VAR Order Selection - univie.ac.athomepage.univie.ac.at/robert.kunst/pres07_var_abdgunyan.pdf · A...

46

Introduction A Sequence of Tests for Determining the VAR Order Criteria for VAR Order Selection Comparison of Order Selection Criteria VAR Order Selection Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan Vector Autoregressive Models January 16th 2008 Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

Transcript of VAR Order Selection - univie.ac.athomepage.univie.ac.at/robert.kunst/pres07_var_abdgunyan.pdf · A...

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

VAR Order Selection

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan

Vector Autoregressive Models

January 16th 2008

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Agenda

1 Introduction

2 A Sequence of Tests for Determining the VAR OrderThe Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

3 Criteria for VAR Order SelectionMinimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

4 Comparison of Order Selection Criteria

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Agenda

1 Introduction

2 A Sequence of Tests for Determining the VAR OrderThe Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

3 Criteria for VAR Order SelectionMinimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

4 Comparison of Order Selection Criteria

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Agenda

1 Introduction

2 A Sequence of Tests for Determining the VAR OrderThe Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

3 Criteria for VAR Order SelectionMinimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

4 Comparison of Order Selection Criteria

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Agenda

1 Introduction

2 A Sequence of Tests for Determining the VAR OrderThe Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

3 Criteria for VAR Order SelectionMinimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

4 Comparison of Order Selection Criteria

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Contrary to the simplifying assumption throughout chapters 1to 3 in Lutkepohl’s (2005) textbook, the lag order of a vectorautoregressive (VAR)(p) process is usually unknown.

However, one should be interested to know the true lag orderbecause it can be shown that the (approximate) mean squarederror (MSE) matrix of the one-step ahead predictor increaseswith lag order p.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

In other words: if the chosen – or the assumed – lag order isunnecessarily large, the forecast precision of the correspondingVAR(p) model will be reduced. Therefore, it is useful to havecertain procedures or criteria for choosing the adequate lagorder p.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

In order to do so, there are several possibilities:

• One could try to visually inspect correlograms (assuggested by Box/Jenkins) similar to the univariate caseto determine p. However, this method does not appear tobe useful in the multivariate case.

• An alternative would be to run so-called diagnostic tests,which means that a lag is to be chosen such that theresiduals of the process pass diagnostics. But thisempirically turned out to be the least reliable approach.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

• A more reasonable suggestion is to run statistical testswith the hypothesis that a certain lag equals zero. Someexamples for this kind of hypothesis tests would be thelikelihood ratio statistic or approximations thereof such asthe Wald F statistic or the LM statistic (see e.g.Wooldridge 2006).

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

• The last and maybe the most elaborated way of copingwith the problem of choosing the right lag order is to useinformation criteria (IC). The common underlyingprinciple of these IC is that each of them minimizes theMSE. Predictors that minimize the MSE are optimalpredictors in case the loss of the forecasters can beapproximated by squares.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

In the following, we will skip the first and the second methodmentioned above as they do not seem to be very accurate andconcentrate on the third and the fourth one.

Afterwards, we will evaluate the discussed approaches andpresent a simple empirical example.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

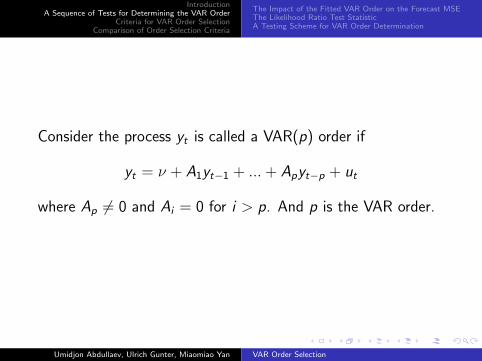

Consider the process yt is called a VAR(p) order if

yt = ν + A1yt−1 + ... + Apyt−p + ut

where Ap 6= 0 and Ai = 0 for i > p. And p is the VAR order.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

From previous section, we know

Σy(1) =T + Kp + 1

TΣu

Obviously, Σy(1) is an increasing function of the order of themodel fitted to the data.

