SITM was established in 1996 as a pioneer in the field of ...

We at SITM are committed to develop world class Telecom Business Leaders, who can e� ectively handle the dynamic and ever - changing technological and business dynamics with absolute ease and authority. The team at SITM � rmly believes in strong academics combined with industry exposure through visits of several experts from the industry. The programs o� ered by SITM integrate a competitive learning environment through a broad curriculum encompassing classroom teaching, valuable industry inputs, research projects, seminars, workshops and a myriad of extra curricular activities. In the pursuit of excellence and to give the curriculum its distinctive � avour, the syllabus is continually revived based on the inputs from the faculty, industry and alumni. All the programs follow

intensive case studies based approach. SITM lays deep emphasis on an all-round development of an individual which includes improving communication skills, nurturing teamwork and inculcating a never say die attitude. The telecommunication systems and IT forms the backbone for any company hence managing them e� ectively and strategically is a need of the hour. SITM has 2000 + strong alumni network and most of our alumni are holding middle level to senior management positions in companies.

Last but not the least, we strive to instil human values to make better citizens with moral courage and zeal to follow their heart, make a di� erence and help them achieve their true potential.

© 2016, Symbiosis Institute of Telecom ManagementAll rights reserved. This publication is the sole property of SITM. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of SITM

1

Dr. Sunil PatilDirector, SITM

DIRECTOR’S MESSAGESITM is the pioneer educational institution in Asia imparting management education to aspiring telecom and ICT managers. SITM has consistently endeavored to take up new initiatives in both business and research domains. One such e� ort is Prévision, SITM’s Annual Telecom Forecast. Prévision is in its 14th year and aims at providing the industry a neutral and insightful single point of view regarding the emerging trends in the telecom and ICT sectors for the forthcoming year. These domains continue to observe new emerging technologies and business models and all of this is making forecasting a challenge. The forecast is presented in the � agship event of SITM, International Telecom Seminar. It is noted that the forecast presented in this report is very well received by the industry.

Prévision involves accumulating inputs from detailed research into contemporary telecom technologies, telecom business and other determinants of change and meticulously analyzing them and forecasting future trends. It is a culmination of the collective endeavor of SITM students with 1500 man hours of e� orts put in by them. The student forecast team is guided by SITM faculty and some of our esteemed alumni. As part of ongoing process improvement for Prévision, SITM students for the past 4 years have been conducting a Corporate Interaction Program. The insights gained from such interactions with Industry Subject Matter Experts have improved the quality of our predictions and the students have bene� tted immensely from their knowledge & experience.

We are fortunate to have Deloitte Haskins & Sells for their continued initiatives in both business and research domains. At the release of the 14th edition of Prévision, I would like to thank the SITM Alumni community and the telecom industry for sharing their valuable insights with Prévision team. Your contribution has helped us in improving the quality of the predictions. I would also like to thank Dr. K.S.S. Iyer, Honorary Adjunct Professor, SITM for guiding the Prévision team in the application of forecasting models for statistical analysis.

2

Dr. Giri G HallurAsst. Professor & Faculty In charge

of Prévision, [email protected]

MESSAGE FROM FACULTY IN CHARGEIt gives me immense pleasure in presenting to you the fourteenth edition of Prévision, SITM’s Annual Telecom Forecast. SITM curriculum lays a lot of emphasis on nurturing research aptitude of the students in the form of Summer Project & Research Project. Prévision is an extension of this thought process. It provides the students a platform to understand the linkages between the theoretical learning and dynamic industry trends. Through the Prévision research process the students are able to understand the e� ect of macro-economic, technological & regulatory factors on the telecom industry in India as well as the world.

Prévision, which is in its 14th year was conceptualised in 2003 by one of our esteemed alumnus Mr. Kundan Das (Batch 1998 - 2000), who then teamed up with two other Alumni, Mr Rahul Sharma (Batch 1999 - 2001) & Mr. Aniruddha Harne (Batch 2002 - 2004). The Alumni team has, over the years grown with active participation by Alumni from subsequent batches, who havecontinuously guided the student team. Prévision was started with the aim of providing the industry a neutral and insightful single point of view regarding the emerging telecom trends. And this year’s Prévision is yet another step in that direction.

The three step research process starts with data collection, followed by data analysis with the help of statistical models and � nally culminates into forecast after incorporating inputs of SITM Alumni & Faculty. The MBA 1st year students, through the activity of data collection under the guidance of the 2nd year students get initiated into the forecast process. At the data analysis stage, the 2nd year students get an opportunity to assimilate knowledge from statistics, technology and experiential learning gained during their summer internships. Whitepapers, written by the students at the end of second stage are reviewed by some of our Alumni, SITM faculty & Industry mentors from Deloitte Haskins & Sells. The � nal Prévision document incorporates the comments/changes suggested by them. The entire Prévision process is closely monitored & guided by SITM faculty. And the process streamlining is supervised by Deloitte Haskins & Sells.

In Prévision 2017, we have, in our special feature discussed the technology, business and � nancial aspects of Smart Cities. In the opinion of the stake holders, Smart Cities need to adopt various models comprising of advertisements to utility based subscription to monetize on the smart city ecosystems. Another key area highlighted was the need for compliances and operation standards mandatory across vendors so as to ensure interoperability and collaboration across multiple platforms and heterogeneous data sources.

For the past 10 years, the SITM Alumni community has guided and provided the Prévision team with their insights on key trends in the telecom domain. I thank the SITM Alumni for their continued support. I also express my gratitude to the telecom fraternity for its support. We look forward for your comments/feedback.

3

Mr. Aniruddha HarneVodafone Group, UK

FOUNDER’S SPEAKSince inception (2003), Prevision from SITM has consistently raised the benchmark for a management institute to portray global telecom ecosystem forecast.

The objective behind this exercise was as dual i.e. to demonstrate the understanding of complex telecom value chain from regulatory impacts to value proposition including analyzing technology, consumer and industry impacts as whole and to venture a step beyond to forecast next year’s impact across various verticals.

SITM students has been successful over the years in demonstrating value in the annual ‘Telecom Forecast’ which is now within noticeable limits by the Industry leaders. Over the years with addition of social impact due to technologies, wider global coverage and added domains, this report has garner much wider interest in the telecom community.

To highlight some of the last year Prevision (2016) forecasts from the Indian telecom domain, they are almost in line with recent TRAI annual reports (FY15-16). This clearly demonstrate the deep value which students of SITM bring to the industry i.e. ability to comprehend and predict the change based on � rm analysis and research.

With inclusion of Mobile payments, VoLTE, IoT, Social Media and New initiatives within India and globally, Prevision has quintessentially become a much sought after report across telecom fraternity.

This entire process, I have been closely following since inception and the annual forecast has taken quantum leaps in terms of technology, global coverage and methodologies adopted for analysis across multiple domains.

‘Prevision’ has de� nitely turned into a powerful script produced every year; which is must read by all students of telecom management and sought after report for Telco professionals globally.

All the Best!

Mr. Rahul SharmaDirector – Digital Works

Cognizant Germany

Back in 2005 neutral academic research to predict technology, and predict it in the near-term which is measurable was totally missing in the Indian Technology landscape. 5-10 year predictions are relatively “safer” and somehow the challenge goes away to see the hits & misses in 5 years. The consumer view was also missing from the industry view and that was something that we wanted to change. The way Prevision has matured over the last decade, it’s an investment well made by SITM.

4

PREFACE“The pursuit of perfection often impedes improvement”

- George Will

Prevision, an endeavour by the students of SITM,under the guidance of our august alumni, industry experts and faculty members. Prevision strives to perfection every year through process improvisation and comprehensive parameter analysis. Smart Cities, the special feature edition of Prevision 17, attempts to present a holistic purview from regulatory, corporate and academic perspectives. As a gesture of our gratitude, we would like to mention all the experts who helped us in enriching the content and concepts of the magazine through their valuable time and constant guidance.

• Dr. A.Ravindra, Chairman, Smart cities India Foundation• Mr. Sohag Sarkar, Associate Director, KPMG Advisory Services Pvt. Ltd.• Mr. Sunit Kumar, Assistant Manager, KPMG Advisory• Mr. Aditya Basu, Product Manager, Happiest Minds Technologies• Mr. Anurag Walia, Vice President - Sales Strategy Execution, Tata Communications• Mr. Vikram Singh, Associate Manager- Smart cities, Sterlite Technologies• Mr. Sridhar Chalapathy, Mass Communication Head, Sify Technologies• Mr. Piyush Gandhi, Vice President, GIFT City, Gandhinagar• Mr. Nirav Patel, GIFT City, Gandhinagar• Mr. Sameer Jain, Sr. consultant, KPMG Advisory Services Pvt. Ltd• Mr. HimanshuJangwal, Manager, KPMG• Mr. Rajul Mehrotra, General manager- Smart cities, IBM

We sincerely appreciate their cooperation and look forward to such associations and interactions in the future.

