UNITED ARAB EMIRATES | 2015 THE PROPERTY REPORT · LOW OIL PRICE ENVIRONMENT TO CURTAIL ECONOMIC...

56

cluttons.com UNITED ARAB EMIRATES | 2015 THE PROPERTY REPORT

Transcript of UNITED ARAB EMIRATES | 2015 THE PROPERTY REPORT · LOW OIL PRICE ENVIRONMENT TO CURTAIL ECONOMIC...

cluttons.com

UNITED ARAB EMIRATES | 2015

THE PROPERTY REPORT

LOW OIL PRICE ENVIRONMENT TO CURTAIL ECONOMIC GROWTH IN 2015As expected, the persistence of a low oil price environment which took hold last autumn has begun to impact the ability of most GCC states to deliver balanced budgets. The UAE too has begun to feel the pressure of diminishing hydrocarbon receipts, which ratings agency Moody’s estimates comprised

75% of the nation’s fiscal reserves during 2014. In fact, the Emirates Inter Bank Offered Rate (EIBOR) surged to its highest level in 16 months during August, while deposit levels have fallen, according to data compiled by Bloomberg.

The 54% fall in oil prices from a high of US$ 110 per barrel last summer to approximately US$ 50 per barrel now is starting to impact the nation’s finances. The IMF estimates a price of US$ 75 is required for a break-even budget for the UAE. As a result, the IMF is now forecasting the UAE to post a 2.3% budget deficit this year; the nation’s first since the ‘great recession’ in 2009. As a consequence of this, GDP expansion is expected to slow to 3.2% in 2015, from 4.2% last year.

ECONOMY

0

20

40

60

80

100

120

140

Jan

2003

Jul 2

003

Jan

2004

Jul 2

004

Jan

2005

Jul 2

005

Jan

2006

Jul 2

006

Jan

2007

Jul 2

007

Jan

2008

Jul 2

008

Jan

2009

Jul 2

009

Jan

2010

Jul 2

010

Jan

2011

Jul 2

011

Jan

2012

Jul 2

012

Jan

2013

Jul 2

013

Jan

2014

Jul 2

014

Jan

2015

Jul 2

015

US$

/ b

arre

l

PERFORMANCE OF OIL PRICES

While it is not unusual for a commodity such as crude oil to experience periods of exceptional volatility, the relative stability in prices between early 2011 and late last year, meant that many OPEC states were tempted into engaging in a wide range of state backed infrastructure and utility projects, many of which are now at risk of being stalled or perhaps even cancelled.

Source: OPEC

2 cluttons.com

In keeping with the government’s usual long-term thinking mantra, the UAE has begun to initiate a series of fiscal measures to help shore up its financial position, while considering additional measures to help cushion it from further oil price shocks. On August 1, the UAE became the first gulf state to begin deregulating fuel prices, effectively removing government funded fuel subsidies that have been in place since the country was formed in 1971. The IMF estimates that petroleum subsidies in the UAE amount to AED 25.7 billion, which forms part of the larger AED 389 billion energy subsidy budget, equating to nearly 7% of GDP.

The fuel price reforms come in the wake of the decision by the emirates of Abu Dhabi and Dubai to hike water and electricity tariffs in recent years as the two emirates’ governments slowly chip away at utility subsidies.

A monthly meeting of the newly formed Fuel Price Committee will set fuel prices each month, based on global averages. For the month of August, the committee announced a 24% hike in petrol prices, while diesel costs fell by nearly a third. Despite this step change, prices at the pump remain about a third cheaper than they are in the USA and nearly four times cheaper than the UK. This is likely to drive up consumer price inflation levels; however the rate of increase may be offset to an extent by lower manufacturing and logistics costs as a result of the fall in diesel prices, thus helping the country to retain a degree of its cost competitive edge, when compared to the rest of the GCC. Moody’s has estimated that the change in petrol prices in August will cost each UAE resident an extra AED 1,420 this year.

OIL PRICE PLUNGE TRIGGERS POLICY CHANGES

3cluttons.com

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

Bahrain

Iran

Kuwait

Oman

Qatar

Saudi Arabia

United Arab Emirates

United Kingdom

United States

Venezuela

AED

/ li

tre

ECONOMY

GLOBAL GASOLINE COSTS PER LITRE

MORE ECONOMIC REFORMS EXPECTEDThe gradual dismantling of federal energy subsidies has not gone unnoticed by the investment community. In fact, Abu Dhabi, which Moody’s estimates controls 94% of the UAE’s total oil production, has already seen its sovereign bond yields decline by 5 basis points, reflecting the boost to the national credit profile. Moody’s estimates that the change in fuel subsidy policies will result in savings of approximately AED 13.8 billion by the Abu Dhabi government.

Aside from fuel subsidies, the government is now also reportedly considering tackling the sensitive issue of value added tax (VAT) and corporation tax, something the federation has taken great care to avoid since its formation. In late July the Ministry of Finance announced that a draft law for the introduction of VAT and corporation tax is expected before the end of 2015; however implementation is not expected this year. Further details on whether or not free zone companies will be exempt from a corporation tax are yet to be announced.

The lack of VAT and corporation taxes has allowed the UAE to emerge unchallenged as the region’s business and commercial nerve centre. The change in policy is however unlikely to dent the UAE’s global reputation. As the economy matures, a raft of economic reforms to bolster government revenues was inevitable and we are now experiencing a period of transition as the national economy matures and the federal government works to diversify its income base away from hydrocarbon receipts.

UAE GDP GROWTH FORECAST

-6

-4

-2

0

2

4

6

8

10

12

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

% c

hang

e pe

r an

num

Source: IMF

Source: GlobalPetrolPrices.com

4 cluttons.com

In the lead up to the historic mid-July deal between six world powers and Iran in Vienna, there was much speculation about the potential boost to the UAE’s economic activity. Prior to the introduction of trade sanctions, Iran was the UAE’s biggest trading partner and tourist arrivals to the UAE from the Iranian republic have fallen by 50% since 2010 according to the IMF. However, despite the sanctions, it has remained an important trade partner for the emirates, emerging as the UAE’s fourth largest trading partner in 2014, according to the latest figures from the Iranian government, which translates into AED 62.4 billion of cross border trade; up 8.3% on 2013.

Our view remains unchanged and we see the landmark deal as a medium to long term catalyst for the UAE’s growth, which is expected to be centred on Dubai. Both local and global businesses have in the past hubbed any Iranian operations out of Dubai and we expect this phenomenon to begin in earnest once the US congress formally agrees to the lifting of the debilitating six-layered UN sponsored trade and economic sanctions.

CAN THE IRAN DEAL BOLSTER ECONOMIC GROWTH IN THE UAE?

In fact, the Iranian government has already announced that estimated investment of AED 734 billion is required over the next five years by its oil and gas industry alone, while the aviation sector requires just over AED 18 billion in immediate investments. We expect to see the vast majority of these funds funnelled through the UAE’s financial system, which should aid in the improvement of national liquidity levels.

The rippling outward of business activity as global firms line up to service an economy that has been starved of investment for over a decade is not only likely to benefit other emirates in the federation, but regional states as well.

The downside to the lifting of trade sanctions is of course the impact of a resumption in Iranian hydrocarbon exports on the fickle oil market. While Iran’s oil export levels are unlikely to rise rapidly, it is our view that further oil price falls are likely once the sanctions are officially lifted. The magnitude of any downward movement and the duration for which the low oil price era lingers very much hinges on how quickly the EU can negotiate a Greek deal and return to growth. At the same time, as the bloc remains one of China’s most important

export markets, the country’s economic performance and therefore demand for oil remain in a holding pattern, which highlights the risks faced by the wider global economy.

REAL ESTATE BOOST LIKELY TO BE FELT IN DUBAI FIRSTFor the real estate landscape, the return of an Iranian variable to the national real estate equation will be particularly momentous.

It is our view that Iranian nationals will seize the opportunity to make significant real estate investments in Dubai, allowing them to climb up the buyer nationality league table. In 2010, Iranian nationals accounted for 12% of Dubai’s real estate transactions, positioning them in fourth place behind Indian, British and Pakistani nationals.

However with the onset of trade sanctions, investment volumes from Iranian nationals dwindled and stood at a low of just 3% during the first quarter of 2015 according to data from the Dubai Land Department. This is expected to be amongst the first lead indicators of the benefits to the UAE from the lifting of Iranian trade sanctions; however an exact date for this is yet to be confirmed.

AED

62.4 bnUAE-Iran cross border trade in 2014

AED

18 bnEstimated investment required by Iran’s aviation sector

Source: Government of Iran

AED

734 bnEstimated investment needed by Iran’s oil and gas sector over the next 5 years

5cluttons.com

ABU DHABI

Sheikh Zayed Grand Mosque

6 cluttons.com

HOUSE PRICE GROWTH STALLS After growing by 0.5% in Q1, house prices across the capital slipped by 0.2% in the second quarter, the first contraction since Q3 2012. The shrinking in average house prices across Abu Dhabi’s investment zones has reduced the annual rate of increase from just over 15% at the end of March to around 3% at the end of June. This equates to a current average house price of AED 1,336 psf.

RESIDENTIAL MARKET

PERFORMANCE OF ABU DHABI RESIDENTIAL VALUES

APARTMENT VALUES STABLEWhile the performance of the market so far this year certainly suggests further downward adjustments are likely as the economy absorbs the impact of the sharp fall in oil prices, apartment values have remained largely stable, with the exception of high-end apartments on Reem Island, where prices slipped by 1.6% during the first half of the year.

BUYER DEMAND POLARISED AT THE EXTREMITIES OF THE MARKETThe nature of demand being stable for the top end, luxury market and the more affordable, sub AED 1,000 psf properties mirrors our own experience in the market. On one hand you have an affluent segment of the population, predominantly comprised of Emirati and GCC buyers, who continue to home in on schemes such as those on Saadiyat due to the perceived exclusivity.

At the other end of the spectrum, you have a large expat population, who are being squeezed out of the rental market due to the rampant rental growth over the past 18 months, which has remained well ahead of inflation and wage growth rates. This group continues to target

schemes that offer the best perceived value for money, which is helping more affordable submarkets such as Ghadeer, weather the downward pressures in the market for the time being.

Furthermore, the strong capital value growth also means some aspiring households are left with little option but to rent for longer while they amass deposits to overcome the strictly enforced Federal Mortgage Caps. It was inevitable that demand would become polarised, with a renewed focus on what is perceived to be more affordable property.

