Vastned Q1 2014 update

32

Vastned Focus on growth in premium city high street shop June 2014 Taco de Groot, CEO Vastned

-

Upload

annekehoijtink -

Category

Investor Relations

-

view

56 -

download

0

Transcript of Vastned Q1 2014 update

Vastned Focus on growth in premium city high street shopsJune 2014Taco de Groot, CEO Vastned

Vastned makes significant progress in executing the premium city high street strategy

Occupancy rate increased from 94.0% year-end 2013 to 96.5% end of Q1 2014

Premium city high street shops: 99.1%

High street shops: 95.1% Non-high street shops: 94.0%

Estimated 2014 direct investment result between € 2.10 - € 2.30 per share

2

Divestments increase quality of the portfolio

Total divestments in Q1 2014: € 48.7 million

Sale of Spanish shopping centres/galleries and retail park successfully finalised

Leasing activity includes 31 leases and amounts to € 2.2 million

Share of non-bank loans increased to over 30%

Successful placement of convertible bond of € 110 million

Q1 2014 update: Vastned’s premium city strategy improves occupancy rate

Occupancy rate increases from 94.0% to 96.5%

4

Total portfolio € 1.5 billion

Premium city high

street shops

High street shops

Non-high

street shops

Total

% % % %

The Netherlands 97.8 95.2 95.8 96.1

France 99.9 100 72.9 96.8

Belgium 98.7 89.7 95.2 95.3

Spain/ Portugal 100 100 100 100

Turkey 100 n.a. n.a. 100

Total 99.1 95.1 94.0 96.5

Leasing activity in Q1 2014 amounts to € 2.2 million

Total leasing activity € 2.2 million

A total of 31 lease contracts were signed

On average leasing contracts were signed 4.6% below old rents mainly due to rent declines in shopping centers in Tongeren and Limoges

Premium city high street shop leases at 7.4% higher rents

5

Premium city high street

shops

High street shops

Non-high street shops

Total

Leasing activity € 0.8 million € 0.9 million € 0.5 million € 2.2 million

Change in rent on new and renewed

leases7.4% 6.7% (33.3)% (4.6)%

Leasing activity in Q1 2014

Divestments increase the quality of the portfolio

Total divestments in Q1 2014: € 48.7 million Netherlands: € 0.6 million France: € 45.2 million Belgium: € 2.9 million

On average 2.6% below book value year-end 2013

Share of premium city high street shops increases from 51% to 52%

Occupancy rate improves significantly from 94.0% to 96.5%

6

Divestment Spanish shopping centres/galleries and retail park successfully finalised

Seven shopping centres/galleries and one retail park Average occupancy rate of the sold assets: 84.5% Leasing activity in 2013 on average at 33% lower rents Selling price: € 160 million Net sales proceeds: € 157.9 million

Current Spanish portfolio*: € 63 million Occupancy rate at end Q1 2014: 100%

7

* Including the Portuguese portfolio

Q1 2014 country performance

The Netherlands: Market remains a challenge for retailers

9

Dutch consumer confidence improves slightly but still low

19 leases signed for € 1.1 million: Credo Men’s fashion De Tuinen MANGO

New leases and lease renewals result in 8.7% rent increase

Divestment of non-strategic assets for € 0.6 million

Occupancy rate slightly lower from 96.8% year-end 2013 to 96.1% end Q1 2014

Developments in Q1 2014

Dutch portfolio: € 623 million Year-end 2013

France: Share of premium city high street shops increases to 77%

10

Polarisation in the French retail market

4 leases signed for a total of € 0.1 million, including 2 leases for shopping centre Corgnac in Limoges

Total divestments: € 45.2 million

Occupancy increases from 95.4% year-end 2013 to 96.8% end Q1 2014

Developments in Q1 2014

French portfolio: about € 310 million After divestments in Q1 2014

Belgium: Stable progress

11

Leasing activity € 0.3 million including 7 contracts of which two in shopping centre Julianus in Tongeren

