Valuing Flexibility - A Real Options Valuation of the...

79

Page 1 of 79 Valuing Flexibility - A Real Options Valuation of the Sisson Tungsten-Molybdenum Project Master Thesis MSc. Finance and International Business Author: Peter Spanner Madsen - Aarhus University, Business and Social Sciences Number of Characters and Pages: 130,175 characters & 79 pages Supervisor: Stefan Hirth, Department of Economics and Business April 2015

Transcript of Valuing Flexibility - A Real Options Valuation of the...

Page 1 of 79

Valuing Flexibility

- A Real Options Valuation of the Sisson

Tungsten-Molybdenum Project

Master Thesis

MSc. Finance and International Business

Author: Peter Spanner Madsen - Aarhus University, Business and Social Sciences

Number of Characters and Pages: 130,175 characters & 79 pages

Supervisor: Stefan Hirth, Department of Economics and Business

April 2015

Page 2 of 79

Abstract

The neoclassical capital budgeting process has been dominated by the DCF analysis, but

recently the real options framework has begun to win acclaim. This is due to the

inherent weaknesses of the DCF framework, which does not recognize uncertainty in

the variables employed in the valuation. As DCF valuation undervalues investment

opportunities under significant uncertainty, companies will underinvest and potentially

miss out on value creating opportunities. The thesis synthesises a real options

framework which recognizes uncertainty as well as the options available to an active

management. A case study approach is employed to illustrate a practical example of the

challenges of the real options analysis, in addition to highlighting the value derived

from the real options. The chosen case is a tungsten-molybdenum mining project in

Canada. The financial data of the project, as well as a comprehensive description of the

project was publicised as part of a Canadian securities regulatory filings. This formed

the basis of the financial data employed in the valuation. Two real options were

identified, the option to abandon the project, and the option to contract the output in the

case of unfavourable conditions. The options were valued separately and combined,

recognizing that the value of the separate real options is not the sum of the two options.

The value of the combined options to the management is estimated at 49.5 C$ Million

(M), an increase of 14.5% compared to the standard NPV value. The thesis concludes

by supporting the propositions made by the real options theory, substantiating the link

between uncertainty, management flexibility and the value of real options.

Page 3 of 79

Contents

1. Introduction............................................................................................................................... 5

1.1 Background & Problem Identification ................................................................................. 5

1.2 Case Study ........................................................................................................................... 7

1.3 Problem Statement ............................................................................................................. 7

1.3.1 Research Questions ...................................................................................................... 8

1.4 Real Options Literature Review ........................................................................................... 9

1.5 Real Options in Practice .................................................................................................... 11

1.6 Transitioning from Financial Options to Real Options ...................................................... 11

2. Theoretical Framework ........................................................................................................... 13

2.1 Valuation Framework ........................................................................................................ 13

2.2 Discounted Cash Flow ....................................................................................................... 14

2.2.1 Assumptions ............................................................................................................... 15

2.2.2 Three Inputs – Discount Rate, Free Cash Flow and Uncertainty ................................ 16

2.3 Simulation ......................................................................................................................... 18

2.4 Decision-tree Analysis ....................................................................................................... 21

2.5 Real Options Valuation ...................................................................................................... 22

2.5.1 When to use Real Options? ........................................................................................ 23

2.5.2 Types of Options......................................................................................................... 24

2.5.3 Determining the Value of an Option .......................................................................... 25

2.5.4 Analytical Approaches ................................................................................................ 27

2.5 Solution Techniques ...................................................................................................... 30

3. Case Study – The Sisson Tungsten-Molybdenum Project ....................................................... 36

3.1 Calculate NPV .................................................................................................................... 36

3.1.1 Assumptions Made in the NI-43-101 ......................................................................... 36

3.1.1.1 Reserves .................................................................................................................. 36

3.1.1.2 Production Capacity ................................................................................................ 37

3.1.2 Calculating the Dynamic Discounted NPV .................................................................. 38

3.1.2.1 Cost of Capital ......................................................................................................... 40

3.1.3 Sensitivity Analysis ..................................................................................................... 46

3.2 Analyse Uncertainty .......................................................................................................... 47

3.2.1 Exchange rate ............................................................................................................. 47

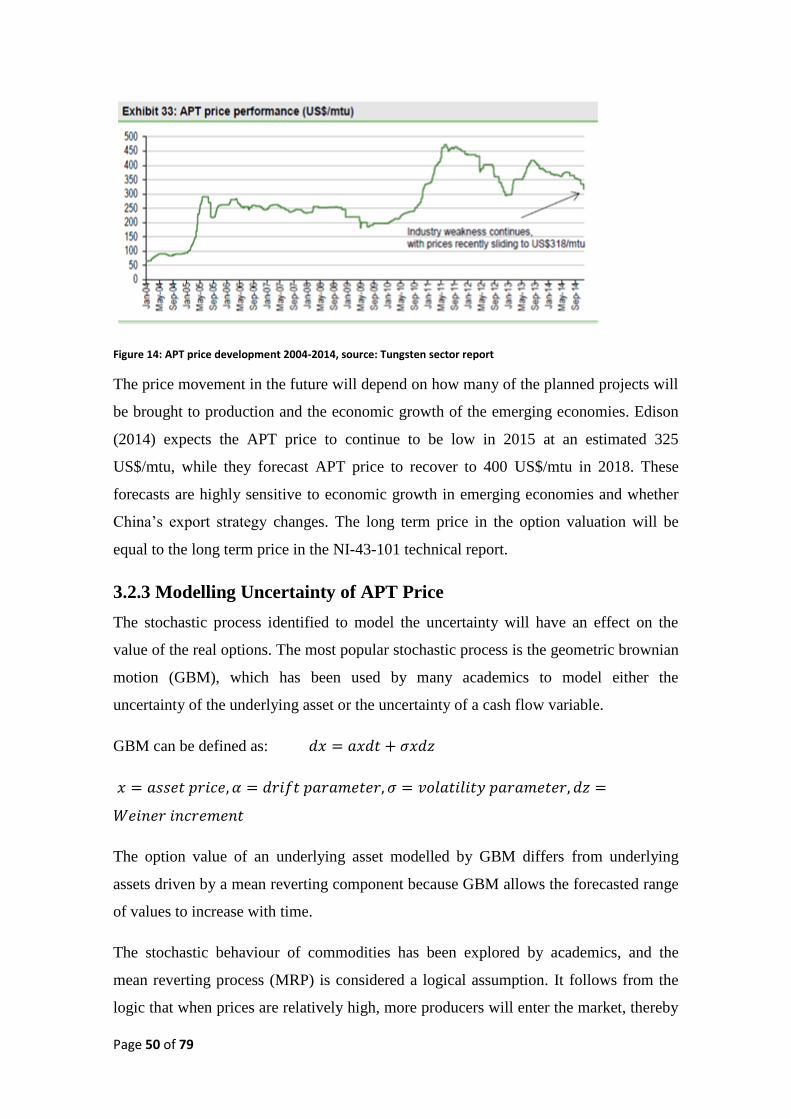

3.2.2 APT Price..................................................................................................................... 48

3.2.3 Modelling Uncertainty of APT Price ........................................................................... 50

Page 4 of 79

3.2.4 Modelling Uncertainty of the Exchange Rate ............................................................ 52

3.2.5 Correlation of Uncertainty Variables ......................................................................... 53

3.2.6 Volatility Estimate of the Underlying Asset ............................................................... 53

3.3 Event Tree ......................................................................................................................... 54

