URealty 2015 Final Printed 23022015 (2)

32

-

Upload

saurabh-agrawal -

Category

Documents

-

view

130 -

download

0

Transcript of URealty 2015 Final Printed 23022015 (2)

PARTICULARS

From the Editor

About Unesta Homes

About the Founders

Indian Real Estate Poised for Real Growth

The Road to Real Returns

Timing is the Key to Investment

Unesta’s Past Events

Hotspots for NRI Investment

Real Estate NRI FAQs

A Complete Home Loan Guide for NRI’s

Page No.

4

6

7

8

11

15

16-17

20-24

26 -28

29-30

Issue No.03 | Released : 2015 Edition

Editor : Saurabh Agarwal, India Homes

Contributor: Joieta Dutta – India Homes | Naveen Jain – India Homes | Siddhart Goel – Cushman & Wakefield India

Designed and Published by : Unesta Homes Limited Free Publication. All the contents of URealty are only for general information and/or use. Such contents do not constitute advice and should not be relied upon in making (or refraining from making) any decision. Any specific advice or replies to queries in any part of the magazine is/are the personal opinion of such experts/consultants/persons and are not subscribed to by URealty Magazine.The information in URealty Magazine is provided on an "AS IS" basis, and all warranties, expressed or implied of any kind, regarding any matter pertaining to any information, advice or replies are disclaimed and excluded. To order reprints contact: Unesta Homes, 52 Brook Street, London W1K 5DS.

UK OfficeAddress:52 Brook Street, London, UK- W1K 5DS Webiste: www.unesta.comTel: +44 (0)207 127 8447

General Enquiries: [email protected]: [email protected]: [email protected]

www.twitter.com/unestarealty www.youtube.com/unestarealtywww.facebook.com/unestarealty

Dubai OfficeAddress:Level 17, Office 1702, The Fairmont Dubai, PO Box 119774, Dubai, UAE Tel: + 9714 311 6795

Email: [email protected]

India OfficeAddress:IndiaHomesIndia World Technologies Pvt LtdGlobal Business Park, Tower D, 9th FloorGurgaon, Haryana-122002Website: www.indiahomes.com

General Enquiries: [email protected]: [email protected]

Offices

IN THIS ISSUE

from the editor

“Buy when no one is buying & Sell when no one is selling”

– Warren Buffett[ ]

In the 3rd Edition of the URealty Magazine, we would like to revisit this mantra. A popular quote by Warren Buffett and just apt for the current market scenario for India Real Estate.

The performance of an economy has a direct effect on the real estate market, something India has experienced all too well. Last year, the economy battled against a weakened rupee, political uncertainty ahead of the general elections, and rising rates of deficit and inflation. This lead to many developers slowing down plans to build, and many investors waiting to see what the market would hold. However, the latter part of 2014 saw real estate activity pick up, and experts have projected that 2015 will be a year of prosperity and growth where real estate is concerned.

In this issue, we examine in-depth the factors that have lead to the turn around, as well as what is expected in terms of GDP and economic growth. We explore the potential of current and up-and-coming markets, consider the changes to regulations and legislation, discover the government’s plans for “smart cities”, and analyse the supply and demand for properties in three of India’s major cities. In addition to examining micro-markets, we also take a general look at what this year holds for India as a whole, a country that is now predicted to have one of that fastest growing property markets in the world. Within these pages lie facts, statistics, expert tips and buying advice, designed to help you make sense of the current state of the market. We hope you enjoy this issue, and learn from it more about the potential real estate investment opportunities that await NRIs in India.

Saurabh Agarwal Editor

DISCLAIMER : This publication is for the purposes of general information only. The views / opinions expressed in this magazine do not necessarily reflect the views of either UNESTA Homes Ltd. or IndiaHomes. The material in this magazine is not offered as advice and no liability is assumed in relation thereto. UNESTA Homes Ltd. or IndiaHomes, their respective staff and the contributors shall not be liable, for the consequences of any action taken or not taken as a result of or, for any reliance placed on, any material published in this magazine. Every investment in the property market inherently contains certain risks. Prospective investors may

therefore take appropriate financial/investment/legal advice prior to making any investments. Neither UNESTA Homes Ltd. nor IndiaHomes accept any responsibility for the content of any advertisement placed in this magazine. Readers may contact the person/entity placing the advertisement for any details thereof. While due care and diligence has been taken in the publication of this magazine, UNESTA Homes Ltd. or IndiaHomes, their respective staff and the contributors shall not be liable for any error which may have inadvertently crept in.

04 EALTYYOUR REALTY

Own Your Nest in India

EALTYYOUR REALTY

Own Your Nest in India EALTYYOUR REALTY

Own Your Nest in India

Advert

05

ABOUT UNESTA HOMESUNESTA HOMES - The Joint Venture of IndiaHomes.com and UnestaIndia has historically posed a bunch of challenges to customers looking to buy a little piece of paradise either as an investment or as a retirement home for themselves or a loved one. The challenges in Indian real estate abound, and while there is a huge opportunity for appreciation and putting together an enviable portfolio, there remain numerous challenges around transparency, the ability of Indian developers to execute huge projects within time and budget, and overall inability of NRI customers to manage their properties when they are not on site. These days buying a property in India is slowly becoming simpler than it used to be in the past. We have found that in the last few years where the IndiaHomes Property Group has been spearheading the transformation of Indian real estate, all stakeholders, including the developers, brokers, customers and most importantly the state governments have become far more appreciative of the value of real estate and have focused on allowing greater transparency, accountability and customer service to become the norm. In our partnership with Unesta, we have found a like-minded friend. The vision of providing NRIs a one-stop shop for all their property related investments in India, is a cherished goal at both IndiaHomes and Unesta; we are committed to ensuring that the Indian customer, no matter where they are in the world, gets access to the best services and the most reliable property in their journey to property ownership. The recent joint venture partnership between the

IndiaHomes Property Group and Unesta Homes will ensure that all major NRI hubs in America, London, Dubai and Singapore have adequate representation in terms of infrastructure, support and knowledge for Indians living anywhere in these markets to be able to make an informed decision. With over close to 100 million dollar investment over the last 4 years, and offices and operations in 50 cities across India, the IndiaHomes Property Group is perfectly placed to partner with Unesta and create a unique proposition for customers anywhere in the world to ensure their interests are protected. “I take this opportunity to wish the team at Unesta all the best, and also to promise customers that the IndiaHomes Property Group stands behind our partner Unesta Homes in supporting them in every possible way to ensure that they provide great value and excellent service to their customers in their exciting journey to owning Indian real estate.” Mr. Samarjit Singh, India Homes. “We couldn’t have found a better partner than India Homes. In addition to being India’s No. 1 real estate advisory company, the company also shares Unesta’s aspiration to make the experience of buying property in India hassle free for NRIs. Through this partnership we hope to offer a wide variety of choice across different cities and leverage their technology and processes needed to offer exceptional services throughout the transaction cycle of a property.”, Mr. Goyal, Unesta Homes. This marks a new beginning of India Real Estate business in the international markets.

