Update on Corporate Class (mutual fund corporation) · PDF fileUpdate on Corporate Class...

35

Update on Corporate Class (mutual fund corporation) Ron Bowes, VP, Sales & Marketing Wilmot George, VP, Tax, Retirement and Estate Planning

Transcript of Update on Corporate Class (mutual fund corporation) · PDF fileUpdate on Corporate Class...

Update on Corporate Class (mutual fund corporation)

Ron Bowes, VP, Sales & Marketing

Wilmot George, VP, Tax, Retirement and Estate Planning

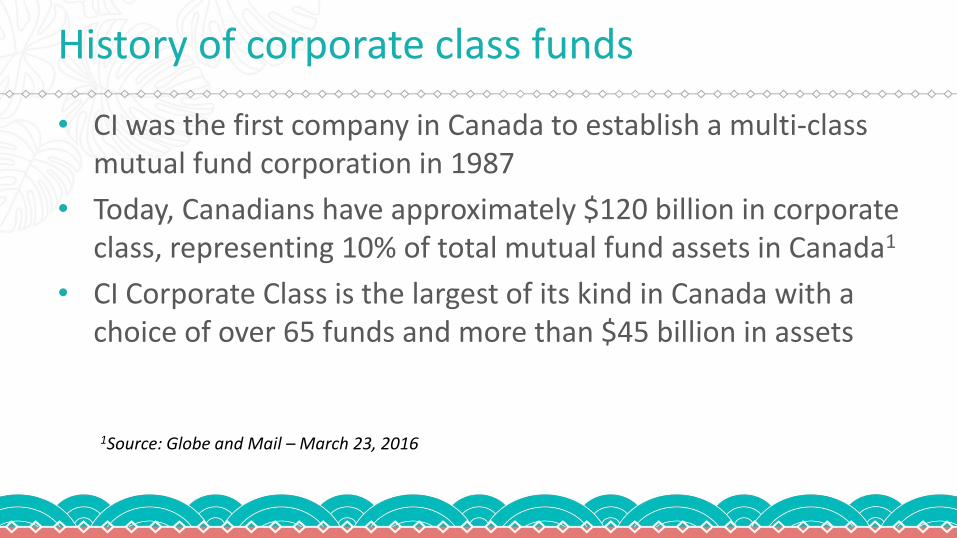

History of corporate class funds

• CI was the first company in Canada to establish a multi-class mutual fund corporation in 1987

• Today, Canadians have approximately $120 billion in corporate class, representing 10% of total mutual fund assets in Canada1

• CI Corporate Class is the largest of its kind in Canada with a choice of over 65 funds and more than $45 billion in assets

1Source: Globe and Mail – March 23, 2016

Summary of key benefits (pre-2016 federal budget)

• Historically, corporate class funds have been attractive to taxable investors because of the ability to: – Switch between fund classes without triggering capital gains tax

– Minimize distributions due to the sharing of expenses across corporate class funds

– When required, receive tax-efficient income in the form of Canadian eligible dividends, capital gains dividends or tax-free return of capital

2016 federal budget

Source – Department of Finance (Canada)

Note: As per proposed legislation released on July 29, 2016, the effective date will be January 1, 2017

