Vidyawarta July To Sept. ISSN: 2319 9318 Peer-Reviewed ...

10

MAH MUL/03051/2012 ISSN: 2319 9318 01 Vidyawarta ® Peer-Reviewed International Journal July To Sept. 2020 Special Issue : Interdisciplinary Multilingual Refereed Journal [dÚmdmVm© Impact Factor 3.102 (IIJIF) Impact Factor 7.041 (IIJIF) TM TM MAH/MUL/ 03051/2012 ISSN :2319 9318 fo|kokrkZ ;k vka rjfo|k’kk[kh; cgw Hkkf”kd =S ekfldkr O;Dr >kkys Y;k erka ’kh ekyd] iz dk’kd] eq nz d] la iknd lger vlrhyp vls ukgh- U;k;{ks =%chM “Printed by: Harshwardhan Publication Pvt.Ltd. Published by Ghodke Archana Rajendra & Printed & published at Harshwardhan Publication Pvt.Ltd.,At.Post. Limbaganesh Dist,Beed -431122 (Maharashtra) and Editor Dr. Gholap Bapu Ganpat. July To Sept. 2020 Special Issue Editors Dr. Nilendra Lokhande Dr. Jyoti Thakur

Transcript of Vidyawarta July To Sept. ISSN: 2319 9318 Peer-Reviewed ...

MAH MUL/03051/2012 ISSN: 2319 9318 01 Vidyawar ta®

Peer-Reviewed International JournalJuly To Sept. 2020

Special Issue

: Interdisciplinary Multilingual Refereed Journal[dÚmdmVm © Impact Factor 3.102 (IIJIF)Impact Factor 7.041(IIJIF)

TMTM

MAH/MUL/ 03051/2012 ISSN :2319 9318

fo|kokrkZ ;k vkarjfo|k’kk[kh; cgwHkkf”kd =Sekfldkr O;Dr >kkysY;k erka’kh ekyd]izdk’kd] eqnzd] laiknd lger vlrhyp vls ukgh- U;k;{ks=%chM

“Printed by: Harshwardhan Publication Pvt.Ltd. Published by Ghodke ArchanaRajendra & Printed & published at Harshwardhan Publication Pvt.Ltd.,At.Post.Limbaganesh Dist,Beed -431122 (Maharashtra) and Editor Dr. Gholap Bapu Ganpat.

July To Sept. 2020Special Issue

Editors

Dr. Nilendra Lokhande Dr. Jyoti Thakur

MAH MUL/03051/2012 ISSN: 2319 9318 02 Vidyawar ta®

Peer-Reviewed International JournalJuly To Sept. 2020

Special Issue

: Interdisciplinary Multilingual Refereed Journal[dÚmdmVm © Impact Factor 3.102 (IIJIF)Impact Factor 7.041(IIJIF)

http://www.printingarea.blogspot.com

Govt. of India,Trade Marks RegistryRegd. No. 2611690

Impact Factor 3.102 (IIJIF)Date of Publication16 Sept. 2020

Vidyawarta is peer reviewed research journal. The review committee & editorial board formed/appointedby Harshwardhan Publication scrutinizes the received research papers and articles. Then the recommendedpapers and articles are published. The editor or publisher doesn’t claim that this is UGC CARE approvedjournal or recommended by any university. We publish this journal for creating awareness and aptitude regardingeducational research and literary criticism.

The Views expressed in the published articles,Research Papers etc. are their writers own. This Journaldose not take any libility regarding appoval/disapproval by any university, institute, academic body and others.The agreement of the Editor, Editorial Board or Publicaton is not necessary. Editors and publishers have the right toconvert all texts published in Vidyavarta (e.g. CD / DVD / Video / Audio / Edited book / Abstract Etc. and other formats).

If any judicial matter occurs, the jurisdiction is limited up to Beed (Maharashtra) court only.