INDUSTRY SPEAK

“Very Good work. Prevision was very professionally handled. Hard work shows, keep it up.”- Ms. Anjali Chatterjee, GM, VSNL, Mumbai

“Prevision was most impressive. The organisation and presentation of the event was of very high order”. - Mr. Abhay Arora, Technical Head, Sterlite Optical Technologies Ltd

“Well organised. Prevision was very interesting. A lot of good work, remarkable insights. Should organise more in depth interaction between students and delegates”. - Mr. Shrinivas Rao Addepalli, Head Corporate Strategy, Tata Communications

“A very wonderful and informative session. The Prevision was extremely informative.”- Mr. Sudhir Gupta, Advisor, TRAI

“Impressed by the Prevision presentation.” - Mr. Asit Tandon

“A very focussed forecast- Prevision . Thanks for the valuable inputs. “ - Mr. K.Seetaraman, TCS

5

PILLARS OF PRÉVISIONPRÉVISION PIONEERS

Kundan Das - Parallel Wireless Inc. Rahul Sharma –Cognizant, Germany Aniruddha Harne–Vodafone Group,UK

ALUMNI MENTORS

Sumit Gandhi - EY Saurabh Saxena - Accenture Nikilesh Kolipakula - Accenture Utkarsh Nalgundwarkar - EYSaksham Saxena - InfosysGaurav Chauhan - EYJaskaran Singh - Sify

INDUSTRY MENTORS

Hemant Joshi - Partner, Deloitte Haskins & SellsShrikrishna Sumant - Deloitte Haskins & Sells Anu Peisker - Deloitte Haskins & Sells

FACULTY MENTOR

STATISTICS

Dr. K.S.S. Iyer (Hon. Adjunct Professor)

FINANCE

Ramamurthy Venkatesh(International Adjunct Faculty)Chintan Vadgama(Assistant Professor - Finance)

FACULTY IN CHARGE

Dr. Giri HallurFaculty (Telecom)

STUDENT IN CHARGE

Sumit Singh

STUDENTS IN CHARGE (TECHNOLOGY)

Jimit RavalKushagra NagpalPrathamesh PandeRishika Ghosh

STUDENTS IN CHARGE (STATISTICS)

Arjun IyerArun SureshFaraaz Ahmed GauseeTanuj Gupta

STUDENT EDITORS

Arpita Ghosh Dhruvika SolankiArnab Mohapatra

STUDENTS IN CHARGE (DESIGN & SOCIAL MEDIA)

Naresh Kumar HegdeSurya Nair

STUDENT IN CHARGE (LOGISTICS)

Arjun Iyer

STUDENT INPUTS

Anoop MathewGirish KumarNayan Jyoti Bhuyan

DisclaimerIn no event shall Symbiosis Institute of Telecom Management, Pune, here after referred to as SITM, be liable for any indirect, punitive, incidental, special or consequential damages arising out of or in any way with any content (or any material provided here under) whether biased or on contract, tort, strict liability or otherwise even if SITM has been advised of the possibility of the damages.

Note to readers: The � nancial year for India is taken from April to March, where as for rest of the world, the calendar year is taken from January to December.© 2016, Symbiosis Institute of Telecom Management.All rights reserved. This publication is the sole property of SITM. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of SITM.

6

PILLARS OF PRÉVISIONSTUDENT TEAMS

INDIAN TELECOM

Anubha Pandit (Head) Tanuj Gupta

ECONOMY

Shivam (Head) Dhruvika Solanki Rituraj Zala

CONSUMER ELECTRONICS

Prathamesh Pande (Head)Chetna Chandiramani

GLOBAL TELECOM

Nareshkumar Hegde (Head) Faraaz Ahmed Gausee Jimit Raval Nikhilesh Harde

TELECOM TECHNOLOGIES

Kushagra Nagpal (Head) Nilesh Bamotriya

STUDENT TEAMS

BROADBAND

Arun Suresh (Head) Roinak Sarkar Rishika Ghosh

COMMUNICATION INFRASTRUCTURE

Arjun Iyer (Head) Akash Agrawal

VAS & MOBILITY

Aakanksha Sharma (Head) Arnab Mohapatra

TELECOM SOFTWARE

Surya Nair (Head) Prashant Tandekar Nikhilesh Harde

SPECIAL FEATURE

Shilpy Sinha (Head) Shreyas Khase Arpita Ghosh Darset Merchant

DisclaimerIn no event shall Symbiosis Institute of Telecom Management, Pune, here after referred to as SITM, be liable for any indirect, punitive, incidental, special or consequential damages arising out of or in any way with any content (or any material provided here under) whether biased or on contract, tort, strict liability or otherwise even if SITM has been advised of the possibility of the damages.

Note to readers: The � nancial year for India is taken from April to March, where as for rest of the world, the calendar year is taken from January to December.© 2016, Symbiosis Institute of Telecom Management.All rights reserved. This publication is the sole property of SITM. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of SITM.

7

INDIAN TELECOM

With a strong growth in the past few decades, the Indian Telecom Industry is currently the world’s second largest telecommunication market. Although the rate of growth has slowed over the past few years, it is still expected to contribute substantially to India’s GDP. The highlights for this year will be the spectrum auction of all bands from 700 MHz to 2500 MHz bands and the impact of RJio’s 4G launch on the telecom industry. The ecosystem for the 700 MHz band is yet to be developed and ambitious base price shall question the a� ordability aspect for TSPs. GSM service providers shall slowly start phasing out their services in the years to come. With the regulatory approval for interconnectivity between circuit switched tra� c and IP, there will be increase in call volumes for NLD/ILD. Also, the reduction of spectrum usage charges (SUC) rate this year will contribute positively to the � nancial health of the telcos and their ecosystem partners .

TELECOM SOFTWARE

Proli� c advancements in the � eld of telecom software are a result of increased subscriber base, frequent application downloads and customization of services. Models which were business oriented have shifted their focus on customers. This has in turn increased the demand for the CRM software, BI tools and customized OSS/BSS markets. The agenda to serve the customers is the best way possible and is gaining clarity at a faster rate. Personalization and customization have put pressures on improvement in the network e� ciency and resource optimization. Softwares like Service Ful� lment, Service Assurance and CRM can help telecom companies achieve these goals.

COMMUNICATION INFRASTRUCTURE

The communication infrastructure industry is set to grow as a result of the high market demand. The increasing subscriber base has encouraged the operators to adopt active and passive infrastructure sharing to reduce their CAPEX and OPEX. Also, with the increase in the number of antennas required for 4G, infrastructure providers are looking at newer implementations like streetlight antennas. Digital India, NOFN and Smart Cities will give impetus to various parameters like structured cabling, optical � bre layout and VSAT. The increase in data creation and consumption is going to lay a lot of emphasis on data centres, submarine cables and satellite antennas. Adoption of environment friendly energy resources will increase as a result of various government incentives .

TELECOM TECHNOLOGIES

Continuous innovations in the domains of network, devices and applications is driving telecom industry growth. Exhaustion of IPv4 addresses has caused service providers to move to more e� cient IPv6. Need for convergence , mobility and rich communication is driving the growth of IMS, 4G LTE, M2M and MPLS. Change of industry from hardware centric to software centric has led to the growth of Cloud Computing. MVNO, Telepresence, RCS-e and BYOD are growing trends in telecom due to the need for di� erentiation in a competitive market. Li� technology, a new parameter this year, is believed to be one of the disruptive technologies that can send large amount of information at very high data rates using light as medium. With exponential increase in the number of smart devices and need for higher data rates, these technologies will shape the future of the ICT industry.

CONSUMER ELECTRONICS

Consumer Electronics is a booming sector which witnesses an assorted range of products added to its list every year. With PC market now dominated by laptops and notebooks, tablet industry strives to grow as a result of convergence. Handset market trends has seen an inevitable shift from feature phones to smartphones. Gaming consoles are serving the niche segment whereas feature-rich smartphones grab casual gamers leading to further strain on sales of consoles. The television industry is now being dominated with OLED technology and ultra-high resolution TVs. The Consumer Electronics industry always has something new to o� er like Smart gadgets, telematics and IOT. With technological improvements, there is a paradigm shift in the adoption of smart devices that in turn will drive the future.

