Week 01 power_point-acct_101_8w_online

38

ACCT 101 Accounting and Financial Management Week #1 ACCT101-Week 1 1

-

Upload

beulah-heights-university -

Category

Education

-

view

140 -

download

0

Transcript of Week 01 power_point-acct_101_8w_online

ACCT 101 Accounting and

Financial Management

Week #1

ACCT101-Week 1 1

WEEK 1 - TOPICS

• Differences Between Not-for-Profit and For

Profit Organizations

• Importance/Purpose of Accounting

• Language and Terminology of Accounting

• The Double-Entry System (Recording

transactions in the Accounting System)

ACCT101-Week 1 2

WEEK 1 - TOPICS

• The Accounting Equation

• Accrual accounting vs Cash Basis

Accounting

• Standard Setting for Financial Reporting

• Audit Report

3ACCT101-Week 1

Differences Between Nonprofit and

For Profit OrganizationsNonprofit For-Profit

Owners None Stockholders

Primary Mission Provide Service needed

by society

Earn profit for the

Stockholders

Tax Status Exempt from Income

Taxes if approved by IRS

under code 501(c)(3)

Corporation and/or their

owners are subject to

Income taxes

Example of Revenue Donor contributions,

grants, membership

dues, program revenue

Sales of products or

services, investment

income, and gains

Excess of Revenue over

Expenses (Profit)

Reinvested to further the

purpose of the

organization

Distributed to owners as

dividend or reinvested

into the business

ACCT101-Week 1 4

Example of Nonprofit

Organizations• Section 501(c)(3) -- the famous one -- describes

[nonprofit!] (1) serving charitable, religious,

scientific or educational purposes (2) no part of

the income of which "inures to the benefit of"

anyone.

• Some Examples are:

• Religious, Educational, Charitable, Scientific, Literary,

Testing for Public Safety, to Foster National or

International Amateur Sports Competition, or Prevention

of Cruelty to Children or Animals Organizations.

ACCT101-Week 1 5

Importance Of Accounting

InformationAccounting provides financial information

that is used by:

Members, Donors, Managers, Investors,

Financial Analysts, Creditors, Regulators,

Employees, etc.

They need to understand the current

financial status of an organization, and the

events that caused a change in that status.

ACCT101-Week 1 6

Purpose of the Accounting

SystemThe purpose of accounting is to:

identify, record, and communicate the economic

events of an organization to interested users.

In another words

Its goal is to collect, summarize, and report

information concerning the impact of various

business events on an organization’s financial

status and financial performance.

ACCT101-Week 1 7

The Accounting Cycle• STEP 1: ANALYZE TRANSACTIONS FROM SOURCE

DOCUMENTS

• STEP 2: RECORD TRANSACTIONS IN A JOURNAL

• STEP 3: POST FROM THE JOURNAL TO THE LEDGER

• STEP 4: PREPARE A TRIAL BALANCE OF THE

LEDGER

• STEP 5: DETERMINE NEEDED ADJUSTMENTS

• STEP 6: PREPARE A WORKSHEET

• STEP 7: PREPARE FINANCIL STATEMENTS FROM A

COMPLETED WORKSHEET

ACCT101-Week 1 8

Financial StatementsMain Financial Statements required by U.S. GAAP

(GAAP = Generally Accepted Accounting Principles )

GAAP also requires the presence of Notes to the Financial Statements

Nonprofit Organizations For-Profit Corporations

Statement of Activities or Statement

of Functional Expenses

Income Statement or Statement of

Operations

Statement of Financial Position Balance Sheet

Statement of Cash Flows Statement of Cash Flows

ACCT101-Week 1 9

Accounting Language and

TerminologyTransaction

• Definition: A business/organization event, expressed in

monetary terms, that is entered into the accounting

records.

• Examples: Purchasing equipment, paying staff

members, and recording a sale are all examples of

accounting transactions.

• For each transaction, one must decide:

1. Which accounts are affected by the transaction

2. Whether the accounts were increased or decreased

3. How to increase or decrease the accounts affected

ACCT101-Week 1 10

Accounting Language and

TerminologyAssets

• Definition: What the business owns and future

economic benefits it is entitled to.

• Examples: Cash, contributions receivable,

accounts receivables, inventory, property,

buildings, equipment, and investments are

examples of what a business owns. Prepaid

insurance is an example of a future economic

benefit the business is entitled to.

