through rights issue (published 7 February)

Buy NOKIA 2019 USD, trading at wide margin to Nokia 2019 EUR

Published on 23 May 2016

Key arguments for the trade

• Last week, Kungsleden announced that its board had decided to conduct a rights issue of around SEK1.6bn in order to strengthen its balance sheet. Consequently, we see a positive credit trend for Kungsleden.

• Kungsleden also presented a revised financial policy, with a near-term target for LTV of 50-55% (previously 55% target for 2020).

• Kungsleden’s bonds have previously traded in line with sector peers such as Klövern and Sagax and the SEK ‘BB’ index. Considering the company’s ambition to strengthen its balance sheet, we think a repricing corresponding to around one credit notch is justified (i.e. around 30-40bp tightening potential on the 2019 bond).

• As of end-September 2016, Kungsleden’s gross LTV was 58%, down from 64% at YE 2015. The secured LTV stood at 54% at end-September. In conjunction with the rights issue announcement, the company stated that it will strive for an LTV in the interval of 50-55% ‘at this point in the cycle’ (pro forma rights issue: 52%).

• Following the company’s announcement, we upgraded our bond recommendation on Kungsleden from Marketweight to Overweight (see Kungsleden - Reducing leverage through rights issue, 7 February 2017).

0

50

100

150

200

250

300

350

400

450

500

2017/01 2018/01 2019/01 2020/01

AS

W (

bp

s)

Castellum Ab Corem Property D Carnegie Fabege AbFastpartner Ab Heimstaden Hemfosa Fastighe Klovern AbKungsleden Sagax Ab Victoria Park Wihlborgs Fastig

40%

45%

50%

55%

60%

65%

2012 2013 2014 2015 2016E 2017E

New LTV target range Gross LTV

66

Recent trade ideas (high yield and unrated)

See the end of this document for a list of our coverage including recommendations.

Source: Danske Bank Markets

Type Trade Currency Idea Date

Outright Buy Kungsleden 2019s in SEK SEK Considering Kungsleden's ambition to strengthen its balance sheet, we think a repricing corresponding to around one credit notch is justified.

07 Feb 2017

Outright Buy SAS SEK 2019 Conv

SEKThe SAS SEK 2019 Conv is attractively priced and backed by a significant cash position of SAS AB.

20 Jan 2017

Outright Buy TDC EUR 3015 Hybrid EUR The TDC 3015 Hybrids trade attractive relative to other 'BB' rated EUR hybrids. 04 Jan 2017

Outright Buy Castellum 2020's in SEK SEK Following the acquisition of Norrporten, Castellum has further strengthened its business risk profile.

08 Nov 2016

Outright Buy Golar LNG Partners bonds NOK, USD The LNG shipping market is set for several tenders for long-term contracts in 2017. We find the yield in Golar LNG Partners attractive at current levels and argue the company should catch up with the relative strong performance of peers.

02 Nov 2016

Outright Buy Fastpartner 2018s in SEK SEK FastPartner’s bonds are still trading at generous spread levels and, in our opinion, the bonds should have potential for further tightening.

31 Oct 2016

Outright Buy Outukumpu 2021 EUR Outukumpu 2021 trade attractive compared to fair value "B+" EUR industrials curve and we expect further deleveraging.

31 Oct 2016

Outright Buy Victoria Park 2020s in SEK SEK Building scale through organic growth and acquisitions. 15 Sep 2016

Switch Buy Kemira 2022s, fund by selling Kemira 2019s EUR The spread differential between the Kemira 2019s and 2022s has widened significantly since the end of 2015. A flattening of the Kemira curve indicates potential for at least 20bp tightening, in our view.

08 Sep 2016

77

Best and worst performers (Nordic coverage universe)- High yield/unrated

Source: Bloomberg, Danske Bank Markets (both charts)

1 week in local currencies 1 month in local currencies

4,000

1,646

1,399

1,351

1,027

522

327

232

63

59

-23

-30

-40

-44

-49

-55

-60

-71

-90

-111

-1000010002000300040005000

Seadrill Ltd NOK 2018

North Atlantic Drilling Ltd NOK 2018

Seadrill Ltd SEK 2019

Farstad Shipping ASA NOK 2018

North Atlantic Drilling Ltd USD 2019

Fred Olsen Energy ASA NOK 2019

Seadrill Ltd USD 2020

Outokumpu OYJ EUR 2019

Teekay Offshore Partners LP/Teekay…

BW Offshore Ltd NOK 2020

Color Group AS NOK 2019

Nynas AB SEK 2018

Ahlstrom OYJ EUR 2019

Golar LNG Partners LP NOK 2017

Corem Property Group AB SEK 2018

BW Offshore Ltd NOK 2021

Beerenberg Holdco II AS NOK 2018

BW Offshore Ltd NOK 2020

BW Offshore Ltd NOK 2022

Teekay Offshore Partners LP NOK 2019

Change in local currencies (bp)

1,242

532

261

104

51

47

39

36

24

17

-2

-2

-2

-6

-8

-9

-12

-43

-65

-816

-1000-500050010001500

North Atlantic Drilling Ltd NOK 2018

Seadrill Ltd NOK 2018

Farstad Shipping ASA NOK 2018

Fred Olsen Energy ASA NOK 2019

Ship Finance International Ltd NOK 2017

BW Offshore Ltd NOK 2020

Hoegh LNG Holdings Ltd NOK 2017

Teekay Offshore Partners LP/Teekay…

Color Group AS NOK 2017

Hoist Kredit AB EUR 2017

Stena AB EUR 2020

Stena AB EUR 2019

Norwegian Air Shuttle ASA EUR 2019

Beerenberg Holdco II AS NOK 2018

SAS AB SEK 2019

SSAB AB SEK 2017

Stolt-Nielsen Ltd NOK 2019

Seadrill Ltd SEK 2019

Seadrill Ltd USD 2020

North Atlantic Drilling Ltd USD 2019

Change in local currencies (bp)

88

Recent Nordic high yield/unrated issuance*

*Excluding increases in existing bond issues (taps)

Source: Bloomberg, Danske Bank Markets

Selected new issues (High yield/unrated)Date Issuer Coupon CCY Volume Maturity S&P / Mdy / Fitch ASW/DM