Empirically, forecast from lower order models are clearlysuperior to higher order models.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

Assume yt is a stable Gaussian (normally distributed) VAR(p)process, and its log-likelihood function is

ln `(β, Σu) =− KT

2ln2π − T

2ln|Σu|

− 1

2[y − (Z ′ ⊗ Ik)β]′(IT ⊗ Σ−1

u )[y − (Z ′ ⊗ Ik)β]

∂ln`

∂β= (Z ⊗ Σ−1

u )y − (ZZ ′ ⊗ Σ−1u )β

Equating to zero gives the unrestricted ML estimator

β = ((ZZ ′)−1Z ⊗ IK )y

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

Suppose the restrictions on β are

Cβ = c

where C is a known (N × (K 2p + K )) matrix of rank N and cis a known (N × 1) vector. The restricted ML estimator can

be found by Lagrangian approach.

L(β, γ) = ln`(β) + γ′(Cβ − c)

∂L∂β

= (Z ⊗ Σ−1u )y − (ZZ ′ ⊗ Σ−1

u )β + C ′γ

∂L∂γ

= Cβ − c

βr = β + [(ZZ ′)−1 ⊗ Σu]C′[C ((ZZ ′)−1 ⊗ Σu)C

′]−1(c − C β)

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

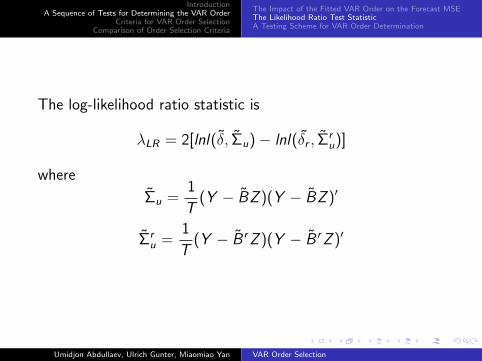

The log-likelihood ratio statistic is

λLR = 2[lnl(δ, Σu)− lnl(δr , Σru)]

where

Σu =1

T(Y − BZ )(Y − BZ )′

Σru =

1

T(Y − B rZ )(Y − B rZ )′

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

Proposition: Let yt be a stationary, stable VAR(p) processwith standard white noise ut . (Here, yt is not necessarilyGaussian) β and βr are the (quasi) ML and restricted (quasi)ML estimators. Then the log-likelihood ratio test statistic is

λLR = 2[ln `(δ, Σu)− ln `(δr , Σru)]

= T (ln |Σru| − ln |Σu|) (1)

= (βr − β)′(ZZ ′ ⊗ (Σru)−1)(βr − β) (2)

= (βr − β)′(ZZ ′ ⊗ Σ−1u )(βr − β) + op(1) (3)

= (C β − c)′[C ((ZZ ′)−1 ⊗ Σu)C′]−1(C β − c) + op(1) (4)

= (C β − c)′[C ((ZZ ′)−1 ⊗ Σru)C

′]−1(C β − c) + op(1) (5)

andλLR

d→ χ2(N)

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

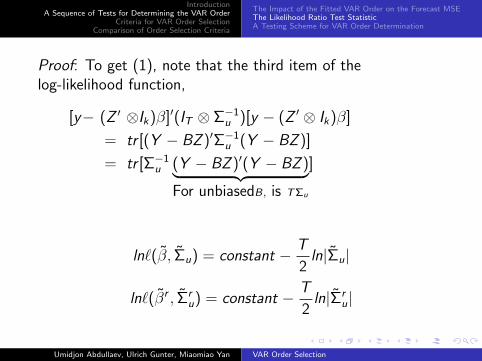

Proof: To get (1), note that the third item of thelog-likelihood function,

[y− (Z ′ ⊗Ik)β]′(IT ⊗ Σ−1u )[y − (Z ′ ⊗ Ik)β]

= tr [(Y − BZ )′Σ−1u (Y − BZ )]

