Vol. XLVI December 2020 / January 2021 Stop And Start

77

GOLD NEWSLETTER 1 Stop And Start Gold’s recovery has been a bumpy one as it struggles to put its recent correction lows behind it. While the bottom appears to be in, the near term seems as cloudy as the long term appears clear. By Brien Lundin T his month’s lead article was going to write itself — until gold was dumped on Wednesday morning. That the metal’s correction had ended and a new rally begun seemed obvious up until then. A sharp decline on November 24 th to a key support level (a 50% retracement of gold’s gains since March) coincided with the full moon and the De- cember options expiration to mark a clear bottom. (I know, throwing the full moon into this seri- ous analysis is sheer lunacy, but analysts across the Twitterverse were noting the coincidence, and not all of their remarks were tongue-in-cheek.) Regardless, gold rallied strongly from that point, rising in four out of five sessions from the November 24 th low at $1,776 on a spot basis to a high on Tuesday of $1,870. It seemed that the planets (and moons) were finally aligned in gold’s favor and the dark days of the correction were finally behind us. And then came the aforementioned sell-off on Wednesday, with gold slipping about $40, back to the low $1,830s. It tried to rally on Thursday, hitting $1,850 at one point, before fading back into the red de- spite supporting data on jobless claims and the CPI. On Friday, gold gained about $5.00 early on as it fought to regain an uptrend. Does this mean that the rebound was nothing more than a head fake? Obviously, it’s impossible to tell at this point. It is worthy of note that I was expecting a typical pattern in which the price would bottom in mid-Decem- ber. While not unheard of, this bottom would be on the early end of the spectrum. What’s interesting about this set back in gold is that all of the media and pundit reports are blaming it on a re- Gold (London PM Fix) $1,750 $1,775 $1,800 $1,825 $1,850 $1,875 $1,900 $1,925 $1,950 $1,975 Sep 8, 2020 Sep 15, 2020 Sep 22, 2020 Sep 29, 2020 Oct 6, 2020 Oct 13, 2020 Oct 20, 2020 Oct 27, 2020 Nov 3, 2020 Nov 10, 2020 Nov 17, 2020 Nov 24, 2020 Dec 1, 2020 Dec 8, 2020 ©2020 Gold Newsletter (Chart provided by Thechartstore.com) Mining Share Update New Orleans 2019 Highlights Potpourri INSIDE: 5 25 75 Vol. XLVI December 2020 / January 2021 DECEMBER 2020 / JANUARY 2021

Transcript of Vol. XLVI December 2020 / January 2021 Stop And Start

GOLD NEWSLETTER1

Stop And Start Gold’s recovery has been a bumpy one as it struggles

to put its recent correction lows behind it.

While the bottom appears to be in, the near term seems as cloudy as the long term appears clear.

By Brien Lundin

This month’s lead article was going to write itself — until gold was dumped on Wednesday morning.

That the metal’s correction had ended and a new rally begun seemed obvious up until then. A sharp decline on November 24th to a key support level (a 50% retracement of gold’s gains since March) coincided with the full moon and the De-cember options expiration to mark a clear bottom.

(I know, throwing the full moon into this seri-ous analysis is sheer lunacy, but analysts across the Twitterverse were noting the coincidence, and not all of their remarks were tongue-in-cheek.)

Regardless, gold rallied strongly from that point, rising in four out of five sessions from the November 24th low at $1,776 on a spot basis to a high on Tuesday of $1,870. It seemed that the planets (and moons) were finally aligned in gold’s favor and the dark days of the correction were finally behind us.

And then came the aforementioned sell-off on Wednesday, with gold slipping about $40, back to the low $1,830s. It tried to rally on Thursday, hitting $1,850 at one point, before fading back into the red de-spite supporting data on jobless claims and the CPI. On Friday, gold gained about $5.00 early on as it fought to regain an uptrend.

Does this mean that the rebound was nothing more than a head fake? Obviously, it’s impossible to tell at this point. It is worthy of note that I was expecting a typical pattern in which the price would bottom in mid-Decem-ber. While not unheard of, this bottom would be on the early end of the spectrum.

What’s interesting about this set back in gold is that all of the media and pundit reports are blaming it on a re-

Gold (London PM Fix)

$1,750

$1,775

$1,800

$1,825

$1,850

$1,875

$1,900

$1,925

$1,950

$1,975

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

Mining Share Update New Orleans 2019 Highlights

Potpourri

INSIDE:

5 25 75

Vol. XLVI December 2020 / January 2021

DECEMBER 2020 / JANUARY 2021

turn to “risk on” investing, as positive vaccine news is driving world equity markets to record highs on the day.

I guess they didn’t notice that all of the major U.S. stock indices were actually in the red as gold was falling. So the easy “risk on” excuse doesn’t hold water.

Given that option expiries are behind us, ma-nipulation by the usual suspects doesn’t seem likely in this case. But considering that stocks and gold had been on a tear over the previous week or so makes a simple corrective move seem a likely excuse for the drop. A slight re-bound in the Dollar Index accompanied by a tick-up in Treasury yields also support that view.

Major Macro While the near term remains muddy, the

long-term view is as clear as ever.

That macro view has always been based on the ever-easier monetary policies being pursued by the Fed and other central banks since the 2008 financial crisis. It has been bolstered, and in fact made in-evitable, but the monstrously large debts that such policies have encouraged, such that these debts now require negative real interest rates and very significant depreciation of the underlying currencies.

The only alternative would be a debt jubilee/financial system reset.

Either path would eventually result in gold and silver prices at multiples of current levels. And min-ing stocks would leverage those gains.

As long as we keep our focus on the horizon, these short-term fluctuations will fade in importance.

I know that’s little consola-tion as we navigate these daily twists and turns in the metals markets, so let’s look at some evidence that the metals are, indeed, setting up for a signifi-cant rebound.

Technically Speaking...

I’ve got some interesting charts to share with you this issue (courtesy, as always, of Ron Griess at TheChartStore.com), as we

GOLD NEWSLETTER2 DECEMBER 2020 / JANUARY 2021

Gold Bugs Index

270

280

290

300

310

320

330

340

350

360

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

U.S. Dollar Index (DX)(Daily with 50 day Moving Average (MA) and Bollinger Bands)

105.00105.00

87.0087.00

91.18

95.56

100.15

91.18

95.56

100.15

DX has broken down and is following the lower Bollinger Band down.