Divestment of non-strategic assets for € 2.9 million

Occupancy rate stable at 95.3% end Q1 2014 (year-end 2013: 95.4%)

Developments in Q1 2014Belgian portfolio: about € 360 million After divestments in Q1 2014

Spain: Focus on premium city high street shops

12

Successful finalisation of the Spanish shopping centres and retail park at the end of Q1 2014

Occupancy rate improves from 86.6% year-end 2013 to 100% end Q1 2014

Developments in Q1 2014

Spanish/Portuguese portfolio: about € 63 million after divestments

Turkey: Stable results Q1 2014

13

Lease renewal with Topshop for Istiklal Caddesi 18 with 4.6% rent increase

Stable occupancy rate at 100%

Developments in Q1 2014

Turkish portfolio: € 129 million Year-end 2013

Strategy update: Focus on growth in premium city high streets

Sharpened high street strategy: Focus on growth in premium cities

Premium city high street shops have the highest preference of retailers and consumers

Premium cities are selected cities with: Positive demographic development Strong purchasing power Historic inner city Tourist destination Presence of national and international

institutions and universities

Growth of high street shops in premium cities to 75% of the total portfolio

15

Strong performance premium city high street shops

In %

Premium city high street

shops

High street shops

Non high street shops Total

Spot occupancy

end Q1 201499.1 95.1 94.0 96.5

2013 Like-for-like rental

growth 4.2 (1.1) (3.6) (1.1)