This also creates a clear opportunity for developers to focus on this relatively untapped portion of the market. While Dubai has made strides to begin addressing the affordable housing challenges it faces, Abu Dhabi still lags its northern neighbour to an extent. That said, in order for any affordable housing initiatives to take hold, intervention at a federal level is required to ensure that the entire nation benefits from the introduction of a new affordable housing class, or affordable housing quotas.

-5

-3

-1

1

3

5

7

9

11

13

15

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

% c

hang

e

Average annual rent in Abu Dhabi

AED

204,000Source: Cluttons, IMF, UAE Ministry of Economy

Average annual expat income

AED

199,000

Source: Cluttons

ABU DHABI

7cluttons.com

ABU DHABI

RENTAL MARKET GAINS MOMENTUMAfter rents stagnated during the first quarter of the year, a 1.5% rise in average rents was registered during the second quarter, pushing annual growth up to 3.9%. This does however mask the fact villas (2.6%) outperformed apartments (0.3%), which continued to see rents stagnate, mirroring the pattern that began in Q1.

Echoing the sentiment from the sales market, it is not surprising that Hydra Village was the strongest performing market in the capital, with rents for three-bedroom villas surging by almost 32% during the first six months of the year to AED 125,000 per annum, while two-bedroom villas (AED 110,000 per annum) registered a near 30% increase in rents. This reflects the increased focus by tenants on properties they perceive to be affordable.

RENTS SLIP ON SAADIYAT ISLANDThe weakest performing apartment market during H1 was on Saadiyat Island. While two-bedroom apartments managed to record a near 3% increase in rents, three- and four-bedroom apartments registered falls of 10.2% and 11.9%, respectively.

While tenants continue to cite the exclusivity factor as the underlying appeal of the capital’s emerging cultural hub, rents here appear to have risen ahead of the market. And with other submarkets such as Reem Island, which is in closer proximity to central Abu Dhabi, tenants are being lured here as rents are still largely below those on Saadiyat Island.

RESIDENTIAL SALES AND LETTINGS MARKETS SHARE MUTE OUTLOOKThe outlook for the capital’s residential market has deteriorated since the start of the year, underpinned by the prolonged weakness in oil prices and the cascading impact this has had on the strength of demand in Abu Dhabi’s commercial and residential sectors. While the residential market has experienced average price rises of 34% since 2010, the rate of change over the past four quarters has been far more subdued. Several factors may influence the behaviour of the residential market in the medium to short term, but with anecdotal evidence pointing to a growing number of stalled infrastructure projects as government spending eases, the subsequent rate of job creation and residential demand is also expected to stabilise, or weaken slightly, therefore denting demand.

For now however, bulk residential lettings deals are still common and are being driven predominantly by the hospitality and education sectors, which often removes stock from the delivery pipeline before it is released onto the market. However, with the rate of job creation likely to slow in the coming months, this trend is likely to subside to an extent.

With this in mind, it is our view that the residential market will see further slight to moderate price falls over the remainder of 2015; however there will continue to be markets, such as Hydra Village, which are expected to outperform for the reasons outlined above. Overall, quarterly house price declines of between 0.5% and 1% can be expected in both Q3 and Q4, while rents are expected to remain largely flat during H2.

THE OUTLOOK FOR THE CAPITAL’S RESIDENTIAL MARKET HAS DETERIORATED SINCE THE START OF THE YEAR, UNDERPINNED BY THE PROLONGED WEAKNESS IN OIL PRICES AND THE CASCADING IMPACT THIS HAS HAD ON THE STRENGTH OF DEMAND

8 cluttons.com

During June, the government of Abu Dhabi announced a range of new regulatory measures, aimed at shoring up confidence in the market. The key highlights of the new rules, which fall under the jurisdiction of the Department of Municipal Affairs, include the creation of a real estate register, the requirement for developers to set up escrow accounts, an off-plan sales register and the licensing of real estate brokers.

While the raft of new laws will offer investors a greater sense of comfort as the authorities work to improve the market’s transparency, there was no mention of the much anticipated introduction of a rent-index, similar to that used in Dubai. For a market like Abu Dhabi where rents have risen by 16% since 2013, well above wage

growth, which we estimate to have grown by just 4.8% over the same period, a rent-index will go a long way in helping to give landlords and tenants a barometer from which they can gauge market performance.

The removal of the rent cap has allowed the market to behave in a more dynamic manner, mirroring real-time market conditions; however the benefit of a rent-index will offer tenants some protection while educating landlords, particularly those of an international, buy-to-let flavour.

It is worth noting that any index will always lag real-time conditions by two to three months and will be unable to capture nuances of variables such as unit size, views, proximity to public transport nodes, etc.

REGULATORY CHANGES ARE A STEP IN THE RIGHT DIRECTION

9cluttons.com

ABU DHABI

OFFICE MARKET

Secondary office rents

AED1,300 psm

Tertiary office rents

AED900 psm

Prime office rents

AED1,850 psm

RENTS STAGNATE AS DEMAND TAILS OFFRents across the capital continued to hold steady through the second quarter, with prime, secondary and tertiary rents all remaining unchanged for the fourth consecutive quarter. Prime rents, which stand at AED 1,850 psm, have remained stable for 14 quarters now.

The office market’s recent stagnation is in large part linked to the slowdown in public spending, which has translated into a drop in demand for new office space. However, due to a general lack of supply, particularly at the Grade A end of the market, rents have held steady and are expected to remain stable over the course of 2015 in our central scenario.

RENT DECLINES LIKELY IN 2016As outlined above, Abu Dhabi’s heavy dependence on hydrocarbon revenues has meant that the rate of office take up, which is traditionally dominated by oil and gas companies, has cooled significantly.

This is likely to put increased downward pressure on more secondary and tertiary locations in the first instance, with prime rents likely to face headwinds shortly thereafter. We do not expect to see this chain of events play out in quick succession, but think it likely that rents will begin to weaken towards the tail end of this year, or at the beginning of 2016 should the emirate’s economy slow further.

Source: Cluttons

10 cluttons.com

SIGNATURE TOWERS’ RATES REMAIN UNCHANGEDFor now however, mirroring the behaviour in the city’s prime office market segment, Abu Dhabi’s ‘signature’ office towers recorded no change in rents during Q2, which means that rents for the most part have remained stable for three consecutive quarters.

Etihad Towers (AED 2,250 psm), International Tower (AED 2,050 psm) and Nation Towers and the World Trade Centre Office Tower (both at AED 2,000 psm) remain the city’s most expensive (aside from Abu Dhabi Global Market). And with occupancy levels remaining at or close to 100%, we are unlikely to see any upward movement in signature towers’ rents until space is returned to the market.

Q2 RENTS IN ‘SIGNATURE’ OFFICE TOWERS

0

500

1,00

0

1,50

0

2,00

0

2,50

0

3,00

0

3,50

0

4,00

0

Etihad Towers

Aldar HQ

World Trade Centre Office Tower

Nation Towers

International Tower

Capital Gate

Capital Tower

Addax Tower

Abu Dhabi Global Market Square

AED psm

Source: Cluttons

Away from this cohort of super-prime buildings, the newly established Abu Dhabi Global Market financial free zone on Maryah Island continues to cement its position as the city’s new ultra-prime office benchmark, with asking rents standing at approximately AED 3,700 psm.

While this still sits above its nearest comparable at the Dubai International Financial Centre (circa. AED 2,400 psm), demand for space here remains stable as international businesses home in, attracted by the international regulatory framework. Still, the vast majority of global organisations continue to headquarter in Dubai, with Abu Dhabi often the location for satellite offices.

11cluttons.com

DUBAI

Dubai Creek

12 cluttons.com

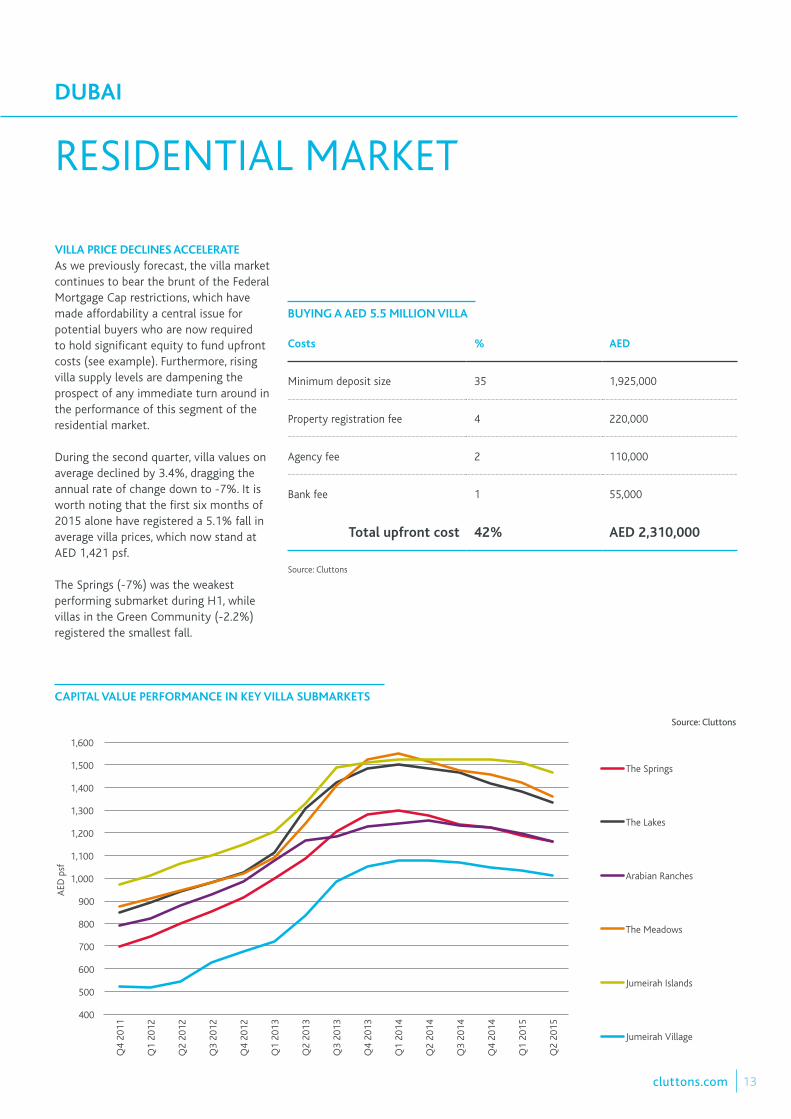

VILLA PRICE DECLINES ACCELERATEAs we previously forecast, the villa market continues to bear the brunt of the Federal Mortgage Cap restrictions, which have made affordability a central issue for potential buyers who are now required to hold significant equity to fund upfront costs (see example). Furthermore, rising villa supply levels are dampening the prospect of any immediate turn around in the performance of this segment of the residential market.