Initial reaction…

Source: Investment Executive – March 22/16

Source: Globe and Mail – March 23/16

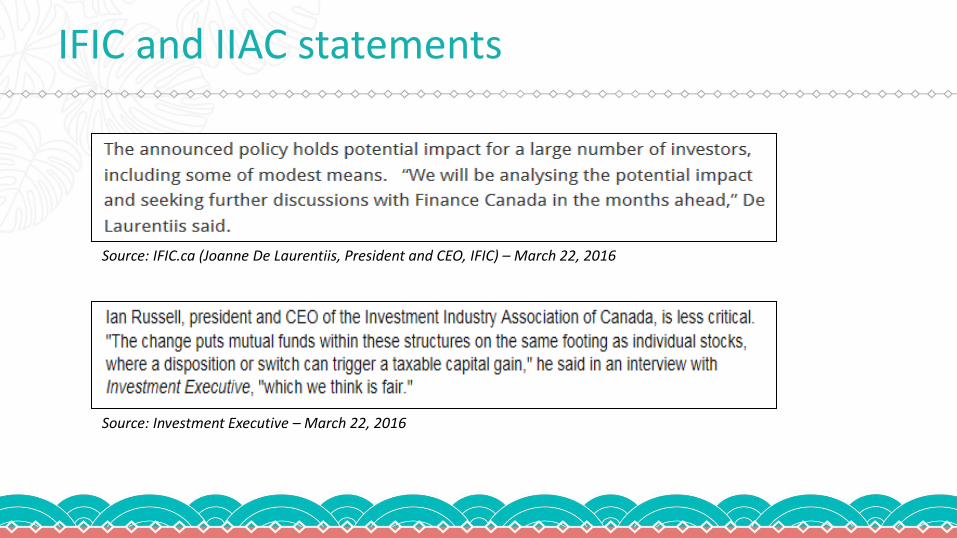

IFIC and IIAC statements

Source: IFIC.ca (Joanne De Laurentiis, President and CEO, IFIC) – March 22, 2016

Source: Investment Executive – March 22, 2016

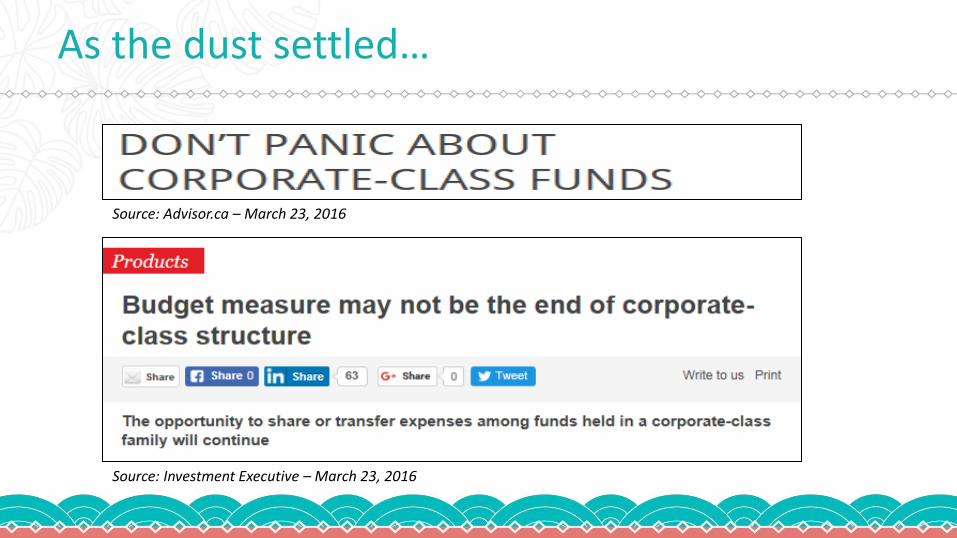

As the dust settled…

Source: Advisor.ca – March 23, 2016

Source: Investment Executive – March 23, 2016

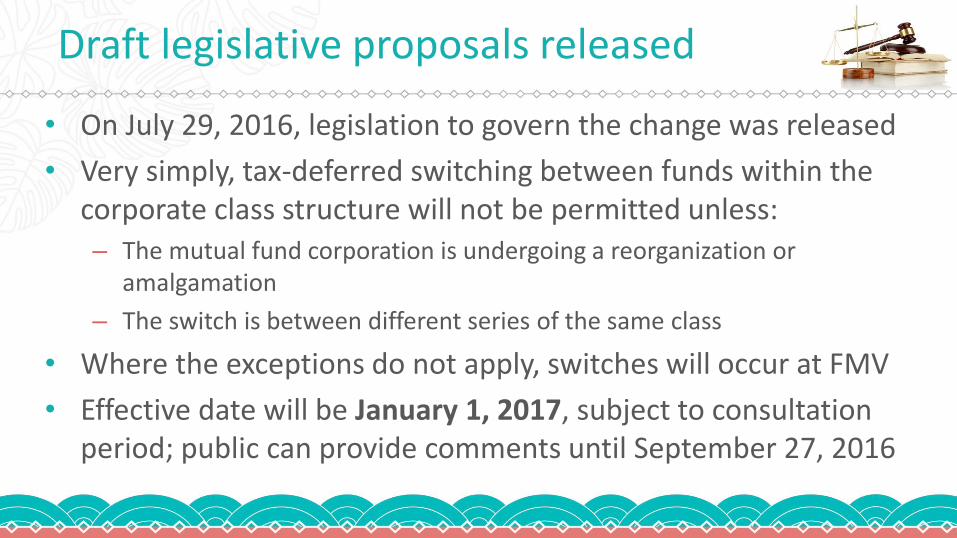

Draft legislative proposals released

• On July 29, 2016, legislation to govern the change was released

• Very simply, tax-deferred switching between funds within the corporate class structure will not be permitted unless: – The mutual fund corporation is undergoing a reorganization or

amalgamation

– The switch is between different series of the same class

• Where the exceptions do not apply, switches will occur at FMV

• Effective date will be January 1, 2017, subject to consultation period; public can provide comments until September 27, 2016

Will corporate class funds still have value?

• Yes, for the following reasons: – Low dividend payout policy

– Tax-efficient Canadian dividends and capital gains dividends (when paid)

– Availability of T-Class shares

• For switches, the change simply balances the playing field; it does not place corporate class funds in a lesser position relative to peers

What the change means to CI Corporate Class Ltd.

• We are reviewing the legislation and monitoring developments to determine impact on CI’s corporate class structure

• Here is what we expect: – Tax deferred switching between fund classes will cease on Jan. 1, 2017