MAH MUL/03051/2012 ISSN: 2319 9318 014 Vidyawar ta®

Peer-Reviewed International JournalJuly To Sept. 2020

Special Issue

: Interdisciplinary Multilingual Refereed Journal[dÚmdmVm © Impact Factor 3.102 (IIJIF)Impact Factor 7.041(IIJIF)

43] Impact of Covid 19 Pandemic on Global Economy as well as on Indian Economy with ...Smita Guha ||193

....................................................................................................................................................................44] Impact of Covid-19 on Employment in Various Industries

Sneha Bansode ||198....................................................................................................................................................................45] WEALTH MANAGEMENT AWARENESS IN THE MARKET

Dr. Surendra Patole ||200....................................................................................................................................................................46] dksfoM 19pk Hkkjrkrhy lq{e] y?kq o e/;e ;k mn;ksx{ks=koj >kysyk ifj.kke vH;kl.ks-

Vallabh Bharat Mudrale ||206....................................................................................................................................................................47] i;ZVu O;olk; ij dksfoM &19 dk çHkko

M‚-lfork rk;Ms ||210....................................................................................................................................................................48] INDIAN ECONOMY AND COVID–19 PANDAMIC

Dr. Sapana Lokhande ||214....................................................................................................................................................................49] dksjksuk egkekjh vkf.k Hkh"k.k lkekftd okLro

M‚- ç'kkar vkj- dkacGs ||214....................................................................................................................................................................50] A Study on Impact of Covid-19 on Indian Economy

Dr. Raj Ankush Soshte ||220....................................................................................................................................................................51] Pandemic COVID-19- As an Opportunity to Change Educational System of India

Somnath S Sanap ||227....................................................................................................................................................................52] IMPACT OF COVID – 19 PANDEMIC ON THE TOURISM INDUSTRY: A REVIEW

Priya Ramesh Yeole ||230....................................................................................................................................................................53] egkfo|ky;hu fo|kF;kZae/khy Hkkofud cqf)eÙkk ¼O;äh&varxZr tk.kho vkf.k vkarjⓈfäd-

ANKITA KUDTARKAR ||234....................................................................................................................................................................54] Repercussions of COVID-19 on Employment in India: The Case of Informal Labor Market

Anuja Sharma, A.M. Jose ||240....................................................................................................................................................................55] COVID 19 and Communications : An empirical study

Dr. Hitesh Vyas ||245....................................................................................................................................................................56] dksjksuk egkekjhpk Hkkjrkrhy f'k{k.k {ks=koj >kysyk ifj.kke

çrh{kk larks"k Hkkysdj ||248....................................................................................................................................................................

MAH MUL/03051/2012 ISSN: 2319 9318 0200 Vidyawar ta®

Peer-Reviewed International JournalJuly To Sept. 2020

Special Issue

: Interdisciplinary Multilingual Refereed Journal[dÚmdmVm © Impact Factor 3.102 (IIJIF)Impact Factor 7.041(IIJIF)

45WEALTH MANAGEMENT

AWARENESS IN THE MARKET

Dr. Surendra Patole,School of Commerce and Management,

YCMOU, Nashik

==============***********===============Abstract

Financial markets are places wherepeople and companies come to buy and sellassets like stocks, bonds, commodities and otherproducts. People have traded on financialmarkets for 100’s of years and they grew out ofa very real practical need – to help people buyand sell things more efficiently, and to helpcompanies that needed money to raise it morequickly.

The India Financial market comprise ofthe primary market, FDIs, alternative investmentoptions, banking and insurance and the pensionsectors, asset management segment as well.With all these elements in the India Financialmarket, it happens to be one of the oldest acrossthe globe and is definitely the fastest growingand best among all the financial markets of theemerging economies.

Wealthma nage rscoordinate reta i lbanking,estate planning,legalresources,taxandinvestment management. Wealth management& private banking business is currently majorarea for development for many of the world’sfinancial firms. The market is large, growing andhighly profitable. Industry is fragmented & thereis no agreed single ‘preferred’ model

The paper deals with an in – depthanalysis of awareness of wealth managementproducts in the market.

Keywords:Financial Market, WealthManagement, Estate Planning, FinancialServices, Asset Management

WEALTH MANAGEMENT AWARENESS IN THEMARKETA) Introduction

Wealth management is a service thatoffers a plethora of services comprising ofinvestment and financial advice, accounting andtaxation services, retirement planning, legal andestate planning to name a few of them. Theseservices are offered with a specific andprescribed fee. Irrespective the kind of plans forfuture we focus upon there are few factors thatneeds to be kept in mind for managing wealthfor the future such as creating of a financialplan, spending consciously, Invest wisely,diversify the investments, monitor theinvestments, plan taxes, etc to name a few ofthem. Wealth management can be provided bylarge corporate entities, independent financialadvisers or multi-licensed portfolio managerswho design services to focus on high-net-worthclients.Large banks and largebrokeragehousescreate segmentation marketing-strategies to sellboth proprietary and non-proprietary productsand services to investors designated as potentialhigh-net-worth clients. Independent wealth-managers use their experience in estateplanning, risk management, and their affiliationswith tax and legal specialists, to manage thediverse holdings of high-net-worth clients.B) Objectives of Research:

The main objectives of the research areas follows:1. To know the awareness among individual forwealth management.2. To figure out popular source of investmentavenues.C) Methodology:

Research methodology is the systematicand theoretical analysis of the methods appliedin the field of study. It involves qualitative andquantities technique. In other words, it is aprocess collecting and information for thepurpose of making business decisions. This partaims to understand the research methodology

MAH MUL/03051/2012 ISSN: 2319 9318 0201 Vidyawar ta®

Peer-Reviewed International JournalJuly To Sept. 2020

Special Issue

: Interdisciplinary Multilingual Refereed Journal[dÚmdmVm © Impact Factor 3.102 (IIJIF)Impact Factor 7.041(IIJIF)

establishing a framework of evaluation andrevaluation of primary and secondary research.The present research paper is based onsecondary as well as primary research. Thevarious sources of data include magazines,journals, news papers, websites, questionnaireetc. The information is collected and analyzed.D) Wealth Management Tools

There is variety of financial productsavailable for investors, families, etc & they areas such1. Public Provident Fund (PPF):

Any Individual, who is a resident of India,can open an account under public provident fundand earn handsome returns on the depositsrelatively higher than the returns on banks fixeddeposits.2. National Saving Certificate (NSC):

Popularly known as NSC, is an IndianGovernment Savings Bond, primarily used forsmall savings and income tax savinginvestments in India. It is part of the postalsavings system of Indian Postal Service (IndiaPost).3. RBI SAVING BOND:

RBI bond comes with a rate of interestof 7.75% which is comparable to the interestoffered on the small saving schemes such asNational Saving Certificate. The Reserve Bankof India recently announced the launch of 7.75percent Savings (taxable) Bonds, 2018 (RBIBond)4. KISAN VIKAS PATRA:

KisanVikas Patra (KVP) isa saving certificate scheme which was firstlaunched in 1998 by India Post. It was successfulin the early months but afterwardsthe Government of India set up a committeeunder supervision of ShyamalaGopinath whichgave its recommendation to the Government thatKVP could be misused. Hence the Governmentof India decided to close this scheme and KVPwas closed in 2011 and the new governmentrelaunched it in 2014.

5. POST OFFICE SMALL SAVINGS ACCOUNTS: Post Office Savings Account is the

deposit scheme offered by the department ofpost on which fixed interest is paid. Theindividual investors deposit a good portion oftheir financial assets in a postal savings accountin order to earn a fixed rate of interest on theinvestments.6. POST OFFICE TIME DEPOSIT:

The Post Office Time Deposits are asaving scheme offered by the Indian PostalService on which a fixed interest is paid. Often,the investors deposit a good chunk of theirfinancial assets with a view to earning a fixedinterest on it.7. FIVE YEAR RECURRING DEPOSIT:

Post office RD is basically a monthlyinvestment for a fixed period of 5 years with ainterest rate of 7.3% per annum (compoundedquarterly). On completion of the fixed tenure offive years, RD account with Rs. 10,000 investedevery month will fetch you Rs. 7,25,051.8. MONTHLY INCOME SCHEME:

A Monthly Income Plan (MIP) is a typeof mutual fund scheme that invests in debt andequity securities. An MIP aims to provide asteady stream of income in the form of dividendpayments. Therefore, it is typically attractive toretired persons or senior citizens without othersubstantial sources of monthlyincome. Available to most investors, MIPs arein frequent use for investors an India.9. SENIOR CITIZEN SAVINGS SCHEME:

An individual of the age of 60 or more,being the citizen of Indiacan open the SCSSaccount.