3/17/2017 Corem Property Grp Ab STIB3M +425bps SEK 500 m Mar/20 / / 425

3/16/2017 Paprec Holding Sa 5.25% EUR 225 m Apr/22 B+ / B1e / -

3/15/2017 Spie Sa 3.125% EUR 600 m Mar/24 BB / Ba3 / -

3/10/2017 Solocal Group EUR003M +0bps EUR 398 m Mar/22 / Caa1 *+ / RD -

3/14/2017 Mpt Oper Partnersp/Finl 3.325% EUR 500 m Mar/25 BBB- / Ba1 / 267

3/14/2017 Peugeot Sa 2% EUR 600 m Mar/24 / Ba2 / BB+ -

3/13/2017 Play Topco Sa 5.375% EUR 500 m Sep/22 B- / Caa1e / B-e -

3/13/2017 Play Topco Sa 5.375% EUR 500 m Sep/22 B- / Caa1e / B-e -

3/9/2017 Nemak Sab De Cv 3.25% EUR 500 m Mar/24 BB+ / Ba1 / BB+ -

3/9/2017 Matthorn Tel Hld 4.875% EUR 117 m May/23 B / Caa1 / -

3/9/2017 Alliance Data Systems Co 4.5% EUR 400 m Mar/22 / / -

3/7/2017 Unione Di Banche Italian 4.45% EUR 500 m Sep/27 BBB- / Ba3 / BB+ 424

3/7/2017 Liberbank Sa 6.875% EUR 300 m Mar/27 / B1 / BB- 670

3/6/2017 Nokia Oyj 1% EUR 500 m Mar/21 BB+ / Ba1 / BB+u -

3/6/2017 Nokia Oyj 2% EUR 750 m Mar/24 BB+ / Ba1 / BB+u -

3/3/2017 Dof Subsea Asa 9.5% USD 175 m Mar/22 / / -

2/27/2017 Mikro Fund 8% EUR 1 m / / 0

3/1/2017 Akademibokhandeln Hold STIB3M +600bps SEK 500 m Mar/21 / / 600

3/3/2017 Nyrstar Netherlands Hold 6.875% EUR 400 m Mar/24 B- / B3 / -

3/1/2017 Avis Budget Finance Plc 4.5% EUR 250 m May/25 BB- / B1 / WD -

99

Company news from the past week (high yield/unrated)

Source: Danske Bank Markets

Name News Implication

Heimstaden

Heimstaden (MW) agreed to acquire Ståhl Fastigheter with some 90,000 square metres ofproperties, of which 50% in Norrköping and 50% in Uppsala. The properties in Norrköpingare mainly residential, while the properties in Uppsala are commercial (offices plus onehotel). The agreed price, including some land, is SEK1.5bn. Heimstaden has been managingthe properties on behalf of Ståhl Fastigheter since 2015. The financing is 60% bank loansand the remainder in cash. The transaction is in line with Heimstaden's acquisitive strategy.We maintain our Marketweight recommendation on the company's SEK bonds that webelieve to be fairly priced relative to sector peers, contingent on Heimstaden maintaining a(net) LTV of below 65% over time (end Q4: 50%).

Credit neutral

SAS

In the seasonally weak Q1 SAS posted EBITDA of SEK-302m versus SEK77m in Q1 16. Thepre-tax loss amounted to SEK697m versus SEK309m in Q1 16. The higher loss is due tofierce price pressure, higher fuel cost y/y and unfavourable FX movements y/y mainly relatedto the stronger USD. The cash outflow was SEK1.1bn and the cash and cash equivalentsamount to SEK7.2bn end Q1 17. With SAS guiding for positive pre-tax profit for the full-year(unchanged) this should support the cash holding in the coming quarters. Adj. net debt toEBITDA was around 4x. Overall a result much in line with expectations, as SAS had alreadywarned of a higher loss y/y in Q1. We continue to see support for the 19cb - it should tradearound the b- curve, which still leaves around 50-70bp tightening potential.

Credit neutral

10

Scandi investment grade

1111

Chart 1. Relative value, indicative mid spreads Chart 2. Spread between 21s and 20s (incl. bid-offer spread)

Source: Bloomberg, Danske Bank Markets Source: Bloomberg, Danske Bank Markets

Switch to NDASS 2% 21s from NDASS 4% 20sThe 20 has outperformed – take the opportunity to extend in Nordea

Buy NOKIA 2019 USD, trading at wide margin to Nokia 2019 EUR

Published on 23 May 2016

Key arguments for the trade

• NDASS 20 has clearly outperformed NDASS 21.

• NDASS 21 is trading at a quite decent level in line with Nordic peers and, while we do not consider it ‘cheap’ on a relative value basis, we think now is a good opportunity to take profit on the 20s and pick up the 21s to maintain Nordea exposure.

• Nordea’s Q4 results beat expectations, driven by higher trading income and lower loan losses. Costs are increasing temporarily due to a number of group-level initiatives but should peak in 2017. The CET1 ratio increased to 18.4% and the management buffer is now a comfortable 100bp.

• On the back of a fairly strong report and more attractive EUR senior pricing, we upgraded our recommendation on Nordea from Underweight to Marketweight in conjunction with the Q4 results (see Post-results - Nordea Q4 16 - Stability despite headwinds, 26 January, for details).

SWEDA (Aa3/AA-) 1.5% '19

SWEDA (Aa3/AA-) 1% '22

SWEDA (Aa3/AA-) 0.625% '21

SWEDA (Aa3/AA-) 0.3% '22

SHBASS (Aa2/NR) 2.625% '22

SHBASS (Aa2/NR) 2.25% '20

SHBASS (Aa2/AA-) 4.375% '21

SHBASS (Aa2/AA-) 2.25% '18

SHBASS (Aa2/AA-) 1.125% '22

SHBASS (Aa2/AA-) 0.25% '22

SEB (Aa3/A+) 2% '21

SEB (Aa3/A+) 2% '19

SEB (Aa3/A+) 1.875% '19

SEB (Aa3/A+) 0.75% '21

OPBANK (Aa3/AA-) 1.75% '18OPBANK (Aa3/AA-) 1.125% '19

OPBANK (Aa3/AA-) 0.875% '21

OPBANK (Aa3/AA-) 0.75% '22

NDASS (Aa3/AA-) 4% '20NDASS (Aa3/AA-) 4% '19

NDASS (Aa3/AA-) 3.25% '22

NDASS (Aa3/AA-) 2% '21

NDASS (Aa3/AA-) 1.375% '18

NDASS (Aa3/AA-) 1.125% '25

NDASS (Aa3/AA-) 1% '23

JYBC (NR/A-) FRN '18

JYBC (NR/A-) 0.625% '21

DNBNO (Aa2/NR) 3.875% '20

DNBNO (Aa2/A+) 4.375% '21DNBNO (Aa2/A+) 4.25% '22

DNBNO (Aa2/A+) 1.125% '23DANBNK (A2/A) 0.75% '23

DANBNK (A2/A) 0.75% '20

DANBNK (A2/A) 0.5% '21

Financials senior AA-

Financials senior AA-

Nordic Financials senior AA-

-20

-10

0

10

20

30

1 2 3 4 5 6 7 8 9 10

Bid Spread (EUR)*

YTW**

* Z-spreads. Discount margin for floaters. Swapped to indicated currency. ** Years-to-worstNote: Fair value curve(s) based on Danske Bank Markets' (mid) peer group of European issuers

-6

-4

-2

0

2

4

6

8

10

Oct-2016 Dec-2016 Feb-2017

Spread between NDASS EUR 2% 2021 and NDASS EUR 4% 2020

1212

Recent trade ideas (investment grade)

Source: Danske Bank Markets

See the end of this document for a list of our coverage including recommendations

Type Trade Currency Idea Date

Switch Switch to NDASS 2% 21s from NDASS 4% 20s

EUR NDASS 20s have clearly outperformed NDASS 21s. Now is a good opportunity to take profit on the 20s and pick up the 21s to maintain Nordea exposure.

