VALUATION REPORT - TASE

39

VALUATION REPORT 490,950 sq. m land Afumati Commune, Ilfov County, Romania Intercolony Investments Limited Valuation Date: 31 st of December 2014

Transcript of VALUATION REPORT - TASE

VALUATION REPORT

490,950 sq. m land

Afumati Commune,

Ilfov County, Romania

Intercolony Investments Limited

Valuation Date: 31st

of December 2014

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY

2 VALUATION REPORT

3 PROPERTY REPORT

PROPERTY DETAILS

LEGAL CONSIDERATIONS

VALUATION METHODOLOGY

OPINION OF VALUE

4 MARKET REPORTS

The contents of this Report may only be relied upon by:

(i) Addressees of the Report; or

(ii) Parties who have received prior written consent from CBRE in the form of a reliance letter.

This Report is to be read and construed in its entirety and reliance on this Report is strictly subject to the

disclaimers and limitations on liability on page 7. Please review this information prior to acting in reliance

on the contents of this Report. If you do not understand this information, we recommend you seek

independent legal counsel.

EXECUTIVE SUMMARY

2

1

EXECUTIVE

SUMMARY

EXECUTIVE SUMMARY

3

EXECUTIVE SUMMARY

The Property

Address: Afumati Commune, Ilfov County, Romania

Best Use: agricultural land

Property rights

From the client’s information and documentation provided to us we understand that the

above mentioned property is owned on the equivalent of freehold of SC TACTICAL

PROPERTY SRL.

Fair Value

€1,476,000 (ONE MILLION FOUR HUNDRED SEVENTY THOUSANDS

EUR), exclusive of VAT

Forced Sale Value

The forced sale value or the liquidation value is the estimated amount of money that an

asset could quickly be sold for; when it is allowed insufficient time to sell on the open

market, thereby reducing its exposure to potential buyers. The forced sale value can

involve a seller compelled to sell and a buyer(s) that purchase(s) fully aware of the

seller’s disadvantage. Forced sale value is a situation when the transaction is actually

closed and does not represent a type of value according Valuation Standards. As a

consequence of this aspect, the analysis of estimated price in a forced sale does not

meet the valuation conditions, being an exception of the Valuation Standards

requirements.

We estimate the forced sale value for the analysed real estate property based on the

following criteria:

Property type;

Location;

EXECUTIVE SUMMARY

4

Medium exposure time for an agricultural land, on the open market, is

approximately 12-18 months, considering the existing demand for similar

properties, but the restricted access to mortgage and liquidities;

In case of a forced sale with an exposure time on the open market less than 6 months,

we estimate a 50% discount from current market value.

Based on the above specifications, in our opinion, forced sale value of the analyzed

property, as at 31st

December 2014, is:

€738,000 (SEVEN HUNDRED THIRTY EIGHT THOUSAND EUROS)

VALUATION REPORT

5

2

VALUATION REPORT

VALUATION REPORT

6

VALUATION REPORT

Report Date 09th

of March 2015

Addressee Intercolony Investments Limited

Client Intercolony Investments Limited

The Property The property consists in 40 land parcels situated in 7

different fields, having the total area of 490,950 sq m.

Ownership Purpose Investment

Instruction To provide our opinion on the Fair Value of the subject

property as at the Valuation Date in accordance with

client’s instruction dated 10th

February 2015.

Valuation Date 31st

of December 2014

Capacity of Valuer External

Purpose Financial reporting

Fair Value €1,476,000 (ONE MILLION FOUR HUNDRED

SEVENTY THOUSANDS EUR), exclusive of VAT

Our opinion of Fair Value is based upon the Scope of

Work and Valuation Assumptions attached.

Compliance with

Valuation Standards

The valuation has been prepared in accordance with The

RICS Valuation – Professional Standards January 2014

(“the Red Book”). In addition, the valuation is also

prepared in compliance with IFRS 13 (International

Financial Reporting Standards 13 – fair value

measurement).

The property details on which valuation is based on are

as set out in this report.

Special Assumptions None.

Assumptions We have made various assumptions as to tenure, town

planning, and the condition of the site – including

ground and groundwater contamination – as set out

VALUATION REPORT

7

below.

If any of the information or assumptions on which the

valuation is based are subsequently found to be

incorrect, the valuation figures may also be incorrect and

should be reconsidered.

The allocations of value for any land distribution must

not be used in conjunction with any other appraisal and

are invalid if so used.

Market Conditions The values stated in this report represent our objective

opinion of Market Value in accordance with the

definition set out above as of the date of

valuation. Amongst other things, this assumes that the

properties had been properly marketed and that

exchange of contracts took place on this date.

Going forward, we would draw your attention to the fact

that the current volatility in the global financial system

has created a significant degree of turbulence in

commercial real estate markets across the

world. Furthermore, the lack of liquidity in the capital

markets means that it may be very difficult to achieve a

sale of property assets in the short-term. We would

therefore recommend that the situation and the

valuations are kept under regular review, and that

specific marketing advice is obtained should you wish to

effect a disposal.

Valuer The Property has been valued by a valuer who is

qualified for the purpose of the valuation in accordance

with the RICS Valuation – Professional Standards January

2014 (The Red Book).