3.4 Create Decision Tree ......................................................................................................... 54

3.5 Estimate Value of Real Options ......................................................................................... 55

3.5.1 Abandonment Option with Changing Strikes ............................................................. 55

3.5.2 Option to Contract with Changing Strikes .................................................................. 56

3.5.3 Real Options Interactions and Non-additivity ............................................................ 57

3.5.4 Options Sensitivity Analysis ........................................................................................ 57

4. Conclusions.............................................................................................................................. 60

4.1 Main insights ..................................................................................................................... 60

4.2 Conclusion ......................................................................................................................... 60

4.3 Limitations and Further Research ..................................................................................... 61

5. References ............................................................................................................................... 63

6. List of Figures........................................................................................................................... 69

7. Appendix ................................................................................................................................. 70

Page 5 of 79

1. Introduction

1.1 Background & Problem Identification

According to Marshallian investment theory (Dixit & Pindyck 1994, p.260), companies

undertake investments to exploit temporary deviations from market-price equilibrium or

to exploit a competitive advantage. However, companies have always found it difficult

to value these investment opportunities. The capital budgeting process has a long

history, but advances in the field are rare. The dominating paradigm in the neoclassical

literature and dating back to the start of the eighties has been the net present value

(NPV) analysis. This is supported by a survey from 1978 which found that in 86% of

423 large companies employed NPV analysis (Schall, Sundem, and Geijsbeek, 1978).

Even before this, discounted cash flow (DCF) was a widely accepted valuation

technique, Segelod (1998) reports that the proportion of Furtune 500 companies using

DCF to value investments has steadily risen from 38% in 1962, 64% in 1977 to 90% in

1990-1993. A more recent study confirms this steady rise, as a survey by Graham and

Campbell (2002) shows that 74.9% of CFO’s in the survey always or almost always

used NPV as their capital budgeting.

However, academics and practicing managers are starting to recognize that NPV

analysis is an inadequate capital budgeting tool. The NPV analysis has several problems

in implementation of the analysis and in the assumptions behind the analysis. The NPV

analysis makes unrealistic assumptions in many cases, such as assuming expected cash

flows to be deterministic and presumes that once an investment decision has been made,

management has no operating flexibility. These kinds of assumptions can lead to

systematic undervaluation of projects as the value of operational flexibility is ignored,

e.g. the possibility to shut down a project (Hayes & Abernathy 1980). This systematic

undervaluation can lead to myopic decisions, underinvestment and a loss of competitive

position, since the companies are not able to properly quantify the value of operational

and strategic flexibility (Hayes and Garvin 1982).

The implementation by managers of the risk adjustment factor in the NPV analysis can

be problematic as the normal approach is to use a company’s weighted average cost of

capital (WACC), however, in practice managers often require hurdle rates much higher

than the cost of capital (Summers 1991, J.P. Morgan 2014), yet they still demand a

Page 6 of 79

positive NPV for projects. Dixit and Pindyck (1995) explain that this systematic

adjustment of the hurdle rate may be a result of managers realising that a company’s

options are valuable and keeping them open is often desirable.

So how should managers value projects that have operational flexibility?

Operational flexibility is potentially valuable when there is uncertainty regarding

expected cash flows and this uncertainty is resolved over time. As the uncertainty is

resolved, management may depart from the original operating strategy to accommodate

for this new information. The management may want to defer, expand, abandon,

contract, shut down or alter the operating strategy in other ways. These options

introduce asymmetry to the probability function of the NPV. This asymmetry makes it

possible to capture additional value available in favourable conditions or limit the

downside losses in unfavourable conditions. To value the options a new valuation

technique has to be employed that applies the expanded net present value criterion. The

sources of the expanded net present value is the traditional NPV (static or passive) of

cash flows plus the option value, which represent the operational flexibility (Trigeorgis

1998).

Expanded NPV (eNPV) = Static (Passive) NPV + Option Premium

The value of the option premium changes the way management should perceive risk.

The risk of the project is a positive factor when determining the value of the option.

This is in contrast to the NPV analysis, which increases the discount rate as the risk of

the project increases, thereby decreasing the NPV of a project. This means that there are

two opposite effects when calculating the real options value.

An investment opportunity in a mining project has been chosen for the case study as it

represents a clear example of the difficulties the traditional NPV approach will

encounter. O’Hara (1982) states that the actual return on investment can differ

substantially from the estimate of the feasibility study (a study determining the

economic viability of a mining project), this is because of errors in estimating capital

costs, ore reserves, operating costs, mineral revenue or operating productivity. This

problem can be alleviated by incorporating flexibility into the valuation to help

management control the errors (Mayer & Kazakidis 2007). To further substantiate the

Page 7 of 79

problem, Davis (1995) reports a discrepancy between the sum of discounted cash flows

in mining companies and its market price.

1.2 Case Study

The research structure applied in the thesis is a linear-analytic structure suggested for

thesis work by Yin (2014). Following this structure, the thesis is compiled as follows:

stating the problem being studied, review of relevant literature, moving on to the

theoretical methods applied, data input collected to be analysed, ending with the

findings, conclusions and implications for the issue being studied.

A case study can be defined in two parts as: “a case study investigates a contemporary

phenomenon (the “case”) in its real-world context, especially when the boundaries

between phenomenon and context may not be clearly evident”. The case is the Sisson

Project, which will be defined below. The second part is a definition of the case study

design and data collection methods (Yin 2014). This case study is designed as a single-

case study to determine whether the circumstances of the case and propositions stated

can be determined to be true or other explanations are more valid. This will enable me

to do a critical test of existing theory.

Case study research allows for a holistic and real-world perspective in the study of a

phenomenon such as capital budgeting processes. At the same time it allows me to do

an exploratory study, as shown in Allison & Zelikow (1999) who utilises a single case

study to form the basis of significant generalization (Cuban missile crises). However,

analytical generalizing of theoretical propositions can also be done by “multiple sets of

experiments that have replicated the same phenomenon under different conditions”. The

analytical technique applied is pattern matching, comparing predictions from theory

with data collected based on the findings of my case.

1.3 Problem Statement

The focus of the thesis is to analyse the valuation process of a natural resource

exploration (NRE) investment project in an uncertain environment to improve the

understanding of why it is necessary to recognize the value of options in corporate

investments. I will develop a framework for valuing options available to an active

management, which will enable managers to make more informed investment decisions

Page 8 of 79

in order to avoid systematic undervaluation and underinvestment of corporate

investment opportunities.

The thesis will apply an eNPV framework to estimate the value of the Sisson Project

when operational flexibility is included in the valuation. The value of the traditional

NPV analysis will be compared to that of the eNPV analysis. This will enable me to

determine if traditional capital budgeting techniques undervalues investment

opportunities with options available to an active management.

The problem statement necessary to uncover this value is:

- What is the expanded net present value of the Sisson Tungsten-Molybdenum

Project in an uncertain environment?

1.3.1 Research Questions

The research questions have been posted as a way of organizing the thesis to help

identify the appropriate research method. At the same time the research questions will

structure which theoretical methods to be analysed.

- Why is DCF methods insufficient? How can the eNPV framework remedy the

problems of other capital budgeting methods?

- How should a valuation of a tungsten mining project be carried out?

- Which solution methods is the most appropriate to be employed in the eNPV

valuation of the case study

- What is the DCF value of the project?

- Which real options are available to the management?

- What is the options and eNPV value of the Sisson project?