10 Mar 2017

Outright Buy SCA Hygiene EUR SCHHYG 2025s trade on the 'BBB-' fair value curve. 23 Feb 2017

Outright Buy Vestas EUR2022s EUR Vestas bonds are trading just tighter than the ‘BB+’ fair value curve, 09 Feb 2017

which leaves them with a substantial performance potential compared to the 'BBB' fair value curve.

Switch Switch to SHBASS 1.125% 2022s from SHBASS 4.375% 2021s EUR The SHBASS 1.125% 2022s have underperformed the SHBASS 4.375% 2021s since the bank reported Q3 16 results. While the impact of Brexit and Basel 4 remain risks, they do not justify the kink in the SHBASS curve, in our view.

04 Jan 2017

Outright Buy Sandvik EUR2022 and EUR2026 EUR Trump could be the trigger for mining bonds. Combined with very attractive valuation of the Sandvik EUR 2022 and EUR 2026 bonds we have become positive on the name.

11 Nov 2016

Outright Buy Metso EUR 2022 EUR Trump could be the trigger for mining bonds. Combined with very attractive valuation of the Metso EUR 2022 bond we recommend to buy the bond.

11 Nov 2016

Outright Buy TVO EUR, SEK

TVO’s EUR curve trades attractive compared to the fair value ‘BB+’ industrials curve and its SEK curve offers a pick up compared to the EUR curve.

25 Oct 2016

Outright Buy Caruna 1.5% 2023 outright EUR Being ‘BBB+’ rated, Caruna trades between the ‘BBB-’ and the ‘BBB’ curve

03 Oct 2016

Outright Buy Carlsberg EUR 2024 (revisited) EUR We recommended to buy the Carlsberg EUR2024. The fundamental case has improved further following the H1 16 report from Carlsberg.

1313

Best and worst performers (Nordic coverage universe)- Investment grade

Source: Bloomberg, Danske Bank Markets (both charts)

1 week in local currencies 1 month in local currencies

10

10

9

8

8

8

8

8

7

7

0

-1

-1

-1

-2

-2

-3

-3

-4

-10

-15-10-5051015

SKF AB EUR 2018

Investor AB EUR 2021

Telia Co AB EUR 2025

Telia Co AB EUR 2021

Telia Co AB EUR 2021

Swedbank AB SEK 2018

BRFkredit A/S EUR 2018

Telia Co AB EUR 2025

Telia Co AB EUR 2031

Vattenfall AB EUR 2018

Nordea Bank AB EUR 2023

Danske Bank A/S SEK 2019

SpareBank 1 SR-Bank ASA NOK 2023

SKF AB EUR 2022

SBAB Bank AB SEK 2019

SpareBank 1 SMN NOK 2021

Swedish Match AB EUR 2024

SCA Hygiene AB EUR 2025

Teollisuuden Voima Oyj EUR 2025

Skandinaviska Enskilda Banken AB EUR…

Change in local currencies (bp)

9

8

8

7

7

7

5

5

4

4

-9

-9

-9

-10

-10

-13

-19

-29

-31

-32

-40-30-20-1001020

Telia Co AB EUR 2025

Telia Co AB EUR 2025

SpareBank 1 SMN EUR 2021

Fortum Varme Holding samagt med…

Telia Co AB EUR 2027

Telia Co AB EUR 2031

Svenska Handelsbanken AB EUR 2022

Swedbank AB EUR 2022

Svenska Handelsbanken AB EUR 2022

Swedish Match AB SEK 2020

Danske Bank A/S SEK 2019

Danske Bank A/S SEK 2019

Statoil ASA EUR 2021

TDC A/S EUR 2022

Vattenfall AB EUR 2021

Skandinaviska Enskilda Banken AB EUR…

Teollisuuden Voima Oyj EUR 2019

Teollisuuden Voima Oyj 2021

Teollisuuden Voima Oyj EUR 2025

Telia Co AB EUR 2027

Change in local currencies (bp)

1414

Selected new investment-grade issues**

Source: Bloomberg, Danske Bank Markets

*Estimated

**Excluding increases in existing bond issues (taps)

Selected new issues (Investment Grade)

Date Issuer Coupon CCY Volume Maturity S&P / Mdy / Fitch ASW/DM

3/15/2017 Santander Consumer Bank STIB3M +73bps SEK 400 m Mar/20 / A3 / A- 73

3/15/2017 Entra Asa NIBOR3M +86bps NOK 750 m Mar/24 / / 86

3/17/2017 Lansforsakringar Bank 0.1% SEK 500 m Mar/19 A / A1 / -

3/17/2017 Spareskillingsbk Krist NIBOR3M +61bps NOK 200 m Sep/20 / / 61

3/14/2017 Vegfinans Oestfold Bompe 1.22% NOK 500 m Jun/17 / / -

3/14/2017 Gjensidige Bank Boligkre NIBOR3M +57bps NOK 2 000 m May/23 A / / 57

3/14/2017 Bergen-Os Bompgselskap A 2.73% NOK 278 m Mar/27 / / -

3/13/2017 Atrium Ljungberg Ab 1.619% SEK 200 m Mar/22 / Baa2e / -

3/13/2017 Atrium Ljungberg Ab STIB3M +115bps SEK 1 100 m Mar/22 / Baa2e / 115

3/13/2017 Voss Veksel-Landmandsbk 1.25% NOK 100 m Aug/17 / / -

3/17/2017 Cargotec Oyj 2.375% EUR 100 m Mar/24 / / -

3/17/2017 Cargotec Oyj 1.75% EUR 150 m Mar/22 / / -

3/17/2017 Norddeutsche Landesbank 0.75% EUR 100 m Mar/21 / Baa1e / A-e -

3/17/2017 Alandsbanken Ab EUR003M +63bps EUR 100 m Mar/20 BBB / / 63

3/17/2017 Abn Amro Bank Nv 1.375% EUR 750 m Jan/37 A / Aaae / AAAe -

3/17/2017 Lb Baden-Wuerttemberg 0.375% EUR 100 m Mar/21 / Aa3 / A- -

3/6/2017 Sparkasse Holstein EUR003M +10bps EUR 120 m May/21 / / A+ 10

3/15/2017 Barclays Bank Plc 0% EUR 200 m Mar/18 A- / A1 / A -

3/16/2017 Landbk Hessen-Thueringen 0.25% EUR 250 m Mar/21 A / Aa3 / A+ -

3/14/2016 Dz Bank Ag 0.31% EUR 150 m Mar/21 A+ / Aa3 / AA- -

3/16/2017 Bnp Paribas Fortis Sa 0.5% EUR 500 m Sep/24 A / Aaae / A+ -

3/15/2017 Deutsche Genossen-Hypobk EUR003M +50bps EUR 100 m Feb/18 AA- / / AA- 50

3/15/2017 Deutsche Genossen-Hypobk EUR003M +50bps EUR 100 m Jan/18 AA- / / AA- 50

1515

Selected new investment-grade issues**

Source: Bloomberg, Danske Bank Markets

*Estimated

**Excluding increases in existing bond issues (taps)

Selected new issues (Investment Grade)

Date Issuer Coupon CCY Volume Maturity S&P / Mdy / Fitch ASW/DM

3/15/2017 Deutsche Genossen-Hypobk EUR003M +50bps EUR 100 m Jan/18 AA- / / AA- 50