Independence The amount representing the payment for our drafting

this report has no connection whatsoever with

mentioning in the report a certain value (from the

valuation) or interval of values that might be favourable

to the client nor is it influenced by the occurrence of a

subsequent event.

Conflict of Interest We have no personal interest or bias with respect to the

subject matter of this appraisal report or the parties

involved.

VALUATION REPORT

8

Reliance This report is for the use only of the party to whom it is

addressed for the specific purpose set out herein and no

responsibility is accepted to any third party for the whole

or any part of its contents.

The appraiser will not be required to give testimony or

appear in court because of having made this appraisal,

with reference to the property in question, unless

previous arrangements have been made.

Publication

Liability Notice

Neither the whole nor any part of our report nor any

references thereto may be included in any published

document, circular or statement nor published in any

way without our prior written approval of the form and

context in which it will appear.

This valuation report (the “Report”) has been prepared

by CBRE Real Estate Consultancy SRL (“CBRE”)

exclusively for Intercolony Investments Limited (the

“Client”) in accordance with the terms of the instruction

letter dated 10th

of February 2015 (“the Instruction”).

The Report is confidential. It must not be disclosed to any

person other than the Client without CBRE's prior written

consent. CBRE has provided this report on the

understanding that it will only be seen and used by the

Client and no other person is entitled to rely upon it,

unless CBRE has expressly agreed in writing.

Where CBRE has expressly agreed that a person other

than the Client can rely upon the report then CBRE shall

have no greater liability to any party relying on this

report than it would have had if such party had been

named as a joint client under the Instruction.

CBRE’s maximum aggregate liability to all parties,

howsoever arising under, in connection with or pursuant

to reliance upon this Report, and whether in contract,

tort, negligence or otherwise shall not exceed the lower

of:

(i) 25% of the value of the property to which the

relates on the date of the Instruction; or

(ii) 20,000 Euro; and

CBRE shall not be liable for any indirect, special or

consequential loss or damage howsoever caused,

VALUATION REPORT

9

whether in contract, tort, negligence or otherwise, arising

from or in connection with this Report. Nothing in this

Report shall exclude liability which cannot be excluded

by law.

Yours faithfully

Ovidiu Ion, MRICS

Director

Head of Valuation

For and on behalf of

CBRE

T: +40 21 302 50 81

Yours faithfully

Florin Ianculescu-Popa

Senior Valuer

For and on behalf of

CBRE

T: +40 21 302 50 84

VALUATION REPORT

10

SCOPE OF WORK & SOURCES OF

INFORMATION

Sources of

Information

We have carried out our work based upon information

supplied to us by the client, which we have assumed to

be correct and comprehensive.

Information furnished by others is assumed to be true,

correct and reliable. A reasonable effort has been

made to verify such information; however, the appraiser

assumes no responsibility for its accuracy. If, for any

reason, future investigations should prove any data to

be in substantial variance with that presented in this

report, the appraiser reserves the right to alter or

change any or all conclusions and/or estimates of

value.

The Property Our report contains a brief summary of the property

details on which our valuation has been based on.

Inspection No inspection.

Areas We rely on the areas as provided by the client to us. We

did not perform effective measurements of the real

estate.

A legal description may not have been furnished, and it

is assumed that the physical characteristics of the

property, with regard to metres and bounds and road

frontages, are essentially as depicted on the plat of the

property.

Environmental

Matters

We have not carried out any investigation into the past

or present uses of the Property, nor of any neighbouring

land, in order to establish whether there is any potential

for contamination and have therefore assumed that

none exists.

Condition We have not carried out any surveys, tested services,

made site investigations, nor any evidence report to

provide the condition of the site.

VALUATION REPORT

11

Town Planning The real estate is assumed consistent with all the

regulations and restrictions related to zoning and use,

except for the situation when non-compliance is

identified, described and considered in this report.

It is assumed that all applicable zoning and use

regulations and restrictions have been complied with,

unless nonconformity has been stated, defined and

considered in the appraisal report.

We have not made verbal enquiries with the local

authority. We have relied upon the planning

information provided by Intercolony Investments Limited.

Titles, Tenures and

Lettings

Details of title/tenure under which the Property is held

and of lettings to which it is subject are as supplied to

us. We have not generally examined nor had access to

all the deeds, leases or other documents relating

thereto. Where information from deeds, leases or other

documents is recorded in this report, it represents our

understanding of the relevant documents. We should

emphasise, however, that the interpretation of the

documents of title (including relevant deeds, leases and

planning consents) is the responsibility of your legal

adviser.

We have not conducted credit enquiries on the financial

status of any tenants. We have, however, reflected our

general understanding of purchasers’ likely perceptions

of the financial status of tenants.

VALUATION REPORT

12

VALUATION ASSUMPTIONS

Valuation Basis

The value of each of the properties has been assessed

in accordance with the relevant parts of RICS Valuation

– Professional Standards (January 2014). In particular,

we have assessed the Fair Value of the properties in

accordance with VS3.5 item 2. Under these provisions,

the term "Fair Value" means:

"The price that would be received to sell an asset, or

paid to transfer a liability, in an orderly transaction

between market participants at the measurement date".

No allowances have been made for any expenses of

realisation nor for taxation which might arise in the

event of a disposal. Acquisition costs have not been

included in our valuation.

No account has been taken of any inter-company

leases or arrangements, nor of any mortgages,

debentures or other charges.