Defining the Case: The Sisson Tungsten-Molybdenum Project

The project plans to develop one of the largest undeveloped tungsten deposits in the

world into a long-life mine. The deposit is located in New Brunswick, Canada. The site

will be developed as an open pit mining operation. The location has access to

infrastructure with sea access to the north and south. In addition, it is located in a

mining jurisdiction with a long history of mining projects.

Page 9 of 79

Tungsten is essential in electrical applications, medical equipment and

telecommunications. Its hardness is similar to diamonds and has a very high heat

resistance, making it a crucial metal for cutting and drilling tools. Molybdenum can be

used for high-grade steel alloys to be used in the automotive-, construction-, electrical-

and other industries. Tungsten and molybdenum ore will be extracted and transported to

the primary crusher. The crushed ore will then go to the processing plant where

grinding, flotation, thickening and de-watering processes will be carried out to produce

tungsten (W) and molybdenum (Mo) concentrate. The tungsten concentrate will then be

moved to a value-added processing plant (APT plant), which will refine the tungsten

concentrate to Ammonium Paratungstate (APT). The APT and molybdenum

concentrate will be trucked out for shipping to North America, Europe, Asia and

Australia.

The Sisson Project is operated by Northcliff Resources ltd. (Northcliff). They are a

mineral development company associated with Hunter Dickinson Inc., which is a global

mining group. Northcliff is a company devoted solely to the Sisson Project. It trades on

the Toronto Stock Exchange (TSX) under the ticker symbol NCF. The Sisson Project is

owned by Northcliff, holding the controlling interest (88.5%) and Todd Corporation of

New Zealand holding an 11.5 % share, functioning as a financing partner. In addition,

the Todd Corporation owns 15 % of Northcliff.

A Project feasibility study was conducted, and in January 2013 Northcliff confirmed the

viability of the project. The Project is now waiting for approval of the Environmental

Impact Assessment (EIA) report, which was submitted in July 2013. They are focusing

on finalising the approval by mid 2015 which will allow for arrangement of funding and

construction commencement. Northcliff estimates that, pending approval of EIA, the

project could start construction in late 2015 with a construction period estimated to last

several years. Commercial production has been planned to start in 2018.

1.4 Real Options Literature Review

Real options valuation (ROV) applies financial option pricing theory to real world

investment valuation. Financial options pricing theory was developed by Black, Scholes

and Merton in 1973. They developed the Black-Scholes (B&S) model for valuing no-

dividend European options by constructing a replicating portfolio with the same cash

flows as the option, relying on no arbitrage to price the option (Damodaran 2002). Cox

Page 10 of 79

and Ross (1976) formalized their theory in a concept where securities are valued by

relying on risk-neutral valuation. This meant that if expected rates of return on the

underlying asset are risk-adjusted, the risk-adjusted cash flows can be discounted at the

risk-free rate (Brennan & Trigeorgis 2000). The implication of the breakthrough in

valuing financial options by constructing a replicating portfolio is clear, as evident by

the volume of trading on The Chicago Board Options Exchange (CBOE). It began

trading in 1973 and was the first public options exchange. In 1975 the traders on the

exchange was using the B&S model for pricing and hedging options positions (Merton

1998). In the most recent market report from 2013, the nominal dollar value traded on

CBOE was US$ 551.701.766.386 in put and call options (2013 Market Statistics).

The transition from financial options to real options was greatly influenced by Myers

(1977) as he suggested that corporate assets such as growth opportunities can be viewed

as call options where the real options value depends on the discretionary future

investments of the firm. The valuation of options was further advanced by Cox, Ross &

Rubinstein (1979) as they recognised that an option can be valued by a binomial

discrete-time approach making option valuation simpler and making it possible to value

American type options. In 1985 Brennan & Schwartz applied real options to determine

the optimal production policy in a natural resource investment project. Later Cortazar &

Casassus (1998) implemented real options valuation for a copper mine with the option

to expand production capacity, they found the real option value to be higher than the

NPV used by the case company. Cortazar et al. (2000) studied the option to defer

exploration investments in a copper mine and found that a significant part of the project

value was due to the options available to the management. Empirical research on real

options in mining is limited, although some important papers tests empirically how well

real options theory predicts reality. Moel & Tufano (2002) studies the opening and

closing decision of mining operations. Utilising a database of North American gold

mines from 1988-1997, they find that real options theory can explain the pattern of the

decision to open or shutdown a mining operation. Colwell, Henker & Ho (2002)

focused on the closure option of Australian gold mines in the period of 1992-1995.

They find the average and median closure option to be economically significant, they

do, however, add the caveat that the option values vary over a large range, leading to a

limited usefulness of real options to some individual mines.

Page 11 of 79

1.5 Real Options in Practice

In the mid-1990’s the interest in real options theory grew substantially. This began in

the oil and gas industries before moving into other industries such as management

consulting, where analysts began to use the framework for valuing investment

decisions. Real options theory has now become a mainstay in mainstream academic

finance texts and has won the attention of the industry (Borison 2005). However, there

are different interpretations of what constitute ‘real options’. For some firms real

options is applied as a conceptual tool for strategic planning, whereas others use it in the

in the more conventional form as a valuation technique (Triantis & Borison 2001).

Busby & Pitts (1997) asked all Finance Directors in FTSE 100 index whether they

recognized options in their businesses, which 50% of them did. Most of the identified

options were growth or abandonment options. 35% of respondents thought that options

were highly or extremely important in influencing investment decisions, however, more

than 75% of the respondents did not have procedures for handling real options

valuation. A later survey by Graham & Harvey (2001) conclude that about one third of

company CEOs in Fortune 1000 always or almost always value investments with real

options. Ryan & Ryan (2002) also surveyed CEOs in Fortune 1000 and found about 10-

15% utilised real options. Triantis (2005) suggests that this discrepancy may be down to

the different definitions of real options. I will show that there are pitfalls in real options

valuation as well as practical implementation difficulties, such as limited understanding

of real options by corporate managers. Further, assumptions are often violated in

practice, which may be some of the explanation why real options proponents have yet to

convince many companies of the value of real options theory.

1.6 Transitioning from Financial Options to Real Options

There are difficulties in the transition from financial options to real options, as Merton

(1998, p. 343) noted in a lecture for the Nobel Prize in Economics, in which he issued a

strong word of caution about the theoretical issues of using the financial options theory

for valuing real options. In his concluding remarks he states "the mathematics of

financial models can be applied precisely, but the models are not at all precise in their

application to the complex real world ... The models should be applied in practice only

tentatively, with careful assessment of their limitations in each application." Other

prominent authors within the field of real options are also weary of the complications

when trying to apply financial models to the real world. Copeland & Tufano (2004)

Page 12 of 79

states that two main differences between financial options and real options should be

considered before applying options theory to corporate investments: Firstly, it can be

problematic to estimate the value of the underlying asset, e.g. R&D of drugs has no

observable market price. However, when the underlying asset has a good proxy in the

market, the market can serve as a guiding point. Secondly, financial options and real

options differ in terms of how the options are defined. It can be unclear what a call real

option buys the caller, and how long it will last. E.g., when developing a new factory,

what is the maturity or how long does an option to expand last? - real options are not

always proprietary, which means a competitor may be able to erode the available

profits. Exercising a real option may also trigger the ability to exercise another option

(Trigeorgis 1996), e.g. building a new factory, could enable the management to expand

the factory in the future, which turns the option into a compound option, requiring a

different valuation method (Copeland & Tufano 2004). These examples show that real

options should not be treated like financial options, which can be valued relying on

market data to achieve a precise valuation. However real options can deliver a good

result when inputs are estimated thoroughly, and while it is not a precise measure, it can

function a way of quantifying the value of the option embedded in the project, to help

management in capital budgeting decisions.