During the second quarter, villa values on average declined by 3.4%, dragging the annual rate of change down to -7%. It is worth noting that the first six months of 2015 alone have registered a 5.1% fall in average villa prices, which now stand at AED 1,421 psf.

The Springs (-7%) was the weakest performing submarket during H1, while villas in the Green Community (-2.2%) registered the smallest fall.

RESIDENTIAL MARKET

CAPITAL VALUE PERFORMANCE IN KEY VILLA SUBMARKETS

BUYING A AED 5.5 MILLION VILLA

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

AED

psf

The Springs

The Lakes

Arabian Ranches

The Meadows

Jumeirah Islands

Jumeirah Village

Costs % AED

Minimum deposit size 35 1,925,000

Property registration fee 4 220,000

Agency fee 2 110,000

Bank fee 1 55,000

Total upfront cost 42% AED 2,310,000

Source: Cluttons

Source: Cluttons

DUBAI

13cluttons.com

-8

-6

-4

-2

0

2

4

6

8

10

12

14

16

18

20

22

24

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

% c

hang

e

RESIDENTIAL MARKET PERFORMANCE: CAPITAL VALUE GROWTH RATES

DUBAI

APARTMENT CAPITAL VALUES SHOW GREATER RESILIENCEApartments on the other hand have performed slightly better, with average values moderating by -0.4% to AED 1,471 during Q2, which translates into a 0.6% fall between January and June this year. Overall, there has been almost no change in average apartment values during H1.

High end apartments in Dubai Marina (-2.6%), mid-range apartments on the Palm Jumeirah (-1.9%) and high-end apartments on the Palm Jumeirah (-1.7%) have been the three weakest performing submarkets, reflecting a combination of previously stubborn vendors reducing prices to reflect market reality and those gradually lowering asking prices below prevailing rates to entice buyers.

Overall, house prices in Dubai’s residential market now stand 3.1% below this time last year and 21% below the Q3 2008 market peak.

TOTAL NUMBER OF RESIDENTIAL TRANSACTIONS FAIRLY STABLELooking specifically at buildings and units, there was a 7% dip in the number of deals recorded, while the value of all real estate transactions slipped by nearly a quarter (Dubai Land Department).

Drilling down further into the residential market, the picture is fairly stable, with data from Reidin showing that transactions during H1 were down 2.3% on the same period last year. The number of apartment transactions dipped by 1.1%, while the number of villas that changed hands decreased by 13.1% when compared to H1 2014, reflecting the affordability challenges outlined above.

Source: Cluttons

14 cluttons.com

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

-16

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

% c

hang

e

RESIDENTIAL MARKET PERFORMANCE: RENTAL VALUE GROWTH RATES

RENTS CONTINUE TO EBB GRADUALLYDuring the second quarter, average rents in Dubai declined by 0.9%, following the 0.4% decrease recorded in Q1. This takes the overall change in the six months to June to -1.3%, while the year-on-year change now stands at -3.6%. Looking specifically at villas, Q2 saw a 1% fall in average rents, with three-bedroom properties in more affordable communities such as the Springs, Jumeirah Village, Falcon City, Al Reem and The Villa seeing rents fall by almost 6% between January and June this year.

This can in part be attributed to a moderation in demand due to the breach of affordability thresholds. Elsewhere, villas on the Palm Jumeirah and those in Jumeirah Islands, The Lakes - Hattan and Arabian Ranches - Hattan have all seen rents remain unchanged so far this year; a trend we expect to persist.

-7%fall in villa values during H1

-0.6%fall in apartment values during H1

-3.1%year-on-year decline in average house prices across Dubai

Source: Cluttons

In contrast to the behaviour of the villa market, apartments in affordable communities such as International City, IMPZ, Discovery Gardens, Jumeirah Village Circle, Jumeirah Village Triangle, Dubai Sports City, Jumeirah Lake Towers and Dubai Land have all held steady in 2015, while the steepest declines have been recorded by one-bedroom properties (-4.4%) at the top end of the market in communities such as Downtown Dubai, Dubai Marina, the Palm Jumeirah and the DIFC.

Source: Cluttons

15cluttons.com

FURTHER WEAKENING EXPECTED IN THE RESIDENTIAL MARKET THIS YEARStiff headwinds in the form of Federal Mortgage Caps and general affordability challenges have been exacerbated by a rise in the number of project announcements; 41,000 units have been announced so far this year. The surge in the number of project announcements over the last two years, which has been a direct result of confidence injected into the market by the 15% rise in average residential values over the same period, has translated into a strengthening supply pipeline through to 2017. In fact, we expect just over 20,000 units to be delivered by the end of 2017, with villas accounting for almost 70% of the total.

This of course is against a backdrop of an already weak villa market, suggesting that a sudden turnaround in values is unlikely. With average villa prices already down by over 5% during H1, we anticipate a further 5% to 7% fall in the second half of the year as values adjust to market conditions and more importantly, buyers’ budgets.

Apartments on the other hand still continue to be viewed favourably by ‘buy-to-let’ and ‘buy-to-leave’ investors, particularly those from the region looking for a safe haven. In addition, the success of recent off-plan project sales, which continue to come to market approximately 10% to 20% below prevailing rates for completed properties, underscores the affordability challenges faced by the domestic market.

However the propensity for developers to promote balloon payment plans, which see buyers paying the majority of the purchase price upon handover, is allowing this market to be accessed by a wider segment of buyers who may have previously been priced out.

RENTAL MARKET TO STAY WEAKDespite falling to 4.2% in July, from a six-year high of 4.7% in May, inflation rates in the emirate are expected to come under increased upward domestic pressure as households adjust to the removal of federal fuel and utility subsidies, which, together with housing costs, account for 44% of the consumer price inflation basket. Still, households can take some comfort in the fact that the strength of the US dollar, to which the dirham maintains a fixed peg, will continue to hold back the level of imported inflation, which to an extent will ease the burden on household finances.

With this in mind, it is our view that the rental market will remain weak, with further slight declines in the region of 1.5% to 2% likely during the second half of the year.

BRIGHT MEDIUM TERM OUTLOOK SCENARIOWhile the continuation of price moderation in the sales market is likely to persist, the rental market is expected to fare slightly better. The Expo 2020 event has moved from being on the medium-term event horizon, to being on the short-term event

horizon and with associated public spending on supporting infrastructure likely to gain further momentum as the event draws closer, job creation levels are unlikely to be dented in the near term.

If anything, the pace at which new jobs are created is expected to rise, which to an extent will go some way to help in absorbing the strengthening supply pipeline, particularly as we expect the population to expand by a further 400,000 to 2.8 million by 2020. This will mitigate the risk of a supply glut and therefore help to sustain rents and stabilise house price growth.

In addition, any weakening in regional demand for Dubai residential assets as a result of continuing oil price declines is expected to be countered to an extent by Iranian funds, which are waiting in the wings as outlined earlier.

However as the Dubai Land Department’s buyer nationality league tables continue to show GCC buyers dominating overall transaction activity, a weakening in long term demand from this cohort does not currently sit in our central forecast scenario. Furthermore, strengthening yields as a result of falling residential values and relatively stable rents will continue to boost Dubai’s overall investment appeal.

DUBAI

APARTMENTS STILL CONTINUE TO BE VIEWED FAVOURABLY BY ‘BUY-TO-LET’ AND ‘BUY-TO-LEAVE’ INVESTORS, PARTICULARLY THOSE FROM THE REGION LOOKING FOR A SAFE HAVEN.

16 cluttons.com

HEADLINE RENTS STAY FLATOver the course of the first six months of 2015, headline office rents for primary, secondary and tertiary space were unchanged at AED 250 psf, AED 130 psf and AED 70 psf, respectively. This does however mask a more complex picture at a submarket level across the city. And there are of course exceptions to average rates, with core DIFC and Emirates Towers for instance, recently quoting AED 275 to AED 325 psf.

Occupier activity is still diverse, with banks, financial institutions, law firms, aviation-linked businesses and the technology-media-telecoms sector accounting for the vast majority of requirements. These remain focussed on the emirate’s primary free zones and submarkets. As previously explained, desirable micro-markets, which can sometimes be as small as individual buildings within some of the larger submarkets, continue to outperform the rest of the market, achieving new benchmark rents when space becomes available.

A good example of this is the DIFC Gate Building and Gate Village, where average base rents currently start at between AED 275 psf to AED 325 psf, considerably higher than the wider DIFC average. It remains to be seen whether this trend will be de-railed by occupiers drawn to new grade A stock in third-party developed, strata-owned towers, such as Burj Daman, Park Central and Index Tower, where rents are around 25% lower than their core DIFC counterparts and service charge rates can be up to 50% lower than that for DIFC owned space.

With the rising amount of supply in the wider DIFC area, the increased competition is requiring landlords to offer space at slightly lower rates in order to secure tenants. This is attracting new operators into the zone while causing an ongoing softening of peripheral DIFC quoting rents.

OFFICE MARKET

Average tertiary office rents (72% below Q3 2008 peak)

AED

70 psf Source: Cluttons

Average secondary office rents (57% below Q3 2008 peak)

AED 130 psf

Average prime office rents (47% below Q3 2008 peak)

AED

250 psf

The pattern of outperformance is however still prevalent in free zones, such as the Dubai Internet and Media Cities, where there is little or no vacancy and rents continue to edge up as a result. Top end rents here currently stand at about AED 225 psf. TECOM is due to launch its new major Innovations Hub development later this year with a proposed handover date of Q4 2017 and this will provide relief for pent up demand from existing tenants looking to expand but remain in this free zone.

Elsewhere, more secondary and tertiary space in locations such as Deira and Bur Dubai, which saw rents move upwards during Q1, have seen a softening of growth in the second quarter. This can be attributed to the recent delivery of several Grade B schemes in submarkets such as Business Bay and Jumeirah Lake Towers, which has presented occupiers with a greater range of options and price points.

17cluttons.com

WITH THE WORLD EXPO IN 2020 LOOMING AND WITH TRADE SANCTIONS ON IRAN ON THE VERGE OF BEING LIFTED, THE OUTLOOK FOR THE OFFICE MARKET SUGGESTS A STABLE PIPELINE OF TAKE-UP ACTIVITY

18 cluttons.com

TAKE UP UNLIKELY TO WANE IN THE MEDIUM TERM AS EXPO 2020 LOOMSOverall market confidence continues to edge up as international and domestic office take up activity continues to rise, albeit at a slightly slower pace than last year. Our experience mirrors the sentiment of the Q2 Emirates NBD Dubai Economy Tracker, which signalled that optimism in future business activity reached a 19-month high in June, despite a slight softening in new orders.