The Property The property is valued as agricultural land.

All measurements, areas and limits are approximately

considered based on survey plans provided to us.

Environmental

Matters

In the absence of any information to the contrary, we

have assumed that:

(a) the Property is not contaminated and is not adversely

affected by any existing or proposed environmental law;

(b) any processes which are carried out on the Property

which are regulated by environmental legislation are

properly licensed by the appropriate authorities.

Repair and Condition In the absence of any information to the contrary, we

have assumed that:

(a) there are no abnormal ground conditions, nor

archaeological remains, present which might adversely

affect the current or future occupation, development or

value of the property;

(b) the Property is free from infestation or latent defect.

VALUATION REPORT

13

Title, Tenure,

Planning and Lettings

Unless stated otherwise within this report, and in the

absence of any information to the contrary, we have

assumed that:

(a) the Property possesses a good and marketable title

free from any onerous or hampering restrictions or

conditions;

(b) all buildings have been erected either prior to

planning control, or in accordance with planning

permissions, and have the benefit of permanent

planning consents or existing use rights for their current

use;

(c) the Property is not adversely affected by town

planning or road proposals;

(d) all buildings comply with all statutory and local

authority requirements including building, fire and

health and safety regulations;

(e) only minor or inconsequential costs will be incurred

if any modifications or alterations are necessary in order

for occupiers of each Property to comply with the

provisions of the relevant disability discrimination

legislation;

(f) there are no tenant’s improvements that will

materially affect our opinion of the rent that would be

obtained on review or renewal;

g) tenants will meet their obligations under their leases;

h) there are no user restrictions or other restrictive

covenants in leases which would adversely affect value;

(i) where appropriate, permission to assign the interest

being valued herein would not be withheld by the

landlord where required; and

(j) vacant possession can be given of all

accommodation which is unlet or is let on a service

occupancy.

PROPERTY REPORT

14

3

PROPERTY REPORT

PROPERTY REPORT

15

PROPERTY DETAILS

Location

The subject Property is located in Afumati. The commune of Afumati is located 16 km

North-East of Bucharest, on DN2 National Road. DN2 connects the Capital with the

region of Moldavia in North-East Romania.

According to the National Statistics Office, the population of Afumati is approximately

7,919 inhabitants as of 2011 national census, while the entire population of Ilfov

County is of 388,738 inhabitants. The total area of Afumati is 6,325 ha, from which

489 ha represent urban land and 5836 ha represent non-urban land, with main use as

agricultural land. Afumati is the third locality in terms of agricultural area from Ilfov

County.

From the 55 km representing total road network, 15 km are asphalt roads and 40 km

are gravel roads.

In the last years, the area has attracted several speculative investors who purchased

undeveloped sites designated for residential units. Along DN2 the land acquired logistic

and industrial use, due to the proximity of Bucharest and the vehicular connections.

For 2014, the local taxes for non-urban land were between 22RON and 30.8RON for

grassland and between 46.2RON and 55RON per ha, for arable land.

Location map is attached in Appendix A.

Situation

The property is located in the North non-urban area of Afumati, with no access to a

main road.

The property consists in 40 land parcels situated in 7 different fields, having the total

area of 490,950 sq. m. The land parcels have a rectangular shape and the area

between 1,200 sq. m and 56,500 sq. m.

The immediate surroundings is predominantly characterised by land under agricultural

use.

The plots are located between DJ 100, DJ200 and DJ200A, without car access any

utility such as electricity, gas, water and sewage.

The distances to a main road are as follows:

Field 12 is located at approx. 1,000 m from DJ200, Stefanesti-Dascalu road;

Field 16 is located at approx. 500 m from DJ200, Stefanesti-Dascalu road;

PROPERTY REPORT

16

Field 19 and Field 20 are located at approx. 600 m from DJ100, Afumati-Stefanesti

road;

Field 21 and Field 22 are located at approx. 1,000 m from DJ200, Stefanesti-

Dascalu road;

Field 32 is located at approx. 1,200 m from DJ200A, Afumati-Petrachioaia road.

Environmental Considerations

We have not been provided with copies of any environmental reports or certificates from

the Owners of the Property. We would recommend that clarification should be sought

from your legal representatives in relation to any contamination concerns or health and

safety issues that could be present at the Property.

We have not conducted any environmental analysis of the Property. We have therefore

assumed that there are no environmental issues affecting the Property, or if so, that

contamination is minor in nature and will not materially affect the continued use of the

Property.

Town Planning

We have not made any further verbal enquiries to the planning department and have

assumed that the current use of the Site does not contravene any town planning

regulations. We were provided with documents by the current owner and have assumed

these to be complete and correct.

PROPERTY REPORT

17

VAT

We have not been advised whether the property is elected for VAT.

All values stated in this report are exclusive of VAT.

PROPERTY REPORT

18

LEGAL CONSIDERATIONS

Ownership Titles

We understand that SC TACTICAL PROPERTY SRL holds the property freehold.

According to the Cadastral Documentation, the property has a total area of 490,950 sq.

NO. FIELD PLOT NO. CADASTRAL NO.