Page 13 of 79

2. Theoretical Framework

In this section I will develop the theoretical framework to handle the valuation and

review the separate parts of the real options analysis to show why an eclectic framework

of previous attempts to quantify the value of flexibility will yield significant

improvements to the valuation framework.

2.1 Valuation Framework

The right valuation framework is dependent on the specific investment opportunity, as

the characteristics of an investment have significant impact on the appropriate valuation

method. Several different valuation methods try to extend the standard DCF framework

to incorporate the value of uncertainty and/or options (e.g. decision tree analysis and

simulation). I will show that these valuation techniques have their merits but also

shortcomings. This thorough review will highlight in which situations the methods are

applicable and in which they fail. The review will allow me to explain why the eNPV

framework is the only appropriate valuation method under significant uncertainty and

operational flexibility.

There are three basic valuation approaches for valuing an asset. The DCF valuation

values an asset based on the expected future cash flows this asset will generate. The

relative valuation uses the prices of other comparable assets to value the asset by

comparing variables that are common for both assets, like cash flows or book value.

Option pricing or contingent claims analysis values the asset by using option pricing

methods for assets, which has options characteristics (Damodaran 2006, p.9). DCF is

necessary for applying option pricing, therefore it is important to understand the

fundamentals of DCF (Damodaran 2002, p.12). Before reviewing the NPV model and

elaborating on why it is essential to the real options analysis, I will review the necessary

features of the valuation framework to be able to value the case project.

Trigeorgis (1996, p.52) states that “the presence of contingencies introduced by

managerial flexibility poses more serious problems, necessitating the use of option-

based valuation”.

I have summarized the most important problems and arguments for extending the

traditional NPV framework. Firstly, DCF techniques systematically undervalue

Page 14 of 79

investment opportunities (Copeland, Weston & Shastri 2004, p.308, Hayes &

Abernathy 1980, Hayes & Garvin 1982), as it fails to incorporate operating flexibility

(possibility to make or revise decisions at a future time) and the strategic option value of

a project (interdependence with future and follow-up investments) (Trigeorgis 1998).

Secondly, misapplication of DCF methods such as excessive risk adjustments in

projects with risk patterns that does not follow a random walk i.e. risk could decrease

with time (e.g. in a R&D project with different risk phases) (Hodder & Riggs

1985).This leads me to conclude that the appropriate valuation framework has to be able

to deal with uncertainty, operational flexibility and strategic options.

Although the NPV framework lacks the ability to value options, it is a fundamental part

of simulation techniques, decision-three analysis and real options valuation; therefore I

will review the NPV framework for application in the case valuation. Afterwards,

frameworks attempting to extend and improve upon the NPV analysis by dealing with

uncertainty, operational flexibility and/or strategic options will be reviewed for

applicability. At the same time I will show that the reviewed frameworks are a

complement to the real options analysis. The frameworks reviewed have been suggested

by decision scientists such as: Hertz 1979, Magee 1964, Trigeorgis & Mason 1987,

Kodukula & Papudesu 2006, Mun 2006, Amram & Kulatilaka 1999 and Copeland

2003.

2.2 Discounted Cash Flow

Firstly, I will, in short, review the basics of an NPV analysis. Secondly, I present the

assumptions underlying the NPV analyses to show why they are problematic in a stand-

alone analysis. Lastly, I will look at the application problems that both the real options

analysis and a stand-alone NPV analysis will have to deal with.

Mun (2006, p.63) states, “Value is defined as the single time-value discounted number

that is representative of all future net profitability”. To calculate this value, the NPV

method is the most widely applied method out of hundreds of DCF methods, that all

have a common goal of calculating the NPV of a project by discounting investment

costs and free cash flows by an appropriate discount rate. The calculated value is the

present value of all the project future cash flows less the investment costs (Kodukula &

Papudesu 2006, p.17). The NPV of an investment is an expression of the value to an

investor who has free access to capital markets, and should be compensated according

Page 15 of 79

to the equilibrium expected return on securities with equivalent risk (Myers 1987), or

put another way, risk should be perceived as the risk to the marginal (investor most

likely to be trading on the stock at any given point in time) well diversified investor in

the firm (Damodaran 2006, p.14, p.28).

2.2.1 Assumptions

The assumptions of an NPV analysis are not automatically fulfilled in a real world

scenario. Myers (1987) and Damodaran (2012) both state that DCF is a standard method

for valuing default-free zero coupon bonds, where discounting the bond at the risk-free

rate will find the present value of the bond. When moving away from this simple

valuation, the assumptions underlying the DCF will have to be reconsidered. This could

be going from valuing the default-free zero coupon bonds to valuing a corporate bond

where default risk is introduced. Moving on to investment projects where the expected

cash flows are assumed uncertain (Damodaran 2012, p.12, Myers 1987).

The assumptions of an NPV analysis assume either a reversible or an irreversible now

or never investment (Miller & Park 2002). If the cash flows are certain, then there is no

need for revising the investment, as the optimal investment strategy can be chosen from

the beginning and the assumptions hold true. This means that NPV method is good for

valuing investment projects which can be termed “cash cows” (projects held in a

projects portfolio for the cash generation and not for strategic value). At the same time,

this means that NPV is not suited for valuing businesses with growth opportunities or

R&D, as a significant component of their value is derived from the strategic option

value or management flexibility inherent in the investment. (Myers 1987, Trigeorgis

1999, p.1). If the investment is assumed reversible, which for many investments is

untrue, e.g. mining projects will not be able to recoup all capital expenses and would

incur a clean-up cost, the assumption of reversibility fails. If the investment is assumed

an irreversible now-or-never investment, the assumption breaks down for proprietary

investment projects, e.g. in mining projects where the land has been leased for a set

amount of time or bought, the investment decision may be delayed until the commodity

to be explored moves to a favourable price level (Dixit & Pindyck 1995). As shown, the

assumptions of the NPV analysis breaks down quite easily, highlighting the need for a

new expanded net present value framework.

Page 16 of 79

2.2.2 Three Inputs – Discount Rate, Free Cash Flow and Uncertainty

There are three inputs which determine the value of an NPV analysis. These will be

reviewed for applicability to the real options analysis.

2.2.2.1 Estimating the Discount Rate

The risk aspect of an investment project is notorious for being one of the most difficult

parts of the valuation to handle appropriately. The discount rate should be set at a level

which values the project according to the risk level. Risk is defined by Kodukula &

Papudesu (2006 p.35) as “...the variance of real outcomes around the expected

outcome”. When deciding the appropriate discount rate two factors are important to

consider. First, the magnitude of uncertainty of the cash flows. If there is no uncertainty,

the risk-free rate should be applied. Alternatively, if there is uncertainty, the type of risk

should be determined. There are two general types of risk, market risk and private risk.

Private risks are defined as risks not influenced by market fluctuations, (e.g.

technological success in R&D or geological risks inherent in mining projects estimate

of resource and reserves). Market risks are defined as risks which are driven by market

forces. Investment costs are usually considered private risk. Production phase free cash

flows are usually influenced by market risk because uncertainty (e.g. demand and price

fluctuations) is market driven (Mun 2006, p.68 & Kodukula & Papudesu 2006). If all

cash flow costs are discounted at the risk-adjusted rate, the costs will be too heavily

discounted, making the project appear more valuable than it really is (Mun 2006, p. 68).