ACCT101-Week 1 11

Accounting Language and

TerminologyLiabilities

• Definition: Amount owed to the creditors in the

form of debts or other obligations. Think of

liabilities as simply “money that you owe.”

• Examples: Accounts payable, accrued

expenses, Debts, deferred income.

ACCT101-Week 1 12

Accounting Language and

TerminologyNet Assets

• Definition: the difference between the assets and

liabilities of a not-for-profit organization.

• Examples: Unrestricted, Temporarily Restricted

and Permanently Restricted.

• Note: It is equivalent to stockholders' equity in

the commercial, or for profit world and a

measure of net worth in our personal financial

world.

ACCT101-Week 1 13

Accounting Language and

TerminologyRevenues

• Definition: Inflows or their enhancements of assets of an

entity or settlement of its liabilities (or a combination of

both) from delivering or producing goods, receiving

services, or other activities that constitute the entity's on

going or central operations. Think of revenues as

Inflows.

• Examples: Not-for-profit organizations generally have

two primary sources of revenue- contributions

(sometimes called “support and contributions”) and fee-

for-services activities.

ACCT101-Week 1 14

Accounting Language and

TerminologyExpenses:

• Definition: Outflows or other using up of assets or

incurrence of liabilities (or a combination of both) from

delivering or producing goods, rendering services, or

carrying out other activities that constitute the entity’s

ongoing major or central operations. Think of expenses

as Outflows.

• Examples: Program expenses, Fundraising expenses,

General and Administrative expenses.

ACCT101-Week 1 15

The Double Entry Accounting

(Dual Aspect of Accounting)

• Every financial transaction, without exception, is

recording at least two pieces of information. If we receive

cash, there are reasons we received the cash:

• Double-entry accounting is the distillation of a financial

transaction into a set of debits and credits that, when

added together, equal zero. The debit entries must

equal the credit entries.

• Debits are left-hand entries

• Credits are right-hand entries.

ACCT101-Week 1 16

Account Name

Debit / Dr. Credit / Cr.

• Accounts: Record of increases and decreases in a specific asset, liability, Net Asset, revenue, or expense item.

• Debit = “Left”

• Credit = “Right”

An Account can be illustrated in a T-Account form.

The Double Entry Accounting

(Dual Aspect of Accounting)

ACCT101-Week 1 17

How Each of the Account is affected by

the Double Entry AccountingAsset Account

• To increase an Asset account, debit it; to decrease it,

credit it.

Liability or Net Asset Account

• To increase a Liability or Net Asset account, credit it; to

decrease it, debit it.

Revenue Account

• To increase a Revenue account, credit it; to decrease it,

debit it.

Expenses Account

• To increase an Expense account, debit it; to decrease it,

credit it. ACCT101-Week 1 18

Examples of Recording

TransactionsJanuary Transaction

• Transaction 1. On January 31, a donor contributes

$10,000, without restriction, for the operation of the

Church. This transaction affects the general ledger

accounts as follows:

Date Account Name Debit Credit

Jan-31 Cash 10,000

Revenue-Contribution General 10,000

Contribution received

ACCT101-Week 1 19

Examples of Recording

TransactionsFebruary Transactions

• Transaction 2. On February 1, the Church rents worship

space. A check is written for $2,000. This covers a one-

time security deposit of $1,000 plus the February rent of

$1,000.

Date Account Name Debit Credit

Feb-01 Security Deposit 1,000

Rent Expenses 1,000

Cash 2,000

Security deposit and rent payment

ACCT101-Week 1 20

Examples of Recording

TransactionsFebruary Transactions

• Transaction 3. On February 2, a $400 check is written

to the utility as a one-time security deposit for electricity

and heat service.

Date Account Name Debit Credit

Feb-02 Security Deposit 400

Cash 400

Security deposit for utilities

ACCT101-Week 1 21

Examples of Recording

TransactionsFebruary Transactions

• Transaction 4. On February 19, the Church receives a

contribution of $8,000 that the donor specifies must be

used for the purchase of furniture. The contribution is

deposited into a money market account. This transaction

affects the general ledger accounts as follows:

Date Account Name Debit Credit

Feb-19 Cash-Money Market Account 8,000

Contribution-Temporarily Restricted 8,000

Contribution received for furniture

ACCT101-Week 1 22

Examples of Recording

TransactionsFebruary Transactions

• Transaction 5. The electricity and heating invoice has

not arrived. It is estimated that the amount for February's

usage was $350, so the following accrual adjusting entry

is recorded on February 28:

Date Account Name Debit Credit

Feb-28 Electricity, Heat and Water Expenses 350

Accrued Expenses 350

Estimated utilities for Feb

ACCT101-Week 1 23

Accounting Equation

Using Elements of the Statement of Financial Position (SOFP)

Assets = Liabilities + Net Assets

Liabilities• Accounts Payable

• Accrued Expenses

• Debt, Short-term

• Deferred Income

• Debt, long-term

Assets• Cash

• Cash Equivalents

• Contributions Receivable

• Accounts Receivable

• Other Receivables

• Investments (Chapter 5)

• Inventory

• Property Plant and Equipment (PP&E)

• Other Fixed Assets

• Other Assets

Net Assets• Unrestricted

• Temporarily Restricted

• Permanently Restricted

24ACCT101-Week 1

Accounting EquationExample # 1• Let’s assume that our not-for-profit organization purchased

Equipment for $3,000 on credit. This transaction has two effects

on the accounting elements:

• Since an asset was acquired, equipment, assets increased

• Since the asset was purchased on credit (Accounts Payable),

liabilities also increased

• Assets = Liabilities + Net Assets

• +$3,000 +$3,000

• Assets ( on one side of the equation) increased by $3,000, while

liabilities ( on the other side of the equation, also increased by

$3,000, thus maintaining the equation in balance. Every business

transaction has at least two effects on the accounting equation.

25ACCT101-Week 1

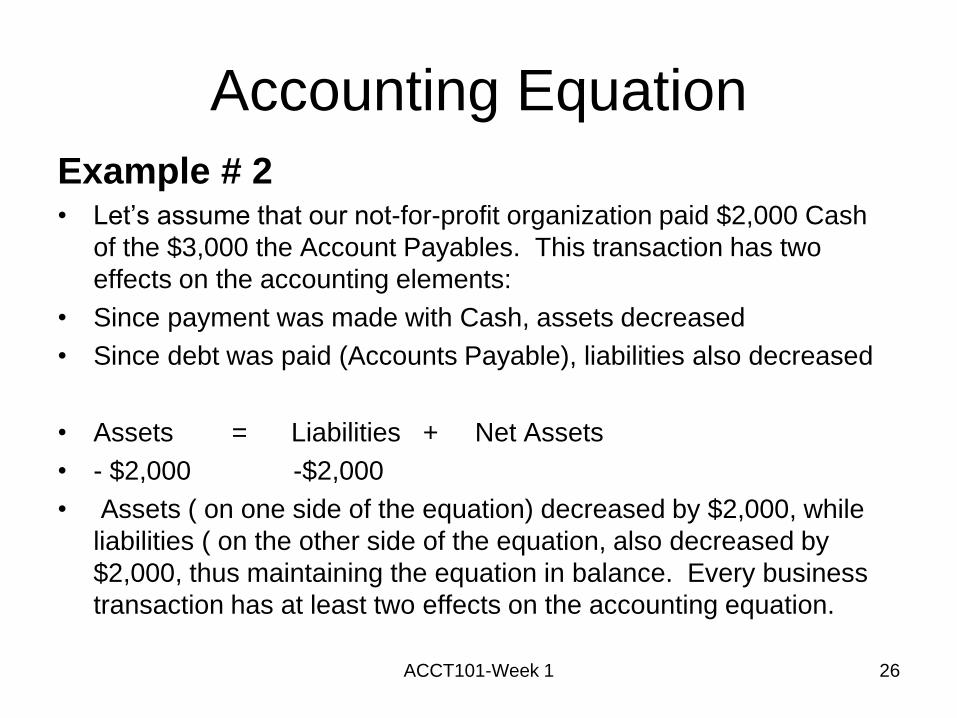

Accounting Equation

Example # 2• Let’s assume that our not-for-profit organization paid $2,000 Cash

of the $3,000 the Account Payables. This transaction has two

effects on the accounting elements:

• Since payment was made with Cash, assets decreased

• Since debt was paid (Accounts Payable), liabilities also decreased

• Assets = Liabilities + Net Assets

• - $2,000 -$2,000

• Assets ( on one side of the equation) decreased by $2,000, while

liabilities ( on the other side of the equation, also decreased by

$2,000, thus maintaining the equation in balance. Every business

transaction has at least two effects on the accounting equation.