– Little to no impact to when/how distributions are paid

– Impact to asset allocation programs will depend on the program

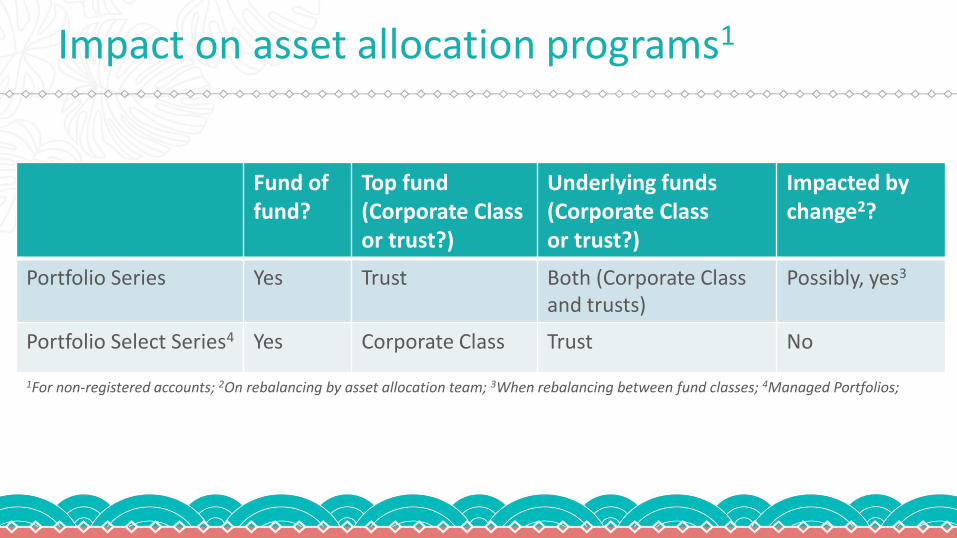

Impact on asset allocation programs1

Fund of fund?

Top fund (Corporate Class or trust?)

Underlying funds (Corporate Class or trust?)

Impacted by change2?

Portfolio Series Yes Trust Both (Corporate Class and trusts)

Possibly, yes3

Portfolio Select Series4 Yes Corporate Class Trust No

1For non-registered accounts; 2On rebalancing by asset allocation team; 3When rebalancing between fund classes; 4Managed Portfolios;

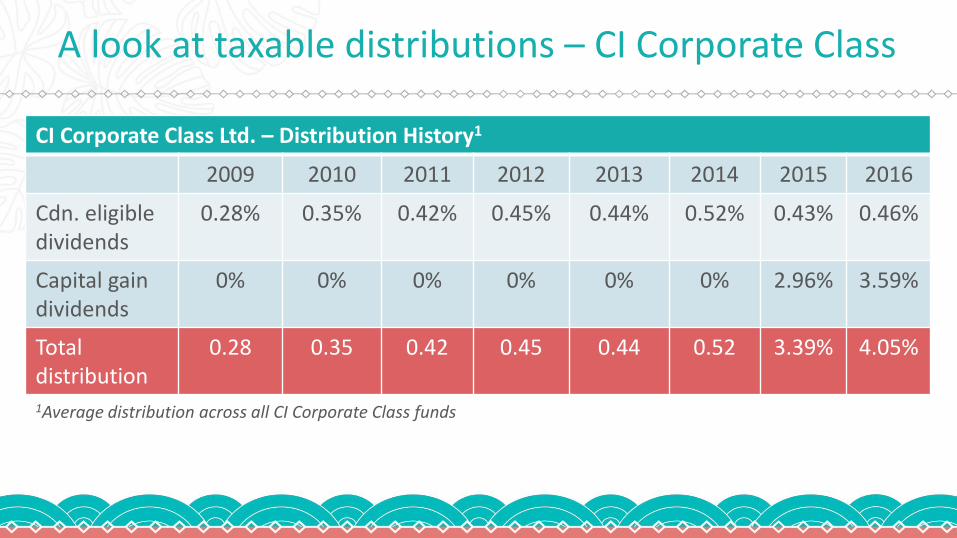

A look at taxable distributions

• Until 2009, CI Corporate Class Ltd. had not paid a taxable distribution since the late 1990s

• Since 2009, average annual distribution has been 1.24% – 0.42% Canadian eligible dividends; 0.82% capital gains dividends