Samis et al. (2004) describes this problem as using an all-use discount factor, which

leads projects with a high discount rate to depreciate the operating costs at a high level,

erroneously increasing the NPV of the project.

When the project has cash flows which are market driven, the discount rate for these

cash flows has to be set at a higher level than the risk free rate, as the risks of the cash

flows cannot be diversified, which means the owners are taking on a larger risk. The

discount rate the project should be commensurate with the risk level of the project. To

estimate the risk levels, the company will ideally try to find a proxy investment. This

proxy should have a similar risk profile as the project. If this is possible the returns of

the proxy will then be used as the discount rate for the project. The most common

method for quantifying the discount rate is to use the Capital Asset Pricing Model

(CAPM) (Damodaran 2012). The CAPM model states that the expected return of the

project should be the risk-free rate and a risk premium. The risk premium is calculated

Page 17 of 79

by the beta (measure of systematic undiversifiable risk relative to the capital markets)

times the difference of the market return and the risk free rate. If a proxy cannot be

found the WACC can be used and a premium can then be added if the project has a

higher than normal risk level (Kodukula & Papudesu 2006, p.43-44). WACC is a

commonly used method when the project is representative of the general risky nature of

the company’s activities (Mun 2006, p.69). When applying WACC the implicit

assumption is that companies adjust their debt levels to achieve a relatively constant

market-value leverage ratio, as reported in Copeland & Tufano (2004) companies will

typically not do this.

Other approaches which extends the CAPM model has been developed, although, these

multi factor models has failed in delivering significant improvement compared to the

default CAPM model. If CAPM is applied thoroughly it is still the most effective model

for dealing with risk (Damodaran 2006, p.35)

2.2.2.2 Estimating the Project’s Future Cash Flows

Free cash flows can be hard to predict, especially in projects where the lifetime is long,

as in the case project where the lifetime is projected to be 29 years. There are ways of

making the forecasts more reliable, e.g. econometric regressions, time-series analysis

and Monte Carlo simulation. Free cash flows are assumed predictable in NPV, but are

usually stochastic and risky in nature (Mun 2006, p. 67), as discussed in the previous

section this is problematic, since managers will have to reconsider their options if the

cash flows turn out differently than expected, which means the assumption of

predictable free cash flows break down when there is uncertainty over the free cash

flows. The real options approach (ROA) remedies the problem by assuming uncertainty,

and as well creating a strategy for the possible outcomes.

2.2.2.3 Dealing with Uncertainty

Typical approaches to modelling uncertainty will be to apply a sensitivity analysis to

assess which single uncertainty variable is the most influential. This will allow the

manager to assess how project NPV varies with each uncertainty variable. The manager

is then able to assess the projects economic viability under different market and

technical circumstances. However, sensitivity analysis is an inferior technique

compared to Monte Carlo simulation as this is an extended version of the sensitivity

analysis which considers the impact of all possible combinations (Trigeorgis 1996,

Page 18 of 79

p.54). Scenario analysis is able to gauge the overall level of uncertainty by recalculating

the free cash flows and NPV for different scenarios of the project. However, the

problem is how to choose between these scenarios (Amram & Kulatilaka, p.39-40

1999). Monte Carlo simulation will be used in the case study to create relevant

probabilities of cash flows to give a more detailed representation of the cash flows.

It is apparent that the standard NPV approach is problematic when valuing uncertain

cash flows over a long time horizon. Sensitivity analysis and scenario analysis can be

applied, but they fail in achieving a thorough estimation of the uncertainties of the

valuation. The eNPV approach will combine the NPV analysis with options based

valuation to overcome to inherent limitation of the NPV approach in dealing with

uncertainty. For modelling uncertainty, simulation has been suggested as a way of

improving the understanding of the variables and the probability function of NPV. In

the following section, I will review the basics of simulation and show why it is a crucial

part of a real options valuation.

2.3 Simulation

Before running a simulation, a deterministic NPV analysis is usually conducted and an

accompanying sensitivity analysis to identify the variables with the most impact on the

NPV. To show this graphically a Tornado chart will be applied. The most sensitive

variables are then chosen for a Monte Carlo simulation to be used in the dynamic NPV

analysis.

Simulation has a number of applications. Firstly, it can be used for modelling

uncertainty in an NPV framework. Secondly, it can be used to combine the variable’s

volatility into a single estimate of project volatility, which is necessary for conducting a

thorough real options analysis. Lastly, it can be utilised as a real option solution

technique. In this section I will focus on the characteristics of a dynamic NPV

simulation, application methods and problems in application. This will allow me to

show why simulation is not appropriate for a stand-alone valuation, but is useful in

combination with real options analysis.

Trigeorgis (1996) describes traditional simulation techniques as “repeated random

sampling from the probability distribution for each of the crucial primary variables

underlying the cash flows of a project...” The crucial primary variables are typically

Page 19 of 79

revenue, costs or other cash flow driving variables. This produces a probability

distribution of the NPV for a chosen management strategy. The management strategy is

put into the simulation as a mathematical model to simulate real-world settings where

the project uncertainty will be resolved over time, dependent on the pre-committed

operating strategy. Simulation is applied in an attempt to handle complex investment

decisions with uncertainty and enable management to handle input variables correlated

with each other. The variables stochastic process (e.g. Geometric Brownian Motion) has

to be predefined, and is determined by the characteristics of the variable(s) in the

simulation. Historical data or management judgement provides the source to determine

these characteristics. These variables may be correlated, if they are, this should be

determined and accounted for. Correlations between variables can be handled by

combining the variables into one combined single project volatility estimate.

Alternatively, if the variables are independent and expected to move in opposite

directions they can be kept separate to be able to distinguish the impact on value of the

separate variables. A rainbow type option allows for this, however, the option pricing

becomes much more complicated (Damodaran 2002).

Alternatively, methods for estimating the volatility includes; Logarithmic Cash Flow

Returns Method, Project Proxy Approach, Market Proxy Approach and Management

Assumption Approach. The Simulation Approach has been chosen for its ability to

include negative cash flows as well as being more accurate in asset analysis (Mun 2006,

p.190).

Monte Carlo simulation software such as Crystal Ball® is typically used for the

simulation. The software will generate an NPV value by simulating a value for each

input parameters from the assigned distribution. This is repeated a specified number of

times to generate the NPV probability distribution. The advantage of this method is its

ability to highlight the variability of input variables determining the NPV. It

acknowledges that the confidence of the accuracy of the single-point estimate of NPV,

traditionally supplied by a standard NPV analysis is often low. This is because

predicting the future in such a precise way is incredibly tough, if not impossible for

most investments (Mun 2006, p.104). Instead, Monte Carlo simulation estimates the

NPV probability distribution, to allow the management to get an estimate of the

probability that project NPV value is positive, and the probability of the ranges of value

the NPV can be within. As an example of how misleading a single best estimate can be,

Page 20 of 79

suppose a company makes a $1 million investment with three equally possible

outcomes, zero per year, $200,000 per year or $400,000 per year. This would come to a

best estimated return of $200,000 per year. However, if the company only has this

project, the company would go bankrupt if the project turns out to yield $0 per year, the

company would have a 1/3 chance of bankruptcy, even though the company’s best

estimate was $200,000 (Hertz 1979). This illustrates that even though an investment

may seem favourable, the dangers of high uncertainty has to be recognized.