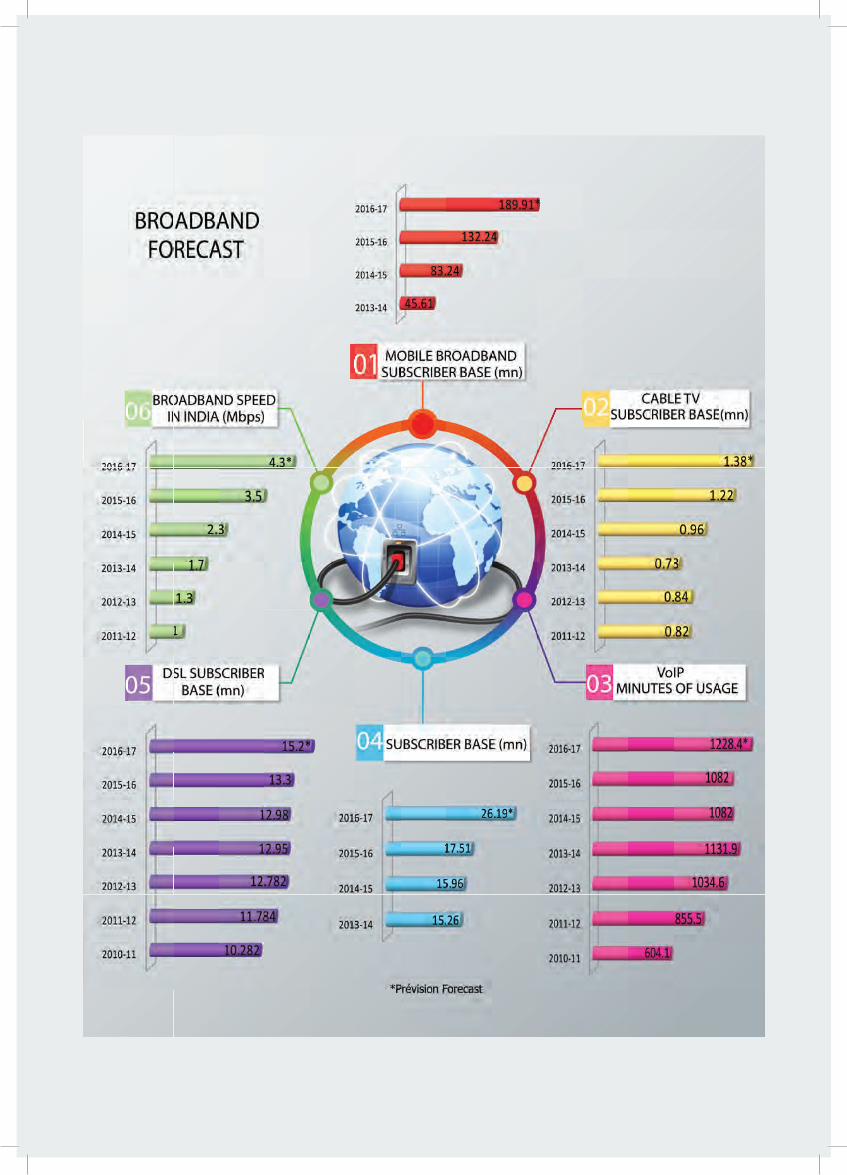

BROADBAND

India is witnessing a makeover in the digital world. A nationwide broadband network will improve the connectivity and access to public services like G2C communication, governance, health, education and entertainment. ADSL and 3G are the broadband technologies that are currently driving the internet market in India. By 2020, broadband in India is targeted to achieve a speed of 2Mbps with 100% coverage and at an a� ordable price. The standard technologies (DSL and cable modems) and the new technologies (VDSL and optical � ber) together are enabling telcos to retain their telephone and cable subscribers. India’s Bharat Broadband project aims to provide high-speed and high quality optical � bre connectivity to over 2.5 lakh

EXECUTIVE SUMMARY

8

village panchayats by 2017. An increase in the optical � ber penetration, shipment of low-cost smart wireless devices, subscribers’ engagement with mobile apps, usage of content-based services and adoption of social networking platforms are some of the factors leading to broadband penetration.

VAS AND MOBILITY

The increasing competition in the telecom industry has made value added services a key di� erentiator for the telcos. Rise in smartphone users and the ongoing rollout of 4G has helped the MVAS to proliferate quickly. Recently launched Pokémon Go is the best example of a rich and immersive M-gaming experience. Start-up India is also picking up pace and has an intention of promoting the spirit of entrepreneurship in India. Mobile connect, introduced by GSMA in 2014 is now gaining importance in India and lot of operators and security developers from around the world are being roped in to make Mobile connect very robust in its outlook. Thus, with the services like these , the VAS ecosystem is bound to expand in the future.

ECONOMY

In 2015-2016, many economies have faced challenges due to recent turmoil in several global markets such as stock market crash in China, Brexit, and reduction in oil Prices. Yet, India had done well during the year because of many current domestic initiatives by the government such as “Make in India”, “Smart Cities”, “Digital India” and macroeconomic stability ensured by regulatory initiatives of RBI. The GST bill is expected to improve the economic performance of the country. China’s GDP has slowed down due to the stock market crash thereby making Yuan weaker in the global economy.Japan’s GDP has also shrunk and is expected to continue the same in near future due to its National Gross Debt and ageing problem similar to that of Russia. Brexit has had a hard impact on the EU. The Geopolitical tension in Middle East, Greece has restrained global investments and con� dence, thereby building up the pressure on the current global economic growth.

GLOBAL TELECOM

Telecom industry continues to grow, but is approaching saturation in the conventional service o� erings. The telecom sector as a whole is shifting its focus towards utilizing trending and upcoming technologies in its service o� erings to the end user. 4G LTE and FTTX are the major trends as they have larger scope in immediate future in both developing and developed markets across the globe. Mobile broadband is seeing a strong growth especially in African countries. In 2015, Latin America witnessed more investments in network infrastructure as the operators are expecting increased customer demand for mobile data and FTTX services. India being one of the aggressive markets, is gearing up for 4G revolution. United States and European countries are moving towards saturation and have little room for immediate growth, whereas highly developed telecom markets like South Korea, Japan and Singapore have already started investing in future possibilities such as 5G, IoT and arti� cial intelligence.

SPECIAL FEATURE

The Smart Cities project intends provide core ICT infrastructure and o� er a decent quality of life to its citizens with a clean and sustainable environment and adoption of applications of ‘Smart’ Solutions. The project has an estimated investment of 113 bn USD over a period of 20 years. With the urban population contributing to 75% of the national GDP in India in the next 15 years, the project holds immense relevance. The government has allocated 100 smart cities across the states based on proportion of urban population and number of towns. The conceptualisation of Smart City, therefore, varies from city to city and state to state. It depends on the level of development, willingness to change and reform, resources and aspirations of the city residents. The cities shall be developed through public private partnership with private sector contributing to 80% of the total investments. Smart Grid, public utilities, security, health and education shall be the focal point of development.

..................................................................................................................................................................................................................................................................... PRÉVISIONSITM ANNUAL FORECAST 2017

9

METHODOLOGYPrévision - SITM Annual Telecom Forecast is in its 13th year, initiated in the year 2003, with the purpose of providing the industry a neutral and insightful single point of view regarding the emerging trends in the telecom sector for the forth coming year, after accumulating inputs from detailed research into contemporary telecom technologies, telecom business and other determinants of change.

STATISTICAL MODELS USED FORFORECASTING

Prévision is a culmination of the collective endeavour of SITM students with 1500 man hours of e� ort put in by them. The student forecast team is guided by the SITM faculty and some of our esteemed alumni. It is the only e� ort of its kind in the telecom domain at this level, which provides comprehensive coverage over various domains in the telecom sphere.

TIME SERIES ANALYSIS

A time series is a sequence of data points, measured typically at successive times, spaced at (often uniform)time intervals. Time series analysis comprises of methods that attempt to understand such time series.Time series forecasting is the use of a model to forecast future events based on known past events to forecast future data points.

EXPONENTIAL SMOOTHING

In statistics, exponential smoothing refers to a particular type of moving average technique applied to time series data, either to produce smoothed data for presentation or to make forecasts.

EXTRAPOLATION

This model statistically extrapolates established pattern and/or existing relationship in order to predict their continuation, assuming that such will not change during the forecasting phase.

LINEAR EXTRAPOLATION

Linear extrapolation means creating a tangent line at the end of the known data and extending it beyond that limit.

POLYNOMIAL EXTRAPOLATION

A polynomial curve can be created through the entire known data or just near the end. The resulting curve can then be extended beyond the end of the known data. The resulting polynomial may be used to extrapolate the data.

TREND ANALYSIS

When a series of measurements of a process is treated as a time series, trend estimation is the application of statistical techniques to make and justify statements about trends in the data.