A look at taxable distributions – CI Corporate Class

CI Corporate Class Ltd. – Distribution History1

2009 2010 2011 2012 2013 2014 2015 2016

Cdn. eligible dividends

0.28% 0.35% 0.42% 0.45% 0.44% 0.52% 0.43% 0.46%

Capital gain dividends

0% 0% 0% 0% 0% 0% 2.96% 3.59%

Total distribution

0.28 0.35 0.42 0.45 0.44 0.52 3.39% 4.05%

1Average distribution across all CI Corporate Class funds

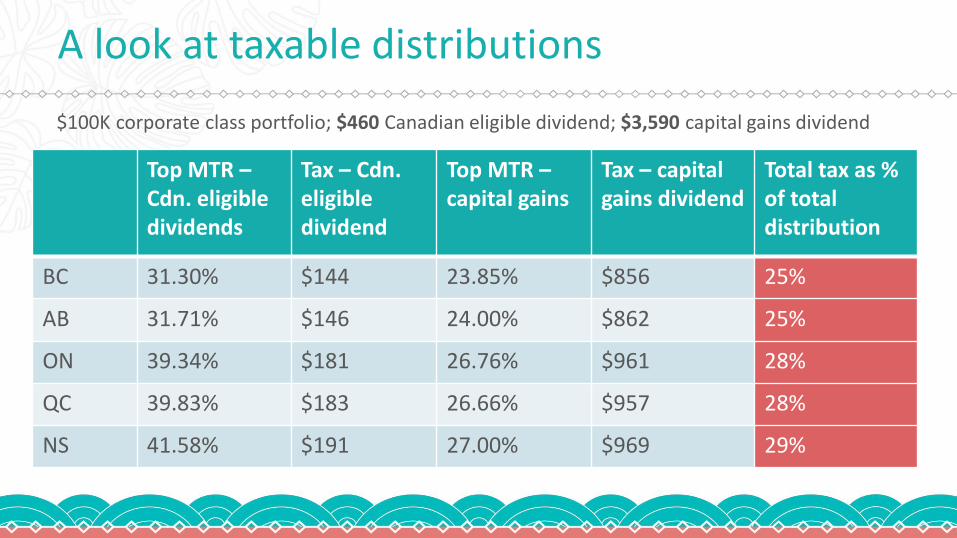

A look at taxable distributions

Top MTR – Cdn. eligible dividends

Tax – Cdn. eligible dividend

Top MTR – capital gains

Tax – capital gains dividend

Total tax as % of total distribution

BC 31.30% $144 23.85% $856 25%

AB 31.71% $146 24.00% $862 25%

ON 39.34% $181 26.76% $961 28%

QC 39.83% $183 26.66% $957 28%

NS 41.58% $191 27.00% $969 29%

$100K corporate class portfolio; $460 Canadian eligible dividend; $3,590 capital gains dividend

Corporate class funds – suitability profiles

• Non-registered investors

• In-trust accounts for minors

• Seniors

• Philanthropic clients

• Incorporated businesses

1) Non-registered investors

• Corporate class funds are best suited for non-registered accounts

– Low dividend payout policy

– Canadian eligible dividends or capital gains dividends (no interest income)

– Tax-efficient capital gains on sale

Source: CI 2016 Personal Tax Quick Reference Card

2) In-trust accounts for minors

• Income from gifts to related minors are subject to attribution – Taxed to related giftor

– Includes gifts to children, grandchildren, nieces and nephews

• Attribution rules do not normally apply to capital gains1

• Creates opportunity to split capital gains with minors

• Corporate class funds may provide reduced distributions; capital gains would be taxed to minor

• When capital gains are realized, the gain may or may not be taxable to minor depending on available deductions/credits

1Assumes in-trust account is set up appropriately to avoid section 75(2) of federal Income Tax Act (ITA)

3) Seniors

• Canadians are living longer retirements – Income/cash flow streams need to last longer

– In today’s environment, accumulation is just as important as preservation of capital

• Corporate class funds can help: – Grow assets tax-efficiently in retirement

– Access to T-class allows for lower net incomes

– Lower net incomes protect income-sensitive benefits (eg. OAS)

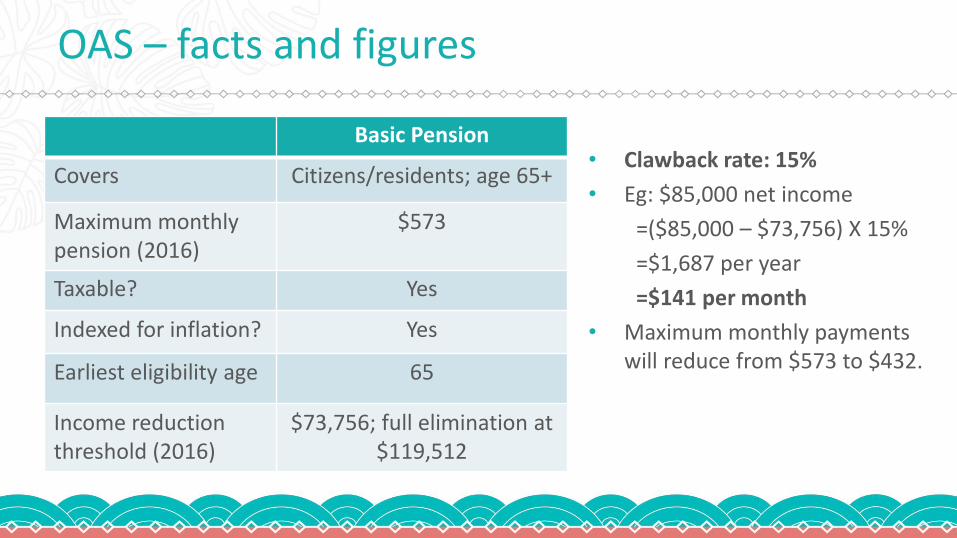

OAS – facts and figures

Basic Pension

Covers Citizens/residents; age 65+

Maximum monthly pension (2016)

$573

Taxable? Yes

Indexed for inflation? Yes

Earliest eligibility age 65

Income reduction threshold (2016)

$73,756; full elimination at $119,512

• Clawback rate: 15%

• Eg: $85,000 net income

=($85,000 – $73,756) X 15%

=$1,687 per year

=$141 per month

• Maximum monthly payments will reduce from $573 to $432.

T-Class mutual funds

$0

$25,000

$50,000

$75,000

$100,000

$125,000

$150,000

Market Value:

$100,000

ACB:

$20,000

Capital

Gain

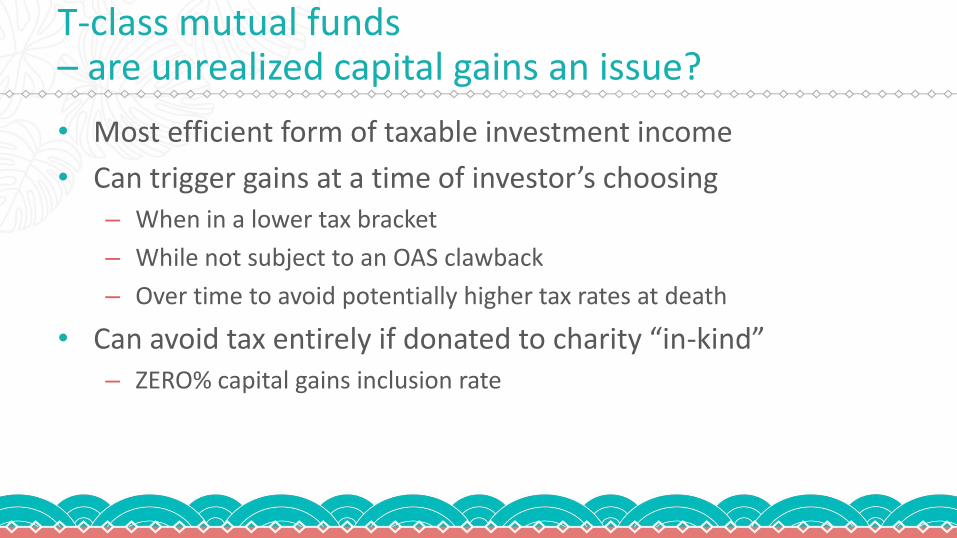

T-class mutual funds – are unrealized capital gains an issue?

• Most efficient form of taxable investment income

• Can trigger gains at a time of investor’s choosing – When in a lower tax bracket

– While not subject to an OAS clawback

– Over time to avoid potentially higher tax rates at death

• Can avoid tax entirely if donated to charity “in-kind” – ZERO% capital gains inclusion rate

4) Philanthropic clients

• Tax credit for donations of up to 75% of net income1

• Unused donations can be carried forward for up to 5 years

• Donations can be shared between spouses/CLPs

• ZERO capital gains tax on “in-kind” donations2

Province Federal/ provincial credit3

After-tax cost : $1K donation3

British Columbia 43.7% $563

Alberta 50.0% $500

Saskatchewan 44.0% $560

Manitoba 46.4% $536

Ontario 40.2% $598

Quebec 53.0% $470

New Brunswick 47.0% $530

Nova Scotia 50.0% $500

PEI 45.7% $543

Newfoundland 45.8% $542

1100% in year of death and year prior; 2Publicly-traded securities; 32016 rates for donations over $200. Ignores 33% federal rate for income > $200K

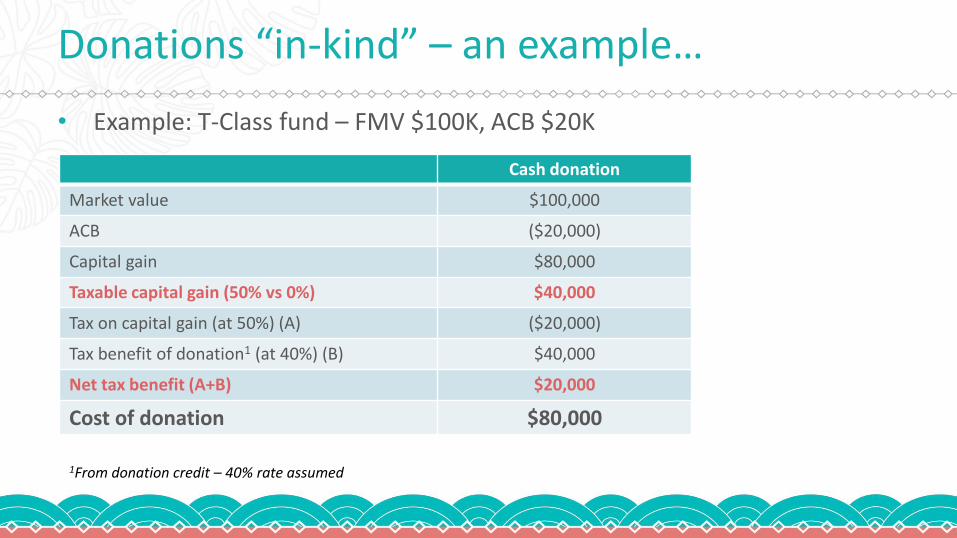

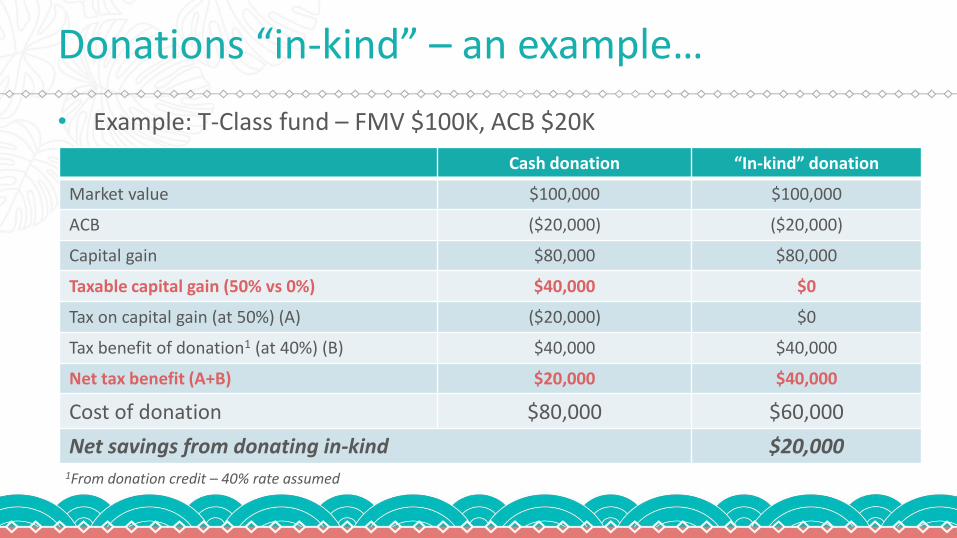

Donations “in-kind” – an example…

• Bill, a long-time corporate class investor, has benefited from tax-efficient growth for years