95.00 - 96.00

93.20 - 93.80

%B

-50-25

0255075

100125150

12/3

0/1

6

3/1

/17

4/2

7/1

7

6/2

3/1

7

8/2

1/1

7

10/1

7/1

7

12/1

3/1

7

2/1

2/1

8

4/1

1/1

8

6/7

/18

8/3

/18

10/1

/18

11/2

7/1

8

1/2

5/1

9

3/2

5/1

9

5/2

1/1

9

7/1

8/1

9

9/1

3/1

9

11/8

/19

1/8

/20

3/6

/20

5/4

/20

6/3

0/2

0

8/2

6/2

0

10/2

2/2

0

12/1

8/2

0

Copyright © 2020 Thechartstore.com

-50-250255075100125150

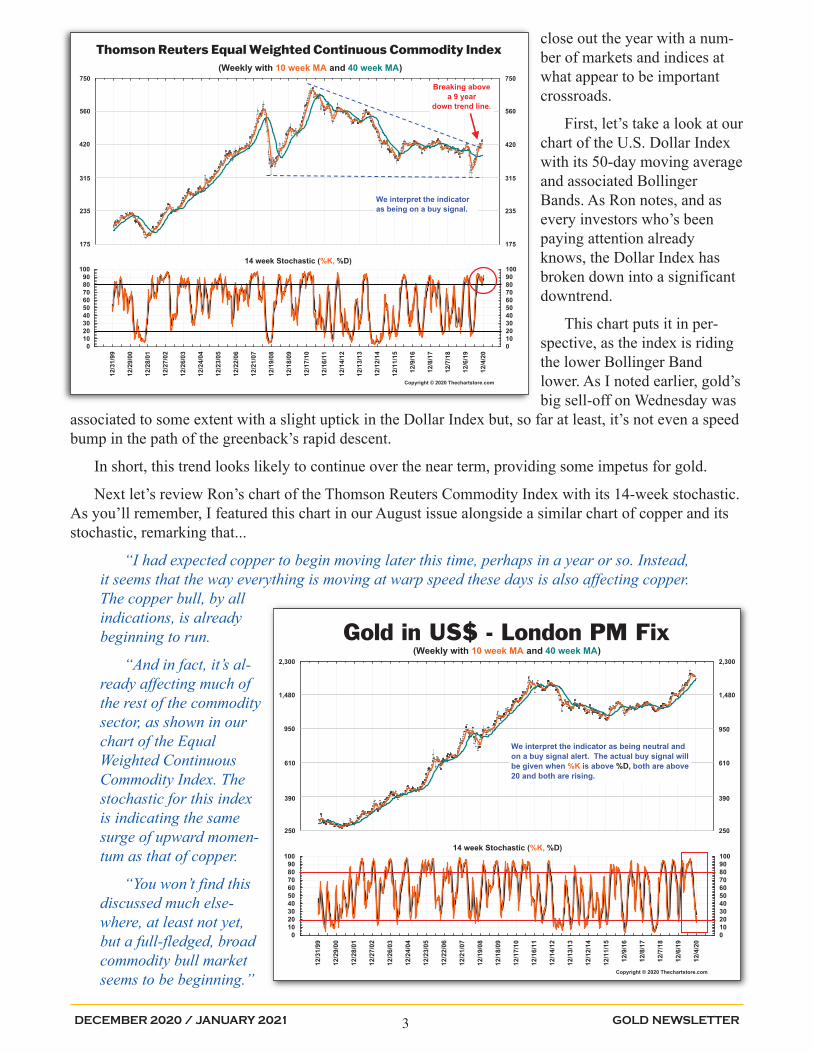

close out the year with a num-ber of markets and indices at what appear to be important crossroads.

First, let’s take a look at our chart of the U.S. Dollar Index with its 50-day moving average and associated Bollinger Bands. As Ron notes, and as every investors who’s been paying attention already knows, the Dollar Index has broken down into a significant downtrend.

This chart puts it in per-spective, as the index is riding the lower Bollinger Band lower. As I noted earlier, gold’s big sell-off on Wednesday was

associated to some extent with a slight uptick in the Dollar Index but, so far at least, it’s not even a speed bump in the path of the greenback’s rapid descent.

In short, this trend looks likely to continue over the near term, providing some impetus for gold.

Next let’s review Ron’s chart of the Thomson Reuters Commodity Index with its 14-week stochastic. As you’ll remember, I featured this chart in our August issue alongside a similar chart of copper and its stochastic, remarking that...

“I had expected copper to begin moving later this time, perhaps in a year or so. Instead, it seems that the way everything is moving at warp speed these days is also affecting copper. The copper bull, by all indications, is already beginning to run.

“And in fact, it’s al-ready affecting much of the rest of the commodity sector, as shown in our chart of the Equal Weighted Continuous Commodity Index. The stochastic for this index is indicating the same surge of upward momen-tum as that of copper.

“You won’t find this discussed much else-where, at least not yet, but a full-fledged, broad commodity bull market seems to be beginning.”

GOLD NEWSLETTER3 DECEMBER 2020 / JANUARY 2021

Thomson Reuters Equal Weighted Continuous Commodity Index(Weekly with 10 week MA and 40 week MA)

750 750

175175

235

315

420

560

235

315

420

560

We interpret the indicator as being on a buy signal.

Breaking above a 9 year

down trend line.

14 week Stochastic (%K, %D)

0102030405060708090

100

12/3

1/99

12/2

9/00

12/2

8/01

12/2

7/02

12/2

6/03

12/2

4/04

12/2

3/05

12/2

2/06

12/2

1/07

12/1

9/08

12/1

8/09

12/1

7/10

12/1

6/11

12/1

4/12

12/1

3/13

12/1

2/14

12/1

1/15

12/9

/16

12/8

/17

12/7

/18

12/6

/19

12/4

/20

Copyright © 2020 Thechartstore.com

0102030405060708090100

Gold in US$ - London PM Fix(Weekly with 10 week MA and 40 week MA)

2,300 2,300

250250

390

610

950

1,480

390

610

950

1,480

We interpret the indicator as being neutral and on a buy signal alert. The actual buy signal will be given when %K is above %D, both are above 20 and both are rising.

14 week Stochastic (%K, %D)

0102030405060708090

100

12/3

1/99

12/2

9/00

12/2

8/01

12/2

7/02

12/2

6/03

12/2

4/04

12/2

3/05

12/2

2/06

12/2

1/07

12/1

9/08

12/1

8/09

12/1

7/10

12/1

6/11

12/1

4/12

12/1

3/13

12/1

2/14

12/1

1/15

12/9

/16

12/8

/17

12/7

/18

12/6

/19

12/4

/20

Copyright © 2020 Thechartstore.com

0102030405060708090100

Of course, everyone is now talking about the copper bull market that we alerted you to back in August.

But what most investors and analysts are missing is what is still being shown in this chart of the Commodity Index and its stochastic. As you can see, after soaring above the 80 level, the sto-chastic has remained ele-vated above it, indicating continued upward momen-tum.

Moreover, as Ron notes in the upper panel, the index has decisively broken through a nine-year down-trend.

The broader commodity complex seems to be foreshadowing a global recovery from the pandemic, likely accompanied by rising inflationary pressures. (Ron would chastise me for throwing in the funda-mental underpinnings and urge me to simply watch what the technicals are saying, but I couldn’t resist.)

For us, an important question remains: Will gold participate in this broad commodity bull market?

Here the evidence is potentially even more compelling. Consider our chart of gold with its 14-week stochastic. As you can see, the stochastic is approaching an area that has typically marked a bottom in downward momentum in past corrections. Importantly, note that the stochastic rarely dawdles long at these lows, and typically makes a quick, sharp rebound.

This is supportive of the view that the recent correction is, if not already behind us, then will be very soon.

Our last chart, of gold with its Bollinger Bands, is an important one that Ron recently created and which I’ve been featuring. As you can see, Ron has noticed three very similar “consolidation/basing” areas, marked here by rectangles. In the two previous instances of these basing areas, gold subsequently embarked on major rallies.

Broadly speaking, a similar consolidation this time would allow for gold to retest or violate recent lows and still set up for a consequential rally.

Taken all together, the technicals seem to support the view that the market either bottomed on No-vember 24, or that it will do so before the end of this month.

Bargain Hunting Season

That all adds up, of course, to a continuance of the buying season for junior mining stocks. Except that, in this case, we also see the intermediate and major producers also sitting on the bargain rack.

GOLD NEWSLETTER4 DECEMBER 2020 / JANUARY 2021

Gold (London PM Fix)(Daily with 50 day Moving Average (MA) and Bollinger Bands)

2,4352,435

1,0001,000

1,250

1,560

1,950

1,250

1,560

1,950

The three consolidation/basing areas marked look similar in form. We have been using the 1,735 to 1,750 zone on this chart since the August 28 Blog. Mission accomplished and time for Gold to resume its move to the upside.

Longer-term Support

1,735 - 1,750

%B

-50-25

0255075

100125150

12/3

0/16

2/27

/17

4/26

/17

6/23

/17

8/18

/17

10/1

6/17

12/1

1/17

2/8/

18

4/9/

18

6/6/

18

8/1/

18

9/27

/18

11/2

2/18

1/22

/19

3/19

/19

5/17

/19

7/15

/19

9/10

/19

11/5

/19

1/3/

20

2/28

/20

4/28

/20

6/25

/20

8/20

/20

10/1

6/20

12/1

1/20

Copyright © 2020 Thechartstore.com

-50-250255075100125150

OVERSOLD

As you’ll see in the charts featured in our following portfolio review, a number of companies have already begun to rebound, while many others have not. Some have bounced due to exploration news, while others are still awaiting results from backed-up labs.

It’s a mixed bag, and we’ve done our best to sort out the buys and holds for you in this month’s cov-erage.