Using Monte Carlo simulation for a dynamic NPV analysis can be problematic. Firstly,

as with any valuation, simulation is subject to the saying “garbage in, garbage out”. The

probability distribution of the variable inputs (e.g. cash flows, costs) has to be estimated

precise, otherwise the NPV probability distribution will be biased. Secondly, all the

interdependencies of the input variables can be very difficult to capture (Trigeorgis

1996). These two notions are true for simulation of project value and for using

simulation as an estimator of project volatility. Modelling NPV uncertainty by

simulation suffers from some of the same issues as a deterministic NPV analysis. I will

present the issues now and show why it is necessary to value the project by simulating

the probability distribution of the NPV as a way of modelling uncertainty to

complement real options theory.

Simulation is an extension of the traditional NPV analysis, and as such it is fallible to

the same assumptions underlying an NPV analysis. Simulation is applied in a forward

looking way as the management predetermines the strategy to be applied. This means

that Monte Carlo simulation does not allow for management flexibility if uncertainty is

resolved unexpectedly. The Monte Carlo simulation of the probability distribution of

NPV is not representative of a real world scenario with uncertainty, as managements in

the real world will have the ability to adapt their strategy to variables (e.g. cash flows)

which differs from expectations. The management might respond to unexpected cash

flows by abandoning, expanding or otherwise altering their operations strategy. This

means that simulation is better suited for projects which are predictable, such as path-

dependent or history-dependent projects (Trigeorgis 1996).

By applying simulation in the eNPV framework, the benefits of an improved

understanding of the NPV can be achieved and an aggregate volatility estimation can be

Page 21 of 79

produced. Using simulation complimentary to the real options analysis will help

overcome the main drawbacks of simulation.

2.4 Decision-tree Analysis

Decision-tree analysis (DTA) is also an extension of DCF, as it offers information about

future decisions under uncertainty and attempt to deal with the possible future decisions.

Decision trees can be used as a way of mapping graphically the strategic pathways a

company can undertake. This is done by “...mapping out all feasible alternative

managerial actions contingent on the possible states of nature in a hierarchical manner.”

(Trigeorgis 1996, p. 57). This method allows the management to analyse a large array of

complex sequential investment opportunities in an organized fashion. However, when a

lot of investment decisions branches into many decisions, the tree can become very

confusing. Trigeorgis (1996, p.66) refers to this problem as the decision-tree becoming

a decision-bush. The basic setup of the decision tree is a set of alternative decisions,

which are mapped by consequences of each decision dependent on a subjective

probability. Management then uses backwards induction to select the strategy where the

expected risk-adjusted NPV is maximized (Trigeorgis 1996). However, there are

problems in the application of decision tree analysis, especially in applying the correct

discount rate.

The expected value should optimally be calculated using risk-neutral probabilities (see

ROA section), as this would allow for the risk-free rate to be used for discounting.

Using risk-neutral probabilities in decision-tree analysis is erroneous for two reasons.

Firstly, the risk-neutral probabilities are calculated assuming a constant volatility. This

assumption is violated because the risk changes with each decision node, since the

decision will alter the project risk (e.g. shutting down a mine while mineral prices are

low). Secondly, risk-neutral probabilities require that the up and down jumps are

identical in size in the binomial lattice (two bifurcations/branches), to allow

recombining lattice. The jumps are not identical in size because the returns are not the

same for different branches in the decision tree. This requirement is known as the

Martingale process (knowledge of prior observed values does not change the

expectation of the next value). Because these requirements are not satisfied, the risk-

neutral probabilities are invalid. Since risk-neutral probabilities assumptions are

violated, the risk-free rate cannot be used as the discount rate ( Mun 2006, p.58).

Page 22 of 79

Applying DTA without the use of risk-neutral probabilities, but instead relying on

different discount rates at each decision nodes and at different time periods is a way to

solve this problem. Using different discount rates is necessary to account for changing

risks associated with the impact of decision nodes on project structure. Subjective

probabilities have to be applied at each node along with estimation of the appropriate

discount rate at each node. Estimation- and probability of occurrence errors will

compound and lead to incorrect valuations (Mun 2006, p.257). In conclusion, decision-

tree analysis does offer a good way of graphically representing the future decisions

available to the management, as decisions trees can be integrated into the real options

framework to map the contingent decisions where each node can be correctly valued by

a real options solution technique. It is however, on a stand-alone basis an economically

incorrect method because of the discount rate problem (Trigeorgis 1996, p.68). The real

options approach can solve this problem by incorporating the combined volatility from

Monte Carlo simulation to allow for risk-neutral valuation.

Having reviewed the alternative methods for handling investment opportunities with

uncertainty and management flexibility I can conclude they all suffer from problems

that can be remedied by applying simulation and decisions tree analysis in conjunction

with real options theory.

2.5 Real Options Valuation

A real option is any non-financial asset investment decision, be it to invest, divest,

expand or abandonment. The option gives the holder the right, but not obligation to

exercise the option at a predetermined price and time period. This is analogous to a call

or put option in the financial markets (Miller & Park 2002). Figure 1 illustrates how

financial- and real options are connected to each other.

Figure 1: Comparison of financial and real options, source: Felix Stellmaszek

Page 23 of 79

2.5.1 When to use Real Options?

Figure 2: when are options valuable, Source: Koller, et al. 2010

There are a number of prerequisites for applying real options analysis in a meaningful

way. Firstly, it should be possible to build a financial model where uncertainty factors

can be modelled and changed as new information arrives. Secondly, the management

should have flexibility, strategic options and be able to exercise the options as

uncertainty is resolved. Further, there has to be a significant uncertainty level regarding

the project cash flows, otherwise the optimal strategy could be chosen from the onset,

and the contingent decision would not be contingent on the outcome of the uncertainty.

Lastly, the management has to be willing, rational in exercising the options. In

companies where management and ownership is separated, principal-agent corporate

governance problems may come into play in these situations. This could be because a

manager’s remuneration is attached to how a specific investment fairs. The

manager/agent will then choose a course of action for the investment to gain maximum

economic benefit for him- or herself even though this could lead to a decrease in

shareholder value (Amram & Kulatilaka 1999, p.24, Mun 2006, p.135).

The real options framework is best suited for investments where the NPV value is either

modestly positive or slightly negative as this is where managers are forced to rely on

intuition to choose between foregoing an investment or investing. In these cases the real

options analysis can be conducted to supply management with the possibility to rely less

Page 24 of 79

on subjective intuition and more on the logic the option value offers to support or

discourage management intuition (Van Putten & MacMillan 2004).

2.5.2 Types of Options

As stated above, the management has to identify the options available and also the type

of option, as this is important when calculating the option value. There are a number of

generic option types, which are available to a mining operation (Haque, Topal & Lilford

2014).

2.5.2.1 Option to Abandon

The management can decide to create an abandonment option or it may already exist.

The real option analysis is able to enlighten the management about which circumstances

it is optimal to exercise the option. This is useful when deciding to abandon an

operating gold mine if prices decline, making exploration unprofitable. The

abandonment option is an option to sell for salvage value, which could include capital

expenditure and the cost of reclamation and closure. This is analogous to a put option in

the financial options terminology (Mun 2006, Copeland & Antikarov 2004).