26ACCT101-Week 1

Accounting Equation

Practice A-1

• Practice Exercise A-1: Fill in the Blanks

• Assets = Liabilities + Net Assets

• 1. $40,000 $25,000 $___________

• 2. $________ $38,000 $52,000

• 3. $70,000 $_______ $48,000

• 4. $75,000 $ -0- $________

27ACCT101-Week 1

The Accounting Equation - Joining the Pieces

_________Net Assets________________

Assets = Liabilities + (Beg. Nets Assets + Revenue - Expenses)Things that Money that Net Assets=Assets minus Inflows that Outflows that

are owned you owe Liabilities increase decrease assets

as well as assets or or increase

future reduce liabilities

economic liabilities

benefits

entitled to

Examples: Examples: Examples Examples: Examples:

Cash Accounts payable Unrestricted Contributions Salary

Cash equivalents Accrued expenses Temporarily Restricted Fees for services Rent

Investments Deferred income Permanently Restricted Utilities

Receivables Depreciation

Inventories

Property, Plant

and Equipment

Prepaid Expenses

28ACCT101-Week 1

The Accounting Equation - Joining the Pieces

Example # 1• Let’s assume that our not-for-profit organization paid salaries of

employees, $1,500. This transaction has two effects on the

accounting elements:

• Since an expense was incurred, Salaries, expenses increased.

• Since the salaries were paid, an asset, Cash, decreased.

………… Net Assets…………………….

• Assets = Liabilities + ( Beg. Net Assets + Revenue - Expense)

• -$1,500 -$1,500

• Assets ( on one side of the equation) decreases by $1500, Net

Assets ( on the other side of the equation, also decreased $1500,

thus maintaining the equation in balance.

29ACCT101-Week 1

The Accounting Equation - Joining the Pieces

Example # 2• Let’s assume that our not-for-profit organization received a

general contribution of $5,000 in cash. This transaction has two

effects on the accounting elements:

• Since Cash was received, Assets increased.

• Since General contribution was received, Revenue increased.

………… Net Assets…………………….

• Assets = Liabilities + ( Beg. Net Assets + Revenue - Expense)

• +$5,000 +$5,000

• Assets ( on one side of the equation) increases by $5,000, Net

Assets ( on the other side of the equation, also increased $5,000,

thus maintaining the equation in balance.

30ACCT101-Week 1

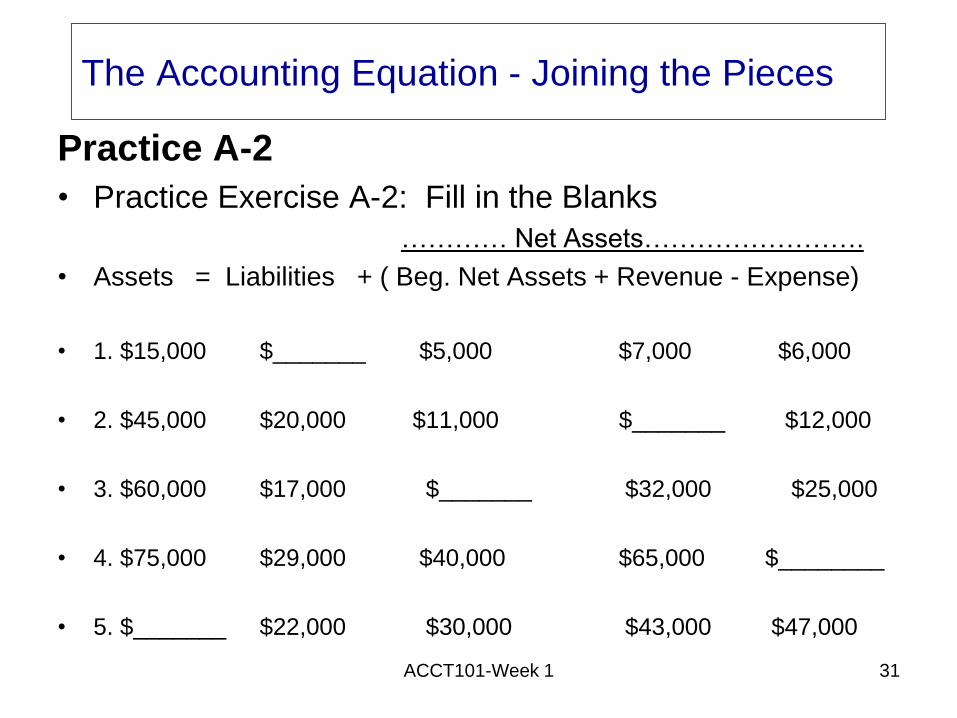

The Accounting Equation - Joining the Pieces

Practice A-2

• Practice Exercise A-2: Fill in the Blanks

………… Net Assets…………………….