1 16 65/7 1418/1

2 19 90/29 1781

3 19 90/30 1891

4 19 90/31 1780

5 19 90/32 1537

6 19 90 536

7 19 90 1273

8 19 90/43 964

9 19 90/27 1307

10 19 90/23/1 1265

11 19 90/23 1460

12 19 90/23/1 1266

13 19 90/33/2 2705

14 19 90/33/1 2707

15 19 90/28 n/a

16 19 90/17 2737

17 19 90/5 1479/1

18 20 94/25 2840

19 21 100 1785

20 21 100 61705

21 21 100 1888

22 21 100 2722

23 21 100 1183

24 21 100 2278

25 21 100/27 1176

26 21 100/7 2606

27 21 100/4 1248

28 22 102/7 1681

29 12 45 2221

30 12 45 2020

31 12 45/47 2609

32 12 45/7 2431

33 12 45/7 2232

34 12 45/8 2376

35 12 45/16 1228

36 12 45/17 1229

37 12 45/6 2700

38 32 136 1505

39 32 135/41 2172

40 32 136/38 1763

PROPERTY REPORT

19

VALUATION METHODOLOGY

Market Comparison Approach

In assessing the market value of the property, we have carried out the market

comparison approach.

We have analysed the agricultural lands, which are in offer stage in the area of Afumati

Commune.

We performed several tasks in developing an opinion of land value:

Gather data on actual sales as well as offers and options.

Identify the similarities and differences in the data.

Identify the highest and best use of each potential comparable sale.

Adjust the sale prices of the comparable to account for the dissimilar

characteristics of the appraised land.

Form a conclusion as to the market value of the subject land.

It is usually reasonable to assume that the subject property will sell for an amount similar

to the adjusted sale prices of the comparable properties or less than the adjusted list

prices of properties on the market or recently off the market.

Land offers in Afumati Commune area

The average asking prices vary between €1.20/sq m and €7/sq m depending on the size

of the land parcel and the proximity to a main road and utilities.

A limited number of investment transactions characterize local market and the use of

investment data is restricted due to the lack of public accessibility to private sector

information. When transactions actually occur, the terms of the exchange are not

disclosed to the public, thereby precluding positive comparability.

As the local market is of immature, non-transparent and strictly confidential natures,

absolute reliable comparable properties to subject site were not available to us. In order

NO. LOCATION TOTAL AREA ASKING PRICE PRICE/SQ. M

1 Afumati 1,000,000 1,200,000 1.20

2 Gradistea 28,000 33,600 1.20

3 Petrachioaia Surlari 25,000 37,500 1.50

4 Petrachioaia 57,500 86,250 1.50

5 Balaceanca- Cernica 12,000 22,000 1.83

6 Bucuresti_Urziceni E85 Area 10,000 20,000 2.00

7 Gradistea 1,000,000 2,500,000 2.50

8 Afumati Ganeasa 25,000 75,000 3.00

9 Afumati Petrachioaia 12,600 50,400 4.00

10 Afumati Petrachioaia 36,000 252,000 7.00

PROPERTY REPORT

20

to support assessed market values, we have to rely on our market knowledge, experience

and discussion with other local agents in the market.

The adjustments that have been made are based on the following criteria:

Adjustment for negotiation 10 – 30% based on local market facts (interviews

with brokers, local investors)

Location: negative or positive adjustments according to the location in the

studied area

Size and access: negative or positive adjustments according to the size, access,

facilities and shape of the each plot

It is usually reasonable to assume that the subject will sell for an amount similar to the

adjusted sale prices of the comparable properties or less than the adjusted list prices of

properties on the market or recently off the market.

The offers data were adjusted to reflect the differences between them and the subject

property. After adjustments were made, the data ranges from 2 to 5 EUR /sq m.

From this interval of prices we have chosen 4 EUR / sq m as a reference value for the

subject property and allocated this value to Field 16 and Field 19 which are the closest

to the facilities and have better access.

A ranking analysis was used to differentiate the subject fields’ values for specific elements

of comparison such as access and distance to facilities. The technique can be used to

test the specific elements of comparison for their market sensitivities. The subject fields

were ranked according to overall comparability with Field 16 and Field 19.

After making the adjustments, the value for the subject property is as follows:

Field 16, Field 19 – €4/ sq. m;

Field 20, Field 21 and Field 22 - €3/ sq. m;

Field 12, Field 32 - €2.5/ sq. m.

FIELD NO. AREA (SQ M)

UNITARY VALUE

(EUR/ SQ M) VALUE (EUR)

FIELD 16 10,650 4 42,600

FIELD 19 115,300 4 461,200

FIELD 20 26,000 3 78,000

FIELD 21 82,800 3 248,400

FIELD 22 11,000 3 33,000

FIELD 12 198,800 2.5 497,000

FIELD 32 46,400 2.5 116,000

Total land 490,950 1,476,200

PROPERTY REPORT

21

OPINION OF VALUE

Fair Value

Given the purpose of the valuation and considering the data available and the inherent

characteristics of the property as well we consider that the fair value of the subject

property as at 31st

of December 2014 is:

€1,476,000 (ONE MILLION FOUR HUNDRED SEVENTY THOUSANDS EUR),

exclusive of VAT

Our opinions of values are based upon the Scope of Work and Valuation Assumptions &

Considerations included in the present report.