3/15/2017 Deutsche Genossen-Hypobk EUR003M +50bps EUR 100 m Feb/18 AA- / / AA- 50

3/15/2017 Deutsche Genossen-Hypobk EUR003M +50bps EUR 100 m Jan/18 AA- / / AA- 50

3/16/2017 Wl Bank 1.375% EUR 250 m Mar/37 AAA / / AA- 5

3/15/2017 Sca Hygiene Ab 0% EUR 300 m Nov/18 (P)BBB+ / Baa1e / 13

3/15/2017 Sca Hygiene Ab 0.625% EUR 600 m Mar/22 (P)BBB+ / Baa1e / 45

3/15/2017 Sca Hygiene Ab 1.125% EUR 600 m Mar/24 (P)BBB+ / Baa1e / 65

3/15/2017 Sca Hygiene Ab 1.625% EUR 500 m Mar/27 (P)BBB+ / Baa1e / 83

3/15/2017 Sca Hygiene Ab 1.625% EUR 500 m Mar/27 (P)BBB+ / Baa1e / 83

3/15/2017 Engie Sa 1.5% EUR 800 m Mar/28 A- / A2e / -

3/15/2017 Engie Sa 0.875% EUR 700 m Mar/24 A- / A2e / -

3/15/2017 Bnp Paribas EUR003M +85bps EUR 1 000 m Sep/22 A / Baa2e / A+e 85

3/15/2017 Proximus Sadp 0.5% EUR 500 m Mar/22 A / A1e / -

3/15/2017 Dnb Boligkreditt As 0.25% EUR 250 m Jun/22 AAA / Aaae / WD -

3/15/2017 Landbk Hessen-Thueringen 1.328% EUR 250 m Mar/27 A / Aa3 / A+ -

3/15/2017 Muenchener Hypothekenbnk EUR006M +30bps EUR 250 m Mar/23 / Aa3 / AA- 30

3/15/2017 Muenchener Hypothekenbnk EUR006M +25bps EUR 250 m Mar/22 / Aa3 / AA- 25

3/14/2017 Credit Agricole Cariparm 1.125% EUR 750 m Mar/25 / Aa2e / -

3/14/2017 Credit Agricole Cariparm 1.625% EUR 750 m Mar/29 / Aa2e / -

3/14/2017 Wolters Kluwer Nv 1.5% EUR 500 m Mar/27 BBB+ / Baa1 / WD -

3/14/2017 Landbk Hessen-Thueringen 1.69% EUR 250 m Mar/31 A / Aa3 / A+ -

1616

Company news from the past week (Investment grade)

Source: Danske Bank Markets

Name News Implication

ESB

ESB delivered a strong H2 16. Revenues declined 3% y/y while group clean EBITDA rose11% y/y, driven mainly by stronger tariffs and by the commissioning of new gas capacity inthe UK being offset partly by weaker GBP/EUR and lower power prices. ESB’s net debt wasunchanged h/h. Lower pension provisions helped drive adjusted net debt-to-EBITDA strongerat 3.6x, down 6% h/h. Overall, it was a credit positive result, which should not have an impacton the rating. We see most value in the ESBIRE 24s and call 28s.

Credit positive

Metso

Metso (OW): S&P affirms the BBB/Stable rating. Metrics are solid for the BBB rating but theweakness in the mining industry has left investors fearing a potential rating downgrade.However, with the increase in order intake in H2 16 (although Metso had a weak Q4 16order intake y/y due to tough comps) and the solid metrics for the rating we expect asignificant tightening of the EUR22bond over the coming months. Yes, it is illiquid but currentvaluation wider than the BBB- curve is way off. We remain Overweight Metso.

Credit neutral

G4S

G4S (MW) reported a credit positive 2016 result with EBITDA of GBP592m vs GBP526min 2015. Operating cash flow increased to GBP638m from GBP395 in 2015. Net debt waslowered to GBP1670m from GBP 1782m in 2015 and net debt to EBITDA declined to 2.8xend-2016 vs 3.4x end-2015 and 3.2x H1 16. G4S still expects to reach the target of netdebt to EBITDA below 2.5x end-2015. The lower leverage moves S&P further away fromdowngrading G4S from the current BBB-/Neg Outlook in our view. With continueddeleveraging in 17 this should support the EUR23 bond that is trading significantly widerthan the BBB curve.

Credit neutral

Danfoss

Despite making bolt-on acquisitions worth DKK1.9bn during 2016 Danfoss kept creditmetrics flattish y/y due to strong operating cash flow and relatively low dividends. Withannual operating cash flow of around DKK5bn Danfoss is well positioned to do more M&Aand we believe these ambitions are likely to postpone any rating upgrade in the short tomedium term, although metrics are solid for the current BBB rating. With the EUR22 bondalready trading close to the BBB+ curve we see the bond as fully valued and maintain ourMarketweight.

Credit neutral

1717

Company news from the past week (Investment grade)

Source: Danske Bank Markets

Name News Implication

Scania

Q4 numbers out this morning. Solid truck order bookings in the quarter driven by largely allregions. Order bookings in Europe remained strong and increased in unit terms 19% y/y inthe quarter. Truck demand from Eurasia rose y/y in the quarter driven by the Russian market,which appears to have bottomed out according to Scania. Service revenues grew 6% y/y inlocal currencies, leaving the service share of group revs at 21% during the full-year 2016.While the favourable development in Europe, high service volumes and FX had positive effectson earnings, this was partly offset by investments related to Scania’s new truck generationand lower deliveries in Brazil. The operating margin was 9.2% in the quarter (Q4 15: 10.3%)and for the FY it was 9.8% (adj. for non-recurring items), compared to 10.2% in FY 15.

Credit neutral

Elisa

Buys part of small Finnish Estonian network company Santa Monica. No acquisition pricedisclosed but co had revenues of EUR44m and an EBIT of EUR3m, i.e. the acquisition price islikely between EUR25-EUR50m (more likely the low end of the range). Elisa does not changethe guidance on the back of this acquisition. Credit neutral overall. Credit neutral

18Credit Indicators

Credit indicators

1919

Chart pack: Euro spreads and returns

Source: Macrobond Financial, Danske Bank Markets [all charts]

Euro IG ASW, iBoxx indices

Euro HY ASW, Merrill Lynch indices

IG total return, iBoxx indices, 2016-01=100

HY total return, Merrill Lynch indices, 2016-01=100

2020

Chart pack: relative value

Source: Macrobond Financial, Danske Bank Markets [all charts]

iTraxx vs iBoxx

Euro vs US CDS indices - IG (Markit) Euro vs US HY bond indices (Merrill Lynch)

2121

Chart pack: general market development

Source: Macrobond Financial, Danske Bank Markets [all charts]