You’ll also notice that this is our annual expanded, year-end issue, covering both December and Jan-uary. As always, this issue features important excerpts — lots of them — from our recently concluded 2020 New Orleans Investment Conference.

The realities of the digital age provide us with the luxury of producing such a monumental issue. If this were still the age of physical newsletters, we of course couldn’t afford to print and mail such a large publication to you. If we somehow managed the feat, it would probably have to be delivered via UPS with the rest of your holiday packages.

Because this year’s event was forced to “go virtual” thanks to the pandemic, I was able to invite even more speakers than usual. The result is that our excerpts, just barely scratching the surface as they do, have led to this year’s year-end edition breaking all our previous records, yet again.

I hope you find time to peruse this immensely valuable information over the holidays. And as you do, please remember that it represents just a small fraction of what was available via the entire 2020 New Orleans Conference.

If you attended this remarkable event, you have access to every video recording and our entire tran-script (which will be delivered to you shortly). You also have access to our continuing content, including our recent special panel event on lithium and our private Zoom calls with leading experts.

If you’re not a member of the New Orleans Conference, you’re missing out on all of this valuable in-telligence and much more to come. To rectify that situation, you can join by CLICKING HERE.

So now, without further delay, let’s take a look at what’s been going on with our favorite junior min-ing companies.

GOLD NEWSLETTER5 DECEMBER 2020 / JANUARY 2021

Mining Share UpdateAmerican Pacific Mining

USGD.CN; USGDF.OTC 604-908-1695

americanpacific.ca

American Pacific’s JV partner Kennecott has released the results from the first of nine holes drilled on the Madison copper-gold project in southwest Montana.

The hole intersected significant grades of both gold and copper down-dip and lateral to the known miner-alization at Madison. Hole 21 cut 23.6 meters of 2.2% copper at 222.8 meters depth and 1.7 meters of 69.4 g/t gold and 0.4% coper at 244.7 meters depth.

Eight holes from this joint program at Madison are still pending, and given their spacing and these early good results, I think they have the chance to surprise the market to the upside.

GOLD NEWSLETTER6 DECEMBER 2020 / JANUARY 2021

In addition, it’s worth revisiting Kennecott’s willingness to spend up to $30 million to earn up to 70% in this project. An exploration arm of mining giant Rio Tinto, this outfit doesn’t chase after small deposits.

The fact that Kennecott has agreed to bankroll the exploration and development of Madison speaks volumes about the potential of the project.

American Pacific, meanwhile, gets a free carried interest on a project that could prove both rich and sizeable. Past production at Madison included 2.7 million pounds of copper with grades ranging be-tween 20% and 35% copper. It also produced 7,570 ounces of gold.

Hitting these high grades of copper and gold in Hole 21 (which included the highest gold grades yet encountered on the project) bodes well for the as-says still to come from this project and from the work ahead in 2021.

In the meantime, American Pacific has been squaring away its two gold projects in Nevada.

The company had already optioned its Tuscarora gold project to Elko Sun Mining, a private company based in British Columbia. Elko Sun has since chosen to cut a subsequent option agreement for the project with Soldera Mining (SOLD.CN; C$0.46).

After these option agreements are worked through, American Pacific will retain a small carried interest in Tuscarora that will give it exposure to any upside here.

In addition, the company has also cut an agreement with GRAC, another private BC company, on its Gooseberry gold project.

GRAC can earn a 51% interest in Gooseberry by paying American Pacific $50,000 in cash, spending $1.5 million over two years on exploration and issuing two million shares to American Pacific.

It can earn another 14% by issuing an additional one million shares to American Pacific and conducting another $3 million in exploration. GRAC can achieve an 80% interest by completing a positive feasibility study on Gooseberry.

Taken together, these moves ensure American Pacific’s focus will remain on the outsized opportunity its Kennecott JV on Madison represents for the company.

USGD has given back ground along with the broader market of late, but given the bright future I see for both gold and copper next year, current trading levels make for an excellent bargain. American Pacific’s still a buy.

American Pacific Mining Corp. Recent Share Price: ...............C$0.16 Shares Outstanding: ......65.4 million Market Cap: ..............C$10.5 million Shares Outstanding Fully Diluted:...............102.1 million Market Cap Fully Diluted:............C$16.3 million

American Pacific Mining

$0.16

$0.20

$0.24

$0.28

$0.32

$0.36

$0.40

$0.44

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

Artemis Gold ARTG.V; ARGTF.OTC

604-558-1107 artemisgoldinc.com

Artemis Gold was the first of three new recom-mendations that I introduced to you in our interim issue last month.

To recap, this is the vehicle that spun out of At-lantic Gold when St Barbara bought that company and its Moose River Consolidated project in Nova Scotia for C$722 million.

That hefty purchase price was a testament to the diligence and focus of Atlantic’s CEO Steven Dean, who conducted enough drilling on MRC that St Barbara felt very comfortable taking over the oper-ation.

Now, with Artemis, Dean has turned his atten-tion to Blackwater, a large, but fairly low-grade

gold deposit in central British Columbia. Artemis purchased the project from mid-tier producer New Gold (NGD.NYSE-A; NGD.TO; US$2.23).

Blackwater has an 8-million-ounce gold reserve and a base-case, after-tax NPV (discounted at 5% and ap-plying a US$1,541/oz. gold price) of C$2.2 billion and a levered, after-tax IRR of 50%.

Those are some solid numbers, especially when you consider that initial capex is C$592 million, or just over a quarter of the implied NPV. Payback period on the project is 2.0 years.

Better still, at a gold price of US$2,050/oz., that NPV jumps to C$3.8 billion and the IRR to 70%. It also has downside protection, with a US$1,300/oz. gold price resulting in a C$1.5 billion NPV and a 38% IRR.

In an attempt to lock in the highest possible profitability from Blackwater, Dean and team have embarked on an intensive grade-control drilling program that will seek to pinpoint a high-grade starter zone within Bench 1570 in the Year 1 pit design.

Bench 1570 would be one of seven benches mined within the first year of operation. Recent met work has reinforced the 93% life-of-mine recoveries reported in the prefeasibility study release on the project this past August.

Between the good work Artemis will do on these areas for initial mining and the possibility that higher gold prices will allow the leverage of a lower-grade mine to develop, Blackwater is primed to become Steven Dean’s next lucrative takeout target.

That’s especially true given that higher gold prices mean major and mid-tier producers will be increas-ingly flush with cash and looking to add projects like Blackwater to their portfolios.

Artemis is already up about 21% from our entry price in our recent interim issue, so that timing was fortu-nate. But given the plan the company has for establishing Blackwater as a mineable project (in an uber-safe jurisdiction), there’s more to come.

Artemis remains a buy.

Artemis Gold Inc. Recent Share Price: ...............C$6.00 Shares Outstanding: ....122.5 million

GOLD NEWSLETTER7 DECEMBER 2020 / JANUARY 2021

Artemis Gold

$4.75

$5.00

$5.25

$5.50

$5.75

$6.00

$6.25

$6.50

$6.75

$7.00

$7.25Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

Market Cap: ...........C$735.0 million Shares Outstanding Fully Diluted: ..............161.5 million Market Cap Fully Diluted:..........C$969.0 million

Blackrock Gold BRC.V; BKRRF.OTC

604-817-6044 blackrockgold.ca

Things are moving fast on Blackrock Gold’s Tonopah West project in Nevada, as the company has released two batches of assays from its aggres-sive drilling program there in the past few weeks.

The most recent assays came from the Denver, Paymaster and Bermuda (DPB) target, where Hole 37 cut 3 metres of 10.5 g/t gold and 1,188 g/t silver (2,238 g/t silver-equivalent) on the Merton vein.

In addition, Hole 27 hit 12.2 meters of 297 g/t silver-equivalent at the intersection of Merton and the Bermuda vein; Hole 22 cut 4.5 meters of 285 g/t silver-equivalent on the Paymaster vein.

Blackrock has traced Merton along strike east-west for 120 meters and to 290 meters down dip. Both the Merton and Bermuda veins remain open in a number of directions. The Paymaster and Denver veins remain open to the east and the west.