• At retirement, to supplement his income, Bill switched from his regular corporate class series to T-class (same fund) for ROC

• Bill has always been philanthropic; wishes to make a large donation to his local hospital, a Canadian registered charity

• At the time of donation, his T-class funds have an ACB of $20K and a FMV of $100K; Bill wishes to donate his T-class shares

• Should Bill sell and donate cash, or, donate the shares in-kind?

Donations “in-kind” – an example…

• Example: T-Class fund – FMV $100K, ACB $20K

Cash donation

Market value $100,000

ACB ($20,000)

Capital gain $80,000

Taxable capital gain (50% vs 0%) $40,000

Tax on capital gain (at 50%) (A) ($20,000)

Tax benefit of donation1 (at 40%) (B) $40,000

Net tax benefit (A+B) $20,000

Cost of donation $80,000

1From donation credit – 40% rate assumed

Donations “in-kind” – an example…

• Example: T-Class fund – FMV $100K, ACB $20K

Cash donation “In-kind” donation

Market value $100,000 $100,000

ACB ($20,000) ($20,000)

Capital gain $80,000 $80,000

Taxable capital gain (50% vs 0%) $40,000 $0

Tax on capital gain (at 50%) (A) ($20,000) $0

Tax benefit of donation1 (at 40%) (B) $40,000 $40,000

Net tax benefit (A+B) $20,000 $40,000

Cost of donation $80,000 $60,000

Net savings from donating in-kind $20,000 1From donation credit – 40% rate assumed

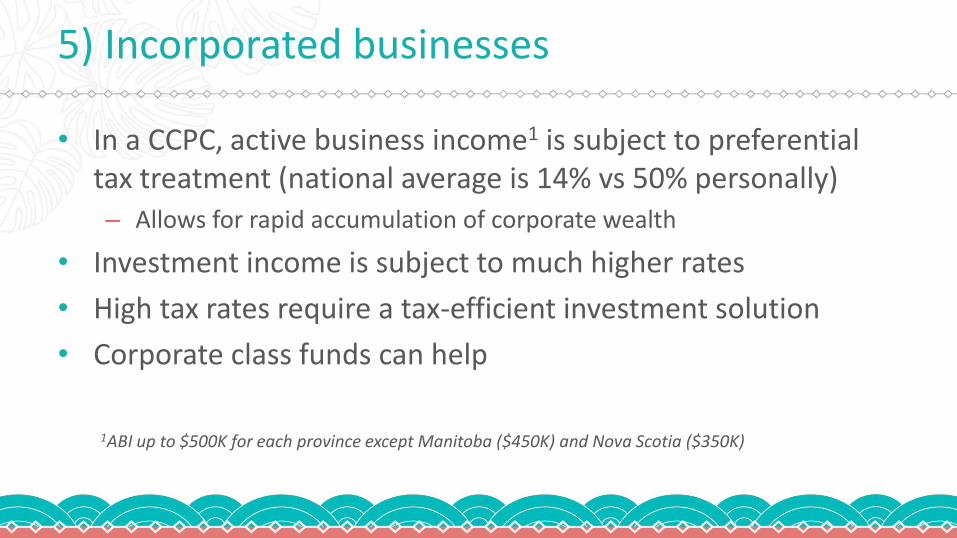

5) Incorporated businesses

• In a CCPC, active business income1 is subject to preferential tax treatment (national average is 14% vs 50% personally) – Allows for rapid accumulation of corporate wealth

• Investment income is subject to much higher rates

• High tax rates require a tax-efficient investment solution

• Corporate class funds can help

1ABI up to $500K for each province except Manitoba ($450K) and Nova Scotia ($350K)