European swap and government yields

Euro swap curve spread

3M Libor, US, Euro area, Sweden and Norway

EUR/USD basis swaps

2222

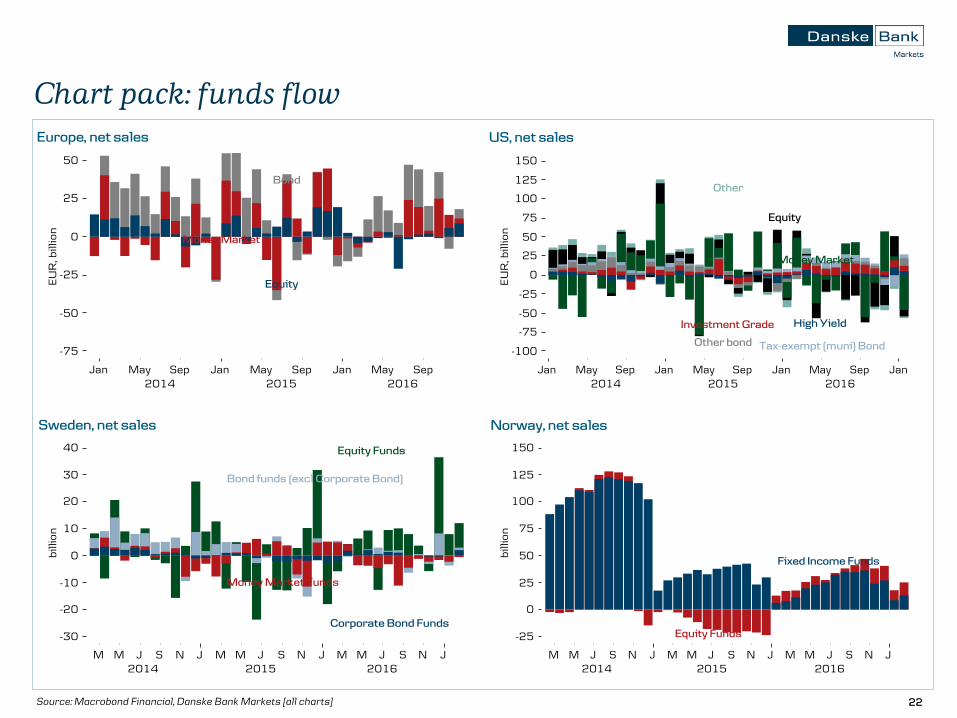

Chart pack: funds flow

Source: Macrobond Financial, Danske Bank Markets [all charts]

Europe, net sales

Sweden, net sales

US, net sales

Norway, net sales

2323

Chart pack: macro

Source: Macrobond Financial, Danske Bank Markets [all charts]

GDP y/y growth, calendar adjusted

Euro area y/y change in bank lending

Purchasing Manager Indices

Euro area lending standards

2424

Chart pack: cash versus CDS

Source: Macrobond Financial, Danske Bank Markets [all charts]

Sub financials cash vs CDS Senior financials cash vs CDS

iTraxx Main vs Iboxx Non-financials A iTraxx Main vs Iboxx Non-financials BBB

25

Coverage universe, credit ratings

and recommendations

2626

Our coverage 1 of 5

Source: Standard & Poor's, Moody's, Fitch, Danske Bank Markets

Ratings from S&P/Moody's/Fitch

Sector Analyst(s)

Company Rating Outlook Rating Outlook Rating OutlookAhlstrom Oyj MATERIALS M. Rosendal / J. Magnussen MARKETWEIGHTAkelius Residential Property Ab BBB- Pos REAL ESTATE L. Landeman / G. Bergin MARKETWEIGHTAktia Bank Plc A- Stable A3 Pos BANKS K. Jensen / G. BerginAlandsbanken Abp BBB Stable BANKS K. Jensen / G. BerginAmbu A/S HEALTHCARE J. Magnussen / M. Rosendal OVERWEIGHTAp Moller - Maersk A/S BBB Neg Baa2 Neg SHIPPING B. Børsting/J. Magnussen MARKETWEIGHTArla Foods Amba CONSUMER GOODS M. Rosendal / G. BerginAtlas Copco Ab A Stable A2 Stable A Stable MACHINERY & HEAVY INDUSTRIALS B. Børsting / M. Rosendal UNDERWEIGHTAvinor As AA- Neg A1 Stable TRANSPORTATION H. Syed/ B. Børsting MARKETWEIGHTBalder BBB Stable Baa3 Stable REAL ESTATE L. Landeman / G. Bergin MARKETWEIGHTBeerenberg Holdco Ii As ENERGY J. Meyer / B. EngebretsenBillerudkorsnas Ab MATERIALS M. Rosendal / L. Landeman MARKETWEIGHTBonum Pankki Oyj BBB Stable BANKS K. Jensen / G. BerginCarlsberg Breweries A/S Baa2 Stable BBB Stable CONSUMER GOODS B. Børsting / M. Rosendal MARKETWEIGHTCaruna Networks Oy BBB+ Stable UTILITIES J.Magnussen / L.Landeman OVERWEIGHTCastellum Ab REAL ESTATE L. Landeman / G. Bergin OVERWEIGHTCitycon Oyj BBB Stable Baa1 Stable REAL ESTATE L. Landeman / G. Bergin MARKETWEIGHTColor Group As TRANSPORTATION B. Børsting / M. Rosendal MARKETWEIGHTCom Hem Holding Ab BB Stable TMT M. Rosendal / J. Magnussen OVERWEIGHTCorem Property Group Ab REAL ESTATE L. Landeman / G. Bergin UNDERWEIGHTDanfoss A/S BBB Stable MACHINERY & HEAVY INDUSTRIALS B. Børsting / J. Magnussen MARKETWEIGHTDestia Group Oy CONSTRUCTION A. Moberg / L. Landeman OVERWEIGHTDfds A/S SHIPPING B. Børsting / M. Rosendal OVERWEIGHTDlg Finance As CONSUMER GOODS M. Rosendal / B. Børsting#N/A Invalid Security TMT M. Rosendal / J. Magnussen OVERWEIGHTDnb Bank Asa A+ Neg Aa2 Neg BANKS K. Jensen / G. Bergin UNDERWEIGHTDong Energy A/S BBB+ Stable Baa1 Neg BBB+ Stable UTILITIES J. Magnussen / L. Landeman MARKETWEIGHTDsv A/S TRANSPORTATION B. Børsting / M. Rosendal OVERWEIGHTEg Holding SERVICES & IT J. Magnussen / B. BørstingEika Boligkreditt As BANKS K. Jensen / G. BerginEika Forsikring As INSURANCE K. Jensen / G. BerginEika Gruppen As FINANCIALS K. Jensen / G. Bergin

Recomm.S&P Moody's Fitch

2727

Our coverage 2 of 5

Source: Standard & Poor's, Moody's, Fitch, Danske Bank Markets

Ratings from S&P/Moody's/Fitch

Sector Analyst(s)