So encouraged is the company by the results from DPB that it has decided to redouble its efforts there in 2021 with the goal of producing a resource estimate for the area by the end of next year.

To go from a maiden round of drilling to a resource estimate on a project like Tonopah West in just 18 months would be impressive feat, though one entirely in keeping with this aggressive management team.

Results from the past-producing Ohio vein turned in less impressive results, while the batch of assays from the Victor target, released toward the end of November, included some narrow intervals of high-grade.

The weak intervals from Ohio notwithstanding, Blackrock’s hit-rate at Tonopah West has been extraordi-nary. The company has done an admirable job posting good results, especially given that the project is pock-marked with historic workings.

In other news, Blackrock kicked off a 3,500-meter drill program on its Silver Cloud project in early No-vember. The goal will be to test targets that may be extensions of the veins that host the high-grade Hollister mine that lies three kilometers to the east.

The program on four key targets will prep the project for a likely spin out into a newco in early 2021.

Thus, BRC’s retreat from its summer is giving us a great opportunity to reload on this stock. Not only will we benefit from a steady stream of drill results (and a resource estimate) from Tonopah West, but we’ll also get a free lottery ticket on Silver Cloud when/if that spinout happens.

These selling points make Blackrock Gold a strong buy right now.

Blackrock Gold Corp. Recent Share Price: ...............C$0.64

GOLD NEWSLETTER8 DECEMBER 2020 / JANUARY 2021

Blackrock Gold

$0.60

$0.65

$0.70

$0.75

$0.80

$0.85

$0.90

$0.95

$1.00

$1.05

$1.10

$1.15

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

Shares Outstanding: ....106.1 million Market Cap: .............C$67.9 million Shares Outstanding Fully Diluted: ..............138.5 million Market Cap Fully Diluted: ...........C$88.6 million

Cassiar Gold GLDC.V; CGLCF.OTC

403-537-5590 cassiargold.com

Cassiar Gold has released two more rounds of assays from the Taurus deposit within its Cassiar project in northern British Columbia.

Like the assays I reported on in our interim issue, these latest results included more examples of mineable-grade gold over impressive widths.

Highlights from the first batch of seven holes included Hole 110 (2.4 g/t gold over 25.1 meters) and Hole 119 (1.8 g/t over 32.8 meters). Both these holes came from the hangingwall of the Taurus West fault.

In addition, expansion drilling on the nearby Wings Canyon target yielded 16.8 meters of 0.64 g/t and 0.5 meters of 19.5 g/t.

The most recent assays came from Taurus, as well as the Sable zone. Hole 116 cut 18.2 meters of 5.4 g/t gold at Sable. At Taurus, we got another long width of mineable-grade gold: 83.4 meters of 1.2 g/t.

These results have the potential to both upgrade and grow the resource already confirmed at Taurus (1.0 million near-surface ounces at 1.4 g/t gold). Plus, the Cassiar South target offers a wealth of past-producing mines that may contain additional high-grade to feed any operation at Taurus.

And with a permitted mill, a highway, ample access roads, a camp and key mine permits to its credit, the Cassiar project as a whole looks like a very attractive takeout target.

As the drills continue to turn, both on Taurus and on some of those high-grade targets in Cassiar South, the project will likely become even more tempting. Management sees potential here for this district-scale land package to host a multi-million-ounce resource.

Led by some of the savviest players in mining business, Cassiar Gold is a company that looks extremely undervalued relative to the assets it already possesses (much less relative to its potential).

In 2021, we’ll see a 15,000-meter drill program to test South Cassiar, which means the company will likely deliver high-grade assays into a resurgent gold market.

Between this potential catalyst and the in situ value this company already boasts, Cassiar Gold is primed to deliver strong leverage on rising gold prices. It’s still a buy.

Cassiar Gold Corp. Recent Share Price:................C$0.55 Shares Outstanding: ......54.3 million Market Cap: .............C$29.9 million

GOLD NEWSLETTER9 DECEMBER 2020 / JANUARY 2021

Cassiar Gold

$0.45

$0.50

$0.55

$0.60

$0.65

$0.70

$0.75

$0.80

$0.85

$0.90

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

Shares Outstanding Fully Diluted: ................80.0 million Market Cap Fully Diluted: ...........C$44.0 million

K2 Gold KTO.V; KTGDF.OTC

604-354-2491 k2gold.com

Well those were nice hits. I’m referring to the assays for the first three holes K2 Gold recently completed on its Mojave project in Southern Cali-fornia.

All three holes came from the Dragonfly zone on the east side of the project. And all three cut wide intervals of very mineable grade gold.

The highlight of the three came from Hole 2 (86.9 meters of 4.0 g/t gold from surface, including 45.7 meters of 6.7 g/t). Hole 1 hit 51.8 meters of 1.2 g/t gold from surface, including 18.3 meters of 3.1 g/t, and Hole 3 intersected 62.5 meters of 1.4 g/t from 3.1 meters, including 18.3 meters of 3.2 g/t.

Even though these holes were largely confirmatory of prior drilling in the late 1990s by BHP, they re-minded that market of why this project has so much potential.

Simply put, near-surface oxide gold like Mojave has proven itself to host typically gets mined. The hold-up has been local resistance to mining in the intervening years.

But the team at K2 Gold is adept at navigating these challenges, as evidenced by its ability to begin drilling the project again.

Core from another 14 holes remain at the lab, so K2 will have more good news flow on the way.

As it was, these first results caused the company’s share price to spike more than C$0.20 in the initial trading after the news. KTO has since retreated a bit from that initial spike and continues to look like a good value at current levels.

I say that because, based on Mojave’s history of near-surface, mineable-grade oxide hits, I think more of the same are likely on the way as assays from the remaining holes drilled in K2’s maiden drilling program there hit the newswires.

A Discovery Group vehicle with a company-making project to its credit, K2 Gold is well positioned to lever up our gains in gold as we move into the new year.

K2 Gold Corp. Recent Share Price: ...............C$0.61 Shares Outstanding: ......51.7 million Market Cap: .............C$31.5 million Shares Outstanding Fully Diluted: ................55.9 million Market Cap Fully Diluted:............C$34.1 million

GOLD NEWSLETTER10 DECEMBER 2020 / JANUARY 2021

K2 Gold

$0.45

$0.50

$0.55

$0.60

$0.65

$0.70

$0.75

$0.80

$0.85

$0.90

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

Montage Gold MAU.V

604-512-2959 montagegoldcorp.com

Montage Gold was the second of my three new recommendations in our interim issue.

As I asserted in that original update, this com-pany is very much a bet on a management team with a highly successful track record.

The Red Back Mining company shepherded two projects (Chirano in Ghana and Tasiast in Mauritania) along the development curve enough to see Kinross take the company out in 2010 for more than $7 billion.

That same Red Back team is now advancing a large, 3,750-square-kilomter property portfolio in Cote d’Ivoire. Originally held by Red Back, these projects host numerous exploration targets.

Chief among those is the advanced-stage Morondo project, which hosts 1.54 million ounces of inferred gold (52.5 million tonnes of 0.91 g/t).

Again, as I mentioned in my recommendation last month, that resource is likely to grow larger still, thanks to an aggressive, five-rig drilling program currently underway at Morondo.

That program will consist of 50,000 meters and will seek to grow Morondo’s resource along strike and at depth. In fact, recent holes have targeted an area as much as 250 meters below the current resource.

Remember, Morondo’s million-ounce resource was outlined in 2018 with only 18,172 meters of drilling. The 8,125 meters of recent drilling has demonstrated that depth potential, and this 50,000-meter program in-cludes 20,000 meters focused just on expanding Morondo’s resource-hosting Kone target.

This work will support an inferred resource upgrade in Q1 2021, along with a PEA. Combined with an indicated resource planned for Q2 2021, Montage’s drilling program at Morondo should keep the news flow-ing throughout the new year.

Cote d’Ivoire itself is an intriguing mining destination, having produced five deposits with substantial re-source estimates in the past five years. A number of companies are operating in the country, including indus-try heavyweight Barrick.