However respondents from all key sectors of the emirate’s economy indicated an anticipated expansion of business activity over the course of 2015. This was in large part underpinned by planned company expansion through recruitment and an expected rise in new orders.

That said, we have recorded instances of downsizing, or consolidation of office space by oil and gas companies, reflecting headcount reductions and budgetary pressures by hydrocarbon linked firms; a pattern we are observing in other global markets as well.

This aside, with the World Expo in 2020 looming and with trade sanctions on Iran on the verge of being lifted, the outlook for the office market suggests a stable pipeline of take-up activity.

As we previously mentioned, we have already noted an upturn in speculative requirements from Dubai-based Iranian businesses looking to expand their premises in anticipation of a resumption in normal trade with Iran. Furthermore, we have also already noted several instances of Iranian businesses in the emirate approaching banks for loans to fund planned expansion.

In addition, we anticipate an upturn in international businesses looking to service any Iranian operations out of Dubai, which will once again place upward pressure on Grade A rents in sought after submarkets, particularly the city’s primary free zones such as the DIFC, the Internet & Media Cities, D3 and Dubai Airport Free Zone.

This, combined with the pipeline of government backed mega-infrastructure projects, such as the AED 117 billion Al Maktoum International Airport expansion, Dubai Metro extension and Jebel Ali Port expansion, in addition to the vast pipeline of leisure, retail and hospitality projects points to a steady, but significant pace of job creation over the short to medium term, which will translate into a steady stream of requirements.

DUBAI

0

10

20

30

40

50

60

70

80

90

Wider Economy Travel & Tourism Construction Wholesale & retail

Inde

x va

lue

(>

50 in

dica

tes

expa

nsio

n)

May 15 June 15

SECTORAL BREAKDOWN OF ENBD DUBAI ECONOMY TRACKER CONFIDENCE INDEX

Source: Emirates NBD, Markit

19cluttons.com

SHARJAH

Al Qasba Canal

20 cluttons.com

RENTS SUCCUMB TO WIDER MARKET DYNAMICSAs expected, the lettings market in Sharjah has continued to gradually slow in response to rent declines in Dubai and the introduction of what is perceived to be high-quality accommodation in neighbouring Ajman.

These constantly evolving market drivers have meant that tenants are now firmly in the driving seat, with many in a position to cherry pick from a range of options both in and out of Sharjah. In fact, our experience points to the trend of reverse migration to Dubai gaining momentum, mirroring previous property cycles, while tenants from other northern Emirates eye a return to Sharjah as its perceived affordability improves.

RESIDENTIAL MARKET

-2.3%Decline in average rents during H1

1.4%Annual change in average villa rents

AED

90,000Average rent for a three-bedroom villa

Source: Cluttons

This constant ebb and flow of tenant requirements in the face of rising supply in Dubai, Sharjah itself and Ajman has undermined the emirate’s rental market, which recorded a 2.3% dip in average rents during Q2, following no change in the first quarter. This now leaves average rents across the city’s main central submarkets just 3.3% ahead of the same time last year. Apartments registered a 4.2% decline during the second quarter, while villa rents edged up slightly by 1.4%.

On a submarket level, Al Majaz was the weakest performing area in the six months to June, with annual rents for three-bedroom flats slipping by almost 12% to AED 75,000. One-bedroom properties also recorded a near 4% decrease in average annual rents and stood at AED 50,000 at the end of Q2. On the villa front, with the exception of three-bedroom properties, which have seen rents rise by just under 6% between January and June to an average of AED 90,000 per annum, there has been no movement in rents.

SHARJAH

21cluttons.com

SHARJAH

RESIDENTIAL MARKET PERFORMANCE: RENTAL VALUE GROWTH RATES

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

-4.0

-2.0

0

2.0

4.0

6.0

8.0

10.0

12.0

% c

hang

e

RESIDENTIAL MARKET OUTLOOK HINGED ON MACROECONOMIC CONDITIONSThe turnaround in the strong rental value growth in 2014 (24.1%) has all but been erased by the anaemic performance during the first six months of 2015. This was largely anticipated, particularly as incomes failed to keep pace with this magnitude of change. While there is no doubt that this has influenced the lettings market heavily, so has the macroeconomic picture that has dented the performance of Dubai’s lettings market, which as always, has direct ramifications for Sharjah.

While authorities are clearly driving a shift away from a reliance on the hydrocarbon sector, the process was always going to be a slow burn.

The catalysing of the real estate market through the introduction of residential sales to the UAE’s expat community will no doubt help to bolster economic growth; further policy changes are likely to emerge to help foster and cement the emirate’s core sectors of manufacturing, small & medium enterprises and aviation.

While these industries continue to be nurtured, it is unlikely that home grown domestic tenant requirements will be sufficient to drive strong rental growth in the second half of this year. Instead, it is our view that rents will slip by another 2% to 4% on average before the end of 2015.

Source: Cluttons

The medium term outlook is however slightly better, with one off factors such as the lifting of trade sanctions on Iran expected to drive residential demand in Dubai up significantly, which will no doubt spill over into Sharjah. This is in turn anticipated to support a gradual return to strong growth as demand starts to overtake supply.

On the supply front, clearly developers have rushed to develop green-field sites throughout the city, but as with any scheme in Sharjah, securing SEWA connections and permits can often delay handover for up to six months, which will help to offset any rapid fall in rents in the short term as the market meanders through a challenging period.

22 cluttons.com

Despite this, Sharjah’s residential landscape continues to experience a phenomenal sea change. The pace at which world-class master planned communities such as Al Zahia and Tilal City are emerging is phenomenal and these developments are setting the benchmark for future master planned communities. These are growing in popularity and we are already seeing developers rush to meet this demand.

And while the scale and pace of development is slower than that of Dubai, or Abu Dhabi, the emirate is blazing a trail in the creation of affordable upscale developments that are designed around the emirate’s rich Islamic culture and heritage.

This in itself is allowing for the emergence of a niche residential market that caters to families who have been priced out of other UAE markets and those that have been waiting for more affordable communities in surroundings that echo their more traditional lifestyles. Sharjah is taking ‘place making’ back to basics and developing communities that people want to be a part of. There

has been a tremendous level of appetite in Sharjah’s first family friendly gated communities.

The government is spearheading the creation of family friendly enclaves on the fringes of the city that are supported with all the necessary community amenities. There is a strong underlying desire to ensure facilities such as mosques, schools, clinics and community shopping centres, along with adequate transportation infrastructure, are in place long before the first residents move in.

At Tilal City for instance, we have been overwhelmed by the demand from the local resident expat community. While UAE nationals account for just over 50% of all transactions to date, we have seen a huge amount of demand from UAE residents who are native to the wider Middle East. While some of them have been motivated to invest in the project to escape the political unrest in their home countries, many are genuinely singling out Tilal City as somewhere they wish to live and raise their families.

COMMUNITY LIVING GAINING TRACTION

23cluttons.com

SHARJAH

OFFICE MARKET

RENTS REMAIN STEADY Office rents in Sharjah’s main submarkets held steady during the second quarter, following no change in Q1. The prime areas of Al Majaz retained their position as the city’s most expensive space (AED 75 psf), while Al Soor remained the most affordable centrally located submarket, with rents standing at AED 60 psf.

The flat performance of the office market reflects a scaling back in overall requirements and take up levels while the dominant oil and gas occupiers assess their expansion plans.

PERFORMANCE OF OFFICE RENTS IN KEY SUBMARKETS

0

10

20

30

40

50

60

70

80

90

AED

psf

Al Soor Al Majaz fringe areas Al Majaz prime

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Q1

2015

Q2

2015

IN MORE SECONDARY AND TERTIARY LOCATIONS WE HAVE ALREADY SEEN LANDLORDS ADJUST RENTS DOWNWARDS IN AN EFFORT TO GENERATE DEMAND.

As previously mentioned, the small & medium enterprises, aviation and finance & banking sectors remain the main occupiers in the market, however there have been notable declines in the level of requirements from these groups so far this year as well. Still, the steady, but weaker level of activity from this cohort has gone some way to keep rents stable during the first six months of this year.

Source: Cluttons

Earlier on in the year, the market appeared to be gearing up for an extended period of low oil prices and the subsequent impact on the emirate’s economy. With this phenomenon now taking centre stage, rents in most centrally located office buildings which have remained frozen and unchanged are in danger of weakening. The ability of the market to weather the continued low oil price environment, or weakening demand, is expected to put rents under pressure, particularly at the top of the market.

24 cluttons.com

MODERATE FALL IN RENTS EXPECTEDIn more secondary and tertiary locations we have already seen landlords adjust rents downwards in an effort to generate demand. This widening gap between the two tiers of the market is unlikely to be sustainable, with Grade A rents likely to slip later on in the year. Overall, rent declines of up to 5% are likely across the board before the end of the year.

Furthermore, the strong rental growth over the past two years in Al Soor (30.4%) and the fringe areas of Al Majaz (18.2%) resulted in several developers and land owners rushing to not only complete office schemes that had previously been on hold, but also speculatively develop new space. This means that we are now at the cusp of a spate of deliveries, which will also hold back any strong return to positive growth.

That said, with a potential boost to the UAE economy likely to begin materialising once trade sanctions are lifted on Iran, Sharjah may feel the benefit in the form of an upturn in requirements from domestic and international occupiers who expand operations to service the Iranian economy.

Although any Iran-linked boost is likely to have a slow-motion impact, the office market can take comfort in the fact that, like the residential market, deliveries and completions are subject to SEWA connection delays, which has in the past prevented a sudden flood of office space onto the market and we expect this to persist in the short to medium term, which should shield the market to an extent.

25cluttons.com

UAE REAL ESTATE MARKET

There are a number of headwinds facing growth across the nation’s biggest real estate markets. The continued and prolonged slump in oil prices is one of our chief concerns, particularly as there is a direct correlation between hydrocarbon revenues and state spending. A further reduction in oil prices is more than likely once Iran receives the green light to begin oil exports.

This is expected to put further pressure on the rate of job creation and therefore the appetite and rate of office space take up and subsequently, the rate of creation of households and overall residential demand at least in the short term.

The nervousness of employers in the event of such a scenario is already materialising in the tapering of the total number of vacancies across the UAE. During Q2, Morgan McKinley reported a 1.2% dip in available jobs, with a marked decline in permanent positions in the oil and gas sector as global oil companies brace for a prolonged era of low oil prices.