2.5.2.2 Option to Expand

An option to expand could be the possibility to expand mining exploration capacity, e.g.

mining twice the amount of ore as usual, by investing additional capital to secure the

necessary surplus capacity for increasing output. This option is typically considered

when the commodity price increases, which can make the thus far non-economically

orebody economically viable because of the increased commodity price. An option to

expand is analogous to a call option.

2.5.2.3 Option to Contract

If a company is unsure of the market development, it might want to reduce its exposure

to the underlying by obtaining an option to contract operations by 50 percent at the time

the company deems it optimal within the next five years. This could be done by signing

a contract with a customer to buy some share of the output at a given price in the future

if the option is exercised. This is analogous to a financial put option.

2.5.2.4 Simultaneous Compound Options

This type of option is used when the value of one option depends on the value of

another option. Compound options were recognized by Black & Scholes in 1973, they

Page 25 of 79

found that the equity of a leveraged firm is actually a call option on the value of the

company, where the strike price is the face value of the debt. If a financial option is

written on the security of the firm, then a compound option is achieved. The option on

the security is then an option on the option on value of the firm. This is a simultaneous

compound option because the two options are active at the same time (Copeland &

Antikarov 2004). The assumptions underlying simultaneous compound options are that

both options occur at the same time and take an equal amount of time (Mun 2006).

2.5.2.5 Sequential Compound Options

In a sequential compound option the investment opportunity has multiple options over

several time phases, where the last option will depend on the success of the previous

option. Developing a factory could require multiple phases, which will depend on the

success of the previous phases.

2.5.2.6 Option to Change Strike Price and Volatility

Some options have changing strike prices or the volatility as time passes. For changing

parameters, it is extremely difficult mathematically to solve these options in a closed-

form model.

2.5.2.7 Option to Choose (Chooser Option)

When multiple mutually exclusive options exist, the management will have to choose

between different options. The combined value of the options are estimated by

incorporating all individual options into one option lattice, stepping backwards in time

by choosing the option which is most valuable at each decision node.

2.5.3 Determining the Value of an Option

2.5.3.1 Volatility (Risk) & Uncertainty

Before moving on to the determination of the value of an option, I will uncover the

difference between uncertainty and risk, as these two variables are sometimes used

interchangeably. However, they are not the same and should be defined, as they are both

important to the real options value.

Cash flows are a main value driver, however, cash flows are not certain in the real world

as cash flows are a forecast of the unknown to be resolved over time, events or actions.

Uncertainty can be thought of as the probability that a foreign exchange rate will be as

forecasted, or put another way the probability of an event occurring. The risk is the

Page 26 of 79

value change on a currency position (short/long) when the exchange rate moves. Mun

(2006) describes risk as “risk is something one bears and is the outcome of uncertainty”.

So if a company has perfectly hedged its exchange rate exposure, it will still be

uncertain about the movement of the exchange rate, but it will bear no risk.

In the real options framework risk is the volatility. The risk of a project is the “net

interaction of all uncertainties on cash flow” (Mun 2006). The risk is calculated using

the volatility of the rates of return. Uncertainty is needed to generate value in an option,

as it is the driver of the value. To be able to graphically show how uncertainty evolves

over time the cone of uncertainty has been developed.

Figure 3: Cone of uncertainty, source: Mun 2006, p.136

The model shows that uncertainty increases over time, which is not necessarily true for

risk. Logically, it makes sense that uncertainty increases over time as it is easier to

predict a project’s cash flows for a few months rather than for the next twenty years.

This is also depicted in the cone of uncertainty as it widens with time. This cone of

uncertainty actually looks like a binomial tree as this widens for every decision node. If

risk changes with time, the bounds of uncertainty become more complex and a

heteroskedastic (volatility changes over time) model for uncertainty need to be

developed. In real options, this is done by using non-recombining lattices.

Having defined the concept of volatility I will now move on to show what determines

the value of a real option. According to Copeland & Antikarov (2004) the value of a

real option depends on five basic variables with the possibility of more, depending on

the characteristic of the real option.

Page 27 of 79

The value of the underlying risky asset: The free cash flow from the project. When

the value of the asset underlying the real option increases, the value of the call option on

the real option increases as well (The opposite is true for a put option).

The exercise price: The exercise price can be seen as the investment cost to exercise

the option if the option is a call option (e.g. the option to expand operations by

increasing the output capacity of a mining operation). If the real option is a put option,

the exercise price is the amount received for exercising the option (e.g. abandoning a

project for salvage value). An increase in exercise price for a call option decreases the

call option value, whereas the value of a put option would increase.

The time to expiration of the option: The time to expiration increases the option

value when the time to expiration increases. This is true for both call and put options.

The standard deviation of the value of the underlying risky asset: The standard

deviation is a measure of the risky nature of the underlying asset. The value of a call

option depends on the value of the underlying exceeding the value of the exercise price.

When the standard deviation increases, the probability of the underlying asset exceeding

the exercise price also increases.

The risk-free rate of investment over the life of the option: The value of the option

increases when the risk-free rate increases.

Dividends: dividends usually belong to the world of financial options, but cash flow

lost to competition etc. can be seen as analogous to dividend in the real options world.

2.5.4 Analytical Approaches

Contradictory analytical approaches for application of real options analysis in practice

have been suggested by academics. It is important that the approach chosen for the real

options valuation is correct. The different approaches will yield different results

depending on the assumptions made in regards to calculating the underlying, what the

calculated value represents. Borison (2005) has analysed different approaches for three

fundamental issues, Applicability, Assumptions and Mechanics. I will review the

approaches and assess which approach is best suited to be applied in the case.

Page 28 of 79

2.5.4.1 The Classic Approach

The classic approach is the most direct application of option pricing theory to non-

financial asset valuation. The value derived from this approach represents financial

market value. This is the same as what the incremental investment would trade for in

the capital markets. The existence of a replicating portfolio from financial option

pricing theory is assumed. (portfolio of traded investments can be constructed to

replicate returns of the option, and the option can be valued based on no-arbitrage

argument). In addition, it is assumed that geometric brownian motion can describe the

asset price movement, which is also an assumption of the B&S model. The replicating

portfolio assumption for real options is lacking empirical evidence to validate that a

traded replicating portfolio of financial assets exists for a typical corporate investment

in real assets. Brealey and Myers (2000) explicitly say that replicating portfolio/no-

arbitrage cannot be used to justify application of real options.

2.5.4.2 The Subjective Approach

This approach uses subjective estimates of inputs instead of identifying a replicating

portfolio (still relies on the assumption that a replicating portfolio exists). The same

assumptions as the classic approach are assumed (the inputs of value of the replicating

portfolio follows a geometric brownian motion). DCF is suggested for determining the

current value of underlying asset. This is a subjective assessment as a proxy for traded

market values. The combination of the replicating portfolio (which is market based)

assumption and the use of subjective data (DCF) is inconsistent. The meaning of an

option value based on subjective DCF data with no-arbitrage assumption is unclear

(Borison 2005).

2.5.4.3 The MAD Approach

The marketed asset disclaimer (MAD) approach does not assume a traded replicating

portfolio, as with option pricing. Instead, the MAD approach assumes that using the

NPV value of the projects expected cash flows without flexibility can be used as an

estimate of the twin security known from the replicating portfolio. This is justified by

arguing that this assumption is not stronger than the assumptions behind the NPV (no-

arbitrage and market equilibrium), which is accepted and widely used. After the

underlying has been calculated the volatility is determined, and the binomial lattice

solution method can be applied.

Page 29 of 79

There is dissent among academics regarding the assumptions of the MAD approach.