Initial metallurgy on Morondo indicates 92% recoveries employing a carbon-in-leach processing method. That the mineralization starts at surface means the deposit is amenable to open-pit development.

And, because numerous projects are within trucking distance of Morondo, it could become the hub of a whole new gold district in the country.

With working capital of C$34.2 million, Montage is fully funded through completion of a feasibility study on Morondo, an effort that management has budgeted at C$22 million.

Add in its Korokaha project’s location near Barrick’s Tongon mine, and you have a company in a great position to put points on the scoreboard in 2021.

It remains very much a buy at current levels.

GOLD NEWSLETTER11 DECEMBER 2020 / JANUARY 2021

Montage Gold

$0.75

$0.80

$0.85

$0.90

$0.95

$1.00

$1.05

$1.10

$1.15

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

Montage Gold Corp. Recent Share Price: ...............C$0.89 Shares Outstanding: ....104.8 million Market Cap: ..............C$93.3 million Shares Outstanding Fully Diluted: ..............113.9 million Market Cap Fully Diluted: .........C$101.4 million

Northern Vertex Mining NEE.V; NHVCF.OTC

855-633-8798 northervertex.com

I had originally planned to update you this month on Northern Vertex’s impressive Q3 2020 perform-ance and the good work it’s doing drilling for more resources on its flagship Moss Mine.

Then came the news announced on Monday that Northern Vertex has reached a deal to merge with an-other Gold Newsletter recommendation: Eclipse Gold Mining (EGLD.V; EGLPF.OTC; C$0.57).

Set to close in February 2021, the move will give the combined company two Walker Lane Trend proj-ects, with one (Moss) already in production. Both projects have million-ounce-plus growth potential.

Assuming the proposed, concurrent C$20 million financing closes, the combined company will have a pro-forma cash position of C$29.5 million. It will also benefit from the growing cash flow positive position of Moss — the mine generated US$12 million in earnings from mine operations in the most recent quarter.

Each holder of Eclipse will receive 1.09 shares of Northern Vertex for each share of Eclipse Gold held. Upon closing, Northern Vertex shareholders will hold 71% of the combined company, Eclipse shareholders will own 18% and new shareholders will hold the remaining 11%.

The financing will raise a minimum of C$20 million via a private placement of subscription receipts. Completion of that financing is a condition of closing.

The newco plans to continue optimizing operations at Moss, growing that project through near-mine and brownfield expansion drilling. The Phase II drilling program at Eclipse’s Hercules project in Nevada contin-ues.

Not only will the combined company likely attract more research coverage, it should also benefit from im-proved market liquidity. That process may also include an upgrade to the TSX, as well as a U.S. exchange list-ing.

The newco will boast a board of directors that has created billions in value in past leadership roles at other companies.

With Moss producing a record 13,083 ounces of gold in its most recent quarter (at a cash cost of just $954/ounce), the merged company is an excellent position to provide leverage to gold prices in 2021.

In short, it’s a great deal for shareholders of both companies. (And, since both merging companies are in our portfolio, you may well own both.)

GOLD NEWSLETTER12 DECEMBER 2020 / JANUARY 2021

Northern Vertex Mining

$0.54

$0.56

$0.58

$0.60

$0.62

$0.64

$0.66

$0.68

$0.70

$0.72

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

Given my enthusiasm for both Eclipse and Northern Vertex, I’m highly supportive of this merger. The mar-ket’s initial reaction sent Eclipse down to near C$0.50, and Northern Vertex down a couple of cents.

I don’t read too much into that reaction, as I think the combined company has a lot to offer shareholders. We’ll move Eclipse to a hold along with Northern Vertex though, while we wait for the transaction to consum-mate.

Northern Vertex Mining Corp. Recent Share Price: ...............C$0.57 Shares Outstanding: ....251.3 million Market Cap: ...........C$143.2 million Shares Outstanding Fully Diluted: ..............358.0 million Market Cap Fully Diluted: .........C$204.1 million

Oro X Mining OROX.V; WRPSF.OTC

604-638-8063 oroxmining.com

Oro X Mining was the last of the three new recs I made in our interim issue.

And while much of that recommendation is based on a top-flight management team and what moves they may make on the acquisition front going for-ward, Oro X’s adjacent Coriorcco and Las Antas projects in Peru certainly factor into the equation.

For one thing, Peru has been and remains a top-tier mining jurisdiction (the Fraser Institute rated it 10th in the world in 2019 for investment attractive-ness). Companies with mines in the country are a who’s who of the world’s major miners. The country is the world’s second largest producer of copper and the sixth largest producer of gold.

Coriorcco encompasses a known area of high-grade mineralization, with the majority of it focused within the Cerro Domo target. Rock chips from underground sampling have graded as high as 59.6 g/t gold over 1.4 meters, and surface sampling has returned channel samples of 16.6 g/t over 2.1 meters and 31.0 g/t over 0.8 me-ters.

The area includes two past-producing veins that generated 5,719 tonnes of 7.5 g/t gold. Coriorcco hosts a number of drill-ready targets and has the potential to host a low-sulphidation epithermal system that is both large and high grade.

Las Antas, meanwhile, is more of a high-sulphidation, bulk tonnage target, one that shows intense alteration at surface, but which has not seen much in the way of exploration since 2013.

Combined with the spin-out potential of Oro X’s Julian project in Ecuador, the company’s Peru holdings provide a firm floor to the company’s current valuation.

But with a team that boasts more than C$3.2 billion of shareholder value creation in the past 13 years, I’m excited to see what Luis Zapata, Paul Matysek and team add to this picture in the coming year.

At a minimum, we should expect a spinout of Julian and a 5,000-meter drilling program (beginning in Q2 2021) at Coriorcco.

GOLD NEWSLETTER13 DECEMBER 2020 / JANUARY 2021

Oro X Mining

$0.62

$0.64

$0.66

$0.68

$0.70

$0.72

$0.74

$0.76

$0.78

$0.80

$0.82

$0.84

$0.86

$0.88

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

GOLD NEWSLETTER DECEMBER 2020 / JANUARY 2021 14

Oro X’s tight share structure, combined with the upsurge in gold prices I see coming in the new year, should make good news on the exploration, acquisition and divestment fronts a key driver for the company’s share price. OROX is another buy.

Oro X Mining Corp. Recent Share Price: ............C$0.71 Shares Outstanding: ...42.9 million Market Cap:............C$30.5 million Shares Outstanding Fully Diluted: .............51.4 million Market Cap Fully Diluted: ........C$36.5 million

Silvercorp Metals SVM.NYSE-A; SVM.TO

888-224-1881 silvercorpmetals.com

Strong silver prices helped Silvercorp Metals boost revenue by 13% on a year-over-year basis in its most recent quarter.

The company posted $56.4 million in rev-enue on the sale of 1.7 million ounces of silver, 2,200 ounces of gold, 18.6 million pounds of lead and 7.4 million pounces of zinc.

Those numbers included an 8% and a 3% de-crease, respectively, in silver and lead sales, and a 100% and an 11% increase, respectively, in gold and zinc sales.

Silvercorp generated net income attributable to shareholders during its most recent quarter of $15.5 million, up 27% from the same quarter last year. All-in sustaining costs, net of by-product credits, were $6.99/ounce in the most recent quarter, an in-crease from $4.15/ounce last year.

The company finished the quarter with $200.1 million in cash and cash equivalents and short-term in-vestments. It declared a semi-annual dividend of $0.0125 per share for shareholders of record as of Nov. 25, 2020.

It also finalized a shelf prospectus that would allow the company to issue a combination of securities equal to $200 million. Management has no immediate plans to tap this financing vehicle.

On the exploration front, Silvercorp’s ongoing exploration of its flagship Ying Mining Complex contin-ues to bear fruit.

The LME mine generated highlight assays from work over the past year of 0.92 meters of 6,455 g/t sil-ver, 10 g/t gold and 5.28% lead. The LMW mine at Ying produced a highlight gold interval of 37.1 g/t over 1.89 meters.

The steady exploration and development work that Silvercorp does, particularly at Ying, helps the com-pany to extend the overall life of its assets.