The impact of this will be variable across the UAE with Abu Dhabi likely to feel the impact most, given its heavy reliance on oil exports. Still, with Saadiyat Island moving closer to realising some of its flagship projects, the appeal of Abu Dhabi’s upmarket communities is rising amongst both domestic and international investors, particularly those looking to diversify their UAE portfolios or those that have been priced out of Dubai.

In Dubai, weaker oil prices may stem the pace of government backed projects; however with tourism showing no signs of abating and with the Expo 2020 just over four years away, the level of job creation in the emirate’s highly diversified economy, is expected to remain stable, if not strengthen as the city gears up for the World Expo.

Furthermore, with sentiment continuing to be buoyed through mega projects such as Meydan One and its record breaking 1.2 km ski-slope and 711m residential tower, Emaar and Dubai Properties’ plans for the former Dubai Lagoons site, the AED 117 billion development of Al Maktoum International Airport, the AED 5 billion expansion of Jebel Ali Port and the planned Dubai Metro extensions will ensure a steady stream of new jobs, which will help to support growth in the real estate sector.

For Sharjah, the lower oil price effect will be slightly more tempered, with the emirate’s drive to diversify into real estate unlikely to wane in the near term primarily due to the price advantage it offers over neighbouring Dubai and Abu Dhabi. Furthermore, government incentives to improve transportation infrastructure and build on the emirate’s reputation as the region’s leading Islamic cultural hub will ensure its continued appeal to the region’s investors, particularly those from the Levant region looking for an affordable regional safe haven.

LEADING JOBS GROWTH INDICATORS

1.89 %growth in the UAE’s total workforce over the last 12 months.

-1.2 %drop in the number of full time jobs during Q2 in the UAE.

Morgan McKinley

1stDubai was the most searched global job destination by US expats; London was second.

Aetna International

OUTLOOK MIXED

26 cluttons.com

Source: Cluttons

THE PROPERTY REPORT IN NUMBERS

ABU DHABI

AED 75 psfoffice rents in Al Soor

-2.3%decline in average residential rents during H1

AED 90,000Average rent for 3 bedroom villa

DUBAI

SHARJAH

AED 250 psfHeadline office rents stay flat

Residential house prices

-3.1%down on summer 2014

41,000 residential units have been announced this year

Prime office rents have remained stable for

14 quarters

1.5% Rise in average residential rents

3%House price growth

UAE GDP Expansion

3.2%

Source: IMF

27cluttons.com

© Cluttons LLC. 2015. This publication is the soleproperty of Cluttons LLC. and must not be copied,reproduced or transmitted in any form or by anymeans, either in whole or in part, without the priorwritten consent of Cluttons LLP. The informationcontained in this publication has been obtainedfrom sources generally regarded to be reliable.However, no representation is made or warrantygiven, in respect of the accuracy of this information.We would like to be informed of any inaccuraciesso that we may correct them. 0768

For further details contactSteve MorganCEO of Middle [email protected]

Faisal DurraniHead of [email protected]

Richard Paul Head of residential valuations [email protected]

Murray Strang Head of investment & agency, [email protected]

Paula Walshe Head of international corporate services [email protected]

Krystyna MawbyAssociate director, valuations, Abu [email protected]

Suzanne Eveleigh

Head of [email protected]

Shane Breen

Associate director commercial valuations, Sharjah [email protected]

Abu DhabiThird FloorEMC buildingAirport RoadPO Box 95246

+971 2 441 1225

DubaiLevel 22Arenco TowerDubai Internet CityPO Box 3087

+971 4 365 7700

SharjahBehind Nova Park HotelKing Faisal StreetPO Box 3615

+ 971 6 572 3794

cluttons.com

اإلمارات العربية املتحدة ا ٢٠١٥

تـقـريــر الـعـقــــارات

٢٠٠٣يناير

٢٠٠٣يوليو

يناير ٢٠٠٤

يوليو ٢٠٠٤

يناير ٢٠٠٥

يوليو ٢٠٠٥

يناير ٢٠٠٦

يوليو ٢٠٠٦

يناير ٢٠٠٧

يوليو ٢٠٠٧

يناير ٢٠٠٨

يوليو ٢٠٠٨

يناير ٢٠٠٩

يوليو ٢٠٠٩

يناير ٢٠١٠

يوليو ٢٠١٠

يناير ٢٠١١

يوليو ٢٠١١

يناير ٢٠١٢

يوليو ٢٠١٢

٢٠١٣يناير

٢٠١٣يوليو

يناير ٢٠١٤

يوليو ٢٠١٤

يناير ٢٠١٥

يوليو ٢٠١٥

١٤٠

١٢٠

١٠٠

٨٠

٦٠

٤٠

٢٠

٠لمي/ بر

ي ريك

أمالر دو

أداء أسعار النفطاملصدر: أوبك

االقتصاد

انخفاض أسعار النفط يحجب النمو االقتصادي يف عام ٢٠١٥

بدأ استمرار انخفاض أسعار النفط ـ كما كان متوقعًا ـ والذي مت تسجيله يف اخلريف املاضي

يف التأثري على قدرة معظم دول جملس التعاون اخلليجي على تقدمي ميزانيات متوازنة. وبدأت دولة اإلمارات العربية املتحدة أيضًا يف مواجهة تبعات ضغوط تناقص إيرادات النفط

والغاز، والذي يشكل طبقًا لتقديرات وكالة

موديز ٪75 من االحتياطيات املالية للبالد خالل عام 2014. ويف الواقع، سجل سعر الفائدة

السائد بني املصارف يف اإلمارات أعلى مستوى له خالل 16 شهرًا يف شهر أغسطس، يف

حني انخفضت مستويات الودائع وفقًا لبيانات جمعتها بلومبريغ.

بدأ االنخفاض البالغ ٪54 يف أسعار النفط، والتي وصلت إىل 50 دوالر أمريكي للربميل بعد أن سجلت ارتفاعًا بلغ 110 دوالر أمريكي للربميل خالل الشهر املاضي، يف التأثري على األوضاع املالية

يف البالد يف اآلونة احلالية. وتشري تقديرات صندوق النقد الدويل أن البالد تفرض أسعارًا تبلغ

75 دوالر أمريكي للربميل للوصول إىل نقطة تعادل يف امليزانية تتساوى فيها اإليرادات مع

التكاليف. ونتيجة لذلك، يتوقع صندوق النقد الدويل أن تسجل دولة اإلمارات العربية املتحدة عجزًا يف امليزانية بنسبة ٪2.3 هذا العام ألول مرة يف تاريخ البالد منذ "الكساد العظيم" يف عام 2009. ونتيجة لذلك، من املتوقع أن يتباطأ

الناجت احمللي اإلجمايل إىل ٪3.2 يف عام 2015 بعد أن سجل ٪4.2 العام املاضي.

ورغم أنه من غري املعتاد أن تشهد سلعة مثل النفط اخلام فرتات تقلب استثنائية، إال أن االستقرار النسبي يف أسعار النفط اخلام بني

أوائل عام 2011 وأواخر العام املاضي يعني أن العديد من دول األوبك متيل إىل االنخراط يف

جمموعة واسعة من مشاريع البنية التحتية واملرافق العامة التي تدعمها الدولة، وكثري من

هذه املشاريع ُمهدد اآلن إما بالتعرث أو حتى اإللغاء.

2cluttons.com

متاشيا مع توجهات احلكومة على املدى الطويل، شرعت دولة اإلمارات العربية املتحدة يف اتخاذ سلسلة من التدابري املالية للمساعدة يف دعم مركزها املايل مع مراعاة اتخاذ تدابري إضافية

حلمايتها من أي صدمات أخرى يف أسعار النفط. وأصبحت اإلمارات العربية املتحدة يف األول من أغسطس الدولة اخلليجية األوىل التي تشرع يف رفع القيود عن أسعار الوقود، والعمل بشكل

فعال على رفع الدعم احلكومي عن الوقود الذي كان مطبقًا منذ تأسيس البالد يف عام 1971. وتشري تقديرات صندوق النقد الدويل أن دعم املنتجات البرتولية يف دولة اإلمارات العربية املتحدة يبلغ 25.7

مليار درهم ويشكل جزءًا كبريًا من ميزانية دعم الطاقة التي تبلغ 389 مليار درهم مبا يعادل حوايل ٪7 من الناجت احمللي اإلجمايل.

وتأتي عمليات إصالح أسعار الوقود يف أعقاب قراٍر من إمارتي أبوظبي ودبي برفع تعرفة املياه والكهرباء يف السنوات األخرية يف ظل توجه حكومتا اإلمارتني إىل رفع الدعم عن املرافق العامة

بوترية متباطئة.

ومن املقرر عقد اجتماع شهري للجنة أسعار الوقود التي تأسست حديثًا لتحديد األسعار كل شهر استنادًا إىل املعدالت العاملية. وقد أعلنت اللجنة خالل شهر أغسطس فرض زيادة نسبتها 24٪

يف أسعار الوقود، يف حني انخفضت تكاليف الديزل بنسبة الثلث تقريبًا. ورغم هذا التغيري املرحلي، ال تزال األسعار يف حمطات الوقود أرخص مبعدل الثلث تقريبًا مما هي عليه يف الواليات املتحدة

األمريكية وأرخص مبعدل أربعة أضعاف مما هي عليه يف اململكة املتحدة. ومن املرجح أن يؤدي هذا إىل رفع مستويات التضخم يف أسعار املنتجات االستهالكية؛ إال أن حدة هذه الزيادة قد تخف نسبيًا نتيجة انخفاض تكاليف التصنيع واخلدمات اللوجستية الناجم عن انخفاض أسعار الديزل، ما

من شأنه أن يساعد البالد يف االحتفاظ بقدرتها التنافسية مع بقية دول جملس التعاون اخلليجي. وتشري تقديرات وكالة موديز أن التغيري املزمع يف أسعار الوقود يف شهر أغسطس سُيكلف كل

مقيم يف دولة اإلمارات العربية املتحدة 1.420 درهمًا إضافيًا خالل هذا العام.