REGRESSION ANALYSIS

Data regression analysis is a technique used for the modelling and analysis of numerical data consisting of values of a dependent variable (response variable) and of one or more independent variables (explanatory variables).

Linear Regression, y = a(x) + bNon-Linear Regression, log(y) = log (a) + x*log (b)

Student Research Projects

IndustryInputs

Industry Watch

Summer Internships

1900 Alumni Mentorship

METHODOLOGY

10

INDEX

INDIANTELECOM

TELECOM SOFTWARE

VAS AND MOBILITY

GLOBALTELECOM

CONSUMERELECTRONICS

TELECOM TECHNOLOGIES

BROADBAND

ECONOMY

COMMUNICATIONINFRASTRUCTURE

SPECIALFEATURE

PAG

E12

PAG

E40

PAG

E68

PAG

E54

PAG

E18

PAG

E48

PAG

E74

PAG

E62

PAG

E26 PAG

E32

11

SCOPE

The objective of this vertical is to provide insights on the current trends in the Indian Telecom industry. It forecasts various key parameters such as wireless and wire-line subscriber base, urban and rural teledensity, telecom revenue, ARPM, NLD and ILD revenue. It throws light on the business scenarios of 2G, 3G and LTE technologies. It also discusses the FDI in� ow in telecom, MNP status, data ARPU of operators and current telecom policies of the government. By using a new parameter coined as the Telecom Index, we try to convey the health of the telecom sector in India by analyzing the changes in AGR with the in� ation rate.

SUBSCRIBER BASE AND TELEDENSITY

Indian Telecom sector has witnessed a robust growth during FY 2015-16. The total subscriber base has reached 1058.86 mn, registering a growth of 6.26% whereas total teledensity has increased at the rate of 5.01% over FY ’14. This growth is accredited to the expansion of mobile networks and strong customer demand resulting from a� ordable tari� plans. Intense competition between operators has created a price war encouraging them to adopt innovative pricing strategies. Rural areas have a subscriber base of 449.17 mn with low teledensity as compared to urban teledensity. This gap is an opportunity for the TSPs to expand their footprint in rural areas. Operators have plans to invest huge amount on infrastructure along with special tari� plans and o� ers targeted at rural consumers. This will increase the subscriber base, bring in additional revenue for operators and enable telcos to provide better service to consumers.

In� uencing Factors

Investment on infrastructure by operators Liberal and progressive policies of government Huge potential for expansion in rural areas

Market Share

INDIAN TELECOM

Student TeamAnubha Pandit | Tanuj Gupta

*Trend Analysis ** Regression Analysis

ARPM (GSM): ₹0.48

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICS FY 2015-16

Wireless Subscriber Base:1058.86 mn

Expected to increase to 1117.25 mn **Expected to come down to 24.77 mn *

Fixed-line Subscriber Base: 25.22 mnTotal Teledensity: 83.36%Urban Teledensity: 154.01%Rural Teledensity: 51.37%Total Telecom Revenue: ₹2637.08 bn

Expected to increase to 96.58% **Expected to increase to 182.32% **

Expected to increase to ₹2690.57 bn *Expected to come down to ₹0.42 *

Expected to increase to 58.39% **

Idea 17.01%

Bharti24.22%

Vodafone19.16%Reliance

9.93%

Aircel8.44%

BSNL8.26%

Tata5.87%

Telenor5.03%

Sistema0.75%

Videocon0.66% MTNL

0.35%

12

MNP

Pan-India MNP became a reality last year. It facilitated mobile users with the convenience of changing their service provider within the state as well as while moving between states keeping the same mobile number.

According to TRAI, around 4.9 mn requests for MNP were received by the telecom operators in April 2016, showing 11.46% hike from 4.4 mn requests received in March 2016. TRAI had also received a number of complaints from subscribers regarding the rejection of MNP requests, reduction in the timeline for number return process, non-payment disconnection issues and ease of process during MNP. To curb such issues, TRAI imposed a penalty of ₹9.45 cr on operators for not complying with MNP rules.

MNP has been a success so far in India and has helped set up a level playing � eld by giving operators opportunities to increase customer base and revenue. Owing to MNP, the subscriber base of Vodafone, Airtel and Idea has increased, but Reliance Communications did not see much success. Moreover, Reliance Jio is also preparing to o� er MNP to get more subscribers hooked on its network.

In� uencing Factors

Large number of call drops Dissatisfaction in terms of QoS, Price and Customer service support Availability of inter-circle portability

NLD AND ILD

*Trend Analysis

The NLD and ILD render national and international transport links between several telecommunication service providers’ networks. NLD operators provide reliable and high quality call completion anywhere in India. Agreements between Basic Service Operators(BSO), Mobile Operators and Telecom PSUs in the country have assisted NLD-ILD providers. Currently, there are more than 40 NLD providers. NLD and ILD revenues are generated through roaming and long distance calls. Better 3G penetration, introduction of 4G network and a� ordable devices will have a positive impact on the NLD-ILD ecosystem.

NLD and ILD contribute 13.28% and 3.12% respectively to AGR. NLD contribution to AGR has declined by ₹579 cr Y-O-Y since December 2014 while the ILD contribution to AGR has increased by ₹18 cr. As per the NLD/ILD amendment of March 2016, interconnectivity between circuit switched tra� c and IP is allowed, which will add call volumes but the impact on the NLD/ILD revenues will be mixed.

OTT players like Skype are posing a great threat to International Carriers, making it essential for the International Carriers to induce VoIP and NGN in their networks. ILD providers are making an endeavor to get into enterprise business backed by cloud IT service delivery and SDN technologies.

In� uencing Factors

Reduction in license fee of NLD Getting into enterprise businesses Increase in tra� c of NLD/ILD due to regulatory approval for VoIP to PSTN/Mobile interconnect

2G

Smartphone users consume more data than voice, due to which data usage is expected to increase many folds from 1.4 GB/ month in 2015 to 7 GB/ month by 2021. Moreover, the demand for high-speed data is increasing amongst young smartphone users leading to a decrease in 2G subscribers as operators are encouraging 2G to 3G migration by o� ering call and internet services at similar prices. Operators like Airtel and Idea have dropped 3G data tari� plans by 67% so as to incentivise users to migrate to 3G networks.

In addition to Government’s “Make in India” initiative, many Chinese handset manufacturers are entering Indian market resulting in pocket-friendly yet feature-rich 3G enabled handsets. This will further drive users to shift from 2G to 3G network. Moreover, government’s spectrum liberalization policy will enable the shifting of the users from one network to another.

As on June 2015, there were approximately 300 mn wireless internet users, out of which 207 mn were 2G users consuming about 200 MB of data per month. Though a� ordable 3G data tari� plans are in� uencing users, unavailability of good 3G network coverage is resulting in 2G driving data growth in such tier-II and tier-III regions.

In� uencing Factors

100% FDI in telecom infrastructure Pocket-friendly yet feature-rich smartphones Spectrum liberalization

IND

IAN

TELECOM

CURRENT STATISTICSFY 2015-16

NLD revenue: ₹323.35 bn

Expected to come down ₹316.43 bn *Expected to increase to ₹179.35 bn *

PRÉVISION FORECASTFOR FY 2016-17

ILD revenue: ₹160.95 bn

..................................................................................................................................................................................................................................................................... PRÉVISIONSITM ANNUAL FORECAST 2017

13

MHz in combination with 2300MHz. There would be a signi� cant uptake of 4G LTE dongles and their number is expected to reach 230 mn by 2020, which would account for around 17% of the total subscribers. In the coming years, 4G adoption rate in India will be about 1.5% of the total wireless subscriber base deployment and growth of 4G is not going to be easy with challenges like insu� cient backhaul capacity, quality of service, security and chipset compatibility, but it will bring a massive revolution in the telecom market.

In� uencing Factors

Need for higher data rate Increasing a� ordability of devices and services Intense competition among telcos Liberalization of spectrum

DATA USAGE

Data users in FY 2015-16(mn)

With a rapid increase in the number of smartphones, the number of people accessing mobile internet has increased, thus increasing mobile data consumption. During FY 2015-16, the data usage (GSM & CDMA) per subscriber per month was 136.63 mb. The data usage for GSM was 122.93 mb while that of CDMA was 412.91 mb. Mobile data usage has more than doubled in the last three years. The huge jump in data consumption can be attributed to the proliferation of social media apps, gaming apps, and e-commerce applications. The young population of India contributes maximum to data usage by streaming music, videos, playing games, accessing maps and GPS for navigation, movie ticket booking, doing mobile recharges and much more. In India, there has been a growth of 85% in 3G data consumption in the last year and has reached 753 mb per month. In the coming years, due to 4G rollouts by telecom operators, data consumption will touch new heights and will give tough competition to 2G and 3G data services, largely due to low introductory tari� s. Still, there is a long way to go in India for a stage where data overtakes the voice which would only be possible with acceptance of data services by the sizeable semi-urban & rural population.