06 EALTYYOUR REALTY

Own Your Nest in India

EALTYYOUR REALTY

Own Your Nest in India EALTYYOUR REALTY

Own Your Nest in India

about the founders

Mr. Vikram GoyalCEO, Unesta Homes Ltd.

Mr. Samarjit SinghMD & Group CEO, IndiaHomes Property GroupWith 16 years of multi-dimensional experience, Mr. Samarjit Singh is the Managing Director and Group CEO- The IndiaHomes Property Group, India’s No.1 Property Advisory Company. He is a graduate of the prestigious St. Stephens College in Delhi and post graduate of the UC Berkeley, USA. Previously, he was the Founder and Managing Director of Candid Marketing, India's number one Marketing Services Company as ranked by the Economic Times Brand Equity Agency Ranking 2010, Samar has also served on the Board of the Entrepreneurs Organisation (EO) for 7 years and served as the President of Board of EO New Delhi in 2007. In partnership with Amit Burman (Vice Chairman of the Dabur Group), he has also co-authored the book, “Winning in India”, a widely regarded compilation of the winning insights of some of the very successful business leaders of India.

Mr. Vikram Goyal is the CEO of Unesta Homes Ltd (a JV between IndiaHomes and Unesta) and has been at the top of the Indian real estate sector catering to the NRI community, for the past 10 years. As Head of Business Development, Vikram is the visionary of the company, looking ahead at trends and key investment opportunities in India. Vikram has launched a number of successful brands onto the international stage whilst operating from London, after his emigration in 2005. A dynamic and keen entrepreneur, Vikram knows what it takes to draw NRIs to invest in properties- transparency and exceptional customer service. His London-based company offered that combination when it ventured in the international market four years ago and continues to do so even today. In fact, Unesta is considered as the leading property advisory company in the UK and European markets for Indian real estate. With key investment in brand building and marketing, Unesta has become a pioneer in offering unique investment products in Indian real estate to high net-worth clients.

07

INDIAN REAL ESTATE POISED FOR REAL GROWTH 2015 is set to be a year of substantial growth for India. With a new government has come a renewed interest and confidence in the property market, as economic conditions are set to stabilize, and growth in terms of both rates of construction and prices is expected. Along with many other countries affected by the recession of 2009, India is finally starting to gain momentum and show signs of recovery. The GDP for Q1 2014/15 was reported at 5.7 per cent, up from 4.6 per cent the prior quarter. Looking ahead to the rest of the year, The World Bank predicts a GDP growth rate of 6.4 per cent overall for 2015, with economists anticipating that India’s economy could overtake that of the UK by 2020. There were already substantial strides made in 2014, with rates of Foreign Direct Investment (FDI) also on the up. The rate of FDI in India rose by 52 per cent in the first half of 2014, and private equity investments were also on the rise. With all of this anticipated growth overall come heightened expectations that the property market will follow suit. So is this in fact the case?

08 EALTYYOUR REALTY

Own Your Nest in India

EALTYYOUR REALTY

Own Your Nest in India EALTYYOUR REALTY

Own Your Nest in India

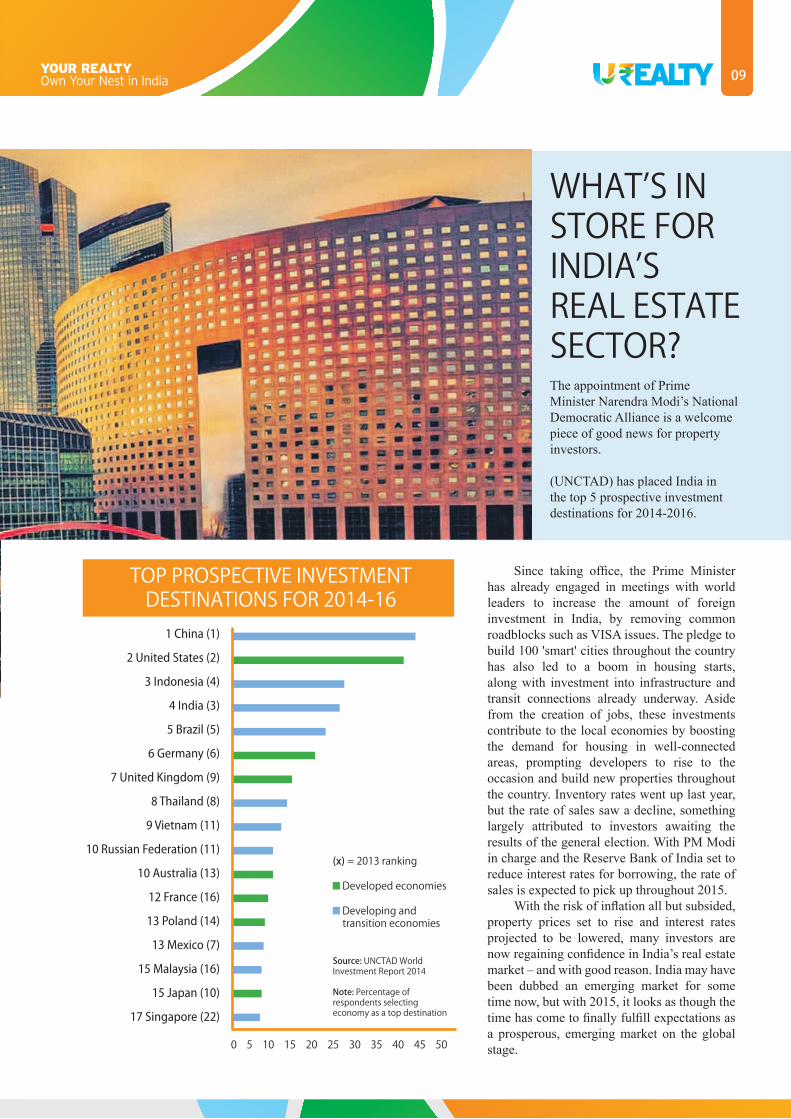

Since taking office, the Prime Minister has already engaged in meetings with world leaders to increase the amount of foreign investment in India, by removing common roadblocks such as VISA issues. The pledge to build 100 'smart' cities throughout the country has also led to a boom in housing starts, along with investment into infrastructure and transit connections already underway. Aside from the creation of jobs, these investments contribute to the local economies by boosting the demand for housing in well-connected areas, prompting developers to rise to the occasion and build new properties throughout the country. Inventory rates went up last year, but the rate of sales saw a decline, something largely attributed to investors awaiting the results of the general election. With PM Modi in charge and the Reserve Bank of India set to reduce interest rates for borrowing, the rate of sales is expected to pick up throughout 2015. With the risk of inflation all but subsided, property prices set to rise and interest rates projected to be lowered, many investors are now regaining confidence in India’s real estate market – and with good reason. India may have been dubbed an emerging market for some time now, but with 2015, it looks as though the time has come to finally fulfill expectations as a prosperous, emerging market on the global stage.