Also, the individual of the age of 55years but less than 60 years, who has retiredon superannuation or VRS can also invest in thescheme provided the account is opened withinone month of retirement benefits and theamount not exceeding the retirement benefitamount.10. BHAVISHYA NIRMAN BONDS:

MAH MUL/03051/2012 ISSN: 2319 9318 0202 Vidyawar ta®

Peer-Reviewed International JournalJuly To Sept. 2020

Special Issue

: Interdisciplinary Multilingual Refereed Journal[dÚmdmVm © Impact Factor 3.102 (IIJIF)Impact Factor 7.041(IIJIF)

The times are uncertain and investorsentiment tends to lean towards debt, mostcommonly bank fixed deposits (FD). But there’sa catch. FD rates vary as per the interest ratesin the economy. And with Reserve Bank ofIndia’s recent liquidity infusing measures, somebanks are considering lowering their depositrates. A better option - BhavishyaNirman bonds11. BANK SAVING ACCOUNT:

A savings account is an interest-bearingdeposit account held at a bank or other financialinstitution that provides a modest interest rate.Financial institutions that offer savings accountsmay limit the number of withdrawals from anaccount each month. They also may charge feesunless you maintain a certain average monthlybalance in the account. In most cases, banks donot provide checks with savings accounts.12. FIXED DEPOSIT ACCOUNT:

Fixed deposits are investmentinstruments offered by banks and non-bankingfinancial companies, where you can depositmoney for a higher rate of interest than savingsaccounts. You can deposit a lump sum of moneyin fixed deposits for a specific period, rangingfrom 7 days to 10 years. 13. DEPOSIT SCHEME FOR RETIRINGGOVERNMENT EMPLOYEES:(a) Any depositor may open an account withany accounts office within three months fromthe date of receiving the retirement benefits fordepositing the amount not exceeding the totalretirement benefits, by applying in Form 1, oras near thereto as possible, together with— (i) a locally executed cheque, pay orderor demand draft, for the amount of deposit, and (ii) a certificate from the employerindicating retirement benefits provided that adepositor who has received the retirementbenefits before the notification of this Scheme,may open an account within three months fromthe date of commencement of the scheme.14. DEPOSIT SCHEME FOR RETIRING PUBLICSECTOR EMPLOYEES:

This Scheme may be called Deposit Scheme forRetiring Employees of Public Sector Companies,1991.(a) Any depositor may open an account withany accounts office within three months fromthe date of receiving the retirement benefits orup to 30-9-1991, whichever is later, fordepositing the amount not exceeding the totalretirement benefits, by applying in Form 1, oras near thereto as possible together with:

(i) a locally payable cheque, pay orderor demand draft, for the amount of deposit, and

(ii) a certificate from the employerindicating retirement benefits:15. MUTUAL FUND:

A mutual fund is a professionallymanaged investment fund that pools moneyfrom many investors to purchase securities.These investors may be retail or institutional innature.Mutual funds have advantages anddisadvantages compared to direct investing inindividual securities. The primary advantages ofmutual funds are that they provide economiesof scale, a higher level of diversification, theyprovide liquidity, and they are managed byprofessional investors. On the negative side,investors in a mutual fund must pay various feesand expenses.16. ANTIQUE:

If you have money to invest and anappreciation of fine craftsmanship, theninvesting in antique art might be the right choicefor you. Antiques are collectible objects suchas furniture or artwork that have a high valuedue to their age, quality, and rarity.17. ART:

These days, many long-term investorslook to diversify their portfolios by investing indifferent, even exotic, asset classes. Some preferto put their money in rare coins and jewels,while others invest in fine wines. Oneinvestment class quickly gaining in popularityis artwork. Not only can fine art enhance yourhome décor and evoke powerful emotions, it can

MAH MUL/03051/2012 ISSN: 2319 9318 0203 Vidyawar ta®

Peer-Reviewed International JournalJuly To Sept. 2020

Special Issue

: Interdisciplinary Multilingual Refereed Journal[dÚmdmVm © Impact Factor 3.102 (IIJIF)Impact Factor 7.041(IIJIF)

appreciate in value simply by hanging on yourliving room wall.18. BOOKS:

A book is a number of pieces of paper,usually with words printed on them, which arefastened together and fixed inside a cover ofstronger paper or cardboard. Books containinformation, stories, or poetry.19. CLOCK & WATCHES:

With interest rates showing no signs ofimproving, investors’ options are limited to onlya few avenues which will prove beneficial in thelong term. Property, collectable cars, wine andart are all good options, but one of the mostinviting and potentially lucrative is watches.20. DIAMOND:

A precious stone consisting of a clearand colourless crystalline form of pure carbon,the hardest naturally occurring substance”adiamond ring”21. GOLD:

Safety, Liquidity and Returns are thethree criteria most conventional investors lookfor before making any investment. While goldmeets the first two criteria swimmingly, itdoesn’t do badly at the last one either. Here aretwo main reasons why you should invest in gold:

a. Gold investment is worthwhilebecause it is an inflation-beating investment.Over a period of time, the return on goldinvestment is in line with the rate of inflation.

b. Gold has an inverse relationship toequity investments. Example, if the equitymarkets start performing poorly, gold too wouldhave performed well. Considering gold as aninvestment option in your investment portfoliowill be a buffer to the overall volatility of yourportfolio.22. SILVER:

A precious shiny greyish-white metal,the chemical element of atomic number 47"asilver necklace”23. PLATINUM:

A precious silvery-white metal, thechemical element of atomic number 78. It wasfirst encountered by the Spanish in SouthAmerica in the 16th century, and is used injewellery, electrical contacts, laboratoryequipment, and industrial catalysts.24. FARM HOUSE:

Farm House living has become a newtrend in India. Urbanites have increasingly begunto invest in farms and farm houses away fromcities for more reasons than one. It is a largehouse set in the middle of a farm, typically witha landscaped garden around it. Farm house isalso called a Country House. Farm Houses cometypically away from one’s urban residence.Generally, farm house owners use their farmhouse as their exclusive private resort as andwhen they the urge to take a break from thehustle and bustle of city life overwhelms them.It follows that farm houses do not necessarilymean rustic in architecture. They can bedesigned as you wish. You can choose to give acontemporary architecture to your farm houseand equip it with modern amenities of yourchoice as well.25. PROPERTY:

A thing or things belonging to someone;possessions collectively.Income properties canbe residential properties, such as single familyhomes or multi-family properties, or they can becommercial properties, such as a strip mall.Money is generally made through holding theproperty and renting it out or selling the propertyafter the value of the property has appreciated.26. HORSE:

A stalking-horse bid is an initial bid onthe assets of a bankrupt company. The bankruptcompany will choose an entity from a pool ofbidders who will make the first bid on the firm’sremaining assets. The stalking horse sets thelow-end bidding bar so that other bidders cannotunderbid the purchase price. The term “stalkinghorse” originates from a hunter trying to concealhimself behind either a real or fake horse.

MAH MUL/03051/2012 ISSN: 2319 9318 0204 Vidyawar ta®

Peer-Reviewed International JournalJuly To Sept. 2020

Special Issue

: Interdisciplinary Multilingual Refereed Journal[dÚmdmVm © Impact Factor 3.102 (IIJIF)Impact Factor 7.041(IIJIF)

27. VINTAGE CARS:Vintage cars date back at least 15 to 25

years, but more importantly, possess somequality that makes them interesting to collect.This may include unusual designs and limitedproduction runs. The rarer the car, the morevaluable it is likely to be. Cars more than a centuryold fall into the separate category of antiques.Asyou would for any investment, research whatyou are interested in buying carefully. Weigheach deal independently and make a sounddecision. That means finding a car that meetsyour budget, is in good shape and is likely tohave strong resale value.E) DATA ANAYLSIS1. Gender

Interpretation: The sample size is of 40 nos.which consist of 23.5% female and 76.50 % malerespondents.2. Age group

Interpretation: Above chart shows that majorityof respondents are from age group from 20 -40.3. Marital Status

Interpretation: Out of respondent contacted70.6% are unmarried.4. Profession

Interpretation: The data presented above clearlyindicates that 88.2% are attached to servicesector, 5.9% are self-employed.5. Invest

Female 23.50%

Male 76.50%

Age Respondents 20-25 35.30% 25-40 64.70% 40-60 0.00% 60 above 0.00%

Married 29.4% Unmarried 70.6% Divorce 0

Student 0%

Service 88.2%

Self Employed 5.9%

other 5.9%

MAH MUL/03051/2012 ISSN: 2319 9318 0205 Vidyawar ta®

Peer-Reviewed International JournalJuly To Sept. 2020

Special Issue

: Interdisciplinary Multilingual Refereed Journal[dÚmdmVm © Impact Factor 3.102 (IIJIF)Impact Factor 7.041(IIJIF)