= tr [Σ−1u (Y − BZ )′(Y − BZ )︸ ︷︷ ︸

For unbiasedB, is TΣu

]

ln`(β, Σu) = constant − T

2ln|Σu|

ln`(βr , Σru) = constant − T

2ln|Σr

u|

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

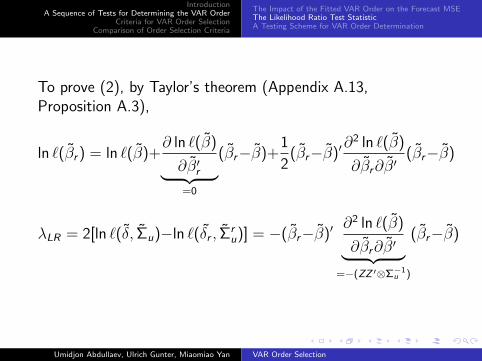

To prove (2), by Taylor’s theorem (Appendix A.13,Proposition A.3),

ln `(βr ) = ln `(β)+∂ ln `(β)

∂β′r︸ ︷︷ ︸=0

(βr−β)+1

2(βr−β)′

∂2 ln `(β)

∂βr∂β′(βr−β)

λLR = 2[ln `(δ, Σu)−ln `(δr , Σru)] = −(βr−β)′

∂2 ln `(β)

∂βr∂β′︸ ︷︷ ︸=−(ZZ ′⊗Σ−1

u )

(βr−β)

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

plim(Σu − Σru) = 0 can be used to show (3).

To get (4) and (5), from the formula of βr ,

λLR = (C β − c)′[C ((ZZ ′)−1 ⊗ Σu)C′]−1

×C ((ZZ ′)−1 ⊗ Σu)((ZZ ′)⊗ Σ−1u )((ZZ ′)−1 ⊗ Σu)C

′

×[C ((ZZ ′)−1 ⊗ Σu)C′]−1(C β − c)

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

The asymptotic distribution ofλLR follows

Proposition C.15(5): Suppose β is an estimator of the

(K × 1) vector β with√

T (β − β)d→ N (0, Σ). If Σ is

nonsingular and plimΣ = Σ, then

T (β − β)′Σ−1(β − β)d→ χ2(K ).

Here, (ZZ ′/T )−1⊗ Σru is a consistent estimator of Γ−1⊗Σu.�

Alternatively, one may consider using the statistic

λLR/Nd→ F (N , T − Kp − 1)

in small samples.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

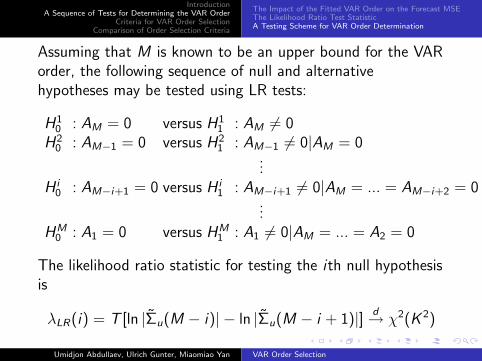

Assuming that M is known to be an upper bound for the VARorder, the following sequence of null and alternativehypotheses may be tested using LR tests:

H10 : AM = 0 versus H1

1 : AM 6= 0H2

0 : AM−1 = 0 versus H21 : AM−1 6= 0|AM = 0

...H i

0 : AM−i+1 = 0 versus H i1 : AM−i+1 6= 0|AM = ... = AM−i+2 = 0

...HM

0 : A1 = 0 versus HM1 : A1 6= 0|AM = ... = A2 = 0

The likelihood ratio statistic for testing the ith null hypothesisis

λLR(i) = T [ln |Σu(M − i)| − ln |Σu(M − i + 1)|] d→ χ2(K 2)

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

It is important to realize that the significance levels ofindividual tests must be distinguished from the Type I error ofthe whole procedure, because rejection of H i

0 means H i+10 , ...,

HM0 are automatically rejected. Denoting

Di ... H j0 is rejected in the jth test when it is actually true.

εi ... the probability of a Type I error for the ith test.

εi = Pr(D1 ∪ D2 ∪ ... ∪ Di)

γj ... the significance level of the jth individual test.