LOCATION PLANS

22

A

LOCATION PLANS

LOCATION PLANS

23

LOCATION PLANS

MARKET REPORTS

24

4

MARKET REPORTS

MARKET REPORTS

25

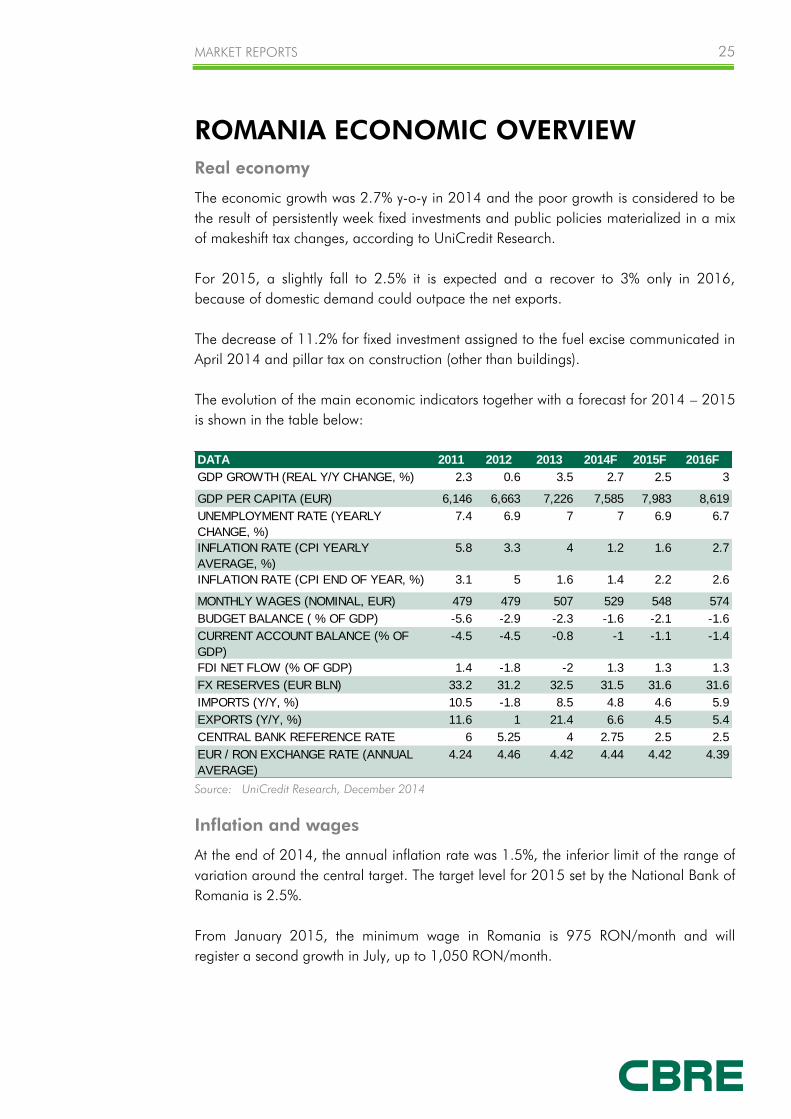

ROMANIA ECONOMIC OVERVIEW

Real economy

The economic growth was 2.7% y-o-y in 2014 and the poor growth is considered to be

the result of persistently week fixed investments and public policies materialized in a mix

of makeshift tax changes, according to UniCredit Research.

For 2015, a slightly fall to 2.5% it is expected and a recover to 3% only in 2016,

because of domestic demand could outpace the net exports.

The decrease of 11.2% for fixed investment assigned to the fuel excise communicated in

April 2014 and pillar tax on construction (other than buildings).

The evolution of the main economic indicators together with a forecast for 2014 – 2015

is shown in the table below:

Source: UniCredit Research, December 2014

Inflation and wages

At the end of 2014, the annual inflation rate was 1.5%, the inferior limit of the range of

variation around the central target. The target level for 2015 set by the National Bank of

Romania is 2.5%.

From January 2015, the minimum wage in Romania is 975 RON/month and will

register a second growth in July, up to 1,050 RON/month.

DATA 2011 2012 2013 2014F 2015F 2016F

GDP GROWTH (REAL Y/Y CHANGE, %) 2.3 0.6 3.5 2.7 2.5 3

GDP PER CAPITA (EUR) 6,146 6,663 7,226 7,585 7,983 8,619

UNEMPLOYMENT RATE (YEARLY

CHANGE, %)

7.4 6.9 7 7 6.9 6.7

INFLATION RATE (CPI YEARLY

AVERAGE, %)

5.8 3.3 4 1.2 1.6 2.7

INFLATION RATE (CPI END OF YEAR, %) 3.1 5 1.6 1.4 2.2 2.6

MONTHLY WAGES (NOMINAL, EUR) 479 479 507 529 548 574

BUDGET BALANCE ( % OF GDP) -5.6 -2.9 -2.3 -1.6 -2.1 -1.6

CURRENT ACCOUNT BALANCE (% OF

GDP)

-4.5 -4.5 -0.8 -1 -1.1 -1.4

FDI NET FLOW (% OF GDP) 1.4 -1.8 -2 1.3 1.3 1.3

FX RESERVES (EUR BLN) 33.2 31.2 32.5 31.5 31.6 31.6

IMPORTS (Y/Y, %) 10.5 -1.8 8.5 4.8 4.6 5.9

EXPORTS (Y/Y, %) 11.6 1 21.4 6.6 4.5 5.4

CENTRAL BANK REFERENCE RATE 6 5.25 4 2.75 2.5 2.5

EUR / RON EXCHANGE RATE (ANNUAL

AVERAGE)

4.24 4.46 4.42 4.44 4.42 4.39

MARKET REPORTS

26

The gross average national wage in August 2014 was 2,331 RON/ month (equiv. of

525 EUR), slightly higher than the similar period of 2013. The highest average values

were registered in air transport industry as 5,277 RON/ month (equiv. of 1,188 EUR)

and the lowest values in hotel and restaurants industry as 1,366 RON/month (equiv. of

308 EUR).

With 3,240 RON/ month (729 EUR), the average salary in Bucharest is approx. 38%

higher than the national average.