All those gold, zinc and lead credits give the company one of the lower cost profiles in the silver sector.

Even with the retreat SVM has made in sympathy with the broader markets in recent weeks doesn’t

Silvercorp Metals

$5.75

$6.00

$6.25

$6.50

$6.75

$7.00

$7.25

$7.50

$7.75

$8.00

$8.25

$8.50

$8.75

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

change the fact that this company remains a great way to play silver. It’s a key hold in our portfolio.

Silvercorp Metals Inc. Recent Share Price: ............US$5.87 Shares Outstanding: ....175.2 million Market Cap: ............US$1.03 billion Shares Outstanding Fully Diluted:...............178.1 million Market Cap Fully Diluted:...........US$1.05 billion

Sonoro Gold SGO.V; SMOFF.OTC

604-632-1764 sonorogold.com

Sonoro Gold is making progress on a couple of fronts.

It has elected to upgrade its planned Heap Leach Pilot Operation to a full-fledged mining operation at Cerro Caliche. It is also successfully drilling on key oxide targets within the project.

Management’s aggressive goal is to have the Heap Leach Mining Operation (HLMO) up and run-ning by the end of 2021. To that end, it has em-barked on a program of met testing and environmental permitting. It will also produce a PEA on the project and attempt to secure financing.

In the meantime, drilling on Cerro Caliche is hitting more intervals of mineable-grade gold that

could help Sonoro grow the project’s existing 201,000-ounce gold-equivalent resource.

The highlight of recent drilling came from the Buena Suerte zone. Hole 109 there intersected 45.7 meters of 0.97 g/t gold, beginning at 3.05 meters. Hole 124 tested Buena Suerte to the southeast and hit 6.1 meters of 4.0 g/t gold. Hole 127, drilled on the middle of the zone, cut 10.7 meters grading 0.96 g/t.

Significantly, the 20 holes from this latest group of assays all hit anomalous mineralization, as have all 107 of the previous holes drilled on the project. This near-surface portion of Cerro Caliche isn’t high-grade, but its oxide material that amenable to the HLMO management has planned for the project.

With a new resource estimate on Cerro Caliche due out in early 2021 and a core drill program to test for higher-grade sulphide material at depth underway, Sonoro Gold should hit the ground running in 2021.

A fast-track development play with exploration upside, this company is a great bet on a gold resurgence in the new year. Sonoro’s a buy.

Sonoro Gold Corp. Recent Share Price:................C$0.25 Shares Outstanding:.......85.1 million Market Cap: ..............C$21.3 million Shares Outstanding Fully Diluted: ..............131.7 million Market Cap Fully Diluted:............C$32.9 million

GOLD NEWSLETTER15 DECEMBER 2020 / JANUARY 2021

Sonoro Gold

$0.23

$0.24

$0.25

$0.26

$0.27

$0.28

$0.29

$0.30

$0.31

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

SSR Mining SSRM.Nasdaq; SSRM.TO

888-338-0046 ssrmining.com

SSR Mining delivered its Q3 2020 financials last month, its first earnings report since its merger of equals with Alacer Gold.

The company is on pace to achieve its updated, full-year production guidance of between 680,000 and 760,000 gold-equivalent ounces at an average AISC of between $965 and $1,040 per gold-equiva-lent ounce.

The newly acquired Copler project in Turkey produced 19,586 ounces of gold at an AISC of $737 between the closing of the Alacer merger and the end of the quarter. For the full quarter, it generated 76,666 ounces.

SSRM’s net attributable income for the quarter was $26.8 million. It ended the quarter with a consolidated cash position of $772.8 million.

In a signal that management is confident about the company’s future, it has also declared a quarterly divi-dend of $0.05. The first payment of that dividend will occur in the first quarter of 2021.

At Copler, meanwhile, the company released both a master plan feasibility study for the reserve case on the project and an alternative PEA case.

The reserve case includes a significant, 22% increase in reserves (to 4.0 million ounces) and a similar, 24% increase to measured and indicated resources (to 7.4 million ounces). Inferred resources increased by 58% to 3.1 million ounces.

The reserve case for project posits an NPV, discounted at 5%, of $1.7 billion on life-of-mine production of 3.6 million ounces of gold. That reserve case production scenario would generate 266,000 ounces of gold at AISC of $865 over the first five years of implementation.

The PEA case, which includes the resources on the nearby Ardich target, would have an NPV, discounted at 5%, of $2.2 billion on life-of-mine production of 4.6 million ounces of gold. Under this scenario, Copler would produce 306,000 ounces annually at AISC of $886 over the first five years of operation.

With exploration continuing to define new resources at Ardich and Copler, there’s a good chance that the project’s global resources will expand further.

Either way, it’s clear that adding Copler has given SSR Mining a world-class asset to go with its already compelling North American projects. It remains a hold at current trading levels.

SSR Mining Inc. Recent Share Price:...........US$18.71 Shares Outstanding: ....217.9 million Market Cap: .............US$4.08 billion

GOLD NEWSLETTER16 DECEMBER 2020 / JANUARY 2021

SSR Mining

$17.00

$17.50

$18.00

$18.50

$19.00

$19.50

$20.00

$20.50

$21.00

$21.50

$22.00

$22.50

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

GOLD NEWSLETTER DECEMBER 2020 / JANUARY 2021 17

Vox Royalty VOX.V; VOXCF.OTC

+1-345-926-4209 voxroyalty.com

Vox added to its royalty portfolio last month, cutting a deal for a suite of royalties on up to eight projects from Breakwater Resources. It also an-nounced a separate transaction for a royalty on the Brits vanadium project in South Africa.

The Breakwater royalty package covers pre-cious and base metal projects in Canada and the United States. Operating partners on these projects include Agnico Eagle, Alamos Gold, Hecla Mining and Galway Metals.

The acquisition, which will total C$980,002, will consist of C$455,002 in cash and C$525,000 of Vox shares (based on the 30-day trailing average trading price as of closing).

The package includes projects with five resource estimates and multiple engineering studies. Key addi-tions will include a 2.0% gross proceeds royalty on the Lynn Lake gold project in Manitoba, a 0.66% NSR on Agnico’s West Malartic project in Quebec and a US$0.20/ton royalty on Hecla’s Montanore silver-copper project in Montana.

To this royalty package, Vox is adding a 1.75% gross sales royalty from Sable Metals and Minerals on Bushveld Minerals’ Brits vanadium project.

To acquire the royalty, Vox will pay US$500,000 up front and issue US$250,000 of Vox shares to Sable. At its election, Vox can pay, in either cash or shares, an additional US$1 million once 210,000 tonnes have been mined over a six-month period at Brits and another US$250,000 once 1.5 million tonnes have been mined over a three-year period.

Brits is located next to Bushveld’s Vametco Mine and would provide a ready source of ore as that com-pany ramps up production on Vametco and the complementary Vanchem processing facility.

With these additions, Vox had conducted 18 transactions to acquire more than 40 different royalties since 2019.

Its portfolio’s combination of low geopolitical risk and near-term production potential make it a must-own in the metals environment I see on the horizon in 2021.

The current market has put Vox Royalty on sale, making it an excellent value and a great potential lever at current levels. It remains a strong buy.

Vox Royalty Corp. Recent Share Price: ...............C$2.45 Shares Outstanding: ......32.6 million Market Cap: ..............C$79.9 million Shares Outstanding Fully Diluted: ................35.2 million Market Cap Fully Diluted: ...........C$86.2 million

Vox Royalty

$2.20

$2.30

$2.40

$2.50

$2.60

$2.70

$2.80

$2.90

$3.00

$3.10

$3.20

$3.30

$3.40

$3.50Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

GOLD NEWSLETTER DECEMBER 2020 / JANUARY 2021 18

Brief Notes • Aftermath Silver (AAG.V; AAGFF.OTC; C$1.01) has amended its agreement with SSR Min-ing on the acquisition of the Berenguela silver-cop-per project in Peru.

The purchase price now calls for $12.725 mil-lion in cash payments instead of $13 million. That $275,000 difference will be made up in Aftermath shares — the junior will now issue SSR Mining C$3.36 million instead of C$3.0 million in shares.