Growth in data consumption in tier-II & tier-III regions

3G

In 2010, the Indian telecom sector underwent a paradigm shift when the government auctioned 3G spectrum for ₹ 67,719 cr across all the 22 circles. 3G turned out to be a huge disappointment mainly due to lack of infrastructure as the operators were burdened with the huge cost of spectrum acquisition. Till Dec 2015, only 93 mn subscribers had active 3G connections. With the increase in the use of smartphones and popularity of online services, demand for high-speed data is increasing day by day. However, the demand for 3G might not increase to a great extent as a superior 4G technology is in the rollout phase. Also, the spectrum usage has been liberalized leading operators to o� er 4G, 3G, and 2G services on any band. Operators are not willing to invest much in 3G as consumer preference shifts to 4G. To add to 3G woes, few subscribers are unable to distinguish between 2G and 3G speed making it pointless to switch from low-cost 2G to relatively high-cost 3G.

Telecom operators are � nding it really hard to push 3G services and it is a challenge for them to decide whether “to invest” or “not to invest” in 3G infrastructure.

In� uencing Factors

Demand for high speed Tari� war between 3G and 4G services Increase in popularity of online services, social networking Availability of smartphones at low cost

4G/LTE

2016 is going to be the year of LTE in India with telecom operators like Airtel and Vodafone launching high-speed 4G services and manufacturers coming up with LTE enabled handsets. Also, Reliance Jio commenced its pan-India commercial operations from September 2016. As a part of promotions, Jio has off ered 4G SIMs with unlimited data for 3 months with its LYF smartphones. Currently, the tari� for 3G and 4G are similar given the price-sensitive nature of Indian market. Operators will resort to competitive pricing for their 4G packages. The average data usage per subscriber in India is expected to double by 2018 and the number of smartphones would cross 200 mn by then. On the 4G front, customers expect seam less connectivity and high QoS across the regions, putting pressure on LTE networks. Operators will have to provide high data rates over larger areas. This will be made possible through the use of low operating frequencies such as 800 and 1800

350

340

330

320

310

300

319.42324.95

342.65

331.66

Q1 Q2 Q4Q3

..................................................................................................................................................................................................................................................................... PRÉVISIONSITM ANNUAL FORECAST 2017

IND

IAN

TEL

ECO

M

14

the ARPU from calls showed a depletion of 9.17%, the ARPU from SMS showed a depletion of 12.97% and the ARPU from VAS services showed a depletion of 6.8% during the above period. This depicts data ARPU is cannibalizing the ARPUs of other services.

Technology advancement is also contributing towards greater data usage, which further enhances the ARPU generated from the data services. An average 3G subscriber consumes approximately four times more data than an average 2G data user. The consumption further goes up with 4G services.

In� uencing Factors

Growing demand of online videos Expansion of 3G & 4G services Optimized data tari� s Availability of a� ordable feature-rich smart phones

FDI IN TELECOM SECTOR

FDI in telecom in FY 2015-16

The Indian telecom market has registered a strong growth in the past decade and currently has the world’s second largest mobile subscriber base. It is likely to grow at 10.3% to reach US $103.9 bn by 2020 and contribute substantially to India’s GDP. The liberal and reformist telecom policies along with strong consumer demand have been instrumental in the rapid growth. The government has slowly raised the FDI permitted in telecom sector from 49% to 74% and � nally raised it to 100% in 2013. The deregulation of FDI norms has made the telecom sector one of the top � ve employment opportunity generator in the country. Over the last 20 years, operators have injected over ₹7.5 lakh cr in setting up the mobile networks. According to data released by Department of Industrial Policy and Promotion (DIPP), the telecom industry has attracted FDI worth US$ 18.38 bn from April 2000 to March 2016. In the last two years, from April 2014 to March 2016, the FDI in� ow has reached almost $4 bn, which is more than double the FDI generated in previous two years which stood at US$1.6 bn. Some recent investments being the ones made by Xiaomi, Axiata Digital, Sterlite Technologies and One Plus. India o� ers an excellent

In� uencing Factors

Aggressive 3G network expansion Increase in smartphone penetration Increased usage of mobile apps Streaming music and video on mobile A� ordable data tari� plans 4G rollout

TELECOM POLICIES

The government has provided opportunities for growth of telecom companies with its proactive and fast-tracked reforms throughout last year. The October 2016 auction will o� er 2,354.55MHz of spectrum at an estimated ₹5.66 trillion. These airwaves will enable operators in improving their QoS and address call drop issues. The government has liberalized the payment terms for spectrum auction by providing payment options i.e. upfront payment and payment in installments. TRAI has recommended alterations in the Uni� ed License so as to facilitate interconnection of IP with PSTN/Mobile amongst licensed operators. It has proposed a Public-Private Partnership model for BharatNet, which is the central government project for setting up of a broadband network in rural India. With a view to increasing consolidation, the government has approved the rules for spectrum trading, thus allowing telecom companies to buy and sell rights to unused spectrum among themselves. Also, spectrum sharing has been approved with an aim to improve spectral e� ciency and QoS. The government has also planned to provide free high-speed Wi-Fi in 2500 cities and towns over the next three years. Keeping in mind the operator friendly policies and introduction of 4G services, India is expected to emerge as a leading player in the telecom world.

DATA ARPU

* Trend Anaysis

Owing to rising popularity of online videos, apps, and other online services, the data services have become the leading revenue-generating segment for the telecom industry. This comes at the cost of depleting the revenue from traditional sources like voice, SMS, and VAS. High data rate from 3G & 4G services facilitates viewing of online videos & other services. Even in B & C circles, the demand for data services has gone up considerably. Data ARPU witnessed a gain of 25.37% from December 2014 to December 2015, whereas

10000

8000

6000

4000

2000

0

2517 Cr

4238 Cr

8637 Cr

6936 Cr

Q1 Q2 Q4Q3

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICSFY 2015-16

Data ARPU: ₹28.31

Expected to increase to ₹31.76 *

..................................................................................................................................................................................................................................................................... PRÉVISIONSITM ANNUAL FORECAST 2017

IND

IAN

TELECOM

15

opportunity to telecom operators, equipment vendors, and manufacturers to diversify their operations in rural India and capture the gains of the telecom boom which is bound to occur in the coming years.

In� uencing Factors

Network expansion in rural India Expanding Indian economy with increased focus on the services sector Government initiatives such as “Make in India”

TELECOM INDEX

* Trend Analysis

Telecom Index analyses the telecommunication industry. The index helps in predicting the impact, positive or negative, on the industry and additionally facilitates in analyzing the trends and current market scenario. So, future choices and predictions regarding the industry are created in a rational manner. Predominantly, the idea of the telecommunication index lies in AGR. The de� nition of AGR keeps on changing as per TRAI recommendations. It is the total of all incomes earned through pure telecom operations adjusted for few pass through items. Any upward or downward movement within the AGR will re� ect the positive or negative impact on the industry. Apart from AGR, the growth of industry can also be expressed by factors like subscriber base, teledensity, and ARPU. The increase in all these factors implies that the industry is growing. But these are not many reliable measures. The basic methodology of Telecom Index is predicated on the fact that AGR or the revenue attained by the operators has to be increasing at a rate over the in� ation rate for that year. If in any year, the rise within AGR is less than the rate of in� ation, then there would be no real growth of telecommunication industry. Telecom Index is a color coded index. Colors and their interpretation are as follows:

According to our Index, the Indian telecom industry is declining and lies within the Pink zone as AGR is declining, but not at a signi� cant pace.

PRÉVISION FORECAST FOR FY 2016-17

CURRENT STATISTICS FY 2015-16

Adjusted Gross Revenue:`187857

Expected to reach:`197222.97 *

In� uencing Factors for AGR

Ease in spectrum trading and sharing Increasing subscriber base Digital India and smart India initiative High density Growth in ARPU

CONCLUSION

The market is expected to grow at 10.3% Y-o-Y. The subscriber base is increasing at a faster pace after reaching 1-bn-mark last year. Growth is attributed to the strong consumer demand and liberal policies of the government. The need for higher data rates and the TRAI regulations on call drop issues have forced operators to enhance network capacity and coverage. Last year saw huge developments with respect to technology and innovation. With 10 smart cities being built in the � rst phase, telecom operators need to provide the requisite infrastructure, which means more revenues for OEMs. The entry of Chinese handsets manufacturers in India will also boost the high-speed data demand of the subscribers increasing data ARPU and hence resulting in higher revenues of the telecom operators. We might also see some mergers and acquisitions of the operators in this � eld as small players are � nding it di� cult to survive in tough competition resulting in number of operators being reduced to 5-6 eventually.