2013 Value movements* 2.2 (2.0) (13.7) (5.8)

16

* Excluding acquisitions

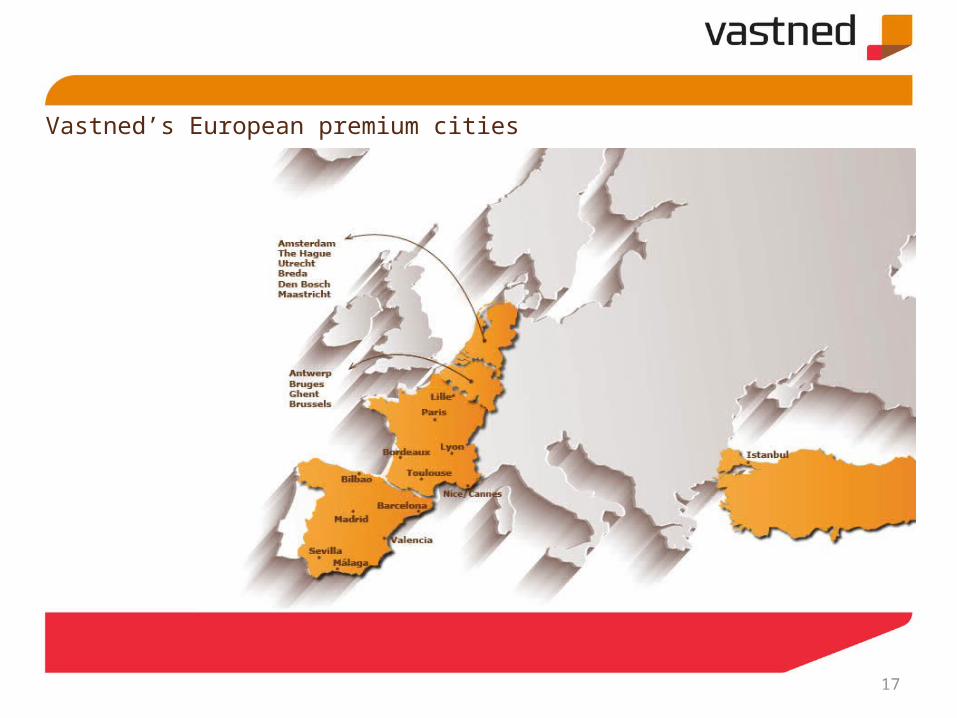

Vastned’s European premium cities

17

Examples of execution of premium city high street strategy

19

Realisation upwards potential: 42% rent increase

P.C. Hooftstraat 49-51

Old tenant New tenant

Old rent € 317,000 per year

Retailer Hugo Boss

New rent € 450,000 per year

Duration 10 years

Rent increase + 42%

RetailersSchaap en Citroen and

IWC Schaffhausen

Vastned increases footprint in historical inner city of Utrecht

20

€ 59 million 17 high street shops

Property portfolio Utrecht

Vastned creates cluster of high street shops in Golden Triangle of Bordeaux

21

€ 84 million 17 high street shops

Property portfolio Bordeaux

2013 financial results

Despite difficult retail market positive like-for-like gross rental growth for premium city high street shops

Premium city high streets

High street other Other Total

portfolio

% % % %

The Netherlands 4.8 (0.6) (3.9) (1.1)

France 3.8 (4.9) 1.0 0.6

Belgium 0.4 1.4 2.0 1.4

Spain/ Portugal 18.8 3.4 (6.8) (4.7)

Turkey 3.3 n.a. n.a. 3.3

Total 4.2 (1.1) (3.6) (1.1)

23

Positive value movements for premium city high street shops in 2013

ValuePremium city high streets

High street other

Other Total

In € million % % % %

The Netherlands 623 1.9 (5.7) (5.3) (3.7)

France 359 1.7 (0.8) (3.1) (0.4)

Belgium 362 8.2 9.6 6.2 7.6

Spain/Portugal 221* 0.6 (4.5) (39.8) (33.2)

Turkey 129 (1.8) n.a. n.a. (1.8)

Total 1.694 2.2 (2.0) (13.7) (5.8)

24

* After the divestment of the seven shopping centres/galleries and the retail park in Spain the value of the portfolio will be € 63 million.

Divestment of non-strategic assets resulted in lower rental income

25

Annualised rent

(€ 1 million)

Annualised

rent e

nd Q4 2012

Loss

of tenan

ts

New Le

ttings

Acquisiti

ons and tr

ansfe

r fro

m pipeline

Divestm

ents

Other

Annualised

rent e

nd Q4 2013

105000000.000

110000000.000

115000000.000

120000000.000

125000000.000

130000000.000

135000000.000

140000000.000

145000000.000

150000000.000

134.6(8.7) 7.8

6.5 (19.2)

0.0 121.0

Strong financial position

26

Roll over 2014 2015 2016 2017 2018 20190

50

100

150

200

250

300

Contract revision by year

Interest revision by year

Average interest rate

1.6%

3.8%

4.9%

4.8%

4.4% 4.2%

4.9%

5.3%

Average interest rate year-end 2013: 4.3%

Interest cover ratio year-end 2013: 2.8

Loan to value: 39.7% after sale Spanish shopping centres/galleries

Significant risk profile improvement

Current unused credit facility more than € 200 million

Total amount of non-bank loans over 30% after placement of € 110 million convertible

2020 ev.

At year-end 2013

Successful placement of convertible bond of € 110 million

Key points: Total placement: € 110 million 30% above reference price Interest coupon: 1.875% Duration: five year

Result: Over 30% non-bank loans Improved negotiation position towards other financiers Contributes to lower average financing costs

27

Net divestments improved quality of the portfolio and reduced direct investment result 2013

In € million FY 2013 FY 2012 Δ

Gross rental income 123.2 133.5 (10.3)

Operating expenses (16.5) (17.8) 1.3

Net financing costs (34.4) (35.9) 1.5

General expenses/taxes (11.3) (10.5) (0.8)

Non-controlling interests (6.8) (6.7) (0.1)

Direct investment result 54.2 62.6 (8.4)