هبوط أسعار النفط يشعلشرارة التغيريات يف السياسة

3 cluttons.com

٠٫٠٠

٠٫٥٠

١٫٠٠

١٫٥٠

٢٫٠٠

٢٫٥٠

٣٫٠٠

٣٫٥٠

٤٫٠٠

٤٫٥٠

٥٫٠٠

٥٫٥٠

٦٫٠٠

٦٫٥٠

٧٫٠٠

فنزويال

الواليات املتحدة األمريكية

اململكة املتحدة

اإلمارات العربية املتحدة

اململكة العربية السعودية

قطر

عمان

الكويت

إيران

البحرين

لرت/ لم رهد

تكاليف الوقود العاملية للرت الواحد

توقعات منو الناجت احمللي اإلجمايل يف دولة اإلمارات العربية املتحدة

٢٠٠٠

٢٠٠١

٢٠٠٢

٢٠٠٣

٢٠٠٤

٢٠٠٥

٢٠٠٦

٢٠٠٧

٢٠٠٨

٢٠٠٩

٢٠١٠

٢٠١١

٢٠١٢

٢٠١٣

٢٠١٤

٢٠١٥

٢٠١٦

٢٠١٧

٢٠١٨

٢٠١٩

١٢

١٠

٨

٦

٤

٢

٠

٢-

٤-

٦-

ويسن

س سا

ى أعلري غيللتة ئويملة اسب

الن

املصدر: صندوق النقد الدويل

Source: GlobalPetrolPrices.com

االقتصاد

توقعات مبزيٍد من اإلصالحات االقتصاديةمل ميّر رفع الدعم احلكومي عن الطاقة بشكل

تدريجي مرور الكرام بالنسبة جملتمع االستثمار يف البالد. ففي الواقع، تشري تقديرات وكالة موديز

أن أبوظبي، التي تستحوذ على ٪94 من إجمايل إنتاج النفط يف دولة اإلمارات العربية املتحدة،

سجلت بالفعل تراجعًا يف عوائد السندات السيادية مبقدار 5 نقاط أساس، ما يعزز الطلب

على االئتمان على مستوى البالد. كما تشري تقديرات وكالة موديز أن التغيري يف سياسات دعم الوقود سيسهم يف قيام حكومة أبوظبي بتحقيق

وفورات تبلغ قيمتها 13.8 مليار درهم تقريبًا.

وباإلضافة إىل دعم الوقود، تشري التقارير إىل أن البالد تدرس حاليًا التصدي لقضية ضريبة القيمة

املضافة والضريبة على الشركات التي حرص االحتاد على تفاديها منذ تأسيسه. وقد أعلنت

وزارة املالية يف أواخر يوليو أنه من املتوقع سّن مشروع قانون ضريبة القيمة املضافة والضريبة

على الشركات قبل نهاية عام 2015؛ غري أنه من غري املتوقع أن يدخل هذا القانون حيز التنفيذ خالل هذا العام. ومن املقرر أن يتم اإلعالن عن مزيد من

التفاصيل حول ما إذا كان سيتم إعفاء شركات املنطقة احلرة من ضريبة الشركات أم ال.

وقد ساعد عدم وجود ضريبة القيمة املضافة والضريبة على الشركات يف بزوغ جنم دولة

اإلمارات العربية املتحدة باعتبارها مركز العصب للشركات واألعمال التجارية يف املنطقة؛ غري أنه من غري املرجح أن يؤثر التغيري يف السياسة على

السمعة العاملية املرموقة لدولة اإلمارات العربية املتحدة. ومع نضوج االقتصاد، مل يكن هناك مفر

من تنفيذ جمموعة من اإلصالحات االقتصادية الرامية إىل دعم اإليرادات احلكومية، ونحن اآلن على

أعتاب مرحلة انتقالية يف ظل تطور االقتصاد وسعي احلكومة االحتادية لتنويع مصادر دخلها

بعيدًا عن إيرادات النفط والغاز.

4cluttons.com

هل ميكن أن تعزز الصفقة اإليرانية النمو االقتصادي يف اإلمارات العربية املتحدة؟

درهم

١٨ مليار القيمة املقدرة لالستثمارات التي يحتاجها قطاع

الطريان يف إيران

درهم

٦٢٫٤ مليار قيمة التبادل التجاري بني اإلمارات و إيران عام 2014

درهم

٧٣٤ مليار القيمة املقدرة لالستثمارات التي يحتاجها قطاع

النفط والغاز يف ايران خالل السنوات اخلمس القادمة

ساد يف الفرتة التي تسبق صفقة منتصف يوليو التاريخية بني القوى العاملية الست وإيران يف فيينا الكثري من التكهنات حول حدوث زيادة

حمتملة يف النشاط االقتصادي يف دولة اإلمارات العربية املتحدة. وكانت إيران قبيل توقيع العقوبات التجارية عليها أكرب شريك

لدولة اإلمارات العربية املتحدة وانخفض عدد السائحني من اجلمهورية اإليرانية إىل اإلمارات

العربية املتحدة بنسبة ٪50 منذ عام 2010 وفقًا لصندوق النقد الدويل. ومع ذلك، ال تزال إيران على الرغم من العقوبات شريكًا جتاريًا مهمًا لإلمارات العربية املتحدة، باعتبارها رابع أكرب شريك جتاري لدولة اإلمارات العربية املتحدة

يف عام 2014، وفقا ألحدث األرقام الصادرة عن احلكومة اإليرانية، وهو ما يرتجم إىل أعمال جتارية

بقيمة 62.4 مليار درهم بزيادة نسبتها 8.3٪ عن عام 2013.

وال يزال رأينا راسخًا يف هذا الصدد، ونحن نرى هذا االتفاق التاريخي حافزًا لتحقيق النمو يف دولة اإلمارات على املدى الطويل والذي من

املتوقع أن يرتكز يف دبي. وقد ركزت كل من الشركات احمللية والعاملية عملياتها اإليرانية

خارج دبي يف السابق، ونحن نتوقع بدء هذه الظاهرة يف القريب العاجل حال موافقة

الكوجنرس األمريكي رسميًا على رفع العقوبات التجارية واالقتصادية السداسية التي ترعاها

األمم املتحدة عن إيران.

ويف الواقع، أعلنت احلكومة اإليرانية بالفعل عن احلاجة إىل استثمارات مقدرة بقيمة 734

مليار درهم على مدى السنوات اخلمس املقبلة من قطاع النفط والغاز وحده، يف حني يتطلب

قطاع الطريان فقط أكرث من 18 مليار درهم كاستثمارات مباشرة. ونحن نتوقع مرور الغالبية

العظمى من هذه األموال عرب النظام املايل يف دولة اإلمارات العربية املتحدة، وهو األمر الذي ينبغي أن يساعد يف حتسني مستويات

السيولة الوطنية.

ولن يعود توسع األنشطة التجارية املرتتب على سعي الشركات العاملية خلدمة اقتصاد قائم

على االستثمار ألكرث من عقد من الزمن بالفائدة على اإلمارات األخرى يف االحتاد فحسب؛ بل

سيصب يف صالح دول املنطقة أيضًا.

وتتمثل مساوئ رفع العقوبات التجارية بالطبع يف تأثري استئناف صادرات النفط والغاز االيرانية

على سوق النفط املتقلب. فرغم أنه من غري املرجح أن ترتفع مستويات تصدير النفط اإليراين

بسرعة، إال أننا نرى أنه من املرجح حدوث مزيد من االنخفاض يف أسعار النفط مبجرد رفع العقوبات عن إيران رسميًا. ويعتمد حجم أي

حركة انخفاض يف األسعار ومدة هذا االنخفاض إىل حد كبري على مدى السرعة التي ميكن لالحتاد

األوروبي بها الوصول إىل اتفاق يوناين والعودة إىل مسار النمو. ويف نفس الوقت، ونظرًا لكونها

أحد أسواق التصدير األكرث أهمية للصني، ال

يزال األداء االقتصادي للبالد ومن ثم الطلب على النفط يف حالة ترقب وانتظار، األمر الذي يسلط

الضوء على اخملاطر التي يواجهها االقتصاد العاملي على نطاق أوسع.

من املرجح أن يؤتي الزخم العقاري ثمارهيف دبي أواًل

بالنسبة للسوق العقارية، سيكون عودة املتغري اإليراين إىل املعادلة الوطنية العقارية أمرًا بالغ

األهمية بشكل خاص.

ونرى بأن املواطنني اإليرانيني سيسعون إىل اغتنام الفرصة إلقامة استثمارات عقارية كربى يف دبي، ما سيتيح لهم تبوء صدارة قائمة أبرز

املشرتين العقاريني يف دبي. ويف عام 2010، استحوذ املواطنون اإليرانيني على ٪12 من

املعامالت العقارية يف دبي، واحتلوا املرتبة الرابعة يف قائمة أبرز املشرتين العقاريني بعد

الهنود والربيطانيني والباكستانيني.

لكن ومع بداية تطبيق العقوبات التجارية، تضاءل حجم االستثمارات من الرعايا اإليرانيني وانخفض إىل ٪3 فقط خالل الربع األول من عام 2015 وفقا للبيانات الصادرة عن دائرة األراضي واألمالك يف دبي، ومن املتوقع أن يكون ذلك أحد املؤشرات

الرئيسية على الفوائد التي ستعود على دولة اإلمارات العربية املتحدة من رفع العقوبات

التجارية على إيران والذي مل يحدد له موعد حتى اآلن.

املصدر: احلكومة اإليرانية

5 cluttons.com

أبـوظـبـي

جامع الشيخ زايد الكبري

6cluttons.com

سوق العقارات السكنية

أداء قيم العقارات السكنية يف أبوظبي

توقف النمو يف أسعار املنازلتراجعت أسعار املنازل يف العاصمة بنسبة 0.2٪

يف الربع الثاين، وهو أول انكماش تشهده البالد منذ الربع الثالث من عام 2012، بعد تسجيل ارتفاع بنسبة ٪0.5 يف الربع األول من العام. وأدى تراجع متوسط أسعار املنازل يف املناطق االستثمارية

يف أبوظبي إىل انخفاض معدل الزيادة السنوية ملا يزيد قلياًل عن ٪15 يف نهاية مارس ليصل إىل

٪3 يف نهاية يونيو. وسجل متوسط سعر املنازل حاليًا 1336 درهم للقدم املربع.

ري غيللتة ئويملة اسب

الن

الربع ١ ٢٠١١

الربع ٢ ٢٠١١

٣ ٢٠١١الربع

الربع ٤ ٢٠١١

الربع ١ ٢٠١٢

الربع ٢ ٢٠١٢

٣ ٢٠١٢الربع

الربع ٤ ٢٠١٢

٢٠١٣الربع ١

٢٠١٣الربع ٢

٢٠١٣ ٣الربع

٢٠١٣الربع ٤

الربع ١ ٢٠١٤

الربع ٢ ٢٠١٤

٣ ٢٠١٤الربع

الربع ٤ ٢٠١٤

الربع ١ ٢٠١٥

الربع ٢ ٢٠١٥

١٥

١٣

١١

٩

٨

٥

٣

١

١-

٣-

٥-

يبلغ متوسط قيم اإليجارات السنوية يف أبوظبي

درهم

٢٠٤،٠٠٠

يبلغ متوسط الدخل السنوي للوافدين

درهم

١٩٩،٠٠٠

املصدر: كالتونز

املصدر: كالتونز، صندوق النقد الدويل، وزارة االقتصاد يف دولة اإلمارات العربية املتحدة

أبوظبي

استقرار أسعار الشققيف حني أن أداء السوق حتى الوقت احلايل من

هذا العام تشري بالتأكيد إىل احتمالية حدوث مزيد من التعديالت الهبوطية يف ظل قيام االقتصاد باستيعاب أثر االنخفاض احلاد يف أسعار النفط،

ظلت أسعار الشقق مستقرًة إىل حد كبري، باستثناء الشقق الفاخرة يف جزيرة الرمي، حيث

تراجعت األسعار بنسبة ٪1.6 خالل النصف األول من العام.