Green

Red

Pink

Yellow

Positive growth

Industry contracting

Urgent revival needed

Trade is reviving

YearVa

lues

in c

rore

(Rs.

)

220000.00

200000.00

180000.00

160000.00

140000.00

120000.00

100000.00

2009-102010-11

20011-122012-132013-142014-152015-162016-17

AGR - Adjusted Gross RevenueUTL - Upper Threshold LimitLTL - Lower Threshold Limit

..................................................................................................................................................................................................................................................................... PRÉVISIONSITM ANNUAL FORECAST 2017

IND

IAN

TEL

ECO

M

16

SCOPE

This vertical throws light on the dynamics of the global economy by analyzing the past and current economic indicators for select countries. Economics has its implications on each and every industry vertical. The impact of various macroeconomic factors like in� ation, � scal de� cit, unemployment, exchange rate, import, and exports is taken into consideration with speci� c emphasis on India. These factors are analyzed using statistical tools to forecast the key trends for the economies of several countries. Moreover, the impact of di� erent qualitative and quantitative variables is studied for forecasting trends for key indicators. This vertical presents a snapshot of the way di� erent economies work and the impact of various � uctuations on the economic ecosystem.

INDIA

India is one of the fastest growing nations in the world with a total population of 1.311 bn and with GDP of 2.074 tn. With the growth rate of 7.244% in 2015 as compared to 6.639% in 2014, it is expected to increase in the coming years due to various foreign investments

and pro-growth government policies.

India in 2015 made investments of around $26.3 bn with almost 930 deals around the world with the telecom sector contributing to about 40% of it. Government initiatives such as the one to build new railway lines to Nepal and big ticket investments by foreign multinational giants (General Motors, Hyundai, Foxconn, etc.) are said to boost the economy even further.

The in� ation rate in 2015 in India was 5.89% as compared to 6.53% in 2014. This variation was due to drought and uneven rainfall in India. Moreover, the government had increased VAT and taxes on imported goods and services which added to the in� ation rates in last few years, speci� cally during the previous � scal year. The � scal de� cit of India in 2015 was 4.13% of GDP as compared to 4.6 % in 2014. The reason for this could be an increase in subsidies, defense expenditure and interest payments.

Unemployment Rate in India during 2015 was 3.4 %. Various government initiatives like Make in India, Digital India, and Smart Cities are expected to generate more employment opportunities and also foster the growth of India’s economy.

In� uencing Factors

Government Initiatives (Make in India, Smart Cities, Digital India) Mergers and Acquisitions made by India Inc. Foreign Investments Low Crude Oil Prices

ECONOMY

Student TeamShivam | Rituraj Zala | Dhruvika Solanki

*Trend Analysis ** Regression Analysis

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICSFY 2015-16

GDP growth rate: 7.6% GDP growth rate: 8.0% **

IIP: 177.5 *IIP: 174.3

In� ation: 5.9%

PMI: 51.3:

In� ation: 4.45% *

PMI: 51.06 *

18

unemployment rate has increased from 8.7% in 2014 to 9.4% in 2015.

Greece’s bailout has heavily impacted EU’s � nances. EU has majorly been impacted by the exit of Britain. The announcement of referendum result sent shockwaves throughout the global economy leading to a dramatic drop in the value of Pound, which had already weakened ahead of the referendum.

Initially, the overall impact of Brexit seemed minor on the overall EU economy, but it remains a challenge for EU.

In� uencing Factors

Brexit Decline in growth in most of the member nations High unemployment rate

CHINA

China’s economy continues to grow moderately at 6.9% in 2015, one of the reasons being the shift of the Chinese economy from manufacturing industries to the service industries. The service sector of the country contributes 50% towards the economic growth of the country. People’s Bank of China surprised markets with devaluations of the Yuan, reducing over 3% of its value. The move was believed to be a desperate attempt by China to boost its exports to in an attempt to tide over the slowest growth rate in a quarter century. Britain’s unexpected decision to leave the European Union will cause a ripple e� ect in the global economy, a� ecting cross-border trade agreements, foreign direct investment strategies thus weakening of external demand for Chinese products.

Moreover, the in� ation rate has decreased to 1.4% as compared to the previous year when the government had targeted 3%. The major contributor towards in� ation rate is the hike in food prices. This price rise is likely to be temporary due to the proposed policy easing in near future.

Huge demand from the services and manufacturing sector has helped China in arresting the unemployment rate.

CAD

For the � scal year 2015-16, CAD remained at 1.1% of GDP i.e. $22.1 bn, as compared to 1.3% of GDP i.e. $26.8 bn in 2014-15. The reasons being reduction in the trade de� cit, which had narrowed to $130.1 bn last � scal from $144.9 bn in 2014-15 and moderation of overall Balance of Payment (BoP) during the � scal from $61.06 bn in 2014-15 to $17.9 bn. Initiatives like “Make in India” will provide a much, needed push to export which in turn will help in reducing CAD. Following Brexit, an anticipated slowdown in the global economy will lead to a decline in prices of commodities like crude. This too, will help India save a lot on its imports.

Although the private remittances received from abroad reduced, yet it stood at a substantial � gure of $15.8 bn. During the given period, exports too declined. FDI increased from $41 bn to $44bn in FY 2015-16.

In� uencing Factors

Reducing expenditure Make in India Trade relationship with countries Lower crude oil price Rise in the value of rupee

EUROPEAN UNION

The bird’s eye view of the EU economy shows that economic growth is moderate. However, the growth rate of individual EU members varied from positive to negative.

Greece is back in recession. Italy is barely growing. Portugal expanded but at half the expected rate. But some countries have also shown a positive growth rate. Germany showed a growth of 0.3% in fourth quarter of 2015 and 1.4% for the whole year. Exports are going to face a challenge in the international scenario in 2016, particularly with the Euro value appreciating in the foreign exchange market. Finland is back in recession with very little growth in the second half of 2015. The

*Trend Analysis

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICSFY 2015-16

CAD: $22.1 bn CAD: $18.39 bn*

*Trend Analysis

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICSFY 2015-16

GDP growth rate: 1.9% GDP growth rate: 2.02%*

In� ation: -0.1% In� ation: 0.27% *

*Trend Analysis

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICSFY 2015-16

GDP growth rate: 6.9% GDP growth rate: 6.62% *

In� ation: 1.4% In� ation: 1.27% *

..................................................................................................................................................................................................................................................................... PRÉVISIONSITM ANNUAL FORECAST 2017

ECON

OM

Y

19

In� uencing Factors

Ageing population Shift towards service sector Decreasing exports to developed nations

SOUTH AFRICA

*Trend Analysis

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICSFY 2015-16

GDP growth rate: 1.3% GDP growth rate: 1.11%*

In� ation: 4.6% In� ation: 3.89% *

South Africa, the second largest economy among the African nations, saw a GDP growth of 1.3 % in 2015 i.e. $312.798 bn as compared to about 1.5% i.e. $349.83 bn in 2014. In� ation was 4.6% in 2015 as compared to 6.4% in 2014. Monetary policy prioritizes in� ation control, both to encourage competitiveness in South African businesses and to protect individual purchasing power. A continuous struggle with the food price in� ation, which is at 9.8% in 2016, is proving to be one of the bottlenecks for SA. In 2015, the unemployment rate was 25.4% while in the � rst quarter of 2016 it has increased to 26.7%. In order to keep all these problems in check, the National Development Plan has aimed to reduce poverty and inequality by creating jobs and improving education by 2030. Following Brexit, the value of the Rand witnessed a huge plunge as SA has close � nancial and trade ties with U.K. To add to this, it had already su� ered a setback due the China’s devaluation of the currency with whom they had a trade and industry deal in the year 2015.

The government continues to remain committed to raising investment, improving labor relations and policy coordination, making it easier for doing business so that the South African economy is better placed to grow in future.

In� uencing Factors

High Food In� ation High Unemployment rate Poor Quality of Education Shrinking of Agriculture and Mining Industries

RUSSIA

*Trend Analysis

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICSFY 2015-16

GDP growth rate: -3.7% GDP growth rate: -0.62% *

In� ation: 15.5% In� ation: 7.69% *

The Russian economy has faced a steep decline of 3.7% in GDP since 2009. Oil and gas account for half of the revenue of Russia. After a fall in the oil prices, per barrel cost of oil hovered around $30. The Russian government had to make cuts in the budget for 2016 as it was � nalized on the assumption of oil price touching $50 per barrel. The economic recession has hit consumers hard. 2.3 mn Russians have been impoverished in � rst 9 months of 2015. In� ation has risen up to 15.5% in 2015. However, the situation got worse with sanctions against Russia by western nations. Demand shifted towards domestic products due to the weakening of the Rouble. Russia’s population is also ageing and unemployment remains at 5.7%.