28

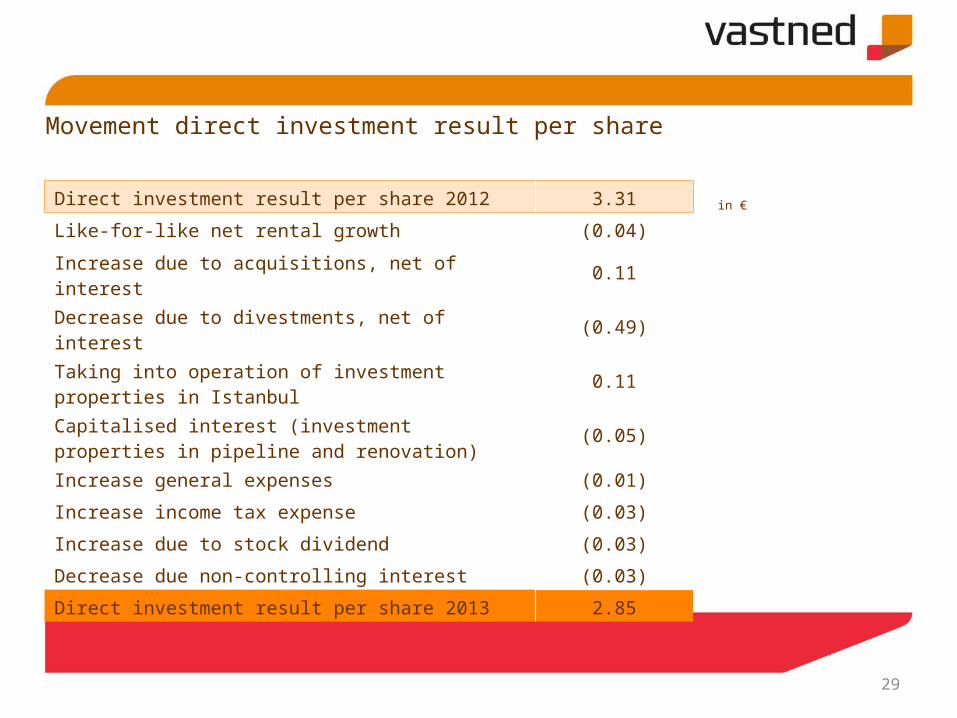

Movement direct investment result per share

in €Direct investment result per share 2012 3.31

Like-for-like net rental growth (0.04)

Increase due to acquisitions, net of interest 0.11

Decrease due to divestments, net of interest (0.49)

Taking into operation of investment properties in Istanbul

0.11

Capitalised interest (investment properties in pipeline and renovation)

(0.05)

Increase general expenses (0.01)

Increase income tax expense (0.03)

Increase due to stock dividend (0.03)

Decrease due non-controlling interest (0.03)

Direct investment result per share 2013 2.85

29

Outlook 2014: Improved quality portfolio enables forecast for 2014 direct investment result Vastned will continue to pragmatically execute the premium city high street

strategy with focus on growth in premium cities

Execution of the strategy has significantly improved quality of the portfolio to more stable and predictable results

As announced before, the premium city high street strategy will lead to lower direct investment result in the short term, but to more stable and predictable results in the long term

Current quality of the portfolio provides sufficient ground to estimate direct investment result per share 2014 between € 2.10 - € 2.30, barring unforeseen circumstances

30

Dividend 2013: € 2.55 per share

Total dividend: € 2.55 per share Pay-out ratio: 89% Ex-dividend date: 19 May 2014 Payment date final dividend: 29 May 2014 Dividend policy unchanged:

pay-out ratio at least 75% of the direct investment result

31

Contact details

Vastned Investor Relations

Anneke Hoijtink

+ 31 10 24 24 368

+ 31 6 31637374

www.vastned.com

32

![Result Update Presentation Q1 FY 16 [Company Update]](https://static.fdocuments.in/doc/165x107/577cb2961a28aba7118c175a/result-update-presentation-q1-fy-16-company-update.jpg)