Company Rating Outlook Rating Outlook Rating OutlookEllevio Ab UTILITIES J.Magnussen / L.LandemanElectrolux Ab A- Stable Wr WD CONSUMER GOODS A. Moberg / G. Bergin MARKETWEIGHTElenia Oy BBB UTILITIES J. Magnussen / L. Landeman MARKETWEIGHTElisa Oyj BBB+ Stable Baa2 Stable TMT M. Rosendal / J. Magnussen MARKETWEIGHTEntra Asa REAL ESTATE H. Syed/ B. Engebretsen MARKETWEIGHTFastpartner Ab REAL ESTATE L. Landeman / G. Bergin OVERWEIGHTFelleskjopet Agri Sa CONSUMER GOODS B. Børsting / M. RosendalFingrid Oyj AA- Stable A1 Pos AA- Stable UTILITIES J. Magnussen / L. Landeman OVERWEIGHTFinnair Oyj TRANSPORTATION B. Børsting / M. Rosendal MARKETWEIGHTFortum Oyj BBB+ Stable Baa1 Stable BBB+ Stable UTILITIES J. Magnussen / L. Landeman UNDERWEIGHTFortum Varme Holding Samagt Med Stockholms Stad AbBBB+ Stable UTILITIES J. Magnussen / L. Landeman MARKETWEIGHTG4S Plc BBB- Neg SERVICES & IT B. Børsting / M. Rosendal MARKETWEIGHTGaslog Ltd SHIPPING J. Meyer / B. Engebretsen MARKETWEIGHTGetinge Ab HEALTHCARE A. Moberg / L. Landeman UNDERWEIGHTGolar Lng Partners Lp SHIPPING J. Meyer / B. Engebretsen OVERWEIGHTHeimstaden Ab REAL ESTATE L. Landeman / G. Bergin MARKETWEIGHTHemso Fastighets Ab A- Stable REAL ESTATE L. Landeman / G. BerginHexagon Ab MACHINERY & HEAVY INDUSTRIALS A. Moberg / L. Landeman MARKETWEIGHTHkscan Oyj CONSUMER GOODS M. Rosendal / B. Børsting MARKETWEIGHTHoegh Lng Holdings Ltd SHIPPING J. Meyer / B. Engebretsen MARKETWEIGHTHoist Kredit Ab Ba1 Stable BANKS G. Bergin / L. Landeman MARKETWEIGHTHusqvarna Ab BBB Stable CONSUMER GOODS A. Moberg / L. Landeman MARKETWEIGHTIca Gruppen Ab CONSUMER GOODS A. Moberg / G. Bergin MARKETWEIGHTIf P&C Insurance Holding Ltd A- Stable INSURANCE K. Jensen / G. BerginIkano Bank Ab BANKS K. Jensen / G. BerginInvestor Ab AA- Stable Aa3 Stable CORPORATES G. Bergin / B. Børsting OVERWEIGHTIss A/S BBB Stable SERVICES & IT B. Børsting / M. Rosendal MARKETWEIGHTJ Lauritzen A/S SHIPPING J. Meyer / B. EngebretsenJefast Holding Ab REAL ESTATE L. Landeman / G. Bergin MARKETWEIGHTJernhusen Ab REAL ESTATE L. Landeman / G. Bergin MARKETWEIGHTJyske Bank A/S A- Stable Baa1U Stable BANKS K. Jensen / G. Bergin OVERWEIGHTKemira Oyj Wr MATERIALS M. Rosendal / L. Landeman OVERWEIGHTKesko Oyj CONSUMER GOODS B. Børsting / G. Bergin OVERWEIGHT

Recomm.S&P Moody's Fitch

2828

Our coverage 3 of 5

Source: Standard & Poor's, Moody's, Fitch, Danske Bank Markets

Ratings from S&P/Moody's/Fitch

Sector Analyst(s)

Company Rating Outlook Rating Outlook Rating OutlookKlaveness Ship Holding As SHIPPING J. Meyer / B. EngebretsenKlovern Ab REAL ESTATE L. Landeman / G. Bergin UNDERWEIGHTKungsleden Ab REAL ESTATE L. Landeman / G. Bergin MARKETWEIGHTLantmannen Ek For CONSUMER GOODS A. Moberg / G. Bergin MARKETWEIGHTLoomis Ab SERVICES & IT B. Børsting / M. RosendalLuossavaara-Kiirunavaara Ab MATERIALS L. Landeman / G. Bergin MARKETWEIGHTMeda Ab HEALTHCARE L. Landeman / G. BerginMetsa Board Oyj BB+ Pos Ba2 Stable MATERIALS M. Rosendal / L. Landeman MARKETWEIGHTMetso Oyj BBB Stable Baa2 Stable MACHINERY & HEAVY INDUSTRIALS B. Børsting / M. Rosendal OVERWEIGHTNcc Ab CONSTRUCTION A. Moberg / L. Landeman MARKETWEIGHTNeste Oyj ENERGY J. Magnussen / L. Landeman MARKETWEIGHTNibe Industrier Ab MACHINERY & HEAVY INDUSTRIALS A. Moberg / L. Landeman MARKETWEIGHTNokia Oyj BB+ Stable Ba1 Stable BB+ Pos TMT M. Rosendal / J. Magnussen MARKETWEIGHTNordax Bank Ab BANKS K. Jensen / G. BerginNordea Bank Ab AA- Neg Aa3 Stable AA- Stable BANKS K. Jensen / G. Bergin MARKETWEIGHTNorwegian Air Shuttle Asa TRANSPORTATION B. Børsting / M. Rosendal MARKETWEIGHTNorwegian Property Asa REAL ESTATE H. Syed/ B. Engebretsen MARKETWEIGHTNykredit Bank A/S A Stable Baa1U Stable A Stable BANKS K. Jensen / G. Bergin MARKETWEIGHTNynas Group ENERGY J. Magnussen / L. Landeman OVERWEIGHTObos Bbl REAL ESTATE H. Syed/ B. Engebretsen MARKETWEIGHTOdfjell Se SHIPPING J. Meyer / B. EngebretsenOlav Thon Eiendomsselskap Asa REAL ESTATE H. Syed/ B. Engebretsen OVERWEIGHTOp Corporate Bank Plc AA- Stable Aa3 Stable WD BANKS K. Jensen / G. Bergin OVERWEIGHTOrkla Asa CONSUMER GOODS H. Syed/ B. Engebretsen MARKETWEIGHTOutokumpu Oyj B3 Pos MATERIALS M. Rosendal / L. Landeman OVERWEIGHTPostnord Ab TRANSPORTATION G. Bergin / L. Landeman UNDERWEIGHTRamirent Oyj CONSTRUCTION J. Magnussen / B. BørstingSaab Ab Wr MACHINERY & HEAVY INDUSTRIALS A. Moberg / G. Bergin OVERWEIGHTSandvik Ab BBB Pos MACHINERY & HEAVY INDUSTRIALS B. Børsting / M. Rosendal OVERWEIGHTSas Ab B Stable Wr Stable TRANSPORTATION B. Børsting / M. Rosendal OVERWEIGHTSbab Bank Ab A Neg A2 Pos BANKS K. Jensen / G. Bergin MARKETWEIGHTSecuritas Ab BBB Stable Wr SERVICES & IT B. Børsting / M. Rosendal MARKETWEIGHT