Russia declared that it had been out of recession for more than 6 months in May 2015 though many Russians still continue to feel the ongoing economic crisis in the country, with real wages falling by 9.5% in 2015. UK’s departure from the EU may send shockwaves across the global economy, which is likely going to have repercussions in the Russian economy too, yet the impact will probably be limited.

In� uencing Factors

Low crude oil price Sanctions by US & Europe Geopolitical issues leading to political uncertainties Weak Rouble

SOUTH KOREA

South Korea, the 11th largest economy in the world contributes 1.898% ($1393 bn) of the world’s nominal GDP. In terms of PPP, its contribution stands at 1.63% amounting to $1849 bn. Over the past 5 years, South Korea has experienced a steady growth of 2.96% although it is lot lower than 6.6% it experienced in 2010. Its annual GDP growth rate stayed at 2.6% in 2015, down from 3.3% in 2014. South Korea’s exports are continuing to fall over past 17 months, the major reason being China’s rising share in global exports. Also, as labour costs in China are comparatively cheaper than South Korea, China continues to be the preferred destination for imports by the United States, Europe and most of the nations. 2012 onwards, Korea’s exports have fallen by $10.4 bn. It currently stands at $45.9 bn as compared with $56.3 bn in 2012. Major exports from Korea include

*Trend Analysis

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICSFY 2015-16

GDP growth rate: 2.6% GDP growth rate: 2.35% *

In� ation: 0.7% In� ation: 0.23% *

..................................................................................................................................................................................................................................................................... PRÉVISIONSITM ANNUAL FORECAST 2017

ECO

NO

MY

20

experience stagnancy till the questions about single market access are not answered.

In� uencing Factors

Brexit and its implication Decline in business investments Lower crude oil prices Higher cost of labor

JAPAN

Japan is the third largest economy in the world after US and China. GDP in the Jan-Mar quarter of 2016 has improved to 0.5% as compared to -0.4% in Oct-Dec quarter of 2015. Japan’s GDP in the Jan-Mar quarter of 2016 stood at 503.2 trillion Yen as compared to 500.2 trillion of Oct-Dec quarter of 2015.

Japan’s gross national debt is increasing year by year. In 2015 its debt to GDP ratio was 229.2 % and in 2016 (end of March it was ¥1,049.37 trillion) it is estimated at about 232.4%, which is twice as that of U.S and is highest in OECD. Amongst the working age population, 60.5% are above the age of 45 years. Ageing population is acting as a hindrance to the growth of the country. However, unemployment rate reduced to 3.2% in Jan-Mar quarter of 2016 and is the least since 21 years, which is a good sign for the near future.

Exports and imports were $468 bn and $471 bn respectively, which estimate to -25% and -54% Y-O-Y percentage change. Even devaluation of Yuan has a� ected the export earnings. The in� ation rate in 2015 was 0.8 % as compared to last year in� ation rate of 2.7 %. Japan’s infl ation rate is declining at a constant rate despite various e� orts taken by the government to keep in� ation high as de� ation has been a long standing issue in the Japanese economy.

In� uencing Factors

Ageing population Rising National Gross Debt Reduction in export of goods Low In� ation

IC chips (14%), cars (7%), petroleum products (8%) and ships (4%) as per 2014 data. The � scal de� cit of South Korea is a mere -0.2% of GDP. In 2015, South Korea’s exports were $674.7 bn and its imports were $564.25 bn, which is a surplus of $110.45 bn.

Weak external demand, tightening � scal policies and weak productivity in services, act as reasons for low GDP. Through its three-year Economic Innovation plan launched in 2014, the government is trying to address the problem of low productivity growth.

In� uencing Factors

Declining Exports Wage in� ation due to aging population Tighter � scal and monetary policy

UK

UK was the � rst largest economy in the world that was surrounded by the looming clouds of Brexit. Though Brexit as of now has not had any profound e� ect on the UK economy, growth may continue to be slow until 2017.

The sectors impacted most will be automobile and steel industries. Once the process of Brexit completes, car manufacturers in the UK would have to apply for separate certi� cation so as to sell their units in EU member countries. Brexit will also impact seamless trade of goods across Europe, a major chunk of which shall be steel.

The unemployment rate may reduce as Britain may impose stricter immigration control policies, making it tougher for immigrants to work in UK. This will also increase labor cost since local workers will be hired as cheaper immigrant skilled workers will not be available in large numbers. This could greatly a� ect manufacturing and agriculture.

Exports may reduce as UK would have to negotiate/re-negotiate terms and treaties with the single market or it could negotiate trade agreements with individual countries. Consequently, if the UK does not have access to the single market, exports and trade, in general, will have signi� cant impact on its economy. But till 2017, trade will not grow but will remain stable. FDI shall

*Trend Analysis

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICSFY 2015-16

GDP growth rate: 2.25% GDP growth rate: 1.96% *

In� ation: 0.3% In� ation: 0.74% *

*Trend Analysis

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICSFY 2015-16

GDP growth rate: 0.5% GDP growth rate: 0.96% *

In� ation: 0.8% In� ation: 0.47% *

..................................................................................................................................................................................................................................................................... PRÉVISIONSITM ANNUAL FORECAST 2017

ECON

OM

Y

21

Current standings indicate Brazil as the 9th largest economy in the world. Its GDP amounts to $1.77 trillion (US). It also continues to be the largest among the South American economies. As of 2015 Brazil contributed 2.812% to the world’s GDP with respect to Purchasing Power Parity (PPP). The backbone of the Brazilian economy is ever-growing service sector, contributing 72% of total GDP. The service sector was followed by industry and agriculture, which contributed ~22% and ~5% towards GDP respectively.

Brazil’s GDP has been on a continuous nose dive since 2010 with minor signs of revival, shortly before Dilma Rousse� s took over. The main reasons for this are ine� cient policy formulation & implementation, political scandals and instability. The GDP fell by 2.8% in 2015. Though investments are � owing into the country due to Rio Olympics, if number of tourists does not match up to the expectation, the fall in GDP will be even deeper.

The devaluation of Chinese Yuan is also hurting the Brazilian economy. Brazil has invested $38 bn in Rio Olympics, but will such investments pay dividends still remains a big question. If not, then GDP will fall further adding to the � scal de� cit. Brazil is unable to attract much foreign investment in the country due to prevailing recessional conditions. Due to an interim government change and implementation of policies, in� ation has eased from 9.3% to 8.8%, however, it is far away from central bank’s acceptable � gure of 4.5%.

In� uencing Factors

Rio Olympics Unstable political system and corruption Weakening Real (R$)

CRUDE OIL

India depends on its crude oil import (nearly about 80% of its crude oil requirement is met by import) and it has imported nearly 202.1 mn tonnes in 2015-2016 as compared to 189.4 mn tonnes of crude oil in previous year i.e. 2014-2015. Per barrel cost of crude oil in India in the year 2015-2016 was $46.17 as compared to $84.16 per barrel in 2014-2015. There are many factors that contribute to it. Some of them are as follows:

1) Increase in production: There are many countries which entered or doubled their output in last few years.

USA

USA continues to be the most powerful economy in the world. As per 2015 World Bank � gures, it held a prime position in terms of nominal GDP, which was a staggering $17,947 bn. In terms of purchasing power parity, it stood 2nd at $17,419 bn just behind China’s $18,031 bn. USA contributed ~25% to the nominal GDP of the world. The average economic growth rate for the past 5 years has been around 2.1 %.

In 2015 the unemployment rate in the US was 5.29% and, if the Republican Presidential candidate Donald Trump wins, US may see an early sharp fall due to stricter policies regarding working immigrants.

USA continues to be one of the major producers of petroleum and natural gas. USA is the third largest oil producer in the world accounting for 12% of the total world produce. USA has almost become self-su� cient in terms of oil production. Hence it has to import less due to which domestic oil prices are low. Thus the supply is more than demand resulting in low oil prices.Due to the Brexit, US may see a fall in trade temporarily. Although till the formal Brexit in 2017, trade � gures are expected to remain more or less the same with the UK. Similarly, China’s surprising move to devalue Yuan could hurt USA’s export to China and may also increase prices of some consumer goods manufactured in China.