WHAT’S IN STORE FOR INDIA’S REAL ESTATE SECTOR? The appointment of Prime Minister Narendra Modi’s National Democratic Alliance is a welcome piece of good news for property investors.

(UNCTAD) has placed India in the top 5 prospective investment destinations for 2014-2016.

TOP PROSPECTIVE INVESTMENT DESTINATIONS FOR 2014-16

(x) = 2013 ranking

Developed economies

Developing and transition economies

Source: UNCTAD World Investment Report 2014

Note: Percentage of respondents selecting economy as a top destination

1 China (1)

2 United States (2)

3 Indonesia (4)

4 India (3)

5 Brazil (5)

6 Germany (6)

7 United Kingdom (9)

8 Thailand (8)

9 Vietnam (11)

10 Russian Federation (11)

10 Australia (13)

12 France (16)

13 Poland (14)

13 Mexico (7)

15 Malaysia (16)

15 Japan (10)

17 Singapore (22)

0 5 10 15 20 25 30 35 40 45 50

09

EALTYYOUR REALTY

Own Your Nest in India10

EALTYYOUR REALTY

Own Your Nest in India EALTYYOUR REALTY

Own Your Nest in India

THE ROAD TO REAL RETURNSAs a real estate investor, having a strong working knowledge of the real estate cycle will help you maximise the returns on your investment.

As it the case with most fi nancial markets, the real estate market is cyclical in nature. It follows a distinct pattern of phases, some of which make it preferable to buy, others to sell, and some in which it is best to hold on to your property. When it comes to making the most of out your investment, identifying and understanding the rudimentary principles of each stage of the property cycle is key.

WHEN IS THE RIGHT TIME TO BUY? There are generally considered to be three phases of the real estate cycle – boom, slump, and recovery. These were outlined over 80 years ago by economist and real estate expert Homer Hoyt, but they are just as applicable to modern markets today. If you are an investor looking to buy-and-hold over the long term, garnering knowledge of these three phases will help you succeed wherever you decide to buy:

11

Boom PhaseWhen a property market is experiencing a “boom”, it is undergoing a period of fast growth in terms of property prices. When market conditions are favourable (low entry price points, excellent infrastructure and local employment, low interest rates, etc.), property investors see an opportunity to “buy low and sell high”. As such, the market is often saturated and properties are snapped up quickly, which in and of itself can drive property prices upwards as the competition grows. The boom phase often tends to be the shortest of the real estate cycle, because it is the least sustainable. As more and more buyers enter the market, more developers construct new units. As the average price rises in the area, it can often mean many of these units are left vacant, resulting in an excess of supply.

Slump Phase The market “slumps” when the supply outstrips the demand. When there are more properties than there is demand, it can result in rental prices going down and vacancy rates going up, meaning income properties may no longer cash flow and actually cost an investor money. Homeowners can experience similar struggles if they overleveraged themselves during the boom phase, and have consequently been left with a property they cannot afford. Many homeowners and investors will then sell during the slump phase, often for less than they paid when they purchased during the boom. Before the market recovers, it must first stabilize. This means that prices will stay roughly in the same region, and interest rates will remain stagnant in order to correct the market economy. Once the market is stable, it can then prepare to experience an upturn.

Recovery Phase Unlike the boom phase, a time of rapid and high-paced growth, the recovery phase is a slow but positive process. During the recovery, property to both buy and rent becomes more affordable, and so vacancy rates tend to fall. As people move back into the area and stimulate the local economy, there is again more demand for accommodation in the neighborhood. This has a positive impact on property prices, which means investors are drawn to the area and the rate of sales also increases.

12 EALTYYOUR REALTY

Own Your Nest in India

EALTYYOUR REALTY

Own Your Nest in India EALTYYOUR REALTY

Own Your Nest in India

SOME THINGS TO CONSIDEREconomists generally submit that the entire real estate cycle takes around five to ten years, and so investors in the market for the long haul should be especially aware of the different phases. That is not to say that you must only buy during a recovery and sell during a boom. At any stage of the property cycle, an astute investor can potentially receive high returns on investment, and a large part of that falls to doing extensive research about the market s/he is entering.

INDIA REAL ESTATE CYCLEWhen looking at Indian markets specifically, it can be seen that this cycle is somewhat faster, as the markets have experienced volatility in recent years. There have been many contributing factors that have seen major markets such as Mumbai, NCR, Bengaluru and Chennai experience intense periods of boom and bust, such as the weakening of the rupee, uncertain buyer sentiment, inflation and political instability. The India Knight Frank Research Report 2014 revealed that 2012 was a “boom” period, but that the residential property market dissolved into a “slump” in the first half of 2014. This slump continued throughout the better part of 2014, but experts believe that is set to turn around in the upcoming year. In fact, the volume of sales in India’s six major markets is expected to soar, especially in larger, more consistent tier-1 markets.

For investors savvy enough to seek out great deals and negotiate attractive prices, bearing in mind the principles of the property cycle will ultimately help them build outstanding portfolios with property acquired in 2015.

Launches and Absorption (Top Six Cities)

222,000

200,000

180,000

160,000

140,000

120,000

100,000

Note: Source:The top six cities are Mumbai, NCR, Bengaluru, Pune, Chennai and Hyderabad | Knight Frank Research

LAUNCHES

ABSORPTION

H1

2012

H2

2012

H1

2013

H2

2013

H1

2014

H2

2014

E

Nu

mb

er o

f un

its

13

EALTYYOUR REALTY

Own Your Nest in India14

EALTYYOUR REALTY

Own Your Nest in India EALTYYOUR REALTY

Own Your Nest in India

TIMING IS THE KEY TO INVESTMENT You’ve heard it's said that “timing is everything”, and it is definitely a key component to success in the real estate market.