γj = Pr(Dj)

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

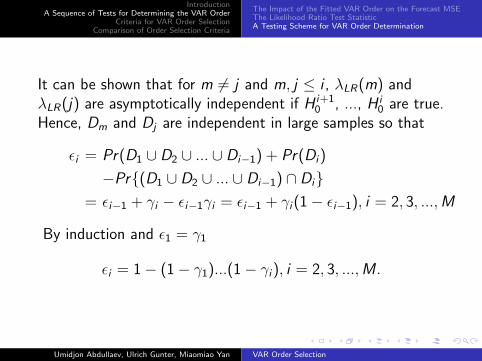

It can be shown that for m 6= j and m, j ≤ i , λLR(m) andλLR(j) are asymptotically independent if H i+1

0 , ..., H i0 are true.

Hence, Dm and Dj are independent in large samples so that

εi = Pr(D1 ∪ D2 ∪ ... ∪ Di−1) + Pr(Di)

−Pr{(D1 ∪ D2 ∪ ... ∪ Di−1) ∩ Di}= εi−1 + γi − εi−1γi = εi−1 + γi(1− εi−1), i = 2, 3, ..., M

By induction and ε1 = γ1

εi = 1− (1− γ1)...(1− γi), i = 2, 3, ..., M .

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

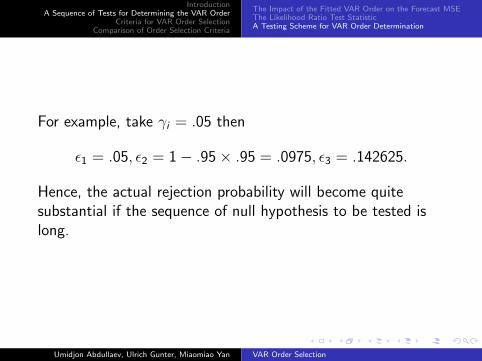

For example, take γi = .05 then

ε1 = .05, ε2 = 1− .95× .95 = .0975, ε3 = .142625.

Hence, the actual rejection probability will become quitesubstantial if the sequence of null hypothesis to be tested islong.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The Impact of the Fitted VAR Order on the Forecast MSEThe Likelihood Ratio Test StatisticA Testing Scheme for VAR Order Determination

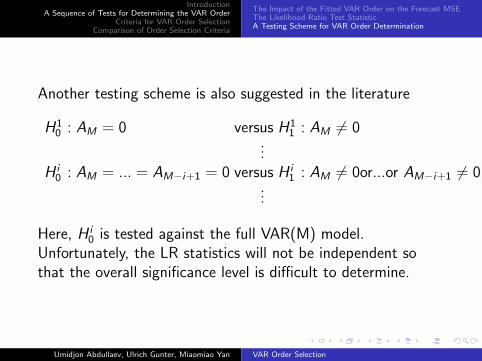

Another testing scheme is also suggested in the literature

H10 : AM = 0 versus H1

1 : AM 6= 0...

H i0 : AM = ... = AM−i+1 = 0 versus H i

1 : AM 6= 0or...or AM−i+1 6= 0...

Here, H i0 is tested against the full VAR(M) model.

Unfortunately, the LR statistics will not be independent sothat the overall significance level is difficult to determine.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Minimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

For prediction purposes, it may not be necessary to find thecorrect lag order p of the data generation process (DGP) asdone by running hypothesis tests because

• one does not automatically obtain a good model forprediction by using hypothesis testing,

• and hypothesis testing as such can have the backdrawthat, with positive probability, one chooses the incorrectlag order even though the time-series length is large.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Minimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

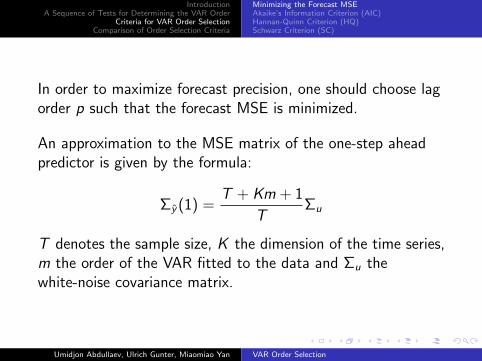

In order to maximize forecast precision, one should choose lagorder p such that the forecast MSE is minimized.