Foreign investment

Foreign Direct Investments in the first half of year 2014 were EUR 1.2 billion. The level

for this year was slightly lower than in the precedent year, but considerably higher than in

2012. FDI level in 2013 registered the highest level of the last 4 years – EUR 2.7 billion,

with an increase of 26.8%.

The highest level was registered in 2008, when EUR 9.5 billion were attracted in the

Romanian economy. The construction and real estate sectors accounted for approx.

13% out of the total level of 2008.

Foreign Direct Investments Romania, 2007 – 2014* estimated

Source: CBRE based on National Bank of Romania

Remittances

For many years, money transfers from Romanians working abroad have been a lifeline

for the economy, with an important impact on the real estate market as well. The highest

level of remittances of EUR 6.51 billion was registered in 2008, whilst 2013 witnessed

the lowest level in the last 8 years of EUR 3.0 billion (EUR 3.7 billion in 2012).

MARKET REPORTS

27

Remittances, 2005 - 2014

Source: CBRE based on National Bank of Romania

National Bank of Romania ('NBR') Interest Rate

The monetary policy interest rate is the interest rate on NBR’s main open-market

operations. The interest rates on the NBR's standing facilities, i.e. the deposit facility and

the lending facility, were set at +/- 4 percentage points around the monetary policy rate

as from 7 May 2008.

As of beginning of 2014, the monetary policy interest rate was decreased 5 times from

3.75% in January to 2.75% in November.

Romania National Bank’s monetary policy interest rate, 2007 – December

2014

Source: CBRE based on National Bank of Romania 2015

MARKET REPORTS

28

Exchange rate

Romanian currency was in December 2014 RON 4.45/ 1 EUR, at a slightly lower level

as of beginning of the year (RON 4.5219/ 1 EUR).

During the last 2 years there were 2 peak levels: RON 4.64/ EUR 1 in August 2012

and RON 4.55/ EUR 1 in June 2013.

MARKET REPORTS

29

LOCAL ECONOMY- BUCHAREST

Demographic Data

Bucharest is the capital and political, economic and cultural centre of the country, with a

population of 1,883,425 according to the latest population census, as of October

2011. The capital is by far the highest populated city in Romania, with about 9% of

entire country’s population:

The population/ city and population/ county in Romania

Source: CBRE based on National Institute of Statistics

The number of people living in Bucharest is expected to grow in the coming years,

despite the general decreasing trend registered over the past 10 years both across the

country and across Bucharest. Several factors determine the increase of population as

the city gathers more than half of the foreign investments in Romania and the average

net salary is the highest thus attracts skilled labour force from across the country, no

taking into account the foreigners that are employed by the multinational corporations

with branches in Bucharest.

Population Composition

The population in Bucharest according to age groups, comparative for Bucharest/Ilfov

county and overall Romania is structured as follows:

CITYPOPULATION /

CITY

RANKING

PER CITYCOUNTY

POPULATION /

COUNTY

RANKING

PER COUNTY

Bucharest 1,883,425 1 Bucharest 1,883,425 1

Cluj Napoca 324,576 2 Iasi 772,348 2

Timisoara 319,279 3 Prahova 762,886 3

Iasi 290,422 4 Cluj 691,106 4

Constanta 283,872 5 Constanta 684,082 5

MARKET REPORTS

30

Structure of Population by age groups

Source: CBRE based on National Institute of Statistics

As seen above, the younger population in Bucharest (aged under 20 years old) is

smaller, percentagewise) as compared with Ilfov and overall Romania (16% vs. approx.

22%). As a consequence, the population aged 20 – 64 (which contributes significantly to

the GDP) is more consistent in Bucharest (69% vs. 65% for Ilfov and 62.5% for

Romania). The older population (of over 65 years old) is the most numerous in overall

Romania (approx.16%) while in Bucharest is 14.4% and Ilfov County the percentage is

approx. 13%.

Income

In August 2014, with gross 3,240 RON/ month (729 EUR), the average salary in

Bucharest is approx. 38% higher than the national average.

Comparison Wages Bucharest/Romania EUR

Source: CBRE based on National Institute of Statistics, 2014

MARKET REPORTS

31

However, it is widely believed that real earnings all over Romania are around 30%

higher than the declared ones, as people supplement their income with shadow market

activities or just do not declare their full earnings. Taking this into consideration the

monthly net income for a person in Bucharest could be nearer to EUR 680.

Gross Domestic Product

Bucharest is the centre of the Romanian economy and industrial output, accounting for

approximately 23% of the country's GDP and about one-quarter of Romania’s industrial

production, although it is only inhabited by 9% of the nation’s population.