Making a judgment call regarding when it is the right time to enter a market is a key part of successful property investment, and so it shouldn’t be left up to guesswork. There are a number of factors to take into consideration, and both reports on a market’s past performance along with economic forecasts for the future can help make sense of these factors. 2014 saw many investors hedging their bets on the future of India’s real estate market, but the formation of a new government saw many deciding that it was in fact the right time to snap up a property. Market analysts were in agreement; the FTSE 100 index listed India as the best place to invest in 2014. Looking ahead to this year, it can be seen that 2015 is set to offer even more investors as the tide begins to turn for India’s economic climate.

15

16

A property exhibition in Wembley, London – India U-Realty Show – will showcase properties from India to prospective NRI buyers in London. The show comes at a time when many in the NRI community look to invest in properties in Indian cities, as the UK property market looks gloomy.

As many as 20 well-known Indian property developers including Godrej Properties, Rustomjee, Omkar Group, Total Environment, G Corp, Adani, Wadhwa, Ansal API, ABIL and Jaypee Greens will showcase their residential, commercial and retail real estate portfolios to prospective London Indians at the two-day property show on October 6 and 7, 2012 in Wembley.

India’s top Developers participated at the Show

The NRI visitors at the URealty India Property Show

Special Investment Seminars held at the Show

URealty Magazine 2012 Edition being launched at the event Sewa Day 2012 celebrated at URealty Property Show

Wembley, London, October 2012

EALTYYOUR REALTY

Own Your Nest in India

EALTYYOUR REALTY

Own Your Nest in India EALTYYOUR REALTY

Own Your Nest in India17

India Real Estate 2013 – Risk, Returns & Reforms.Unesta brought together a global panel of prominent business leaders at a packed event, which educated potential investors and the general public on real estate investment opportunities in India. The URealty Leadership Programme focusing on Indian Real Estate 2013 – Risk, Return & Reforms took place at The MayFair Hotel, London, on February 7th, 2013 and included over a hundred potential investors discussing the challenges and opportunities that Indian real estate presents.

International property consultants Cushman & Wakefield, leading banking provider State Bank of India, global accountancy firm KPMG and prominent developers Experion from Delhi NCR and G-Corp Estates from Bangalore joined with Unesta to provide a platform for NRIs (Non-resident Indians) and PIOs (Persons of Indian origin) to share their thoughts on investing in Indian real estate.With dignitaries including Lord Dholakia, Deputy Leader of the Liberal Democrats in the House of Lords and Dr. Mohan Kaul, Co-Chair Commonwealth Business Council, the URealty Leadership Programme brought together eminent Speakers from Banking, Legal and Taxation industry including Mr. MrutyunjayMahapatra, Regional Head of the State Bank of India in the UK and Mr. Vijay Goel, Partner, Singhania& Co. LLP.

LEADERSHIP PROGRAMME 2013

The panel of leading Property Developers, Bankers and experts in Legal and Taxation from India and the UK at the URealty Leadership Programme

Guests at the reception of the URealty Leadership Programme at The Mayfair Hotel Guests at the seminar at Mayfair Hotel

UNESTA’S PAST EVENTS

WHY 2015 IS THE RIGHT TIME TO INVEST IN INDIA After experiencing a turbulent two years, the residential real estate market is finally set to turn around, according to experts. Executive Chairman of Cushman and Wakefield Carlo Barel di Sant’Albano recently named India as a top market in which investors can expect to see growth with a long-term investment over 5-20 years. There are four primary reasons why analysts are projecting such rapid growth – urbanisation, the growth of India’s middle class, the country’s young demographic, and a rise in demand for property. Urbanisation has already contributed to strong growth in India’s eight major markets, and it is expected to do so further as more people move to the cities. A study as per United Nations estimates that by 2050, 843 million people will be living in cities, a growth rate of 42 per cent over the next forty years. Currently, 590 million people live in cities, a figure almost double that of the US general population! India’s rising middle class is also gaining more purchasing power; with the new government in place, interest rates are expected to be lowered this year, making borrowing a more affordable and attractive option. Along with better access to credit, the middle class is also experiencing an increase in annual income, and a high savings-to-spending ratio. It is estimated that by 2050, 91 million households will be deemed middle class, meaning there will be substantial pressure applied on developers and investors to have properties available near to economic hubs and areas of employment. The young make-up of India’s demographic is also good news for investors. By 2020 it is predicted that the average age in India will be 29, meaning Generation Y will be firmly in

control. This is a generation known for being aspirational and consumer-driven, meaning they are more likely to spend more on rent to live in desirable areas/neighborhoods near work, and to want to purchase homes for themselves in the future. Perhaps one of the key reasons that now is the time to buy in India is the rise in demand. Young people and families moving for work need accommodation, international travellers require short-term lets for business travel, and investors are returning to the market looking to bulk up their portfolios. According to figures from Cushman & Wakefield, an estimated 18 per cent of the demand in India will be concentrated across the top eight major markets, and projections also outlined that there will be a demand for roughly 13 million units in urban areas by 2018.

TIMING IS THE KEY TO INVESTMENT

IN SUMMARY: As the middle class grows and NRI investors reconsider India, now is the time to buy to experience the highest price growth.

According to all major economic forecasts, India’s GDP is set to rise in the coming years, with immediate growth expected in 2015. For buyers looking to enter the market at a time of economic stability, and to hold onto investments over the long term to experience maximum price appreciation, rental yields and demand, there’s simply no time like the present to invest in India.