An approximation to the MSE matrix of the one-step aheadpredictor is given by the formula:

Σy(1) =T + Km + 1

TΣu

T denotes the sample size, K the dimension of the time series,m the order of the VAR fitted to the data and Σu thewhite-noise covariance matrix.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Minimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

However, we do not know Σu.

⇒ We have to estimate it:

Σu(m) =T

T − Km − 1Σu(m)

This is a least squares (LS) estimator of Σu with degrees offreedom adjustment T/(T − Km − 1), where Σu(m) is themaximum likelihood (ML) estimator of Σu obtained by fittinga VAR(m) model to the data.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Minimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

For a better interpretation and for obtaining a unique solution,the final criterion should be a scalar rather than a matrix.

⇒ We take the determinant and define the resulting criterionas Final Prediction Error (FPE):

FPE (m) = det

[T + Km + 1

T

T

T − Km − 1Σu(m)

]=

[T + Km + 1

T − Km − 1

]K

det Σu(m)

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Minimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

Based on the FPE criterion, we choose the estimation p(FPE )of the lag order p such that

FPE [p(FPE )] = min {FPE (m)|m = 0, 1, ..., M}

VAR models of order m = 0, 1, ..., M are estimated and thecorresponding FPE values are computed. Then, the order mminimizing the FPE is chosen as estimate of the trueunderlying lag order p.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Minimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

FPE (m) =

[T + Km + 1

T − Km − 1

]K

det Σu(m)

The first term in the above equation increases if m increases,whereas the second term decreases for increasing m.

Thus, when these two forces are balanced in equilibrium, oneobtains the estimate of the lag order.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Minimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

Akaike’s Information Criterion (AIC) is defined as follows:

AIC (m) = ln |Σu(m)|+ 2mK 2

T

|Σu(m)| is the same as det Σu(m) and decreasing in m, mK 2

is the number of freely estimated parameters in a VAR model.2mK 2/T is the penalty term that increases in m andconverges to zero for T →∞.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Minimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

We choose the estimate p(AIC ) of p such that AIC(m) isminimized.

One could additionally show that FPE(m) and AIC(m) aresimilar for some constant N , although the AIC has beenderived based on a different reasoning. Hence, both criteriahave similar properties, for example the following...

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Minimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

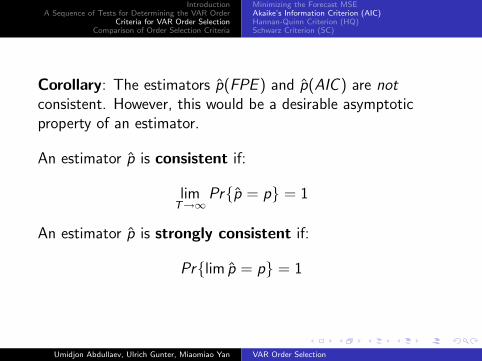

Corollary: The estimators p(FPE ) and p(AIC ) are notconsistent. However, this would be a desirable asymptoticproperty of an estimator.

An estimator p is consistent if:

limT→∞

Pr{p = p} = 1

An estimator p is strongly consistent if:

Pr{lim p = p} = 1

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Minimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

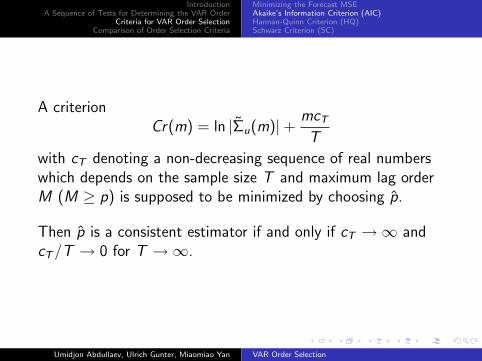

A criterionCr(m) = ln |Σu(m)|+ mcT

T

with cT denoting a non-decreasing sequence of real numberswhich depends on the sample size T and maximum lag orderM (M ≥ p) is supposed to be minimized by choosing p.