Additionally, Bucharest’s citizens and companies pay almost one third of national taxes.

The GDP/capita in Bucharest was of approx. EUR 14,772/capita in 2012 and in 2013 it

is estimated to reach EUR 15,636/ capita.

GDP/Capita in Bucharest EUR

Source: CBRE based on National Commission for Prognosis 2014

Employment

In Bucharest, the total number of employees was of 895,196 persons in August 2014.

More than three quarters of Bucharest’s workforce activates in the services sector (78%),

while the industry and construction represent 21% of the total number of employees in

Bucharest. The agriculture and other services account for less than 1% of the total

workforce population.

According to the National Institute of Statistics, the unemployment rate in Bucharest

(related to the total active population) was relatively constant since June 2011 until June

2014 to 2.0% - 2.1%. This level is approx. 2.3 times lower than the national average of

4.9% (as of June 2014). The only county with lower unemployment rate is Ilfov County

(1.5%), but the majority of the population living in this county is working in Bucharest.

0

5,000

10,000

15,000

20,000

25,000

2008 2009 2010 2011 2012 2013*2014*2015*2016*2017*

EU

R/

capi

ta

MARKET REPORTS

32

Evolution Unemployment Rate Bucharest – Romania – Ilfov County

Source: CBRE based on National Institute of Statistics, 2014

MARKET REPORTS

33

INVESTMENT MARKET COMMENTARY

General Overview

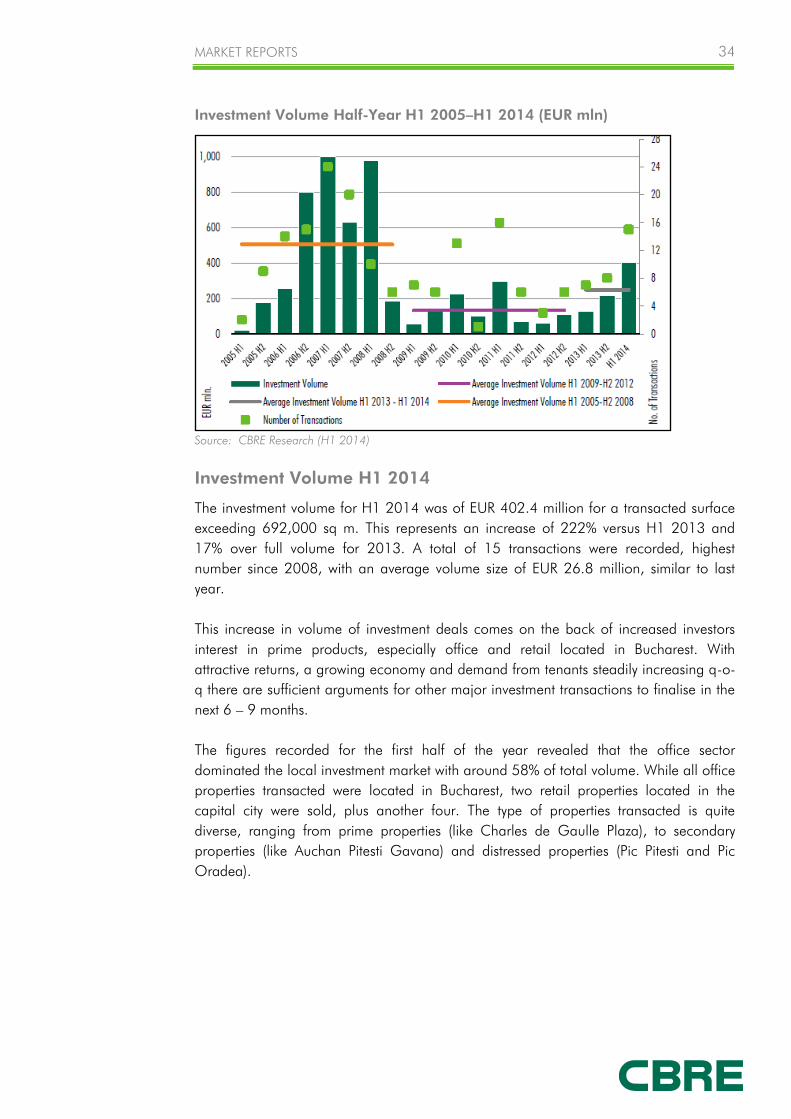

The investment volume in Romania in H1 2014 rose by 222% compared to H1 2013,

reaching approx. EUR 402.4 million. This represents the highest volume per half year

since H1 2008.

H1 2014 H2 2013

CEE Investment Volume (EUR bln) 3,723 5,024

Romania Total Investment Volume (EUR mln) 402.4 217.9

No Transactions 15 8

Average Transactions Size (EUR mln) 27 27

Positive macroeconomic forecast place GDP growth at around 3% for 2014 and 3.2%

for 2015. Excluding Russia, CEE investment volume on the rise versus H1 2013,

reaching a total of EUR 2.56 billion, with Poland, Czech Republic generating the highest

investment volume.

Profile of transactions was quite diverse in terms of sector (office segment leading with

58% of total volume), in terms of type of properties (prime properties generating 55% of

total volume), in terms of buyer typology (developers and institutional funds the most

active, out of which Globalworth generating 54% of volume).

Land transactions are on the rise in terms of number, volume value and type of

properties. Three major types of buyers active in the market: retailers, industrial/

production occupiers and office developers.