18 EALTYYOUR REALTY

Own Your Nest in India

EALTYYOUR REALTY

Own Your Nest in India EALTYYOUR REALTY

Own Your Nest in India19

EALTYYOUR REALTY

Own Your Nest in India

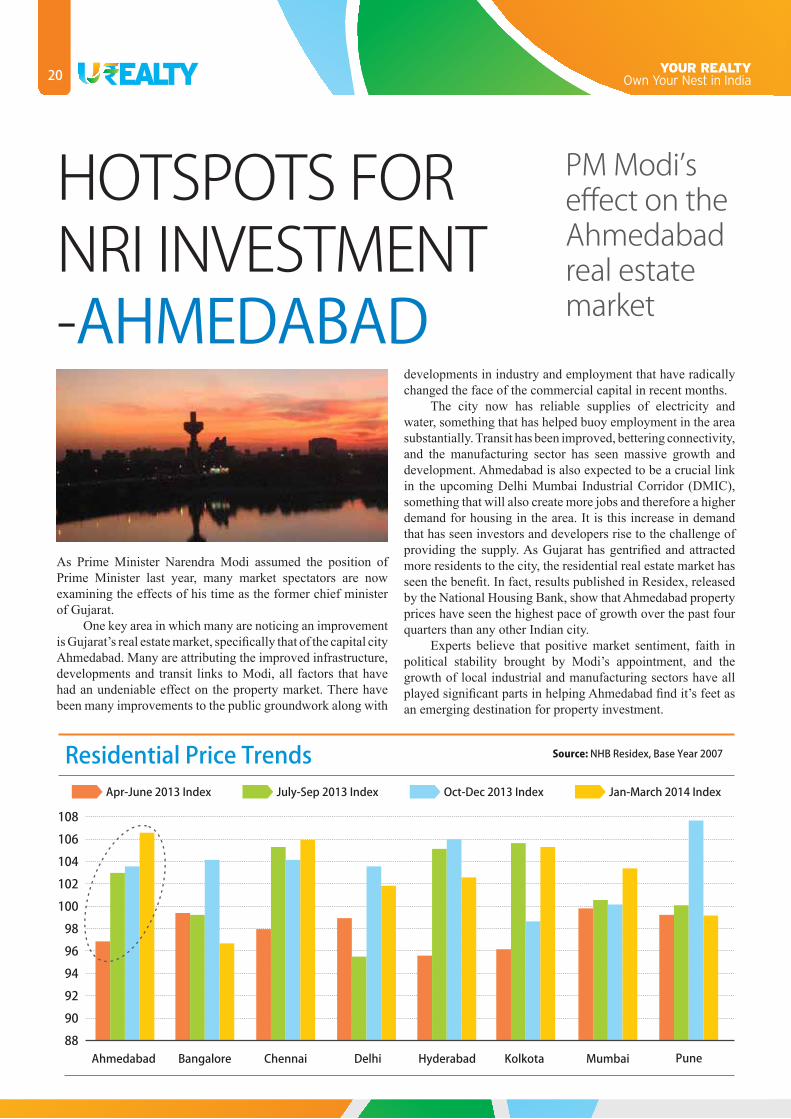

As Prime Minister Narendra Modi assumed the position of Prime Minister last year, many market spectators are now examining the effects of his time as the former chief minister of Gujarat. One key area in which many are noticing an improvement is Gujarat’s real estate market, specifically that of the capital city Ahmedabad. Many are attributing the improved infrastructure, developments and transit links to Modi, all factors that have had an undeniable effect on the property market. There have been many improvements to the public groundwork along with

developments in industry and employment that have radically changed the face of the commercial capital in recent months. The city now has reliable supplies of electricity and water, something that has helped buoy employment in the area substantially. Transit has been improved, bettering connectivity, and the manufacturing sector has seen massive growth and development. Ahmedabad is also expected to be a crucial link in the upcoming Delhi Mumbai Industrial Corridor (DMIC), something that will also create more jobs and therefore a higher demand for housing in the area. It is this increase in demand that has seen investors and developers rise to the challenge of providing the supply. As Gujarat has gentrified and attracted more residents to the city, the residential real estate market has seen the benefit. In fact, results published in Residex, released by the National Housing Bank, show that Ahmedabad property prices have seen the highest pace of growth over the past four quarters than any other Indian city. Experts believe that positive market sentiment, faith in political stability brought by Modi’s appointment, and the growth of local industrial and manufacturing sectors have all played significant parts in helping Ahmedabad find it’s feet as an emerging destination for property investment.

HOTSPOTS FOR NRI INVESTMENT -AHMEDABAD

PM Modi’s effect on the Ahmedabad real estate market

20

EALTYYOUR REALTY

Own Your Nest in India EALTYYOUR REALTY

Own Your Nest in India21

Call 020 7127 0617 or visit www.unesta.com

Thane has in recent years been rejuvenated from industrial town to a cosmopolitan city, largely thanks to the growth of the IT sector in the area. The sustained injection of funds from Thane Municipal Council has improved transit and infrastructure substantially over the past twenty years, bettering connectivity and trade with nearby Mumbai. The growth of the IT/ITeS sectors called for new commercial buildings to be developed, and as more people began to utilise the new transit links to travel into Thane for work, the demand grew for housing in the area. Developers such as Rustomjee, DLF and Hiranandani Developers among others have since focused on building high-rise residential units and townships throughout Thane to house the ever-growing local workforce. The area of Ghodbunder Road especially has seen a great deal of development and growth, owing to its excellent connection to Mumbai’s Eastern Express Highway (EEH) and Western Express Highway (WEH). In addition to better transportation, Thane is now also home to educational institutions, retail outlets, leisure facilities, entertainment venues, hospitals and schools. This bustling city is expected to provide a high return on investment for buyers looking to purchase a property in the area, with Jones Lang LaSalle India predicting that capital values and rental rates will rise by nearly 50 per cent by 2020. This strong performance in the residential real estate sector is set to endure as more improvements to infrastructure and commercial buildings/facilities take place.

IT @ HEART OF THANE’S RECENT RE-BIRTHWhen looking at cities in India that have undergone a substantial transformation in recent years, perhaps nothing stands out quite like Thane.

Situated to the north-east of Mumbai, Thane was the host to India’s first ever train connectivity route. Thane has undergone a makeover from being an industrial town with affordable residential housing to a now-favoured IT and relatively upmarket residential destination. Various infrastructural initiatives by the government executed under the aegis of the nodal development authority, Thane Municipal Corporation (TMC), have greatly enhanced the connectivity of Thane to the prime business hubs of Mumbai and Navi Mumbai.

MUMBAI

THANE

22 EALTYYOUR REALTY

Own Your Nest in India

EALTYYOUR REALTY

Own Your Nest in India EALTYYOUR REALTY

Own Your Nest in India23

The two main clusters in New Gurgaon along the upcoming Dwarka-Gurgaon Expressway are Sectors 102 to 113 and Sectors 76 to 95. New Gurgoan is well connected with three highways, NH8, Kundli–Manesar–Palwal Expressway and Dwarka-Gurgaon Expressway, Railway Station and the Airport. This so-called micro-market is receiving a great deal of interest from prospective buyers, and is one area that experts have noted is poised for substantial price growth and property development, along with the Dwarka Expressway Corridor. The building of over 44,000 residential units has got underway, and those that have been completed and have made it onto the market have already experienced substantial positive price growth. According to figures released by research firm PropEquity, prices of residential apartments have grown from Rs 1,825/sq ft to roughly Rs 4,983/sq ft in the past five years, rising a staggering 173 per cent. Units that are still under construction are expected to be ready for residents within the next three years. So just what is driving New Gurgaon? Aside from excellent connectivity through roads and transit, further expansion of infrastructure, economic hot spots, employment opportunities, along with an increase in the construction of commercial office space is propping up the demand for both short-term and long-term accommodation in the area. As New Gurgaon becomes a key destination for business travellers, short-term lets are increasing in demand too, something reflected in the development of hotels in the area. That New Gurgaon is not restricted in terms of borders or the physical capacity for growth is also proving beneficial, as developers can build high-rise projects along with houses and plenty of commercial buildings to cater to the anticipated influx of residents. With a mix of both affordable and premium listings available in the area, the New Gurgaon corridor has something for any investor looking to buy here, irrespective of price point. And with sizable growth and development in the area already underway, these residential units are expected to provide a high ROI to investors that are ready to buy.