In� uencing Factors

Presidential elections and the associated policy uncertainty Low Oil prices Brexit Strong US dollar Low-interest rates

BRAZIL

*Trend Analysis

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICSFY 2015-16

GDP growth rate: 2.6% GDP growth rate: 2.72% *

In� ation: 1% In� ation: 1% *

*Trend Analysis

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICSFY 2015-16

GDP growth rate: -3.8% GDP growth rate: -4.58% *

In� ation: 8% In� ation: 8.23% *

*Trend Analysis

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICSFY 2015-16

Price per barrel: $46.17 Price per barrel: $41.99*

..................................................................................................................................................................................................................................................................... PRÉVISIONSITM ANNUAL FORECAST 2017

ECO

NO

MY

22

In� uencing Factors

Global oil prices Fed interest rate US Presidential Election

INR v/s YUAN

India and China are two of the biggest economies (seventh and second respectively) in the world, the former is an ITES & outsourcing hub while latter is manufacturing base for the world and hence, � uctuation in their currency matters to the world. In past few years, there have been constant ups and downs in the two currencies. In 2014, INR (Indian Rupee) per 1 CNY (Chinese Yuan Renminbi) was 9.855 and it increased to 10.25 in 2015, but there was a slight dip in the currency in last quarter of 2015 as it went down from 10.34 in the third quarter to 10.195 INR per 1 CNY.

There are few reasons that were responsible for the price � uctuation in the currencies. First is devaluation in the Yuan in the middle of the third quarter due to which INR per 1 CNY came down to 10.195 from 10.34. Second is Chinese market being hit by Britain’s exit from EU and as it represents one of China’s important markets and its � nancial base outside Asia.

The dip in the INR v/s CNY could be temporary as India’s dependency on Chinese products especially in the Automobile industry, Pharmaceuticals, Metal and Metal-based Products is more. Additionally, the import and export growth rate between the countries has an important contribution to this. In Pharmaceuticals Industry, about 80% need is ful� lled by Chinese import and India has nearly spent about $2.22 bn in drugs import from China. The above conditions hint at further � uctuations between the two currencies.

In� uencing Factors

Devaluation in Chinese currency Brexit High imports from China to India

CONCLUSION

Growth continues to lose momentum in developed economies, while there is a notable disparity in performance across developing nations and emerging markets. OPEC nations have been hit hard due to fall

U.S has increased its production to almost double in last several years. Also, Saudi Arabia, Algeria, and Nigeria are competing in Asian Market which has also a� ected the crude oil price.

2) Iran’s and Saudi Arabia’s role: Iran and Saudi Arabia hold the major imported share of the crude oil. Saudi Arabia and Iran contribute around 940,000 and 930,000 barrels per day crude oil respectively, which estimates around half of the total crude oil import.

Besides these, China’s devaluation of its currency and Iran-U.S nuclear deal has also made an impact on the reduction of crude oil prices all over the world. Moreover, automotive companies are making fuel e� cient vehicles which are further reducing the demand of crude oil.

In� uencing Factors

Increase in crude oil Production in world Geopolitical and economic events in oil producing regions China’s devaluation and Iran-U.S Nuclear deal impact

RUPEE v/s DOLLAR

Rupee performed quite well in 2015, withstanding the US Fed hike, Yuan devaluation, RBI rate cuts and declining crude oil prices.

The interest rate hike in the US, however just 25 bps, denoted a vital movement in Fed approach which has held interest rates consistent since June 2006. This may have strengthened US dollar, and provided a push to exports, while conceivably restricting the growth of imported products.

Subsequent to the beginning of 2015, the Indian Rupee had fallen by around 1.6% till mid- June, which made it one of the top performers in the list of emerging currencies for the year 2015.

Fate of rupee will largely be dependent on outcomes of US Presidential elections, the anticipated US’s narrow money policy which will tighten the liquidity and � ow of dollars in the global market. This will have a direct e� ect on exports and imports, leading to narrowing of current account de� cit and thus, future exchange rates.

*Trend Analysis

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICSFY 2015-16

$1 = ` 65.46 $1 = ` 67.31*

*Trend Analysis

PRÉVISION FORECASTFOR FY 2016-17

CURRENT STATISTICSFY 2015-16

1 CNY = ₹10.2 1 CNY = ₹10.91*

..................................................................................................................................................................................................................................................................... PRÉVISIONSITM ANNUAL FORECAST 2017

ECON

OM

Y

23

of oil prices. Due to a lot of policies and uncertainties in developed economies, investment and growth continue to be on a slow pace. In China, industrial activity is slowing because of strong growth in the service industry. Russia and Brazil are still under the in� uence of recession. Growth in South Asia remains moderately high, led by India. Domestic demand will continue to be the key driver of growth in South Asia.

Britain’s referendum for exiting EU has sent shockwaves throughout the global economy. US saw slowing exports because of a strong dollar and weak demand from emerging markets, though low oil prices have helped US in cutting down its expenditure. All these reasons are evident to prove that the global economy will grow with the same sluggish growth as last year.

..................................................................................................................................................................................................................................................................... PRÉVISIONSITM ANNUAL FORECAST 2017

ECO

NO

MY

24

SCOPEGlobal Telecom vertical provides an insight on the latest happenings in the telecom domain across USA, South America, Southeast Asia, Africa, Middle East, Europe and Australia. Using facts and � gures, it provides a clear picture of upcoming developments and technologies on the Global Telecom arena. Spectrum auctions, 4G, 5G, FTTX and factors impacting the various telecom parameters globally have been put forward in this vertical.

KENYA

Kenya’s telecommunications market is undergoing some signi� cant changes. The rapid growth of mobile market can be seen with a rise in the number of wireless subscribers from 33,632,631 in 2014 to 37,715,944 in 2015. At the same time, the number of � xed line subscribers has gone to 85,496 in 2015 from 179,990 in 2014 showing a decrease of 52.5%. However, the teledensity is growing at a steady pace, rising from 73.84 in 2014 to 80.68 in 2015. The continued growth in mobile subscriptions indicates that there is still an opportunity for growth in the mobile telephony services.

The main reason behind this increase is the launch of LTE-Advanced network in Kenya. It o� ers speeds of up to 100 mbps, which is more than twice the speed o� ered by 3G technology, thereby boosting network capacity, data rate and performance. The existing operators are also rolling out 4G technology with the support of government’s revised open-access approach to license LTE network. With the laying out of four � ber-optic cable networks in recent years, several � ber infrastructure sharing agreements have happened which in turn have

resulted in an improved international connectivity.

Moreover, the Communication Authority of Kenya (CAK) has reduced the interconnection tari� s and implemented a new simpli� ed and converged licensing regime. It has lowered the barriers to market entry and increased competition by allowing operators to o� er any kind of service in a service & technological neutral regulatory framework.

NIGERIA

Nigerian telecom market is the largest and fastest growing market in Africa. Due to liberalization, the companies can now provide more and better services in an independently regulated market. There are 150 mn subscribers and as the number increases, service penetration is also likely to increase in urban, semi-urban and rural areas. The number of wireless subscribers in the country reached to 150.83 mn by end of 2015, witnessing a signi� cant growth of 8%. In 2015, the teledensity of the region saw an increase of 5%, reaching to a � nal count of 82.18.

Nigeria also houses one of the largest set of internet users with 28% users in Africa region. 3G, 4G and WiMAX wireless broadband services have been aggressively rolled out augmented by new national and international � ber links. The broadband internet penetration has deepened due to auctioning of the 2.6 GHz spectrum by the Nigerian Communication Commission (NCC) to MTN Nigeria Communications Limited.

Economic development in Nigeria is directly dependent on huge demand for data services and broadband deployment, giving a GDP per capita of $2640.3. The

GLOBAL TELECOM

Student TeamNareshkumar Hegde | Jimit Raval | Faraaz Ahmed Gausee | Nikhilesh Harde

26

percentage of contribution by Telecom industry to the GDP in the year 2015 was 8.5%. The regulator has approved infrastructure sharing and outsourcing the management of towers to third parties, this will help improve the � nancial performance of the telcos.

THE MIDDLE EAST

UAE

Global FTTH ranked UAE 2nd position with more than 74% household FTTH penetration. UAE has shown an upward trend in 2015 with a 6.5% YOY growth in the wireless subscriber base up from 16.81 mn in 2014 to 17.94 mn in 2015, while the broadband subscriber � gures have seen a rise of approx. 12.4% YOY (from 1.09 mn in 2014 to 1.22 mn in 2015). Telecom operators have seen rise in the customer base as well as sales but the ARPU remained low as compared to the previous year. With 68% active social media accounts in early 2016 from 41% active social media accounts in 2014, social media penetration has greatly increased.