تركز الطلب من املشرتين على اجلانب األعلى من السوق

تعكس طبيعة استقرار الطلب على عقارات السوق الفاخرة وعقارات السوق الفرعية ذات

األسعار امليسورة البالغة قيمتها 1000 درهم للقدم املربع خربتنا يف السوق. فمن ناحية، تضم السوق

شريحة من السكان األثرياء، تتألف يف الغالب من مشرتين من دولة اإلمارات العربية املتحدة ودول

جملس التعاون اخلليجي األخرى، الذين يواصلون االستحواذ على مشاريع كتلك املوجودة يف جزيرة

السعديات بسبب تفردها ومتيزها املتصور.

وعلى اجلانب اآلخر، حتتوي السوق عددًا كبريًا من السكان الوافدين الذين يتعرضون للطرد من سوق

اإليجارات نتيجة لنمو اإليجارات السائد على مدار الثمانية عشر شهرًا املاضية، والذي ظل أعلى بكثري من معدالت التضخم ومنو األجور. وتستمر

هذه الفئة يف استهداف املشاريع التي توفر أفضل قيمة متصورة للمال والتي تساعد األسواق

الفرعية التي توفر أسعارًا معقولة أكرث مثل الغدير يف الصمود يف وجه الضغوط الهبوطية يف

السوق يف الوقت الراهن.

وعالوة على ذلك، يرتتب على النمو القوي يف قيم رأس املال أيضًا عدم ترك أي خيارات أمام

بعض األسر الطموحة سوى التأجري على املدى الطويل يف الوقت الذي جتمع فيه تلك األسر

الودائع للتغلب على قيود الرهن العقاري االحتادية الصارمة. وكان ال بد لذلك أن يسفر عن تركز الطلب

على قطاع حمدد يف السوق، مع جتدد الرتكيز على ما ينظر إليها باعتبارها عقارات ميسورة

بدرجة أكرب.

ويخلق هذا أيضًا فرصة سانحة للمطورين للرتكيز على هذا اجلزء غري املستغل نسبيًا من السوق.

ويف حني خطت دبي خطوات للشروع يف التصدي لتحديات اإلسكان امليسور التي تواجهها، ال تزال

أبوظبي على النقيض من جارتها الشمالية إىل حد ما. ومن هذا املنطلق، وسعيًا لتدشني أي مبادرات

لإلسكان امليسور، فال بد من أن تتدخل الدولة لضمان استفادة جميع فئات السكان من طرح

منازل جديدة ميسورة.

7 cluttons.com

أبوظبي

سوق اإليجارات يكسب زخمًايف أعقاب ركود اإليجارات خالل الربع األول من

العام، سجلنا ارتفاعًا بنسبة ٪1.5 يف متوسط االيجارات خالل الربع الثاين، ليصل النمو السنوي

إىل ٪3.9. ومع ذلك، يخفي هذا حقيقة أن الفيالت )٪2.6( جتاوز أداؤها الشقق السكنية

)٪0.3( والتي استمرت يف تسجيل انخفاض يف اإليجارات، ما يعكس النمط الذي شهدناه يف

الربع األول من العام.

ومع األخذ يف االعتبار وجهة النظر السائدة يف سوق املبيعات، فإنه ليس من املستغرب

أن تكون قرية هيدرا أقوى األسواق أداًء يف العاصمة، حيث ارتفعت إيجارات الفيالت املكونة من ثالث غرف بنسبة ٪32 خالل األشهر الستة

األوىل من العام احلايل لتصل إىل 125 ألف درهم سنويًا، يف حني سجلت الفيالت املكونة من

غرفتني )110 ألف درهم سنويًا( زيادة تقرتب من ٪30 يف اإليجارات، وهذا يعكس زيادة الرتكيز

من قبل املستأجرين على العقارات التي ينظرون إليها باعتبارها ذات أسعار ميسورة.

تراجع اإليجارات يف جزيرة السعدياتمتثلت أضعف أسواق الشقق أداًء خالل النصف

األول من العام يف جزيرة السعديات. ففي حني سجلت الشقق املكونة من غرفتني زيادة

تقرتب من ٪3 يف اإليجارات، تراجعت الشقق املكونة من ثالث وأربع غرف بنسبة 10.2٪

و٪11.9 على التوايل. ويف الوقت الذي يواصل فيه املستأجرون اإلشارة إىل عامل التفرد باعتباره

عامل اجلذب األساسي للمحور الثقايف الناشئ يف العاصمة، يبدو أن اإليجارات هنا قد سجلت

ارتفاعًا غري مسبوق يف السوق. أما بالنسبة لألسواق الفرعية األخرى مثل جزيرة الرمي، التي

تقع على مقربة من وسط أبوظبي، تتوجه أنظار املستأجرين إىل هنا إذ ال تزال اإليجارات هنا أقل

كثريًا من تلك السائدة يف جزيرة السعديات.

أسواق املبيعات والتأجري السكنية تتقاسم توقعات الرتاجع

تراجعت توقعات سوق العقارات السكنية يف العاصمة منذ مطلع العام مدعومًة بضعف

أسعار النفط لوقت طويل وما خلفه ذلك من تأثري متتابع على قوة الطلب يف القطاعات

التجارية والسكنية يف إمارة أبوظبي. ويف حني شهد سوق العقارات السكنية ارتفاعًا يف

متوسط األسعار بنسبة ٪34 منذ عام 2010، كان معدل التغري خالل األرباع األربعة املاضية أكرث هدوًء بكثري. وقد تكون هناك عدة عوامل تؤثر على سلوك السوق السكنية على املدى

املتوسط إىل القصري، غري أن ثمة دالئل تشري إىل عدد متزايد من مشاريع البنية التحتية املتوقفة مع تخفيف اإلنفاق احلكومي، ومن املتوقع أيضًا

أن يسجل معدل توفري فرص العمل والطلب على الوحدات السكنية بعد ذلك بعض االستقرار

أو قلياًل من الرتاجع، ما يؤثر سلبًا على الطلب.

ومع ذلك، ال تزال معظم صفقات االيجارات السكنية اجلماعية شائعة حتى يومنا هذا

مدفوعة يف الغالب من قبل قطاعات الضيافة والتعليم، والتي ال تزال تستوعب املعروض

اجلديد من الوحدات قبل طرحها يف السوق؛ غري أنه مع وجود توقعات بتباطؤ معدل توفري

الوظائف خالل األشهر املقبلة، فمن املرجح أن يرتاجع هذا االجتاه نسبيًا.

ومع أخذ هذا بعني االعتبار، نرى أن سوق العقارات السكنية ستشهد زيادة طفيفة

لتخفيف الرتاجع يف األسعار خالل الفرتة املتبقية من عام 2015؛ غري أنه من املتوقع أن تواصل األسواق، مثل قرية هيدرا، جتاوز

التوقعات لألسباب املذكورة أعاله. وعمومًا، ميكن توقع حدوث انخفاض يف أسعار املنازل

الفصلية بنسبة ترتاوح بني ٪0.5 و٪1 يف كل من الربعني الثالث واألخري من العام، يف حني أنه من املتوقع أن تظل اإليجارات ثابتًة إىل حد كبري خالل

النصف الثاين من العام.

تراجعت توقعات سوق العقارات السكنية يف العاصمة منذ مطلع العام

مدعومًة بضعف أسعار النفط لوقت طويل وما خلفه ذلك من تأثري متتابع

على قوة الطلب

8cluttons.com

التغيريات التنظيمية خطوة يف االجتاه الصحيح

أعلنت حكومة أبوظبي خالل شهر يونيو عن تطبيق حزمة من اإلجراءات التنظيمية

اجلديدة، التي تهدف إىل تعزيز الثقة يف السوق. وتشمل أبرز مالمح القواعد اجلديدة،

التي تقع ضمن اختصاص دائرة الشؤون البلدية، إنشاء سجل عقاري، ومطالبة

املطورين بفتح حسابات الضمان، وسجل للمبيعات على اخلريطة، وإصدار تراخيص

للوسطاء العقاريني.

ورغم أن جمموعة القوانني اجلديدة ستمنح املستثمرين شعورًا أكرب بالراحة يف ظل سعي السلطات لتحسني الشفافية يف

السوق، إال أن اإلشارة إىل مؤشر اإليجارات الذي طال انتظاره على غرار املؤشر امُلطبق يف

دبي ال تزال طي الكتمان. وبالنسبة لسوق مثل أبوظبي ارتفعت اإليجارات فيها مبعدل ٪16 منذ عام 2013 مبا يفوق بكثري معدل منو

األجور الذي سجل منوًا بلغ حسب تقديرنا

٪4.8 خالل الفرتة نفسها، سيلعب مؤشر اإليجارات دورًا كبريًا يف تقدمي مقياس لكٍل

من املالك واملستأجرين ُيمكنهم من قياس أداء السوق.

وقد أتاح رفع سقف اإليجارات للسوق أن تتصرف بطريقة أكرث ديناميكية، وهو ما

يعكس الظروف احلقيقة للسوق؛ غري أن طرح مؤشر اإليجارات سيوفر بعض احلماية

للمستأجرين، كما سيقوم بتوعية املالك، السيما األجانب، بثقافة الشراء من أجل

التأجري.

ومن اجلدير بالذكر أن أي مؤشر سيؤدي إىل تراجع الظروف احلقيقية للسوق ملدة ترتاوح

بني شهرين وثالثة أشهر ولن يكون قادرًا على التعرف على الفروق الدقيقة للمتغريات

مثل حجم الوحدة واإلطاللة والقرب من شبكة النقل العام وغريها.