NEW GURGAON – THE RISING STAR OF DELHI NCR

Situated beyond the second toll plaza of the NH-8, the area now known as “New Gurgaon” is proving popular with end-users and property investors alike.

24 EALTYYOUR REALTY

Own Your Nest in India

EALTYYOUR REALTY

Own Your Nest in India EALTYYOUR REALTY

Own Your Nest in India25

Call 020 7127 0617 or visit www.unesta.com

Q1. Why invest in property in India?

Ans: To tap the potential of the Indian real estate market and expedite the sector with a double digit growth rate, the developers have shifted their focus to offer timely possession of projects and adapt to the new FDI rules.The economic contribution of the real estate sector is most likely to increase significantly during the period, from 6.3% in 2013 to almost 13% in 2025. This spiral growth is attributed to the intensive demand for first-rated projects that can be delivered on time.During H1 2014, prices in Bengaluru have appreciated at the fastest pace of 11%, compared to H1 2013. Mumbai, currently suffering a downfall of 49% is expected to recover the sales volume by the end of FY 2014. As real estate demand in India improves, capital values in other major cities are also likely to increase, albeit marginally. Purchasing a property in India, thus, stands as a top priority for a non-resident Indian (NRI). The purchase transaction is governed by the Reserve Bank of India (RBI) and the rules and regulations that fall under the purview of the Foreign Exchange Management Act (FEMA).

Q2. Can an NRI/PIO acquire agricultural land/plantation property/farm house in India?

Ans: Potentially; doing so requires specific approval of Reserve Bank of India, and the proposals are considered in consultation with the Government of India.

Q3. What is the Tax treatment for income generated from property selling or renting for NRI/ PIO/OCI?

Ans: The mere acquisition of property does not attract income tax. However, any income accruing from the ownership of it, in the form of rent (if it is let out)/annual value of the house (it is not let out and it is not the only residential property owned by that person in India) and/or capital gains (short term or long term) arising on the sale of this house or part thereof is taxable in the hands of the owner.

Q4. Does Capital Gains Tax (CGT) apply for NRI/PIO/OCI?

Ans: Yes. Long-term and short-term capital gains are taxable in the hands of non-residents.

Q5. Do NRI/PIO have to file returns in India for their property rental income and Capital Gains Tax?

Ans: The Government of India has granted general permission for NRI/PIO/OCI to buy property in India and they do not have to pay any taxes even while acquiring property in India. However, taxes have to be paid if they are selling this property. Rental income earned is taxable in India and they will have to obtain a PAN and file return of income if they have rented this property. On sale of the property, the profit on sale shall be subject to 9 capital gains. If they have held the Property for less than or equal to 3 years after taking actual possession, then the gains would be short term capital gains, which are to be included in their total income as tax as per the normal slab rates shall be payable and if the property has been held for more then 3 years then the resultant gain would be long term capital gains subject to 20% tax plus applicable cess.Rate of tax deduction at source (TDS): Long term: 20.6% Short term: 30.9%

Q6. Is there a way for exempting the tax upon income generated by the property located in India? How does the Double Taxation Avoidance Agreement work in the context of tax on income and Capital Gains tax paid in India by NRI?

Ans: Exemption available (only for long term capital gains).The long term capital gains arising on sale of a residential house can be invested in buying/constructing another residential house, within the prescribed time. The exemption is restricted to the amount of capital gains or the amount invested in new residential house, whichever is lower.

Real Estate NRI FAQs

26 EALTYYOUR REALTY

Own Your Nest in India

EALTYYOUR REALTY

Own Your Nest in India EALTYYOUR REALTY

Own Your Nest in India

If the amount of capital gains is invested in bonds of National Highways Authority of India (NHAI) or Rural Electrification Corporation, then the entire capital gain is exempted, else only the proportionate gain is exempted. As per the financial budget 2007-08, a cap of Rs. 50 Lakhs has been imposed on investment that can be made in capital tax saving bonds.India has DTAA’s with several countries which give a favorable tax treatment in respect of certain heads of income. However, in case of sale of immovable property, the DTAA with most countries provide that the capital gains will be taxed in the country where the immovable property is situated. Hence, the non-resident will be subject to tax in India on the capital gains which arise on the sale of immovable property in India. Letting of immovable property in India would be taxed under most tax treaties in view of the fact that the property is situated in India.

Q7. How does Double Taxation Avoidance Agreement work in the context of CGT paid in India for the foreign tax treatment?

Ans: In case the non-resident pays any tax on capital gains arising in India, he would normally be able to obtain a tax credit in respect of the taxes paid in India in the home country, because the income in India would also be included in the country of tax residence. The amount of the tax credit as also the basis of computing the tax credit that can be claimed are specified in the respective country’s DTAA and is also dependent on the laws of the home country where the tax payer is a tax resident.

Q8. What’s the best way to file tax returns?

Ans: Traditionally, you could file your return either by giving a power of attorney to someone in India, or by sending your form and documents to a tax expert in India who would then file returns on your behalf. However nowadays, the easiest option for NRIs to file their Indian tax returns is by using the online platform. There are several options to file online.

Q9. What are the rules governing the repatriation of the proceeds of sale of immovable properties by NRI/PIO as prescribed by the Reserve Bank of India?

Ans: (a) If the property was acquired out of foreign exchange sources, i.e. remitted through normal banking channels/ by debit to NRE/FCNR (b) account, the amount to be repatriated should not exceed the amount paid for the property: (i) In foreign exchange received through normal banking channel or (ii) By debit to NRE account (foreign currency equivalent, as on the date of payment) or debit to FCNR (B) account.