Borison (2005) argues that there are differences in the traded twin security known from

DCF to that of option pricing. In DCF, a twin security refers to having the same beta, in

option pricing it refers to a security with the same returns in all states of the world. He

also criticises this approach for the use of subjective data for all input parameters except

cost of capital, which means that arbitrage opportunities may exist. In addition he

criticises Copeland & Antikarov’s (2004) assumption that the value of the underlying

follows a GBM walk which is attributed to Samuelsons Proof. He argues that this

argument is not necessarily true, as “there is no reason why a subjective assessment of

asset value must follow a random walk”. This topic is clearly subject to some

disagreement over the most appropriate method and assumptions to apply. However,

Copeland & Antikarov (2005) has answered this criticism by objecting to the statement

of subjective input parameters, as they clarify that a Monte Carlo simulation should be

used to model the uncertainty to calculate the volatility of the rate of return on the

project, thereby incorporating market data. The simulation can include input variables

correlated or uncorrelated with the market (i.e. public and private). In regards to the

stochastic nature of the input variables, they state that when modelling the inputs for the

cash flows they do not assume a GBM process. However, when estimating the volatility

of the rate of return of the project they argue that this follows a GBM process as

“changes in expectations are random, even though the expected cash flows have a

cyclical pattern” (e.g. mean-reversion in some commodities).

2.5.4.4 The Revised Classic Approach

This approach instructs that classic finance-based real options should be used where

investments are dominated by market-priced/public risks. Dynamic

programming/decision analysis should be used when investments are dominated by

private risks. The classic finance-based real options are interpreted just like with the

classic approach. For dynamic programming/decision analysis it is more complicated,

as the investment is dominated by private risks and subjective assessments are used to

evaluate risks.

Dixit & Pindyck (1994) explains this method as using contingent claims analysis

(option pricing) where the value of the asset is spanned by existing assets in the

economy (e.g. commodities traded on spot and/or future markets and goods that are

correlated with the values of shares or portfolios). When the value of the asset is not

Page 30 of 79

spanned, they suggest using dynamic programming/decision analysis. Amram &

Kulatilaka (1999) use the term ‘tracking’ instead of ‘spanned’ to make a similar

argument.

The primary difficulty in this approach is separating the investments in public or private

risks. After this, the approach suffers from the same problems as the classic approach

when risks are market driven. When risks are private in nature the problems of decision

analysis persists. For decision analysis it is a problem of getting correct subjective

inputs from experts.

2.5.4.5 The Integrated Approach

This approach separates the public and private risks like the revised classic approach,

however, this approach does not choose between an either public or privately dominated

investment, it determines which risks are public and which are private. Public risks are

assessed by identifying the replicating portfolio and applying no-arbitrage assumption

as in the classic approach. Private risks are assessed subjectively as in the revised

classic approach. The Integrated approach does not assume GBM. Borison (2005)

considers this approach to be more burdensome and difficult to explain to management,

however he also concludes that the integrated approach is based on the most accurate

and consistent theoretical and empirical foundation and should be applied where

quality and credibility is important (Borison 2005).

In the case study I will apply The MAD Approach described by Copeland & Antikarov

(2005), as this approach is the most intuitively appealing and it assumes no-arbitrage,

enabling the use of market data. It assumes that there is no perfectly correlated twin

security, but instead uses the NPV of the project without flexibility. The MAD approach

also allows me to estimate the volatility of the rate of return of the project by simulation

of changes in project value, thereby incorporating as much market information as

possible.

2.5 Solution Techniques

There are three general options valuation techniques for valuing real options: Partial

Differential Equations, Simulation and Lattices. Each of these techniques has different

solution methods applicable in different situations (Amram & Kulatilaka 1999,

Kodukula & Papudesu 2006). I will review the basics of these techniques, as well as the

limitations, assumptions, and applicability to the case. This will allow me to illustrate

Page 31 of 79

why the chosen method is applied and how other techniques could be useful in other

instances.

Figure 4: Real options solution techniques, source: Kodukula & Papudesu 2006

2.5.1 Partial Differential Equations

Partial differential equations (PDE) includes closed form solutions, where the most

widely known is the Black-Scholes equation. Other partial differential equations include

analytical approximation and numerical methods such as finite difference method. A

PDE can be defined as “an equation describing the changes in option values to changes

in the underlying asset value”. The option value is calculated by using the PDE and the

boundary conditions (equations describing decision rules and extreme values of the

option value). If possible, an analytical solution or closed-form solution like B&S can

then be calculated. However, option features such as multiple sources of uncertainty or

sequential options will make an analytical solution too complex (Amram & Kulatilaka

1999). If an analytical analysis is unfeasible, another solution method such as the

binomial model can be chosen, as this method can handle many types of real options. I

will only review the B&S model of the PDE’s as they can be very difficult to solve and

has many limitations which other methods can overcome (e.g. numerical methods can

typically only handle two sources of uncertainty) (Amram & Kulatilaka 1999, p.110).

Black & Scholes developed the first closed form equations, which assumes

deterministic exercise price of the real options:

B&S Equation: C = N(d1) S0 – N(d2) X exp(-rT)

C is the value of the call option, S0 is the current value of the underlying asset, X is the

cost of the investment or strike price, r is the risk-free rate, T is the time to expiration, d1

Page 32 of 79

equals [ln (S0/X) + (r + 0.5σ2)T]/T, d2 is equal to d1- σ √T, σ is the annual volatility of

the future cash flows of the underlying asset, and N(d1) and N(d2) are the values of the

standard normal distribution of d1 and d2 (Kodukula & Papudesu 2006). Copeland &

Antikarov (2004) lists seven assumptions of the B&S model. I have reviewed them and

explained why most of the assumption often is not met in a real corporate investment

project.

1. B&S assumes that the option to be valued is a European type option, however

most real options are possible to exercise early (e.g. abandoning a mine before

the resources are exhausted.

2. The option depends on only one source of uncertainty; the cash flows of a

natural resource investment will depend on more variables than the resource

market price, such as investment costs and operating costs.

3. The option depends solely on one underlying asset. This assumption rules out

valuing compound options such as staged construction.

4. No dividend; competition eroding profits can be seen as an analogy to dividends

5. Market price and stochastic process of the underlying are known; when the

market is liquid for the resource in questions this assumption can hold true.

However if the market is illiquid the market price can be unobservable.

6. The volatility is constant; the volatility may change as options are exercised, e.g.

if an option is exercised, it changes the riskiness of the project, the project

volatility will be changed.

7. Exercise price is known and constant; the price of an expansion will be an

estimate, which will often differ from the true cost.

As highlighted, the assumptions of the B&S model are very restrictive in a real options

setting, but other solution method will also require some of the assumptions to be

relaxed. Looking at real options methodologies applied in practice, the B&S model is

applied only sparingly, as the assumptions are generally not met. Further, the formula

does not reveal to the management how the option values are obtained, the term “black

box” has been used to describe the model’s lack of intuitive and explanatory features,

unlike the binomial lattice model (Triantis & Borison 2005).

Page 33 of 79

2.5.2 Monte Carlo Simulation

Monte Carlo simulation (MCS) can be used for valuing European options and American

type options. Boyle (1977) suggested valuing European options by simulating price

movements, thereby approximating a probability distribution of the option. The average

of the cash flow simulation is calculated and then discounted using the risk-free rate

(Gonzalo Cortazar 2000). Simulation for real option solutions are similar to the

technique for the NPV analysis described earlier. American and European options have