With the addition of Berenguela, Aftermath is onboarding a project with a JORC-compliant meas-ured and indicated resource of 98 million ounces of silver and 624 million pounds of copper and an in-ferred resource of 28 million ounces of silver and 147 million pounds of copper.

Plus, an updated, NI 43-101 compliant resource estimate is on the way soon for Aftermath’s Challacollo silver-gold project in Chile.

Bottom line: This company is developing into a unique silver development story that should provide ex-cellent leverage to silver’s next big run. It’s still a buy.

• Amex Exploration (AMX.V; AMXEF.OTC; C$3.04) released more high-grade results from Perron last week. Holes drilled on the HGZ expanded the bonanza grade portion of its western area. Another hole ex-panded HGZ to the east by 75 meters.

These results are in line with the consistently good assays that this section of Perron’s Eastern Gold zone has generated. With drills set to generate 10,000 meters of core per month, Amex won’t lack for news flow anytime soon. It’s still a hold.

• Cabral Gold (CBR.V; CBGZF.OTC; C$0.61) reported more results from Cuiu Cuiu last week. Surface work identified another target, dubbed Tracaja, north of the Medusa target. Drilling on the Alonso target failed to yield any significant results.

So far, Cabral has drilled 20 holes on Medusa and just positioned its newly arrived second RC rig on Machichie/Machichie SW to further test that area.

A recent rounds of warrant exercises has added C$4.46 million to the company treasury. That’s money it can use to continue its rapid testing of the myriad targets it has outlined on Cuiu Cuiu.

Don’t get too focused on the blanks Cabral shot at Alonso. That’s going to be par for the course for this kind of drilling program. The fact remains that there is a lot of gold in this system; Cabral just needs to stay diligent in its search for it.

Market-moving assays could arrive at any time. On the thought that they will, Cabral remains a buy.

• Drilling to test for more breccia pipes at Soledad has yielded more quality results for Chakana Copper (PERU.V; CHKKF.OTC; C$0.49).

The Phase 3, 15,000-meter program is focused on the Paloma and Huancarama breccia complexes. High-lights from recent holes drilled on Paloma West include 12.2 meters of 5.8 g/t gold, 3.0% copper and 252 g/t silver and 5.0 meters of 4.0 g/t gold, 2.0% copper and 37.2 g/t silver (Hole147) and 10.7 meters of 7.3 g/t gold, 10.2% copper and 163.5 g/t silver and 8.1 meters of 0.28 g/t gold, 4.1% copper and 53.8 g/t silver (Hole 145).

Aftermath Silver

$0.70

$0.75

$0.80

$0.85

$0.90

$0.95

$1.00

$1.05

$1.10

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

As ever, the goal with this program is to prove up enough of these high-grade and deep (but narrow) breccia pipes to make up an eco-nomically mineable resource at Soledad.

Nothing about recent results suggests Chakana won’t eventually achieve its goal here. It remains a buy.

• Cornerstone Capital Resources (CGP.V; CTNXF.OTC; C$5.10) provided an update on the prefeasibility study of Alpala, the resource-hosting portion of the Cascabel project in which Cornerstone owns a 21.1% direct and indirect interest.

Originally slated to hit the market in Q3 2020, the study has been hampered by Covid restrictions and a need to need to redesign some of the underground infrastructure that will be needed to access the ore at Al-pala.

The new timeline calls for a recently created Alpala Project Committee to conduct a review and report its findings toward the end of January 2021. An update on the new timing for the PFS will follow.

Based on Alpala’s world-class scale, this delay in the prefeasibility process is one well worth waiting through. Cornerstone’s sizeable share of the project still has the potential to result in a significant re-rating of the company’s shares. It’s another buy.

• Fabled Silver Gold (FCO.V; C$0.07) has closed on its purchase of the Santa Maria mine in Chihuahua State, Mexico.

The deal with Golden Minerals (AUMN.NYSE-A; US$0.60) will consist of an initial payment of $500,000 cash and the issuance of one million FCO shares. This will be followed by a $1.5 million cash pay-ment 12 months from closing and another $2.0 million payment 24 months from closing. FCO must also pay another C$480,000 in staged payments to the underlying optioner.

Fabled will cover the initial payments with the C$4.6 million it raised via its previously closed placement of 92 million subscription receipts. Those were priced at C$0.05 and consist of one share and a warrant that is redeemable at C$0.10 until Dec. 4, 2022.

With this transaction consummated, Fabled will move forward with surface exploration in support of an eventual drilling program at Santa Maria. The company hopes to build on the small gold-silver resource al-ready established on the project.

The prospects look good, as the region has produced over 250 million ounces of silver historically. At Santa Maria itself, at least 21 distinct silver veins have been located so far, although only two have been drilled over limited strike lengths and depths. Now that the deal has been consummated, I expect strong news flow over the next six months.

And with a market cap of less than C$5.5 million, positive announcements for this new silver play could have an outsized effect on the share price.

As a shareholder myself, I’m excited to see work get going here. Fabled remains a buy at current levels.

• Fireweed Zinc (FWZ.V; FWEDF.OTC; C$0.94) cut two separate deals last month to add to large pieces of land to its property position at Macmillan Pass.

With the additions, Fireweed has increased the total land package at Mac Pass from 544 square kilometers to 936 square kilometers. The bulk of the additions are on the western side of the Fertile Corridor and Bound-ary zone.

GOLD NEWSLETTER19 DECEMBER 2020 / JANUARY 2021

“The prospects look good, as the re-gion has produced over 250 million ounces of silver historically. At Santa Maria itself, at least 21 distinct silver veins have been located so far, al-though only two have been drilled over limited strike lengths and depths.”

They add an exploration lottery ticket to sup-plement the good work Fireweed is doing at Boundary and the large resources it has already es-tablished at Tom and Jason. With growth of that re-source a near certainty with more work on Boundary, FWZ remains a buy.

• Genesis Metals (GIS.V; GGISF.OTC; C$0.23) has hit into more high-grade within the Main zone at Chevrier. Best assays from this latest batch of holes include 13.0 g/t over 10.7 meters (Hole 76), 7.5 g/t over 4.6 meters (Hole 77) and 5.0 g/t over 1.6 meters (Hole 74).

These holes help define the continuity of the gold in what management is dubbing the Fox sub-zone within the Main zone. Genesis will likely have to step out more from the Main zone (and test new targets) to get a boost from assays of this qual-ity.

For now, GIS is a hold as we await more re-sults.

• An updated resource estimate for Goldsource Mines’ (GXS.V; GXSFF.OTC; C$0.13) Eagle Mountain gold project in Guyana should hit the market in early Q1 2021.

The 15,000 meters Goldsource has drilled so far this year on both the Eagle Mountain and Salbora de-posits indicate that the project will see a significant upgrade of their resources. Good assays from new targets like Montgomery and Ann hold out the possibility that the overall resource will grow as well.

We’ll use that report to gauge how to position GXS in our portfolio for 2021. For now, we’ll keep it a hold.

• Grande Portage Resources (GPG.V; GPTRF.OTC; C$0.42) has released additional batches of assays from this year’s drilling program on its Herbert project in southeast Alaska. That 8,375-meter program is now com-plete, with assays expected to continue to trickle in from slow labs over the next couple of months.

The latest assays indicate that the Main, Deep Trench and Goat veins extend at depth and to the east, be-yond any known area of drilling. They also show strong results, including 1.48 meters of 29.21 g/t gold, in the Ridge vein, and intermediate vein between the larger Goat and Main Veins.

Unfortunately, GPG had the bad luck to deliver these solid assays into a turbulent gold market.

That said, I think the chance for this program to produce more high-grade results and demonstrate the need to drill Herbert further in 2021 continue to make it a solid bet on the return of rising gold prices.

However, we’ll make it a hold for now as we await more results from the drilling, and as the news vac-uum of the winter approaches.

• Great Bear Resources (GBR.V; GTBAF.OTC; C$16.21) been largely rangebound in recent weeks, though its share price has generally held up well against the headwinds the broader gold market has delivered.