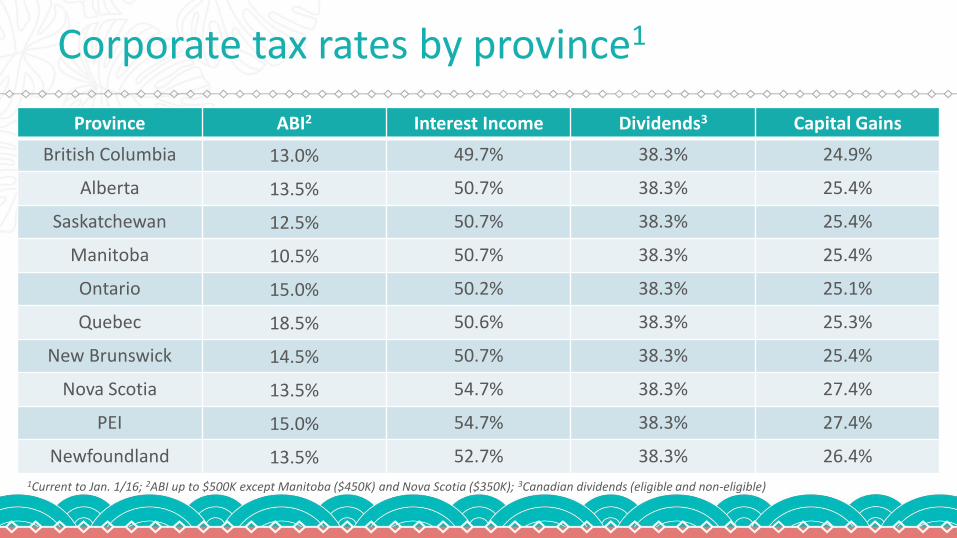

Corporate tax rates by province1

Province ABI2 Interest Income Dividends3 Capital Gains

British Columbia 13.0% 49.7% 38.3% 24.9%

Alberta 13.5% 50.7% 38.3% 25.4%

Saskatchewan 12.5% 50.7% 38.3% 25.4%

Manitoba 10.5% 50.7% 38.3% 25.4%

Ontario 15.0% 50.2% 38.3% 25.1%

Quebec 18.5% 50.6% 38.3% 25.3%

New Brunswick 14.5% 50.7% 38.3% 25.4%

Nova Scotia 13.5% 54.7% 38.3% 27.4%

PEI 15.0% 54.7% 38.3% 27.4%

Newfoundland 13.5% 52.7% 38.3% 26.4% 1Current to Jan. 1/16; 2ABI up to $500K except Manitoba ($450K) and Nova Scotia ($350K); 3Canadian dividends (eligible and non-eligible)

Taxation of interest income (B.C.)

Dividend to shareholder ($810)1

Personal tax = $329 (40.6%) After-tax cash = $481 (59.4%)

Corporation Corporate tax = $497 (49.7%)

Refundable tax = $307 (30.7%) Retained earnings = $503 (50.3%)

Interest Income

$1,000

1Non-eligible dividend

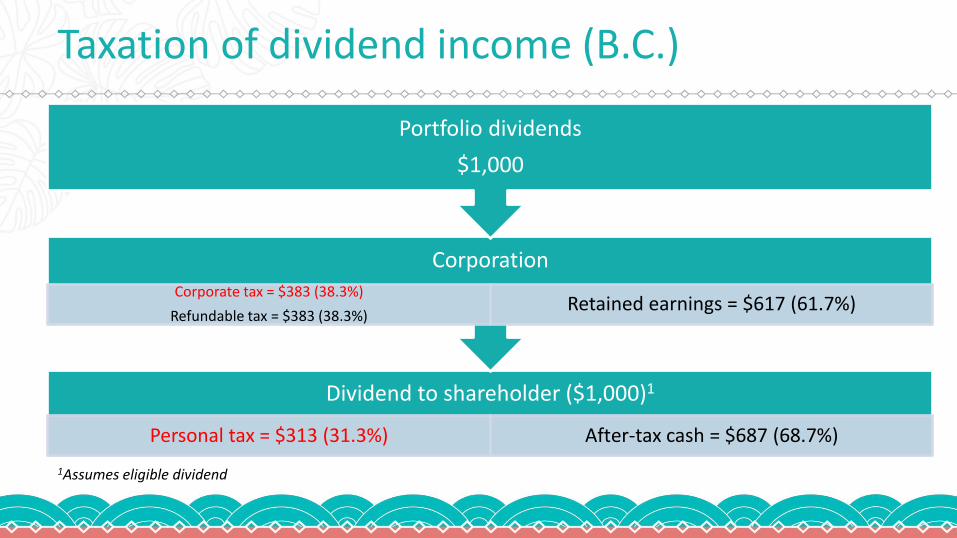

Taxation of dividend income (B.C.)

Dividend to shareholder ($1,000)1

Personal tax = $313 (31.3%) After-tax cash = $687 (68.7%)

Corporation Corporate tax = $383 (38.3%)

Refundable tax = $383 (38.3%) Retained earnings = $617 (61.7%)

Portfolio dividends

$1,000

1Assumes eligible dividend

Capital dividend account (CDA)

CDA balance

Plus: Non-taxable

portion of capital gains

Plus: Non-taxable

portion of ECP

Plus: Capital dividends received

Plus: Net proceeds of a life insurance

policy

Less: Capital dividends paid

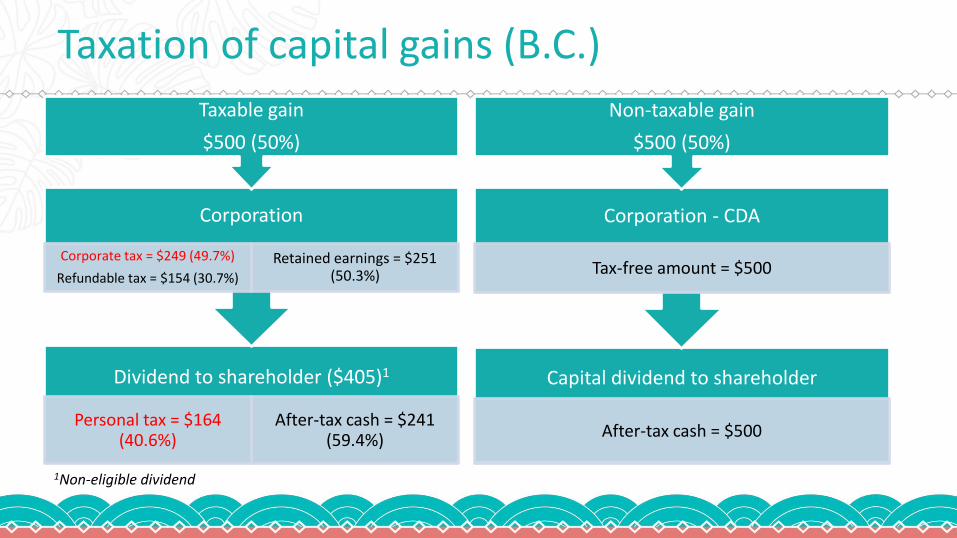

Taxation of capital gains (B.C.)