Recomm.S&P Moody's Fitch

2929

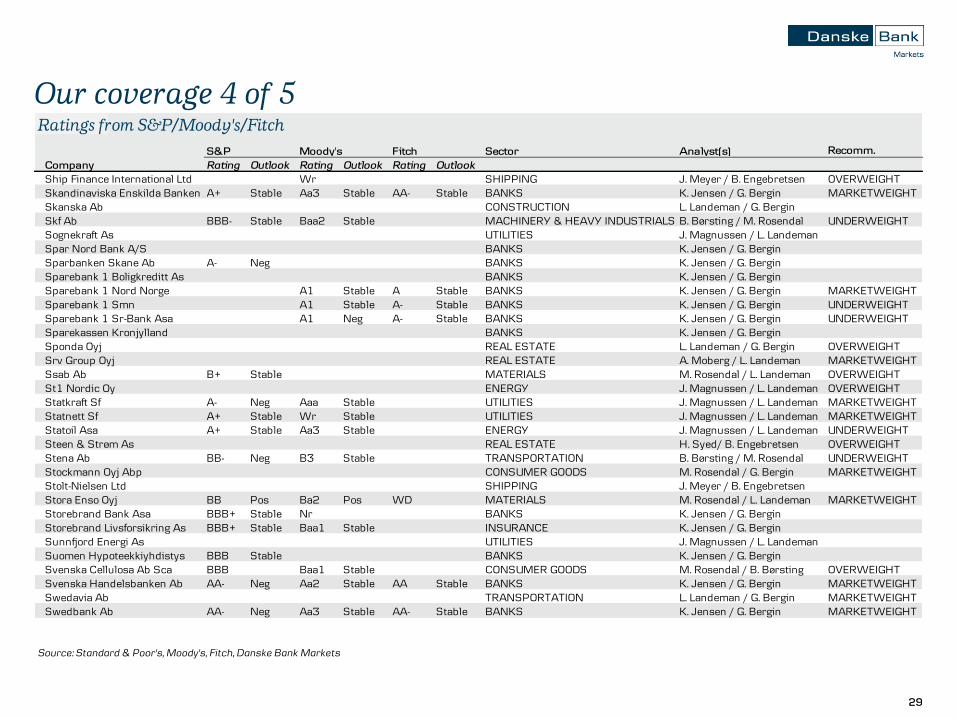

Our coverage 4 of 5

Source: Standard & Poor's, Moody's, Fitch, Danske Bank Markets

Ratings from S&P/Moody's/Fitch

Sector Analyst(s)

Company Rating Outlook Rating Outlook Rating OutlookShip Finance International Ltd Wr SHIPPING J. Meyer / B. Engebretsen OVERWEIGHTSkandinaviska Enskilda Banken AbA+ Stable Aa3 Stable AA- Stable BANKS K. Jensen / G. Bergin MARKETWEIGHTSkanska Ab CONSTRUCTION L. Landeman / G. BerginSkf Ab BBB- Stable Baa2 Stable MACHINERY & HEAVY INDUSTRIALS B. Børsting / M. Rosendal UNDERWEIGHTSognekraft As UTILITIES J. Magnussen / L. LandemanSpar Nord Bank A/S BANKS K. Jensen / G. BerginSparbanken Skane Ab A- Neg BANKS K. Jensen / G. BerginSparebank 1 Boligkreditt As BANKS K. Jensen / G. BerginSparebank 1 Nord Norge A1 Stable A Stable BANKS K. Jensen / G. Bergin MARKETWEIGHTSparebank 1 Smn A1 Stable A- Stable BANKS K. Jensen / G. Bergin UNDERWEIGHTSparebank 1 Sr-Bank Asa A1 Neg A- Stable BANKS K. Jensen / G. Bergin UNDERWEIGHTSparekassen Kronjylland BANKS K. Jensen / G. BerginSponda Oyj REAL ESTATE L. Landeman / G. Bergin OVERWEIGHTSrv Group Oyj REAL ESTATE A. Moberg / L. Landeman MARKETWEIGHTSsab Ab B+ Stable MATERIALS M. Rosendal / L. Landeman OVERWEIGHTSt1 Nordic Oy ENERGY J. Magnussen / L. Landeman OVERWEIGHTStatkraft Sf A- Neg Aaa Stable UTILITIES J. Magnussen / L. Landeman MARKETWEIGHTStatnett Sf A+ Stable Wr Stable UTILITIES J. Magnussen / L. Landeman MARKETWEIGHTStatoil Asa A+ Stable Aa3 Stable ENERGY J. Magnussen / L. Landeman UNDERWEIGHTSteen & Strøm As REAL ESTATE H. Syed/ B. Engebretsen OVERWEIGHTStena Ab BB- Neg B3 Stable TRANSPORTATION B. Børsting / M. Rosendal UNDERWEIGHTStockmann Oyj Abp CONSUMER GOODS M. Rosendal / G. Bergin MARKETWEIGHTStolt-Nielsen Ltd SHIPPING J. Meyer / B. EngebretsenStora Enso Oyj BB Pos Ba2 Pos WD MATERIALS M. Rosendal / L. Landeman MARKETWEIGHTStorebrand Bank Asa BBB+ Stable Nr BANKS K. Jensen / G. BerginStorebrand Livsforsikring As BBB+ Stable Baa1 Stable INSURANCE K. Jensen / G. BerginSunnfjord Energi As UTILITIES J. Magnussen / L. LandemanSuomen Hypoteekkiyhdistys BBB Stable BANKS K. Jensen / G. BerginSvenska Cellulosa Ab Sca BBB Baa1 Stable CONSUMER GOODS M. Rosendal / B. Børsting OVERWEIGHTSvenska Handelsbanken Ab AA- Neg Aa2 Stable AA Stable BANKS K. Jensen / G. Bergin MARKETWEIGHTSwedavia Ab TRANSPORTATION L. Landeman / G. Bergin MARKETWEIGHTSwedbank Ab AA- Neg Aa3 Stable AA- Stable BANKS K. Jensen / G. Bergin MARKETWEIGHT

Recomm.S&P Moody's Fitch

3030

Our coverage 5 of 5

Source: Standard & Poor's, Moody's, Fitch, Danske Bank Markets

Ratings from S&P/Moody's/Fitch

Sector Analyst(s)

Company Rating Outlook Rating Outlook Rating OutlookSwedish Match Ab BBB Stable Baa2 Stable CONSUMER GOODS A. Moberg / B. Børsting OVERWEIGHTSydbank A/S Baa1 Stable BANKS K. Jensen / G. Bergin OVERWEIGHTTallink Grupp As TRANSPORTATION B. Børsting / J. Magnussen MARKETWEIGHTTdc A/S BBB- Stable Baa3 Stable BBB- Stable TMT M. Rosendal / J. Magnussen MARKETWEIGHTTechnopolis Oyj REAL ESTATE L. Landeman / G. Bergin MARKETWEIGHTTeekay Lng Partners Lp SHIPPING J. Meyer / B. Engebretsen MARKETWEIGHTTele2 Ab TMT M. Rosendal / J. Magnussen OVERWEIGHTTelefonaktiebolaget Lm Ericsson BBB Neg Baa3 Neg BBB+ Neg TMT M. Rosendal / J. Magnussen UNDERWEIGHTTelenor Asa A Stable A3 Stable TMT M. Rosendal / J. Magnussen MARKETWEIGHTTelia Co Ab A- Baa1 Stable A- Stable TMT M. Rosendal / J. Magnussen UNDERWEIGHTTeollisuuden Voima Oyj BB+ Stable Wr BBB Neg UTILITIES J. Magnussen / L. Landeman OVERWEIGHTThon Holding As REAL ESTATE H. Syed/ B. Engebretsen OVERWEIGHTTopdanmark A/S INSURANCE K. Jensen / G. BerginTryg Forsikring A/S INSURANCE K. Jensen / G. BerginUpm-Kymmene Oyj BBB- Pos Baa3 Stable WD MATERIALS M. Rosendal / L. Landeman OVERWEIGHTVasakronan Ab REAL ESTATE L. Landeman / G. Bergin MARKETWEIGHTVattenfall Ab BBB+ Neg A3 Neg BBB+ Stable UTILITIES J. Magnussen / L. Landeman MARKETWEIGHTVestas Wind Systems A/S MACHINERY & HEAVY INDUSTRIALS J. Magnussen / M. Rosendal OVERWEIGHTVictoria Park Ab REAL ESTATE L. Landeman / G. Bergin OVERWEIGHTVolvo Ab BBB Pos Baa2 Stable BBB Stable MACHINERY & HEAVY INDUSTRIALS A. Moberg / M. Rosendal MARKETWEIGHTWihlborgs Fastigheter Ab REAL ESTATE L. Landeman / G. Bergin MARKETWEIGHTWilh Wilhelmsen Asa SHIPPING J. Meyer / B. EngebretsenYit Oyj CONSTRUCTION A. Moberg / L. Landeman MARKETWEIGHT