Repatriation of sale proceeds of residential property purchased by NRI’s/PIO’s out of foreign exchange is restricted to not more than two such properties. Capital gains, if any, may be credited to the NRO account from where the NRI’s/PIO’s may

repatriate an account up to USD one million, per financial year, as discussed below. If the property was acquired out of Rupee sources, NRI/PIO may remit an amount up to USD one million, per financial year, out of the balances held in the NRO account (inclusive of sale proceeds of assets acquired by way of inheritance or settlement), for all the bonafide purposes to the satisfaction of the Authorized Dealer bank and subject to tax compliance. The NRI/PIO may use this facility to remit capital gains, where the acquisition of the subject property was made by funds sourced by remittance through normal banking channels/by debit to NRE/FCNR(B) account.

Q10. Is the rental income from property repatriable and what are the RBI rules?

Ans: The rental income, being a current account transaction, is repatriable, subject to the appropriate deduction of tax and the certification thereof by a Chartered Accountant in practice. Repatriation of sale proceeds is subject to certain conditions. The amount of repatriation cannot exceed the amount paid for acquisition of the immovable property in foreign exchange.

Q11. Are NRI/PIO/OCI eligible for Housing loans to buy property from any Indian Bank?

Ans: An authorised dealer or a housing finance institution in India approved by the National Housing Bank may provide housing loan to a non-resident Indian or a person of Indian origin residing outside India. A maximum of 80% amount is financed by the financial institution. The rest has to be given by the NRI.

For acquiring a residential property in India, the buyer is subject to the following conditions, namely: (a) The quantum of loans, margin money and the period of repayment shall be at par with those applicable to housing finance provided to a person residing in India. (b) The loan amount shall not be credited to Non- resident External (NRE)/Foreign Currency Non-resident (FCNR)/Non-resident non-repatriable (NRNR) account of the borrower. (c) The loan shall be fully secured by an equitable mortgage by deposit of title deal for the property proposed to be acquired, and if necessary, also be lien on the borrower’s other assets in India. (d) The instalment of loan, interest and other charges, if any, shall be paid by the borrower by remittances from outside India through normal banking channels or out of funds in his Non-resident External (NRE)/Foreign Currency Non-resident (FCNR)/Non-resident Non- repatriable (NRNR)/Non-resident Ordinary (NRO)/non- resident Special Rupee (NRSR) account in India, or out of rental income derived from renting out the property acquired by utilization of the loan or by any relative of the borrower in India by crediting the borrower’s loan account through the bank account of such relative (The word ‘relative’ means ‘relative’ as

27

defined in section 6 of the Companies Act, 1956.) (e) The rate of interest on the loan shall conform to the directives issued by the Reserve Bank of India or, as the case may be, the National Housing Bank.

Q12. What documents are required to buy a property in India?

Ans: The following documents are required for buying a property in India: a) Pan card (Permanent account number) b) OCI/PIO card (In case of OCI/PIO) c) Passport (In case of NRI) d) Passport size photographs e) Address proof

Q13. What documents are required for a home loan?

Ans: For salaried individuals, the following documents are required: a) Copy of employment contract b) Latest Salary slip c) Latest work permit d) Bank statement for 4 months or NRE/NRO a/c 6 months statement e) Passport/visa copy f) Utility bill for address proof g) PIO/OCI card h) Power of Attorney (if applicable, in respective bank’s format) i) Customer credit check report j) Property agreement duly registered or other related docs k) Income Tax returns last 2 years

For self-employed, the following documents are required. a) Balance sheets and P&L a/c of the company for last 3 years b) Bank a/c statements for the last 6 months for company and individual, both c) Income tax returns (3 years) d) Passport/visa copy e) Utility bill for address proof f) PIO/OCI card g) Power of Attorney (if applicable, in respective bank’s format) h) Credit check report i) Property agreement or other related docs

Q14. Are there any restrictions upon the number of properties bought by NRI/PIO/OCI?

Ans: There are no restrictions on the number of properties that can be bought.

Q15. Is there any specific way of payment for buying/acquisition of immovable property by NRI/PIO ?

Ans: There are multiple ways as mentioned below: • Funds received in India through normal banking channels by way of inward remittance from any place outside India • Funds held in any non-resident account maintained in accordance with the provisions of the Act and the regulations made by the Reserve Bank • No payment of the purchase price for acquisition of immovable property shall be made either by traveler’s cheque or by foreign currency notes or by other mode other than those specifically permitted as above

Q16. What are the key points to be considered at the time of purchase?

Ans: Investment in real estate is a simple but long-term move so, one should be cautious enough at the time of purchase to secure the deal.

Few points of consideration are mentioned below: • Property Title: The title of property should be clear from the issues and the seller should have the required right to sell it, especially if it is inherited or any joint property • NDC: Always check that there will be no outstanding electricity/water bills or any other authority dues pending with the property. Take a no dues certificate from the seller at the time of purchase • Bank release letter: It is advisable to take the bank release letter from the concerned bank, if the property had been mortgaged as security in any type of loan • Permits: The property for sale should have all approvals and permits from the civic authorities in terms of construction

Q17. What are the key points that ensure a safe deal to buy a property in India?

Ans: Below are the key safety measures to be considered while buying a property: • Whenever you plan to invest in real estate, you should go through the proper channels, either through a Reliable Broking Firm, friend or relative to ensure the authenticity of the property • You can also approach through property expos and seminars to choose a right property and select reputed developer • It will be wise to get the title papers of the property verified by a lawyer before going ahead • If and when you want to purchase /dispose the property, you can give Power of Attorney to a reliable person who is resident in India & who may be able to act on your behalf to complete formalities such as registration, possession, execution of the agreement of sale,etc.

28 EALTYYOUR REALTY

Own Your Nest in India

EALTYYOUR REALTY

Own Your Nest in India EALTYYOUR REALTY

Own Your Nest in India

A COMPLETE HOME LOAN GUIDE FOR NRI’SBuying a home for an NRI has always been a big challenge, especially identifying the right property sitting thousands of miles away. In addition to that, the availability of the right information has almost been impossible, unless s/he is visiting India and has enough time to investigate, identify and shortlist a property during the short stay. Traditionally, NRIs have relied mostly on friends, family and relatives get information in identifying the right property. But with time, property advising has evolved beyond brokers, and numerous online companies with huge investments have started realizing the potential of the NRI market. They have developed processes to guide the prospective buyers from scratch by asking relevant questions, like the purpose of buying a property, budget, and how they plan to finance it. Financing a property purchase through loans has its own challenges and involves lots of paperwork, which delays the whole process.

NRIs can obtain loans by mortgaging an existing residential property; however, there are certain conditions that NRIs need to fulfill in order to avail the home loans.

Age – The minimum age for a loan applicant is 18-21 years age. The maximum age limit is 60 years or retirement age (whichever is earlier) at the time of loan maturity.