• Assets = Liabilities + ( Beg. Net Assets + Revenue - Expense)

• 1. $15,000 $_______ $5,000 $7,000 $6,000

• 2. $45,000 $20,000 $11,000 $_______ $12,000

• 3. $60,000 $17,000 $_______ $32,000 $25,000

• 4. $75,000 $29,000 $40,000 $65,000 $________

• 5. $_______ $22,000 $30,000 $43,000 $47,000

31ACCT101-Week 1

Accrual vs. Cash Basis Accounting

Accrual- Required by GAAP

• Revenues are recognized when they are earned, regardless of when the cash is actually collected.

• Revenues must be realizable, i.e. the organization must at some time in the future be able to convert any receivables resulting from revenue recognition to cash.

• Match expenses to the revenue they generate, as applicable.

• Recognize some expenses in the fiscal year or accounting period in which they are used by the organization, i.e. organization receives the benefit of the expense, as applicable.

• Recognize some expenses using a systematic allocation of costs to accounting periods (classic example: depreciation expense)

32ACCT101-Week 1

Accrual vs. Cash Basis Accounting

Cash Basis

• Transactions are only recorded when cash is received or disbursed.

• Terms to use are cash receipts and disbursements, not revenues and expenses

• Pure application of cash basis of accounting, only asset would be balance in cash account. There would be no liabilities, and the cash balance would equal the total net assets.

• In actual practice, pure cash basis is seldom used. More often, a modified cash basis is used.

– Property, plan and equipment and long-term debt are recorded.

– Certain payables and receivables are recorded.

33ACCT101-Week 1

The Institutional Setting and

Development of Financial Reporting

Standards• Foundation of accounting consists of a set of what are called

generally accepted accounting principles, or GAAP, for short

• Currently, these principles are established by Financial Accounting Standards Board, FASB

- Created in 1973

- Consists of seven leading accountants and a

professional staff

-nongovernmental organization, private

-financially controlled and supported by the

Financial Accounting Foundation (FAF)

-FAF funded by contributions from business

firms and the accounting profession

-FAF also oversees the Governmental Accounting Standards Board (GASB), which sets GAAP for governmental entities.

34ACCT101-Week 1

American Institute of Certified

Accountants (AICPA)

• National, professional organization for all Certified Public Accountants

• Mission: provide resources, information and leadership to its members

• Organization has also issued accounting guidance in the past that is part of the accounting principles that comprise GAAP for not-for-profit organizations

• Specifically

- Advocacy

- Certification and Licensing

- Communications

- Recruiting and Education

- Standards and Performance35ACCT101-Week 1

The Internal Revenue Service (IRS)

• Has certain powers given by Congress to

regulate the ways in which taxable income

is calculated for purposes of assessing

income taxes

• Specific Filing Requirements for Not-for-

Profit Organizations

• Specific Reporting Requirements for Not-

for-Profit Organizations

36ACCT101-Week 1

The Audit Report

• Who is responsible for preparing the financial statements that are being audited?

• What is the independent auditor hired to do?

• Types of opinions on the financial statements issued by the auditor:

- unqualified ( aka “ a clean opinion)

-qualified ( i.e. financial statements are prepared in accordance with GAAP , with some exceptions)

-adverse (i.e. Financial statements are not prepared in accordance with GAAP)

37ACCT101-Week 1

The Audit Report

• It is the responsibility of the not-for-profit organization’s management to prepare the financial statements

• Independent auditors are hired to perform an audit and issue an opinion as to whether or not the financial statements are prepared in accordance with GAAP

• The financial statements include:

- Statement of Financial Position (For-Profit: Balance

Sheet)

- Statement of Activities ( For-Profit: Income

Statement

- Statement of Cash Flows ( For-Profit: the same

- Notes to the Financial Statements (For-Profit: the

same.

38ACCT101-Week 1