9 cluttons.com

أبوظبي

سوق املكاتب

إيجارات املكاتب الثانوية

درهم

١،٣٠٠ للمرت املربع

إيجارات املكاتب الرئيسية

درهم

١،٨٥٠ للمرت املربع

إيجارات املكاتب الثالثية

درهم

900 للمرت املربع

ركود اإليجارات بسبب تراجع الطلبواصلت اإليجارات يف العاصمة استقرارها

خالل الربع الثاين من العام، حيث ظلت اإليجارات الرئيسية والثانوية والثالثية كما هي دون

تغيري للربع الرابع على التوايل. وظلت اإليجارات الرئيسية، التي سجلت 1850 درهم للمرت املربع،

مستقرة ملدة ثالثة أعوام ونصف حتى اآلن.

يرتبط الركود الذي شهده سوق املكاتب مؤخرًا بدرجة كبرية بتخفيف اإلنفاق العام، والذي

أدى إىل انخفاض يف الطلب على املساحات املكتبية اجلديدة. ومع ذلك، ونتيجة للنقص

العام يف العروض، وخاصة يف الشريحة األوىل من السوق، حافظت اإليجارات على استقرارها، ومن املتوقع أن تظل مستقرة طوال عام 2015

طبقًا للسيناريو الرئيسي لدينا.

قيم اإليجار من املرجح أن ترتاجع يف عام 2016كما أوضحنا أعاله، سيؤدي اعتماد أبو ظبي الكبري على

عائدات النفط والغاز إىل تراجع أسعار املكاتب التي تهيمن عليها شركات النفط والغاز تراجعًا ملحوظًا.

ومن املرجح أن يفرض هذا مزيدًا من الضغط الهبوطي على املواقع الثانوية والثالثية يف املقام

األول، مع توقعات بأن تواجه اإليجارات الرئيسية رياحًا معاكسًة بعد ذلك بوقت قصري. ونحن ال نتوقع وقوع

هذه السلسلة من األحداث بوترية سريعة، غري أننا نعتقد بأنه من املرجح أن تبدأ اإليجارات مسرية

الرتاجع بنهاية هذا العام أو يف مطلع عام 2016 يف حال سجل اقتصاد اإلمارة مزيدًا من الرتاجع.

املصدر: كالتونز

10cluttons.com

أسعار األبراج الفاخرة ال تزال ثابتةومع ذلك، وانعكاسًا لسلوك قطاع سوق

املكاتب الرئيسية يف الوقت الراهن، مل تسجل األبراج اإلدارية الفاخرة يف أبوظبي أي تغيري يف

اإليجارات خالل الربع الثاين من العام، ما يعني أن اإليجارات سجلت يف معظمها حالة من

االستقرار على مدار ثالثة أشهر متتالية.

وظلت أبراج االحتاد )2250 درهم للمرت املربع(، وإنرتناشيونال تاور )2050 درهم للمرت املربع(

ونيشن تاورز وبرج مركز التجارة العاملي اإلداري )2000 درهم للقدم املربع لكل منهما( األكرث غالء

يف املدينة )بصرف النظر عن سوق أبوظبي العاملي(. ومع استقرار مستويات اإلشغال

أو اقرتابها من حتقيق اإلشغال الكامل، فمن غري احملتمل أن نسجل أي حركة صعودية يف

إيجارات األبراج الفاخرة حلني عودة املعروض إىل السوق جمددًا.

إيجارات الربع الثاين يف األبراج اإلدارية الفاخرة

٠٥٠٠

١،٠٠٠

١،٥٠٠

٢،٠٠٠

٢،٥٠٠

٣،٠٠٠

٣،٥٠٠

٤،٠٠٠

مربعة سوق أبوظبي العاملي

برج أداكس

برج العاصمة

بوابة العاصمة

إنرتناشيونال تاور

أبراج نيشن

برج مكاتب مركز التجارة العاملي

مبنى الدار

أبراج االحتاد

درهم للمرت املربع

املصدر: كالتونز

بعيدًا عن هذا املعروض من املباين الفاخرة، تواصل املنطقة املالية احلرة يف سوق

أبوظبي العاملي الذي مت إنشاؤه مؤخرًا يف جزيرة املارية تعزيز مكانتها باعتبارها معيارًا

جديدًا لقطاع املكاتب الفاخرة يف املدينة، حيث تسجل اإليجارات املطلوبة ما يقرب من 3700

درهم للمرت املربع.

ورغم أن هذه األسعار ال تزال تتجاوز األسعار السائدة يف مركز دبي املايل العاملي القريب )2400 درهم للمرت املربع(، إال أن الطلب على

املساحات ال يزال مستقرًا مع قدوم الشركات العاملية إىل هنا مدفوعني باإلطار التنظيمي

العاملي الذي تطبقه السوق. ومع ذلك، تواصل الغالبية العظمى من الشركات العاملية نقل

مقراتها الرئيسية إىل دبي، بينما ال تزال دبي يف الغالب قبلة الستضافة أفرع لتلك الشركات.

11 cluttons.com

دبــي

خور دبي

12cluttons.com

تسارع تراجع أسعار الفيالتكما توقعنا سابقًا، ال تزال سوق الفيالت ترزح

حتت وطأة القيود االحتادية على سقف الرهن العقاري، التي جعلت قضية القدرة على حتمل

التكاليف قضية جوهرية للمشرتين احملتملني الذي يتوجب عليهم يف اآلونة احلالية امتالك مبلغ

كبري من املال لتمويل التكاليف األولية )انظر املثال أدناه(. وعالوة على ذلك، يخفف ارتفاع مستويات

املعروض من احتمالية حدوث أي تغيري مفاجئ يف أداء هذه الشريحة من سوق العقارات السكنية.

وقد انخفض متوسط أسعار الفيالت يف الربع الثاين من العام بنسبة ٪3.4، ليرتاجع معدل التغري

السنوي اىل 7-٪. جتدر اإلشارة إىل أن األشهر الستة األوىل من عام 2015 وحده سجلت انخفاضًا

بنسبة ٪5.1 يف متوسط أسعار الفيالت، التي تبلغ اآلن 1421 درهم للقدم املربع

وسجل مشروع الينابيع أضعف أداء لألسواق الفرعية خالل النصف األول من العام ، حيث بلغ )٪٧-(،

بينما سجلت الفيالت يف مشروع غرين كومينيتي )اجملتمع األخضر( أقل انخفاض بلغ )2.2%-(.

سوق العقارات السكنية

أداء قيم رأس املال يف أسواق الفيالت الرئيسية

١،٦٠٠

١،٥٠٠

١،٤٠٠

١،٣٠٠

١،٢٠٠

١،١٠٠

١،٠٠٠

٩٠٠

٨٠٠

٧٠٠

٦٠٠

٥٠٠

٤٠٠

الينابيع

البحريات

املرابع العربية

املروج

جزر جمريا

قرية جمريا

عةملرب

م اقد

م للرهد

الربع ٤ ٢٠١١

الربع ١ ٢٠١٢

الربع ٢ ٢٠١٢

٣ ٢٠١٢الربع

الربع ٤ ٢٠١٢

٢٠١٣الربع ١

٢٠١٣الربع ٢

٢٠١٣ ٣الربع

٢٠١٣الربع ٤

الربع ١ ٢٠١٤

الربع ٢ ٢٠١٤

٣ ٢٠١٤الربع

الربع ٤ ٢٠١٤

الربع ١ ٢٠١٥

الربع ٢ ٢٠١٥

املصدر: كالتونز

دبي

شراء فيال بقيمة 5.5 مليون درهم

درهم%التكاليف

٣٥١،٩٢٥،٠٠٠احلد األدنى للوديعة

٤٢٢٠،٠٠٠رسوم تسجيل العقار

٢١١٠،٠٠٠رسوم الوكالة

١٥٥،٠٠٠الرسوم املصرفية

٢،٣١٠،٠٠٠٪٤٢إجمايل التكلفة األولية

املصدر: كالتونز

درهم

13 cluttons.com

ري غيللتة ئويملة اسب

الن

الربع ١ ٢٠١١

الربع ٢ ٢٠١١

٣ ٢٠١١الربع

الربع ٤ ٢٠١١

الربع ١ ٢٠١٢

الربع ٢ ٢٠١٢

٣ ٢٠١٢الربع

الربع ٤ ٢٠١٢

٢٠١٣الربع ١

٢٠١٣ ٢ الربع

٢٠١٣ ٣الربع

٢٠١٣الربع ٤

الربع ١ ٢٠١٤

٢ ٢٠١٤ الربع

٣ ٢٠١٤الربع

الربع ٤ ٢٠١٤

الربع ١ ٢٠١٥

٢ ٢٠١٥ الربع

٢٤٢٢٢٠١٨١٦١٤١٢١٠٨٦٤٢٠٢-٤-٦-٨-

سوق العقارات السكنية: معدالت منو قيم رأس املال

دبي

استقرار إجمايل عدد الصفقات السكنية نسبيًابالنظر بوجه خاص إىل املباين والوحدات، كان هناك

تراجع بنسبة ٪7 يف عدد الصفقات املسجلة، يف حني تراجعت قيمة جميع الصفقات العقارية

بنحو الربع.

وبالتغلغل أكرث يف سوق العقارات السكنية، تبدو اآلفاق مستقرًة إىل حد ما، حيث تظهر

البيانات الصادرة عن شركة "ريدين" انخفاض الصفقات خالل النصف األول بنسبة ٪2.3 عن

الفرتة نفسها من العام املاضي. كما تراجع عدد صفقات الشقق بنسبة ٪1.1 يف حني تراجع

عدد الفيالت املتداولة من مالك آلخر بنسبة ٪13.1 باملقارنة مع النصف األول من عام 2014،

مما يعكس حتديات القدرة على حتمل التكاليف املذكورة أعاله.

املصدر: كالتونز

قيم رأس مال الشقق تظهر مرونة أكربحققت الشقق من ناحية أخرى أداًء أفضل قلياًل، حيث تراجعت متوسطات قيم رأس املال تراجعًا

بنسبة ٪0.4- لتصل إىل 1471 درهم خالل الربع الثاين من العام، وهو ما يرتجم إىل انخفاض بنسبة 0.6٪

بني شهري يناير ويونيو من هذا العام. وعمومًا، مل يكن هناك أي تغيري يف متوسط قيم الشقق خالل

النصف األول من العام.

كانت الشقق الفاخرة يف دبي مارينا )2.6٪-(، والشقق املتوسطة يف نخلة جمريا )1.9٪-(

والشقق الفاخرة يف نخلة جمريا )٪1.7-( األسواق الفرعية الثالثة األضعف أداًء، مما يعكس مزيجًا

يجمع بني املالك الرافضني لتخفيض األسعار على نحو يعكس واقع السوق وأولئك الذين خفضوا