Then p is a consistent estimator if and only if cT →∞ andcT/T → 0 for T →∞.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Minimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

p is strongly consistent if and only if the above holds and, inaddition, cT/2 ln ln T > 1 for T →∞.

If M > p, p(AIC) and due to similarity also p(FPE) are notconsistent estimators because in this case mcT/T = 2mK 2/Tor cT = 2K 2, which contradicts cT →∞ and cT/T → 0 forT →∞.

Both estimators usually overestimate the true lag order withpositive probability.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Minimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

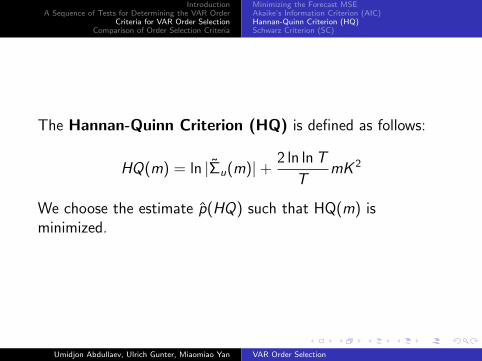

The Hannan-Quinn Criterion (HQ) is defined as follows:

HQ(m) = ln |Σu(m)|+ 2 ln ln T

TmK 2

We choose the estimate p(HQ) such that HQ(m) isminimized.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Minimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

Here cT = 2K 2 ln ln T . cT →∞ and cT/T → 0 for T →∞.

⇒ p(HQ) is consistent.

p(HQ) is even strongly consistent for K > 1 because in thiscase cT/2 ln ln T = K 2 > 1.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Minimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

The Schwarz Criterion (SC) is defined as follows:

SC (m) = ln |Σu(m)|+ ln T

TmK 2

We choose the estimate p(SC ) such that SC(m) is minimized.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Minimizing the Forecast MSEAkaike’s Information Criterion (AIC)Hannan-Quinn Criterion (HQ)Schwarz Criterion (SC)

Here cT = K 2 ln T . cT →∞ and cT/T → 0 for T →∞.

Moreover, cT/2 ln ln T = K 2 ln T/2 ln ln T > 1 for any K .

⇒ p(SC ) is always strongly consistent.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Small sample comparison of AIC, HQ, and SC

Proposition 4.3. Let y−M+1, . . . , y0, y1, . . . , yT be anyK -dimensional multiple time series and suppose that VAR(m)models, m = 0, 1,. . . , M , are fitted to y1, . . . , yT . Then thefollowing relations hold:

• p(SC ) ≤ p(AIC ) ifT ≥ 8

• p(SC ) ≤ p(HQ) for allT

• p(HQ) ≤ p(AIC ) ifT ≥ 16.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

A consequence of previous results is that

limT→∞ Pr{p(AIC ) < p}= 0 and

lim Pr{p(AIC ) > p}> 0

The same holds for FPE because it is asymptoticallyequivalent to AIC.

Large sample results sometimes are good approximations onlyif extreme sample sizes are available.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

A sequential testing procedure may give the same order as aselection criterion if the significance levels are chosenaccordingly.

For instance, AIC chooses an order smaller than the maximumorder M if AIC(M − 1) ¡ AIC(M) or, equivalently, if

λLR(1) = T (ln |Σu(M−1)|−ln |Σu(M)|) < 2MK 2−2(M−1)K 2

For K=2, 2K 2 = 8 ≈ χ2(4).90.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

The sequential testing procedure will not lead to a consistentorder estimator if the sequence of individual significance levelsis held constant.

For M > p and a fixed significance level γ,

H0 : AM = 0

is rejected with probability γ.

This problem can be circumvented be letting the significancelevel go to zero as T →∞.

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection

IntroductionA Sequence of Tests for Determining the VAR Order

Criteria for VAR Order SelectionComparison of Order Selection Criteria

Some simulation results

Data: quarterly, seasonally adjusted series for fixed investment,disposable income, consumption expenditures for WestGermany in billions of DM, 1960Q1-1982Q4;

Umidjon Abdullaev, Ulrich Gunter, Miaomiao Yan VAR Order Selection