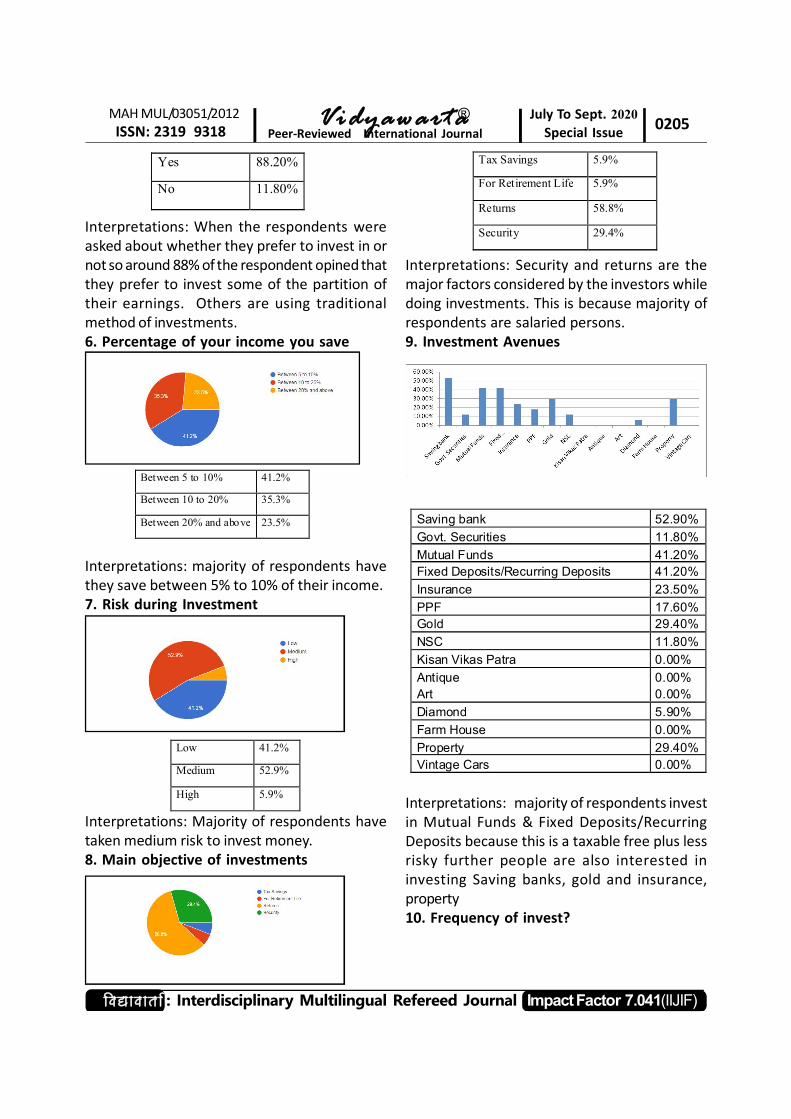

Interpretations: When the respondents wereasked about whether they prefer to invest in ornot so around 88% of the respondent opined thatthey prefer to invest some of the partition oftheir earnings. Others are using traditionalmethod of investments.6. Percentage of your income you save

Interpretations: majority of respondents havethey save between 5% to 10% of their income.7. Risk during Investment

Interpretations: Majority of respondents havetaken medium risk to invest money.8. Main objective of investments

Interpretations: Security and returns are themajor factors considered by the investors whiledoing investments. This is because majority ofrespondents are salaried persons.9. Investment Avenues

Interpretations: majority of respondents investin Mutual Funds & Fixed Deposits/RecurringDeposits because this is a taxable free plus lessrisky further people are also interested ininvesting Saving banks, gold and insurance,property10. Frequency of invest?