Recomm.S&P Moody's Fitch

3131

Fixed Income Credit Research team

Find the latest Credit Research: :

Danske Bank Markets: http://www.danskebank.com/danskemarketsresearch Bloomberg: DNSK<GO>

Thomas Hovard

Head of Credit Research

+45 45 12 85 05

Gabriel Bergin

Strategy, Financials

+46 8 568 80602

Katrine Jensen

Financials

+45 45 12 80 56

Jakob Magnussen

Utilities, Energy

+45 45 12 85 03

Henrik René Andresen

Credit Portfolios

+45 45 13 33 27

Bendik Engebretsen

Industrials

+47 85 40 69 14

Brian Børsting

Industrials

+45 45 12 85 19

Niklas Ripa

Credit Portfolios

+45 45 12 80 47

Louis Landeman

Industrials, Real Estate

+46 8 568 80524

Mads Rosendal

Industrials, TMT

+45 45 14 88 79

August Moberg

Industrials & Construction

+46 8 568 80593

Haseeb Syed

Industrials

+47 85 40 54 19

Jonas Meyer

Shipping

+47 85 40 70 79

3232

Disclosures

This research report has been prepared by Danske Bank Markets, a division of Danske Bank A/S ('Danske Bank'). The authors of this research report are Jonas Meyer, Senior Analyst, Haseeb Syed, Senior Analyst, and Bendik Engebretsen, Analyst.

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in the research report accurately reflect the research analyst’s personal view about the financial instruments and issuers covered by the research report. Each responsible research analyst further certifies that no part of the compensation of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority (UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation Authority are available from Danske Bank on request.

Danske Bank’s research reports are prepared in accordance with the recommendations of the Danish Securities Dealers Association.

Danske Bank is not registered as a Credit Rating Agency pursuant to the CRA Regulation (Regulation (EC) no. 1060/2009); hence, Danske Bank does not comply with nor seek to comply with the requirements applicable to Credit Rating Agencies.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-quality research based on research objectivity and independence. These procedures are documented in Danske Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any request that might impair the objectivity and independence of research shall be referred to Research Management and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do not report to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate finance or debt capital transactions.

Danske Bank, its affiliates and subsidiaries are engaged in commercial banking, securities underwriting, dealing, trading, brokerage, investment management, investment banking, custody and other financial services activities, may be a lender to the companies mentioned in this publication and have whatever rights are available to a creditor under applicable law and the applicable loan and credit agreements. At any time, Danske Bank, its affiliates and subsidiaries may have credit or other information regarding the companies mentioned in this publication that is not available to or may not be used by the personnel responsible for the preparation of this report, which might affect the analysis and opinions expressed in this research report.

3333

Completion and first dissemination

The completion date and time in this research report mean the date and time when the author hands over the final version of the research report to Danske Bank’s editing function for legal review and editing.

The date and time of first dissemination mean the date and estimated time of the first dissemination of this research report. The estimated time may deviate up to 15 minutes from the effective dissemination time due to technical limitations.

See the final page of this research report for the date and time of first dissemination.

Validity time period

This communication as well as the communications in the list referred to below are valid until the earlier of (a) dissemination of a superseding communication by the author, or (b) significant changes in circumstances following its dissemination, including events relating to the market or the issuer, which can influence the price of the issuer or financial instrument.

Investment recommendations disseminated in the preceding 12-month period

A list of previous investment recommendations disseminated by the lead analyst(s) of this research report in the preceding 12-month period can be found in Danske Banks’ DCM research database at http://www-2.danskebank.com/danskemarketsresearch.

Other previous investment recommendations disseminated by Danske Bank Markets, DCM Research are also available in the database.

See http://www-2.danskebank.com/Link/researchdisclaimer for further disclosures and information.

3434

General disclaimer

This research has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for informational purposes only. It does not constitute or form part of, and shall under no circumstances be considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments (i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or options, warrants, rights or other interests with respect to any such financial instruments) ('Relevant Financial Instruments').

The research report has been prepared independently and solely on the basis of publicly available information that Danske Bank considers to be reliable. While reasonable care has been taken to ensure that its contents are not untrue or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and reflect their judgement as of the date hereof. These opinions are subject to change, and Danske Bank does not undertake to notify any recipient of this research report of any such change nor of any other changes related to the information provided in this research report.

This research report is not intended for, and may not be redistributed to, retail customers in the United Kingdom or the United States.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank's prior written consent.

Disclaimer related to distribution in the United States

This research report was created by Danske Bank A/S and is distributed in the United States by Danske Markets Inc., a U.S. registered broker-dealer and subsidiary of Danske Bank A/S, pursuant to SEC Rule 15a-6 and related interpretations issued by the U.S. Securities and Exchange Commission. The research report is intended for distribution in the United States solely to 'U.S. institutional investors' as defined in SEC Rule 15a-6. Danske Markets Inc. accepts responsibility for this research report in connection with distribution in the United States solely to 'U.S. institutional investors'.

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence of research analysts. In addition, the research analysts of Danske Bank who have prepared this research report are not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements of a non-U.S. jurisdiction.

Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial Instrument may do so only by contacting Danske Markets Inc. directly and should be aware that investing in non-U.S. financial instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be registered with the U.S. Securities and Exchange Commission and may not be subject to the reporting and auditing standards of the U.S. Securities and Exchange Commission.

Report completed: 20 March 2017, 14:16 GMTReport first disseminated: 21 March 2017, 07:00 GMT

![Parliament · (Oslo) Norwegian Krone (NOK) 1 NOK 5.65 Inn 7.07 NOK 1 5utnâ 17 5 (King Harald V) inn]ulJLnu (Copenhagen) (Jutland) 43,077 406 90 no (Greenland)](https://static.fdocuments.in/doc/165x107/5fa77841f9f7cc1be702dab3/parliament-oslo-norwegian-krone-nok-1-nok-565-inn-707-nok-1-5utn-17-5-king.jpg)