On the back of increased investors’ interest, prime yield for office segment compressed

at 8%. Other yields stable. In terms of prime rent, the evolution is relatively stable: EUR

60/sq m/mth - shopping centre, EUR 18/sq m/mth - office and EUR 3.8 /sq m/mth-

industrial.

MARKET REPORTS

34

Investment Volume Half-Year H1 2005–H1 2014 (EUR mln)

Source: CBRE Research (H1 2014)

Investment Volume H1 2014

The investment volume for H1 2014 was of EUR 402.4 million for a transacted surface

exceeding 692,000 sq m. This represents an increase of 222% versus H1 2013 and

17% over full volume for 2013. A total of 15 transactions were recorded, highest

number since 2008, with an average volume size of EUR 26.8 million, similar to last

year.

This increase in volume of investment deals comes on the back of increased investors

interest in prime products, especially office and retail located in Bucharest. With

attractive returns, a growing economy and demand from tenants steadily increasing q-o-

q there are sufficient arguments for other major investment transactions to finalise in the

next 6 – 9 months.

The figures recorded for the first half of the year revealed that the office sector

dominated the local investment market with around 58% of total volume. While all office

properties transacted were located in Bucharest, two retail properties located in the

capital city were sold, plus another four. The type of properties transacted is quite

diverse, ranging from prime properties (like Charles de Gaulle Plaza), to secondary

properties (like Auchan Pitesti Gavana) and distressed properties (Pic Pitesti and Pic

Oradea).

MARKET REPORTS

35

Profile of transacted properties by value (EUR)

Source: CBRE Research (H1 2014)

First half of 2014 registered a quite diverse range of properties transacted - from retail

(6 properties - total value EUR 56.6 mln), to industrial (1 property - total value EUR 12

mln), residential (2 properties - total value EUR 101.7 mln) and office (6 properties -

total value EUR 232.1 mln).

Investment transactions in H1 2014

Source: CBRE Research, official press releases (H1 2014)

In terms of profile of buyers - again their profile is quite diverse, ranging local

companies (generating 17% of total investment volume), to developers (like Immochan

or Globalworth) and institutional funds. While 2013 was dominated by transactions

closed by NEPI, in H1 2014 the dominance comes from Globalworth with 54% of total

investment volume.

MARKET REPORTS

36

Romania Investment Volume H1 2010 – H1 2014 (EUR mln)

Source: CBRE Research (H1 2014)

CEE Investment & Yields

In H1 2014 total commercial real-estate investment volume in CEE region, excluding

Russia, reached EUR 2.56 billion, an increase by 15% compared to volumes of last year.

Including Russia, the investment volume reached a decrease, on the back of a

substantial 60% fall in investment flows in Russia.

Poland and Czech Republic account for the majority of the investment turnover in the

region, with Poland attracting a strong interest from investors, while Czech Republic

registered an increase of 36% y-o-y. Some of the most important H1 transactions in the

region: sale of Rondo 1, office skyscraper in Warsaw, Poland , worth EUR 300 million,

Poznan City Center, a recently opened 58,000 sq m shopping center in Poznan, Poland,

or Allee shopping center in Budapest, Hungary, previously owned by ING Real Estate.

On the back of investors interest for prime office projects in Bucharest, prime yield for

this sector compressed to 8% with potential future compression in the next 6 months, if

current pending transactions are to be finalised. Other segments yields are stable, with

potential for compression for both retail and industrial segment by the end of the year.

MARKET REPORTS

37

Prime Yields CEE Region Q2 2014

Source: CBRE Research (Q2 2014)

Land Market

Comparable with commercial real-estate investment transactions, number and volume of

land transactions are on the rise. We have recorded 15 major land transactions, in all

parts of Romania for a total cumulated surface of 630,000 sq m.

We have identified three major categories of buyers of land properties: retailers (mainly

Lidl, Dedeman, Kaufland, Leroy Merlin) looking to buy properties in prime and

secondary cities, industrial occupiers interested in plots of land for the development of

factories (Dr. Oetker, Best Food, Continental) and real-estate developers securing prime

properties in major cities for future landmark developments (NEPI, Globalworth and

Kiseleff Development). Timisoara was a “hot” area for land transactions, with 47% of the

total transacted surface in H1 2014 concluded here, followed by Bucharest, Brasov and

a number of tertiary cities, interesting mostly for future industrial developments.

Pricing for land properties continues to vary depending of future use, location &

accessibility, availability in the area. Having said this, prime properties located in

Bucharest or in prime cities in Romania, suitable for retail or office development can be

transacted at prices between EUR 200 - 500 / sq m, with very special properties fetching

prices in excess of EUR 500 / sq m.

Outlook

Better than initially forecasted macroeconomic indicators provide a positive and

encouraging environment for completion of capital markets deals.

Several important investment transactions for office segment are expected to be

completed in the next 6 - 9 months, on the back of increased investors’ interest for

outstanding quality properties located in Bucharest.

Following this consistent interest from investors, prime yield compressed to 8% with

further potential for compression to 7.5% - 7.75%.

MARKET REPORTS

38

While land transactions continue to be a market dominated by distressed sales, there is

a revived interest from developers and retailers for prime properties, priced within the

market parameters. We expect the number of such transactions to grow in the next

quarters.