Yes 88.20%

No 11.80%

Between 5 to 10% 41.2%

Between 10 to 20% 35.3%

Between 20% and above 23.5%

Low 41.2%

Medium 52.9%

High 5.9%

Tax Savings 5.9%

For Retirement Life 5.9%

Returns 58.8%

Security 29.4%

Saving bank 52.90% Govt. Securities 11.80% Mutual Funds 41.20% Fixed Deposits/Recurring Deposits 41.20% Insurance 23.50% PPF 17.60% Gold 29.40% NSC 11.80% Kisan Vikas Patra 0.00% Antique 0.00% Art 0.00% Diamond 5.90% Farm House 0.00% Property 29.40% Vintage Cars 0.00%

MAH MUL/03051/2012 ISSN: 2319 9318 0206 Vidyawar ta®

Peer-Reviewed International JournalJuly To Sept. 2020

Special Issue

: Interdisciplinary Multilingual Refereed Journal[dÚmdmVm © Impact Factor 3.102 (IIJIF)Impact Factor 7.041(IIJIF)

Interpretations: majority of respondents investmonthly and this is a good habit of investing or saving,some peoples are investing on half yearly and yearlyalso as per their part of investing planning.F) CONCLUSION

Wealth management is a form of financialservices provided to wealthy clients mainly to theindividuals and their families. Over the years, marketshave grown bigger and faster. More people than everbefore are now able to get access to these markets. Oncethey were the preserve of big banks, finance housesand very wealthy individuals, but no longer.

From the above analysis, we can say thatmajority of respondents are from service sectors.1. Majority of respondents are unmarried so their

monthly expenses are less compared to marriedindividual. They have more money for investing.

2. While investing they consider safety, returns andliquidity as their priority for investment with lowrisk.

3. This survey conducted due to understandinginvestment behaviour of general people withthe exotic investment behaviour.

4. They follow the traditional method ofinvestments and additions to it they invest insaving accounts and mutual funds.

REFRENCES1. Paripex, Indian Journal of Research.2. Investment Management, http://www.

investopedia.com3. Investment book – TATA McGraw hill.4. https://businessjargons.com5. www.policybazar.com6. https://www.wealthmanagement.com

Monthly 52.9% Quarterly 0% Half Yearly 11.8% Yearly 35.3%

46

dksfoM 19pk Hkkjrkrhy lq{e]y?kq o e/;e ;k mn;ksx{ks=koj>kysyk ifj.kke vH;kl.ks-

Mr. Vallabh Bharat Mudrale.Assistant Professor in CommerceSNDT Arts and Commerce Collage

for Women, Pune

==============***********===============Lkkjk a’k%&

vkt laiq.kZ tx ,d dBh.k dkGkrqutkr vkgs- dksfoM&19 P;k fo”kk.kqeqGs laiq.kZtxkyk xzklys vkgs ifj.kkeh yksdkaps thou vkf.kçR;sd ns’kkph vFkZO;oLFkk dksyeMyh vkgs-dksfoM&19 gh 2020 eèkhy egkvkiÙkh iSdh,d vkiÙkh vkgs- vkf.k ;k vkiÙkhpk ifj.kkeiw.kZi.ks vfuf’pr o vuvisf{kr vkgs- ;k la’kksèkufucaèkkpk mn~ns’k Hkkjrkrhy lq{e] y?kq o eè;em|ksxkaoj >kysyk ifj.kke vH;kl.ks gk vkgs-MSME {ks= gs vFkZO;oLFksph thouokfguh vkgs-l kF k h P; k dkykoè k k h u arj MSME P; kiqUuthouklkBh dk; j.kuhrh vlsy] Make InIndia, Lokoyach gs LoIu lkdkj dj.;klkBhHkkjrkus dks.kR;k fHkUu mik;;kstuk djkO;kr\;kapk vH;kl dsY;kuarj laèkksèkudR;kZyk vk<Gysdh Hkkjrh; MSME O;olk; iènrh iq.kZi.kscnyY;k tkrhy- lkFkhP;k vktkjkuarj fMftVyiènrhpk voyac] uouohudYiuk fLodkj.ks]foÙkiqjoBk dj.ks] u¶;k,soth jks[k¼ iS’kkP;k½çokgkoj y{k dsaæhr dj.ks vko’;d vlsyMSME lkBh 3 yk[k dksVh ir geh tkghjdsY;kus MSME {ks=kyk R;kapk uôhp Qk;nk gksbZy-

![International Standard Serial Number (ISSN): 2319 …ijupbs.com/Uploads/25. RPA130096.pdfInternational Standard Serial Number (ISSN): 2319-8141 Ocimum sanctum [48] (Lamiaceae) Ethanolic](https://static.fdocuments.in/doc/165x107/5e5486d9a3e5e369735207a1/international-standard-serial-number-issn-2319-rpa130096pdf-international.jpg)