Qualification – The minimum qualification of the loan seeker has to be that of a graduate.

Income – The loan applicant has to have a minimum monthly income of $2,000 (This criterion may differ across HFCs). Moreover, the eligibility is also determined by the stability and continuity of your business or employment.

Payment options – There are the Equated Monthly Installments which the NRI needs to route through cheques or his/her NRE/NRO account. Making payments from another source such as a savings account in India is not allowed.

Number of dependents - Another aspect of NRI Home Loans is that the eligibility of the applicant is also determined by the number of dependents, assets and liabilities.

General guidelines for availing Home Loan

Based on the repayment capacity and the cost of the property, an NRI applicant is eligible to receive a home loan that ranges

from a minimum of Rs 3-5 lakhs to a maximum of Rs 1 crore, this again is subject to variables depending on the priorities of the home loan. A loan applicant can be eligible for a maximum of 85% of the cost of the property or the cost of construction as applicable and 75% of the cost of land in case of purchase of land, based on the repayment capacity of the borrower. Besides, the Home Loan Tenure for NRIs is different from Resident Indians. An NRI can also enhance his or her loan eligibility by applying for home loans with a co-applicant who has a separate source of income. Also, the rate of interest for home loans to NRIs is higher than those offered to Resident Indians. There is a difference which varies from 0.25%-0.50%. Some HFCs also have an internal 'negative criterion' for NRI home loans. As such, the NRIs who hails from locations that are marked as being 'negative' in the books of HFCs may find it difficult to procure a home loan. The cost of a dwelling unit which is own contribution financed less the loan amount, can be met from direct remittances from abroad through normal banking channels, the Non-Resident (External) [NR(E)] Account and /or Non-Resident (Ordinary) [NR (O)] account in India. However, repayment of the loan, comprising of the principal and interest, including all the charges are to be remitted to the HFC from abroad through normal banking channels, the Non-Resident (External) [NR(E)] Account and /or Non-Resident (Ordinary) [NR (O)] account in India. The repayment option for NRIs as they can pay through the funds held in any non-resident account maintained in accordance with the provisions of the Foreign Exchange Management Act, 1999, and the regulations made by the RBI from time to time. As most of the home loan provider companies consider the economic stability of the applicant, home loans for NRIs are quite feasible, because they are well in economic resource.

Documentation required for Home Loans • Passport and Visa. • Bank Statements for the last six months. • The labor card/identity card (translated in English and countersigned by the consulate) if the person is employed in the Middle East Salary certificate (in English) specifying name, date of joining, designation and salary details. • Valid work permit. • A copy of the appointment letter and contract from the company employing the applicant.

29

• Another document of vital importance that is required while processing an NRI home loan is the power of attorney (POA). The POA is important because, since the borrower is not based in India; the HFC would need a 'representative' 'in lieu of' the NRI to deal with and if needed. Although not obligatory, the POA is usually drawn on the NRI’s parents/wife/ children. An important point to be noted here is that the documentation is different for Salaried NRI Applicants and Self-Employed NRI applicants.

Salaried NRI applicants need to provide • Overseas bank account for the last three months showing salary credits. • Copy of valid visa/ work permit/ equivalent document supporting the NRI status of the proposed account holder. • Copy of valid passport showing Visa stamps. • Latest contract copes evidence salary/ salary certificate/ wage slips.

Self-employed NRI applicants need to provide • Six months overseas bank account statement and NRE/ NRO account. • Brief profile of the applicant and business/ trade license or equivalent document. • Passport copy with valid visa stamp. • Computation of income, P&L account and B/ Sheet for the last three years certified by the CA/ CPA or any equivalent authority, as the case may be (or equivalent company accounts).

Property Documents that need to be arranged • Original title deeds tracing the title of the property for a minimum period of the last 13 years. • Encumbrance Certificate for the last 13 years. • Agreement of sale /construction, if any. • Receipts for payments made for the purchase of the dwelling unit. • Approved plan / license. • ULC clearance /conversion order etc. • Receipts for having invested the margin money through normal banking channels from the Non-Resident (External) account in India and / or the Non-Resident (Ordinary) account in India. • Latest tax paid receipt. • Allotment letter from the co-operative society /

association of apartment owners. • Agreement for sale / sale deed /detailed cost estimate from Architect / Engineer for property to be purchased / constructed /extended / improved. • Copy of approved drawings of proposed construction/purchase/extension.

However, if the PIO card is not available, photocopies of the documents below will work, • The current passport, with birthplace as 'INDIA' • The Indian passport, if held by the individual earlier. • Parents/grandparents Indian passport/birth certificate/marriage certificate substantiating the individuals claim as a person of Indian origin.

Lastly, one basic query that every NRI has in mind is that whether NRI/PIO avail of loan from an authorized dealer for acquiring a flat / house in India for his or her own residential use against the security of funds held in an NRE Fixed Deposit account/ FCNR (B) account. So, the answer for the query is yes. Such loans are subject to the terms and conditions as laid down in Schedules 1 and 2 to Notification No. FEMA 5/2000-RB dated May 3, 2000 as amended from time to time. However, banks cannot grant fresh loans or renew existing loans in excess of Rupees 20 lakh against NRE and FCNR (B) deposits either to the depositors or to third parties [cf. A.P. (DIR Series) Circular No. 29 dated January 31, 2007].

Such loans can be re-paid (a) by way of inward remittance through normal banking channel or (b) by debit to his NRE / FCNR (B) / NRO account or (c) out of rental income from such property. (d) By the borrower's close relatives, as defined in section 6 of the Companies Act, 1956, through their account in India by crediting the borrower's loan account.

If anyone says the process is easy, it’s not. But, with the right advice, the whole process can be made a lot less cumbersome and if the above points are kept in mind, one will be able to ask the right questions while moving through the whole process. This is where companies like IndiaHomes are taking a lead and going beyond just selling, they are helping & guiding the customer through the whole process.

ABOUT THE AUTHORNaveen Kumar Jain, VP & Head of Business Operations & Customer Services, Indiahomes.comNaveen is an MBA & LLB with 16 years of experience in operations and customer services. At IndiaHomes.com, he is responsible to ensure that all processes, policies and practices followed by the organisation are customer centric and should result in an optimal solution for the end user. Naveen has held senior leadership roles in ING Vysya Bank, HDFC Bank & Stock Holding Corporation of India. Being a certified six sigma black belt & ISO 9001: 2008 lead auditor, the implementation of quality management systems and standards for operational excellence have been Naveen’s key strengths and areas of focus.

30