Dividend to shareholder ($405)1

Personal tax = $164 (40.6%)

After-tax cash = $241 (59.4%)

Corporation

Corporate tax = $249 (49.7%)

Refundable tax = $154 (30.7%)

Retained earnings = $251 (50.3%)

Taxable gain

$500 (50%)

Capital dividend to shareholder

After-tax cash = $500

Corporation - CDA

Tax-free amount = $500

Non-taxable gain

$500 (50%)

1Non-eligible dividend

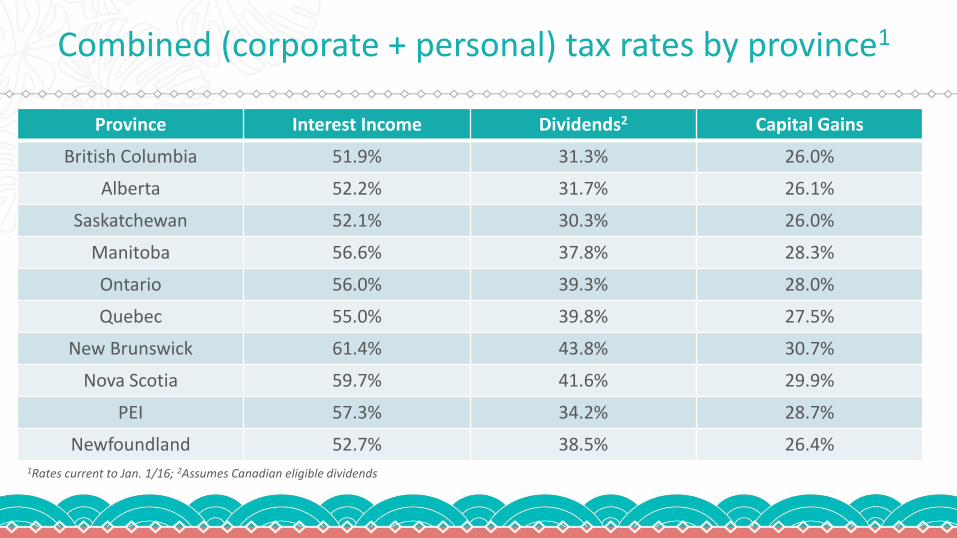

Combined (corporate + personal) tax rates by province1

Province Interest Income Dividends2 Capital Gains

British Columbia 51.9% 31.3% 26.0%

Alberta 52.2% 31.7% 26.1%

Saskatchewan 52.1% 30.3% 26.0%

Manitoba 56.6% 37.8% 28.3%

Ontario 56.0% 39.3% 28.0%

Quebec 55.0% 39.8% 27.5%

New Brunswick 61.4% 43.8% 30.7%

Nova Scotia 59.7% 41.6% 29.9%

PEI 57.3% 34.2% 28.7%

Newfoundland 52.7% 38.5% 26.4% 1Rates current to Jan. 1/16; 2Assumes Canadian eligible dividends

CI Corporate Class funds

• CI Corporate Class Ltd. – Established in 1987

• Over 65 Corporate Class funds across all asset types1

• Over $45 billion in AUM1

• T-Class and $US options available

1Equity, balanced, income/specialty; current to September 2016

Have you had a chance to explore TREP.ci.com?

Thank You

Commissions, trailing commissions, management fees and expenses may be associated with mutual fund investments. Please read the prospectus before investing. Unless otherwise indicated and except for returns for periods less than one year, the indicated rates of return are the historical annual compounded total returns including changes in security value. All performance data assume reinvestment of all distributions or dividends and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any security holder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. This presentation is provided as a general source of information and should not be considered personal investment advice or an offer or solicitation to buy or sell securities. Every effort has been made to ensure that the material contained in this commentary is accurate at the time of publication. However, CI Investments Inc. cannot guarantee its accuracy or completeness and accepts no responsibility for any loss arising from any use of or reliance on the information contained herein. All charts and illustrations in this guide are for illustrative purposes only; they are not intended to predict or project investment results. This report may contain forward-looking statements about CI funds, future performance, strategies or prospects, and possible future fund action. These statements reflect the portfolio managers’ current beliefs and are based on information currently available to them. Forward-looking statements are not guarantees of future performance. We caution you not to place undue reliance on these statements as a number of factors could cause actual events or results to differ materially from those expressed in any forward-looking statement, including economic, political and market changes and other developments. ®CI Investments and the CI Investments design are registered trademarks of CI Investments Inc. Published September 2016. FOR ADVISOR USE ONLY – NOT FOR DISTRIBUTION TO CLIENTS