The company’s aggressive drilling program to outline a resource on Dixie’s LP Fault zone continues apace. Given that high expectations for this program are already baked into its share price, it has become in-creasingly difficult for even spectacular results to move the needle here.

Even the company’s latest news, including high-grade results from a deep hole at the Hinge zone that dou-bled its depth to over 850 meters, and the discovery of a new regional vein zone halfway between the Hinge

GOLD NEWSLETTER20 DECEMBER 2020 / JANUARY 2021

Fireweed Zinc

$0.65

$0.70

$0.75

$0.80

$0.85

$0.90

$0.95

$1.00

$1.05

$1.10

$1.15

$1.20

$1.25

$1.30

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

and Arrow zones, failed to move the share price sig-nificantly.

That said, 2021 will be a pivotal year for Great Bear, as it steadily moves Dixie toward a maiden re-source estimate. Production of that report could kick takeout discussions into high gear — likely at prices substantially higher than GBR’s current trading lev-els.

The company is a hold through the new year, but that’s a recommendation I’ll be revisiting regu-larly, in case market-induced weakness may create a relative bargain in GBR.

• Group Ten Metals (PGE.V; PGEZF.OTC; C$0.36) reported some promising results from sur-face work and drilling on its Stillwater West PGE-nickel-copper-cobalt-gold project in Montana.

As a reminder, Stillwater West is a district-scale project, and Group Ten is targeting a large, platreef

style of mineralization, similar to that found within South Africa’s Bushveld complex.

PGEs, gold and the base metals available here all have the chance to have a great year in 2021, as a Covid vaccine gooses the economy and inflation simultaneously. An expensive wager on that possibility, Group Ten Metals is still a buy.

• Integra Resources (ITRG.NYSE-A; ITR.V; US$3.68) had a couple of nice hits from this year’s drilling on the War Eagle target at DeLamar.

Hole 14 cut 24.2 g/t gold and 655.1 g/t silver over 7.6 meters, including 98.0 g/t gold and 278.1 g/t silver over 1.8 meters. Hole 17 intersected 1.5 meters of 21.9 g/t gold and 76.4 g/t silver. To date, the program has outlined two structures, located 150 meters apart, that extend for more than 500 meters along strike.

Since War Eagle is outside of the deposits already outlined at DeLamar and Florida Mountain, continued success here could make a nice addition to those resources.

Integra’s share price has been muddling through this weak phase for the gold market. Overall though, it’s been holding its own (and remains up more than 300% from out initial entry point). We’ll keep Integra a hold for now.

• Midland Exploration (MD.V; MIDLF.OTC; C$0.86) has completed a spate of work on several projects lo-cated in Quebec’s portion of the Abitibi region. None of the work generated blockbuster news, but collec-tively, the company’s active approach it its large portfolio — work funded in many cases by JV partners — reminds us that few prospect generators execute this exploration model better than Midland. It remains a hold.

• Millrock Resources (MRO.V; MLRKF.OTC; C$0.12) provided the market with an update on drilling on its 64North project in Alaska. That program is being funded by JV partner Resolution Minerals.

The partners are currently drilling two holes that are following up on a quartz vein intersected by Hole 7. Another two holes are planned before drilling is wrapped up for this year.

So far, this program at 64North hasn’t generated the fire I was hoping for, though it has produced a bit of smoke. Given its location near the producing Pogo mine, I remain willing to be patient with this program and with Millrock generally.

Thanks to MRO’s prospect generator model, it has plenty of other irons in the fire if this one doesn’t pan out. Millrock’s still a hold.

GOLD NEWSLETTER21DECEMBER 2020 / JANUARY 2021

Great Bear Resources

$14.50

$15.00

$15.50

$16.00

$16.50

$17.00

$17.50

$18.00

$18.50

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

• Northern Dynasty Minerals (NAK.NYSE-A; NDM.TO; US$0.34) fell off a cliff last month on word that the U.S. Army Corps of Engineers had rejected NDM’s revised environmental impact statement for Pebble.

That denial effectively halts development of this world-class gold-copper-moly resource.

An investment on NDM has always been a bet on the idea that, by hook or by crook, the company would be able to shuttle Pebble through the permit-ting process. With a new administration due to take power that will likely to be more hostile to mining, it’s hard to see a clear path forward over the near or intermediate term for Northern Dynasty.

As long-time readers will remember, we’ve covered Northern Dynasty since it was a penny stock. In fact, I believe we were the first newsletter to recommend it, and our readers enjoyed extraor-dinary returns as it soared in value. Thus, it is with

a good deal of reluctance and disappointment that I am ceasing coverage on the company for now.

• Piedmont Lithium (PLL.ASX; PLL.Nasdaq; A$0.36/ADR: US$25.72) has engaged a team of consultants to help it put together a feasibility study for its Piedmont lithium project in North Carolina.

The study will focus on a combination of a spodumene concentrator and a 160,000 tonne-per-year quarry. Another study will kick off in early 2021 on a chemical plant to process that concentrate.

Lithium stories are staying on the market’s radar, thanks to the surging EV trend. We’ll keep Piedmont a hold for now, but will look at moving it to a buy as the company gets closer to releasing these feasibility stud-ies.

• Radisson Mining Resources (RDS.V; RMRDF.OTC; C$0.35) keeps turning out high-grade results at its O’Brien gold project. The latest highlights came from Hole 167 (111.0 g/t over 2.5 meters) and Hole 159 (10.9 g/t over 3.2 g/t and 13.6 g/t over 2.10 meters).

Hole 167 hit mineralization near the eastern and lower boundaries of the first mineralized trend out-lined 300 meters east of the old O’Brien mine. Hole 159 opened up the possibility of resource expansion to the west of the mine.

With another 11,500 meters of core currently awaiting assay, Radisson won’t lack for news flow any time soon. And if the past is prelude, we’ll see a lot more high-grade from O’Brien in the weeks ahead.

The company clearly seems to be on the track of a large resource expansion on this historic mining area. That makes Radisson a key lever on our port-folio of gold equities and a buy.

• Roughrider Exploration (REL.V; C$0.17) an-nounced an agreement last week to take a 70% in-terest in Industria Metals’ Scottie West property in

GOLD NEWSLETTER22DECEMBER 2020 / JANUARY 2021

Piedmont Lithium

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

Northern Dyansty

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

$1.20

Sep

8,

2020

Sep

15,

2020

Sep

22,

2020

Sep

29,

2020

Oct

6,

2020

Oct

13,

2020

Oct

20,

2020

Oct

27,

2020

Nov

3,

2020

Nov

10,

2020

Nov

17,

2020

Nov

24,

2020

Dec

1,

2020

Dec

8,

2020

© 2020 Gold Newsletter (Chart provided by Thechartstore.com)

northwest British Columbia.

The deal involves C$500,000 of staged cash payments, the issuance of C$500,000 of Roughrider shares and an exploration commitment of C$1 million over four years.

The option gives the company another project supplement work on its flagship Empire Mine property on Vancouver Island.

The company provided an update on surface work at Empire this week. Sampling in the Southwest and Snowbird areas has added more potential targets to a diamond drill program that is budgeted C$1 million and will begin in Q1 2021.

I continue to like this project and the team leading it. The Scottie West option indicates that the company will remain on the lookout for accretive deals. Based on the potential of the upcoming drill program at Em-pire, Roughrider Exploration remains a buy.

• An initial 2,500-meter drill program to test Silver Sands Resources’ (SAND.CN; SSRSF.OTC; C$0.25) Virginia project in Argentina is ongoing, with six holes completed to date. The program is designed to build on Virginia’s existing silver resource (11.9 million indicated ounces and 3.1 million inferred ounces) by focus-ing on extensions of, and gaps between, the known veins on the project.

With growth upside available via exploration and a solid base of silver resources, Silver Sands makes a great lever on rising silver prices. Now we just need the broader market to cooperate.

On the thought that it will in 2021, Silver Sands is still a buy.

• Infill drilling on the key zones within Skeena Resources’ (SKE.TO; SKREF.OTC; C$2.88) Eskay Creek project in BC’s Golden Triangle con-tinues to generate high-grade assays.